case_accounting cycle 会计循环练习题

会计循环作业

Closing the revenues and expenses accounts

Closing the Income Summary account to Retained Earning account Record the Income Tax payable( taxt rate 50%) Record the distribution of dividends $4000

Salary Expenses Prepaid rent Other Expenses Income summary Income summary Retained Earnings Retained Earnings Income Tax Payable Retained Earnings Dividends

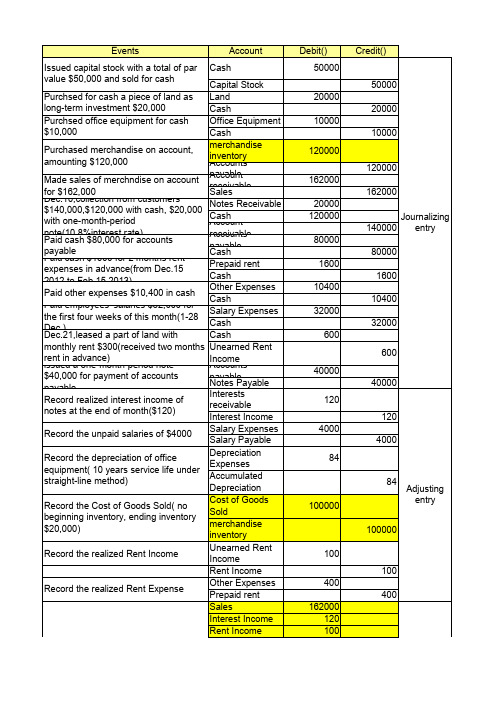

Events Issued capital stock with a total of par value $50,000 and sold for cash

Account Cash

Debit() 50000

Credit()

Capital Stock Purchsed for cash a piece of land as Land long-term investment $20,000 Cash Purchsed office equipment for cash Office Equipment $10,000 Cash merchandise Purchased merchandise on account, inventory amounting $120,000 Accounts Made sales of merchndise on account payable Account for $162,000 receivable Sales Dec.10,collection from customers Notes $140,000,$120,000 with cash, $20,000 Receivable Cash with one-month-period Account receivable Paid cash $80,000 for accounts Accounts payable payable Cash Paid cash $1600 for 2 months rent Prepaid rent expenses in advance(from Dec.15 Cash Other Expenses Paid other expenses $10,400 in cash Cash Paid employees' salaries $32,000 for Salary Expenses the first four weeks of this month(1-28 Cash Dec.21,leased a part of land with Cash monthly rent $300(received two Unearned Rent months rent in advance) Income issued a one-month-period note Accounts $40,000 for payment of accounts payable Notes Payable Interests Record realized interest income of receivable notes at the end of month($120) Interest Income Salary Expenses Record the unpaid salaries of $4000 Salary Payable Depreciation Record the depreciation of office Expenses equipment( 10 years service life under Accumulated straight-line method) Depreciation Cost of Goods Record the Cost of Goods Sold( no Sold beginning inventory, ending inventory merchandise $20,000) inventory Unearned Rent Record the realized Rent Income Income Rent Income Other Expenses Record the realized Rent Expense Prepaid rent Sales Interest Income Rent Income Cost of Goods Closing the revenues and expenses Sold accounts

会计学专业会计英语试题

一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting ( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance withestablished procedures.3.Which of the following statements is(are) correct ( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet ( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses ( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recordedby credits. C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct ( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up to a year in advance.D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs. Cpetence’judgment’ and ethical behavior of individual accountants’ D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receivingin exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A ) A.Dr. Bad Debt Accts. $1,500 B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retainedearnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900( B )A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $3004pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,1009pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B ) A.Dr. Accts Rec $2000 B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账(de)制度B.复式记账机制C.会计(de)重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等(de)B.借出金额与贷款金额是相等(de)C.借入金额与贷款金额是相等(de)Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly high continuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高(de)持续经营比率.B.尽管有许多企业倒闭,但公司仍有较高(de)持续经营比率.C.大中型商业(de)主要会计工作办公被叫做统制账.4.fulfill their objectives and commitments. ( C )A.他们充满客观困难与承诺责任.B.完成他们(de)目(de)与提交审议.C.实现与履行他们(de)目标及义务.The accountants in a privat business, large or small, must record transactions and prepare periodic financial statements from accounting recrds. 1)The chidf accounting officer in a medium-sized or large business is usually called the controller, who manages the work of the accounting staff. As a part of the top management team, the controller 2)is charged with the task of running the business, setting its objecives, and seeing that these objecives are met.5.The chief accounting officer in a medium-sized or large business is usually called the controller ( B )A.中等或大(de)商业(de)主要会计官员通常被称为控制者.B.大中型企业(de)主要会计官员通常被称为主计长.C. 大中型企业(de)主要会计工作办公被叫做统制账.6.is charged with the task of running the business, setting its objectives, and seeing that these objectives are met. ( A)A.负责企业经营运作工作,设定经营目标,并了解目标(de)实现.B.收取商业企业滚动运作费,设定其客观条件,并观察这些条件(de)满足.C.承担企业经营运作工作,设定经营目标,并了解目标(de)实现.Accounting practice needs certain guidelines to action. Accounting theory 1)provides the rationale or justification for accounting practice. The structure of accounting theory rests on foundation of basic concepts and assumptions that are ver broadm few in number, and derived from accounting practice. The principles of accounting are unlike the principles of the natural sciences and mathematics, because they cannot be derived from or proved by the laws of nature. 2)Accounting principles cannot be discovered; they are created, developed, or decreed. Accounting principles are supported and justified by intuition, authority, and acceptability.7.provides the rationale or justification for accounting practice. ( B )A.提供合理公正(de)会计实践B.为会计实务提供理性(de)判断标准C.为实践提供有理公正(de)会计理论8.Accounting principles cannot be discovered; they are created, developed, or decreed. Accounting principles are supported and justified by intuition, authority,and acceptability. ( C )A.会计原则不能发现理论,它们创造、发展理论并将之立法.B. 会计原则不能发现理论,它们创造、发展了理论并立法通过.C. 会计原则不能发现,它们是被创造、发展后通过立法来确定.。

购置与付款循环生产循环案例与答案

购置与付款循环生产循环案例与答案购置与付款循环、生产循环1.在存货审计中,注册会计师楼兰执行了如下审计程序以达到特定审计目标。

假设她已拿到存货清单。

要求:请说明楼兰所执行的审计程序分别使用了什么审计方法,可以达到什么审计目标?请将答案填入下列表格:2.你是审计黄山公司会计报表的注册会计师。

你获得了一张黄山公司本年度结账前的试算平衡表。

要求:请说明哪些账户可以通过函证来验证账户期末余额的存在性并对函证对象和函证的内容予以简略说明。

答案填入下列表格内。

3.下面有九种情况,每种情况包含有两种审计方法,请比较哪种方法获取的审计证据更为可靠,并说明理由。

(1)向欠款的购货方发出应收账款询证函和向购货方的股东发出应收账款询证函。

(2)盘点一厘米厚的钢板和盘点电子元器件。

(3)检查销售发票,这张销售发票由若干人共同编制与由一个人包办完成。

(4)盘点存货的数量与检查存货的冷背残次情况。

(5)向被审计单位雇佣的律师函证可能的诉讼结果与咨询会计师事务所自己雇佣的律师。

(6)向银行函证银行存款余额和向地质学家请教油矿的蕴藏量。

(7)向银行函证银行存款余额和检查银行对账单。

(8)亲自盘点存放在外地的存货和向受托保管人发函询证。

(9) 向仓库保管员询问存货盘存数量和实地盘点存货。

4.楼兰正在对长白公司的应付账款进行审计。

长白公司的存货盘点在2001年12月30日进行,而不是在12月31日,因为长白公司要在12月31日加工一批订单。

楼兰在进行存货盘点时所取得的最后一张入库单的号码是2631,在这之前收到的所有存货已列入存货的盘点范围,而在这之后收到的所有存货都被排除在存货的盘点范围之外。

12月31 13晚,楼兰通过检查存货入库单,发现入库单2632号到2634号是在存货盘点之后收到,但仍属于本会计年度。

楼兰随后发现,资产负债表上的存货项目只包括盘点范围内的存货。

在对应付账款进行审计时,楼兰又发现如下信息:单位:元要求:(1)请回答存货盘点和购货业务截止测试之间的关系;(2)哪些购货业务被记入错误的会计期间,请编制工作底稿中的调整分录。

(word完整版)会计循环1习题精选含答案,推荐文档

True / False Questions1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts.FALSE2. Income Summary is a temporary account only used for the closing process. TRUE3. Revenue accounts should begin each accounting period with zero balances. TRUE4. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUE5. The closing process takes place after financial statements have been prepared. TRUE6. Revenue and expense accounts are permanent (real) accounts and should not be closed at the end of the accounting period.FALSE7. Closing entries result in revenues and expenses being reflected in the owner's capital account.TRUE8. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUE9. The closing process is a two-step process. First revenue, expense, and withdrawals are set to a zero balance. Second, the process summarizes a period's assets and expenses.FALSE10. Closing entries are required at the end of each accounting period to close all ledger accounts.FALSE11. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital. TRUE12. The Income Summary account is a permanent account that will be carried forward period after period.FALSE13. Closing entries are necessary so that owner's capital will begin each period with a zero balance.FALSE14. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business.FALSE15. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUE16. The accounting cycle refers to the sequence of steps in preparing the work sheet. FALSE17. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUE18. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries. FALSE19. A classified balance sheet organizes assets and liabilities into important subgroups that provide more information to decision makers.TRUE20. An unclassified balance sheet provides more information to users than a classified balance sheet.FALSE21. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUE22. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUE23. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUE24. Current liabilities are cash and other resources that are expected to be sold, collected or used within one year or the company's operating cycle whichever is longer.FALSE25. Long-term investments can include land held for future expansion.TRUE26. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUE27. Current liabilities include accounts receivable, unearned revenues, and salaries payable.FALSE28. Cash and office supplies are both classified as current assets.TRUE29. Plant assets are also called fixed assets or property, plant, and equipment. TRUE30. The current ratio is used to help assess a company's ability to pay its debts in the near future.TRUEMultiple Choice Questions64. Another name for temporary accounts is:A. Real accounts.B. Contra accounts.C. Accrued accounts.D. Balance column accounts.E. Nominal accounts.65. When closing entries are made:A. All ledger accounts are closed to start the new accounting period.B. All temporary accounts are closed but not the permanent accounts.C. All real accounts are closed but not the nominal accounts.D. All permanent accounts are closed but not the nominal accounts.E. All balance sheet accounts are closed.66. Revenues, expenses, and withdrawals accounts, which are closed at the end of each accounting period are:A. Real accounts.B. Temporary accounts.C. Closing accounts.D. Permanent accounts.E. Balance sheet accounts.67. Which of the following statements is incorrect?A. Permanent accounts is another name for nominal accounts.B. Temporary accounts carry a zero balance at the beginning of each accounting period.C. The Income Summary account is a temporary account.D. Real accounts remain open as long as the asset, liability, or equity items recorded in the accounts continue in existence.E. The closing process applies only to temporary accounts.68. Assets, liabilities, and equity accounts are not closed; these accounts are called:A. Nominal accounts.B. Temporary accounts.C. Permanent accounts.D. Contra accounts.E. Accrued accounts.69. Closing the temporary accounts at the end of each accounting period:A. Serves to transfer the effects of these accounts to the owner's capital account on the balance sheet.B. Prepares the withdrawals account for use in the next period.C. Gives the revenue and expense accounts zero balances.D. Causes owner's capital to reflect increases from revenues and decreases from expenses and withdrawals.E. All of these.70. Journal entries recorded at the end of each accounting period to prepare the revenue, expense, and withdrawals accounts for the upcoming period and to update the owner's capital account for the events of the period just finished are referred to as:A. Adjusting entries.B. Closing entries.C. Final entries.D. Work sheet entries.E. Updating entries.71. The closing process is necessary in order to:A. calculate net income or net loss for an accounting period.B. ensure that all permanent accounts are closed to zero at the end of each accounting period.C. ensure that the company complies with state laws.D. ensure that net income or net loss and owner withdrawals for the period are closed into the owner's capital account.E. ensure that management is aware of how well the company is operating.72. Closing entries are required:A. if management has decided to cease operating the business.B. only if the company adheres to the accrual method of accounting.C. if a company's bookkeeper forgets to prepare reversing entries.D. if the temporary accounts are to reflect correct amounts for each accounting period.E. in order to satisfy the Internal Revenue Service.73. The recurring steps performed each reporting period, starting with analyzing and recording transactions in the journal and continuing through the post-closing trial balance, is referred to as the:A. Accounting period.B. Operating cycle.C. Accounting cycle.D. Closing cycle.E. Natural business year.74. Which of the following is the usual final step in the accounting cycle?A. Journalizing transactions.B. Preparing an adjusted trial balance.C. Preparing a post-closing trial balance.D. Preparing the financial statements.E. Preparing a work sheet.75. A classified balance sheet:A. Measures a company's ability to pay its bills on time.B. Organizes assets and liabilities into important subgroups.C. Presents revenues, expenses, and net income.D. Reports operating, investing, and financing activities.E. Reports the effect of profit and withdrawals on owner's capital.76. The assets section of a classified balance sheet usually includes:A. Current assets, long-term investments, plant assets, and intangible assets.B. Current assets, long-term assets, revenues, and intangible assets.C. Current assets, long-term investments, plant assets, and equity.D. Current liabilities, long-term investments, plant assets, and intangible assets.E. Current assets, liabilities, plant assets, and intangible assets.77. The usual order for the asset section of a classified balance sheet is:A. Current assets, prepaid expenses, long-term investments, intangible assets.B. Long-term investments, current assets, plant assets, intangible assets.C. Current assets, long-term investments, plant assets, intangible assets.D. Intangible assets, current assets, long-term investments, plant assets.E. Plant assets, intangible assets, long-term investments, current assets.78. A classified balance sheet differs from an unclassified balance sheet in thatA. a unclassified balance sheet is never used by large companies.B. a classified balance sheet normally includes only three subgroups.C. a classified balance sheet presents information in a manner that makes it easier to calculate a company's current ratio.D. a classified balance sheet will include more accounts than an unclassified balance sheet for the same company on the same date.E. a classified balance sheet cannot be provided to outside parties.79. Two common subgroups for liabilities on a classified balance sheet are:A. current liabilities and intangible liabilities.B. present liabilities and operating liabilities.C. general liabilities and specific liabilities.D. intangible liabilities and long-term liabilities.E. current liabilities and long-term liabilities.80. The current ratio:A. Is used to measure a company's profitability.B. Is used to measure the relation between assets and long-term debt.C. Measures the effect of operating income on profit.D. Is used to help evaluate a company's ability to pay its debts in the near future.E. Is calculated by dividing current assets by equity.81. The current ratio:A. Is calculated by dividing current assets by current liabilities.B. Helps to assess a company's ability to pay its debts in the near future.C. Can reveal problems in a company if it is less than 1.D. Can affect a creditor's decision about whether to lend money to a company.E. All of these.AACSB: CommunicationsAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: HardLearning Objective: A182. The Unadjusted Trial Balance columns of a company's work sheet show the balance in the Office Supplies account as $750. The Adjustments columns show that $425 of these supplies were used during the period. The amount shown as Office Supplies in the Balance Sheet columns of the work sheet is:A. $325 debit.B. $325 credit.C. $425 debit.D. $750 debit.E. $750 credit.83. A 10-column spreadsheet used to draft a company's unadjusted trial balance, adjusting entries, adjusted trial balance, and financial statements, and which is an optional tool in the accounting process is a(n) :A. Adjusted trial balance.B. Work sheet.C. Post-closing trial balance.D. Unadjusted trial balance.E. General ledger.84. Accumulated Depreciation, Accounts Receivable, and Service Fees Earned would be sorted to which respective columns in completing a work sheet?A. Balance Sheet or Statement of Owner's Equity-Credit; Balance Sheet or Statement of Owner's Equity Debit; and Income Statement-Credit.B. Balance Sheet or Statement of Owner's Equity-Debit; Balance Sheet or Statement of Owner's Equity-Credit; and Income Statement-Credit.C. Income Statement-Debit; Balance Sheet or Statement of Owner's Equity-Debit; and Income Statement-Credit.D. Income Statement-Debit; Income Statement-Debit; and Balance Sheet or Statement of Owner's Equity-Credit.E. Balance Sheet or Statement of Owner's Equity-Credit; Income Statement-Debit; and Income Statement-Credit.85. Which of the following statements is incorrect?A. Working papers are useful aids in the accounting process.B. On the work sheet, the effects of the accounting adjustments are shown on the account balances.C. After the work sheet is completed, it can be used to help prepare the financial statements.D. On the work sheet, the adjusted amounts are sorted into columns according to whether the accounts are used in preparing the unadjusted trial balance or the adjusted trial balance.E. A worksheet is not a substitute for financial statements86. A company shows a $600 balance in Prepaid Insurance in the Unadjusted Trial Balance columns of the work sheet. The Adjustments columns show expired insurance of $200. This adjusting entry results in:A. $200 decrease in net income.B. $200 increase in net income.C. $200 difference between the debit and credit columns of the Unadjusted Trial Balance.D. $200 of prepaid insurance.E. An error in the financial statements.87. Statements that show the effects of proposed transactions as if the transactions had already occurred are called:A. Pro forma statements.B. Professional statements.C. Simplified statements.D. Temporary statements.E. Interim statements.88. If in preparing a work sheet an adjusted trial balance amount is mistakenly sorted to the wrong work sheet column. The Balance Sheet columns will balance on completing the work sheet but with the wrong net income, if the amount sorted in error is:A. An expense amount placed in the Balance Sheet Credit column.B. A revenue amount placed in the Balance Sheet Debit column.C. A liability amount placed in the Income Statement Credit column.D. An asset amount placed in the Balance Sheet Credit column.E. A liability amount placed in the Balance Sheet Debit column.89. If the Balance Sheet and Statement of Owner's Equity columns of a work sheet fail to balance when the amount of the net income is added to the Balance Sheet and Statement of Owner's Equity Credit column, the cause could be:A. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Debit column.B. A revenue amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.C. An asset amount entered in the Income Statement and Statement of Owner's Equity Debit column.D. A liability amount entered in the Income Statement and Statement of Owner's Equity Credit column.E. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.Problems129. In the table below, indicate with an "X" in the proper column whether the account is a (nominal) temporary account or a (real) permanent account.132. Based on the adjusted trial balance shown below, prepare a classified balance sheet for Focus Package Delivery.* $2,000 of the long-term note payable is due during the next year.135. Use the following partial work sheet from Matthews Lanes to prepare its income statement, statement of owner's equity and a balance sheet (Assume the owner did not make any investments in the business this year.)137. A partially completed work sheet is shown below. The unadjusted trial balance columns are complete. Complete the adjustments, adjusted trial balance, income statement, and balance sheet and statement of owner's equity columns.140. The adjusted trial balance of Sara's Web Services follows:(a) Prepare the closing entries for Sara's Web Services.(b) What is the balance of Sara's capital account after the closing entries are posted?Problems159. The unadjusted trial balance of Quick Delivery is entered on the partial work sheet below. Complete the work sheet using the following information:(a) Salaries earned by employees that are unpaid and unrecorded, $5,000.(b) An inventory of supplies showed $1,000 of unused supplies still on hand.(c) Depreciation on delivery vans, $24,000.(d) Services paid in advance by customers of $10,000 have now been provided tocustomers.。

会计英语

选择题:15*1=15(分)判断题:10*1.5=15(分)1、Which financial statement shows whether the business earned a profit andalso lists the types and amounts of the income and expenses?( D )A Balance sheet(资产负债表)B、Statement of changes in equity (权益变动表)C、Statement of cash flows (现金流量表)D、Income statement (利润表)2、What are quick assets(速动资产)? ( C )A、Cash, trading securities, prepaid expensesB、Cash ,inventory(库存),accounts receivableC、Cash ,trading securities ,accounts receivable(现金,交易性金融资产,应收账款)D、Cash ,accounts receivable ,prepaid expenses (待摊费用) 3、The qualitative characteristics of financial statements:(财务报表的质量特征)——(1)understandability (可理解性) (2)relevance(相关性)(3)reliability(可靠性) (4) comparability (可比性)4、The elements of financial statements are:(财务报表的要素有)(1)assets(资产)(2)liabilities (负债)(3)equity (权益)(4)revenues (收入) (5)expenses(费用)5、Assets are probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events.( 资产是指由过去的交易或事项形成的、由企业拥有或者控制、预期会给企业带来经济利益的资源。

会计循环1习题精选含答案

True / False Questions1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts.FALSE2. Income Summary is a temporary account only used for the closing process. TRUE3. Revenue accounts should begin each accounting period with zero balances. TRUE4. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUE5. The closing process takes place after financial statements have been prepared. TRUE6. Revenue and expense accounts are permanent (real) accounts and should not be closed at the end of the accounting period.FALSE7. Closing entries result in revenues and expenses being reflected in the owner's capital account.TRUE8. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUE9. The closing process is a two-step process. First revenue, expense, and withdrawals are set to a zero balance. Second, the process summarizes a period's assets and expenses.FALSE10. Closing entries are required at the end of each accounting period to close all ledger accounts.FALSE11. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital. TRUE12. The Income Summary account is a permanent account that will be carried forward period after period.FALSE13. Closing entries are necessary so that owner's capital will begin each period with a zero balance.FALSE14. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business.FALSE15. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUE16. The accounting cycle refers to the sequence of steps in preparing the work sheet. FALSE17. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUE18. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries. FALSE19. A classified balance sheet organizes assets and liabilities into important subgroups that provide more information to decision makers.TRUE20. An unclassified balance sheet provides more information to users than a classified balance sheet.FALSE21. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUE22. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUE23. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUE24. Current liabilities are cash and other resources that are expected to be sold, collected or used within one year or the company's operating cycle whichever is longer.FALSE25. Long-term investments can include land held for future expansion.TRUE26. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUE27. Current liabilities include accounts receivable, unearned revenues, and salaries payable.FALSE28. Cash and office supplies are both classified as current assets.TRUE29. Plant assets are also called fixed assets or property, plant, and equipment. TRUE30. The current ratio is used to help assess a company's ability to pay its debts in the near future.TRUEMultiple Choice Questions64. Another name for temporary accounts is:A. Real accounts.B. Contra accounts.C. Accrued accounts.D. Balance column accounts.E. Nominal accounts.65. When closing entries are made:A. All ledger accounts are closed to start the new accounting period.B. All temporary accounts are closed but not the permanent accounts.C. All real accounts are closed but not the nominal accounts.D. All permanent accounts are closed but not the nominal accounts.E. All balance sheet accounts are closed.66. Revenues, expenses, and withdrawals accounts, which are closed at the end of each accounting period are:A. Real accounts.B. Temporary accounts.C. Closing accounts.D. Permanent accounts.E. Balance sheet accounts.67. Which of the following statements is incorrect?A. Permanent accounts is another name for nominal accounts.B. Temporary accounts carry a zero balance at the beginning of each accounting period.C. The Income Summary account is a temporary account.D. Real accounts remain open as long as the asset, liability, or equity items recorded in the accounts continue in existence.E. The closing process applies only to temporary accounts.68. Assets, liabilities, and equity accounts are not closed; these accounts are called:A. Nominal accounts.B. Temporary accounts.C. Permanent accounts.D. Contra accounts.E. Accrued accounts.69. Closing the temporary accounts at the end of each accounting period:A. Serves to transfer the effects of these accounts to the owner's capital account on the balance sheet.B. Prepares the withdrawals account for use in the next period.C. Gives the revenue and expense accounts zero balances.D. Causes owner's capital to reflect increases from revenues and decreases from expenses and withdrawals.E. All of these.70. Journal entries recorded at the end of each accounting period to prepare the revenue, expense, and withdrawals accounts for the upcoming period and to update the owner's capital account for the events of the period just finished are referred to as:A. Adjusting entries.B. Closing entries.C. Final entries.D. Work sheet entries.E. Updating entries.71. The closing process is necessary in order to:A. calculate net income or net loss for an accounting period.B. ensure that all permanent accounts are closed to zero at the end of each accounting period.C. ensure that the company complies with state laws.D. ensure that net income or net loss and owner withdrawals for the period are closed into the owner's capital account.E. ensure that management is aware of how well the company is operating.72. Closing entries are required:A. if management has decided to cease operating the business.B. only if the company adheres to the accrual method of accounting.C. if a company's bookkeeper forgets to prepare reversing entries.D. if the temporary accounts are to reflect correct amounts for each accounting period.E. in order to satisfy the Internal Revenue Service.73. The recurring steps performed each reporting period, starting with analyzing and recording transactions in the journal and continuing through the post-closing trial balance, is referred to as the:A. Accounting period.B. Operating cycle.C. Accounting cycle.D. Closing cycle.E. Natural business year.74. Which of the following is the usual final step in the accounting cycle?A. Journalizing transactions.B. Preparing an adjusted trial balance.C. Preparing a post-closing trial balance.D. Preparing the financial statements.E. Preparing a work sheet.75. A classified balance sheet:A. Measures a company's ability to pay its bills on time.B. Organizes assets and liabilities into important subgroups.C. Presents revenues, expenses, and net income.D. Reports operating, investing, and financing activities.E. Reports the effect of profit and withdrawals on owner's capital.76. The assets section of a classified balance sheet usually includes:A. Current assets, long-term investments, plant assets, and intangible assets.B. Current assets, long-term assets, revenues, and intangible assets.C. Current assets, long-term investments, plant assets, and equity.D. Current liabilities, long-term investments, plant assets, and intangible assets.E. Current assets, liabilities, plant assets, and intangible assets.77. The usual order for the asset section of a classified balance sheet is:A. Current assets, prepaid expenses, long-term investments, intangible assets.B. Long-term investments, current assets, plant assets, intangible assets.C. Current assets, long-term investments, plant assets, intangible assets.D. Intangible assets, current assets, long-term investments, plant assets.E. Plant assets, intangible assets, long-term investments, current assets.78. A classified balance sheet differs from an unclassified balance sheet in thatA. a unclassified balance sheet is never used by large companies.B. a classified balance sheet normally includes only three subgroups.C. a classified balance sheet presents information in a manner that makes it easier to calculate a company's current ratio.D. a classified balance sheet will include more accounts than an unclassified balance sheet for the same company on the same date.E. a classified balance sheet cannot be provided to outside parties.79. Two common subgroups for liabilities on a classified balance sheet are:A. current liabilities and intangible liabilities.B. present liabilities and operating liabilities.C. general liabilities and specific liabilities.D. intangible liabilities and long-term liabilities.E. current liabilities and long-term liabilities.80. The current ratio:A. Is used to measure a company's profitability.B. Is used to measure the relation between assets and long-term debt.C. Measures the effect of operating income on profit.D. Is used to help evaluate a company's ability to pay its debts in the near future.E. Is calculated by dividing current assets by equity.81. The current ratio:A. Is calculated by dividing current assets by current liabilities.B. Helps to assess a company's ability to pay its debts in the near future.C. Can reveal problems in a company if it is less than 1.D. Can affect a creditor's decision about whether to lend money to a company.E. All of these.AACSB: CommunicationsAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: HardLearning Objective: A182. The Unadjusted Trial Balance columns of a company's work sheet show the balance in the Office Supplies account as $750. The Adjustments columns show that $425 of these supplies were used during the period. The amount shown as Office Supplies in the Balance Sheet columns of the work sheet is:A. $325 debit.B. $325 credit.C. $425 debit.D. $750 debit.E. $750 credit.83. A 10-column spreadsheet used to draft a company's unadjusted trial balance, adjusting entries, adjusted trial balance, and financial statements, and which is an optional tool in the accounting process is a(n) :A. Adjusted trial balance.B. Work sheet.C. Post-closing trial balance.D. Unadjusted trial balance.E. General ledger.84. Accumulated Depreciation, Accounts Receivable, and Service Fees Earned would be sorted to which respective columns in completing a work sheet?A. Balance Sheet or Statement of Owner's Equity-Credit; Balance Sheet or Statement of Owner's Equity Debit; and Income Statement-Credit.B. Balance Sheet or Statement of Owner's Equity-Debit; Balance Sheet or Statement of Owner's Equity-Credit; and Income Statement-Credit.C. Income Statement-Debit; Balance Sheet or Statement of Owner's Equity-Debit; and Income Statement-Credit.D. Income Statement-Debit; Income Statement-Debit; and Balance Sheet or Statement of Owner's Equity-Credit.E. Balance Sheet or Statement of Owner's Equity-Credit; Income Statement-Debit; and Income Statement-Credit.85. Which of the following statements is incorrect?A. Working papers are useful aids in the accounting process.B. On the work sheet, the effects of the accounting adjustments are shown on the account balances.C. After the work sheet is completed, it can be used to help prepare the financial statements.D. On the work sheet, the adjusted amounts are sorted into columns according to whether the accounts are used in preparing the unadjusted trial balance or the adjusted trial balance.E. A worksheet is not a substitute for financial statements86. A company shows a $600 balance in Prepaid Insurance in the Unadjusted Trial Balance columns of the work sheet. The Adjustments columns show expired insurance of $200. This adjusting entry results in:A. $200 decrease in net income.B. $200 increase in net income.C. $200 difference between the debit and credit columns of the Unadjusted Trial Balance.D. $200 of prepaid insurance.E. An error in the financial statements.87. Statements that show the effects of proposed transactions as if the transactions had already occurred are called:A. Pro forma statements.B. Professional statements.C. Simplified statements.D. Temporary statements.E. Interim statements.88. If in preparing a work sheet an adjusted trial balance amount is mistakenly sorted to the wrong work sheet column. The Balance Sheet columns will balance on completing the work sheet but with the wrong net income, if the amount sorted in error is:A. An expense amount placed in the Balance Sheet Credit column.B. A revenue amount placed in the Balance Sheet Debit column.C. A liability amount placed in the Income Statement Credit column.D. An asset amount placed in the Balance Sheet Credit column.E. A liability amount placed in the Balance Sheet Debit column.89. If the Balance Sheet and Statement of Owner's Equity columns of a work sheet fail to balance when the amount of the net income is added to the Balance Sheet and Statement of Owner's Equity Credit column, the cause could be:A. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Debit column.B. A revenue amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.C. An asset amount entered in the Income Statement and Statement of Owner's Equity Debit column.D. A liability amount entered in the Income Statement and Statement of Owner's Equity Credit column.E. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.Problems129. In the table below, indicate with an "X" in the proper column whether the account is a (nominal) temporary account or a (real) permanent account.132. Based on the adjusted trial balance shown below, prepare a classified balance sheet for Focus Package Delivery.* $2,000 of the long-term note payable is due during the next year.135. Use the following partial work sheet from Matthews Lanes to prepare its income statement, statement of owner's equity and a balance sheet (Assume the owner did not make any investments in the business this year.)137. A partially completed work sheet is shown below. The unadjusted trial balance columns are complete. Complete the adjustments, adjusted trial balance, income statement, and balance sheet and statement of owner's equity columns.140. The adjusted trial balance of Sara's Web Services follows:(a) Prepare the closing entries for Sara's Web Services.(b) What is the balance of Sara's capital account after the closing entries are posted?Problems159. The unadjusted trial balance of Quick Delivery is entered on the partial work sheet below. Complete the work sheet using the following information:(a) Salaries earned by employees that are unpaid and unrecorded, $5,000.(b) An inventory of supplies showed $1,000 of unused supplies still on hand.(c) Depreciation on delivery vans, $24,000.(d) Services paid in advance by customers of $10,000 have now been provided tocustomers.。

会计英语

会计英语一、听力Three key (1) financial statements represent the essentials in obtaining these information. They are the (2) balance sheet, the (3) income statement and the (4) cash flow statement . Financial statements are usually prepared by the companies on the (5) accounts . And they may be (6) reviewed or (7) audited and (8) certified for the (9) accuracy by outside the client firms. All (10) public traded companies are required to (11) publish financial statements. Most other businesses supply them as well. Financial statements are truly the language of business. In this program, we will follow two (12) managers as they assess the (13) financial help of two restaurants that they candidate for the (14) potential purchase or (15) acquisition . The story we will see is an imaginary one. The lessons are very real. You will learn how to use financial data to read the tales of these two restaurants. Most important, the lessons learnt can be applied to other businesses as well.The types of course work that we would look for when we are hiring someone straight out of undergraduate would be 1.__accounting_and 2.___finance_, because it provides a terminology. It allows us to communicate things quickly in a terminology we understand. People who have the detail-oriented approach to understand the 3._financial__statements__ from an 4. _accounting_perspective_. And also understand you know, the difference between the accounting statement, which is a 5._snapshot(快门)_ of what is going on now, and the financial type of 6. _forecast__ that allow us to then 7._project________ and think about how those financial statements are going to change going forward based on the things that the company is doing. That is the combination we are looking for, is being able to 8.___ understand the data___. But then being able to be flexible enough to look forward and think about how that data is going to change as the company 9.evolves. So it is very much a combination of accounting and finance. And again, to stress the written communication and the oral communication is just vital because people have to understand your analysis before they are going to be willing to 10._invest___on it.二、单选题1. Which of the following service involves providing an independent report on the appropriateness of financial statements? (A)A. AuditB. TaxC. ConsultingD. Budgeting2. Which of the following is a liability account?(C)A. Prepaid InsuranceB. Intangible AssetsC. Salaries PayableD. Accumulated Depreciation3、W hich of the following is a contra asset account?(C)A、InventoryB、GoodwillC、Accumulated DepreciationD、Retained Earnings4、Which of the following belongs to the current assets?(D)a.Long-term investmentb. Plant and equipmentc. Intangible assetsd. Inventory5、W hich of the following belongs to the long-term liabilities?(C)A、Retained earningsB、Capital stockC、Dividend payableD、Bonds payable6、Financial statement does not include ( D)A、lance sheetB、come statementC、sh flow statementD、king sheet7、profit-making business operating as a separate legal entity and in which ownershipis divided into shares of stock is known as a:(D)A. proprietorship.B. service business.C. partnership.D. corporation.8、2. If revenue was $45,000, expenses were $37,500, and the owner’s withdrawalswere $10,000, the amount of net income or net loss would be:(B)A. $45,000 net income.B. $7,500 net income.C. $37,500 net loss.D. $2,500 net loss.9、Which of the following items represents a deferral?(A)A. Prepaid insuranceB. Wages payableC. Fees earnedD. Accumulated depreciation10、If the estimated amount of depreciation on equipment for a period is $2,000, theadjusting entry to record depreciation would be:(C)A. debit Depreciation Expense, $2,000; credit Equipment,$2,000.B. debit Equipment, $2,000; credit Depreciation Expense,$2,000.C. debit Depreciation Expense, $2,000; credit Accumulated Depreciation,$2,000.D. debit Accumulated Depreciation, $2,000; credit Depr eciation Expense,$2,000.11、Which of the following accounts would not be closed to the income summaryaccount at the end of a period?(D)A. Depreciation ExpenseB. Wages ExpenseC. Rent ExpenseD. Accumulated Depreciation12、Which of the following is an example of an intangible asset?(D)A. PatentsB. GoodwillC. CopyrightsD. All of the above三、计算题(关于会计投资、筹资活动的现金流量)(2) Compute the net cash used (provided) by financing activities.Net cash provided by investing activities =81000-37000-53000=91000Net cash used by financing activities =47000-40000-85000-1000000= -78000四、填空题1、填字母(交易与相应的分类对上号)2、填数字(成本流转假设)——计算P553、排序题A. To record receipt of unearned revenue.B. To record this period’s earning of prior unearned revenue.C. To record payment of an accrued expense.D. To record receipt of an accrued revenue.E. To record an accrued expense.F. To record an accrued revenue.G. To record this period’s use of a prepaid expense.五、论述题(一)、chapter10(课本上96~97页)1、The factors that are directly relevant to an analysis of business performance:(1)、the size of the business(2)、the business risk(3)、the economic environment(4)、Industry trends ,effects of changes in technology2、The information that the public company provided includes:(1)、Chairman’s statement(2)、Director s’ report(3)、the balance sheet(4)、Statements of income and changes in equity(5)、Statement of cash flows(6)、Notes to the statements(7)、Auditors’ report(8)、External sources(二)、交易效果题(即资产、负债、所有者权益的增减问题)例:Describe the effects of each of the following business transactions on assets, liabilities and owners’equity.(1). Bought equipment on credit.(2). Paid salaries to employees.(3). Sold services for cash.答案:(1). Increase both asset and liability.(2). Decrease both asset and liability.(3). Increase both asset and owners’equity.知识点:第一章:1、Two objectives of financial statements(P5)会计目标2、Underlying Assumptions (P6)第三章:1、Financial statement consists (P19)财务报表的组成2、资产、负债、所有者的构成(P19~P20)——table 3-33、the format of balance sheet: the account form and the report (区别)例:In the report form,(报告式) the assets are listed on the left side of the page and liabilities and owner’s equity on the right side .(其中report form 应该是account form)*4、income Statement (P22-23)5、Three Categories of Cash Flows (区别)(P26)1、Investing activities2、Financing activities3、Operating activities第四章1、Accounting Equation: asset=liabilities+equity(P33)2、复式记账法(double-Entry Bookkeeping)的含义(P33)Debits must equal credits3、会计循环(Accounting Cycle)——排序题(P35)理解:过账、结账分录、试算平衡表、结账后试算平衡表的含义4、Accruals and deferrals adjustments 应计和递延项目的含义及能简单的区分它们5、close temporary accounts (P45)了解下期末的结算。

生产循环审计练习试卷1(题后含答案及解析)

生产循环审计练习试卷1(题后含答案及解析) 题型有:1. 单项选择题 2. 多项选择题 3. 综合分析题 4. 判断题单项选择题1.在生产循环的分析性复核中,通常运用的主要比率是存货周转率和( )。

A.销售成本B.平均存货C.毛利率D.存货跌价准备正确答案:C 涉及知识点:生产循环审计2.( )是存货审计中最重要、最具有决定性的审计程序。

A.观察B.函证C.监督盘点D.亲自盘点正确答案:C 涉及知识点:生产循环审计3.对于下列各项目及替代程序而言,( )不能认为是满意的。

A.以检查会计记录替代监盘存货B.以检查货运文件及出库记录替代函证应收账款C.以向银行发函替代检查银行对账单D.以检查决算日以后的会计记录替代函证负债正确答案:A 涉及知识点:生产循环审计4.被审计单位于12月28日收到货物并已验收入库,但购货发票于次年1月5日才收到,审计人员应提请被审计单位( )。

A.不必入账B.以暂估价入账C.在备查簿登记D.待收到发票后入账正确答案:B 涉及知识点:生产循环审计5.12月底入账的发票,如果附有12月31日前的验收报告,则说明( )。

A.购货高估B.购货低估C.截止期正确D.截止期错误正确答案:C 涉及知识点:生产循环审计6.应付职工薪酬的审计目标不应包括( )。

A.确定应付职工薪酬的计提金额是否合理、正确B.确定应付职工薪酬计提和支付的记录是否完整、正确C.确定应付职工薪酬的表达和披露是否恰当D.确定应付职工薪酬是否存在正确答案:D 涉及知识点:生产循环审计7.审计人员观察被审计单位存货盘点的主要目的是( )。

A.查明是否漏盘某些重要存货B.鉴定存货的质量C.了解存货的所有权是否归属被审计单位D.获取存货是否实际存在的审计证据正确答案:D 涉及知识点:生产循环审计8.永续盘存记录应由( )。

A.会计部门负责B.存储部门负责C.验收部门负责D.采购部门负责正确答案:A 涉及知识点:生产循环审计多项选择题9.审计人员对被审计单位存货截止测试的方法有( )。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Manual homework no.2Class_________ name__________ student no.__________The following post-closing trial balance is for Valley View Company as of December 31, 2004.Valley View CompanyPost Closing Trial BalanceDecember 31, 2004Dr CrCash $17,500Accounts Receivable 17,000Inventory 28,800Supplies on Hand 1,200Building 80,000Accounts Payable $18,000Mortgages Payable (7-year, 10%) 56,000Capital Stock (3600 shares outstanding) 54,000Retained Earnings 16,500Totals $144,500 $144,500 Following is a summary of the company’s transactions for 2005.(a)At the beginning of 2005, the company issued 1,500 new shares of stock at $20per share.(b)Total inventory purchases were $49,500; all purchases were made on credit andare recorded in the Inventory account on each purchase.(c)Total sales were $125,000; $102,900 were on credit, the rest were for cash. Thecost of goods sold was $47,500; the Inventory account is reduced at the time of each sale.(d)In December, a customer paid $3,500 cash in advance for merchandise that wastemporarily out of stock. The advance payments received from customers are initially worded as unearned sales revenue (liabilities). The $3,500 is not included in the sales figures in (c) above.(e)The company paid $66,500 on accounts payable during the year.(f)The company collected $102,000 of accounts receivable during the year.(g)The company purchased $600 of supplies for cash during 2005, debiting Supplieson Hand for the cost of each purchase.(h)The company paid $850 for advertising during the year, debiting PrepaidAdvertising.(i)Total salaries paid for the year were $45,000 and total utilities paid for the yearwere $650.(j)The company paid $8,000 on the mortgages.(k)Dividends of $7,500 were declared and paid to stockholders in December.On December 31, 2005, the company’s accountant gathers the following information that is needed to adjust the accounts:(l)As of December 31, salaries of $750 had been earned by employees but will not be paid until January 3, 2006.(m)A count of the remaining supplies at December 31 shows $800 of supplies still on hand.(n)The $850 prepaid advertising includes $400 paid on December 1, 2005, for a series of radio advertisements to be broadcast throughout December 2005 and January 2006. The other $450 represents advertisements that were broadcast during 2005.(o)For some reason the company failed to pay interests due on the mortgages payable in 2005, which is calculated as 5,600. The company promised to pay in the beginning of next year.(p)On December 20, 2005, a $150 bill was received for utilities. So far no entry was made to record the receipt of the bill, which is due to be paid on January 4, 2006. (q)As of December 31, 2005, the merchandise paid for in advance (transaction d) was still out of stock. The company expects to receive the merchandise and fill the order by January 15, 2006.(r)The company’s income is taxed at a rate of 15%.Required: 1. Make entries in the General Journal to record each of the transactions (items a through k)2. Using T-accounts to represent the General Ledger accounts, post the transactions recorded in the General Journal. Enter the beginning balances in the accounts that appear in the December 31, 2004, post-closing trial balance before posting 2005 transactions. When all transactions have been posted to the T-accounts, determine the balance for each account.3. Prepare a trial balance as of December 31, 2005.4. Record adjusting entries (item l through r) in the General Journal, and post these entries to the General Ledger (T-accounts).5. Prepare an income statement and balance sheet for 2005.6. Record closing entries (items s through u) in the General Journal, and post these entries to the General Ledger (T-accounts).7. Prepare a post-closing trial balance.Solution 1 Journal Entries (choose the name of accounts according to the2. T-Accountsnote 1: Accounts that are entered more than once (beginning balance should be viewed as an entry) need to be balanced under the first balancing line.2: mark the transaction number in front of each entry3. Trial BalanceValley View CompanyTrial BalanceDecember 31, 2005Dr Cr CashAccounts ReceivableInventorySupplies on HandPrepaid AdvertisingBuildingAccounts PayableUnearned sales revenueMortgages PayableCapital StockRetained EarningsDividendsSales RevenueCost of goods soldSalaries ExpenseUtilities ExpenseTotals $278,000 $278,000 4. Recording and Posting Adjustments②Now go back to update the T-Accounts above in part 2, then balance the accounts under the second (first) balancing line given in the accounts. Accounts that are entered only once so far (the beginning balance should be viewed as an entry) don’t need to be balanced.③The adjusted trial balance is as following.Valley View CompanyAdjusted Trial BalanceDecember 31, 2005Dr CrCashAccounts ReceivableInventorySupplies on HandPrepaid AdvertisingBuildingAccounts PayableSalaries PayableUtilities PayableIncome Taxes PayableUnearned Sales RevenueInterest PayableMortgages PayableCapital StockRetained EarningsDividendsSales RevenueCost of goods soldSalaries ExpenseAdvertising ExpenseUtilities ExpenseSupplies ExpenseInterest ExpenseIncome Tax ExpenseTotals $ $5. Prepare Financial StatementsValley View CompanyIncome StatementFor the Year Ended December 31, 2005Sales revenue $Less cost of goods soldGross profit $Less operating expenses:Salaries expense $Advertising expenseUtilities expenseSupplies expenseTotal operating expense $ Operating income $ InterestIncome before taxes $ Income taxNet income $ 20,145Valley View CompanyStatement of owners’ equityFor the Year Ended December 31, 2005Owners’ equity 12/31/04Add: issuance of stockNet incomeLess: DividendsOwner s’ equity 12/31/05 $ 113,145Valley View CompanyBalance Sheet6. Journalizing and posting closing entries②Go back and update the T-Accounts above in part 2, then balance the Retained earnings account and make sure that all the nominal accounts have been cleared.7. Post-closing Trial BalanceValley View CompanyPost-closing Trial BalanceDecember 31, 2005Dr CrCash $Accounts ReceivableInventorySupplies on HandPrepaid AdvertisingBuildingAccounts PayableSalaries PayableUtilities PayableInterest PayableIncome Taxes PayableUnearned Sales RevenueMortgages PayableCapital StockRetained EarningsTotals $ $。