实用会计英语(第四版) (6)

会计英语6-10章 中文翻译(叶建芳 孙红星)

制造企业主要包括以下三类存货: 1. 原材料,指企业取得的并将用于生产过程的物品。 2. 在产品,指正在各个生产工序加工的产品。记入在产品的成本包括原材料的成本, 直接人工成本和制造费用。 3. 产成品,指已经完工待售的产品。 在出售时,将产成品的成本确认为销售成本。成本确认的一个大致规则是,工厂内部发 生的成本确认为存货的成本,而工厂外部发生的成本记为销售费用或管理费用。 存货成本包括购买成本以及使存货达到预定可销售状态所发生的一切成本。 合理地计算 存货成本对于企业正确制定其产量, 定价以及战略决策是非常关键的。 生产过程的全部成本 以及使存货达到预定可销售状态的成本都应记入存货成本。与销售相关的成本作为期间费 用。 我们按存货的原始成本记录存货。 存货成本包括为使存货达到目前状态与位置的一切支 出。因此成本包括发票价格,运输费,运输途中保险费,以及其他相关费用。 对于生产制造企业来讲,存货的成本包括原材料成本,生产过程的人工成本,以及其他 相关制造费用。因此资本化的存货成本包括三类不同的存货:原材料,在产品和产成品。 ◇谁拥有存货? 一般地,只有企业拥有存货的法定所有权,才可以将其作为存货列示在资产负债表中。 在离岸价格交货的情况下,在途商品的所有权归买方所有。因为在这种情况下,商品的 所有权已于商品装上运输工具时转移给买方。若采用目的地交货,卖方支付运输费用,并拥 有商品的所有权,当商品抵达目的地后,其所有权才转移给买方。 在委托代销的情况下,商品的所有者(委托人)将商品转给零售商(受托人) 。受托人 为委托人销售商品,但并不享有商品的所有权。 只有在满足以下两个条件时,存货才能被确认: (a)与该存货有关的经济利益很可能流 入企业;(b)该存货的成本能够可靠计量。

6.3 存货成本流转假设

当存货的单位成本一直不变时,确定期末存货的单位成本是很容易的。但现实生活中, 存货的单位成本一直在变。 如果我们可以确定期末存货中每一件存货的取得成本, 那么就可 以很容易地确定期末存货的总成本。 这种确定期末存货成本的方法称为个别认定法。 个别认 定法按存货的实物流转来分配成本。从理论角度,个别认定法较受青睐,尤其是对于单位价 值比较高的单一存货。但若企业存货数量较多时,采用个别认定法,一一认定每件存货的取 得成本会使成本计算任务繁重,费时费力,且核算成本非常高。对于存货数量多,且存货单 价较低的企业一般采用下面三种存货成本流转假设: (注意存货成本流转假设只是出于会计 目的,与存货实物流转无关。 ) 1.平均成本流转假设 按平均成本确定每件存货的成本。这种方法假设所销售的商品 的成本等于平均成本,即每次购入存货的成本的加权平均。 2.先进先出法 假设先购入的存货先发出。先进先出法的假设有一定的道理,因为我 们认为企业都想不断地更新自己的存货,并将最先购入的存货最先售出。通货膨胀时,使用 先进先出法计算出的净利润比其他方法下计算出的高, 因为此时根据先进先出法的假定, 售 出的是最先购入的存货,而在通货膨胀存在的情况下,最先购入的存货的单价较低,所以企 业的销售成本较低。若企业在通货膨胀,物价水平较高时,不断地补充存货,则由此所产生 的高利润一般被成为“存货利润”或“虚假利润” 。在通货紧缩时,使用先进先出法的影响 与上述相反,会使净利润偏低。 3.后进先出法 假设后购入的存货先发出。当物价上涨时,使用后进先出法计算的当 期净利润会比其他方法少。因此在物价上涨时,使用后进先出法是比较稳健的做法。因为近 期购入的存货的成本接近于企业存货的重置成本。 因此, 后进先出法把当期成本与当期收入 很好地进行配比。同时,由于净利润相对偏低,后进先出法还具有减少企业所得税的优点。 在通货紧缩,物价水平下降时,后进先出法的影响与上述相反。在物价水平下降时,使用后

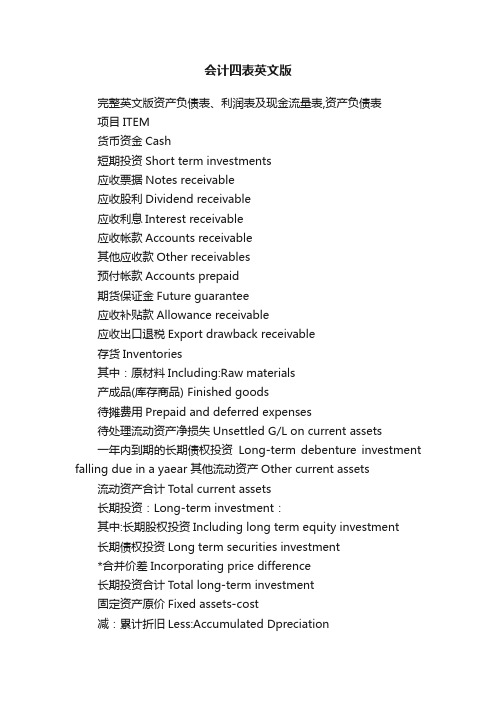

会计四表英文版

会计四表英文版完整英文版资产负债表、利润表及现金流量表,资产负债表项目ITEM货币资金Cash短期投资Short term investments应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款Other receivables预付帐款Accounts prepaid期货保证金Future guarantee应收补贴款Allowance receivable应收出口退税Export drawback receivable存货Inventories其中:原材料Including:Raw materials产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets长期投资:Long-term investment:其中:长期股权投资Including long term equity investment长期债权投资Long term securities investment*合并价差Incorporating price difference长期投资合计Total long-term investment固定资产原价Fixed assets-cost减:累计折旧Less:Accumulated Dpreciation固定资产净值Fixed assets-net value减:固定资产减值准备Less:Impairment of fixed assets固定资产净额Net value of fixed assets固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理Including:Fixed assets repair固定资产改良支出Improvement expenditure of fixed assets 其他长期资产Other long term assets其中:特准储备物资Among it:Specially approved reserving materials无形及其他资产合计Total intangible assets and other assets 递延税款借项Deferred assets debits资产总计Total Assets资产负债表(续表) Balance Sheet项目ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款Other payable to government其他应付款Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year 其他流动负债Other current liabilities流动负债合计Total current liabilities长期借款Long-term loans payable应付债券Bonds payable长期应付款long-term accounts payable专项应付款Special accounts payable其他长期负债Other long-term liabilities其中:特准储备资金Including:Special reserve fund长期负债合计Total long term liabilities递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"s capital 集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve公益金public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列)Unaffirmed investmentloss未分配利润Retained earnings外币报表折算差额Converted difference in Foreign Currency Statements所有者权益合计T otal shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表INCOME STA TEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales减:销售折扣与折让Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales减:销售费用Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain forprevious years利润总额Total profit减:所得税Less:Income tax净利润Net profit现金流量表Cash Flows StatementPrepared by:Period: Unit:Items1.Cash Flows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)V alue added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activities2.Cash Flows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activities3.Cash Flows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activities4.Effect of Foreign Exchange Rate Changes on Cash/doc/2e18298201.html, Increase in Cash and Cash EquivalentsSupplemental Information1.Investing and Financing Activities that do not Involve inCash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investories2.Reconciliation of Net Profit to Cash Flows from Operating Activities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activities/doc/2e18298201.html, Increase in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents现金流量表的现金流量声明拟制人:时间:单位:项目1.cash流量从经营活动:01 )所收到的现金从销售货物或提供劳务02 )收到的租金增值税销售额收到退款的价值03 )增值税缴纳04 )退回的其他税收和征费以外的增值税07 )其他现金收到有关经营活动08 )分,总现金流入量09 )用现金支付的商品和服务10 )用现金支付经营租赁11 )用现金支付,并代表员工12 )增值税购货支付13 )所得税的缴纳14 )支付的税款以外的增值税和所得税17 )其他现金支付有关的经营活动18 )分,总的现金流出19 )净经营活动的现金流量2.cash流向与投资活动:20 )所收到的现金收回投资21 )所收到的现金从分配股利,利润22 )所收到的现金从国债利息收入现金净额收到的处置固定资产,无形资产23 )资产和其他长期资产26 )其他收到的现金与投资活动27 )小计的现金流入量用现金支付购建固定资产,无形资产28 )和其他长期资产29 )用现金支付,以获取股权投资30 )用现金支付收购债权投资33 )其他现金支付的有关投资活动34 )分,总的现金流出35 )的净现金流量,投资活动产生3.cash流量筹资活动:36 )的收益,从发行股票37 )的收益,由发行债券38 )的收益,由借款41 )其他收益有关的融资活动42 ),小计的现金流入量43 )的现金偿还债务所支付的44 )现金支付的费用,对任何融资活动45 )支付现金,分配股利或利润46 )以现金支付的利息费用47 )以现金支付,融资租赁48 )以现金支付,减少注册资本51 )其他现金收支有关的融资活动52 )分,总的现金流出53 )的净现金流量从融资活动4.effect的外汇汇率变动对现金/doc/2e18298201.html,增加现金和现金等价物补充资料1.investing活动和筹资活动,不参与现金收款和付款56 )偿还债务的转让固定资产57 )偿还债务的转移投资58 )投资在形成固定资产59 )偿还债务的转移库存量2.reconciliation净利润现金流量从经营活动62 )净利润63 )补充规定的坏帐或不良债务注销64 )固定资产折旧65 )无形资产摊销损失处置固定资产,无形资产66 )和其他长期资产(或减:收益)67 )损失固定资产报废68 )财务费用69 )引起的损失由投资管理(或减:收益)70 )defered税收抵免(或减:借记卡)71 )减少存货(或减:增加)72 )减少经营性应收(或减:增加)73 )增加的经营应付账款(或减:减少)74 )净支付的增值税(或减:收益净额75 )净经营活动的现金流量/doc/2e18298201.html,增加现金和现金等价物76 )的现金,在此期限结束77 )减:现金期开始78 )加:现金等价物在此期限结束79 )减:现金等价物期开始80 ),净增加现金和现金等价物。

会计英语(第四版)

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1 会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的围要大于簿记。

图表1-1是信息在会计系统的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2 组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3 编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计实用英语

会计实用英语第一篇:会计实用英语account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specifictime periods ,typically one year(通常是一年)资产负债表:balance sheet 可以不大写b利润表: income statements(or statements of income)利润分配表:retained earnings现金流量表:cash flowsAccounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室accountant genaral 会计主任 account balancde 结平的帐户 account bill 帐单account books 帐account classification 帐户分类Income statement 损益表 Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会 Statement of cash flow 现金流量表 Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系 Assets 资产 Business entity 企业个体 Capital stock 股本 Corporation 公司 Cost principle 成本原则 Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设 Inflation 通货膨涨 Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量 Operating activities 经营活动 Owner's equity 所有者权益 Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设 Stockholders 股东Stockholders' equity 股东权益Window dressing 门面粉饰Account 帐第二篇:会计常用英语现金 Cash in hand银行存款 Cash in bank其他货币资金-外埠存款Other monetary assetscashier‘s check其他货币资金-银行汇票 Other monetary assetscredit cards 其他货币资金-信用证保证金Other monetary assetscash for investment短期投资-股票投资 Investmentsstocks短期投资-债券投资 Investmentsbonds短期投资-基金投资 Investmentsfunds短期投资-其他投资 Investmentsothers短期投资跌价准备 Provision for short-term investment长期股权投资-股票投资 Long term equity investmentothers长期债券投资-债券投资 Long term securities investemntothers长期投资减值准备 Provision for long-term investment应收票据 Notes receivable应收股利 Dividends receivable应收利息 Interest receivable应收帐款 Trade debtors坏帐准备-应收帐款 Provision for doubtful debtsother debtors 其他流动资产 Other current assets物资采购 Purchase原材料 Raw materials包装物 Packing materials低值易耗品 Low value consumbles材料成本差异 Material cost difference自制半成品 Self-manufactured goods库存商品 Finished goods商品进销差价Difference between purchase & sales of commodities委托加工物资 Consigned processiong material 委托代销商品 Consignment-out受托代销商品 Consignment-in分期收款发出商品 Goods on instalment sales存货跌价准备 Provision for obsolete stocks待摊费用 Prepaid expenses待处理流动资产损益 Unsettled G/L on current assets待处理固定资产损益 Unsettled G/L on fixed assets委托贷款-本金 Consignment loaninterest委托贷款-减值准备 Consignment loanBuildings固定资产-机器设备Fixed assetsElectronic Equipment, furniture and fixtures固定资产-运输设备Fixed assetsspecific materials工程物资-专用设备 Project materialprepaid for equipment工程物资-为生产准备的工具及器具 Project materialpatent无形资产-非专利技术 Intangible assetstrademark rights无形资产-土地使用权 Intangible assetsgoodwill无形资产减值准备 Impairment of intangible assets长期待摊费用 Deferred assets未确认融资费用 Unrecognized finance fees其他长期资产 Other long term assets递延税款借项 Deferred assets debits应付票据 Notes payable应付帐款 Trade creditors预收帐款 Adanvances from customers代销商品款 Consignment-in payables其他应交款 Other payable to government其他应付款 Other creditors应付股利 Proposed dividends待转资产价值 Donated assets预计负债 Accrued liabilities应付短期债券 Short-term debentures payable其他流动负债 Other current liabilities预提费用 Accrued expenses应付工资 Payroll payable应付福利费 Welfare payable短期借款-抵押借款 Bank loanspledged短期借款-信用借款 Bank loanscredit短期借款-担保借款 Bank loansguaranteed一年内到期长期借款 Long term loans due within one year一年内到期长期应付款 Long term payable due within one year 长期借款 Bank loansPar value应付债券-债券溢价 Bond payableDiscount应付债券-应计利息 Bond payableincome tax应交税金-增值税 Tax payablebusiness tax应交税金-消费税 Tax payableothers递延税款贷项 Deferred taxation credit股本 Share capital已归还投资 Investment returned利润分配-其他转入Profit appropriationstatutory surplus reserve利润分配-提取法定公益金 Profit appropriationreserve fund利润分配-提取企业发展基金Profit appropriationstaff bonus and welfare fund利润分配-利润归还投资Profit appropriationpreference shares dividends利润分配-提取任意盈余公积Profit appropriationordinary shares dividends利润分配-转作股本的普通股股利Profit appropriationshare premium资本公积-接受捐赠非现金资产准备Capital surpluscash donation资本公积-股权投资准备 Capital surplussubsidiary资本公积-外币资本折算差额 Capital surplusothers盈余公积-法定盈余公积金Surplus reserveother surplus reserve盈余公积-法定公益金 Surplus reservereserve fund盈余公积-企业发展基金Surplus reservereture investment by investment主营业务收入 Sales主营业务成本 Cost of sales主营业务税金及附加 Sales tax营业费用 Operating expenses管理费用 General and administrative expenses财务费用 Financial expenses投资收益 Investment income其他业务收入 Other operating income营业外收入 Non-operating income补贴收入 Subsidy income其他业务支出 Other operating expenses营业外支出 Non-operating expenses所得税 Income tax一、资产类 assets现金 cash on hand银行存款 cash in bank其他货币资金 other cash and cash equivalent短期投资 short-term investment短期投资跌价准备short-term investments falling price reserve应收票据 notes receivable应收股利 dividend receivable应收利息 interest receivable应收帐款 accounts receivable坏帐准备 bad debt reserve预付帐款 advance money应收补贴款 cover deficit receivable from state subsidize其他应收款 other notes receivable在途物资 materials in transit原材料 raw materials包装物 wrappage低值易耗品 low-value consumption goods库存商品 finished goods委托加工物资 work in process-outsourced委托代销商品trust to and sell the goods on a commission basis受托代销商品commissioned and sell the goods on a commission basis存货跌价准备 inventory falling price reserve 分期收款发出商品 collect money and send out the goods by stages待摊费用 deferred and prepaid expenses长期股权投资 long-term investment on stocks长期债权投资 long-term investment on bonds长期投资减值准备 long-term investment depreciation reserve 固定资产 fixed assets累计折旧 accumulated depreciation工程物资 project goods and material在建工程 project under construction固定资产清理 fixed assets disposal无形资产 intangible assets开办费 organization/preliminary expenses长期待摊费用 long-term deferred and prepaid expenses待处理财产损溢 wait deal assets loss or income二、负债类 debts短期借款 short-term loan应付票据 notes payable应付帐款 accounts payable预收帐款 advance payment代销商品款 consignor payable应付工资 accrued payroll应付福利费 accrued welfarism应付股利 dividends payable应交税金 tax payable其他应交款 accrued other payments 其他应付款 other payable预提费用 drawing expenses in advance 长期借款 long-term loan应付债券 debenture payable长期应付款 long-term payable递延税款 deferred tax住房周转金 revolving fund of house 三、所有者权益 owners equity股本 paid-up stock资本公积 capital reserve盈余公积 surplus reserve本年利润 current year profit利润分配 profit distribution四、成本类 cost生产成本 cost of manufacture制造费用 manufacturing overhead 五、损益类 profit and loss(p/l)主营业务收入 prime operating revenue 其他业务收入 other operating revenue 折扣与折让 discount and allowance投资收益 investment income补贴收入 subsidize revenue营业外收入 non-operating income主营业务成本 operating cost主营业务税金及附加tax and associate charge其他业务支出other operating expenses存货跌价损失 inventory falling price loss营业费用 operating expenses管理费用 general and administrative expenses财务费用 financial expenses营业外支出 non-operating expenditure所得税 income tax以前损益调整 adjusted p/l for prior year第三篇:会计英语求职信在外企上班用英语的求职信是不是会跟合适点呢?来看看如何写一篇好的英语求职信吧。

会计英语概述

2019/2/13

Decision Making

Economic Events

Reports

Exhibit 1-1

Financial statements report accounting information about resources, earning prospects, expected cash collections, incurred expenses, repayment ability, tax collection and negotiating wage agreements.

1、transaction n.交易;处理 Related transactions 关联交易 Transactions cost 交易成本 Business transactions 经济业务;商业交易 2、accounts n.帐目;会计账户;会计账簿 Accounts manager 会计部经理 Accounts receivables 应收账款 Accounts payable应付账款 Accounts department 会计部 3、Statements n.报告;报表 Accounting statement 会计报表=financial statement=statements Financial statements analysis 财务报表分析 Combination statements 汇总报表;合并报表 Suppliers statements 供应商对账单

【 LESSON 】

Recording Transactions

【 LESSON 】

Adjusting the Accounts, Preparing the Statements, and Completing the Accounting Cycle

《实用会计英语》课件

积极互动

与同学和老师积极互动,主 动参与讨论和演练。

实用技能和应用

财务报表分析

学会分析财务报表,评估公司 的财务状况和经营绩效。

预算编制与监控ห้องสมุดไป่ตู้

掌握预算编制和监控的技巧, 有效管理公司的财务资源。

税务筹划

了解税务规定,为公司进行税 务筹划,合法降低税负。

总结和要点

掌握专业英语表达能力

熟悉会计领域的英语术语,流利地与国际同行交流。

深入了解会计知识

掌握财务报表分析、预算编制等核心会计技能。

应用于实际工作

将所学知识应用到实际会计工作中,提高工作效率。

《实用会计英语》PPT课 件

本课程将帮助您掌握实用会计英语的关键知识和技能,从而能够更好地应对 会计工作中的各种挑战。

课程目标

1 强化英语能力

提高对会计领域英语表 达的理解和运用能力。

2 丰富会计知识

深入学习会计相关的词 汇、概念和原则。

3 提升职场竞争力

使您能够流利地与国际 客户、同事和合作伙伴 沟通。

课程大纲

1. 会计基础知识 2. 财务报表的分析和解读 3. 预算和成本管理 4. 税务法规和会计准则

课程重点

1 会计术语

掌握会计领域的专业术语,如资产、负债、利润等。

2 财务报表

了解并学会分析、解读财务报表,如利润表、资产负债表等。

3 会计信息系统

学习使用会计软件和工具,提高工作效率。

课程难点

1 专业词汇

理解和运用会计领域的专业术语和词汇。

2 复杂概念

掌握财务会计和管理会计中的复杂概念和原则。

3 实际应用

将所学知识应用到实际会计工作中。

学习方法和技巧

会计英语第四版参考答案

会计英语第四版参考答案会计英语第四版参考答案会计英语是会计专业学生必修的一门课程,它旨在帮助学生掌握会计领域的专业术语和表达方式。

《会计英语第四版》是一本广泛使用的教材,其中包含了大量的习题和案例,供学生练习和巩固知识。

本文将为大家提供《会计英语第四版》的参考答案,希望对学习者有所帮助。

第一章:会计概述1. 会计的定义是什么?会计是一门研究经济活动并提供相关信息的学科,它通过记录、分类、汇总和报告财务信息,帮助用户做出经济决策。

2. 什么是会计要素?会计要素是构成会计信息的基本要素,包括资产、负债、所有者权益、收入和费用。

3. 会计的目标是什么?会计的目标是提供有关企业财务状况、经营成果和现金流量的信息,帮助用户做出正确的经济决策。

第二章:会计准则和规范1. 什么是会计准则?会计准则是规范会计信息记录和报告的原则和规则,它确保财务报表的准确性、可比性和可理解性。

2. 什么是国际财务报告准则(IFRS)?国际财务报告准则是由国际会计准则委员会制定的全球通用的会计准则,旨在提高财务报告的质量和可比性。

3. 什么是美国通用会计准则(US GAAP)?美国通用会计准则是美国财务会计准则委员会制定的会计准则,适用于在美国注册的公司。

第三章:资产负债表1. 什么是资产负债表?资产负债表是一份反映企业财务状况的报表,它列出了企业的资产、负债和所有者权益。

2. 资产负债表的基本公式是什么?资产负债表的基本公式是:资产=负债+所有者权益。

3. 什么是流动资产和非流动资产?流动资产是指在一年内可以变现或消耗的资产,如现金、应收账款等;非流动资产是指长期持有的资产,如固定资产和投资。

第四章:利润表1. 什么是利润表?利润表是一份反映企业经营成果的报表,它列出了企业的收入、费用和利润。

2. 利润表的基本公式是什么?利润表的基本公式是:利润=收入-费用。

3. 什么是毛利润和净利润?毛利润是指企业在销售产品或提供服务后剩余的金额,净利润是指扣除所有费用后的利润。

《实用会计英语》课件

Summary

The application of accounting English in business communication can improve communication efficiency and accuracy.

Detailed description

Familiarity with the English expression of financial statements helps to accurately interpret and analyze financial information.

Summary

Financial statements such as balance sheets, income statements, and cash flow statements have specific expressions and terminology in English. Mastering these expressions can help learners better understand the content of financial statements, conduct financial analysis, and make decisions.

Summary words: Basic assumptions and principlesDetailed description: The basic assumptions of accounting include going concern, accounting period, and accrual basis. These assumptions provide the foundation for accounting procedures and methods, and affect the preparation of financial statements. Accounting principles, also known as general principles or accounting standards, are norms that guide accounting practice, including reliability, relevance, comprehensibility, comparability, substance over form, importance, prudence, and timeliness.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

高等教育出版社

3 Types of Long-lived Assets

高等教育出版社

4 6.1 Types of Assets

Definition:

▲ Assets are economic resources of a business that are expected to be of benefit in the future. It includes all property, rights as a creditor to others, and other rights.

Depreciation of a fixed asset is based upon the asset’s

(1) Cost (2)Estimated useful life (3)Estimated residual value

高等教育出版社

8 6.3 Depreciation of Fixed Assets

Classification:

▲ Assets can be classified into current assets and non-current assets. (1) Current assets refers to those assets which will be realized or consumed

▲ Application of the cost principle

(1) Land and land improvements (2) Buildings (3) Equipment (4) A lump-sum (Basket) purchase of assets

高等教育出版社

7 6.3 Depreciation of Fixed Assets

高等教育出版社

6.3 Depreciation of Fixed Assets

9

Depreciation method

高等教育出版社

10 6.3 Depreciation of Fixed Assets

Method 1: Straight-line

▲ Under the straight-line method, depreciation is the same for each year of the asset’s useful life. It is measured solely by the passage of the time. In order to compute Depreciation Expense, it is necessary to first determine depreciation cost. Depreciation cost is the cost of the asset less its residual value. And then depreciation cost is divided by the asset’s useful life to determine Depreciation Expense.

Definition:▲ Th allocation of a Fixed Asset’s cost to expense over the asset’s useful life is called depreciation. Depreciation accounting matches the asset’s cost (expenses) against the revenue earned by the asset, as the matching principle directs.

高等教育出版社

6.1 Types of Assets

5

高等教育出版社

6 6.2 Fixed Assets

Definition:

▲ Fixed Assets mainly include Land, Land Improvements, Buildings and Equipments. Like the purchase of a home by an individual, the acquisition of Property, Buildings and Equipments is an important decision for a business enterprise.

Measurement:

▲ Fixed assets are recorded at historical cost in accordance with the cost principle of accounting. Cost consists of all expenditures necessary to acquire the asset and make it ready for its intended use. For example, the purchase price, freight costs paid by the purchaser, and installation costs are all considered part of factory machinery.

Unit 6 Long-Lived Assets

1

葛军 吴晓华

高等教育出版社

2

Outline of Unit 6

6.1 Types of Assets 6.2 Fixed Assets 6.3 Depreciation of Fixed Assets 6.4 Disposing of Fixed Assets 6.5 Natural Resources and Intangible Assets

within one year of their acquisition, or within an operating cycle longer than a year, including cash, short-term investments, accounts receivable, prepayments, and inventories. (2) Non-current assets consist of long- term investment and those economic resources that are held for operational purpose, including fixed assets, natural resources and intangible assets, etc.