实用会计英语(第四版) (7)

会计英语(第四版)(完整教资)

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

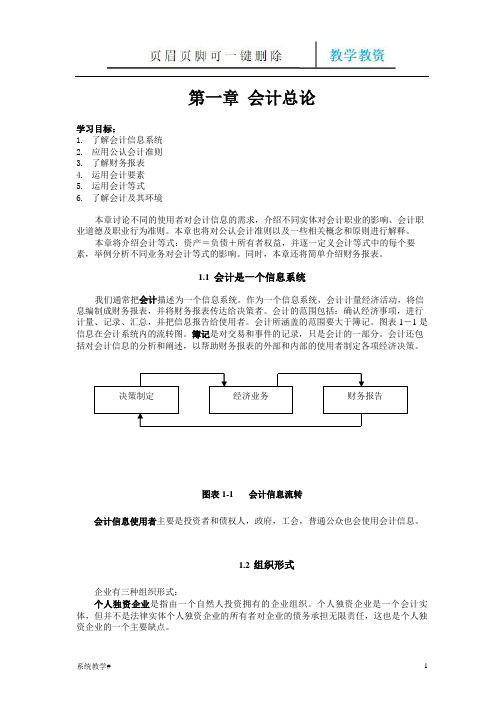

1.1 会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

决策制定经济业务财务报告图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2 组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3 编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

立信《会计专业英语》课件LESSON-SEVEN教学教材

免除,赦免(债务,职责,惩罚等) Remit a tax 免除税款 Remit fees 免费

NEW WORDS,PHRASES AND SPECIAL TERMS

Realty agent 房地产经纪人 Estate agent; Realtor; real estate

此课件下载可自行编辑修改,仅供参考! 感谢您的支持,我们努力做得更好!谢谢

NEW WORDS,PHRASES AND SPECIAL TERMS

Designate:

~sth. (as) sth.命名;指定

This area has been designated (as) a Nation Park.

~sb. (as) sth.指定,选派,委任(某人任某 职)

The director is allowed to designate his successor.

sentences

The party who is to bear transportation costs is designated by the terms “F.O.B. destination ”(seller) and “F.O.B. shipping point” (buyer).

NEW WORDS,PHRASES AND SPECIAL TERMS

Designate

标示,标明

The different types are designated by the letters A,B and C.

NEW WORDS,PHRASES AND SPECIAL T

to a customer.

实用会计英语课件1-18

Operating results of business Profit sharing policy

Make decisions

Whether to increase, or decrease investments

1-20

Present and Potential Creditors

Banks

Owners of the business

Hired managers

1-18

Management

Major function of accounting To provide management with relevant and useful information

Such as: what was the company’s net income during the past year?

1-23

Other Groups

Financial analysts and advisers brokers lawyers economists the financial press

They advise investors and creditors and have an Indirect interest in the financial performance of a business.

well.

Income taxes Social security Payroll taxes Excised taxes

Sales taxes

Tax authorities don’t have direct financial interest in the company, but they usually analyze the tax status undertaken by a business to establish tax policy.

会计英语第四版参考答案

会计英语第四版参考答案Chapter 1: Introduction to Accounting1. What is accounting?- Accounting is the systematic recording, summarizing, and reporting of financial transactions and events of a business entity.2. What are the main functions of accounting?- The main functions of accounting are to providefinancial information for decision-making, ensure compliance with laws and regulations, and facilitate the management of a business.3. What are the two main branches of accounting?- The two main branches of accounting are financial accounting and management accounting.4. What is the purpose of financial accounting?- The purpose of financial accounting is to provide an accurate and fair representation of an entity's financial position and performance to external users.5. What is the double-entry bookkeeping system?- The double-entry bookkeeping system is a method of recording financial transactions in which every transactionis recorded twice, once as a debit and once as a credit, to maintain the equality of the accounting equation.Chapter 2: Accounting Concepts and Principles1. What are the fundamental accounting concepts?- The fundamental accounting concepts include the accrual basis of accounting, going concern, consistency, and materiality.2. What is the accrual basis of accounting?- The accrual basis of accounting records transactions when they occur, regardless of when cash is received or paid.3. What is the going concern assumption?- The going concern assumption is the premise that a business will continue to operate for the foreseeable future.4. What is the principle of consistency?- The principle of consistency requires that an entity should apply accounting policies consistently over time.5. What is the principle of materiality?- The principle of materiality states that only items that could potentially affect the decisions of users of financial statements are included in the financial statements.Chapter 3: The Accounting Equation and Financial Statements1. What is the accounting equation?- The accounting equation is Assets = Liabilities +Owner's Equity.2. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, statement of changes in equity, and cashflow statement.3. What is the purpose of the balance sheet?- The balance sheet provides a snapshot of an entity's financial position at a specific point in time.4. What is the purpose of the income statement?- The income statement reports the revenues, expenses, and net income of an entity over a period of time.5. What is the purpose of the cash flow statement?- The cash flow statement reports the cash inflows and outflows of an entity over a period of time.Chapter 4: Recording Transactions1. What is a journal entry?- A journal entry is the initial recording of atransaction in the general journal.2. What are the steps in the accounting cycle?- The steps in the accounting cycle are analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries.3. What is the difference between a debit and a credit?- A debit is an increase in assets or a decrease inliabilities or equity, while a credit is an increase in liabilities or equity or a decrease in assets.4. What are adjusting entries?- Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are recorded in the correct period.5. What is the purpose of closing entries?- Closing entries are made to transfer the balances of temporary accounts to the owner's equity account and to prepare the accounts for the next accounting period.Chapter 5: Accounting for Merchandising Businesses1. What is a merchandise inventory?- A merchandise inventory is the stock of goods held by a business for sale to customers.2. What is the cost of goods sold?- The cost of goods sold is the direct cost of producing the merchandise sold during an accounting period.3. What is the gross profit?- The gross profit is the difference between the sales revenue and the cost of goods sold.4. What is the difference between a perpetual and a periodic inventory system?- A perpetual inventory system updates inventory records in real-time with each sale or purchase, while a periodicinventory system updates inventory records at specific intervals, such as at the end of an accounting period.5. What is the retail method of inventory pricing?- The retail method of inventory pricing is a method of estimating the cost of ending inventory by applying a cost-to-retail ratio to the retail value of the inventory.Chapter 6: Accounting for Service Businesses1. What are the main differences in accounting for service businesses compared to merchandise businesses?- Service businesses do not have inventory and their primary expenses are typically labor and overhead costs.2. What is the main source of revenue for service businesses? - The main source of revenue for service businesses is the fees charged for the services provided.3. What are the typical expenses。

ppt07 Liabilities 会计英语(第四版) 教学课件

8

Interest Payable Example

What entry would Porter Company make on December 31, the fiscal year-end?

D ate

D es c rip tio n

D eb it

C red it

YE SUN AccountingEnglish

income tax payable of $9,000.

Income

Tax

Statement Return Difference

Revenues Less:

Depreciation Other expenses

$ 1,000,000 $1,000,000 $

-

200,000 650,000

320,000 650,000

payable is recorded in an account called

deferred taxes.

YE SUN AccountingEnglish

15

Deferred Income Taxes Example

Examine the December 31, 1998 information for X-Off Inc.

taxes following tax

law.

YE SUN AccountingEnglish

14

Deferred Income Taxes

GAAP is the set of rules for preparing financial statements.

The tax law is the set of rules for preparing

会计专业英语 Lesson Seven 第七课 课件 教案

• A typical sequence of events • 典型的顺序如 is as follows: 下: • (1)A request for a • (1)当需要购 purchase,called a purchase 买某些商品或 requisition,is initiated by the 者某些存货的 person in charge of 数量低于再定 merchandise stock records 货点时,负责 whenever certain items are 存货记录的人 needed or when quantities of 员可填写请购 certain merchandise fall 单交购货部门。 below established reorder points.The requisition is forwarded to the purchasing department.

• 1月1日 • 销售商品$5000给K· 奥 利森,发票#101,付款 提货,到达站交货,货 到收运费。收到奥利森 的支票计$4800,即已 减去由他代付给承运商 的运费$200后的净额。

• 借:现金 4800 • 销货运费 200 • 贷:销货 5000 • (记入现金收入日记账)

New Words, Phrases and Special Terms

LESSON SEVEN

AN ILLUSTRATION 实例

• We shall list a few • 我们将列举若干 transactions to demonstrate 笔交易来说明它 how they are recorded in 们是怎样记录在 the several journals 第六课所表述的 mentioned in Lesson Six. 那几种日记账中 Pay attention to the credit 的。请注意各笔 terms involved in respective 交易中包含的赊 transactions. Note that cash 账条件。并请注 discounts are calculated on 意:现金折扣是 the billed price of 根据在每笔购货 merchandise retained in a 或销货中留下的 purchase or sale-not on 商品发票价格计 amounts representing 算的,不涉及表 returns and allowances or 示退货、折让或 transportation costs. 运输费用的金额。

_会计英语(B)试题及答案《实用会计英语》(第四版)李海红[5页]

![_会计英语(B)试题及答案《实用会计英语》(第四版)李海红[5页]](https://img.taocdn.com/s3/m/fa39fce890c69ec3d4bb7574.png)

会计英语期末考试题I. Words and terms (20%)1. bankruptcy _________2. financial performance________3. debit ______________4. compound entry__________5. accrual accounting__________6. gross proceeds____________7. marketable securities __________ 8.operating expenses___________9. cash flow______________ 10. store credit_____________11.预付费用________ 12.累计折旧______13.试算平衡________ 14.资产负债表________15.业主提款账户_______ 16.坏账准备账户________17.贴现利息________ 18.会计循环_______19.股息________ 20.日记账___II Fill in the blanks with proper words.(20%)1. Accounting profession is sorted into ____________________, government accounting, management accounting and __________________.2._________________,____________________________,_________________________are the three basic forms of business activities.3.____________________________ is considered as the heart of modern accounting.4. Basically, the T account has three parts: _______________, the debit and ______________.5.Each source document should include at least three parts: the date, the_________________ and ______________________________________.6. After the transactions have been entered in the journal, they must be transferred to the _______________________________ and this process is called ____________.7. The first step of the closing entries is the ________________ accounts are closed by transferring their balances to the ___________________________ account.8. At the beginning of accounting period, the investment cost of marketable securities includes _____________________, taxes, and ________________________ .9. The accounts that can’t be collected are called _____________________________ or ___________________.10. A 60-day, 6%, $4000 note was issued on October 3rd. The note will be due on ________________ and the maturity value of the note is _________________.III. Write T ( true) before the statements which are true and (F) which are false.(5%)1. ( ) The profits and losses in a partnership must be allocated equally by the partners.2. ( ) The total of the debits equals the total of the credits means there is not any error in the process of recording and calculating.3. ( ) The balance of the temporary accounts such as revenue, expense and withdrawals should be zero in preparation for the start of the next accounting period.4. ( ) The collection of the credit sales will increase the balance of Accounts Receivable.5. ( ) The company can discount the promissory note to the bank or other financial units when it needs cash.IV. Match the classifications in Column A with the expression in Column B and write the correct letters on the lines.(15%)Column A Column BCurrent asset a. cash in the safe________________ b. five-year bondsc. lathesd. drillse. accounting system softwareLong –term asset f. cash in bank_______________ g. pencilsh. stationaryi. brand namej. import quotasIntangible asset k. notes receivable______________ l. desksm. motion picture filmn. customer and supplier relationshipo. countersV. Translate the following sentences (15%)1.Bookkeeping is the day-to-day record-keeping involved in the process of accounting.2. The journal records transactions day by day and shows an explanation of each transaction.3. If the prepaid expenses are not adjusted at the end of accounting period, the assets will be exaggerated and the expenses will be understated.4. Income statement is used to track revenues and expenses so that you can determine the operating performance of the business over a period of time.5.While profit is the amount of money you expect to make over a given period of time, cash iswhat you must have to keep your business running.VI. Calculation ( 10% )1.At the beginning of the year , Kevin Young company ‘s assets were 220,000, and its ownersequity was $ 123,000 . During the year, assets increased $60,000, and the liabilities decreased $ 10,000. What was the owner’s equity at the end of the year?2. A sale is made on August 1 for $ 400 ,terms 2/10, n/30, on which a sales return of $ 100 isgranted on August 6 .What is the dollar amount received for payment in full on August 9 ?VII. Make entries (15%)Tom Vega, after receiving his degree in computer science, began his own business called A Star System Company. He completed the following transactions soon after starting the business. Make entries to record these transactions using the following account titles: Cash, Accounts Receivable, Prepaid Rent, Computer Supplies, Minicomputer, System Library, Accounts Payable, Service Revenue, Expense, Tom Vega, Capital and Tom Vega, Withdrawals.1.Tom began his business with a $10,000 cash investment, and a system library, which cost$920.2.Paid two months’ rent for an office. Rent is $360 per month.3.Purchased a minicomputer for $4,500 in cash.4.Purchased computer supplies on credit, $620.5.Collected revenue from a client, $730.6.Billed a client $450 upon completion of a short project.7.Paid expenses of $230.8.Received $450 from the client billed previously.9.Withdrew $210 in cash for personal expense.10.Paid $620 of amount owed in transaction 4.会计英语答案I. Words and terms1. 破产2. 财务业绩3.借方4.复合分录5. 权责发生制会计6.毛利润7.有价证券8.营业费用9.现金流10.赊账11.Prepaid Expense 12. Accumulated Depreciation 13. trial balance 14. balance sheet 15. Withdrawals Account 16. Allowance for Uncollectible Accounts 17. discount 18. accounting cycle 19. dividend 20. journal评分标准:共计20分,每题1分。

会计英语第7章

◦ Both selling expenses and administrative expenses are period

5. Research and Development Costs

◦ Research and development (R&D) are activities undertaken by a firm to create new products, design new processes, improve old products, or to discover valuable new knowledge.

A company must be very careful to use these two words and try not to misuse.

According to the matching principle, once revenues have been recognized in conformity withria for any reporting period, expenses occurred in generating these revenues should also be recognized in the same period.

advertising expenses insurance expenses commission expenses

◦ ……

(3)Administrative Expenses

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

▲ They are classified as either current or long-term. The distinction between the two is based on maturity.

(1) Liabilities which become due and payable within one year from the date of the balance sheet or within the operating cycle are classified as current.

高等教育出版社

7.3 Non-current Liabilities

9

高等教育出版社

10 7.4 Share Capital

▲ Among the most common examples of current liabilities are Accounts Payable, Notes Payable, Short Term Loans, the current portion of LongTerm Debt, accrued liabilities (such as Interest Payable, Income Taxes Payable, and Payroll Liabilities), and Unearned Revenue.

Unit 7 Liabilities and Shareholders’ Equity

1

葛军 吴晓华

高等教育出版社

2

Outline of Unit 7

7.1 Types of Liabilities 7.2 Current Liabilities 7.3 Non-current Liabilities 7.4 Share Capital 7.5 Shareholders’ Equity

▲ Among the most common examples of current liabilities are Accounts Payable, Notes Payable, Short Term Loans, the current portion of LongTerm Debt, accrued liabilities (such as Interest Payable, Income Taxes Payable, and Payroll Liabilities), and Unearned Revenue.

(2) All others are considered to be long-term in nature..

高等教育出版社

7.1 Types of Liabilities

5

高等教育出版社

6 7.2 Current Liabilities

Definition:

▲ The time period used in defining current liabilities parallels that used in defining current assets. A requirement for classification as a current liability is the expectation that the debt will be paid from current assets (or through the rendering of services). A requirement for classification as a current liability is the expectation that the debt will be paid from current assets (or through the rendering of services). Liabilities that do not meet these conditions are classified as long-term liabilities.

高等教育出版社

7.2 Curren.3 Non-current Liabilities

Definition:

▲ Liabilities which become due and payable after one year from the date of the balance sheet or beyond the operating cycle are classified as noncurrent liabilities or long-term liabilities.

高等教育出版社

3 Accounting Equation

高等教育出版社

4 7.1 Types of Liabilities

Definition:

▲ A liability is something which a firm owes to a person or another firm. It may be in the form of creditors - people or firms who have sold you goods which you have not yet paid for, or it may be money borrowed from a financial institution - loans or overdrafts. Liabilities are amounts owed by a business to external parties. Liabilities may be defined as debts or obligations arising from past transactions or events that require settlement at a future date.