chapter2金融工程

金融工程2

案例续

长期资本管理公司以“不同市场证券间不合理价差生灭自 然性”为基础,制定了“通过电脑精密计算,发现不正常 市场价格差,资金杠杆放大,入市图利”的投资策略。 舒尔茨和默顿将金融市场历史交易资料,已有的市场理论、 学术研究报告和市场信息有机结合在一起,形成了一套较 完整的电脑数学自动投资模型。他们利用计算机处理大量 历史数据,通过连续而精密的计算得到两种不同金融工具 间的正常历史价格差,然后结合市场信息分析它们之间的 最新价格差。如果两者出现偏差,并且该偏差正在放大, 电脑立即建立起庞大的债券和衍生工具组合,大举套利入 市投资;经过市场一段时间调节,放大的偏差会自动恢复 到正常轨迹上,此时电脑指令平仓离场,获取偏差的差值。

金融工程

福建师范大学经济学院 张业圳

第一节 金融工程的作用

提供风险管理的工具与技术 投机和套利机会的发掘 公司重组安排与财务配置 避税策略和税务筹划

一、提供风险管理的工具与技术

风险管理在金融工程中居于核心地位。 风险即不确定性 1、用不确定性来代替风险; 2、替换掉与己不利的风险,保留有利风险。 3、分散风险 案例:最初出现于20世纪70年代初的美国住房 抵押贷款市场资产证券化方案的实施

案例:ESL 投资基金收购K-Mart

K-Mart经营不善债务累累﹐二十亿美金的债务 无法偿还﹐导致这个百 年老店被迫进入破产保 护。2003年5月5日是K-Mart可以走出破产法庭 最后期限﹐就在此生死存亡关头﹐当时名不见 经传的康州40岁投资人爱得华兰博(Edward Lampert) 的ESL 投资基金 公司成功地将二十 亿美金的债务折价买下(具体金额是保密的﹐ 业内灵通人士估计在二亿五至五亿之间)﹐然 后投资三亿五定向增发给ESL﹐使得他成为走 出破产后K-Mart公司的69%大股东。

第二章 金融工程基本原理《金融工程》PPT课件

相同,但它们的成本(价格)不同,这时市场存在套利机 会。 ➢ (2)如果存在两个相同成本(价格)的组合,第一个组合 在所有状态下的收益都不低于第二个组合,而且至少存在 一种状态,在此状态下第一个组合的收益大于第二个组合 ,这时市场存在套利机会。 ➢ (3)如果一个组合的构建成本为0,但在所有状态下这个 组合的收益都不小于0,而且至少存在一种状态,在此状态 下这个组合的收益大于0,则市场存在套利机会。

90

无风险资产:

1 1

1

144 108 81

1 1 1

B:

PB

128

PB1 110

PB2

101

16

无套利定价原理的应用

复制策略的确定用倒推法:

(1)在t=0.5时刻:

当PA=120时:144x y 128

x 0.5

108x y 110

y 56

PB1 120 0.5 56 116

当PA=90时:

0 -1个B:-101

合计:

0

1/3A: 27

存款: 74

020

第二节 风险中性定价方法

一、风险中性的概念 ➢ 公平博彩 ➢ 如果一个参加者,他刚好可以接受这样一个统计意

义上的公平博彩,他就是风险中性的 ➢ 风险中性投资者投资于风险证券,不需要风险补偿

,只要收益率等于无风险利率就可以了 ➢ 如果市场上的投资者都是风险中性的,则任何一个

持有证券B空头 持有动态复制策略多头

-1个B:-128 0.5A: 72 存款: 56

卖出B: 110元 买入0.4A:-40元 存款68元:-68 合计: 2

02 金融工程的基本理论

市场交易中的异象

⑴ 交易动机与交易策略——传统金融理论认为,在假设和市场预期均衡状态 下,交易者都会持有一个由市场组合和无风险证券构成的投资组合,其持 有的证券比例取决于交易者的风险承受能力。但统计数据显示,美国纽约 证券交易所市场中一天成交7亿股,投资者的交易行为呈现出“非理性”的 过度交易倾向。 ⑵ 分散不足与随机分散——投资者持有的证券数量很少,显著少于标准的投 资组合理论所推荐的构成分散化投资组合的证券数量,而且投资者在构建 投资组合时采用随机方式选择证券。

2 1 2 1

假设:资产2为无 E ( rp ) = ω1 E ( r1 ) + ( 1-ω1 )rf = rf -ω1 ( E ( r1 )-rf ) 风险资产:

σ p = ω1σ1

ρ≤1

设

r = r1 -tr2

= E[(r1 - r1 ) - t(r2 - r2 )] 2

2 2 = σ1 - 2 tσ 12 + t 2 σ 2 ≥0

1. 有效市场假设的含义 2. 有效市场假设下的投资管理 3. 有效市场理论的检验 4. 与有效市场理论相悖的异象

有效市场假设的含义

1970年,法马采用公平博弈模型来描述有效市场假设,公平博弈模型的假 设条件是:在任一时点,有关某种证券的所有信息都已经充分反映在股票 价格中。模型对信息的处理是非常详尽的,目的是达到“充分反映”的要 求,从而验证了股票价格或收益率序列在统计上不具有“记忆性”,所以 投资者无法根据历史的价格来预测其未来的走势。

金融工程 Financial Engineering

第2章 金融工程的基本理论

1 2 3 4

• 有效市场理论

• 资产组合理论

• 资本资产定价模型 • 因素模型和套利定价模型

金融工程Chapter2

2

金融远期合约(Forward Contracts)是指双方约定在未 来的某一确定时间,按确定的价格买卖一定数量的某种金 融资产的合约。在合约中,未来将买入标的物的一方称为 多方(Long Position),而在未来将卖出标的物的一方称 为空方(Short Position)。

23

❖ 特定期货合约的合约规模、交割日期和交割地点等都 是标准化的,在合约上均有明确规定,无须双方再商 定,价格是期货合约的唯一变量。

❖ 一般来说,常见的标准期货合约条款包括: (1)交易单位。交易所对每个期货产品都规定了统 一的数量和数量单位,统称“交易单位”(Trade Unit)或“合约规模”(Contract Size)。不同交 易所、不同期货品种的交易单位规定各不相同。

17

与远期合约的分类相似,根据标的资产不同, 常见的金融期货主要可分为股票指数期货、外汇期 货和利率期货等。 -股票指数期货是指以特定股票指数为标的资产的期 货合约,S&P500股指期货合约就是典型代表。 -外汇期货则以货币作为标的资产,如美元、德国马 克、法国法郎、英镑、日元、澳元和加元等。 -利率期货是指标的资产价格依赖于利率水平的期货 合约,如欧洲美元期货和长期国债期货等。

Copyright© Zheng Zhenlong & Chen Rong, 2008

8

3.远期股票合约 远期股票合约(Equity Forwards)是指在将来某一特 定日期按特定价格交付一定数量单只股票或一揽子 股票的协议。远期股票合约在世界上出现时间不长, 总交易规模也不大。

Copyright© Zheng Zhenlong & Chen Rong, 2008

金融工程2(金融市场)共36页

缅甸玉石的启示:新信息

在缅甸开采玉石矿的市场上,摆放着各种未 经过任何雕琢的矿石。这些矿石中有可能包 含有大量的翡翠,也可能只有很少一点翡翠。 买卖双方其实都不知道这些矿石中究竟含有 玉多 以 现石便 玉少?请使 石翡得大之 有翠到家露可。新讨出能买信论更含主息:多有可你之有高以是后关成选否,成色择有对色的打必你的翡磨要有信 翠和去好息 ,擦打处, 那拭磨吗一 么玉一?旦 卖石块发 方, 就会相应提高价格,反之降价。从这个例子 中,我们可以得出两点重要的发现:(1) 信 息越多的地方,不确定性就越少,越容易形 成双方都接受的稳定价格。(2) 市场价格的 变动是由新出现的信息推动的,因为新信息 改变了人们对某资产未来价值的预期。

1Leabharlann 0、倚南

窗

以

寄

傲

,

审

容

膝

之

易

安

。

第二章 金融市场 -Financial Market

我们需要了解金融市场的目的

金融市场提供什么样的信息? 如何利用金融市场的信息作正确的决定? 资本性资产定价如何在金融市场上定价? 企业和金融市场之间存在什么关系? 市场对于金融三要素的反应。

课堂讨论—《黑天鹅》作者名言选读

例2-1:第四个和尚买水喝 例2-3:经济大萧条时期为什么会有人销毁高炉? 例2-4:安然公司垄断现货市场为什么还会破产? 例2-5:国家储备局的失误

思考:是什么促成了金融市场价格波动?

有效金融市场假设

什么是有效金融市场呢?

一个简单的定义就是:在一个有效金融市场 上,以当时的市场价格简单地买入或者卖出 一项金融资产,并不能够使投资人实现任何 套利的利润(该定义引自Richard A. Brealey和

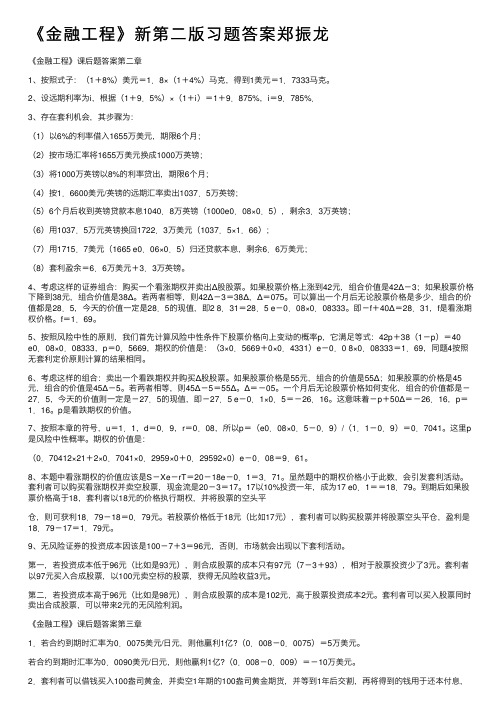

《金融工程》新第二版习题答案郑振龙

《⾦融⼯程》新第⼆版习题答案郑振龙《⾦融⼯程》课后题答案第⼆章1、按照式⼦:(1+8%)美元=1.8×(1+4%)马克,得到1美元=1.7333马克。

2、设远期利率为i,根据(1+9.5%)×(1+i)=1+9.875%,i=9.785%.3、存在套利机会,其步骤为:(1)以6%的利率借⼊1655万美元,期限6个⽉;(2)按市场汇率将1655万美元换成1000万英镑;(3)将1000万英镑以8%的利率贷出,期限6个⽉;(4)按1.6600美元/英镑的远期汇率卖出1037.5万英镑;(5)6个⽉后收到英镑贷款本息1040.8万英镑(1000e0.08×0.5),剩余3.3万英镑;(6)⽤1037.5万元英镑换回1722.3万美元(1037.5×1.66);(7)⽤1715.7美元(1665 e0.06×0.5)归还贷款本息,剩余6.6万美元;(8)套利盈余=6.6万美元+3.3万英镑。

4、考虑这样的证券组合:购买⼀个看涨期权并卖出Δ股股票。

如果股票价格上涨到42元,组合价值是42Δ-3;如果股票价格下降到38元,组合价值是38Δ。

若两者相等,则42Δ-3=38Δ,Δ=075。

可以算出⼀个⽉后⽆论股票价格是多少,组合的价值都是28.5,今天的价值⼀定是28.5的现值,即2 8.31=28.5 e-0.08×0.08333。

即-f+40Δ=28.31,f是看涨期权价格。

f=1.69。

5、按照风险中性的原则,我们⾸先计算风险中性条件下股票价格向上变动的概率p,它满⾜等式:42p+38(1-p)=40e0.08×0.08333,p=0.5669,期权的价值是:(3×0.5669+0×0.4331)e-0.0 8×0.08333=1.69,同题4按照⽆套利定价原则计算的结果相同。

6、考虑这样的组合:卖出⼀个看跌期权并购买Δ股股票。

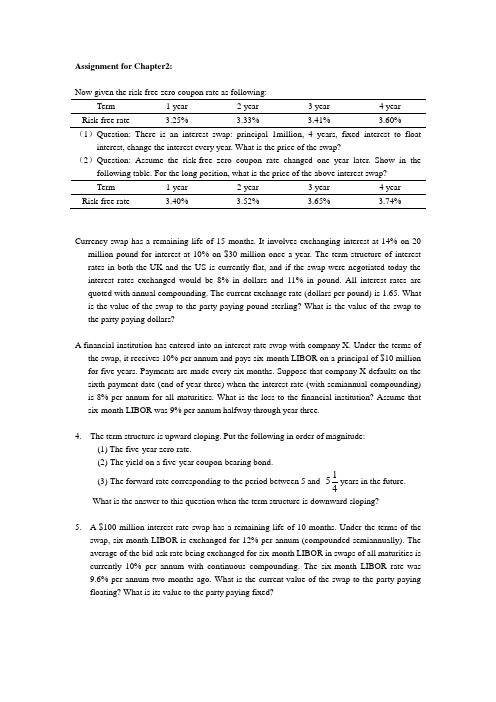

Assignment for Chapter 2宋逢明金融工程习题

Assignment for Chapter2:Now given the risk-free zero coupon rate as following:Term1 year2 year3 year4 year Risk-free rate 3.25% 3.33% 3.41% 3.60%(1)Question: There is an interest swap: principal 1million, 4 years, fixed interest to floatinterest, change the interest every year. What is the price of the swap?(2)Question: Assume the risk-free zero coupon rate changed one year later. Show in the Risk-free rate 3.40% 3.52% 3.65% 3.74%Currency swap has a remaining life of 15 months. It involves exchanging interest at 14% on 20 million pound for interest at 10% on $30 million once a year. The term structure of interest rates in both the UK and the US is currently flat, and if the swap were negotiated today the interest rates exchanged would be 8% in dollars and 11% in pound. All interest rates are quoted with annual compounding. The current exchange rate (dollars per pound) is 1.65. What is the value of the swap to the party paying pound sterling? What is the value of the swap to the party paying dollars?A financial institution has entered into an interest rate swap with company X. Under the terms of the swap, it receives 10% per annum and pays six-month LIBOR on a principal of $10 million for five years. Payments are made every six months. Suppose that company X defaults on the sixth payment date (end of year three) when the interest rate (with semiannual compounding) is 8% per annum for all maturities. What is the loss to the financial institution? Assume that six-month LIBOR was 9% per annum halfway through year three.4. The term structure is upward sloping. Put the following in order of magnitude:(1) The five-year zero rate.(2) The yield on a five-year coupon-bearing bond.(3) The forward rate corresponding to the period between 5 and 415years in the future. What is the answer to this question when the term structure is downward sloping?5. A $100 million interest rate swap has a remaining life of 10 months. Under the terms of theswap, six-month LIBOR is exchanged for 12% per annum (compounded semiannually). The average of the bid-ask rate being exchanged for six-month LIBOR in swaps of all maturities is currently 10% per annum with continuous compounding. The six-month LIBOR rate was9.6% per annum two months ago. What is the current value of the swap to the party paying floating? What is its value to the party paying fixed?。

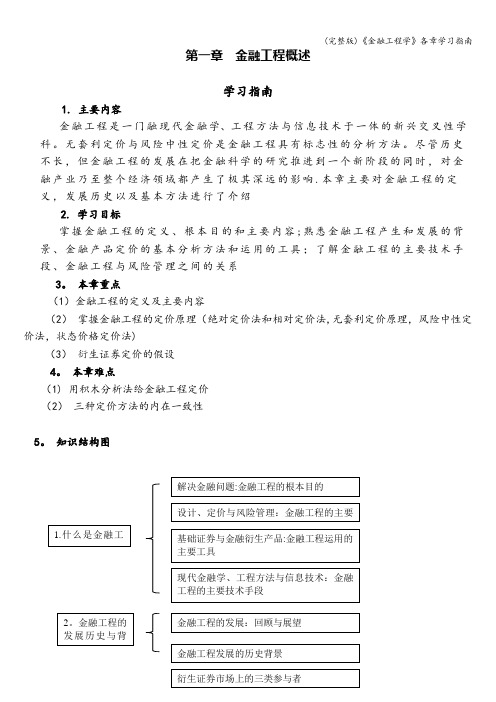

(完整版)《金融工程学》各章学习指南

第一章 金融工程概述学习指南1. 主要内容 金融工程是一门融现代金融学、工程方法与信息技术于一体的新兴交叉性学科。

无套利定价与风险中性定价是金融工程具有标志性的分析方法。

尽管历史不长,但金融工程的发展在把金融科学的研究推进到一个新阶段的同时,对金融产业乃至整个经济领域都产生了极其深远的影响.本章主要对金融工程的定义,发展历史以及基本方法进行了介绍2. 学习目标掌握金融工程的定义、根本目的和主要内容;熟悉金融工程产生和发展的背景、金融产品定价的基本分析方法和运用的工具;了解金融工程的主要技术手段、金融工程与风险管理之间的关系3。

本章重点(1)金融工程的定义及主要内容(2) 掌握金融工程的定价原理(绝对定价法和相对定价法,无套利定价原理,风险中性定价法,状态价格定价法)(3) 衍生证券定价的假设4。

本章难点(1) 用积木分析法给金融工程定价(2) 三种定价方法的内在一致性5。

知识结构图6. 学习安排建议本章是整个课程的概论,介绍了有关金融工程的定义、发展历史和背景、基本原理等内容,是今后本课程学习的基础,希望同学们能多花一些时间理解和学习,为后续的学习打好基础。

● 预习教材第一章内容;● 观看视频讲解;● 阅读文字教材;● 完成学习活动和练习,并检查是否掌握相关知识点,否则重新学习相关内容。

● 了解感兴趣的拓展资源。

第二章 远期与期货概述学习指南 1。

主要内容远期是最基本、最古老的衍生产品。

期货则是远期的标准化.在这一章里,我们将了解远期和期货的基础知识,包括定义、主要类型和市场制度等,最后将讨论两者的异同点2. 学习目标掌握远期、期货合约的定义、主要种类;熟悉远期和期货的区别;了解远期和期货的产生和发展、交易机制3。

本章重点(1) 远期、期货的定义和操作(2) 远期、期货的区别4. 本章难点远期和期货的产生和发展、交易机制5. 知识结构图6. 学习安排建议本章主要对远期和期货的基础知识进行介绍,是之后进行定价、套期保值等操作的基础,建议安排1课时的时间进行学习。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1 ÙThe Time Value of Money!ÀJ K1.A bank must satisfy certain creditworthiness criteria in order to be able to accepta LIBOR quote from another bank and receive deposits from that bank at LIBOR.Typically it must have to have a£¤credit rating.A.AAAB.AAC.AaaD.Aa2.Derivatives traders regard£¤rates as a better indication of the”true”risk-free ratethan Treasury rates.A.LIBORB.NIBORC.HIBORD.SIBOR3.The most common type of repo is an£¤,in which the agreement is renegotiatedeach day.A.everyday repoB.overnight repoC.data repoD.term repo4.The n-year zero-coupon interest rate is sometimes also referred to as the n-year£¤,the n-year£¤,or just the n-year£¤.A.zero rateB.par rateC.spot rateD.zero5.The£¤for a certain bond maturity is the coupon rate that causes the bond priceto equal its par value£The par value is the same as the principal value¤.A.bond yieldB.spot rateC.par yieldD.forward rate6.A largefinancial institution can at no cost lock in the forward rate for a future timeperiod,so the value of the FRA where the forward rate is earned is£¤.A.positiveB.negativeC.zeroD.unknown121 ÙTHE TIME VALUE OF MONEY7.A zero-coupon bond that lasts n years has a duration of n years.However,a coupon-bearing bond lasting n years has a duration of£¤n years,because the holder receives some of the£¤payments prior to year n.A.more thanB.less thanC.interestD.principal8.There is a£¤relationship between bond prices and bond yields.When bond yieldsincrease,bond prices£¤.When bond yields decrease,bond prices£¤.A.positiveB.negativeC.increaseD.decrease9.Theories of the term structure of interest rates mainly include£¤A.expectations theoryB.risk value theoryC.liquidity preference theoryD.market segmentation theory!§äK(3 ( K )ÒS y”√”§ Ø K )ÒS y”×”)1.The higher the credit risk§the higher the interest rate that is promised by theborrower.()2.Treasury rates are regarded as risk-free rates©()3.Derivatives traders do not usually use Treasury rates as risk-free rates,instead theyuse LIBID rates.()4.The limit as the compounding frequency,m,tends to infinity is known as continuouscompounding.For most practical purposes,con tinuous compounding can be thought of as being equivalent to monthly compounding.()5.A largefinancial institution can at no cost lock in the forward rate for a future timeperiod,so the value of the FRA where the forward rate is earned is zero.()6.A zero-coupon bond that lasts n years has a duration of n years.However,a coupon-bearing bond lasting n years has a duration of less than n years,becaus e the holder receives some of the principal payments prior to year n.()7.The bond price is thefinal value of all payments.The duration is therefore a weightedaverage of the times when payments are made,with the weight applied to time t i being equal to the proportion of the bond’s totalfinal value provided by the cash flow at time t i.()38.There is a negative relationship between bond prices and bond yields.When bondyields increase,bond prices decrease.When bond yields decrease,bond prices in-crease.()9.When duration is used for bond portfolios,there is an implicit assumption that theyields of all bonds will change by the same amount.()10.The convexity of a bond portfolio tends to be greatest when the portfolio providespayments evenly over a long period of time.It is least when the payments are concentrated around one particular point in time.()11.By matching convexity as well as duration,a company can make itself immune torelatively large nonparallel shifts in the zero curve.However,it is still exposed to nonparallel/parallel shifts.()n!¶c)º1.LIBOR2.LIBID3.A Repo or Repurchase Agreement4.Repo Rate5.Zero Rates6.Bond Yield7.Forward Interest Rate8.Forward Rate Agreement(FRA)9.Duration10.The Duration of a Bond Portfolioo!O K1.A bank quotes you an interest rate of l4%Per annum with quarterly compound-ing©What is the equivalent rate with(a)continuous compounding and(b)annual compounding?41 ÙTHE TIME VALUE OF MONEY2.What rate of interest with continuous compounding is equivalent to15%per annumwith month1y compounding?3.A deposit account pays l2%per annum with continuous compounding§but interestis actually paid quarterly©How much interest will be paid each quarter on a$10000 deposit?4.Suppose that zero interest rates with continuous compounding are as follows.Calculateforward interest rates for the second,third,fourth,andfifth years.Maturity£years¤Rate£%per annum¤18.027.537.247.05 6.95.Suppose that6-month§12-month§18-month§24-month§and30-month zero ratesare4%§4.2%§4.4%§4.6%§and4.8%per annum with continuous compounding respectively.Estimate the cash price of a bond with a face value of l00that will mature in30months pays a coupon of4%perineum semiannually©6.Suppose that the6-month§12-month§18-month§and24-month zero rates are5%§6%,6.5%,and7%§respectively©What is the two-year par yield?7.Afive-year bond with a yield of11%(continuously compounded)pays an8%couponat the end of each year.a.What is the bond’s price?b.What is the bond’s duration?Ê!ØãK1.Theories of the term structure of interest rates.。