会计学英文版作业

Assignment 会计学基础英文版作业1

Assignment1.What information is presented in a balance sheet?Assets liabilities and equity.2.Why are the personal activities of a business owner excluded from the financial statements of the owner’s business?A financial statementthat reports the assets, liabilities, and equityof an entityat one point in time.3.What’s the significance of money-measurement concept?The money-measurement concept states that accounting reports only those facts that can be stated as monetary amounts.4.Find a piece of news about FASB.Eternal convergenceMay 9th 2012, 17:20 by L.G. | NEW YORKHOW is an investor to compare financial statements from companies in two different countries? That was the question asked a decade ago when the International Accounting Standards Board (IASB) began drawing up a new set of International Financial Reporting Standards. At the same time, the IASB set out to harmonise its standards with America’s Financial Accounting Standards Board (FASB). It even seemed possible that if the two boards got close enough with harmonisation that America might adopt the international standards wholesale.At a conference at Baruch College in New York on May 3rd, grandees from the FASB and the Securities and Exchange Commission (which would make the decision to adopt international standards) explained where the project has got to. A wholesale adoption of the international standards now seems off the table. Instead, the talk is of “endorsement”. The FASB, rather than going out of business or becoming America’s l ocal branch of the IASB, would remain America’s standard-setter, and America’s generally accepted accounting principles (known as US GAAP) would not be replaced by international rules.Instead, the SEC staff envisions that FASB would work with IASB on the drawing up of standards. When IASB came up with a new one, the FASB would issue the same standard itself, only adding modifications when American conditions required it. And only in the rare cases, where the two boards could not agree, would it issue a different standard.The SEC staff expects and hopes that such disagreements should be "rare", and it is hard to disagree with the aspiration at least. Leslie Seidman, FASB's chairwoman, detailed some of the remaining disagreements between the boards at the conference. But this raises several awkward questions. If it is predetermined that differences would be rare, does it really make sense to keep the FASB and US GAAP? If differences are not rare—and worse, if they are not trivial—is the benefit of a single set of standards not lost?Already, many countries that have "adopted" the IASB's standards have added local exceptions to the rules, threatening the project of a single, global set of standards. This headache has been on the mind of Hans Hoogevorst, who took over as chairman IASB last year. In speech after speech he has been reminding smaller countries to fully accept his organisation's rules. Jawboning smaller countries will get much harder if the world’s biggest capital market, America, pointedly insists o n its own tailored version of the standards.American critics of IASB make several points, many to do with fair-value or“mark-to-market” accounting of financial instruments. FASB once wanted all such instruments booked at their market value, whereas IASB favoured an approach that would book most such assets at their historical cost. The difference has largely been narrowed, through the ongoing convergence process. FASB is now considering a “three-bucket” approach which would classify assets in three differ ent ways, depending on the assets’ own characteristics, as well as the business model of the companies using them. (Broadly, those loans being held to term for their income would be booked at historical cost; those meant to be traded would be booked at fair value.)But even as the boards have gotten closer on this point, residual American skepticism remains. Fair-value partisans think that FASB has already gone too far in IASB’s direction, and worry about political influence on the standard-setters. The critics think that European governments have tried to protect their banks by hiding market losses on the balance sheets.The two boards are still working on convergence in three other areas: revenue recognition, insurance and leasing. Impenetrably technical as they may seem, the issues are important. Revenue recognition governs nothing less than when a company can say it has earned a certain chunk of money for a piece of contracted work. Insurance is less contentious, but leasing is giving companies the jitters. Both boards have agreed that they should move more leases (those longer than a year) on to the balance sheet (with the obligation to pay as a liability and the right to use the leased thing as an asset). The sums at stake are big, and could cause some companies to bust loan covenants with banks.By and large, the boards have brought the goal of a single set of standards closer. But the endpoint—truly unified standards that make financial statements around the world comparable—remains distant. Dennis Nally, the boss of PricewaterhouseCoopers, one of the “Big Four” accounting firms, which all support the adoption of global standards, points to several more hurdles. Little sudden movement is expected this year,with a presidential election looming. (Americans in favour of international standards are not keen to look as though they are foisting rules, developed byunelected bureaucrats, on hardworking American business-owners.) Theongoing consequences of the financial crisis have also sharpened opinions all round. And smaller companies who do not do much dealing abroad see the switch to international standards as just another unwelcome cost.So the politics of sovereignty and national pride sometimes seem to be as big a hurdle as technical accounting questions are. American opinions are, of course, due a good deal of deference. Its adoption of international standards would go a long way to getting companies like India, China and Japan on board as well. But if America is unlikely to ever accept IASB’s standards, some grumble, perhaps it should no longer have the biggest say on IASB’s board: four of 14 seats.Clarification: This article originally stated that Leslie Seidman, FASB's chairwoman, said that differences between FASB and IASB "should be 'rare'". We did not mean to say that she expects they will be rare. Indeed, she believes significant differences will remain, though both boards should and will work to narrow them.5. Provide an example of a transaction that creates the described effects:a. Decreases an asset and decreases equity.The cellphone belong to you goes down in value by ¥1000.b. Decreases an asset and decreases a liability.Selling a piece of real estate.c. Decreases a liability and increases a liability.Paying off the debt and assuming the debt.d. Increases an asset and decreases an asset.Buying equipment with cash.e. Increases an asset and increases a liability.Buying equipment on credit.f Increases an asset and increases equity.Buying computer equipment for one’s office.g. Decreases a liability and increases equity.Using someone’s loan invest one’s company.。

会计学英文版作业

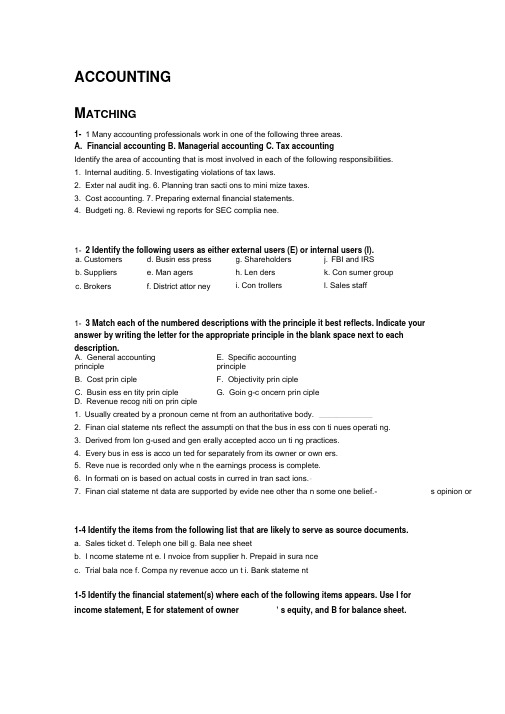

ACCOUNTINGM ATCHING1- 1 Many accounting professionals work in one of the following three areas.A. Financial accountingB. Managerial accountingC. Tax accountingIdentify the area of accounting that is most involved in each of the following responsibilities.1. Internal auditing. 5. Investigating violations of tax laws.2. Exter nal audit ing. 6. Planning tran sacti ons to mini mize taxes.3. Cost accounting. 7. Preparing external financial statements.4. Budgeti ng. 8. Reviewi ng reports for SEC complia nee.1- 2 Identify the following users as either external users (E) or internal users (I).1- 3 Match each of the numbered descriptions with the principle it best reflects. Indicate youranswer by writing the letter for the appropriate principle in the blank space next to eachdescription.A. General accounting principleB. Cost prin cipleC. Busin ess en tity prin ciple E. Specific accountingprincipleF. Objectivity prin cipleG. Goin g-c oncern prin cipleD. Revenue recog niti on prin ciple1. Usually created by a pronoun ceme nt from an authoritative body. ____________2. Finan cial stateme nts reflect the assumpti on that the bus in ess con ti nues operati ng.3. Derived from Ion g-used and gen erally accepted acco un ti ng practices.4. Every bus in ess is acco un ted for separately from its owner or own ers.5. Reve nue is recorded only whe n the earnings process is complete.6. In formati on is based on actual costs in curred in tran sact ions.-7. Finan cial stateme nt data are supported by evide nee other tha n some one belief.-1-4 Identify the items from the following list that are likely to serve as source documents.a. Sales ticket d. Teleph one bill g. Bala nee sheetb. I ncome stateme nt e. I nvoice from supplier h. Prepaid in sura ncec. Trial bala nce f. Compa ny revenue acco un t i. Bank stateme nt1-5 Identify the financial statement(s) where each of the following items appears. Use I forincome statement, E for statement of owner ' s equity, and B for balance sheet.a. Customersb. Suppliersc. Brokersd. Busin ess presse. Man agersf. District attor neyg. Shareholdersh. Len dersi. Con trollersj. FBI and IRSk. Con sumer groupl. Sales staffs opinion or1-6 The following are common categories on a classified balance sheet.A. Current assetsD. Intan gible assets B. Lon g-term in vestme ntsE. Current liabilities C. Plant assetsF. Lon g-term liabilities For each of the following items, select the letter that identifies the balance sheet category where theitem typically would appear._____ 1. Land not curre ntly used in operati ons _____ 5. Acco unts payable_____ 2. Notes payable (due in three years) ______ 6. Store equipme nt_____ 3. Acco unts receivable _____ 7. Wages payable_____ 4. Trademarks ______ 8. Cash 1-7 In the blank space beside each numbered balance sheet item, enter the letter of itsbalance sheet classification. If the item should not appear on the balance sheet, enter a Z inthe blank.1-8 In the blank space beside each numbered balance sheet item, enter the letter of itsbalance sheet classfication. If the item should not appear on the balance sheet, enter a Z inthe blank.A. Current assets E. Curren t liabilitiesB. Long-term investments F. Long-term liabilitiesC. Pla nt assets G. EquityD. Intan gible assets_____ 1. Commissi ons earned______ 11. Rent receivable _____ 2. In terest receivable ______ 12. Salaries payable_____ 3. Lon g-term in vestme nt in stock ________ 13. I ncome taxes payablea. Cash withdrawal by ownerb. Office equipme ntc. Acco unts payabled. Cashe. Utilities expe nsesf. Office suppliesg. Prepaid renth. Unearned feesi. Service fees earnedA. Current assetsD. Intan gible assetsB. Lon g-term in vestme nts E. Curre nt liabilitiesC. Plant assets_____ 1. Lon g-term in vestme nt in stock_____ 2. Depreciatio n expe nse — Buildi ng_____ 3. Prepaid rent_____ 4. I nterest receivable_____ 5. Taxes payable_____ 6. Automobiles_____ 7. Notes payable (due in 3 years)_____ 8. Acco unts payable ___ 9. Prepaid in sura nce 10. Owner,Capital 11. Unearned services revenueF. Lon g-term liabilitiesG. Equity _____ 12. Accumulated depreciatio n — Trucks _____ 13. Cash _____ 14. Build ings _____ 15. Store supplies _____ 16. Office equipme nt _____ 17. Land (used in operatio ns) __ 18. Repairs expe nse __ 19. Office supplies__ 20. Current portion of Ion g-term note payable_____ 4. Prepaid in sura nee _____ 14. Owner, Capital_____ 5. Machi nery _____ 15. Office supplies_____ 6. Notes payable (due in 15 years) ________ 16. In terest payable_____ 7. Copyrights ______ 17. Rent revenue_____ 8. Current porti on of Ion g-term note payable _____ 18. Notes receivable (due in 120 days) _____ 9. Accumulated depreciati on — Trucks ________ 19. Land (used in operatio ns)_____ 10. Office equipme nt ______ 20. Depreciati on expe nse —TrucksEASSAY QUESTION2- 1 What is the purpose of accounting in society?2- 2 Ide ntify the four basic finan cial stateme nts of a bus in ess.2- 3 What in formati on is reported in an in come stateme nt?2-4 What in formati on is reported in a bala nee sheet?2-5 Discuss the steps in process ing bus in ess tran sact ions.2-6 What is a company ' s operating cycle?2-7 Why is the accrual basis of acco unting gen erally preferred over the cash basis?3- 1 Prepare journal entries for each of the following selected transactions.a. On January 13, DeShaw n Tyler ope ns a Ian dscap ing bus in ess called Elega nt Law ns by in vest ing $70,000 cash along with equipment having a $30,000 value.b. On January 21, Elega nt Law ns purchases office supplies on credit for $280.c. On Jan uary 29, Elega nt Law ns receives $7,800 cash for perform ing Ian dscap ing services.d. On January 30, Elega nt Law ns receives $1,000 cash in adva nee of providi ng Ian dscap ing services to a customer.3- 2 The adjusted trial bala nee for Chiara Compa ny as of December 31,2008, follows.Debit CreditCash ................................................................... $ 30,000Acco unts receivable ........................................... 52,000In terest receivable ............................................... 18,000Notes receivable (due in 90 days) .......................... 168,000Office supplies ..................................................... 16,000Automobiles ........................................................ 168,000Accumulated depreciatio n —Automobiles ........... $ 50,000Equipme nt ........................................................ 138,000Accumulated depreciatio n —Equipme nt ............... 18,000Land .................................................................... 78,000Acco unts payable ............................................... 96,000In terest payable ................................................. 20,000Salaries payable .................................................. 19,000Unearned fees .................................................... 30,000Lon g-term no tes payable ................................ 138,000R.Chiara,Capital ................................................ 255,800R.Chiara,Withdrawals ............................. 46,000Fees earned ........................................................ 484,000In terest earned ................................................... 24,000Depreciati on expe nse—Automobiles ............... 26,000Depreciati on expe nse—Equipme nt ................. 18,000Salaries expe nse ............................................... 188,000Wages expe nse ................................................. 40,000In terest expe nse ............................................... 32,000Office supplies expe nse ..................................... 34,000Advertis ing expe nse .......................................... 58,000Repairs expe nse— Automobiles ........................ 24,800Totals ................................................................ $1,134,800 $1,134,800Required1. Use the in formati on in the adjusted trial bala nce to prepare (a) the in come stateme nt for the year ended December 31,2008; (b) the statement of owner' equity for the year ended December 31,2008;a nd (c) the bala ncesheet as of December 31,2008.2. Calculate the profit margin for year 2008.3- 3 On April 1,2008, Jiro Nozomi created a new travelagency, Adventure Travel. The following tran sact ions occurred duri ng the compa ny ' s first mon th..April 1 Nozomi in vested $30,000 cash and computer equipme nt worth $20,000 in the bus in ess.s (April) rei2 Ren ted furni shed office space by pay ing $1,800 cash for the first month3 Purchased $1,000 of office supplies for cash.10 Paid $2,400 cash for the premium on a 12-m onth in sura nce policy. Coverage beg ins onApril 11.14 Paid $1,600 cash for two weeks ' salaries earned by employees.24 Collected $8,000 cash on commissi ons from airli nes on tickets obta ined for customers.28 Paid another $1,600 cash for two weeks ' salaries earned by employees.29 Paid $350 cash for minor rep airs to the company ' s computer.30 Paid $750 cash for this mon th ' s telepho ne bill.30 Nozomi withdrew $1,500 cash for pers onal use.The company ' s chart of accounts follows:101 Cash 405 Commissi ons Earned106 Acco unts Receivable 612 Depreciati on Expe nse —Computer Equip.124 Office Supplies 622 Salaries Expe nse128 Prepaid In sura nee 637 In sura nee Expe nse167 Computer Equipme nt 640 Rent Expe nse168 Accumulated Depreciati on —Computer Equip. 650 Office Supplies Expe nse209 Salaries Payable 684 Repairs Expe nse301 J.Nozomi,Capital 688 Telepho ne Expe nse302 J.Nozomi,Withdrawals 901 In come SummaryRequired:1. Use the bala nee colu mn format to set up each ledger acco unt listed in its chart of acco un ts.2. Prepare journal entries to record the transactions for April and post them to the ledger accounts.The compa ny records prepaid and unearned items in bala nee sheet acco un ts.3. Prepare an unadjusted trial balance as of April 30.4. Use the follow ing in formati on to journ alize and post adjusti ng en tries for the mon th:a. Two-thirds of one mon th ' s in sura nce coverage has expired.b. At the end of the mon th, $600 of office supplies are still available.c. This month ' s depreciation on the computer equipme$500.d. Employees earned $420 of un paid and un recorded salaries as of mon th-e nd.e. The compa ny earned $1,750 of commissi ons that are not yet billed at mon th-e nd.5. Prepare the in come stateme nt and the stateme nt of owner ' s equity for the mdnth of April a the balance sheet at April 30, 2008.6. Prepare journal en tries to close the temporary acco unts .7. Prepare a post-clos ing trial bala nce.。

会计英语练习题

会计英语练习题会计英语练习题在全球化的今天,学习外语已经成为了必不可少的技能。

对于会计专业的学生来说,掌握会计英语更是至关重要。

会计英语是会计学中的一门专业英语,它涵盖了会计的各个方面,包括财务报表、成本管理、税务等。

为了帮助大家更好地掌握会计英语,下面将提供一些练习题,希望能对大家的学习有所帮助。

1. What is the English term for "资产负债表"?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Statement of Retained Earnings2. Which of the following is not an expense?A. RentB. SalaryC. Accounts ReceivableD. Utilities3. What is the English term for "总账"?A. General LedgerB. Trial BalanceC. Income StatementD. Cash Flow Statement4. What is the English term for "应收账款"?A. Accounts PayableB. Accounts ReceivableC. InventoryD. Prepaid Expenses5. What is the English term for "固定资产"?A. Current AssetsB. Fixed AssetsC. Intangible AssetsD. Accounts Payable6. What is the English term for "净利润"?A. Gross ProfitB. Operating IncomeC. Net IncomeD. Retained Earnings7. What is the English term for "应付账款"?A. Accounts PayableB. Accounts ReceivableC. Accrued ExpensesD. Prepaid Expenses8. What is the English term for "现金流量表"?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Statement of Retained Earnings9. What is the English term for "财务报表分析"?A. Financial Statement AnalysisB. Cost AccountingC. TaxationD. Budgeting10. What is the English term for "税务"?A. Financial Statement AnalysisB. Cost AccountingC. TaxationD. Budgeting以上是一些关于会计英语的练习题,希望大家能够认真思考并给出正确答案。

会计学基础学习知识原理英文版一单元习题集

1. Accounting is an information and measurement system that identifies, records, and communicates relevant, reliable, and comparable information about an organization's business activities.2. Bookkeeping is the recording of transactions and events and is only part of accounting.3. An accounting information system communicates data to help businesses make better decisions.4. Managerial accounting is the area of accounting that provides internal reports to assist the decision making needs of internal users.5. Internal operating activities include research and development, distribution, and human resources.6. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze and interpret an organization's activities.7. External auditors examine financial statements to verify that they are prepared according to generally accepted accounting principles.8. External users include lenders, shareholders, customers, and regulators.9. Regulators often have legal authority over certain activities of organizations.10. Internal users include lenders, shareholders, brokers and managers.11. Opportunities in accounting include auditing, consulting, market research, and tax planning.12. Identifying the proper ethical path is easy.13. The Sarbanes-Oxley Act (SOX) requires each issuer of securities to disclose whether is has adopted a code of ethics for its senior financial officers and the contents of that code.14. The fraud triangle asserts that there are three factors that must exist for a person to commit fraud; these factors are opportunity, pressure, and rationalization.15. The Sarbanes-Oxley Act (SOX) does not require public companies to apply both accounting oversight and stringent internal controls.16. A partnership is a business owned by two or more people.17. Owners of a corporation are called shareholders or stockholders.18. In the partnership form of business, the owners are called stockholders.19. The balance sheet shows a company’s net income or loss due to earnings activities over a period of time.20. The Financial Accounting Standards Board is the private group that sets both broad and specific accounting principles.21. The business entity principle means that a business will continue operating for an indefinite period of time.22. Generally accepted accounting principles are the basic assumptions, concepts, and guidelines for preparing financial statements.23. The business entity assumption means that a business is accounted for separately from other business entities, including its owner or owners.24. As a general rule, revenues should not be recognized in the accounting records until it is received in cash.25. Specific accounting principles are basic assumptions, concepts, and guidelines for preparing financial statements and arise out of long-used accounting practice.26. General accounting principles arise from long-used accounting practices.27. A sole proprietorship is a business owned by one or more persons.28. Unlimited liability is an advantage of a sole proprietorship.29. Understanding generally accepted accounting principles is not necessary to use and interpret financial statements.30. The International Accounting Standards board (IASB) has the authority to impose its standards on companies around the world.31. Objectivity means that financial information is supported by independent unbiased evidence.32. The idea that a business will continue to operate instead of being closed or sold underlies the going-concern assumption.33. According to the cost principle, it is preferable for managers to report an estimate of an asset's value.34. The monetary unit assumption means that all international transactions must be expressed in dollars.35. The International Accounting Standards Board (IASB) is the government group that establishes reporting requirements for companies that issue stock to the public. 36. A limited liability company offers the limited liability of a partnership or proprietorship and the tax treatment of a corporation.37. The Securities and Exchange Commission (SEC) is a government agency that has legal authority to establish GAAP.38. The three common forms of business ownership include sole proprietorship, partnership, and non-profit.39. The three major types of business activities are operating, financing, and investing.40. Planning is defining an organization's ideas, goals, and actions.41. Strategic management is the process of determining the right mix of operating activities for the type of organization, its plans, and its markets.42. Planning activities are the means an organization uses to pay for resources like land, buildings, and equipment to carry out its plans.43. Investing activities are the acquiring and disposing of resources that an organization uses to acquire and sell its products or services.44. Owner financing refers to resources contributed by creditors or lenders.45. Revenues are increases in equity from a company's earning activities.46. A net loss occurs when revenues exceed expenses.47. Net income occurs when revenues exceed expenses.48. Liabilities are the owner's claim on assets.49. Assets are the resources of a company and are expected to yield future benefits.50. Owner’s withdrawals are expenses.51. The accounting equation can be restated as: Assets - Equity = Liabilities.52. The accounting equation implies that: Assets + Liabilities = Equity.53. Owner's investments are increases in equity from a company's earnings activities.54. Every business transaction leaves the accounting equation in balance.55. An external transaction is an exchange of value within an organization.56. From an accounting perspective, an event is a happening that affects the accounting equation, but cannot be measured.57. Owner's equity is increased when cash is received from customers in payment of previously recorded accounts receivable.58. An owner's investment in a business always creates an asset (cash), a liability (note payable), and owner's equity (investment.)59. Return on assets is often stated in ratio form as the amount of average total assets divided by income.60. Return on assets is also known as return on investment.61. Return on assets is useful to decision makers for evaluating management, analyzing and forecasting profits, and in planning activities.62.Arrow’s net income of $117 million and average assets of $1,400 million results in a return on assets of 8.36%.63. Return on assets reflects the effectiveness of a company’s ability to generate profit through productive use of its assets.64. Risk is the uncertainty about the return we expect to earn.65. Generally the lower the risk, the lower the return that can be expected.66. U. S. Government Treasury bonds provide high return and low risk to investors.67. The four basic financial statements include the balance sheet, income statement, statement of owner's equity, and statement of cash flows.68. An income statement reports on investing and financing activities.69. A balance sheet covers a period of time such as a month or year.70. The income statement displays revenues earned and expenses incurred over a specified period of time due to earnings activities.71. The statement of cash flows shows the net effect of revenues and expenses for a reporting period.72. The income statement shows the financial position of a business on a specific date.73. The first section of the income statement reports cash flows from operating activities.74. The balance sheet is based on the accounting equation.75. Investing activities involve the buying and selling of assets such as land and equipment that are held for long-term use in the business.76. Operating activities include long-term borrowing and repaying cash from lenders, and cash investments or withdrawals by the owner.77. The purchase of supplies appears on the statement of cash flows as an investing activity because it involves the purchase of assets.78. The income statement reports on operating activities at a point in time.79. The statement of cash flows identifies cash flows separated into operating, investing, and financing activities over a period of time.80. Ending capital reported on the statement of owner’s equity is calculated by adding owner investments and net losses and subtracting net incomes and withdrawals. Multiple Choice Questions81. Accounting is an information and measurement system that does all of the following except:A. Identifies business activities.B. Records business activities.C. Communicates business activities.D. Does not use technology to improve accuracy in reporting.E. Helps people make better decisions.82. Technology:A. Has replaced accounting.B. Has not changed the work that accountants do.C. Has closely linked accounting with consulting, planning, and other financial services.D. In accounting has replaced the need for decision makers.E. In accounting is only available to large corporations.83.The primary objective of financial accounting is:A. To serve the decision-making needs of internal users.B. To provide financial statements to help external users analyze an organization's activities.C. To monitor and control company activities.D. To provide information on both the costs and benefits of looking after products and services.E. To know what, when, and how much to produce.84.The area of accounting aimed at serving the decision making needs of internal users is:A. Financial accounting.B. Managerial accounting.C. External auditing.D. SEC reporting.E. Bookkeeping.85.External users of accounting information include all of the following except:A. Shareholders.B. Customers.C. Purchasing managers.D. Government regulators.E. Creditors.86. All of the following regarding a Certified Public Accountant are true except:A. Must meet education and experience requirements.B. Must pass an examination.C. Must exhibit ethical character.D. May also be a Certified Management Accountant.E. Cannot hold any certificate other than a CPA.87. Ethical behavior requires:A. That auditors' pay not depend on the success of the client's business.B. Auditors to invest in businesses they audit.C. Analysts to report information favorable to their companies.D. Managers to use accounting information to benefit themselves.E. That auditors' pay depend on the success of the client's business.88. Social responsibility:A. Is a concern for the impact of our actions on society.B. Is a code that helps in dealing with confidential information.C. Is required by the SEC.D. Requires that all businesses conduct social audits.E. Is limited to large companies.89. All of the following are true regarding ethics except:A. Ethics are beliefs that separate right from wrong.B. Ethics rules are often set for CPAs.C. Ethics do not affect the operations or outcome of a company.D. Are critical in accounting.E. Ethics can be hard to apply.90. The accounting concept that requires financial statement information to be supported by independent, unbiased evidence other than someone's belief or opinion is:A. Business entity assumption.B. Monetary unit assumption.C. Going-concern assumption.D. Time-period assumption.E. Objectivity91. A corporation:A. Is a business legally separate from its owners.B. Is controlled by the FASB.C. Has shareholders who have unlimited liability for the acts of the corporation.D. Is the same as a limited liability partnership.E. Is not subject to double taxation.92. The group that attempts to create more harmony among the accounting practices of different countries is the:A. AICPA.B. IASB.C. CAP.D. SEC.E. FASB.93. The private group that currently has the authority to establish generally accepted accounting principles in the United States is the:A. APB.B. FASB.C. AAA.D. AICPA.E. SEC.94. The accounting assumption that requires every business to be accounted for separately from other business entities, including its owner or owners is known as the:A. Time-period assumption.B. Business entity assumption.C. Going-concern assumption.D. Revenue recognition principle.E. Cost principle.95. The rule that requires financial statements to reflect the assumption that the business will continue operating instead of being closed or sold, unless evidence shows that it will not continue, is the:A. Going-concern assumption.B. Business entity assumption.C. Objectivity principle.D. Cost Principle.E. Monetary unit assumption.96. If a parcel of land that was originally acquired for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land should be recorded in the purchaser's books at:A. $95,000.B. $137,000.C. $138,500.D. $140,000.E. $150,000.97. To include the personal assets and transactions of a business's owner in the records and reports of the business would be in conflict with the:A. Objectivity principle.B. Monetary unit assumption.C. Business entity assumption.D. Going-concern assumption.E. Revenue recognition principle.98. The accounting principle that requires accounting information to be based on actual cost and requires assets and services to be recorded initially at the cash orcash-equivalent amount given in exchange, is the:A. Accounting equation.B. Cost principle.C. Going-concern assumption.D. Realization principle.E. Business entity assumption.99. The rule that (1) requires revenue to be recognized at the time it is earned, (2) allows the inflow of assets associated with revenue to be in a form other than cash, and (3) measures the amount of revenue as the cash plus the cash equivalent value of any noncash assets received from customers in exchange for goods or services, is called the:A. Going-concern assumption.B. Cost principle.C. Revenue recognition principle.D. Objectivity principle.E. Business entity assumption.100. The question of when revenue should be recognized on the income statement (according to GAAP) is addressed by the:A. Revenue recognition principle.B. Going-concern assumption.C. Objectivity principle.D. Business entity assumption.E. Cost principle.101. The International Accounting Standards Board (IASB):A. Hopes to create harmony among accounting practices of different countries.B. Is the government group that establishes reporting requirements for companies that issue stock to the public.C. Has the authority to impose its standards on companies.D. Is the only source of generally accepted accounting principles (GAAP).E. Only applies to companies that are members of the European Union.102. The Maxim Company acquired a building for $500,000. Maxim had the building appraised, and found that the building was easily worth $575,000. The seller had paid $300,000 for the building 6 years ago. Which accounting principle would require Maxim to record the building on its records at $500,000?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Revenue recognition principle.103. On December 15 of the current year, Myers Legal Services signed a $50,000 contract with a client to provide legal services to the client in the following year. Which accounting principle would require Myers Legal Services to record the legal fees revenue in the following year and not the year the cash was received?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Revenue recognition principle.104. Marian Mosely is the owner of Mosely Accounting Services. Which accounting principle requires Marian to keep her personal financial information separate from the financial information of Mosely Accounting Services?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Matching principle.105. A limited partnership:A. Includes a general partner with unlimited liability.B. Is subject to double taxation.C. Has owners called stockholders.D. Is the same as a corporation.E. May only have two partners.106. A partnership:A. Is also called a sole proprietorship.B. Has unlimited liability for its partners.C. Has to have a written agreement in order to be legal.D. Is a legal organization separate from its owners.E. Has owners called shareholders.107. Which of the following accounting principles would require that all goods and services purchased be recorded at cost?A. Going-concern assumption.B. Matching principle.C. Cost principle.D. Business entity assumption.E. Consideration assumption.108. Which of the following accounting principles prescribes that a company record its expenses incurred to generate the revenue reported?A. Going-concern assumption.B. Matching principle.C. Cost principle.D. Business entity assumption.E. Consideration assumption.109. Revenue is properly recognized:A. When the customer's order is received.B. Only if the transaction creates an account receivable.C. At the end of the accounting period.D. Upon completion of the sale or when services have been performed and the business obtains the right to collect the sales price.E. When cash from a sale is received.110. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land account transaction amount to handle the sale of the land in the seller's books is:A. $85,000 increase.B. $85,000 decrease.C. $137,000 increase.D. $137,000 decrease.E. $140,000 decrease.111. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. What is the effect of the sale on the accounting equation for the seller?A. Assets increase $52,000; owner's equity increases $52,000.B. Assets increase $85,000; owner's equity increases $85,000.C. Assets increase $137,000; owner's equity increases $137,000.D. Assets increase $140,000; owner's equity increases $140,000.E. Assets decrease $85,000; owner's equity decreases $85,000.112. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. At the time of the sale, assume that the seller still owed $30,000 to TrustOne Bank on the land that was purchased for $85,000. Immediately after the sale, the seller paid off the loan to TrustOne Bank. What is the effect of the sale and the payoff of the loan on the accounting equation?A. Assets increase $52,000; owner's equity increases $22,000; liabilities decrease $30,000B. Assets increase $52,000; owner's equity increases $30,000; liabilities decrease $30,000C. Assets increase $22,000; owner's equity increases $52,000; liabilities decrease $30,000D. Assets decrease $30,000; owner's equity decreases $30,000; liabilities decrease $30,000E. Assets decrease $55,000; owner's equity decreases $55,000; liabilities decrease $30,000113. An example of a financing activity is:A. Buying office supplies.B. Obtaining a long-term loan.C. Buying office equipment.D. Selling inventory.E. Buying land.114. An example of an operating activity is:A. Paying wages.B. Purchasing office equipment.C. Borrowing money from a bank.D. Selling stock.E. Paying off a loan.115. Operating activities:A. Are the means organizations use to pay for resources like land, buildings and equipment.B. Involve using resources to research, develop, purchase, produce, distribute and market products and services.C. Involve acquiring and disposing of resources that a business uses to acquire and sell its products or services.D. Are also called asset management.E. Are also called strategic management.116. An example of an investing activity is:A. Paying wages of employees.B. Withdrawals by the owner.C. Purchase of land.D. Selling inventory.E. Contribution from owner.117. Net Income:A. Decreases equity.B. Represents the amount of assets owners put into a business.C. Equals assets minus liabilities.D. Is the excess of revenues over expenses.E. Represents owners' claims against assets.118. If equity is $300,000 and liabilities are $192,000, then assets equal:A. $108,000.B. $192,000.C. $300,000.D. $492,000.E. $792,000.119. Resources that are expected to yield future benefits are:A. Assets.B. Revenues.C. Liabilities.D. Owner's Equity.E. Expenses.120. Increases in equity from a company's earnings activities are:A. Assets.B. Revenues.C. Liabilities.D. Owner's Equity.E. Expenses.121. The difference between a company's assets and its liabilities, or net assets is:A. Net income.B. Expense.C. Equity.D. Revenue.E. Net loss.122. Creditors' claims on the assets of a company are called:A. Net losses.B. Expenses.C. Revenues.D. Equity.E. Liabilities.123. Decreases in equity that represent costs of assets or services used to earn revenues are called:A. Liabilities.B. Equity.C. Withdrawals.D. Expenses.E. Owner's Investment.124. The description of the relation between a company's assets, liabilities, and equity, which is expressed as Assets = Liabilities + Equity, is known as the:A. Income statement equation.B. Accounting equation.C. Business equation.D. Return on equity ratio.E. Net income.125. Revenues are:A. The same as net income.B. The excess of expenses over assets.C. Resources owned or controlled by a companyD. The increase in equity from a company’s earning activities.E. The costs of assets or services used.126. If assets are $99,000 and liabilities are $32,000, then equity equals:A. $32,000.B. $67,000.C. $99,000.D. $131,000.E. $198,000.127. Another name for equity is:A. Net income.B. Expenses.C. Net assets.D. Revenue.E. Net loss.128. The excess of expenses over revenues for a period is:A. Net assets.B. Equity.C. Net loss.D. Net income.E. A liability.129. A payment to an owner is called a(n):A. Liability.B. Withdrawal.C. Expense.D. Contribution.E. Investment.130. Distributions of assets by a business to its owners are called:A. Withdrawals.B. Expenses.C. Assets.D. Retained earnings.E. Net Income.131. The assets of a company total $700,000; the liabilities, $200,000. What are the claims of the owners?A. $900,000.B. $700,000.C. $500,000.D. $200,000.E. It is impossible to determine unless the amount of this owners' investment is known.132. On June 30 of the current year, the assets and liabilities of Phoenix, Inc. are as follows: Cash $20,500; Accounts Receivable, $7,250; Supplies, $650; Equipment, $12,000; Accounts Payable, $9,300. What is the amount of owner's equity as of June 30 of the current year?A. $8,300B. $13,050C. $20,500D. $31,100E. $40,400133. Assets created by selling goods and services on credit are:A. Accounts payable.B. Accounts receivable.C. Liabilities.D. Expenses.E. Equity.134. An exchange of value between two entities is called:A. The accounting equation.B. Recordkeeping or bookkeeping.C. An external transaction.D. An asset.E. Net Income.135. Photometer Company paid off $30,000 of its accounts payable in cash. What would be the effects of this transaction on the accounting equation?A. Assets, $30,000 increase; liabilities, no effect; equity, $30,000 increase.B. Assets, $30,000 decrease; liabilities, $30,000 decrease; equity, no effect.C. Assets, $30,000 decrease; liabilities, $30,000 increase; equity, no effect.D. Assets, no effect; liabilities, $30,000 decrease; equity, $30,000 increase.E. Assets, $30,000 decrease; liabilities, no effect; equity $30,000 decrease.136. How would the accounting equation of Boston Company be affected by the billing of a client for $10,000 of consulting work completed?A. +$10,000 accounts receivable, -$10,000 accounts payable.B. +$10,000 accounts receivable, +$10,000 accounts payable.C. +$10,000 accounts receivable, +$10,000 cash.D. +$10,000 accounts receivable, +$10,000 revenue.E. +$10,000 accounts receivable, -$10,000 revenue.137. Zion Company has assets of $600,000, liabilities of $250,000, and equity of $350,000. It buys office equipment on credit for $75,000. What would be the effects of this transaction on the accounting equation?A. Assets increase by $75,000 and expenses increase by $75,000.B. Assets increase by $75,000 and expenses decrease by $75,000.C. Liabilities increase by $75,000 and expenses decrease by $75,000.D. Assets decrease by $75,000 and expenses decrease by $75,000.E. Assets increase by $75,000 and liabilities increase by $75,000.138. Viscount Company collected $42,000 cash on its accounts receivable. The effects of this transaction as reflected in the accounting equation are:A. Total assets decrease and equity increases.B. Both total assets and total liabilities decrease.C. Total assets, total liabilities, and equity are unchanged.D. Both total assets and equity are unchanged and liabilities increase.E. Total assets increase and equity decreases.139. If the liabilities of a business increased $75,000 during a period of time and the owner's equity in the business decreased $30,000 during the same period, the assets of the business must have:A. Decreased $105,000.B. Decreased $45,000.C. Increased $30,000.D. Increased $45,000.E. Increased $105,000.140. If the assets of a business increased $89,000 during a period of time and its liabilities increased $67,000 during the same period, equity in the business must have:A. Increased $22,000.B. Decreased $22,000.C. Increased $89,000.D. Decreased $156,000.E. Increased $156,000.141. If the liabilities of a company increased $74,000 during a period of time and equity in the company decreased $19,000 during the same period, what was the effect on the assets?A. Assets would have increased $55,000.B. Assets would have decreased $55,000.C. Assets would have increased $19,000.D. Assets would have decreased $19,000.E. None of these.142. If a company paid $38,000 of its accounts payable in cash, what was the effect on the assets, liabilities, and equity?A. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would decrease $38,000.B. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would increase $38,000.C. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would not change.D. There would be no effect on the accounts because the accounts are affected by the same amount.E. None of these.。

会计学英文版作业教程文件

会计学英文版作业教程文件Accounting Homework TutorialIntroduction:Step 1: Read and Understand the QuestionsBefore starting your accounting homework, thoroughly read the questions and ensure you understand what is being asked. Identify any key terms or concepts that are mentioned. Take notes and highlight important details.Step 2: Review Relevant Concepts and PrinciplesOnce you have a clear understanding of the questions, review the relevant concepts and principles that apply to the assignment. Refer to your textbook, lecture notes, or any other reliable sources to refresh your knowledge. Understanding the underlying principles will allow you to approach the problems correctly and accurately.Step 3: Organize and Plan Your ApproachStep 4: Work on the ProblemsStart working on the problems, following your plan. Show all your calculations and include explanations where required. Make sure you apply the correct formulas, rules, and standards of accounting, such as the Generally Accepted Accounting Principles (GAAP).Step 5: Double-Check Your WorkStep 6: Seek Clarification if NeededStep 7: Revise and ProofreadStep 8: Submit Your HomeworkOnce you are satisfied with your work, prepare your assignment for submission. Follow the guidelines provided by your instructor, such as formatting requirements, file type, and submission method. Ensure that you submit your homework within the given deadline.Tips for Success in Accounting Homework:2. Practice regularly: Regular practice of accounting problems will enhance your understanding and speed.3. Form study groups: Collaborating with classmates can help clarify concepts and reinforce learning.4. Utilize online resources: Access online tutorials, video lectures, and practice questions to supplement your learning.5. Stay organized: Keep track of deadlines, create a schedule, and maintain a neat and orderly workspace.6. Seek help when needed: Don't hesitate to approach your instructor or classmates for assistance.Conclusion:。

会计专业英语试卷(推荐5篇)

A.withdrawalsB.accounts receivableC.interest payable 6.Which of the following is an assets account?

A.notes missionC.bonds payable 7.Which of the following is an owner’s equity account?

Passage 1

Many rule govern drivers on the streets and highways.The most common one is the speed limit.The speed limit controls how fast a car may go.On streets in the city, the speed limit is usually 25 or 35 miles per hour.On the highways between cities, the speed limit is usually 55 miles per hour.When people drive faster than the speed limit, a policeman can stop them.The policeman gives them pieces of paper which call traffic tickets.Traffic tickets tell the drivers how much they must pay.When drivers receive too many tickets, they probably cannot drive for a while.The rush hour is when people are going to or returning from work.At rush hour there are many cars on the streets and traffic moves very slowly.Nearly al big cities have rush hours and traffic jams.Drivers do not get tickets very often for speeding during the rush hour because they cannot drive fast.1.The most common rule to govern drivers on the streets and highways is _____.A.the traffic lightB.the traffic licenseC.the traffic jamD.th计专业英语试卷(推荐5篇)

会计英语作业 英语

会计英语作业英语Here's a sample of an accounting English assignmentthat meets the given requirements:Accounting, it's like a language of its own. You gotta know the right terms and figures to make sense of it all. Like, "assets" are the things that have value, like cash or equipment. And "liabilities" are what you owe, like loansor unpaid bills.In accounting, everything has to balance out. Like a scale, you have the debit side and the credit side. Whenyou make a sale, it goes on one side, and when you pay for something, it goes on the other. It's all about keepingtrack of where the money's coming from and where it's going.The financial statements are like the snapshots of a company's financial health. You can see how much money they made, how much they spent, and what they own. It's like looking at a person's bank account and credit cardstatements to get a sense of their financial situation.Audits are when someone comes in and checks your accounting books to make sure you're not cooking the books. They'll look at your receipts, invoices, and.。

会计英语试题及答案

会计英语试题及答案一、选择题(每题2分,共20分)1. Which of the following is not a basic accounting element?A. AssetsB. LiabilitiesB. RevenuesD. Equity答案:C2. The accounting equation can be expressed as:A. Assets = Liabilities + EquityB. Assets + Liabilities = EquityC. Assets - Liabilities = EquityD. Liabilities - Equity = Assets答案:A3. What does the term "Double Entry Bookkeeping" refer to?A. Recording transactions in two accountsB. Recording transactions in two different currenciesC. Recording transactions in two different formatsD. Recording transactions in two different books答案:A4. Which of the following is not a type of adjusting entry?A. AccrualB. PrepaymentC. DepreciationD. Amortization答案:B5. The purpose of closing entries is to:A. Prepare financial statementsB. Adjust for accruals and deferralsC. Record the sale of inventoryD. Record the purchase of fixed assets答案:A6. Which of the following is a measure of a company's liquidity?A. Return on Investment (ROI)B. Debt to Equity RatioC. Current RatioD. Profit Margin答案:C7. The term "Depreciation" refers to:A. The decrease in value of an asset over timeB. The increase in value of an asset over timeC. The amount of an asset that is used upD. The process of selling an asset答案:A8. What is the purpose of a trial balance?A. To calculate net incomeB. To check the accuracy of accounting recordsC. To determine the value of assetsD. To calculate the cost of goods sold答案:B9. Which of the following is not a financial statement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Budget答案:D10. The accounting principle that requires expenses to be recorded in the same period as the revenues they generate is known as:A. Going ConcernB. Matching PrincipleC. Historical Cost PrincipleD. Materiality答案:B二、填空题(每题2分,共20分)1. The __________ is the process of recording financial transactions in a systematic way.答案:Journalizing2. The __________ is a summary of the financial transactionsof a business during a specific period.答案:Ledger3. __________ is the accounting principle that requires all accounting information to be based on historical cost.答案:Historical Cost Principle4. The __________ is a financial statement that shows a company's financial position at a specific point in time.答案:Balance Sheet5. __________ is the process of estimating revenues and expenses for a future period.答案:Budgeting6. __________ is the accounting principle that requires all transactions to be recorded in the period in which they occur.答案:Accrual Basis Accounting7. The __________ is a financial statement that shows the results of a company's operations over a period of time.答案:Income Statement8. __________ is the process of determining the value of a company's assets and liabilities.答案:Valuation9. __________ is the accounting principle that requires alltransactions to be recorded in the order in which they occur.答案:Chronological Order10. The __________ is a financial statement that shows the sources and uses of cash during a period of time.答案:Cash Flow Statement三、简答题(每题15分,共30分)1. 描述会计信息的质量特征有哪些,并简要解释它们的含义。

大学会计专业英语作文

大学会计专业英语作文Accounting is an important field in the business world, and studying accounting in college is a great way toprepare for a career in this field. As a college accounting student, I have learned a great deal about accounting principles and practices, as well as the role ofaccountants in the business world. In this essay, I will discuss some of the key concepts and skills that I have learned in my college accounting courses.One of the most important concepts in accounting is the idea of double-entry bookkeeping. This means that every transaction in a business must be recorded in two different accounts: one account to show the increase in assets, and another account to show the decrease in assets. For example, if a business purchases a new computer for $1,000, the transaction would be recorded in two accounts: the computer asset account would be increased by $1,000, and the cash account would be decreased by $1,000. This ensures that the books are always balanced and accurate.Another important concept in accounting is the use of financial statements. These statements provide a snapshotof a business's financial position at a given point in time. The three main financial statements are the balance sheet, the income statement, and the statement of cash flows. The balance sheet shows a business's assets, liabilities, and equity at a specific point in time. The income statement shows a business's revenue, expenses, and net income over a period of time. The statement of cash flows shows theinflows and outflows of cash during a period of time.In addition to these concepts, accounting students also learn a variety of skills that are essential for success in the field. One of the most important skills is attention to detail. Accountants must be meticulous in their work, ensuring that every transaction is recorded accurately and completely. They must also be able to analyze financialdata and draw conclusions from it. This requires strong analytical skills and the ability to think critically.Another important skill for accountants iscommunication. Accountants must be able to explainfinancial information to people who may not have a background in accounting. They must also be able to work effectively with others, including clients, colleagues, and managers.Finally, accounting students must also be familiar with accounting software and technology. Many businesses use accounting software to manage their finances, and accountants must be able to use these programs effectively. They must also be familiar with other technologies, such as spreadsheets and databases, that are used in accounting.In conclusion, studying accounting in college has provided me with a strong foundation in accounting principles and practices. I have learned about double-entry bookkeeping, financial statements, and a variety of skills that are essential for success in the field. I am confident that my education will prepare me for a rewarding career in accounting.。

会计学专业 会计英语试题

一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting? ( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance with established procedures.3.Which of the following statements is(are) correct?( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet? ( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses?( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recorded by credits.C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct?( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’ equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management? ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up toa year in advance. D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement? ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information? ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs.petence’judgment’and ethical behavior of individual accountants’D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receiving in exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance? ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A )A.Dr. Bad Debt Accts. $1,500B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retained earnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900( B )A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $300pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )A.Dr. Office Equipment $2,000B.Dr.Office Equipment $2,000Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,100pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B )A.Dr. Accts Rec $2000B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )A.Dr.Office equipment $2500B.Dr. Office equipment $2500Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账的制度B.复式记账机制C.会计的重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等的B.借出金额与贷款金额是相等的C.借入金额与贷款金额是相等的Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly high continuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高的持续经营比率。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

a. Cash withdrawal by owner d. Cash g. Prepaid rentb. Office equipment e. Utilities expenses h. Unearned feesc. Accounts payable f. Office supplies i. Service fees earned1-6 The following are common categories on a classified balance sheet.A. Current assets D. Intangible assetsB. Long-term investments E. Current liabilitiesC. Plant assets F. Long-term liabilitiesFor each of the following items, select the letter that identifies the balance sheet category where the item typically would appear.______ 1. Land not currently used in operations ______ 5. Accounts payable______ 2. Notes payable (due in three years) ______ 6. Store equipment______ 3. Accounts receivable ______ 7. Wages payable______ 4. Trademarks ______ 8. Cash1-7 In the blank space beside each numbered balance sheet item, enter the letter of its balance sheet classification. If the item should not appear on the balance sheet, enter a Z in the blank.A. Current assets D. Intangible assets F. Long-term liabilitiesB. Long-term investments E. Current liabilities G. EquityC. Plant assets______ 1. Long-term investment in stock ______ 12. Accumulated depreciation—Trucks ______ 2. Depreciation expense—Building ______ 13. Cash______ 3. Prepaid rent______ 4. Interest receivable ______ 14. Buildings______ 5. Taxes payable ______ 15. Store supplies______ 6. Automobiles ______ 16. Office equipment______ 7. Notes payable (due in 3 years) ______ 17. Land (used in operations)______ 8. Accounts payable ______ 18. Repairs expense______ 9. Prepaid insurance ______ 19. Office supplies______ 10. Owner, Capital ______ 20. Current portion of long-term note payable ______ 11. Unearned services revenue1-8 In the blank space beside each numbered balance sheet item, enter the letter of its balance sheet classfication. If the item should not appear on the balance sheet, enter a Z in the blank.A. Current assets E. Current liabilitiesB. Long-term investments F. Long-term liabilitiesC. Plant assets G. Equity3-2 The adjusted trial balance for Chiara Company as of December 31, 2008, follows.Debit CreditCash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 30,000Accounts receivable . . . . . . . . . . . . . . . . . . . . . . . 52,000Interest receivable . . . . . . . . . . . . . . . . . . . . . . . . 18,000Notes receivable (due in 90 days) . . . . . . . . . . . . . 168,000Office supplies . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,000Automobiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168,000Accumulated depreciation—Automobiles . . . . . . . $ 50,000Equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138,000Accumulated depreciation—Equipment . . . . . . . . . 18,000Land . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78,000Accounts payable . . . . . . . . . . . . . . . . . . . . . . . . . 96,000Interest payable . . . . . . . . . . . . . . . . . . . . . . . . . . 20,000Salaries payable . . . . . . . . . . . . . . . . . . . . . . . . . . 19,000Unearned fees . . . . . . . . . . . . . . . . . . . . . . . . . . . 30,000Long-term notes payable . . . . . . . . . . . . . . . . . . . 138,000R.Chiara,Capital . . . . . . . . . . . . . . . . . . . . . . . . . 255,800R.Chiara,Withdrawals . . . . . . . . . . . . . . . 46,000Fees earned . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 484,000Interest earned . . . . . . . . . . . . . . . . . . . . . . . . . . 24,000Depreciation expense—Automobiles . . . . . . . . . . 26,000Depreciation expense—Equipment . . . . . . . . . . . . 18,000Salaries expense . . . . . . . . . . . . . . . . . . . . . . . . . . 188,000Wages expense . . . . . . . . . . . . . . . . . . . . . . . . . . 40,000Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . 32,000Office supplies expense . . . . . . . . . . . . . . . . . . . . 34,000Advertising expense . . . . . . . . . . . . . . . . . . . . . . . 58,000Repairs expense—Automobiles . . . . . . . . . . . . . . 24,800Totals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,134,800 $1,134,800Required1. Use the information in the adjusted trial balance to prepare (a) the income statement for the year ended December 31,2008; (b) the statement of owner’s equity for the year ended December 31,2008;and (c) the balance sheet as of December 31, 2008.2. Calculate the profit margin for year 2008.3-3 On April 1, 2008, Jiro Nozomi created a new travel agency, Adventure Travel. The following transactions occurred during the company’s first month..April 1 Nozomi invested $30,000 cash and computer equipment worth $20,000 in the business.2 Rented furnished office space by paying $1,800 cash for the first month’s (April) rent.3 Purchased $1,000 of office supplies for cash.10 Paid $2,400 cash for the premium on a 12-month insurance policy. Coverage begins onApril 11.14 Paid $1,600 cash for two weeks’salaries earned by employees.24 Collected $8,000 cash on commissions from airlines on tickets obtained for customers.28 Paid another $1,600 cash for two weeks’salaries earned by employees.29 Paid $350 cash for minor rep airs to the company’s computer.30 Paid $750 cash for this month’s telephone bill.30 Nozomi withdrew $1,500 cash for personal use.The company’s chart of accounts follows:101 Cash 405 Commissions Earned106 Accounts Receivable 612 Depreciation Expense—Computer Equip.124 Office Supplies 622 Salaries Expense128 Prepaid Insurance 637 Insurance Expense167 Computer Equipment 640 Rent Expense168 Accumulated Depreciation—Computer Equip. 650 Office Supplies Expense209 Salaries Payable 684 Repairs Expense301 J.Nozomi,Capital 688 Telephone Expense302 J.Nozomi,Withdrawals 901 Income SummaryRequired:1. Use the balance column format to set up each ledger account listed in its chart of accounts.2. Prepare journal entries to record the transactions for April and post them to the ledger accounts. The company records prepaid and unearned items in balance sheet accounts.3. Prepare an unadjusted trial balance as of April 30.4. Use the following information to journalize and post adjusting entries for the month:a. Two-thirds of one month’s insurance coverage has expired.b. At the end of the month, $600 of office supplies are still available.c. This month’s depreciation on the computer equipment is $500.d. Employees earned $420 of unpaid and unrecorded salaries as of month-end.e. The company earned $1,750 of commissions that are not yet billed at month-end.5. Prepare the income statement and the statement of owner’s equity for the month of April a nd the balance sheet at April 30, 2008.6. Prepare journal entries to close the temporary accounts .7. Prepare a post-closing trial balance.。