Interests in Joint Ventures IAS 31

国际会计准则(1~41)中英文目录对照

国际会计准则(1~41)中英文目录对照国际会计准则(1~41)中英文目录对照1.IAS1:Presentation of Financial Statements《IAS1——财务报表的列报》2.IAS2:Inventories《IAS2——存货》3.IAS3:Consolidated Financial Statements《IAS3——合并财务报表》(已被IAS27和IAS28取代)4.IAS4:Depreciation Accounting《IAS4——折旧会计》(已被IAS16、IAS22和IAS38取代)5.IAS5:Information to Be Disclosed in Financial Statements《IAS5——财务报表中披露的信息》(已被IAS1取代)6.IAS6:Accounting Responses to Changing Prices《IAS6——物价变动会计》(已被IAS15取代)7.IAS7:Cash Flow Statements《IAS7——现金流量表》8.IAS8:Accounting Policies, Changes in Accounting Estimates and Errors 《IAS8——当期净损益、重大差错和会计政策变更》9.IAS9:Accounting for Research and Development Activities《IAS9——研发活动会计》(已被IAS38取代)10.IAS10:Events after the Balance Sheet Date《IAS10——资产负债表日后事项》11.IAS11:Construction Contracts《IAS11——建造合同》12.IAS12:Income Taxes《IAS12——所得税》13.IAS13:Presentation of Current Assets and Current Liabilities 《IAS13——流动资产和流动负债的列报》(已被IAS1取代)14.IAS14:Segment Reporting《IAS14——分部报告》15.IAS15:Information Reflecting the Effects of Changing Prices《IAS15——反映物价变动影响的信息》(2003年已被撤销)16.IAS16:Property, Plant and Equipment《IAS16——不动产、厂场和设备》17.IAS17:Leases《IAS17——租赁》18.IAS18:Revenue《IAS18——收入》19.IAS19:Employee Benefits《IAS19——雇员福利》20.IAS20:Accounting for Government Grants and Disclosure of Government Assistance《IAS20——政府补助会计和政府援助的披露》21.IAS21:The Effects of Changes in Foreign Exchange Rates《IAS21——汇率变动的影响》22.IAS22:Business Combinations《IAS22——企业合并》(已被IFRS3取代)23.IAS23:Borrowing Costs《IAS23——借款费用》24.IAS24:Related Party Disclosures《IAS24——关联方披露》25.IAS25:Accounting for Investments《IAS25——投资会计》(已被IAS39 和IAS40取代)26.IAS26:Accounting and Reporting by Retirement Benefit Plans《IAS26——退休福利计划的会计和报告》27.IAS27:Consolidated and Separate Financial Statements《IAS27——合并财务报表及对子公司投资会计》28.IAS28:Investments in Associates《IAS28——对联合企业投资会计》29.IAS29:Financial Reporting in Hyperinflationary Economies《IAS29——恶性通货膨胀经济中的财务报告》30.IAS30:Disclosures in the Financial Statements of Banks and Similar Financial Institutions《IAS30——银行和类似金融机构财务报表中的披露》31.IAS31:Interests in Joint Ventures《IAS31——合营中权益的财务报告》32.IAS32:Financial Instruments: Disclosure and Presentation《IAS32——金融工具:披露和列报》33.IAS33:Earnings per Share《IAS33——每股收益》34.IAS34:Interim Financial Reporting《IAS34——中期财务报告》35.IAS35:Discontinuing Operations《IAS35——终止经营》(已被IFRS5取代)36.IAS36:Impairment of Assets《IAS36——资产减值》37.IAS37:Provisions, Contingent Liabilities and Contingent Assets 《IAS37——准备、或有负债和或有资产》38.IAS38:Intangible Assets《IAS38——无形资产》39.IAS39:Financial Instruments: Recognition and Measurement《IAS39——金融工具:确认和计量》40.IAS40:Investment Property《IAS40——投资性房地产》41.IAS41:Agriculture《IAS41——农业》国际会计准则中文版文件格式:Pdf可复制性:可复制TAG标签:会计学点击次数:更新时间:2010-03-30 15:23介绍国际会计准则中文版,国际会计准则在2008年做了更新,中文版不知道是否同步更新,这个对于会计从业人员的帮助很大,在网上找了很久中文版都是2003的老版本,不知道楼主上传的版本对我是否有用。

ias31_en

International Accounting Standard 31Interests in Joint VenturesScope1 This Standard shall be applied in accounting for interests in joint ventures and the reporting of jointventure assets, liabilities, income and expenses in the financial statements of venturers and investors, regardless of the structures or forms under which the joint venture activities take place. However, it does not apply to venturers’ interests in jointly controlled entities held by:(a) venture capital organisations, or(b) mutual funds, unit trusts and similar entities including investment-linked insurance fundsthat upon initial recognition are designated as at fair value through profit or loss or are classified as held for trading and accounted for in accordance with IAS 39 Financial Instruments: Recognition and Measurement. Such investments shall be measured at fair value in accordance with IAS 39, with changes in fair value recognised in profit or loss in the period of the change. A venturer holding such an interest shall make the disclosures required by paragraphs 55 and 56.2 A venturer with an interest in a jointly controlled entity is exempted from paragraphs 30(proportionate consolidation) and 38 (equity method) when it meets the following conditions:(a) the interest is classified as held for sale in accordance with IFRS 5 Non-current Assets Held forSale and Discontinued Operations;(b) the exception in paragraph 10 of IAS 27 Consolidated and Separate Financial Statementsallowing a parent that also has an interest in a jointly controlled entity not to presentconsolidated financial statements is applicable; or(c) all of the following apply:(i) the venturer is a wholly-owned subsidiary, or is a partially-owned subsidiary ofanother entity and its owners, including those not otherwise entitled to vote, havebeen informed about, and do not object to, the venturer not applying proportionateconsolidation or the equity method;(ii) the venturer’s debt or equity instruments are not traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including localand regional markets);(iii) the venturer did not file, nor is it in the process of filing, its financial statements witha securities commission or other regulatory organisation, for the purpose of issuingany class of instruments in a public market; and(iv) the ultimate or any intermediate parent of the venturer produces consolidated financial statements available for public use that comply with International FinancialReporting Standards.Definitions3 The following terms are used in this Standard with the meanings specified:Control is the power to govern the financial and operating policies of an economic activity so as to obtain benefits from it.The equity method is a method of accounting whereby an interest in a jointly controlled entity is initially recorded at cost and adjusted thereafter for the post-acquisition change in the venturer’s share of net assets of the jointly controlled entity. The profit or loss of the venturer includes the venturer’s share of the profit or loss of the jointly controlled entity.An investor in a joint venture is a party to a joint venture and does not have joint control over that joint venture.Joint control is the contractually agreed sharing of control over an economic activity, and exists only when the strategic financial and operating decisions relating to the activity require the unanimous consent of the parties sharing control (the venturers).A joint venture is a contractual arrangement whereby two or more parties undertake an economicactivity that is subject to joint control.Proportionate consolidation is a method of accounting whereby a venturer’s share of each of the assets, liabilities, income and expenses of a jointly controlled entity is combined line by line with similar items in the venturer’s financial statements or reported as separate line items in the venturer’s financial statements.Separate financial statements are those presented by a parent, an investor in an associate or a venturer in a jointly controlled entity, in which the investments are accounted for on the basis of the direct equity interest rather than on the basis of the reported results and net assets of the investees.Significant influence is the power to participate in the financial and operating policy decisions of an economic activity but is not control or joint control over those policies.A venturer is a party to a joint venture and has joint control over that joint venture.4 Financial statements in which proportionate consolidation or the equity method is applied are not separatefinancial statements, nor are the financial statements of an entity that does not have a subsidiary, associate or venturer’s interest in a jointly controlled entity.5 Separate financial statements are those presented in addition to consolidated financial statements, financialstatements in which investments are accounted for using the equity method and financial statements in which venturers’ interests in joint ventures are proportionately consolidated. Separate financial statements need not be appended to, or accompany, those statements.6 Entities that are exempted in accordance with paragraph 10 of IAS 27 from consolidation, paragraph 13(c) ofIAS 28 Investments in Associates from applying the equity method or paragraph 2 of this Standard from applying proportionate consolidation or the equity method may present separate financial statements as their only financial statements.Forms of joint venture7 Joint ventures take many different forms and structures. This Standard identifies three broad types—jointlycontrolled operations, jointly controlled assets and jointly controlled entities—that are commonly described as, and meet the definition of, joint ventures. The following characteristics are common to all joint ventures:(a) two or more venturers are bound by a contractual arrangement; and(b) the contractual arrangement establishes joint control.Joint control8 Joint control may be precluded when an investee is in legal reorganisation or in bankruptcy, or operates undersevere long-term restrictions on its ability to transfer funds to the venturer. If joint control is continuing, these events are not enough in themselves to justify not accounting for joint ventures in accordance with this Standard.Contractual arrangement9 The existence of a contractual arrangement distinguishes interests that involve joint control from investmentsin associates in which the investor has significant influence (see IAS 28). Activities that have no contractual arrangement to establish joint control are not joint ventures for the purposes of this Standard.10 The contractual arrangement may be evidenced in a number of ways, for example by a contract between theventurers or minutes of discussions between the venturers. In some cases, the arrangement is incorporated in the articles or other by-laws of the joint venture. Whatever its form, the contractual arrangement is usually in writing and deals with such matters as:(a) the activity, duration and reporting obligations of the joint venture;(b) the appointment of the board of directors or equivalent governing body of the joint venture and thevoting rights of the venturers;(c) capital contributions by the venturers; and(d) the sharing by the venturers of the output, income, expenses or results of the joint venture.11 The contractual arrangement establishes joint control over the joint venture. Such a requirement ensures thatno single venturer is in a position to control the activity unilaterally.12 The contractual arrangement may identify one venturer as the operator or manager of the joint venture. Theoperator does not control the joint venture but acts within the financial and operating policies that have been agreed by the venturers in accordance with the contractual arrangement and delegated to the operator. If the operator has the power to govern the financial and operating policies of the economic activity, it controls the venture and the venture is a subsidiary of the operator and not a joint venture.Jointly controlled operations13 The operation of some joint ventures involves the use of the assets and other resources of the venturers ratherthan the establishment of a corporation, partnership or other entity, or a financial structure that is separate from the venturers themselves. Each venturer uses its own property, plant and equipment and carries its own inventories. It also incurs its own expenses and liabilities and raises its own finance, which represent its own obligations. The joint venture activities may be carried out by the venturer’s employees alongside the venturer’s similar activities. The joint venture agreement usually provides a means by which the revenue from the sale of the joint product and any expenses incurred in common are shared among the venturers.14 An example of a jointly controlled operation is when two or more venturers combine their operations,resources and expertise to manufacture, market and distribute jointly a particular product, such as an aircraft.Different parts of the manufacturing process are carried out by each of the venturers. Each venturer bears its own costs and takes a share of the revenue from the sale of the aircraft, such share being determined in accordance with the contractual arrangement.15 In respect of its interests in jointly controlled operations, a venturer shall recognise in its financialstatements:(a) the assets that it controls and the liabilities that it incurs; and(b) the expenses that it incurs and its share of the income that it earns from the sale of goods orservices by the joint venture.16 Because the assets, liabilities, income and expenses are recognised in the financial statements of the venturer,no adjustments or other consolidation procedures are required in respect of these items when the venturer presents consolidated financial statements.17 Separate accounting records may not be required for the joint venture itself and financial statements may notbe prepared for the joint venture. However, the venturers may prepare management accounts so that they may assess the performance of the joint venture.18 Some joint ventures involve the joint control, and often the joint ownership, by the venturers of one or moreassets contributed to, or acquired for the purpose of, the joint venture and dedicated to the purposes of the joint venture. The assets are used to obtain benefits for the venturers. Each venturer may take a share of the output from the assets and each bears an agreed share of the expenses incurred.19 These joint ventures do not involve the establishment of a corporation, partnership or other entity, or afinancial structure that is separate from the venturers themselves. Each venturer has control over its share of future economic benefits through its share of the jointly controlled asset.20 Many activities in the oil, gas and mineral extraction industries involve jointly controlled assets. Forexample, a number of oil production companies may jointly control and operate an oil pipeline. Each venturer uses the pipeline to transport its own product in return for which it bears an agreed proportion of the expenses of operating the pipeline. Another example of a jointly controlled asset is when two entities jointly control a property, each taking a share of the rents received and bearing a share of the expenses.21 In respect of its interest in jointly controlled assets, a venturer shall recognise in its financialstatements:(a) its share of the jointly controlled assets, classified according to the nature of the assets;(b) any liabilities that it has incurred;(c) its share of any liabilities incurred jointly with the other venturers in relation to the jointventure;(d) any income from the sale or use of its share of the output of the joint venture, together with itsshare of any expenses incurred by the joint venture; and(e) any expenses that it has incurred in respect of its interest in the joint venture.22 In respect of its interest in jointly controlled assets, each venturer includes in its accounting records andrecognises in its financial statements:(a) its share of the jointly controlled assets, classified according to the nature of the assets rather than asan investment. For example, a share of a jointly controlled oil pipeline is classified as property,plant and equipment.(b) any liabilities that it has incurred, for example those incurred in financing its share of the assets.(c) its share of any liabilities incurred jointly with other venturers in relation to the joint venture.(d) any income from the sale or use of its share of the output of the joint venture, together with its shareof any expenses incurred by the joint venture.(e) any expenses that it has incurred in respect of its interest in the joint venture, for example thoserelated to financing the venturer’s interest in the assets and selling its share of the output.Because the assets, liabilities, income and expenses are recognised in the financial statements of the venturer, no adjustments or other consolidation procedures are required in respect of these items when the venturer presents consolidated financial statements.23 The treatment of jointly controlled assets reflects the substance and economic reality and, usually, the legalform of the joint venture. Separate accounting records for the joint venture itself may be limited to those expenses incurred in common by the venturers and ultimately borne by the venturers according to their agreed shares. Financial statements may not be prepared for the joint venture, although the venturers may prepare management accounts so that they may assess the performance of the joint venture.24 A jointly controlled entity is a joint venture that involves the establishment of a corporation, partnership orother entity in which each venturer has an interest. The entity operates in the same way as other entities, except that a contractual arrangement between the venturers establishes joint control over the economic activity of the entity.25 A jointly controlled entity controls the assets of the joint venture, incurs liabilities and expenses and earnsincome. It may enter into contracts in its own name and raise finance for the purposes of the joint venture activity. Each venturer is entitled to a share of the profits of the jointly controlled entity, although some jointly controlled entities also involve a sharing of the output of the joint venture.26 A common example of a jointly controlled entity is when two entities combine their activities in a particularline of business by transferring the relevant assets and liabilities into a jointly controlled entity. Another example is when an entity commences a business in a foreign country in conjunction with the government or other agency in that country, by establishing a separate entity that is jointly controlled by the entity and the government or agency.27 Many jointly controlled entities are similar in substance to those joint ventures referred to as jointlycontrolled operations or jointly controlled assets. For example, the venturers may transfer a jointly controlled asset, such as an oil pipeline, into a jointly controlled entity, for tax or other reasons. Similarly, the venturers may contribute into a jointly controlled entity assets that will be operated jointly. Some jointly controlled operations also involve the establishment of a jointly controlled entity to deal with particular aspects of the activity, for example, the design, marketing, distribution or after-sales service of the product.28 A jointly controlled entity maintains its own accounting records and prepares and presents financialstatements in the same way as other entities in conformity with International Financial Reporting Standards.29 Each venturer usually contributes cash or other resources to the jointly controlled entity. These contributionsare included in the accounting records of the venturer and recognised in its financial statements as an investment in the jointly controlled entity.Financial statements of a venturerProportionate consolidation30 A venturer shall recognise its interest in a jointly controlled entity using proportionate consolidation orthe alternative method described in paragraph 38. When proportionate consolidation is used, one of the two reporting formats identified below shall be used.31 A venturer recognises its interest in a jointly controlled entity using one of the two reporting formats forproportionate consolidation irrespective of whether it also has investments in subsidiaries or whether it describes its financial statements as consolidated financial statements.32 When recognising an interest in a jointly controlled entity, it is essential that a venturer reflects the substanceand economic reality of the arrangement, rather than the joint venture’s particular structure or form. In a jointly controlled entity, a venturer has control over its share of future economic benefits through its share of the assets and liabilities of the venture. This substance and economic reality are reflected in the consolidated financial statements of the venturer when the venturer recognises its interests in the assets, liabilities, income and expenses of the jointly controlled entity by using one of the two reporting formats for proportionate consolidation described in paragraph 34.33 The application of proportionate consolidation means that the statement of financial position of the venturerincludes its share of the assets that it controls jointly and its share of the liabilities for which it is jointly responsible. The statement of comprehensive income of the venturer includes its share of the income and expenses of the jointly controlled entity. Many of the procedures appropriate for the application of proportionate consolidation are similar to the procedures for the consolidation of investments in subsidiaries, which are set out in IAS 27.34 Different reporting formats may be used to give effect to proportionate consolidation. The venturer maycombine its share of each of the assets, liabilities, income and expenses of the jointly controlled entity withthe similar items, line by line, in its financial statements. For example, it may combine its share of the jointly controlled entity’s inventory with its inventory and its share of the jointly controlled entity’s property, plant and equipment with its property, plant and equipment. Alternatively, the venturer may include separate line items for its share of the assets, liabilities, income and expenses of the jointly controlled entity in its financial statements. For example, it may show its share of a current asset of the jointly controlled entity separately as part of its current assets; it may show its share of the property, plant and equipment of the jointly controlled entity separately as part of its property, plant and equipment. Both these reporting formats result in the reporting of identical amounts of profit or loss and of each major classification of assets, liabilities, income and expenses; both formats are acceptable for the purposes of this Standard.35 Whichever format is used to give effect to proportionate consolidation, it is inappropriate to offset any assetsor liabilities by the deduction of other liabilities or assets or any income or expenses by the deduction of other expenses or income, unless a legal right of set-off exists and the offsetting represents the expectation as to the realisation of the asset or the settlement of the liability.36 A venturer shall discontinue the use of proportionate consolidation from the date on which it ceases tohave joint control over a jointly controlled entity.37 A venturer discontinues the use of proportionate consolidation from the date on which it ceases to share inthe control of a jointly controlled entity. This may happen, for example, when the venturer disposes of its interest or when such external restrictions are placed on the jointly controlled entity that the venturer no longer has joint control.Equity method38 As an alternative to proportionate consolidation described in paragraph 30, a venturer shall recogniseits interest in a jointly controlled entity using the equity method.39 A venturer recognises its interest in a jointly controlled entity using the equity method irrespective of whetherit also has investments in subsidiaries or whether it describes its financial statements as consolidated financial statements.40 Some venturers recognise their interests in jointly controlled entities using the equity method, as described inIAS 28. The use of the equity method is supported by those who argue that it is inappropriate to combine controlled items with jointly controlled items and by those who believe that venturers have significant influence, rather than joint control, in a jointly controlled entity. This Standard does not recommend the use of the equity method because proportionate consolidation better reflects the substance and economic reality of a venturer’s interest in a jointly controlled entity, that is to say, control over the venturer’s share of the future economic benefits. Nevertheless, this Standard permits the use of the equity method, as an alternative treatment, when recognising interests in jointly controlled entities.41 A venturer shall discontinue the use of the equity method from the date on which it ceases to have jointcontrol over, or have significant influence in, a jointly controlled entity.Exceptions to proportionate consolidation and equity method42 Interests in jointly controlled entities that are classified as held for sale in accordance with IFRS 5 shallbe accounted for in accordance with that IFRS.43 When an interest in a jointly controlled entity previously classified as held for sale no longer meets thecriteria to be so classified, it shall be accounted for using proportionate consolidation or the equity method as from the date of its classification as held for sale. Financial statements for the periods since classification as held for sale shall be amended accordingly.44 [Deleted]45When an investor ceases to have joint control over an entity, it shall account for any remaining investment in accordance with IAS 39 from that date, provided that the former jointly controlled entity does not become a subsidiary or associate. From the date when a jointly controlled entity becomes a subsidiary of an investor, the investor shall account for its interest in accordance with IAS27 and IFRS 3 Business Combinations (as revised by the International Accounting Standards Board in2008). From the date when a jointly controlled entity becomes an associate of an investor, the investorshall account for its interest in accordance with IAS 28. On the loss of joint control, the investor shall measure at fair value any investment the investor retains in the former jointly controlled entity. The investor shall recognise in profit or loss any difference between:(a)the fair value of any retained investment and any proceeds from disposing of the partinterest in the jointly controlled entity; and(b)the carrying amount of the investment at the date when joint control is lost.45A When an investment ceases to be a jointly controlled entity and is accounted for in accordance with IAS 39, the fair value of the investment when it ceases to be a jointly controlled entity shall be regarded as its fair value on initial recognition as a financial asset in accordance with IAS 39.45B If an investor loses joint control of an entity, the investor shall account for all amounts recognised in other comprehensive income in relation to that entity on the same basis as would be required if the jointly controlled entity had directly disposed of the related assets or liabilities. Therefore, if a gain or loss previously recognised in other comprehensive income would be reclassified to profit or loss on the disposal of the related assets or liabilities, the investor reclassifies the gain or loss from equity to profit or loss (as a reclassification adjustment) when the investor loses joint control of the entity. For example, if a jointly controlled entity has available-for-sale financial assets and the investor loses joint control of the entity, the investor shall reclassify to profit or loss the gain or loss previously recognised in other comprehensive income in relation to those assets. If an investor’s ownership interest in a jointly controlled entity is reduced, but the investment continues to be a jointly controlled entity, the investor shall reclassify to profit or loss only a proportionate amount of the gain or loss previously recognised in other comprehensive income.Separate financial statements of a venturer46 An interest in a jointly controlled entity shall be accounted for in a venturer’s separate financialstatements in accordance with paragraphs 37–42 of IAS 27.47 This Standard does not mandate which entities produce separate financial statements available for public use. Transactions between a venturer and a joint venture48 When a venturer contributes or sells assets to a joint venture, recognition of any portion of a gain orloss from the transaction shall reflect the substance of the transaction. While the assets are retained by the joint venture, and provided the venturer has transferred the significant risks and rewards of ownership, the venturer shall recognise only that portion of the gain or loss that is attributable to the interests of the other venturers.1 The venturer shall recognise the full amount of any loss when the contribution or sale provides evidence of a reduction in the net realisable value of current assets or an impairment loss.49 When a venturer purchases assets from a joint venture, the venturer shall not recognise its share of theprofits of the joint venture from the transaction until it resells the assets to an independent party.A venturer shall recognise its share of the losses resulting from these transactions in the same way asprofits except that losses shall be recognised immediately when they represent a reduction in the net realisable value of current assets or an impairment loss.50 To assess whether a transaction between a venturer and a joint venture provides evidence of impairment of anasset, the venturer determines the recoverable amount of the asset in accordance with IAS 36 Impairment of Assets. In determining value in use, the venturer estimates future cash flows from the asset on the basis of continuing use of the asset and its ultimate disposal by the joint venture.1See also SIC-13 Jointly Controlled Entities—Non-Monetary Contributions by Venturers.Reporting interests in joint ventures in the financial statements of an investor51 An investor in a joint venture that does not have joint control shall account for that investment inaccordance with IAS 39 or, if it has significant influence in the joint venture, in accordance with IAS 28.Operators of joint ventures52 Operators or managers of a joint venture shall account for any fees in accordance with IAS 18Revenue.53 One or more venturers may act as the operator or manager of a joint venture. Operators are usually paid amanagement fee for such duties. The fees are accounted for by the joint venture as an expense. Disclosure54 A venturer shall disclose the aggregate amount of the following contingent liabilities, unless theprobability of loss is remote, separately from the amount of other contingent liabilities:(a) any contingent liabilities that the venturer has incurred in relation to its interests in jointventures and its share in each of the contingent liabilities that have been incurred jointly withother venturers;(b) its share of the contingent liabilities of the joint ventures themselves for which it iscontingently liable; and(c) those contingent liabilities that arise because the venturer is contingently liable for theliabilities of the other venturers of a joint venture.55 A venturer shall disclose the aggregate amount of the following commitments in respect of its interestsin joint ventures separately from other commitments:(a) any capital commitments of the venturer in relation to its interests in joint ventures and itsshare in the capital commitments that have been incurred jointly with other venturers; and(b) its share of the capital commitments of the joint ventures themselves.56 A venturer shall disclose a listing and description of interests in significant joint ventures and theproportion of ownership interest held in jointly controlled entities. A venturer that recognises its interests in jointly controlled entities using the line-by-line reporting format for proportionate consolidation or the equity method shall disclose the aggregate amounts of each of current assets, long-term assets, current liabilities, long-term liabilities, income and expenses related to its interests in joint ventures.57 A venturer shall disclose the method it uses to recognise its interests in jointly controlled entities. Effective date58 An entity shall apply this Standard for annual periods beginning on or after 1 January 2005. Earlierapplication is encouraged. If an entity applies this Standard for a period beginning before 1 January 2005, it shall disclose that fact.58A IAS 27 (as amended by the International Accounting Standards Board in 2008) amended paragraph 45 and added paragraphs 45A and 45B. An entity shall apply those amendments for annual periods beginning on or after 1 July 2009. If an entity applies IAS 27 (amended 2008) for an earlier period, the amendments shall be applied for that earlier period.。

ifrs12国际财务报告准则12号

IFRS12 International Financial Reporting Standard12Disclosure of Interests in Other EntitiesIn May2011the International Accounting Standards Board(IASB)issued IFRS12Disclosure of Interests in Other Entities.IFRS12replaced the disclosure requirements in IAS27Consolidated and Separate Financial Statements,IAS28Investments in Associates and IAS31Interests in Joint Ventures.In June2012,IFRS12was amended by Consolidated Financial Statements,Joint Arrangements and Disclosure of Interests in Other Entities:Transition Guidance(Amendments to IFRS10,IFRS11and IFRS12).These amendments provided additional transition relief in IFRS12,limiting the requirement to present adjusted comparative information to only the annual period immediately preceding the first annual period for which IFRS12is applied.Furthermore, for disclosures related to unconsolidated structured entities,the amendments removed the requirement to present comparative information for periods before IFRS12is first applied.Other IFRSs have made minor consequential amendments to IFRS12,including Investment Entities(Amendments to IFRS10,IFRS12and IAS27)(issued October2012).IFRS Foundation A505IFRS12C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL FINANCIAL REPORTING STANDARD12 DISCLOSURE OF INTERESTS IN OTHER ENTITIESOBJECTIVE1 Meeting the objective2 SCOPE5 SIGNIFICANT JUDGEMENTS AND ASSUMPTIONS7 Investment entity status9A INTERESTS IN SUBSIDIARIES10 The interest that non-controlling interests have in the group’s activities andcash flows12 The nature and extent of significant restrictions13 Nature of the risks associated with an entity’s interests in consolidatedstructured entities14 Consequences of changes in a parent’s ownership interest in a subsidiarythat do not result in a loss of control18 Consequences of losing control of a subsidiary during the reporting period19 INTERESTS IN UNCONSOLIDATED SUBSIDIARIES(INVESTMENT ENTITIES)19A INTERESTS IN JOINT ARRANGEMENTS AND ASSOCIATES20 Nature,extent and financial effects of an entity’s interests in jointarrangements and associates21 Risks associated with an entity’s interests in joint ventures and associates23 INTERESTS IN UNCONSOLIDATED STRUCTURED ENTITIES24 Nature of interests26 Nature of risks29 APPENDICESA Defined termsB Application guidanceC Effective date and transitionD Amendments to other IFRSsFOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONAPPROVAL BY THE BOARD OF IFRS12ISSUED IN MAY2011APPROVAL BY THE BOARD OF CONSOLIDATED FINANCIAL STATEMENTS,JOINT ARRANGEMENTS AND DISCLOSURE OF INTERESTS IN OTHERENTITIES:TRANSITION GUIDANCE(AMENDMENTS TO IFRS10,IFRS11ANDIFRS12)ISSUED IN JUNE2012APPROVAL BY THE BOARD OF INVESTMENT ENTITIES(AMENDMENTS TOIFRS10,IFRS12AND IAS27)ISSUED IN OCTOBER2012A506IFRS FoundationIFRS12 BASIS FOR CONCLUSIONSIFRS Foundation A507IFRS12International Financial Reporting Standard12Disclosure of Interests in Other Entities (IFRS12)is set out in paragraphs1–31and Appendices A–D.All the paragraphs have equal authority.Paragraphs in bold type state the main principles.Terms defined in Appendix A are in italics the first time they appear in the IFRS.Definitions of other terms are given in the Glossary for International Financial Reporting Standards.IFRS12 should be read in the context of its objective and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.A508IFRS FoundationIFRS12 IntroductionIN1IFRS12Disclosure of Interests in Other Entities applies to entities that have an interest in a subsidiary,a joint arrangement,an associate or an unconsolidatedstructured entity.IN2The IFRS is effective for annual periods beginning on or after1January2013.Earlier application is permitted.Reasons for issuing the IFRSIN3Users of financial statements have consistently requested improvements to the disclosure of a reporting entity’s interests in other entities to help identify theprofit or loss and cash flows available to the reporting entity and determine thevalue of a current or future investment in the reporting entity.IN4They highlighted the need for better information about the subsidiaries that are consolidated,as well as an entity’s interests in joint arrangements and associatesthat are not consolidated but with which the entity has a special relationship.IN5The global financial crisis that started in2007also highlighted a lack of transparency about the risks to which a reporting entity was exposed from itsinvolvement with structured entities,including those that it had sponsored.IN6In response to input received from users and others,including the G20leaders and the Financial Stability Board,the Board decided to address in IFRS12theneed for improved disclosure of a reporting entity’s interests in other entitieswhen the reporting entity has a special relationship with those other entities.IN7The Board identified an opportunity to integrate and make consistent the disclosure requirements for subsidiaries,joint arrangements,associates andunconsolidated structured entities and present those requirements in a singleIFRS.The Board observed that the disclosure requirements of IAS27Consolidatedand Separate Financial Statements,IAS28Investments in Associates and IAS31Interestsin Joint Ventures overlapped in many areas.In addition,many commented thatthe disclosure requirements for interests in unconsolidated structured entitiesshould not be located in a consolidation standard.Therefore,the Boardconcluded that a combined disclosure standard for interests in other entitieswould make it easier to understand and apply the disclosure requirements forsubsidiaries,joint ventures,associates and unconsolidated structured entities. Main features of the IFRSIN8The IFRS requires an entity to disclose information that enables users of financial statements to evaluate:(a)the nature of,and risks associated with,its interests in other entities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.IFRS Foundation A509IFRS12General requirementsIN9The IFRS establishes disclosure objectives according to which an entity discloses information that enables users of its financial statements(a)to understand:(i)the significant judgements and assumptions(and changes tothose judgements and assumptions)made in determining thenature of its interest in another entity or arrangement(iecontrol,joint control or significant influence),and indetermining the type of joint arrangement in which it has aninterest;and(ii)the interest that non-controlling interests have in the group’sactivities and cash flows;and(b)to evaluate:(i)the nature and extent of significant restrictions on its ability toaccess or use assets,and settle liabilities,of the group;(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities;(iii)the nature and extent of its interests in unconsolidatedstructured entities,and the nature of,and changes in,the risksassociated with those interests;(iv)the nature,extent and financial effects of its interests in jointarrangements and associates,and the nature of the risksassociated with those interests;(v)the consequences of changes in a parent’s ownership interest in asubsidiary that do not result in a loss of control;and(vi)the consequences of losing control of a subsidiary during thereporting period.IN10The IFRS specifies minimum disclosures that an entity must provide.If the minimum disclosures required by the IFRS are not sufficient to meet thedisclosure objective,an entity discloses whatever additional information isnecessary to meet that objective.IN11The IFRS requires an entity to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of therequirements in the IFRS.An entity shall aggregate or disaggregate disclosuresso that useful information is not obscured by either the inclusion of a largeamount of insignificant detail or the aggregation of items that have differentcharacteristics.IN12Investment Entities(Amendments to IFRS10,IFRS12and IAS27),issued in October 2012,introduced an exception to the principle in IFRS10Consolidated FinancialStatements that all subsidiaries shall be consolidated.The amendments define aninvestment entity and require a parent that is an investment entity to measureits investment in particular subsidiaries at fair value through profit or loss inaccordance with IFRS9Financial Instruments(or IAS39Financial Instruments: A510IFRS FoundationIFRS12Recognition and Measurement,if IFRS9has not yet been adopted)instead of consolidating those subsidiaries in its consolidated and separate financial statements.Consequently,the amendments also introduced new disclosure requirements for investment entities in this IFRS and IAS27Separate Financial Statements.IFRS Foundation A511IFRS12International Financial Reporting Standard12Disclosure of Interests in Other EntitiesObjective1The objective of this IFRS is to require an entity to disclose information that enables users of its financial statements to evaluate:(a)the nature of,and risks associated with,its interests in otherentities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.Meeting the objective2To meet the objective in paragraph1,an entity shall disclose:(a)the significant judgements and assumptions it has made in determining:(i)the nature of its interest in another entity or arrangement;(ii)the type of joint arrangement in which it has an interest(paragraphs7–9);(iii)that it meets the definition of an investment entity,if applicable(paragraph9A);and(b)information about its interests in:(i)subsidiaries(paragraphs10–19);(ii)joint arrangements and associates(paragraphs20–23);and(iii)structured entities that are not controlled by the entity(unconsolidated structured entities)(paragraphs24–31).3If the disclosures required by this IFRS,together with disclosures required by other IFRSs,do not meet the objective in paragraph1,an entity shall disclosewhatever additional information is necessary to meet that objective.4An entity shall consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the requirements in thisIFRS.It shall aggregate or disaggregate disclosures so that useful information isnot obscured by either the inclusion of a large amount of insignificant detail orthe aggregation of items that have different characteristics(see paragraphsB2–B6).Scope5This IFRS shall be applied by an entity that has an interest in any of the following:(a)subsidiaries(b)joint arrangements(ie joint operations or joint ventures)A512IFRS FoundationIFRS12(c)associates(d)unconsolidated structured entities.6This IFRS does not apply to:(a)post-employment benefit plans or other long-term employee benefitplans to which IAS19Employee Benefits applies.(b)an entity’s separate financial statements to which IAS27SeparateFinancial Statements applies.However,if an entity has interests inunconsolidated structured entities and prepares separate financialstatements as its only financial statements,it shall apply therequirements in paragraphs24–31when preparing those separatefinancial statements.(c)an interest held by an entity that participates in,but does not have jointcontrol of,a joint arrangement unless that interest results in significantinfluence over the arrangement or is an interest in a structured entity.(d)an interest in another entity that is accounted for in accordance withIFRS9Financial Instruments.However,an entity shall apply this IFRS:(i)when that interest is an interest in an associate or a joint venturethat,in accordance with IAS28Investments in Associates and JointVentures,is measured at fair value through profit or loss;or(ii)when that interest is an interest in an unconsolidated structuredentity.Significant judgements and assumptions7An entity shall disclose information about significant judgements and assumptions it has made(and changes to those judgements andassumptions)in determining:(a)that it has control of another entity,ie an investee as described inparagraphs5and6of IFRS10Consolidated Financial Statements;(b)that it has joint control of an arrangement or significant influenceover another entity;and(c)the type of joint arrangement(ie joint operation or joint venture)when the arrangement has been structured through a separate vehicle.8The significant judgements and assumptions disclosed in accordance with paragraph7include those made by the entity when changes in facts andcircumstances are such that the conclusion about whether it has control,jointcontrol or significant influence changes during the reporting period.9To comply with paragraph7,an entity shall disclose,for example,significant judgements and assumptions made in determining that:(a)it does not control another entity even though it holds more than half ofthe voting rights of the other entity.(b)it controls another entity even though it holds less than half of thevoting rights of the other entity.IFRS Foundation A513IFRS12(c)it is an agent or a principal(see paragraphs B58–B72of IFRS10).(d)it does not have significant influence even though it holds20per cent ormore of the voting rights of another entity.(e)it has significant influence even though it holds less than20per cent ofthe voting rights of another entity.Investment entity status9A When a parent determines that it is an investment entity in accordance with paragraph27of IFRS10,the investment entity shall discloseinformation about significant judgements and assumptions it has made indetermining that it is an investment entity.If the investment entity does nothave one or more of the typical characteristics of an investment entity(seeparagraph28of IFRS10),it shall disclose its reasons for concluding that it isnevertheless an investment entity.9B When an entity becomes,or ceases to be,an investment entity,it shall disclose the change of investment entity status and the reasons for the change.Inaddition,an entity that becomes an investment entity shall disclose the effect ofthe change of status on the financial statements for the period presented,including:(a)the total fair value,as of the date of change of status,of the subsidiariesthat cease to be consolidated;(b)the total gain or loss,if any,calculated in accordance withparagraph B101of IFRS10;and(c)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in subsidiaries10An entity shall disclose information that enables users of its consolidated financial statements(a)to understand:(i)the composition of the group;and(ii)the interest that non-controlling interests have in thegroup’s activities and cash flows(paragraph12);and(b)to evaluate:(i)the nature and extent of significant restrictions on itsability to access or use assets,and settle liabilities,of thegroup(paragraph13);(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities(paragraphs14–17);(iii)the consequences of changes in its ownership interest in asubsidiary that do not result in a loss of control(paragraph18);andA514IFRS FoundationIFRS12(iv)the consequences of losing control of a subsidiary duringthe reporting period(paragraph19).11When the financial statements of a subsidiary used in the preparation of consolidated financial statements are as of a date or for a period that is differentfrom that of the consolidated financial statements(see paragraphs B92and B93of IFRS10),an entity shall disclose:(a)the date of the end of the reporting period of the financial statements ofthat subsidiary;and(b)the reason for using a different date or period.The interest that non-controlling interests have in thegroup’s activities and cash flows12An entity shall disclose for each of its subsidiaries that have non-controlling interests that are material to the reporting entity:(a)the name of the subsidiary.(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary.(c)the proportion of ownership interests held by non-controlling interests.(d)the proportion of voting rights held by non-controlling interests,ifdifferent from the proportion of ownership interests held.(e)the profit or loss allocated to non-controlling interests of the subsidiaryduring the reporting period.(f)accumulated non-controlling interests of the subsidiary at the end of thereporting period.(g)summarised financial information about the subsidiary(seeparagraph B10).The nature and extent of significant restrictions13An entity shall disclose:(a)significant restrictions(eg statutory,contractual and regulatoryrestrictions)on its ability to access or use the assets and settle theliabilities of the group,such as:(i)those that restrict the ability of a parent or its subsidiaries totransfer cash or other assets to(or from)other entities within thegroup.(ii)guarantees or other requirements that may restrict dividendsand other capital distributions being paid,or loans and advancesbeing made or repaid,to(or from)other entities within thegroup.(b)the nature and extent to which protective rights of non-controllinginterests can significantly restrict the entity’s ability to access or use theassets and settle the liabilities of the group(such as when a parent isobliged to settle liabilities of a subsidiary before settling its ownIFRS Foundation A515IFRS12liabilities,or approval of non-controlling interests is required either toaccess the assets or to settle the liabilities of a subsidiary).(c)the carrying amounts in the consolidated financial statements of theassets and liabilities to which those restrictions apply.Nature of the risks associated with an entity’s interestsin consolidated structured entities14An entity shall disclose the terms of any contractual arrangements that could require the parent or its subsidiaries to provide financial support to aconsolidated structured entity,including events or circumstances that couldexpose the reporting entity to a loss(eg liquidity arrangements or credit ratingtriggers associated with obligations to purchase assets of the structured entity orprovide financial support).15If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to aconsolidated structured entity(eg purchasing assets of or instruments issued bythe structured entity),the entity shall disclose:(a)the type and amount of support provided,including situations in whichthe parent or its subsidiaries assisted the structured entity in obtainingfinancial support;and(b)the reasons for providing the support.16If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to apreviously unconsolidated structured entity and that provision of supportresulted in the entity controlling the structured entity,the entity shall disclosean explanation of the relevant factors in reaching that decision.17An entity shall disclose any current intentions to provide financial or other support to a consolidated structured entity,including intentions to assist thestructured entity in obtaining financial support.Consequences of changes in a parent’s ownershipinterest in a subsidiary that do not result in a loss ofcontrol18An entity shall present a schedule that shows the effects on the equity attributable to owners of the parent of any changes in its ownership interest in asubsidiary that do not result in a loss of control.Consequences of losing control of a subsidiary duringthe reporting period19An entity shall disclose the gain or loss,if any,calculated in accordance with paragraph25of IFRS10,and:(a)the portion of that gain or loss attributable to measuring any investmentretained in the former subsidiary at its fair value at the date whencontrol is lost;andA516IFRS FoundationIFRS12(b)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in unconsolidated subsidiaries(investment entities)19A An investment entity that,in accordance with IFRS10,is required to apply the exception to consolidation and instead account for its investment in a subsidiaryat fair value through profit or loss shall disclose that fact.19B For each unconsolidated subsidiary,an investment entity shall disclose:(a)the subsidiary’s name;(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary;and(c)the proportion of ownership interest held by the investment entity and,if different,the proportion of voting rights held.19C If an investment entity is the parent of another investment entity,the parent shall also provide the disclosures in19B(a)–(c)for investments that arecontrolled by its investment entity subsidiary.The disclosure may be providedby including,in the financial statements of the parent,the financial statementsof the subsidiary(or subsidiaries)that contain the above information.19D An investment entity shall disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements)on the ability of an unconsolidated subsidiary to transferfunds to the investment entity in the form of cash dividends or to repayloans or advances made to the unconsolidated subsidiary by theinvestment entity;and(b)any current commitments or intentions to provide financial or othersupport to an unconsolidated subsidiary,including commitments orintentions to assist the subsidiary in obtaining financial support.19E If,during the reporting period,an investment entity or any of its subsidiaries has,without having a contractual obligation to do so,provided financial orother support to an unconsolidated subsidiary(eg purchasing assets of,orinstruments issued by,the subsidiary or assisting the subsidiary in obtainingfinancial support),the entity shall disclose:(a)the type and amount of support provided to each unconsolidatedsubsidiary;and(b)the reasons for providing the support.19F An investment entity shall disclose the terms of any contractual arrangements that could require the entity or its unconsolidated subsidiaries to providefinancial support to an unconsolidated,controlled,structured entity,includingevents or circumstances that could expose the reporting entity to a loss(egliquidity arrangements or credit rating triggers associated with obligations topurchase assets of the structured entity or to provide financial support).IFRS Foundation A517IFRS1219G If during the reporting period an investment entity or any of its unconsolidated subsidiaries has,without having a contractual obligation to do so,providedfinancial or other support to an unconsolidated,structured entity that theinvestment entity did not control,and if that provision of support resulted inthe investment entity controlling the structured entity,the investment entityshall disclose an explanation of the relevant factors in reaching the decision toprovide that support.Interests in joint arrangements and associates20An entity shall disclose information that enables users of its financial statements to evaluate:(a)the nature,extent and financial effects of its interests in jointarrangements and associates,including the nature and effects of itscontractual relationship with the other investors with joint control of,or significant influence over,joint arrangements and associates(paragraphs21and22);and(b)the nature of,and changes in,the risks associated with its interestsin joint ventures and associates(paragraph23).Nature,extent and financial effects of an entity’sinterests in joint arrangements and associates21An entity shall disclose:(a)for each joint arrangement and associate that is material to thereporting entity:(i)the name of the joint arrangement or associate.(ii)the nature of the entity’s relationship with the joint arrangementor associate(by,for example,describing the nature of theactivities of the joint arrangement or associate and whether theyare strategic to the entity’s activities).(iii)the principal place of business(and country of incorporation,ifapplicable and different from the principal place of business)ofthe joint arrangement or associate.(iv)the proportion of ownership interest or participating share heldby the entity and,if different,the proportion of voting rightsheld(if applicable).(b)for each joint venture and associate that is material to the reportingentity:(i)whether the investment in the joint venture or associate ismeasured using the equity method or at fair value.(ii)summarised financial information about the joint venture orassociate as specified in paragraphs B12and B13.A518IFRS FoundationIFRS12(iii)if the joint venture or associate is accounted for using the equitymethod,the fair value of its investment in the joint venture orassociate,if there is a quoted market price for the investment.(c)financial information as specified in paragraph B16about the entity’sinvestments in joint ventures and associates that are not individuallymaterial:(i)in aggregate for all individually immaterial joint ventures and,separately,(ii)in aggregate for all individually immaterial associates.21A An investment entity need not provide the disclosures required by paragraphs21(b)–21(c).22An entity shall also disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements between investors with joint control of or significantinfluence over a joint venture or an associate)on the ability of jointventures or associates to transfer funds to the entity in the form of cashdividends,or to repay loans or advances made by the entity.(b)when the financial statements of a joint venture or associate used inapplying the equity method are as of a date or for a period that isdifferent from that of the entity:(i)the date of the end of the reporting period of the financialstatements of that joint venture or associate;and(ii)the reason for using a different date or period.(c)the unrecognised share of losses of a joint venture or associate,both forthe reporting period and cumulatively,if the entity has stoppedrecognising its share of losses of the joint venture or associate whenapplying the equity method.Risks associated with an entity’s interests in jointventures and associates23An entity shall disclose:(a)commitments that it has relating to its joint ventures separately fromthe amount of other commitments as specified in paragraphs B18–B20.(b)in accordance with IAS37Provisions,Contingent Liabilities and ContingentAssets,unless the probability of loss is remote,contingent liabilitiesincurred relating to its interests in joint ventures or associates(includingits share of contingent liabilities incurred jointly with other investorswith joint control of,or significant influence over,the joint ventures orassociates),separately from the amount of other contingent liabilities.IFRS Foundation A519。

香港会计准则与国际会计准则对照表

Comparison of Hong Kong Accounting Standards with International Accounting Standards (IASs)/ International Financial Reporting Standards (IFRSs)for the June 2006 examinationsHKG document TitleINTdocumentTitleExaminablePaper(s)Preface to Hong Kong Financial Reporting Standards 1.1, 2.5, 2.6, 3.13.6Framework for the Preparation and Presentation of Financial Statements Framework for the Preparation and Presentation of Financial Statements 1.1 (Note 5), 2.5,2.6,3.1, 3.6HKAS 1 Presentation of Financial Statements IAS 1Presentation of Financial Statements 1.1, 2.5, 2.6, 3.1, 3.6HKAS 1 Amendment Capital Disclosures 1.1, 2.5, 2.6, 3.1,3.6HKAS 2 Inventories IAS 2 Inventories 1.1, 2.5, 2.6, 3.1,3.6HKAS 7 Cash Flow Statements IAS 7 Cash Flow Statements 1.1 (Note 1), 2.5(Note 1), 2.6, 3.1,3.6HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors 1.1, 2.5, 2.6, 3.1,3.6HKAS 10 Events After the Balance Sheet Date IAS 10Events After the Balance Sheet Date 1.1, 2.5, 2.6, 3.1, 3.6HKAS 11 Construction Contracts IAS 11 Construction Contracts 2.5, 2.6, 3.1, 3.6 HKAS 12 Income Taxes IAS 12 Income Taxes 2.5, 2.6, 3.1, 3.6 HKAS 14 Segment Reporting IAS 14 Segment Reporting 2.5, 2.6, 3.1, 3.6HKAS 16 Property, Plant and EquipmentIAS 16 Property, Plant and Equipment 1.1, 2.5, 2.6, 3.1, 3.6HKAS 17 Leases IAS 17 Leases 2.5, 2.6, 3.1, 3.6HKAS 18 RevenueIAS 18 Revenue 1.1, 2.5, 2.6, 3.1,3.6HKAS 19 Employee Benefits IAS 19 Employee Benefits 3.6HKAS19 Amendment Employee Benefits – Actuarial Gains and Losses, Group Plans andDisclosures3.6HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance IAS 20Accounting for Government Grants and Disclosure of GovernmentAssistance2.5, 2.6,3.1, 3.6HKAS 21 The Effects of Changes in Foreign Exchange Rates IAS 21 The Effects of Changes in Foreign Exchange Rates 3.6HKAS 23 Borrowing Costs IAS 23 Borrowing Costs 2.5, 2.6, 3.1, 3.6 HKAS 24 Related Party Disclosures IAS 24 Related Party Disclosures 2.5, 2.6, 3.1, 3.6 HKAS 27 Consolidated and Separate Financial Statements IAS 27 Consolidated and Separate Financial Statements 2.5, 2.6, 3.1, 3.6HKAS 28 Investments in AssociatesIAS 28 Investments in Associates2.5, 2.6,3.1, 3.6HKAS 29 Financial Reporting in Hyperinflationary Economies IAS 29 Financial Reporting in Hyperinflationary Economies 3.6HKAS 31 Investments in Joint Ventures IAS 31 Interests in Joint Ventures 2.5, 2.6, 3.1, 3.6 HKAS 32 Financial Instruments: Disclosure and Presentation IAS 32 Financial Instruments: Disclosure and Presentation 2.5, 2.6, 3.1, 3.6 HKAS 33 Earnings per Share IAS 33 Earnings per Share 2.5, 2.6, 3.1, 3.6HKAS 34 Interim Financial Reporting IAS 34 Interim Financial Reporting 3.6HKAS 36 Impairment of Assets IAS 36 Impairment of Assets 2.5, 2.6, 3.1, 3.6HKAS 37 Provisions, Contingent Liabilities and Contingent Assets IAS 37 Provisions, Contingent Liabilities and Contingent Assets 1.1 (Note 2), 2.5,2.6,3.1, 3.6HKAS 38 Intangible Assets IAS 38 Intangible Assets 1.1 (Note 3), 2.5,2.6,3.1, 3.6HKAS 39 Financial Instruments: Recognition and Measurement IAS 39 Financial Instruments: Recognition and Measurement 2.5, 2.6, 3.1, 3.6HKAS 39 Amendment Transition and Initial Recognition of Financial Assets and FinancialLiabilities2.5, 2.6,3.1 ,3.6HKAS 39AmendmentCash Flow Hedge Accounting of Forecast Intragroup Transactions 2.5, 2.6, 3.1 ,3.6 HKAS 39AmendmentThe Fair Value Option 2.5, 2.6, 3.1 ,3.6HKAS 39 & HKFRS 4 Amendment Financial Instruments: Recognition and Measurement and InsuranceContracts – Financial Guarantee Contracts2.5, 2.6,3.1 ,3.6(HKFRS 4 Amend3.6 only)HKAS 40 Investment Property IAS 40 Investment Property 2.5, 2.6, 3.1, 3.6HKAS 41 Agriculture IAS 41 Agriculture 3.6 HKFRS 1 First-time adoption of Hong Kong Financial Reporting Standards IFRS 1 First –time adoption of International Financial Reporting Standards 2.5, 2.6, 3.1, 3.6HKFRS 1 & 6 Amendment First-time Adoption of Hong Kong Financial Reporting Standards andExploration for and Evaluation of Mineral Resources2.5, 2.6,3.1, 3.6(HKFRS 6 Amend3.6 only)HKFRS 2 Share-based Payment IFRS 2 Share-based Payment 3.6HKFRS 3 Business Combinations IFRS 3 Business Combinations 1.1 (Note 6), 2.5,2.6,3.1, 3.6 HKFRS 4 Insurance Contracts IFRS 4 Insurance Contracts 3.6HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations IFRS 5 Non-current Assets Held for Sale and Discontinued Operations 1.1 (Note 4), 2.5,2.6,3.1, 3.6 HKFRS 7 Financial Instruments: Disclosures IFRS 7 Financial Instruments: Disclosures 2.5, 2.6, 3.1, 3.6 HKFRS 6 Exploration for and Evaluation of Mineral Resources IFRS 6 Exploration for and Evaluation of Mineral Resources 3.6HK-INT 3 Revenue – Pre Completion Contracts for the Sale of DevelopmentProperties2.5, 2.6,3.1, 3.6 HK-INT 4 Leases – Determination of The Length of Lease Term in respect of HongKong Land Leases2.5, 2.6,3.1, 3.6 HKAS-INT 10 Government Assistance – No Specific Relation to Operating Activites SIC 10 Government assistance – No specific relation to operating activities 2.5, 2.6, 3.1, 3.6 HKAS-Int 12 Consolidation – Special Purpose Entities SIC 12 Consolidation – Special Purpose Entities 3.6HKAS-Int 12 Amendment Scope of HKAS-Int 12 Consolidation – Special Purpose Entities3.6HKAS-Int 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers SIC 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers 3.6 HKAS-Int 15 Operating Leases – Incentives SIC 15 Operating Leases – Incentives 3.6 HKAS-Int 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets SIC 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets 3.6HKAS-Int 25 Income Taxes – Changes in the Tax Status of an Enterprise or Its Shareholders SIC 25 Income Taxes – Changes in the Tax Status of an Enterprise or ItsShareholders3.6HKAS-Int 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease SIC 27 Evaluating the Substance of Transactions In the Legal Form of a Lease3.6HKAS-Int 29 Disclosure – Service Concession Arrangements SIC 29 Disclosure – Service Concession Arrangements 3.6HKAS-Int 31 Revenue – Barter Transactions Involving Advertising Services SIC 31 Revenue – Barter Transactions Involving Advertising Services 3.6HKAS-Int 32 Intangible Assets – Web Site Costs SIC 32 Intangible Assets – Web Site Costs 3.6HKFRS-Int 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities 3.6HKFRS-Int 4 Determining Whether an Arrangement contains a Lease IFRIC 4 Determining Whether an Arrangement contains a Lease 2.5, 2.6, 3.1, 3.6HKFRS-Int 5 Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds IFRIC 5 Rights to Interests arising from Decommissioning, Restoration andEnvironmental Funds3.6 IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies3.6 DP Preliminary Views on Accounting Standards for Small and Medium-sized Entities3.6 ED Proposed Amendment to IFRS 3, Business Combinations 3.6 ED Proposed Amendment to IAS 27, Consolidated and Separate FinancialStatements3.6 ED Proposed Amendment to IAS 37, Provisions, Contingent Liabilities andContingent Assets3.6 DP Measurement Bases for Financial Reporting – Measurement on InitialRecognition3.6 DP Management Commentary 3.6Notes1. Cash flow statements are examinable for 1.1 and2.5 but excluding group cash flow statements and cash flow statements including foreign currency.2. Examinable for 1.1 only to the extent of candidates providing definitions and simple calculations.3. Examinable for 1.1 only to cover basic knowledge of Research and Development and Goodwill.4. Examinable for 1.1 only to cover disclosures in relation to Discontinuing Operations.5. The Framework for the preparation of financial statements is examinable for 1.1 at an introductory level only.6. Examinable for 1.1 only to cover basic consolidation.。

ACCA-P2知识要点汇总

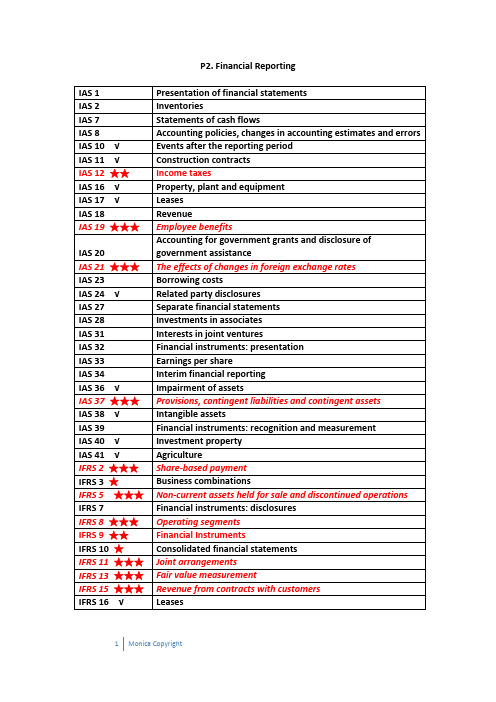

P2. Financial ReportingIAS 1 Presentation of financial statementsIAS 2 InventoriesIAS 7 Statements of cash flowsIAS 8 Accounting policies, changes in accounting estimates and errors IAS 10 √ Events after the reporting periodIAS 11 √ Construction contractsIAS 12 ★★ Income taxesIAS 16 √ Property, plant and equipmentIAS 17 √ LeasesIAS 18 RevenueIAS 19 ★★★ Employee benefitsIAS 20 Accounting for government grants and disclosure of government assistanceIAS 21 ★★★ The effects of changes in foreign exchange ratesIAS 23 Borrowing costsIAS 24 √ Related party disclosuresIAS 27 Separate financial statementsIAS 28 Investments in associatesIAS 31 Interests in joint venturesIAS 32 Financial instruments: presentationIAS 33 Earnings per shareIAS 34 Interim financial reportingIAS 36 √ Impairment of assetsIAS 37 ★★★ Provisions, contingent liabilities and contingent assetsIAS 38 √ Intangible assetsIAS 39 Financial instruments: recognition and measurementIAS 40 √ Investment propertyIAS 41 √ AgricultureIFRS 2 ★★★ Share‐based paymentIFRS 3 ★ Business combinationsIFRS 5 ★★★ Non‐current assets held for sale and discontinued operations IFRS 7 Financial instruments: disclosuresIFRS 8 ★★★ Operating segmentsIFRS 9 ★★ Financial InstrumentsIFRS 10 ★ Consolidated financial statementsIFRS 11 ★★★ Joint arrangementsIFRS 13 ★★★ Fair value measurementIFRS 15 ★★★ Revenue from contracts with customersIFRS 16 √ Leases不考or非重点:IAS 26 * Accounting and reporting by retirement benefit plans IAS 29 * Financial reporting in hyperinflationary economiesIAS 30 * Disclosure in the financial statements of banks and similar financial institutions (not examinable)IFRS 1* First time adoption of International Financial Reporting StandardsIFRS 4 * Insurance contractsIFRS 6 * Exploration for and evaluation of mineral resourcesIFRS 12* Disclosures of interests in other entitiesIFRS 14* Regulatory deferral accountsPart 1.The IASB’s Conceptual Framework for Financial Reporting1.财报的目的:The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit.2.财报提供的信息:General purpose financial reports do not and cannot provide all of the information,需要结合其他信息,譬如整个经济环境和预期,政治风向和事件,行业及公司展望等。

Lecture 7 Notes_Accounting for Interests in Joint Ventures_6 slides to a page

ACCT 2542 -Corporate Financial Reporting & Analysis Session 2, 2009Lecture Topic7Lecture Topic 7Accounting for Interests in Joint VenturesReading Materials⏹Deegan 5e: Chapter 34⏹Picker et al: Chapter 23, section 23.6.2, pages 974 to980 only⏹AASB 131 “Interests in Joint Ventures”Learning OutcomesBy the end of this topic, you should be able to:1.Explain the nature of joint ventures (“JV”)2.Identify the different forms of a joint venture3.Account for a venturer’s interest:•In a jointly controlled operation (“JCO”)•In a jointly controlled asset (“JCA”)•In a jointly controlled entity (“JCE”)What is a Joint Venture?JVs are a separate type of investment because they aredefined by a level of control that differs from thecontrol exerted over subsidiaries or associatesTwo or more"parent"companies agree to share capital,Two or more parent companies agree to share capital,technology, human resources, risks and rewards in aformation of a new entity under shared control.Joint venture From WikipediaA joint venture(often abbreviated JV) is a legal entity formed between two or more parties to undertake economic activity together. The parties agree to create a new entity by both contributing equity, and they then share in thed t l f th t i Threvenues, expenses, and control of the enterprise. The venture can be for one specific project only, or a continuing business relationship such as the Sony Ericsson joint venture. This is in contrast to a strategic alliance, which involves no equity stake by the participants, and is a muchless rigid arrangement.Investors in Joint Ventures⏹A JV is:“a contractual arrangement whereby two or more partiesundertake an economic activity that is subject to jointcontrol”⏹The parties sharing control are “venturers” whilst otherinvestors in the joint venture are referred to as “investors”Types of joint ventures⏹The form of and manner of accounting for the joint venturedepends on whether the joint control is:–Jointly controlled operations (like aircraft manufacture)J i tl t ll d t(lik il i li)–Jointly controlled assets (like an oil pipeline)–Jointly controlled entities (sharing the entity’s profits)•a separate entity is established–A company or a partnership or a trustMethods used by venturer to account for interests in JV⏹One-line method–One line in the venturer’s b/s, e.g. “Investment in JV”(Investment adjusted for contributions anddistributions)–Effectively the equity method -AASB 131 gives theoption of using the equity method for JCEsoption of using the equity method for JCEs⏹Line-by-line method–also known as proportional consolidation–venturer records proportionate share in assets,liabilities, revenues and expenses in its accounts–AASB 131 requires this method for JCOs/JCAs andgives this as the preferred method for JCEsIllustrationContribution in ABC’s books (in ‘000s)One line method:Dr Invsmt in JV 1,000Cr Cash1,000to record ABC’s contribution in Line-by-line method:Dr Cash in JV 1,000Cr Cash 1,000 to record ABC’s contributionto record ABC s contribution in the JV to record ABC s contributionas a one line controlaccountOne year later JCO accounts show the following detailsCash600,000Land750,000Explorations Costs -Mining leases500,000Explorations Costs -Salaries & benefits200,000Provision for Employee benefits( 50,000)Contributions from venturers$ 2,000,000Journal entries (in ‘000s) in ABC’s books a year laterOne line method:-no entry -Line-by-line method:Dr Cash (50% of $600K)300Dr Land (50% of $750K)375Dr Exp Costs -Min leases250Dr Exp Costs -Sal & Ben 100C P i i f E E tCr Provision for Emp Ent 25Cr Cash in JVO 1,000to replace one line control accountwith ABC’s 50% share in eachasset, liability and expensecomponent of the JVAccounting for jointly controlled operations•Each venturer recognises in its own statements its own assets& liabilities as well as its expenses and income share from thejoint ventureE h t it t l t d i t d•Each venturer uses its own property, plant and equipment andcarries own inventory•Venturer contributions toward costs are capitalised in a work-in-progress accountMotivations for formingJointly Controlled Operations⏹Venturer holds no equity in JCOs unlike in JCEs⏹Flexible -less regulation relative to a JCE⏹JCO is not a taxable entityVenturer is free to set up its own policies⏹Venturer is free to set up its own policies–Depreciation is recorded in investor’s rather than JV’s records ⏹JCO preferred over partnerships–avoid joint & several liability–avoid common taxation -each venturer may be in a differenttax situation to other venturersAccounting for jointly controlled assets•Venturer recognises in its financial statements:•Share of jointly controlled assets according to nature ofassetAny liabilities it incurs and share of liabilities incurred jointly•Any liabilities it incurs and share of liabilities incurred jointlywith other venturers relating to the JV•Any income from sale or use of its share of JV output withshare of expenses incurred by JV and any expenses itincurs regarding its interest in the JVAccounting by a venturer in an jointly controlled entity⏹A JCE involves establishing a separate structure in which eachventurer has an interest⏹The JCE controls the assets, incurs liabilities and expenses andearns income⏹Examples:–Two entities combine activities in a specific line of businessby transferring assets/liabilities into a JCE–Entity commences operations in a foreign country with thegovernment or other agency in that countryAccounting by a venturer in an jointly controlled entity (Continued)⏹JCE maintains own accounting records and prepares financialstatements in accordance with IFRSsE h t ll t ib t h th t⏹Each venturer usually contributes cash or other resources toJCE.⏹A venturer recognises its interest in a JCE using proportionateconsolidation or the equity method unless interest in JCE isheld for sale then account for in accordance with AASB 5.Accounting by a venturer in a jointly controlled entityAASB 131 allows either:⏹Proportionate consolidation–Choice of reporting format•Combine share of assets, liabilities, rev., and exp. of JCEwith similar items, line by line, in its f/s OR•Include separate line items for its share of assets,liabilities, rev., and exp. of the JCE in its f/s.OR⏹The equity method (i.e. records initial investment at cost andadjusts thereafter for post-acquisition change in venturer’sshare equity of JCE as per AASB 128)Motivations for forming Jointly Controlled Entities⏹Way of undertaking high risk, expensive and complexactivities with long gestation period⏹Allow venturers to share commercial and financial risks,resources and output⏹Foreign participationg p p⏹Restrictive foreign ownership⏹Common in industries such as:–Real estate development–Joint oil or gas drilling–Financing motion pictures–Research activityTransactions between a Venturer and a JV⏹Venturer must only recognise portion of gain/loss oncontribution/sale of asset to JV that is attributable to theinterests of other venturers.If venturer purchases asset from the JV share of profits can⏹If venturer purchases asset from the JV share of profits canonly be recognised when venturer resells asset to anindependent party.⏹Losses are recognised immediatelyLecture Illustration 1Transaction between venturersOn 1 July 20X8, Honey Ltd and Bee Ltd enter into a jointventure operation to search for pollen nestled in Wattleland.The JV agreement states that venturers share allcontributions, output and costs equally. On the same day, the venturers made the following contributions to the JV:Type Carrying Agreedamount valueHoney Ltd Cash$5,000$5,000Bee Ltd P & E4,000 5,000The plant and equipment is recorded in Bee’s records at a cost of $6,000 and accum depn of $2,000.What are the journal entries to record original contribution? (Assume equity method)Honey's Records Bee's recordsInv in JV DR 5,000 DR 4,500 Accum depn - P&E DR 2,000 p,Cash CR5,000Profit from sale of asset CR 500 Plant & Equipement CR 6,000 To record contribution in venturers respective books and part sale of non-current assets (net method) Disclosures required by AASB 131⏹Aggregate of•contingent liabilities and capital commitments⏹A listing and description of interests in significant JVs ⏹% of ownership interest held in JCEsAggregate amounts of each asset liability income and ⏹Aggregate amounts of each asset, liability, income andexpense related to interests in JVs⏹Accounting method used to recognise interests in JCEs。

IAS31

范围Scope本号准则适用于合营中权益的会计处理,以及在合营者和投资者的财务报表中对合营资产、负债、收入和费用的报告,而不论合营活动是在何种结构或形式下发生的。