外籍人个税计算要点英文版

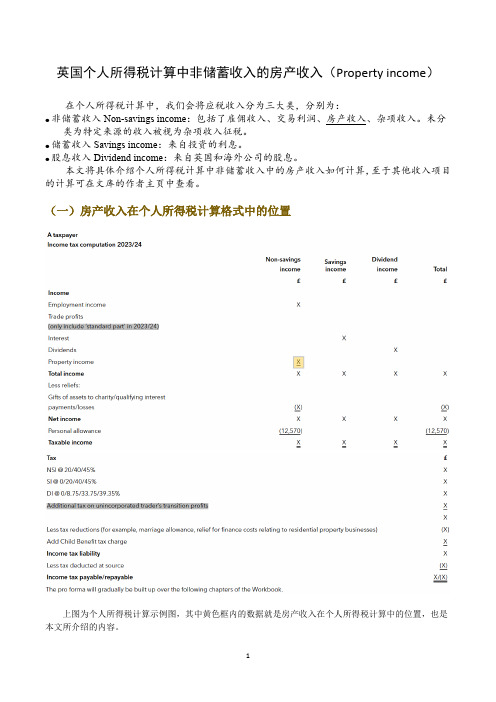

英国个人所得税计算中非储蓄收入的房产收入(Property income)

英国个人所得税计算中非储蓄收入的房产收入(Property income)在个人所得税计算中,我们会将应税收入分为三大类,分别为:●非储蓄收入Non-savings income:包括了雇佣收入、交易利润、房产收入、杂项收入。

未分类为特定来源的收入被视为杂项收入征税。

●储蓄收入Savings income:来自投资的利息。

●股息收入Dividend income:来自英国和海外公司的股息。

本文将具体介绍个人所得税计算中非储蓄收入中的房产收入如何计算,至于其他收入项目的计算可在文库的作者主页中查看。

(一)房产收入在个人所得税计算格式中的位置上图为个人所得税计算示例图,其中黄色框内的数据就是房产收入在个人所得税计算中的位置,也是本文所介绍的内容。

(二)房产收入介绍房产收入的税收:房产收入的税收通常是基于房东所获得的总租金收入来计算的。

具体而言,税收的计算方法取决于采用的会计基础:现金制和应计制两种方式。

-现金制(收付实现制)下,房东只有在实际收到租金时,才会把该部分租金收入计入税务申报,如果租金收入未及时收到,则不会影响当年的税务负担。

-应计制(权责发生制)下,无论租金是否已经实际收取,房东都需要在租赁合同规定的期间内,根据租金收入的确认时间来计算并申报税务。

因此,若房东在某一年已确认租金收入,但未实际收到款项,这部分收入仍然需要纳税。

可扣除的费用:在计算房产收入时,房东可扣除一些必要的支出,这些支出会减少应纳税的收入。

常见的可扣除费用包括:-更换家用物品的支出:如更换家具、电器、窗帘等用于出租物业的物品,这些支出可以作为费用在税务申报时扣除。

-财务费用:如果房东为购买或维护物业而借款,支付的贷款利息属于财务费用,通常也可以扣除。

同时,财务费用通常是根据基本税率享受税收减免,这意味着贷款利息等支出可以在计算应纳税收入时减去,从而减少税负。

亏损的处理:如果房东在某一年度的房产收入中出现亏损(即支出超过收入),这些亏损并不会立即导致税务减免。

个人所得税法英文版)

第15章个人所得税法Chapter 15 Individual Income Tax•Who are the individuals liable to Individual Income Tax?•What is the income from sources within China?•What is the income from sources outside China?•What income earned by an individual is subject to Individual Income Tax?•How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?•What does wage, salary income include specifically?•How are salaries and wages assessed for Individual Income Tax payable?•How is the “additional deduction for expenses”regulated for wages and salaries? •How to compute the income tax payable on the bonus income on the year-end in one payment?•How to compute the income tax payable on the income of welfare in kind?•How to compute the income tax payable on the income stock options of employees of enterprises?•How is severance pay taxed?•How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?•What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?•How to calculate the taxable income of individual Industrial and Commercial Households?•What are the rules concerning deductions for Individual Industrial and Commercial Households?•How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?•How do single proprietorship enterprises compute and pay income tax payable on their production and business income?•How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?•How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return from their investment?•How is income from contracted or leased operation of enterprises or institutions assessed for Individual Income Tax?•How is income from remuneration for personal service assessed for Individual Income Tax payable?•How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?•What expenses are not allowed for deductions for Individual Industrial and Commercial Households?•What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?•How to deduct the expenses concerning intangible assets used by Individual Industrial and Commercial Households?•How do Individual Industrial and Commercial Households compute their income tax payable?•How additional income tax is levied on remuneration income that is excessively high at one payment?•How is author’s remuneration income assessed for Individual Income Tax payable? •How is income from royalties assessed for Individual Income Tax payable?•How is income from lease of property assessed for Individual Income Tax payable? •How is income from transfer of property assessed for Individual Income Tax payable?•How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?•What do the interest, dividend, bonus, contingent income and/ or other income include specifically?•How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?•How to compute the income tax payable on income derived by two individuals or more together?•How is donation income assessed for Individual Income Tax payable?•How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?•How is income derived from sources outside China assessed for Individual Income Tax payable?•What are the main exemptions for Individual Income Tax?•What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?•What are the main reductions for Individual Income Tax?•What are the rules concerning the mode, time and places for Individual Income Tax payment?•How to report and pay income tax on wages and salaries income?•How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?•How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?•How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?•How to report and pay income tax on income earned by taxpayers from sources outside China?纳税义务人判定标准征税对象范围1.居民纳税人(负无限纳税义务)(1)在中国境内有住所的个人(2)在中国境内无住所,而在中国境内居住满一年的个人。

外籍人员个人所得税课件

税收协定

减免税

税收协定

一、定义: 两个或两个以上主权国家,为了协调相互之间的税收管辖 关系和处理有关税务问题,通过谈判缔结的书面协议。

二、适用范围: 1、人的范围: 仅适用于缔约国一方或双方的居民(法人、个人)。 2、税种的范围:所得和财产的税种

三、一般原则: 1、避免双重征税; 2、协定优于国内法; 3、对等互利:公平、公正得确认所得税征免

1、个人在中国境内外商投资企业中任职、受雇应取得的 工资、薪金,应由该外商投资企业支付。凡由于该外商投 资企业与境外企业存在关联关系,上述本应由外商投资企 业支付的工资、薪金中部分或全部由境外关联企业支付的, 对该部分由境外关联企业支付的工资、薪金,境内外商投 资企业仍应依照中华人民共和国个人所得税法的规定,据 实汇集申报有关资料,负责代扣代缴个人所得税。

1-5年

V

无住所

不满90天

V

(居民) 第6年以后 不满一年

V

满一年

V

境外所得 境外支付 境内支付 或负担 或负担

X X

V(高管)

X V

V(高管)

V

V

X

V(高管)

V

V(高管)

ห้องสมุดไป่ตู้

V

V

境外支付 或负担

X

国税发【19

X

94】148号、 国税函发

【1995】125

X 号、国税函 【2007】946

X号

X

V

三、纳税计算-----工资薪金所得

是指在一个纳税年度中一次不超过30日或者多次累计不超过90日的离 境)。 • 在中国境内居住的天数为实际在华逗留天数,入境、离境、往返及多次 往返的当日,均按照1天计算。

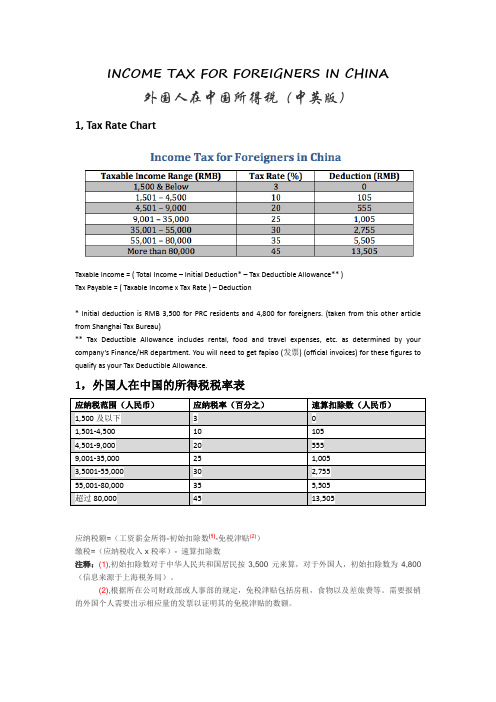

外国人税收方案INCOME TAX FOR FOREIGNERS IN CHINA

INCOME TAX FOR FOREIGNERS IN CHINA外国人在中国所得税(中英版)1, Tax Rate ChartTaxable Income = ( Total Income – Initial Deduction* – Tax Deductible Allowance** )Tax Payable = ( Taxable Income x Tax Rate ) – Deduction* Initial deduction is RMB 3,500 for PRC residents and 4,800 for foreigners. (taken from this other article from Shanghai Tax Bureau)** Tax Deductible Allowance includes rental, food and travel expenses, etc. as determined by your company’s Finance/HR department. You will need to get fapiao (发票) (official invoices) for these figures to qualify as your Tax Deductible Allowance.1,外国人在中国的所得税税率表应纳税范围(人民币)应纳税率(百分之)速算扣除数(人民币)1,500及以下 3 01,501-4,50010 1054,501-9,00020 5559,001-35,00025 1,0053,5001-55,00030 2,75555,001-80,00035 5,505超过80,00045 13,505应纳税额=(工资薪金所得-初始扣除数(1)-免税津贴(2))缴税=(应纳税收入x税率)- 速算扣除数注释:(1),初始扣除数对于中华人民共和国居民按3,500元来算,对于外国人,初始扣除数为4,800(信息来源于上海税务局)。

个人所得税缴纳说明(中英文版)

关于缴纳所得税的说明**同志2011年的年薪总收入为*****元,月平均收入****.**元。

2011年住房公积金和社保共****元允许税前扣除。

按照《中华人民共和国个人所得税法》2007年第五次修正版之规定,人员月平均收入2000元以内的不缴纳个人所得税,月平均收入超过额度的按照累进税率计缴个人所得税。

因此2011年已缴个人所得税****元,年薪净总收入*******元左右。

其计算公式如下:应缴纳个人所得税=([(年薪总收入-个税起征点×12个月-全年缴纳社保及住房公积金)/12个月]×税率-速算扣除数)×12个月。

2011年应缴个税为:*******(元)******公司2011年1月1日Explanation of Individual Income Tax CalculationIn 2011, the annual income of **** is RMB*****; then his average income isRMB***** per month. Meanwhile, social insurance and house fund is RMB****. According to Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China in 2007, tax threshold is RMB2000 per month and those amounts exceeding this will be tax payable. In 2011, ****’s total amount of tax payment was RMB****, and annual net income was RMB****.The calculation formula is as following:annual tax payable = {[(annual income –tax threshold × 12 months – annual social insurance and house fund ) / 12 months] ×tax rate - quick calculation deduction } × 12 months.tax payable in 2010:RMB************* Co., Ltd.1st , Jan. 2011When you are old and grey and full of sleep,And nodding by the fire, take down this book,And slowly read, and dream of the soft lookYour eyes had once, and of their shadows deep;How many loved your moments of glad grace,And loved your beauty with love false or true,But one man loved the pilgrim soul in you,And loved the sorrows of your changing face; And bending down beside the glowing bars, Murmur, a little sadly, how love fledAnd paced upon the mountains overheadAnd hid his face amid a crowd of stars.The furthest distance in the worldIs not between life and deathBut when I stand in front of youYet you don't know thatI love you.The furthest distance in the worldIs not when I stand in front of youYet you can't see my loveBut when undoubtedly knowing the love from both Yet cannot be together.The furthest distance in the worldIs not being apart while being in loveBut when I plainly cannot resist the yearningYet pretending you have never been in my heart.The furthest distance in the worldIs not struggling against the tidesBut using one's indifferent heartTo dig an uncrossable riverFor the one who loves you.倚窗远眺,目光目光尽处必有一座山,那影影绰绰的黛绿色的影,是春天的颜色。

个人所得税法英文版

from their institutions Individual 第 15 章 个人所得税法Chapter 15 Individual Income TaxWho are the individuals liable to Individual Income Tax? What is the income from sources within China? What is the income from sources outside China?What income earned by an individual is subject to Individual Income Tax?How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?What does wage, salary income include specifically?How are salaries and wages assessed for Individual Income Tax payable?How is the “ additional deduction for expenses ” regulated for wages and salaries? How to compute the income tax payable on the bonus income on the year-end in one payment?How to compute the income tax payable on the income of welfare in kind?How to compute the income tax payable on the income stock options of employees of enterprises? How is severance pay taxed?How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?How to calculate the taxable income of individual Industrial and CommercialHouseholds?What are the rules concerning deductions for Individual Industrial and Commercial Households? How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?How do single proprietorship enterprises compute and pay income tax payable on their production and business income?How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return investment? How is income from contracted or leased operation of enterprises or assessed for Individual Income Tax?How is income from remuneration for personal service assessedfor Income Tax payable? How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?What expenses are not allowed for deductions for Individual Industrial and Commercial Households?What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?How to deduct the expenses concerning intangible assets used by IndividualIndustrial and Commercial Households?How do Individual Industrial and Commercial Households compute their income tax payable? How additional income tax is levied on remuneration income that is excessively high at onepayment?How is author ' s remuneration income assessed for Individual Income Tax payable?How is income from royalties assessed for Individual Income Tax payable?How is income from lease of property assessed for Individual Income Tax payable?How is income from transfer of property assessed for Individual Income Tax payable?How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?What do the interest, dividend, bonus, contingent income and/ or other income include specifically?How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?How to compute the income tax payable on income derived by two individuals or more together? How is donation income assessed for Individual Income Tax payable?How to compute the income tax payable in case that the employers bear theIndividual Income Tax for the taxpayers?How is income derived from sources outside China assessed for Individual IncomeTax payable?What are the main exemptions for Individual Income Tax?What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?What are the main reductions for Individual Income Tax?What are the rules concerning the mode, time and places for Individual Income Tax payment? How to report and pay income tax on wages and salaries income?How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?How to report and pay income tax on income earned by taxpayers from sources outside China?税率 个丄八所得税法趙颔累进税率*九级、五级 比例税率;20^0(有加咸与減征)应纳税所得额规走Y J 纳税申报及缴纳代扣代缴L 两个判走标准厂纳税义筈兀1-居民纳税人与非居民纳税人划分应税所得项目’ 11个税目税收优惠境外所得已纳税额扣除’分国又分项计算扣除限额,差颔补税自行申扌艮 纳税义务人 判定标准 征税对象范围1.居民纳税人 (负无限纳税 义务) (1) 在中国境内有住所的个人(2) 在中国境内无住所,而在中国境内居住满一年的个 人。

外国人税收方案INCOME TAX FOR FOREIGNERS IN CHINA

INCOME TAX FOR FOREIGNERS IN CHINA外国人在中国所得税(中英版)1, Tax Rate ChartTaxable Income = ( Total Income – Initial Deduction* – Tax Deductible Allowance** )Tax Payable = ( Taxable Income x Tax Rate ) – Deduction* Initial deduction is RMB 3,500 for PRC residents and 4,800 for foreigners. (taken from this other article from Shanghai Tax Bureau)** Tax Deductible Allowance includes rental, food and travel expenses, etc. as determined by your company’s Finance/HR department. You will need to get fapiao (发票) (official invoices) for these figures to qualify as your Tax Deductible Allowance.1,外国人在中国的所得税税率表应纳税范围(人民币)应纳税率(百分之)速算扣除数(人民币)1,500及以下 3 01,501-4,50010 1054,501-9,00020 5559,001-35,00025 1,0053,5001-55,00030 2,75555,001-80,00035 5,505超过80,00045 13,505应纳税额=(工资薪金所得-初始扣除数(1)-免税津贴(2))缴税=(应纳税收入x税率)- 速算扣除数注释:(1),初始扣除数对于中华人民共和国居民按3,500元来算,对于外国人,初始扣除数为4,800(信息来源于上海税务局)。

个人所得税法(英文版)

第15章个人所得税法Chapter 15 Individual Income Tax•Who are the individuals liable to Individual Income Tax?•What is the income from sources within China?•What is the income from sources outside China?•What income earned by an individual is subject to Individual Income Tax? •How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?•What does wage, salary income include specifically?•How are salaries and wages assessed for Individual Income Tax payable? •How is the “additional deduction for expenses” regulated for wages and salaries?•How to compute the income tax payable on the bonus income on the year-end in one payment?•How to compute the income tax payable on the income of welfare in kind? •How to compute the income tax payable on the income stock options of employees of enterprises?•How is severance pay taxed?•How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?•What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?•How to calculate the taxable income of individual Industrial and Commercial Households?•What are the rules concerning deductions for Individual Industrial and Commercial Households?•How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?•How do single proprietorship enterprises compute and pay income tax payable on their production and business income?•How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?•How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return from their investment?•How is income from contracted or leased operation of enterprises or institutions assessed for Individual Income Tax?•How is income from remuneration for personal service assessed for Individual Income Tax payable?•How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?•What expenses are not allowed for deductions for Individual Industrial andCommercial Households?•What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?•How to deduct the expenses concerning intangible assets used by Individual Industrial and Commercial Households?•How do Individual Industrial and Commercial Households compute their income tax payable?•How additional income tax is levied on remuneration income that is excessively high at one payment?•How is author’s remuneration income assessed for Individual Income Tax payable?•How is income from royalties assessed for Individual Income Tax payable? •How is income from lease of property assessed for Individual Income Tax payable?•How is income from transfer of property assessed for Individual Income Tax payable?•How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?•What do the interest, dividend, bonus, contingent income and/ or other income include specifically?•How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?•How to compute the income tax payable on income derived by two individuals or more together?•How is donation income assessed for Individual Income Tax payable? •How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?•How is income derived from sources outside China assessed for Individual Income Tax payable?•What are the main exemptions for Individual Income Tax?•What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State? •What are the main reductions for Individual Income Tax?•What are the rules concerning the mode, time and places for Individual Income Tax payment?•How to report and pay income tax on wages and salaries income?•How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?•How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses? •How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?•How to report and pay income tax on income earned by taxpayers from sourcesoutside China?纳税义务人判定标准征税对象围1.居民纳税人(负无限纳税义务)(1)在中国境有住所的个人(2)在中国境无住所,而在中国境居住满一年的个人。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.Policy summary:

1)Days in China refers to the entry-departure history of your passport, both the entry date and departure will be deemed as half an day in China

Any 30 successive days or 90 days in total off China in a calendar year constitute a “less than 1 year”

For those foreign countries that reached double taxation agreement with China, 183 days is very important. (90 days for those not yet)

2)Days in China less than 183 days

a)Get paid from China, taxable;

b)Get paid from outside China, but relevant expense will finally be Charge back to Chinese enterprises, taxable;

c)Get paid from outside China and expense borne by foreign country, exempted from IIT in China.

When you are off China, those portion of incomes get paid from neither China or outside China will be exempted from IIT. This will be shown as a ratio in IIT calculating.

If a foreign guy now working in China luckily get paid from 3 party, A RMB from China, B RMB from HQ but will later charge back to the Chinese Company, and C RMB from another affiliate company that will not be borne by the Chinese company. (B and C RMB amount are foreign currency amount multiply month end exchange rate) And in Sep he has 12 days in China and the other 18 days off China.

then Calculation formula:

◆

Incomes get paid by either China or out

Tax to be calculated first for all incomes Determines the Ratio of taxable income out of total income

3)Days in China more than 183 days but less than one year

a)Get paid from China, taxable;

b)Get paid from outside China, taxable;

when you are off China, those portion of incomes get paid from neither China or outside China will be exempted from IIT.

Calculation formula:

◆

Incomes get paid by either China or out China when off China are tax free

Tax to be calculated first for all incomes All incomes get paid when stay in China will be taxable

4)Days in China more than one year but less than 5 years

a)Get paid from China, taxable;

b)Get paid from outside China, taxable;

when you are off China, those portion of incomes get paid from China will be charged with IIT while those paid from outside China will be exempted from IIT. Which is different from the said above 2 situations.

Calculation formula:

Only those portion of income get Tax to be calculated first for all incomes

5)Days in China more than one year but less than 5 years

a)Get paid from China, taxable;

b)Get paid from outside China, taxable;

c)No portion of income to be treated as tax free even for those days off China.。