Bodie2e_Chapter01 Financial Economics 英文版PPT金融学(第二版) 教学课件

金融经济学 Financial_Economics_2

Economic functions

• Primitive societies: investment financed by own savings • Modern societies: investment financed by others’ savings • Without financial markets and intermediaries, most investment would be unintended inventory accumulation

2. The future is uncertain

• Savers expect to earn interest, but are not certain to do so. • The greater the uncertainty, the less likely they are to save • In other words, the greater the uncertainty, the higher the interest rate needed to persuade them to save.

Asset A Price (A + B )

Asset B

Time

ห้องสมุดไป่ตู้

4.Risk taking (speculation)

• Some risks cannot be diversified away.

• But they can be transferred to speculators • For example, an airline can undertake a swap agreement on the price of jet fuel.

《金融学教学课件》bodie2e_chapter04

Future Value of $1000

3 ,0 0 0

2 ,5 0 0

2 ,0 0 0

1 ,5 0 0

1 ,0 0 0

500

0

0

2

4

6

8

10

12

14

16

Y ea rs 10

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• Investing $1 for yet another year promises to produce 1.10 *(1+10/100) or $1.21 in 2-years

5 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

6 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Value of $5 Invested

• More generally, with an investment of $5 at 10% we osh Flow for Number of Periods

FV PV * (1 i)n

FV (1 i)n PV

ln FV ln (1 i)n n *ln1 i PV

n

ln FV PV

ln1 i

lnFV lnPV ln1 i

19 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

PV

货币金融学(第十二版)英文版题库及答案Web chapter 1

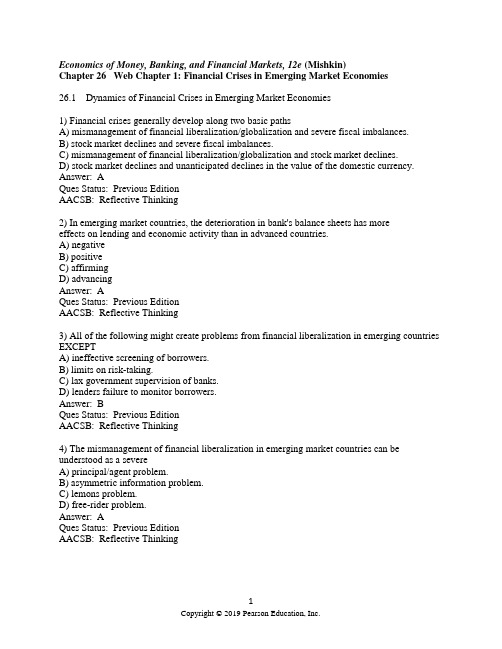

Economics of Money, Banking, and Financial Markets, 12e (Mishkin)Chapter 26 Web Chapter 1: Financial Crises in Emerging Market Economies26.1 Dynamics of Financial Crises in Emerging Market Economies1) Financial crises generally develop along two basic pathsA) mismanagement of financial liberalization/globalization and severe fiscal imbalances.B) stock market declines and severe fiscal imbalances.C) mismanagement of financial liberalization/globalization and stock market declines.D) stock market declines and unanticipated declines in the value of the domestic currency. Answer: AQues Status: Previous EditionAACSB: Reflective Thinking2) In emerging market countries, the deterioration in bank's balance sheets has more ________ effects on lending and economic activity than in advanced countries.A) negativeB) positiveC) affirmingD) advancingAnswer: AQues Status: Previous EditionAACSB: Reflective Thinking3) All of the following might create problems from financial liberalization in emerging countries EXCEPTA) ineffective screening of borrowers.B) limits on risk-taking.C) lax government supervision of banks.D) lenders failure to monitor borrowers.Answer: BQues Status: Previous EditionAACSB: Reflective Thinking4) The mismanagement of financial liberalization in emerging market countries can be understood as a severeA) principal/agent problem.B) asymmetric information problem.C) lemons problem.D) free-rider problem.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking5) Factors likely to cause a financial crisis in emerging market countries includeA) severe fiscal imbalances.B) decreases in foreign interest rates.C) a foreign exchange crisis.D) too strong oversight of the financial industry.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking6) The two key factors that trigger speculative attacks on emerging market currencies areA) deterioration in bank balance sheets and severe fiscal imbalances.B) deterioration in bank balance sheets and low interest rates abroad.C) low interest rates abroad and severe fiscal imbalances.D) low interest rates abroad and rising asset prices.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking7) Severe fiscal imbalances can directly trigger a currency crisis sinceA) investors fear that the government may not be able to pay back the debt and so begin to sell domestic currency.B) the government may stop printing money.C) the government may have to cut back on spending.D) the currency must surely increase in value.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking8) In emerging market countries, many firms have debt denominated in foreign currency like the dollar or yen. A depreciation of the domestic currencyA) results in increases in the firm's indebtedness in domestic currency terms, even though the value of their assets remains unchanged.B) results in an increase in the value of the firm's assets.C) means that the firm does not owe as much on their foreign debt.D) strengthens their balance sheet in terms of the domestic currency.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking9) A sharp depreciation of the domestic currency after a currency crisis leads toA) higher inflation.B) lower import prices.C) lower interest rates.D) decrease in the value of foreign currency-denominated liabilities.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking10) The key factor leading to the financial crises in Mexico and the East Asian countries wasA) a deterioration in banks' balance sheets because of increasing loan losses.B) severe fiscal imbalances.C) a sharp increase in the stock market.D) a sharp decline in interest rates.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge11) Factors that led to worsening conditions in Mexico's 1994-1995 financial markets includeA) failure of the Mexican oil monopoly.B) the ratification of the North American Free Trade Agreement.C) increased uncertainty from political shocks.D) decline in interest rates.Answer: CQues Status: Previous EditionAACSB: Application of Knowledge12) Factors that led to worsening financial market conditions in East Asia in 1997-1998 includeA) weak supervision by bank regulators.B) a rise in interest rates abroad.C) unanticipated increases in the price level.D) increased uncertainty from political shocks.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge13) Factors that led to worsening conditions in Mexico's 1994-1995 financial markets, but did not lead to worsening financial market conditions in East Asia in 1997-1998 includeA) rise in interest rates abroad.B) bankers' lack of expertise in screening and monitoring borrowers.C) deterioration of banks' balance sheets because of increasing loan losses.D) stock market decline.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge14) Argentina's financial crisis was due toA) poor supervision of the banking system.B) a lending boom prior to the crisis.C) fiscal imbalances.D) lack of expertise in screening and monitoring borrowers at banking institutions.Answer: CQues Status: Previous EditionAACSB: Application of Knowledge15) A feature of debt markets in emerging-market countries is that debt contracts are typicallyA) very short term.B) long term.C) intermediate term.D) perpetual.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking16) The economic hardship resulting from a financial crises is severe, however, there are also social consequences such asA) increased crime.B) difficulty getting a loan.C) currency devaluations.D) loss of output.Answer: AQues Status: Previous EditionAACSB: Reflective Thinking17) Before the South Korean financial crisis, sales by the top five chaebols (family-owned conglomerates) wereA) nearly 50% of GDP.B) about 10% of GDP.C) almost 90% of GDP.D) nearly 25% of GDP.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge18) The chaebols encouraged the Korean government to open up Korean financial markets to foreign capital. The Korean government responded byA) allowing unlimited short-term foreign borrowing but maintained quantity restrictions on long-term foreign borrowing by financial institutions.B) allowing unlimited short-term and long-term foreign borrowing by financial institutions.C) maintaining quantity restrictions on short-term foreign borrowing but allowing unlimited long-term foreign borrowing by financial institutions.D) not allowing any foreign borrowing by financial institutions.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge19) At the time of the South Korean financial crisis, the government allowed many chaebol owned finance companies to convert to merchant banks. Finance companies ________ allowed to borrow abroad and merchant banks ________.A) were not; could borrow abroadB) were not; could not borrow abroadC) were; could borrow abroadD) were; could not borrow abroadAnswer: AQues Status: Previous EditionAACSB: Application of Knowledge20) At the time of the South Korean financial crisis, the merchant banks wereA) almost virtually unregulated.B) subject to heavy government regulation.C) engaged in long-term lending to the corporate sector.D) restricted to long-term foreign borrowing.Answer: AQues Status: Previous EditionAACSB: Application of Knowledge21) What two key factors trigger speculative attacks leading to currency cries in emerging market countries?Answer: The deterioration in bank balance sheets and severe fiscal imbalances are the key factors. To counter a speculative attack, a country might try to raise interest rates. Raising interest rates, however, would worsen the problem of banks that are already in trouble. Speculators recognize this and seize the opportunity. When their are severe fiscal imbalances, there is concern that government debt will not be paid back. Funds are pulled out of the country and domestic currency is sold leading to a decline in the value of the domestic currency. Speculators will once again seize the opportunity.Ques Status: Previous EditionAACSB: Reflective Thinking。

滋维博迪 投资学Chap012

12-12

Figure 12.2 Pricing of Royal Dutch Relative to Shell (Deviation from Parity)

INVESTMENTS | BODIE, KANE, MARCUS

12-13

INVESTMENTS | BODIE, KANE, MARCUS

12-8

Figure 12.1 Prospect Theory

INVESTMENTS | BODIE, KANE, MARCUS

12-9

Limits to Arbitrage

• Behavioral biases would not matter if rational arbitrageurs could fully exploit the mistakes of behavioral investors. • Fundamental Risk:

CHAPTER 12

Behavioral Finance and Technical Analysis

INVESTMENTS | BODIE, KANE, MARCUS

McGraw-Hill/Irwin Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

INVESTMENTS | BODIE, KANE, MARCUS

D1 PV0 kg

12-16

Technical Analysis and Behavioral Finance

• Technical analysis attempts to exploit recurring and predictable patterns in stock prices.

布兰查德宏观经济学

Price of the one-year

bond:

$100 $P1t 1 i1t

Price of the two-year bond:

$100 $P2t (1i1t)(1ie1t1)

Chapter 15: Financial Markets and Expectations

The yield to maturity on a two-year bond, is closely approximated by:

i2t

1 2(i1t

i ) e 1t1

In words, the two-year interest rate is the average of the current one-year interest rate and next year’s expected one-year interest rate.

Given

$ P2t

$ Pe1t 1 1 i1t

and

$Pe1t1

$100 (1ie1t1)

,

then:

$100 $P2t (1i1t)(1ie1t1)

In words, the price of two-year bonds is the present value of the payment in two years— discounted using current and next year’s expected one-year interest rate.

The relation between maturity and yield is called the yield curve, or the term structure of interest rates.

《金融学教学课件》bodie2e_chapter03

The Income Statement

• Summarizes the profitability of a company

during a time period

$23.4 +30.0 -10.0 -30.0 +12.0 25.4

- Investment in new ppe *Cash flow from investing activities

பைடு நூலகம்

-90.0 -90.0

- Dividends paid +Increase in short-term debt *Cash flow from financing

– Focuses on a firm’s cash situation

• A firm may be profitable and short of cash

– Unlike the balance sheet and income statement, cash flow statements are independent of accounting methods

– Corporate Taxes

» Net income

9

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

GPC Income Statement for Year Ending 2xx1

Sales revenues Cost of goods sold *Gross margin

金融学第二版课后答案英文版中国人民大学Bodie2-IM-Ch01

金融学第二版课后答案英文版中国人民大学Bodie2_IM_Ch01CHAPTER 1 – Financial EconomicsEnd-of-Chapter ProblemsDefining Finance1. What are your main goals in life? How does finance play a part in achieving those goals? What are the major tradeoffs you face?SAMPLE ANSWER:Finish schoolGet good paying job which I likeGet married and have childrenOwn my own homeProvide for familyPay for children’s educationRetireHow Finance Plays a Role:SAMPLE ANSWER:Finance helps me pay for undergraduate and graduate education and helps me decide whether spending the money on graduate education will be a good investment decision or not.Higher education should enhance my earning power and ability to obtain a job I like.Once I am married and have children I will have additional financial responsibilities (dependents) and I will have to learn how to allocate resources among individuals in the household and learn how to set aside enough money to pay for emergencies, education, vacations etc. Finance also helps me understand how to manage risks such as for disability, life and health.Finance helps me determine whether the home I want to buyis a good value or not. The study of finance also helps me determine the cheapest source of financing for the purchase of that home.Finance helps me determine how much money I will have to save in order to pay for my children’s education as well as my own retirement.Major Tradeoffs:SAMPLE ANSWERSpend money now by going to college (and possibly graduate school) but presumably make more money once I graduate due to my higher education.Consume now and have less money saved for future expenditures such as for a house and/or car or save more money now but consume less than some of my friendsFinancial Decisions of Households2. What is your net worth? What have you included among your assets and your liabilities? Would you list the value of your potential lifetime earning power as an asset or liability? How does it compare in value to other assets you have listed?SAMPLE ANSWER:$ ____________ (very possibly negative at this point)Assets:Checking account balanceSavings account balanceFurniture/Jewelry (watch)Car (possibly)Liabilities:Student loansCredit card balanceIf renting, remainder of rental agreement (unless sublettingis a possibility)Car payments (possibly)Students typically don’t think about the high value of their potential lifetime earning power when calculating their net worth but for young people it is often their most valuable asset.3. How are the financial decisions faced by a single person living alone different from those faced by the head of a household with responsibility for several children of school age? Are the tradeoffs they have to make different, or will they evaluate the tradeoffs differently?A single person needs only to support himself and therefore can make every financial decision on his own. If he does not want health insurance (and is willing to bear the financial risks associated with that decision) then no one will be affected by that decision other than that single person. In addition, this person needs to make no decisions about allocating income among dependents. A single person is very mobile and can choose to live almost anywhere. The tradeoffs this individual makes generally concern issues of consuming (or spending) today versus saving for consumption tomorrow. Since this person is supporting only himself, the need to save now is less important than for the head of household discussed next.T he head of household with several children must share resources (income) among dependents. This individual must be prepared to deal with risk management issues such as how to be prepared for potential financial emergencies (such as a serious health problem experienced by a member of the family or home owners insurance in case of a fire or other mishap). Because there are more people in this household than with a single person, there are greater risks that someone will get sick or injured. Andbecause there are dependents, the wage earner(s) should think carefully about life and disability insurance. In addition, the family is not as mobile as the single individual. Because of the school age children, the family might want to live near “good schools” thinking that a stronger education will eventually help those children’s future well being and financial situation. Thus, the tradeoffs for the head of household are more complex: more money is needed to consume today (he or she needs to support more dependents), but a lot more money is also needed to save for future expenses such as education and housing and more money is needed for risk management such as life and disability insurance.4. Family A and family B both consist of a father, mother and two children of school age. In family A both spouses have jobs outside the home and earn a combined income of $100,000 per year. In family B, only one spouse works outside the home and earns $100,000 per year. How do the financial circumstances and decisions faced by the two families differ?With two wage earners, there is less risk of a total loss of family income due to unemployment or disability than there is in a single wage earning household. The single wage earning family will probably want more disability and life insurance than the two wage earning family. On the flip side, however, the two wage earning family may need to spend extra money on child care expenses if they need to pay someone to watch the children after school.5. Suppose we define financial independence as the ability to engage in the four basic household financial decisions without resort to the use of relative’s resources when making financing decisions. At what age should children be expected to becomefinancially independent?Students will have differing responses to this question depending upon their specific experiences and opinions. Most will probably say independence should come after finishing their education, and they have a significant flow of income.6. You are thinking of buying a car. Analyze the decision by addressing the following issues:a.Are there are other ways to satisfy your transportation requirements besides buying a car? Make a list ofall the alternatives and write down the pros and cons.Transportation Mode Pros ConsWalking ?Takes you directly where you wantto goNo out of pocket costsConvenient ?Takes a long time ?Destination may be too far Bicycle ?Takes you directly to where youwant to goNo out of pocket marginal costsConvenient ?Requires physical strength and endurance ?Destination may be too farBus ?InexpensiveReaches more distant destinations ?May not take you directly where you want to go ?Inconvenient schedules to go ?Many stops, not efficientSubway ?InexpensiveFast ?May not take you directly where you want to goLocal destinations only on limited networkTrain ?Reaches distant destinations ?Moderately expensiveMay not take you directly whereyou want to goAirplane ?Reaches distant destinationsFast ?Most expensiveWill not take you directly where you want to gob. What are the different ways you can finance the purchase of a car?F inance through a bank loan or lease, finance through a car dealer with a loan or a lease or finance the car out of your own savings.c. Obtain information from at least three different providers of automobile financing on the terms they offer.d. What criteria should you use in making your decision?Your decision will be to select the financing alternative that has the lowest cost to you.When analyzing the information, you should consider the following:Do you have the cash saved to make an outright purchase? What interest rate would you be giving up to make that purchase? Do you pay a different price for the car if you pay cash rather than finance?For differing loan plans, what is the down payment today? What are the monthly payments? For how long? What is the relevant interest rate you will be paying? Does the whole loan get paid through monthly payments or is there a balloon payment at the end? Are taxes and/or insurance payments included in the monthly payments? ?For differing lease plans, what is the down payment today? What are the monthly payments? For how long? Do you own the car at the end of the lease? If not, what does it cost to buy the car? Do you have to buy the car at the end of the lease or is it an option? Is there a charge if you decide not to buy the car? What relevant interest rate will you be paying? Are taxesand/or insurance payments included in the monthly payments? Are there mileage restrictions?7. Match each of the following examples with one of the four categories of basic types of household financial decisions.At the Safeway paying with your debit card rather than taking the time to write a checkDeciding to take the proceeds from your winning lottery ticket and use it to pay for an extended vacation on the Italian RivieraFollowing Hillary’s advice and selling your Microsoft shares to invest in pork belly futuresHelping your 15-year old son learn to drive by letting putting him behind the wheel on the back road into townTaking up the offer from the pool supply company to pay off your new hot tub with a 15-month loan with zero payments for the first three monthsThe first is the most difficult since in practice it is simply a cash transaction involving no financing. As such the purchase is a consumption decision only and the payment choice is not a financing decision. The second is also a consumption/saving decision. The third is an exchange of one financial asset for another and therefore an investment decision. The fourth is a risk-management decision since you have subjected yourself to increased risk that is not covered by insurance. The final example is a financing decision involving a loan to finance a purchase.Forms of Business Organization8. You are thinking of starting your own business, but have no money.a.Think of a business that you could start without having to borrow any money.A ny business that involves a student’s own personal service would be cheap to start up. For instance he or she could start a business running errands for others, walking their dogs, shopping etc. Along those same lines they could start some kind of consulting business. Both of these businesses could be run out of their dorm room or their own home and could be started with very little capital. If they wanted to hire additional workers, they would have to be paid on a commission basis to limit upfront expenses.b. Now think of a business that you would want to start if you could borrow any amount of money at the going market interest rate.Certainly there are many interesting businesses that could be started if one could finance 100% of the business with borrowed capital and no equity. Since you will be able to borrow 100% of the financing, you will be willing to take a lot greater risk than if you were investing your own money.c. What are the risks you would face in this business?[Answer is, of course, dependent on answer to question “b.”]d. Where can you get financing for your new business?Depending upon the size of the financing needed, students should be looking for both debt and equity financing. The sources of this financing ranges from individuals and credit cards (for very small sums) to banks, venture capitalists, public debt and equity markets, insurance companies and pension funds9. Choose an organization that is not a firm, such as a club or church group and list the most important financial decisions it has to make. What are the key tradeoffs the organization faces? What role do preferences play in choosing among alternatives?Interview the financial manager of the organization and check to see if he or she agrees with you.SAMPLE ANSWER:Local Church group. Most important financial decisions:Whether or not to repair damage done to church and grounds during last big hurricane (specifically repairing the leaking roof)What project to put off in order to pay for repair damageHow to pay for renovations to downstairs Sunday school roomsHow to increase member attendance and contributionsHow to organize and solicit volunteers for the annual Church Sale (largest fund raiser of the year)Key Tradeoffs and Preferences:C hurch group funds are severely limited, so the organization needs to prioritize expenses based upon cost and need. Not all projects that are needed will be undertaken due to the expense involved. An equally large amount of timewill be spent trying to raise financing since funds inflow is variable. Since not all projects can be financed, preferences of different important individuals (such as the pastor) take on great significance in the decision-making process.Market Discipline: Takeovers10. Challenge Question: While there are clear advantages to the separation of management from ownership of business enterprises, there is also a fundamental disadvantage in that it may be costly to align the goals of management with those of the owners. Suggest at least two methods, other than the takeover market, by which the conflict can be reduced, albeit at some cost.One way is to provide incentives for the managers so that they increase their pay when owners interests are improved. An example would be compensating managers with stock options, the value of which increase with the market value of shareholder’s int erests. A second method is to more closely monitor the behavior of the managers. Outside management consultants and auditors serve this role in part particularly to the extent that they report their findings to representatives from ownership groups. Both of these solutions assume the management cannot effectively deceive markets or consultant/auditors through misleading information or actions to inflate the market value of the ownership shares or there performance records.11. Challenge Question:Consider a poorly run local coffee shop with its prime location featuring a steady stream of potential clients passing by on their way to and from campus. How does the longtime disgruntled, sloppy and inefficient owner-manager of Cup-a-Joe survive and avoid disciplining from the takeover market? This is not a question about a misalignment of the goals of the owner(s) and manager(s) of a firm since we have explicitly said the firm is owner-managed. If in fact the coffee shop is mismanaged the potential exists for an outsider to purchase a controlling interest in the operation and put more efficient management into place if the purchase price does not exceed the value of profits to be generated by the efficiently managed firm. If the present owner chooses not to sell he must value the firm for more than the value of the profits generated by an efficiently managed firm. Therefore his position in the firm must generate for him non-pecuniary benefits, or benefits unrelated to the firm’s profitability and he is therefore not avalue maximizer. Perhaps he enjoys making fun of his clients or takes pride in his eclectic tastes in interior decorating. In any case the takeover market does discipline him in the sense that he will be forced to pay for his non-pecuniary benefits in the sense that he trades off profits.The same could be said of an owner-manager who lacks the required specialized skills to properly run the firm but never the less continues to operate the company inefficiently because he ‘likes’ the work!The Role of the Finance Specialist in a Corporation12. Which of the following tasks undertaken within a corporate office are likely to fall under the supervision of the treasurer? The controller?Arranging to extend a line of credit from a bankArranging with an investment bank for a foreign exchange transactionProducing a detailed analysis of the cost structure of the company’s alternative product linesTaking cash payments for company sales and purchasing U.S. Treasury BillsFiling quarterly statements with the Securities and Exchange CommissionThe first two and the fourth items are responsibilities of the treasurer while the third and fifth items fall under the workload of the controller’s office.Objectivesy Define finance.y Explain why finance is worth studying.y Introduce two of the main players in the world of finance—households and firms—and the kinds of financial decisions theymake. The other main players, financial intermediaries and government, are introduced in chapter 2.Contents1.1Defining Finance1.2Why Study Finance?1.3Financial Decisions of Households1.4Financial Decisions of Firms1.5Forms of Business Organization1.6Separation of Ownership and Management1.7The Goal of Management1.8Market Discipline: Takeovers1.9The Role of the Finance Specialist in a CorporationSummaryFinance is the study of how to allocate scarce resources over time. The two features that distinguish finance are that the costs and benefits of financial decisions are spread out over time and are usually not known with certainty in advance by either the decision maker or anybody else.A basic tenet of finance is that the ultimate function of the system is to satisfy people’s consumption preferences. Economic organizations such as firms and governments exist in order to facilitate the achievement of that ultimate function. Many financial decisions can be made strictly on the basis of improving the trade-offs available to people without knowledge of their consumption preferences.There are at least five good reasons to study finance:y To manage your personal resources.y To deal with the world of business.y To pursue interesting and rewarding career opportunities.y To make informed public choices as a citizen.y To expand your mind.The players in finance theory are households, business firms, financial intermediaries, and governments. Households occupy a special place in the theory because the ultimate function of the system is to satisfy the preferences of people, and the theory treats those preferences as given. Finance theory explains household behavior as an attempt to satisfy those preferences. The behavior of firms is viewed from the perspective of how it affects the welfare of households.Households face four basic types of financial decisions:y Saving decisions: How much of their current income should they save for the future?y Investment decisions: How should they invest the money they have saved?y Financing decisions: When and how should they use other people’s money to sa tisfy their wants and needs?y Risk-management decisions: How and on what terms should they seek to reduce the economic uncertainties they face or to take calculated risks?There are three main areas of financial decision making in a business: capital budgeting, capital structure, and working capital management.There are five reasons for separating the management from the ownership of a business enterprise: y Professional managers may be found who have a superior ability to run the business.y To achieve the efficient scale of a business the resources of many households may have to be pooled.y In an uncertain economic environment, owners will want to diversify their risks across many firms. Such efficient diversification is difficult to achieve without separation ofownership and management.y To achieve savings in the costs of gathering information.y The “learning curve” or “going concern” effect: When the owner is also the manager, the new owner has to learn the business from the former owner in order to manage it efficiently. If the owner is not the manager, then when the business is sold, the manager continues in place and works for the new owner.The corporate form is especially well suited to the separation of ownership and management of firms because it allows relatively frequent changes in owners by share transfer without affecting the operations of the firm.The primary goal of corporate management is to maximize shareholder wealth. It leads managers to make the same investment decisions that each of the individual owners would have made had they made the decisions themselves.A competitive stock market imposes a strong discipline on managers to take actions to maximize the market value of the firm’s shares.。

营运资金管理外文文献

1

Department of Accounting and Finance, Caleb University, Lagos, Nigeria, email: Barikem@

inventory costs, lost returns on excess cash holdings and receivables; and under investment with its attendant stock-out, illiquidity and bad debts costs; determine its working capital policies ensuring it improves corporate profitability; appraise investments in working capital using capital investment models, determining ahead the viability of such investment; and ascertain and compare working capital costs and benefits to determine the existence of gains if any before investment in the proposed working capital.

218

Working capital management efficiency and corporate profitability...

2 Theoretical framework and review of literature

2.1 Theoretical framework

《金融学教学课件》bodie2e_chapter09

10 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

16 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Ease of Use

• We have to introduce a simplifying

assumption that captures our understanding of dividend behavior

Ease of Use

• Estimating next year’s dividend is straightforward, but estimating next year’s price appears to be much more difficult

• The problem is that next year’s price is obtained (eventually) by estimating, and discounting, every future dividend

9.2 The Discounted Dividend Model

• A discounted dividend model is any

model that computes the value of a share of a stock as the present value of the expected future cash dividends

《金融学教学课件》bodie2e_chapter09.ppt

9.2 The Discounted Dividend Model

• A discounted dividend model is any

model that computes the value of a share of a stock as the present value of the expected future cash dividends

• If you decide to trade shares as odd lots

you will pay higher commissions • Stock splits and stock dividends can

cause you to hold odd lots

8 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• Equivalently, we start with the discounted cash flow model, and obtain the holding period return

10 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

16 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Ease of Use

• We have to introduce a simplifying

assumption that captures our understanding of dividend behavior

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

7 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.2 Why Study Finance?

• To manage your personal resources

Defining Finance

• When impleake use of the Financial System defined as the set of markets and other institutions used for financial contracting and exchange of assets and risks

– strategic plans may change radically over time

– the firm’s business may be defined in terms of a group of products, technologies or customers

12 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

– The basic unit of analysis is the investment project. Investment projects are identified,

triaged, and implemented in the capital budgeting process

13 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

5 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Defining Finance

• Financial theory consists of:

– the set of concepts that help to organize one’s thinking about how to allocate resources over time

– Preferred stock holders usually gain some control if preferred dividends are not paid

– Bondholder covenants restrict decisions that could adversely affect bond values

– Capital structure is the amount of the firm’s

market value allocated to each category of issued securities. It determines ownership and risk level of the firms future cash flows

– loss of investor and creditor confidence

• delayed in investment schedules • sub-optimal temporary finance • unscheduled sale of the firms assets

16 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Financial Decisions of Firms

• The Capital Budgeting Process

– The preparation of a plan for acquiring factories, machinery, research laboratories, show rooms, warehouses, and human assets to implement the strategic plan

9 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Important Terms

• Assets • Personal investing & Asset allocation • Liability, Debt • Net Worth = Assets - Liabilities • Exogenous and endogenous elements

Chapter 1:

Financial Economics

Objective

To Define Finance The Value of Finance

Introduction to the Players

1 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

17 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Forms of Business Operation

flows are often known only probabilistically

• Understanding finance helps you evaluate these uncertain cash flows

4 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

11 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Financial Decisions of Firms

• Strategic plans specify the business the firm is in

– the set of quantitative models used to help evaluate alternatives, make decisions, and implement them

• These concepts and models apply at all levels and scales of decision making

• To deal with the world of business

• To pursue interesting and rewarding career opportunities

• To make informed public choices as a citizen

• The intellectual challenge

– Capital structure’s unit of analysis is the firm

as a whole (not an investment project )

14

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Financial Decisions of Firms

• The capital structure also determines who controls the firm under different contingencies

– Common stock holders usually determine the membership of the board of directors

1.1 Defining Finance

• Finance is the study of how people

allocate scarce resources over time

– costs and benefits are distributed over time – but the actual timing and size of future cash

8 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.3 Financial Decisions of Households

• Consumption and saving decisions • Investment Decisions • Financing Decisions • Risk-management decisions

10 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.4 Financial Decisions of Firms

• Business Firms

– entities whose primary function is to produce goods and services

15 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Financial Decisions of Firms

• Working Capital

– all firms (including highly profitable ones) that do not pay sufficient attention to working capital management may be seriously damaged by the resulting