Chapter_14An Overview of Corporate Financing(公司金融)

Chapter_14An Overview of Corporate Financing(公司金融,英文版)

Seventh Edition

Chapter 14

An Overview of Corporate Financing

Richard A. Brealey Stewart C. Myers

Slides by Matthew Will

McGraw Hill/Irwin

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 13

Corporate Debt

TABLE 14-5 Large firms issue many different securities. This table shows some of the debt securities on Heinz's balance sheet in May 2000.

14- 11

Preferred Stock

Preferred Stock - Stock that takes priority over common stock in regards to dividends. Net Worth - Book value of common shareholder’s equity plus preferred stock. Floating-Rate Preferred - Preferred stock paying dividends that vary with short term interest rates.

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

习题答案Principles of Corporate Finance第十版 Chapter14

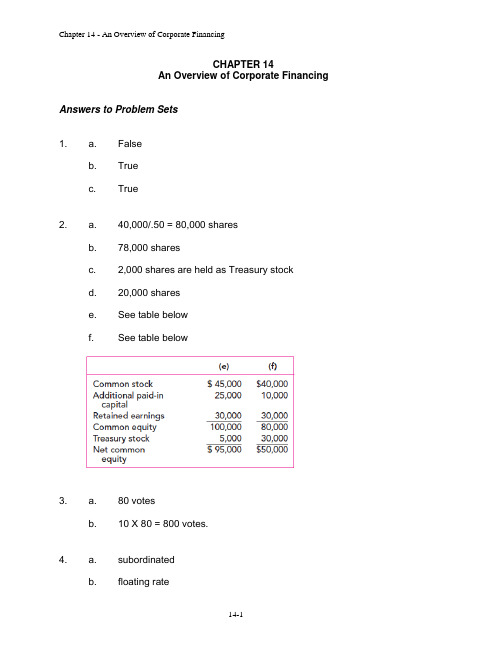

CHAPTER 14An Overview of Corporate Financing Answers to Problem Sets1. a. Falseb. Truec. True2. a. 40,000/.50 = 80,000 sharesb. 78,000 sharesc. 2,000 shares are held as Treasury stockd. 20,000 sharese. See table belowf. See table below3. a. 80 votesb. 10 X 80 = 800 votes.4. a. subordinatedb. floating ratec. convertibled. warrante. common stock; preferred stock.5. a. Falseb. Truec. False6. a. Par value is $0.05 per share, which is computed as follows:$443 million/8,863 million sharesb. The shares were sold at an average price of:[$443 million + $70,283 million]/8,863 million shares = $7.98c. The company has repurchased:8,863 million – 6,746 million = 2,117 million sharesd. Average repurchase price:$57,391 million/2,117 million shares = $27.11 per share.e. The value of the net common equity is:$443 million + $70,283 million + $44,148 million – $57,391million= $57,483 million7. a. The day after the founding of Inbox:Common shares ($0.10 par value) $ 50,000Additional paid-in capital 1,950,000Retained earnings 0Treasury shares 0Net common equity $ 2,000,000b. After 2 years of operation:Common shares ($0.10 par value) $ 50,000Additional paid-in capital 1,950,000Retained earnings 120,000Treasury shares 0Net common equity $ 2,120,000c. After 3 years of operation:Common shares ($0.10 par value) $ 150,000Additional paid-in capital 6,850,000Retained earnings 370,000Treasury shares 0Net common equity $ 7,370,0008. a.Common shares ($1.00 par value) $1,008Additional paid-in capital 5,444Retained earnings 16,250Treasury shares (14,015)Net common equity $8,687b.Common shares ($1.00 par value) $1,008Additional paid-in capital 5,444Retained earnings 16,250Treasury shares (14,715)Net common equity $7,9879. One would expect that the voting shares have a higher price because theyhave an added benefit/responsibility that has value.10. a.Gross profits $ 760,000Interest 100,000EBT $ 660,000Tax (at 35%) 231,000Funds available to common shareholders $ 429,000b.Gross profits (EBT) $ 760,000Tax (at 35%) 266,000Net income $ 494,000Preferred dividend 80,000Funds available to common shareholders $ 414,00011. Internet exercise; answers will vary.12. a. Less valuableb. More valuablec. More valuabled. Less valuable13. Answers may differ. Some key events of the financial crisis through the end of2008 include:June 2007: Bear Stearns pledges $3.2 billion to aid one of its ailing hedge funds Sept. 2007: Northern Rock receives emergency funding from the Bank of England Oct. 2007: Citigroup begins a string of writedowns based on mortgage losses Dec. 2007: Fed establishes Term Auction Facility linesJan. 2008: Ratings agencies threaten to downgrade Ambac and MBIA (major bond issuers)Feb. 2008: Economic stimulus package signed into lawMar. 2008: JPMorgan purchases Bear Stearns with support from the FedMar. 2008: SEC proposes ban on naked short sellingJuly 2008: FDIC takes over IndyMac BankSept. 2008: Lehman forced into bankruptcyB of A purchases Merrill Lynch10 banks create $70 billion liquidity fundAIG debt downgradedRMC money market fund “breaks the buck”Treasury bailout plan voted down in the HouseOct. 2008: 9 large banks agree to capital injection from TreasuryRevised bailout plan passes in HouseConsumer confidence hits lowest point on recordThe NY Fed has an excellent timeline of events at:/research/global_economy/Crisis_Timeline.pdf14. Answers will differ. Some purported causes of the financial crisis include:•Long periods of very low interest rates leading to easy credit conditions•High leverage ratios•The bursting of the US housing market bubble•High rates of default on subprime mortgages•Massive losses on investments in mortgage backed securities• Opaque derivative markets and amplified losses through credit default swaps • High rates of unemployment and job losses 15.a.For majority voting, you must own or otherwise control the votes of a simple majority of the shares outstanding, i.e., one-half of the shares outstanding plus one. Here, with 200,000 shares outstanding, you must control the votes of 100,001 shares.b.With cumulative voting, the directors are elected in order of the total number of votes each receives. With 200,000 shares outstanding and five directors to be elected, there will be a total of 1,000,000 votes cast. To ensure you can elect at least one director, you must ensure that someone else can elect at most four directors. That is, you must have enough votes so that, even if the others split their votes evenly among five other candidates, the number of votes your candidate gets would be higher by one.Let x be the number of votes controlled by you, so that others control (1,000,000 - x) votes. To elect one director:Solving, we find x = 166,666.8 votes, or 33,333.4 shares. Because there are no fractional shares, we need 33,334 shares.15x000,000,1x +-=。

管理定量分析(Quantitative

Course Descriptionsfor Full-time Bilingual Top-up Bachelor ProgramsMANAGEMENT FINANCE ENGLISHBUSINESS INFORMATION TECHNOLOGY MANAGEMENTCourse Code: MGT01Course Title: 管理定量分析(Quantitative Analysis for Management)Credits: 3Course Description:管理定量分析课程是研究如何利用数据信息,作出最优决策的一门学科,是管理学科的主干课程之一。

本课程的任务是阐述管理科学中定量分析的基本思想、基本原理和方法,使学生对定量分析方法有较为全面的了解和认识,学会科学地分析已有的数据信息,统筹安排管理工作中的整体步骤,避免决策的随意性和盲目性。

其主要环节包括经验数据的提取、整理和分析、数学模型的建立、发展趋势的预测和推断、决策, 方案优劣的评判以及最优方案的确定等。

There has been an increasing tendency to turn to quantitative methods and models as a potential means for solving many of the problems that arise in management. The aims of this course are to enable students to familiarized themselves with the quantitative approaches to management decision marking, to enhance their reasoning and analytical capabilities and to develop their problem-solving skills. This course will impart an understanding of the application of quantitative methods to the areas of planning and control and to other management branches.Course Code: MGT02Course Title: 经济学(Economics)Credits: 3Course Description:本课程主要介绍有关现代经济学的一些基本原理及其应用。

罗斯《公司理财CorporateFinance》(第七版)英文课件Ch

If how you slice the pie affects the size of the pie, then the capital struቤተ መጻሕፍቲ ባይዱture decision matters.

1-9

Hypothetical Organization Chart

Board of Directors Chairman of the Board and Chief Executive Officer (CEO)

Shareholders’ Equity

1-5

The Balance-Sheet Model

of the Firm

The Capital Budgeting Decision

Current

Current Assets

Liabilities

Long-Term Debt

Fixed Assets 1 Tangible 2 Intangible

Cost Accounting Data Processing

1-10

The Financial Manager

To create value, the financial manager should: 1. Try to make smart investment decisions. 2. Try to make smart financing decisions.

How much shortterm cash flow does a company need to pay its bills?

Shareholders’ Equity

1-8

Capital Structure

The value of the firm can be thought of as a pie.

金融英语3corporatefinancenew精品文档

In Britain, stock is also used to refer to all kinds of securities(有价证券), including government bonds.

Investors at this stage have a lower risk of loss than venture capitalist, but less chance of making a big profit.

13

3.2 Stocks and shares(1)

Stocks and shares are certificates representing part ownership of a company.

If the company goes into liquidation(进入清 算), holders of preference shares are repaid(偿还) before other shareholders, but after owners of bonds and other debts.

Latest Economic news

China central bank pledges more co-operation to stem global financial crisis 中国央行投入更多合作来遏制全球金 融危机

0

BEIJING, Oct. 10 (Xinhua) -- China's central bank on Friday said it will continue international cooperation to tackle the global financial crisis and maintain market stability.

第一章财务管理导论Corporate Finance Financial Management

3

什么是财务管理?

财务管理解决下述三个问题 :

1.

2.

3.

投资决策:公司应该投资于什么样的长期资产?— —涉及到资本预算 融资决策:公司如何筹资,以支付投资支出所需 要的资金?——涉及到资本结构 营运资本管理:公司应该如何管理它在经营中的 现金流量( cash flow )?——涉及到净营运资 本决策

10

融资决策

公司应如何为长期投资筹集所需的长期资金? 这些长期资金将利用股东权益方式还是通过 借入资金方式筹集? 这属于企业的长期筹资决策。 资本结构( Capital Structure)决策

11

融资决策

公司价值(The value of the firm )可以被看做一个圆饼. 财务经理的目标是增加圆饼 的大小 资本结构(Capital Structure)决策可以视做 怎样去最佳地分割圆饼 70% 25% 50% 30% 股 Debt Debt权 负债 75% 50% Equity

由于对圆饼的分割(资本结构)将直接影响 到圆饼 大小(公司价值),因此资本结构决 策就非常重要

12

营运资本管理决策

企业应如何管理日常的财务活动,即企业应 如何取得短期资金以及是否要进行赊销?等等 这属于企业由流动资产和流动负债组成的营 运资金管理决策。 净营运资本=流动资产 - 流动负债

净营运资本(Net Working Capital)决策

虽然有限台伙企业的形式在石油天然气租赁和房地产等行业较为普遍但它对于许多其他经营活动并不很适合50有限合伙制企业区别有限合伙人limitedpartnership普通合伙人generalpartnership出资金额大部分95小部分5经营控制权对企业债务的责任仅仅以出资额为限承担有限责任以个人财产承担无限责任专业技术总体上承担无限责任和难以维持持续经营等不利因素使一些规模非常大的企业很难以合伙企业的组织形式进行运作

习题答案Principles-of-Corporate-Finance第十-Chapter

CHAPTER 18How Much Should a Corporation Borrow?Answers to Problem Sets1. The calculation assumes that the tax rate is fixed, that debt is fixed and perpetual,and that investors’ personal tax rates on interest and equity income are the same. 2. a. PV tax shield = T c D = $16. b. T c X 20 = $8. 3.Relative advantage of debt =()()c pE pT T T ---111=()()00.165.165.=Relative advantage=()()18.165.85.65.=4. A firm with no taxable income saves no taxes by borrowing and paying interest. The interest payments would simply add to its tax-loss carry-forwards. Such a firm would have little tax incentive to borrow.5. a. Direct costs of financial distress are the legal and administrative costs ofbankruptcy. Indirect costs include possible delays in liquidation (EasternAirlines) or poor investment or operating decisions while bankruptcy is being resolved. Also the threat of bankruptcy can lead to costs.b. If financial distress in creases odds of default, managers’ andshareholders’ incentives change. This can lead to poor inves tment orfinancing decisions.c. See the answer to 5(b ). Examples are the “games 〞 described in Section 18-3.6. Not necessarily. Announcement of bankruptcy can send a message of poorprofits and prospects. Part of the share price drop can be attributed to anticipatedbankruptcy costs, however. 7. More profitable firms have more taxable income to shield and are less likely to incur the costs of distress. Therefore the trade-off theory predicts high (book) debt ratios. In practice the more profitable companies borrow least.8. D ebt ratios tend to be higher for larger firms with more tangible assets. Debtratios tend to be lower for more profitable firms with higher market-to-book ratios.9. W hen a company issues securities, outside investors worry that managementmay have unfavorable information. If so the securities can be overpriced. This worry is much less with debt than equity. Debt securities are safer than equity, and their price is less affected if unfavorable news comes out later.A company that can borrow (without incurring substantial costs of financial distress) usually does so. An issue of equity would be read as “bad news 〞 by investors, and the new stock could be sold only at a discount to the previous market price.10. a. The cumulative requirement for external financing. b. More profitable firms can rely more on internal cash flow and need less external financing.11. Financial slack is most valuable to growth companies with good but uncertaininvestment opportunities. Slack means that financing can be raised quickly for positive-NPV investments. But too much financial slack can tempt -mature companies to overinvest. Increased borrowing can force such firms to pay out cash to investors.12. a. $25.931.08$1,000)0.35(0.08r 1D)(r T shield)PV(tax D D C =⨯=+=b. $111.80shield)PV(tax =⨯=∑=51)08.1()000,1$08.0(35.0t tc. PV(tax shield) = T C D = $35013.For $1 of debt income:Corporate tax = $0Personal tax = 0.35 ⨯ $1 = $0.350 Total = $0.350For $1 of equity income, with all capital gains realized immediately:Corporate tax = 0.35 ⨯ $1 = $0.350Personal tax = 0.35 ⨯ 0.5 ⨯ [$1 – (0.35⨯$1)] + 0.15 ⨯ 0.5 ⨯ [$1 – (0.35⨯$1)] =$0.163Total = $0.513For $1 of equity income, with all capital gains deferred forever:Corporate tax = 0.35 ⨯ $1 = $0.350Personal tax = 0.35 ⨯ 0.5 ⨯ [$1 – (0.35⨯$1)] = $0.114 Total = $0.46414.Consider a firm that is levered, has perpetual expected cash flow X, and has an interest rate for debt of r D . The personal and corporate tax rates are T p and T c , respectively. The cash flow to stockholders each year is:(X - r D D)(1 - T c )(1 - T p )Therefore, the value of the stockholders’ position is:where r is the opportunity cost of capital for an all-equity-financed firm. If the stockholders borrow D at the same rate r D , and invest in the unlevered firm, their cash flow each year is:The value of the stockholders’ position is then:The difference in stockholder wealth, for investment in the same assets, is:V L – V U = DT c)T (1)(r )T (1)T (1D)()(r )T (1(r))T (1)T (1(X)V p D p c D p p c L -------=)]T (1D)()T (1(r))T (1)T (1(X)V c p p c L -----=[)]T (1D)()r ()]T (1)T (1[(X )p D p c ----[)T (1)(r )T (1D)()(r )T (1(r))T (1)T (1(X)V p D p D p p c U ------=D)T (1(r))T (1)T (1(X)V p p c U ----=This is the change in stockholder wealth predicted by MM.If individuals could not deduct interest for personal tax purposes, then:Then: So the value of the shareholders’ posit ion in the levered firm is relatively greater when no personal interest deduction is allowed.15.Long-term debt increases by: $10,000 − $4,943 = $5,057 million The corporate tax rate is 35%, so firm value increases by:0.35 ⨯ $3,874 = $1,770 millionThe market value of the firm is now: $79,397 + $1,770 = $81,167 million The market value balance sheet is:16.Assume the following facts for Circular File:Book Values Net working capital $20 $50 Bonds outstandingFixed assets 80 50 Common stock Total assets $100 $100 Total valueMarket Values Net working capital $20 $25 Bonds outstanding Fixed assets 10 5 Common stock Total assets$30 $30Total valuea.Playing for TimeSuppose Circular File foregoes replacement of $10 of capital equipment, so that the new balance sheet may appear as follows:)T (1)(r D))((r )T (1(r))T (1)T (1(X)V p D D p p c U -----=)T (1)(r )]T (1)T (1D))(r ([D)()(r V V p D p c D D U L ----=-⎪⎪⎭⎫⎝⎛-+=-)T (1T D)T D (V V p p c U LMarket ValuesNet working capital $30 $29 Bonds outstandingFixed assets 8 9 Common stockTotal assets $38 $38 Total valueHere the shareholder is better off but has obviously diminished the firm’scompetitive ability.b. Cash In and RunSuppose the firm pays a $5 dividend:Market ValuesNet working capital $15 $23 Bonds outstandingFixed assets 10 2 Common stockTotal assets $25 $25 Total valueHere the value of common stock should have fallen to zero, but thebondholders bear part of the burden.c. Bait and SwitchMarket ValuesNet working capital $30 $20 New Bonds outstanding20 Old Bonds outstandingFixed assets 20 10 Common stockTotal assets $50 $50 Total value17. Answers here will vary according to the companies chosen; however, theimportant considerations are given in the text, Section 19.3.18. a. Stockholders win. Bond value falls since the value of assets securingthe bond has fallen.b. Bondholder wins if we assume the cash is left invested in Treasury bills.The bondholder is sure to get $26 plus interest. Stock value is zerobecause there is no chance that the firm value can rise above $50.c. The bondholders lose. The firm adds assets worth $10 and debtworth $10. This would increase Circular’s debt ratio, l eaving the oldbondholders more exposed. The old bondholders’ loss is thestockholders’ gain.d. Both bondholders and stockholders win. They share the (net) increasein firm value. The bondholders’ position is not eroded by the issue of ajunior security. (We assume that the preferred does not lead to stillmore game playing and that the new investment does not make the firm’s assets safer or riskier.)e. Bondholders lose because they are at risk for a longer time.Stockholders win.19. a. SOS stockholders could lose if they invest in the positive NPV project andthen SOS becomes bankrupt. Under these conditions, the benefits of theproject accrue to the bondholders.b. If the new project is sufficiently risky, then, even though it has a negativeNPV, it might increase stockholder wealth by more than the moneyinvested. This is a result of the fact that, for a very risky investment,undertaken by a firm with a significant risk of default, stockholders benefitif a more favorable outcome is actually realized, while the cost ofunfavorable outcomes is borne by bondholders.c. Again, think of the extreme case: Suppose SOS pays out all of its assetsas one lump-sum dividend. Stockholders get all of the assets, and thebondholders are left with nothing. (Note: fraudulent conveyance laws mayprevent this outcome)20. a. The bondholders may benefit. The fine print limits actions that transferwealth from the bondholders to the stockholders.b. The stockholders may benefit. In the absence of fine print, bondholderscharge a higher rate of interest to ensure that they receive a fair deal. Thefirm would probably issue the bond with standard restrictions. It is likelythat the restrictions would be less costly than the higher interest rate. 21. Other things equal, the announcement of a new stock issue to fund aninvestment project with an NPV of $40 million should increase equity value by$40 million (less issue costs). But, based on past evidence, managementexpects equity value to fall by $30 million. There may be several reasons forthe discrepancy:(i) Investors may have already discounted the proposed investment. (However,this alone would not explain a fall in equity value.)(ii) Investors may not be aware of the project at all, but they may believe instead that cash is required because of, say, low levels of operating cash flow.(iii) Investors may believe that the firm’s decision to issue equity rather than debt signals management’s belief that the stock is overvalued.If the stock is indeed overvalued, the stock issue merely brings forward a stockprice decline that will occur eventually anyway. Therefore, the fall in value is notan issue cost in the same sense as the underwriter’s spread. If the stock is not overvalued, management needs to consider whether it could release someinformation to convince investors that its stock is correctly valued, or whether it could finance the project by an issue of debt.22. a. Masulis’ results are consistent with the view that debt is always preferablebecause of its tax advantage, but are not consistent with the ‘tradeoff’theory, which holds that management strikes a balance between the taxadvantage of debt and the costs of possible financial distress. In thetradeoff theory, exchange offers would be undertaken to move the firm’sdebt level toward the optimum. That ought to be good news, if anything,regardless of whether leverage is increased or decreased.b. The results are consistent with the evidence regarding the announcementeffects on security issues and repurchases.c. One explanation is that the exchange offers signal management’sassessment of the firm’s prospects. Management would only be willing totake on more debt if they were quite confident about future cash flow, forexample, and would want to decrease debt if they were concerned aboutthe firm’s ability to meet debt payments in the future.23. a.Expected Payoff to Bank Expected Payoff to Ms. Ketchup Project 1 +10.0 +5Project 2 (0.4⨯10) + (0.6⨯0) = +4.0 (0.4⨯14) + (0.6⨯0)=+5.6Ms. Ketchup would undertake Project 2.b. Break even will occur when Ms. Ketchup’s expected payoff from Project 2is equal to her expected payoff from Project 1. If X is Ms. Ketchup’spayment on the loan, then her payoff from Project 2 is:0.4 (24 – X)Setting this expression equal to 5 (Ms. Ketchup’s payoff from Project 1),and solving, we find that: X = 11.5Therefore, Ms. Ketchup will borrow less than the present value of thispayment.24. One advantage of setting debt-equity targets based on bond ratings is that firmsmay minimize borrowing costs. This is especially true of bond covenantsestablish lower ratings as a condition of default. One disadvantage is that firms may not take full advantage of tax benefits from debt financing if they refuse toborrow amounts they could finance with relative safety.25. The right measure in principle is the ratio derived from market-value balancesheets. Book balance sheets represent historical values for debt and equitywhich can be significantly different from market values. Any changes in capitalstructure are made at current market values.The trade-off theory proposes to explain market leverage. Increases ordecreases in debt levels take place at market values. For example, a decision to reduce the likelihood of financial distress by retirement of debt means thatexisting debt is acquired at market value, and that the resulting decrease ininterest tax shields is based on the market value of the retired debt. Similarly, a decision to increase interest tax shields by increasing debt requires that new debt be issued at current market prices.Similarly, the pecking-order theory is based on market values of debt and equity.Internal financing from reinvested earnings is equity financing based on currentmarket values; the alternative to increased internal financing is a distribution ofearnings to shareholders. Debt capacity is measured by the current marketvalue of debt because the financial markets view the amount of existing debt as the payment required to pay off that debt.26. If it was always possible to issue stock quickly and use the additional proceeds torepurchase debt, then firms may indeed avoid financial distress. But potentialequity investors may be reluctant to buy stock in a firm if adverse market events are likely to place the bonds in default: they would effectively be putting moneyinto a sinking ship, and those proceeds would go to repay the senior bond claims in bankruptcy. This is especially true if the bonds quickly move into default (or ifthere are cross-default provisions where one bond series default triggers otherdefaults).In some cases, bondholders may recognize that the firm has greater value as agoing concern and agree to take a haircut on interest payments in exchange for an equity infusion. Under these circumstances, a firm may indeed be able toraise additional equity—but the negotiations and gamesmanship of theseworkout situations can get tricky.。

《Corporate Finance (公司金融学)》课件 (12)

12.1 The Cost of Equity Capital

Firm with excess cash

Pay cash dividend

Shareholder invests in financial asset

A firm with excess cash can either pay a dividend or make a capital investment

– Movie studios have revenues that are variable, depending upon whether they produce “hits” or “flops”, but their revenues are not especially dependent upon the business cycle.

• It is frequently argued that one can better estimate a firm’s beta by involving the whole industry.

• If you believe that the operations of the firm are similar to the operations of the rest of the industry, you should use the industry beta.

• Don’t forget about adjustments for financial leverage.

12.3 Determinants of Beta

• Business Risk – Cyclicity of Revenues – Operating Leverage

361度体育用品公司品牌定位研究 (2)

361度体育用品公司品牌定位研究摘要品牌定位是企业根据消费者对品牌的认识、了解和重视程度,给自己的品牌规定一定的市场地位,树立产品在消费者心目中的特色和形象,以满足消费者的某种偏爱和需要。

尽管许多企业目前已经认识到其对企业竞争力的重要影响,但在具体的实践和操作过程中却存在很多问题,导致品牌定位的实施结果不佳。

本文从品牌定位的理论出发,结合361度体育用品公司品牌定位的具体实践,探讨如何有效的进行品牌定位。

笔者首先详细介绍品牌定位的理论背景和基础,接着介绍361度品牌定位目前状况,包括企业品牌定位的概况以及现状。

然后对361度的品牌定位进行分析,包括外部市场分析、内部条件分析、市场细分、选择目标市场以及品牌的具体定位。

最后针对公司存在的问题提出以情景定位策略为指导,用媒体组合理论以推广等主要的改进意见。

对361度体育用品公司品牌定位的研究目的是希望能使企业尽快摆脱受到的困扰,能够从消费者心理采取行动,树立品牌在消费者心目中的特色和形象,以满足消费者的某种偏爱和需要。

拥有成功的品牌定位,才能在同行中取得竞争优势。

该论文研究意义在于作者对体育用品行业的大型企业的品牌定位方面存在的问题进行全面深入的研究,并提出改进建议,具有一定的参考意义。

关键词:品牌定位,品牌推广,体育用品IAbstractBrand positioning is the corporate brand, according to consumer awareness, understanding and importance attached to certain provisions of its own brand market position, establish the product in the consumers mind and image to meet a consumer preference and needs. Although many companies today have recognized its enterprise competitiveness on the important influence in the specific practice and there are many problems leading to poor results of the implementation brand.In this paper, the theory of brand positioning, combined with 361 degrees sports brand positioning with the concrete practice of the company on how effectively the brand positioning. I first introduced the brand positioning of the theoretical background and foundation of the brand positioning and then describes the current status of 361 degrees, including an overview of corporate brand positioning and the status. Then on the 361-degree analysis of brand positioning, market analysis, including external and internal conditions of analysis, market segmentation and target market selection. Finally, the problems the company positioning strategy scenarios proposed to the guidance of portfolio theory with the media to promote the views of other major improvements. Sports 361 degrees during the company's brand positioning research objective is to enable enterprises to quickly get rid of trouble being able to take from the consumption of this psychological Action, establish a brand in the consumers mind and image, in order to meet consumer preferences and needs of a successful brand positioning to gain competitive advantage in the peer. Significance of this research is that the author's large enterprises on the sporting goods industry's brand positioning problems in a comprehensive in-depth study and make recommendations for improvement with some reference value.Keywords: Brand Positioning, brand promotion, Sporting GoodsII目录摘要 (I)ABSTRACT (II)第一章绪论 (1)1.1研究的背景和意义............................................................................. 错误!未定义书签。

(完整版)Chapter1AnOverviewOnInternationalInvestment

(完整版)Chapter1AnOverviewOnInternationalInvestment Chapter 1 An Overview On International Investment Section 1: The conception and the types of International Investment The conceptionSimply stated, investment is a vehicle into which funds can be placed with the expectation that they will be preserved or will increase in value or will generate positive returns. The term investment can cover a wide range of activities. Idle cash is not an investment, since its value is likely to be eroded by inflation and it fails to provide any type of return. The same cash placed in a bank savings account would be considered as an investment, since the account provides a positive return. The various types of investments can be differentiated on the basis of a few factors, such as option; short or long term; domestic or international.International Investment refers to any economic behaviors through which investors such as TNCs, transnational financial institutions, official and semi-official institutions and individuals invest their assets in countries other than their own with the expectation of positive return. Although international investments cover almost the same varieties of domestic investments, they are extensively regarded more complicated and difficult than domestic ones due to its internationalization. International investment can be divided into many types according to different standards. For example, we have long-run investments and short-run investments according to the period an investment paybackcovers. Official investments and private investments based on investors themselves; according to whether investors own control right in the management of a firm or not, it usually falls into two types; foreign direct investment (FDI)and international indirect investment ( also Foreign Portfolio Equity Investment, abbreviated as FPEI),FDI and FPEI are the most cited types in both the practice and theoretical study of international investment.FDI and FPEIAccording to the IMF and OECD definitions, FDI reflects the aim of obtaining a lasting interest by a resident entity of one economy (direct investor) in an enterprise that is resident in another economy (the direct investment enterprise).The “lasting interest” implies the existence of a long-term relationship between the direct investor and the direct investment enterprise and a significant degree of influence on the management of the latter.FDI involves both the initial transaction establishing the relationship between the investor and the enterprise and all subsequent capital transactions between them and among affiliated enterprises, both incorporated and unincorporated. It should be noted that capital transactions which do not give rise to any settlement, e.g. an interchange of shares among affiliated companies, must also be recorded in theBalance of Payments and in the IIP(International Investment Position).The fifth Edition of the IMF’s Balance of Payment Manual defines the owner of 10% or more of a company’s capital as a direct investor. This guideline is not a fast rule, as it acknowledges that smaller percentage may entail a controlling interest in the company (and, conversely, that a share of more than 10% may not signify control).But the IMF recommends using this percentage as the basic dividing line between direct investment and portfolio investment in the form of shareholdings. Thus, when a non-resident who previously had no equity in a resident enterprise purchases 10% or more of the shares of that enterprise from a resident, the price of equity holdings acquired should be recorded as direct investment. From this moment, any further capital transactions between these two companies should be recorded as a direct investment. When a non-resident holds less than 10% of the shares of an enterprise as portfolio investment, and subsequently acquires additional shares resulting in a direct investment (10% of more), only the purchase of additional shares is recorded as direct investment in the Balance of Payments. The holdings that were acquired previously should not be reclassified from portfolio to direct investment in the Balance of Payments but the total holdings should be reclassified in the IIP.The classification of direct investment is based firstly on the direction of investment both for assets or liabilities; secondly, on theinvestment instrument used (shares, loans, etc.); and thirdly on the sector breakdown.As for the direction, it can be looked at it from the home and the host perspectives. From the home one, financing of any type extended by the resident parent company to its nonresident affiliated would be included as direct investment abroad. By contrast, financing of any type extended by non-resident subsidiaries, associates or branches to their resident parentcompany are classified as a decrease in direct investment abroad, rather than as a foreign direct investment. From the host one, the financing extended by non-resident parent companies to their resident subsidiaries, associates or branches would be recorded, in the country of residence of the affiliated companies, under foreign direct investment, and the financing extended by resident subsidiaries, associates and branches to their non-resident parent company would be classified as a decrease in foreign direct investment rather than as a direct investment abroad. This directional principle does not apply if the parent company and its subsidiaries, associates or branches have cross-holdings in each other’s share capital of more than 10%.As for the instruments, Direct investment capital transactions are made up of three basic components: (i) Equity capital; (ii) Reinvested earnings: (iii) Other direct investment capital: covering the borrowing and lending of funds, including debt securities and trade credits.Section 2: Emerge and development of International Investment Emerged early in the late 18th century, International investment has been developing into the most active driving force in the world economy today. After more than two hundred years, International investments have experienced great changes in many aspects. According to the investment size and the modes, it can be divided into four phases:From the beginning of 19 centuries to before 1914: International investments appeared because production surplus resulted from the second industrial revolution. And the indirect investment dominated in the international investment during that period.1914~1945:a slowly developing period. Due to the two world wars, international investments were held back heavily. The foreign investment value by major investor countries dropped to US $ 38 billion in 1945 when the Second World War ended. Indirect investment was still the mainmode.1945~1979:International investments started to develop again. During this period, international investments increased rapidly, the value from developed countries reaching US$600 billion in 1978 from US$51 billion in 1945. And another obvious feature is that direct investment replaced indirect investment to dominate in international investment. For example, FDI reached US$369.3 billion in 1978, accounting for 61.6% of the total from the US$20.0 billion in 1945. Please see Table 1.1 for detailed increase.Table 1.1 Private Foreign Direct Investment from Main Capitalist countries (Unit: 1 billion US$)since 1980s: a rapid development phase. Technological progress, financial innovations and globalization facilitate international investment both in FDI and indirect investment and the development speed exceeds that of GDP. Please refer to Table 1.2 for the great change. Table 1.3 for the comparison between FDI and some production indices and Table 1.4 for FPEI of developed countries.Table 1.2 International Investments in 1989 and 1999( as per the share in GDP)Source: World Bank, World Development Indicators. 2001Table 1.3 FDI and Related Production Indices (US $1billion, %)Table 1.4 Transnational transactions in Bonds and Stocks by Main DCs (% of GDP)Figure 1.1Global inflows of FDI, 1993-2002, by groups of countries$ billionsFigure 1.2Inflows of FDI to developing countries, 1995-2002, by region 发展中国家FDI 分布05010015020025019951996199719981999200020012002Developing countriesAsia and the Pacific Latin America/Caribbean ChinaAfricaLDCsInflows of FDI to developing countries, 1995-2002, by region$ billions发展中国家亚太地区拉美加勒⽐海地区⾮洲中国The Latest development of International investmentWorld Investment Report 2006 (WIR2006): FDI from Developing and Transition EconomiesMain Contents1. FDI in 2005 grew for the second consecutive year, and it was a worldwide phenomenon.2. It was spurred by cross-border M & As, with increasing deals also undertaken by collective investment funds3. Most inflows went into services, but the sharpest rise in FDI was in natural resources.4. There has been a significant increase in developing-country firms inthe universe of transnational corporations.5. Liberalization continues, but some protectionist tendencies are also emerging.6. Africa attracted much higher levels of FDI.7. South, East and South-East Asia is still the main magnet for inflows into developing countries,while West Asia received an unprecedented level of inflows.8. Latin America and the Caribbean continued to receive substantial FDI.9. FDI flows to South-East Europe and the Commonwealth of Independent States remained relatively high. while there was an upturn in FDI to developed countries.10. Overall, FDI should continue to grow in the short term.Section 3: Comment on Current International Investments Developing for more than two centuries combined with the effects of globalization and increasingly intensive competition in economy, great changes are taking place in the field of international investment. It becomes easier for investors to reach many investment instruments on the one hand, risks thereof are much more subtle and managerial technologies and skills seem much more important than ever before. So investors must be well informed of everything related and skillful with each investment vehicle as well as skills to manage them. Here are somefeatures of current international investments.1.International investment instruments increased.As economy develops, more and more international investment instruments come out of the horizon in the investment market fore investors to choose. Besides traditional vehicles such as short-term securities, common stock, fixed income securities, we also have options, futures, mutual funds, real estate, annuities, as well as many newly-created financial derivatives. As globalization and world economic integration develop, new vehicles will be increased. Therefore, it is convenient for investors to reach investment vehicles, and international investment will become more knowledge and skill demanded.2.Investment modes and patterns are diversifiedIn 1960s —1970s, private investments were, on the whole, equal with official ones. The 1990s witnessed a sea change in the pattern of international capital flows. In 1990, official sources accounted for more than half of international capital flows to developing countries. In 1991, Privatization accounted for 76 per cent of FDI inflows into Central and Eastern Europe. By 1995 over three-quarters came from private sources. The biggest story was the explosion in portfolio ( equity and debt ) investment, which soared from US$5 to us$61 billion from 1990 to 1995.The mode of investments is changing, from privatization to licensing and joint ventures. FDI predominated in the overall scale relative toindirect investment, but the share of FPEI expands swiftly, and gained and equal importance with FDI soon. This change results from the increasing demand for long-term financing, expanded credit as well as financing internationalized. Another more important reason is the fast increase of securities investment, such as development of securities market, privately held shares or stocks in foreign enterprises, increase of speculative investments and so on. In recent years Non-equity arrangement, such as technology investment, equipment rental and leasing, franchising, management contracts, partnerships, cooperative distribution, and co-contracting projects, has extensively spreaded in developing countries and become important modes of investment there.3.The profile of investors is changingFor years western developed countries have dominated the international investment. The “Triad”(The EU, Japan, the United States )occupies the major share of global investments at the present and in 1991 its share reached 86%. The profile of investors is changing now. An inspiring fact is that foreign investments from developing countries, especially newly industrialized countries and regions(NICs) have developed rapidly since 1990s, For example, foreign investments from developing countries in 1980-1984 accounted for only 5% of the global total, but they went up to 15% to US$47 billion in 1995, exhibiting an inspiring picture o investment abroad at a high speed, though its absolute share was lowthen.4.Direction of International investment is multipliedThe direction of investment has changed a lot. Instead of flowing among developed countries, a lot of investments take place within various regions or economic Groups, which wer established in 1990s for the benefits of individual country in these areas, such as NAFTA, APEC, and EU. Along with the world economic regionalization and collectivization, FDI flows tend to be regional or collective.Some newly emerging economies with fast and stable growth are the most attractive to foreign investments. For example, 80% of FDI into developing countries were absorbed by 10 fast growing developing Asian, American and European countries or regions, among which inward flows into East and Southeast Asia account for 2/3. Central and Eastern Europe are hot points for investments, too.5.FDI is shifting towards servicesIn recent decades, international investments have been shifted from traditional resource and labor-intensive fields to modern technology-intensive manufacturing and service industries. High technological enterprises, finance, insurance and service are the greatest attractions for international investments. A large share of FDI is shifting towards services industry. For example, service sector accounted for only one-quarter of the world FDI stock in the early 1970s; but in 1990 thisshare was almost half of the world total; and by 2002, it had occupied about 60% to US $4trillion. Over the same period, the share of FDI stock in the primary sector declined from 9% to 6%, and it dropped much more in the manufacturing sector, from 42% to 34%. FDI in services accounted for two thirds of the total FDI inflows on the average during 2001-2001, amounting to approximately US$500 billion.Outward FDI in services continues to be dominated by developed countries, but has become more evenly distributed among them. Developing countries’outward FDI in services began to grow wore visible from the 1990s. Their share in the global outward FDI services stock climbed from 1% in 1990 to 10% in 2002, faster than in other sectors, On the inward side, thedistribution of services FDI stock has become relatively balanced, though developed countries still account for the largest share, The faster growth has taken place in Western Europe and the United States, reflecting the fact that most service FDI is market-seeking. Today, developed countries account for an estimated 72% of the inward FDI stock in services, developing economies for 25% and CEE (Central Eastern Europe ) for the balance . In 2002, the United States was the largest host economy in terms of the size of its inward FDI stock in services. With a few exceptions (such as China ), countries that have participated in the FDI boom in services also strengthened their position among home and host countries for all FDI.6.The continuing liberalization of FDI.There were 244 changes in laws and regulations affecting FDI in 2003, 220 of which were in the direction of more liberalization. In that year, 86 bilateral investment treaties (BITs) and 60 double taxation treaties (DTTs) were concluded, bringing the totals to 2265 and 2316, respectively. However, the annual number of new treaties concluded has declined, since the case of BITs in 2002 and that of DTTs in 2000. The attractiveness to FDI shows that economies such as the Czech Republic, Hong Kong and Ireland continued to absorb significant investment even during the FDI recession. In contrast, countries such as Japan, South Africa and Thailand have yet to realize their full potential to attract FDI, according to their rankings on UNCTAD’s Inward FDI potential Index as compared with that on the inward FDI performance index.In short, International investment has become an indispensable force pushing the world economy forward. No matter in what modes it is conducted, how large the size would be, what features it may have, both FDI and FPEI are undoubtedly the most vigorous force driving the world economy forward through intense international competition.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

May 2000 Market price = # of shares

$35/sh x 347

Market Value $12.1 bt © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 6

Patterns of Corporate Financing

? How do we define debt ?

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 9

Common Stock

Example - Heinz Book Value vs. Market Value (5/2000) Total Shares outstanding = 347 million

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 8

Common Stock

Book Value vs. Market Value

Book value is a backward looking measure. It tells us how much capital the firm has raised from shareholders in the past. It does not measure the value that shareholders place on those shares today. The market value of the firm is forward looking, it depends on the future dividends that shareholders expect to receive.

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 4

Patterns of Corporate Financing

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 7

Patterns of Corporate Financing

DEBT TO TOTAL CAPITAL Book Canada France Germany Italy Japan United Kingdom United States 39% 48 38 47 53 28 37 Book, Adjusted 37% 34 18 39 37 16 33 Market 35% 41 23 46 29 19 28 Market, Adjusted 32% 28 15 36 17 11 23

14- 11

Preferred Stock

Preferred Stock - Stock that takes priority over common stock in regards to dividends. Net Worth - Book value of common shareholder’s equity plus preferred stock. Floating-Rate Preferred - Preferred stock paying dividends that vary with short term interest rates.

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 12

Corporate Debt

Debt has the unique feature of allowing the borrowers to walk away from their obligation to pay, in exchange for the assets of the company. “Default Risk” is the term used to describe the likelihood that a firm will walk away from its obligation, either voluntarily or involuntarily. “Bond Ratings”are issued on debt instruments to help investors assess the default risk of a firm.

Common Shares ($1 par) Additionalpaid in capital Retained earnings Other adjustments Net common equity (Book Value) 108 304 4,757 - 652 1,596

Treasuryshares - 2,920

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 10

Common Stock

Example - Mobil Book Value vs. Market Value (5/00) Total Shares outstanding = 347 million

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 2

Topics Covered

Patterns of Corporate Financing Common Stock Preferred Stock Debt Financial Markets and Institutions

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 15

Corporate Debt

Subordinate Debt - Debt that may be repaid in bankruptcy only after senior debt is repaid. Secured Debt - Debt that has first claim on specified collateral in the event of default. Investment Grade - Bonds rated Baa or above by Moody’s or BBB or above by S&P. Junk Bond - Bond with a rating below Baa or BBB.

Debt 1,234 1,717 .60 Total assets 4,903

Long term liabilitie s 1,717 .47 Long term liabilitie s equity 1,717 1,951

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 13

Corporate Debt

TABLE 14-5 Large firms issue many different securities. This table shows some of the debt securities on Heinz's balance sheet in May 2000.

Principles of Corporate Finance

Seventh Edition

Chapter 14

An Overview of Corporate Financing

Richard A. Brealey Stewart C. Myers

Slides by Matthew Will

McGraw Hill/Irwin

US dollar debt Bank loans Commercial paper Senior unsecured notes and debentures Eurodollar notes Revenue bonds Foreign currency debt Sterling notes Euro notes Lire notes

McGraw Hill/Irwin

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved

14- 3

Patterns of Corporate Financing

Firms may raise funds from external sources or plow back profits rather than distribute them to shareholders. Should a firm elect external financing, they may choose between debt or equity sources.