成本与管理会计英文课件(1)

合集下载

亨格瑞成本与管理会计(中英第15版)中文PPT (12)[38页]

![亨格瑞成本与管理会计(中英第15版)中文PPT (12)[38页]](https://img.taocdn.com/s3/m/83c244d3a6c30c2258019eb7.png)

许多组织引入了平衡计分卡方法来追踪改进和 管理它们战略的执行。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 12-7

平衡计分卡将组织的使命和战略转化为一系列 业绩衡量标准,它们为战略的执行提供了框架。

平衡计分卡不仅仅关注实现财务目标,它还强调 一些非财务目标,这是一个组织为达到和保持它 的财务目标所必须实现的。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 12-2

战略确定一个组织如何匹配自己的能力和市场 机会来实现目标。

战略描述一个组织如何区别于竞争者,为其顾客 创造价值。

在设计战略时,组织必须对它所在的行业有彻底 的理解。行业分析集中于五方面的力量。

12-12

这一维度集中于为顾客创造价值的内部运作,内 部运作通过增加股东价值来促进财务维度。

包括三个子流程:

1. 创新流程 2. 经营流程 3. 售后服务流程

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

12-13

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

重组是为了提高业绩关键指标 (如成本、质量、 服务、速度、顾客满意度等)而对业务流程进行 的基本再思考和再设计。

换句话说,再造就是重新设计业务流程,通过 降低成本和提高质量来提高性能。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 12-6

亨格瑞成本与管理会计(中英第15版)中文PPT (11)[39页]

![亨格瑞成本与管理会计(中英第15版)中文PPT (11)[39页]](https://img.taocdn.com/s3/m/6577b6349b89680202d825c7.png)

11-10

增量成本—是指某一作业所引起的总成本的增 加。

差量成本—是指两种方案下总(相关)成本之间 的差值。

增量收入—是指某一作业所引起的总收入的增 加。

差量收入—是指两种方案总收入之间的差值。

应注意的是,在实务中有时会将增量成本与差 量成本交替使用。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

满意度等。

虽然定性因素很难用财务数据表示,但是它们和定 量因素一样重要。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 11-7

过去(历史)成本作为预测基础可能很有用,但过去 的成本本身却是决策制定的不相关成本。

可通过检查预期的未来收入与成本之间的差异来比 较不同方案。

11-8

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 11-9

已经发生且无法改变的成本被分类为沉没成本。

沉没成本被排除是因为无论未来采取什么措施,它 们都不可避免,而且无法改变。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

相关成本是预期的未来成பைடு நூலகம்。 相关收入是预期的未来收入。 历史成本(过去的成本),与决策制定无关,

也称做沉没成本。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 11-6

定量因素是指可用数字计量的结果。 定性因素是指很难用数字准确计量的结果,如

成本与管理会计-亨格瑞-第13版-英文版-CA07共75页文档

2020/6/8

10

Static Budget

What was the actual operating profit?

Revenues (10,000 × $125) $1,250,000

Less Expenses:

Variable (10,000 × $95.01)

950,100

Fixed

285,000

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS) BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

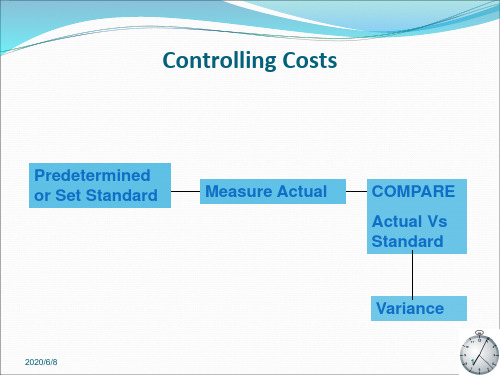

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2020/6/8

2

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

2020/6/8

$276 000 $120/JACKET 12 000JACKETS 10 000JACKETS

6

2020/6/8

7

Static Budget

es and sells jackets.

成本与管理会计 亨格瑞 第13版 英文版 CA18PPT课件

CHAPTER 18

Spoilage, Rework, and Scrap

Terminology

Spoilage, rework, and scrap have distinctive definitions in cost accounting that may not be the definition commonly used. P510(639) It is important that these terms be used properly, as each receives a different accounting treatment.

Normal spoilage is spoilage inherent in the production process.

It is viewed arising even in an efficient manufacturing process.

Typically, normal spoilage is included as a part of the cost of good units manufactured.

Scrap is residual material that results from manufacturing a product.

It has low or zero sales value.

Spoilage

Different types of Spoilage P511(639)

Spoilage is divided into two types: normal spoilage and abnormal spoilage.

the remaining 100 units are spoiled because of machine breakdown and operation errors.

Spoilage, Rework, and Scrap

Terminology

Spoilage, rework, and scrap have distinctive definitions in cost accounting that may not be the definition commonly used. P510(639) It is important that these terms be used properly, as each receives a different accounting treatment.

Normal spoilage is spoilage inherent in the production process.

It is viewed arising even in an efficient manufacturing process.

Typically, normal spoilage is included as a part of the cost of good units manufactured.

Scrap is residual material that results from manufacturing a product.

It has low or zero sales value.

Spoilage

Different types of Spoilage P511(639)

Spoilage is divided into two types: normal spoilage and abnormal spoilage.

the remaining 100 units are spoiled because of machine breakdown and operation errors.

亨格瑞成本与管理会计(中英第15版)中文PPT (16)[30页]

![亨格瑞成本与管理会计(中英第15版)中文PPT (16)[30页]](https://img.taocdn.com/s3/m/0e132f0076eeaeaad0f330c7.png)

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-8

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-9

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

副产品—联合生产过程中,与主产品或联产品相 比具有很低价值的产品。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-5

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-6

销售价值有高有低

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-4

主产品—当联合生产过程中,有一种产品与流程 中其他产品相比有较高销售价值时,我们称这种 产品为主产品。

联产品—当联合生产过程中有多种产品与其他 产品相比有较高销售价值时,这些产品称为联产 品。

16-17

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

16-18

固定毛利率可实现净值法对所有产品都采用相 同的毛利率来将联合成本分配给联产品。这种 方法是反向操作的,因为首先计算的是总毛利 率。

联合成本计算的是从每种产品的最终产品销售 价值中减去毛利和预计可分属成本的剩余金额。

16-13

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-9

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

副产品—联合生产过程中,与主产品或联产品相 比具有很低价值的产品。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-5

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-6

销售价值有高有低

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 16-4

主产品—当联合生产过程中,有一种产品与流程 中其他产品相比有较高销售价值时,我们称这种 产品为主产品。

联产品—当联合生产过程中有多种产品与其他 产品相比有较高销售价值时,这些产品称为联产 品。

16-17

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

16-18

固定毛利率可实现净值法对所有产品都采用相 同的毛利率来将联合成本分配给联产品。这种 方法是反向操作的,因为首先计算的是总毛利 率。

联合成本计算的是从每种产品的最终产品销售 价值中减去毛利和预计可分属成本的剩余金额。

16-13

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

【成本与管理会计】英文版ppt讲义1

1.2 Financial accounting and Management accounting

Management Accounting Internal managers

Day-to-day operating decisions Long-range strategic decisions

Internal - management

Size of audience

Usually large

Small

Needs of audience

Presumed

Specified

Uses of reports

Presumed

Known

1.3 Cost Accounting

▶ Cost Accounting

Chapter 1

An Introduction to Costing

Content

Topic 1 Financial accounting, Management accounting and Cost Accounting

Topic 2 Cost, Cost driver, Cost Centers and Cost Units Topic 3 Cost Classification Topic 4 Cost behaviour and Analysis Topic 5 Product costing systems

Special attention-calling and problem-solving reports

Operational - subjective

Values used

Accuracy of information

Speed of producing information

成本和管理会计 知识拓展课件(供双语教学使用)

A-12

The Profit-Maximizing Price

Under certain conditions, the profit-maximizing price can be determined using the following formula:

Profit-maximizing markup on = variable cost

A-15

The Profit-Maximizing Price

The 75 percent markup for the strawberry glycerin soap is lower than the 141 percent

markup for the apple-almond shampoo. This is because the demand for strawberry

A-5

Price Elasticity of Demand

Demand for a product is elastic if a change in price has a substantial effect on the number of units sold.

Example The demand for gasoline is relatively elastic because if a gas station raises its price,

Pricing Products and Services

Appendix A

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

A-2

Learning Objective 1

亨格瑞成本与管理会计(中英第15版)中文PPT (19)[32页]

公司也正在使用质量管理和测量方法,以求找到 有效的方法来减少空气污染、废水、石油泄漏、 有害废品处置等环境和经济成本。

产品质量也可能是环境发展的一个重要动力。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-3

1. 设计质量—衡量的是产品或服务的功能符合 顾客需求的程度。

的原因 6. 确定延迟的成本 7. 使用财务和非财务时间指标

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-2

质量—根据规格制造或执行的产品或服务的总 特征和特性,以满足顾客在购买和使用期间的 具体需求。

这些公司发现,关注一种产品或服务的质量可以 成为产品生产的专家,降低生产成本,使该产品 的顾客产生较高的满意度,并为销售这些产品的 公司带来更高的未来收益。

随机差异可能发生,例如,设备高速运转中的随 机波动会导致生产出缺陷产品。

非随机差异也会发生,一般发生在因系统问题 (如不正确的速度设定、有缺陷的零件设计,或 组成部分处理不当) 而生产出缺陷产品时。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-15

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-16

超出控制范围的观测值作为帕累托图中的输入 点。

帕累托图反映的是每种缺陷发生的频率,按照从 最经常发生到频率最小的次序排列。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

产品质量也可能是环境发展的一个重要动力。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-3

1. 设计质量—衡量的是产品或服务的功能符合 顾客需求的程度。

的原因 6. 确定延迟的成本 7. 使用财务和非财务时间指标

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-2

质量—根据规格制造或执行的产品或服务的总 特征和特性,以满足顾客在购买和使用期间的 具体需求。

这些公司发现,关注一种产品或服务的质量可以 成为产品生产的专家,降低生产成本,使该产品 的顾客产生较高的满意度,并为销售这些产品的 公司带来更高的未来收益。

随机差异可能发生,例如,设备高速运转中的随 机波动会导致生产出缺陷产品。

非随机差异也会发生,一般发生在因系统问题 (如不正确的速度设定、有缺陷的零件设计,或 组成部分处理不当) 而生产出缺陷产品时。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-15

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-16

超出控制范围的观测值作为帕累托图中的输入 点。

帕累托图反映的是每种缺陷发生的频率,按照从 最经常发生到频率最小的次序排列。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

成本和管理会计 知识拓展课件(供双语教学使用)

ቤተ መጻሕፍቲ ባይዱ

= -2.34

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

A-11

Price Elasticity of Demand

The price elasticity of demand for the strawberry glycerin soap is larger, in absolute value, than the apple-almond shampoo. This

This graph depicts how the profit-maximizing markup is generally affected by how sensitive unit sales are to price.

McGraw-Hill/Irwin

Optimal markup on variable cost

A-7

Price Elasticity of Demand

Єd =

ln(1 + % change in quantity sold) ln(1 + % change in price)

Price elasticity of demand Natural log function

McGraw-Hill/Irwin

unit sales will drop as customers seek lower prices

elsewhere.

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

A-6

= -2.34

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

A-11

Price Elasticity of Demand

The price elasticity of demand for the strawberry glycerin soap is larger, in absolute value, than the apple-almond shampoo. This

This graph depicts how the profit-maximizing markup is generally affected by how sensitive unit sales are to price.

McGraw-Hill/Irwin

Optimal markup on variable cost

A-7

Price Elasticity of Demand

Єd =

ln(1 + % change in quantity sold) ln(1 + % change in price)

Price elasticity of demand Natural log function

McGraw-Hill/Irwin

unit sales will drop as customers seek lower prices

elsewhere.

McGraw-Hill/Irwin

Copyright © 2008, The McGraw-Hill Companies, Inc.

A-6

亨格瑞成本与管理会计(中英第15版)中文PPT (20)[37页]

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

20-13

安全库存是指始终恒定的一种存货水平,而不管 经济订货量模型计算出的订货量是多少。

安全库存作为一种保护,能够防止需求的意外上升、 采购间隔期的不确定性以及供应商的产品短缺带来的 风险。

20-11

管理待售商品的第二个决策是确定订货时间。 再订货点—指需要再订货时持有存货的数量水平。

再订货点=单位时间内销售的数量×采购间隔期

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

20-12

本图表假设需求和采购间隔期是确定的; 需求=250副/周; 采购间隔期=2周。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

20-15

相关存货持有成本,此成本包括相关增量成本 和资本的相关机会成本。

相关增量成本指采购公司随存货持有数量变动 而变化的成本。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

管理待售商品的第一个决策是确定某种指定产 品的订购量。

经济订货量(EOQ)是一种决策模型,可以在一 系列假设的基础上计算订货的最优数量。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved. 20-8

最简单的经济订货量模型假设只有订货成本和持 有成本,因为这些成本是存货最一般的成本。

4. 缺货成本—当顾客需要某种产品而这种产品 又不能被提供时(缺货),公司必须迅速补充 存货以满足这一需求,否则就会发生损失。