[VIP专享]公司金融离线作业答案

公司金融课后题答案CHAPTER 18

CHAPTER 18VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRMAnswers to Concepts Review and Critical Thinking Questions1.APV is equal to the NPV of the project (i.e. the value of the project for an unlevered firm)plus the NPV of financing side effects.2. The WACC is based on a target debt level while the APV is based on the amount ofdebt.3.FTE uses levered cash flow and other methods use unlevered cash flow.4.The WACC method does not explicitly include the interest cash flows, but it doesimplicitly include the interest cost in the WACC. If he insists that the interest payments are explicitly shown, you should use the FTE method.5. You can estimate the unlevered beta from a levered beta. The unlevered beta is the betaof the assets of the firm; as such, it is a measure of the business risk. Note that the unlevered beta will always be lower than the levered beta (assuming the betas are positive). The difference is due to the leverage of the company. Thus, the second risk factor measured by a levered beta is the financial risk of the company.Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1. a.The maximum price that the company should be willing to pay for the fleet of carswith all-equity funding is the price that makes the NPV of the transaction equal tozero. The NPV equation for the project is:NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation Tax Shield)If we let P equal the purchase price of the fleet, then the NPV is:NPV = –P + (1 – .35)($140,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5Setting the NPV equal to zero and solving for the purchase price, we find:0 = –P + (1 – .35)($140,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5P = $320,068.04 + (P)(0.35/5)PVIFA13%,5P = $320,068.04 + .2462P.7538P = $320,068.04P = $424,609.54b.The adjusted present value (APV) of a project equals the net present value of theproject if it were funded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation Tax Shield)The company paid $395,000 for the fleet of cars. Because this fleet will be fullydepreciated over five years using the straight-line method, annual depreciationexpense equals:Depreciation = $395,000/5Depreciation = $79,000So, the NPV of an all-equity project is:NPV = –$395,000 + (1 – 0.35)($140,000)PVIFA13%,5 + (0.35)($79,000)PVIFA13%,5 NPV = $22,319.49NPV(Financing Side Effects)The net present value of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt, so:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Payments)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt R B. So, the NPV of the financing side effects are:NPV = $260,000 – (1 – 0.35)(0.08)($260,000)PVIFA8%,5– [$260,000/(1.08)5]NPV = $29,066.93So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects) APV = $22,319.49 + 29,066.93APV = $51,386.422.The adjusted present value (APV) of a project equals the net present value of the projectif it were funded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation Tax Shield)Since the initial investment of $1.9 million will be fully depreciated over four yearsusing the straight-line method, annual depreciation expense is:Depreciation = $1,900,000/4Depreciation = $475,000NPV = –$1,900,000 + (1 – 0.30)($685,000)PVIFA9.5%,4 + (0.30)($475,000)PVIFA13%,4 NPV (All-equity) = – $49,878.84NPV(Financing Side Effects)The net present value of financing side effects equals the aftertax present value of cash flows resulting from the firm’s debt. So, the NPV of the financing side effects are:NPV = Proceeds(Net of flotation) – Aftertax PV(Interest Payments) – PV(PrincipalPayments)+ PV(Flotation Cost Tax Shield)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, R B. Since the flotation costs will be amortized over the life of the loan, the annual flotation costs that will be expensed each year are:Annual flotation expense = $28,000/4Annual flotation expense = $7,000NPV = ($1,900,000 – 28,000) – (1 – 0.30)(0.095)($1,900,000)PVIFA9.5%,4–$1,900,000/(1.095)4+ 0.30($7,000) PVIFA9.5%,4NPV = $152,252.06So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects) APV = –$49,878.84 + 152,252.06APV = $102,373.233. a.In order to value a firm’s equity using the flow-to-equity approach, discount thecash flows available to equity holders at the cost of the firm’s levered equity. Thecash flows to equity holders will be the firm’s net income. Remembering that thecompany has three stores, we find:Sales $3,600,000COGS 1,530,000G & A costs 1,020,000Interest 102,000EBT $948,000Taxes 379,200NISince this cash flow will remain the same forever, the present value of cash flowsavailable to the firm’s equity holders is a perpetuity. We can discount at the leveredcost of equity, so, the value of the company’s equity is:PV(Flow-to-equity) = $568,800 / 0.19PV(Flow-to-equity) = $2,993,684.21b.The value of a firm is equal to the sum of the market values of its debt and equity, or:V L = B + SWe calculated the value of the company’s equity in part a, so now we need tocalculate the value of debt. The company has a debt-to-equity ratio of 0.40, whichcan be written algebraically as:B / S = 0.40We can substitute the value of equity and solve for the value of debt, doing so, wefind:B / $2,993,684.21 = 0.40B = $1,197,473.68So, the value of the company is:V = $2,993,684.21 + 1,197,473.68V = $4,191,157.894. a.I n order to determine the cost of the firm’s debt, we need to find the yield tomaturity on its current bonds. With semiannual coupon payments, the yield tomaturity in the company’s bonds is:$975 = $40(PVIFA R%,40) + $1,000(PVIF R%,40)R = .0413 or 4.13%Since the coupon payments are semiannual, the YTM on the bonds is:YTM = 4.13%× 2YTM = 8.26%b.We can use the Capital Asset Pricing Model to find the return on unlevered equity.According to the Capital Asset Pricing Model:R0 = R F+ βUnlevered(R M– R F)R0 = 5% + 1.1(12% – 5%)R0 = 12.70%Now we can find the cost of levered equity. According to Modigliani-MillerProposition II with corporate taxesR S = R0 + (B/S)(R0– R B)(1 – t C)R S = .1270 + (.40)(.1270 – .0826)(1 – .34)R S = .1387 or 13.87%c.In a world with corporate taxes, a firm’s weighted average cost of capital is equalto:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SThe problem does not provide either the debt-value ratio or equity-value ratio.H owever, the firm’s debt-equity ratio of is:B/S = 0.40Solving for B:B = 0.4SSubstituting this in the debt-value ratio, we get:B/V = .4S / (.4S + S)B/V = .4 / 1.4B/V = .29And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .29S/V = .71So, the WACC for the company is:R WACC = .29(1 – .34)(.0826) + .71(.1387) R WACC = .1147 or 11.47%5. a.The equity beta of a firm financed entirely by equity is equal to its unlevered beta.Since each firm has an unlevered beta of 1.25, we can find the equity beta for each.Doing so, we find:North PoleβEquity = [1 + (1 – t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($2,900,000/$3,800,000](1.25)βEquity = 1.87South PoleβEquity = [1 + (1 – t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($3,800,000/$2,900,000](1.25)βEquity = 2.31b.We can use the Capital Asset Pricing Model to find the required return on eachfirm’s equity. Doing so, we find:North Pole:R S = R F+ βEquity(R M– R F)R S = 5.30% + 1.87(12.40% – 5.30%)R S = 18.58%South Pole:R S = R F+ βEquity(R M– R F)R S = 5.30% + 2.31(12.40% – 5.30%)R S = 21.73%6. a.If flotation costs are not taken into account, the net present value of a loan equals:NPV Loan = Gross Proceeds – Aftertax present value of interest and principalpaymentsNPV Loan = $5,350,000 – .08($5,350,000)(1 – .40)PVIFA8%,10– $5,350,000/1.0810NPV Loan = $1,148,765.94b.The flotation costs of the loan will be:Flotation costs = $5,350,000(.0125)Flotation costs = $66,875So, the annual flotation expense will be:Annual flotation expense = $66,875 / 10 Annual flotation expense = $6,687.50If flotation costs are taken into account, the net present value of a loan equals:NPV Loan = Proceeds net of flotation costs – Aftertax present value of interest andprincipalpayments + Present value of the flotation cost tax shieldNPV Loan = ($5,350,000 – 66,875) – .08($5,350,000)(1 – .40)(PVIFA8%,10)– $5,350,000/1.0810 + $6,687.50(.40)(PVIFA8%,10)NPV Loan = $1,099,840.407.First we need to find the aftertax value of the revenues minus expenses. The aftertaxvalue is:Aftertax revenue = $3,800,000(1 – .40)Aftertax revenue = $2,280,000Next, we need to find the depreciation tax shield. The depreciation tax shield each year is:Depreciation tax shield = Depreciation(t C)Depreciation tax shield = ($11,400,000 / 6)(.40)Depreciation tax shield = $760,000Now we can find the NPV of the project, which is:NPV = Initial cost + PV of depreciation tax shield + PV of aftertax revenueTo find the present value of the depreciation tax shield, we should discount at the risk-free rate, and we need to discount the aftertax revenues at the cost of equity, so:NPV = –$11,400,000 + $760,000(PVIFA6%,6) + $2,280,000(PVIFA14%,6)NPV = $1,203,328.438.Whether the company issues stock or issues equity to finance the project is irrelevant.The company’s optimal capital structure determines the WACC. In a world wi th corporate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .80(1 – .34)(.072) + .20(.1140)R WACC = .0608 or 6.08%Now we can use the weighted average cost of capital to discount NEC’s unlevered cash flows. Doing so, we find the NPV of the project is:NPV = –$40,000,000 + $2,600,000 / 0.0608NPV = $2,751,907.399. a.The company has a capital structure with three parts: long-term debt, short-termdebt, and equity. Since interest payments on both long-term and short-term debt aretax-deductible, multiply the pretax costs by (1 – t C) to determine the aftertax coststo be used in the weighted average cost of capital calculation. The WACC using thebook value weights is:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = ($3 / $19)(.035)(1 – .35) + ($10 / $19)(.068)(1 – .35) + ($6 / $19)(.145)R WACC = 0.0726 or 7.26%ing the market value weights, the company’s WACC is:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = ($3 / $40)(.035)(1 – .35) + ($11 / $40)(.068)(1 – .35) + ($26 / $40)(.145) R WACC = 0.1081 or 10.81%ing the target debt-equity ratio, the target debt-value ratio for the company is:B/S = 0.60B = 0.6SSubstituting this in the debt-value ratio, we get:B/V = .6S / (.6S + S)B/V = .6 / 1.6B/V = .375And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .375S/V = .625We can use the ratio of short-term debt to long-term debt in a similar manner to find the short-term debt to total debt and long-term debt to total debt. Using the short-term debt to long-term debt ratio, we get:STD/LTD = 0.20STD = 0.2LTDSubstituting this in the short-term debt to total debt ratio, we get:STD/B = .2LTD / (.2LTD + LTD)STD/B = .2 / 1.2STD/B = .167And the long-term debt to total debt ratio is one minus the short-term debt to total debt ratio, or:LTD/B = 1 – .167LTD/B = .833Now we can find the short-term debt to value ratio and long-term debt to value ratio by multiplying the respective ratio by the debt-value ratio. So:STD/V = (STD/B)(B/V) STD/V = .167(.375) STD/V = .063And the long-term debt to value ratio is:LTD/V = (LTD/B)(B/V)LTD/V = .833(.375)LTD/V = .313So, using the target capital structure weights, the company’s WACC is:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = (.06)(.035)(1 – .35) + (.31)(.068)(1 – .35) + (.625)(.145)R WACC = 0.1059 or 10.59%d.The differences in the WACCs are due to the different weighting schemes. Thecompany’s WACC will most closely resemble the WACC calculated using targetweights since future projects will be financed at the target ratio. Therefore, theWACC computed with target weights should be used for project evaluation.Intermediate10.The adjusted present value of a project equals the net present value of the project underall-equity financing plus the net present value of any financing side effects. In the joint venture’s case, the NPV of financing side effects equals the aftertax present value of cash flows resulting from the firms’ debt. So, the APV is:APV = NPV(All-Equity) + NPV(Financing Side Effects)The NPV for an all-equity firm is:NPV(All-Equity)NPV = –Initial Investment + PV[(1 – t C)(EBITD)] + PV(Depreciation Tax Shield)Since the initial investment will be fully depreciated over five years using the straight-line method, annual depreciation expense is:Annual depreciation = $30,000,000/5Annual depreciation = $6,000,000NPV = –$30,000,000 + (1 – 0.35)($3,800,000)PVIFA5.13%,20 +(0.35)($6,000,000)PVIFA5,13%,20NPV = –$5,262,677.95NPV(Financing Side Effects)The NPV of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt. The coupon rate on the debt is relevant to determine the interest payments, but the resulting cash flows should still be discounted at the pretax cost of debt. So, the NPV of the financing effects is:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Repayments)NPV = $18,000,000 – (1 – 0.35)(0.05)($18,000,000)PVIFA8.5%,15– $18,000,000/1.08515 NPV = $7,847,503.56So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,262,677.95 + $7,847,503.56APV = $2,584,825.6111.If the company had to issue debt under the terms it would normally receive, the interestrate on the debt would increase to the company’s normal cost of debt. The NPV of an all-equity project would remain unchanged, but the NPV of the financing side effects would change. The NPV of the financing side effects would be:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Repayments)NPV = $18,000,000 – (1 – 0.35)(0.085)($18,000,000)PVIFA8.5%,15–$18,000,000/((1.085)15NPV = $4,446,918.69Using the NPV of an all-equity project from the previous problem, the new APV of the project would be:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,262,677.95 + $4,446,918.69APV = –$815,759.27The gain to the company from issuing subsidized debt is the difference between the two APVs, so:Gain from subsidized debt = $2,584,825.61 – (–815,759.27)Gain from subsidized debt = $3,400,584.88Most of the value of the project is in the form of the subsidized interest rate on the debt issue.12.The adjusted present value of a project equals the net present value of the project underall-equity financing plus the net present value of any financing side effects. First, we need to calculate the unlevered cost of equity. According to Modigliani-Miller Proposition II with corporate taxes:R S = R0 + (B/S)(R0– R B)(1 – t C).16 = R0 + (0.50)(R0– 0.09)(1 – 0.40)R0 = 0.1438 or 14.38%Now we can find the NPV of an all-equity project, which is:NPV = PV(Unlevered Cash Flows)NPV = –$21,000,000 + $6,900,000/1.1438 + $11,000,000/(1.1438)2 +$9,500,000/(1.1438)3NPV = –$212,638.89Next, we need to find the net present value of financing side effects. This is equal the aftertax present value of cash flows resulting from the firm’s debt. So:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Payments)Each year, an equal principal payment will be made, which will reduce the interest accrued during the year. Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, so the NPV of the financing effects are:NPV = $7,000,000 – (1 – .40)(.09)($7,000,000) / (1.09) – $2,333,333.33/(1.09)– (1 – .40)(.09)($4,666,666.67)/(1.09)2– $2,333,333.33/(1.09)2– (1 – .40)(.09)($2,333,333.33)/(1.09)3– $2,333,333.33/(1.09)3 NPV = $437,458.31So, the APV of project is:APV = NPV(All-equity) + NPV(Financing side effects)APV = –$212,638.89 + 437,458.31APV = $224,819.4213. a.To calculate the NPV of the project, we first need to find the company’s WACC. Ina world with corporate taxes, a firm’s weighted average cost of ca pital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SThe market value of the company’s equity is:Market value of equity = 6,000,000($20)Market value of equity = $120,000,000So, the debt-value ratio and equity-value ratio are:Debt-value = $35,000,000 / ($35,000,000 + 120,000,000)Debt-value = .2258Equity-value = $120,000,000 / ($35,000,000 + 120,000,000)Equity-value = .7742Since the CEO believes its current capital structure is optimal, these values can beused as the target weights in the firm’s weighted average cost of capital calculation.The yield to maturity of the company’s debt is its pretax cost of debt. To find thecompany’s cost of equity, we need to calculate the stock beta. The stock beta can becalculated as:β = σS,M / σ2Mβ = .036 / .202β = 0.90Now we can use the Capital Asset Pricing Model to determine the cost of equity. The Capital Asset Pricing Model is:R S = R F+ β(R M– R F)R S = 6% + 0.90(7.50%)R S = 12.75%Now, we can calculate the company’s WACC, which is:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .2258(1 – .35)(.08) + .7742(.1275)R WACC = .1105 or 11.05%Finally, we can use the WACC to discount the unlevered cash flows, which givesus an NPV of:NPV = –$45,000,000 + $13,500,000(PVIFA11.05%,5)NPV = $4,837,978.59b.The weighted average cost of capital used in part a will not change if the firmchooses to fund the project entirely with debt. The weighted average cost of capitalis based on optimal capital structure weights. Since the current capital structure isoptimal, all-debt funding for the project simply implies that the firm will have touse more equity in the future to bring the capital structure back towards the target.Challenge14. a.The company is currently an all-equity firm, so the value as an all-equity firmequals the present value of aftertax cash flows, discounted at the cost of the firm’sunlevered cost of equity. So, the current value of the company is:V U = [(Pretax earnings)(1 – t C)] / R0V U = [($28,000,000)(1 – .35)] / .20V U = $91,000,000The price per share is the total value of the company divided by the sharesoutstanding, or:Price per share = $91,000,000 / 1,500,000Price per share = $60.67b.The adjusted present value of a firm equals its value under all-equity financing plusthe net present value of any financing side effects. In this case, the NPV offinancing side effects equals the aftertax present value of cash flows resulting fromthe firm’s debt. Given a known level of debt, debt cash flows can be discounted atthe pretax cost of debt, so the NPV of the financing effects are:NPV = Proceeds – Aftertax PV(Interest Payments)NPV = $35,000,000 – (1 – .35)(.09)($35,000,000) / .09NPV = $12,250,000So, the value of the company after the recapitalization using the APV approach is:V = $91,000,000 + 12,250,000V = $103,250,000Since the company has not yet issued the debt, this is also the value of equity after the announcement. So, the new price per share will be:New share price = $103,250,000 / 1,500,000New share price = $68.83c.The company will use the entire proceeds to repurchase equity. Using the shareprice we calculated in part b, the number of shares repurchased will be:Shares repurchased = $35,000,000 / $68.83Shares repurchased = 508,475And the new number of shares outstanding will be:New shares outstanding = 1,500,000 – 508,475New shares outstanding = 991,525The value of the company increased, but part of that increase will be funded by the new debt. The value of equity after recapitalization is the total value of thecompany minus the value of debt, or:New value of equity = $103,250,000 – 35,000,000New value of equity = $68,250,000So, the price per share of the company after recapitalization will be:New share price = $68,250,000 / 991,525New share price = $68.83The price per share is unchanged.d.In order to v alue a firm’s equity using the flow-to-equity approach, we mustdiscount the cash flows available to equity holders at the cost of the firm’s levered equity. According to Modigliani-Miller Proposition II with corporate taxes, the required return of levered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .20 + ($35,000,000 / $68,250,000)(.20 – .09)(1 – .35)R S = .2367 or 23.67%After the recapitalization, the net income of the company will be:EBIT $28,000,000Interest 3,150,000EBT $24,850,000 Taxes 8,697,500 Net incomeThe firm pays all of its earnings as dividends, so the entire net income is availableto shareholders. Using the flow-to-equity approach, the value of the equity is:S = Cash flows available to equity holders / R SS = $16,152,500 / .2367S = $68,250,00015. a.If the company were financed entirely by equity, the value of the firm would beequal to the present value of its unlevered after-tax earnings, discounted at itsunlevered cost of capital. First, we need to find the company’s unlevered cash flows,which are:Sales $28,900,000Variable costs 17,340,000EBT $11,560,000Tax 4,624,000Net incomeSo, the value of the unlevered company is:V U = $6,936,000 / .17V U = $40,800,000b.According to Modigliani-Miller Proposition II with corporate taxes, the value oflevered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .17 + (.35)(.17 – .09)(1 – .40)R S = .1868 or 18.68%c.In a world with corporate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SSo we need the debt-value and equity-value ratios for the company. The debt-equityratio for the company is:B/S = 0.35B = 0.35SSubstituting this in the debt-value ratio, we get:B/V = .35S / (.35S + S)B/V = .35 / 1.35B/V = .26And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .26S/V = .74So, using the capital structure weights, the comp any’s WACC is:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .26(1 – .40)(.09) + .74(.1868)R WACC = .1524 or 15.24%We can use the weighted average cost of capital to discount the firm’s unlevered aftertax earnings to value the company. Doing so, we find:V L = $6,936,000 / .1524V L = $45,520,661.16Now we can use the debt-value ratio and equity-value ratio to find the value of debt and equity, which are:B = V L(Debt-value)B = $45,520,661.16(.26)B = $11,801,652.89S = V L(Equity-value)S = $45,520,661.16(.74)S = $33,719,008.26d.In order to value a firm’s equity using the flow-to-equity approach, we can discountthe cash flows available to equity holders at the cost of the firm’s levered equity.First, we need to calculate the levered cash flows available to shareholders, which are:Sales $28,900,000Variable costs 17,340,000EBIT $11,560,000Interest 1,062,149EBT $10,497,851Tax 4,199,140Net incomeSo, the value of equity with the flow-to-equity method is:S = Cash flows available to equity holders / R SS = $6,298,711 / .1868 S = $33,719,008.2616. a.Since the company is currently an all-equity firm, its value equals the present valueof its unlevered after-tax earnings, discounted at its unlevered cost of capital. Thecash flows to shareholders for the unlevered firm are:EBIT $83,000Tax 33,200Net incomeSo, the value of the company is:V U = $49,800 / .15V U = $332,000b.The adjusted present value of a firm equals its value under all-equity financing plusthe net present value of any financing side effects. In this case, the NPV offinancing side effects equals the after-tax present value of cash flows resulting fromdebt. Given a known level of debt, debt cash flows should be discounted at thepre-tax cost of debt, so:NPV = Proceeds – Aftertax PV(Interest payments)NPV = $195,000 – (1 – .40)(.09)($195,000) / 0.09NPV = $78,000So, using the APV method, the value of the company is:APV = V U + NPV(Financing side effects)APV = $332,000 + 78,000APV = $410,000The value of the debt is given, so the value of equity is the value of the companyminus the value of the debt, or:S = V – BS = $410,000 – 195,000S = $215,000c.According to Modigliani-Miller Proposition II with corporate taxes, the requiredreturn of levered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .15 + ($195,000 / $215,000)(.15 – .09)(1 – .40)R S = .1827 or 18.27%d.In order to value a firm’s equity using the flow-to-equity approach, we can discountthe cash flows available to equity holders at the cost of the firm’s levered equity.First, we need to calculate the levered cash flows available to shareholders, whichare:EBIT $83,000Interest 17,550EBT $65,450Tax 26,180Net incomeSo, the value of equity with the flow-to-equity method is:S = Cash flows available to equity holders / R SS = $39,270 / .1827S = $215,00017.Since the company is not publicly traded, we need to use the industry numbers tocalculate the industry levered return on equity. We can then find the industry unlevered return on equity, and re-lever the industry return on equity to account for the different use of leverage. So, using the CAPM to calculate the industry levered return on equity, we find:R S = R F+ β(MRP)R S = 5% + 1.2(7%)R S = 13.40%Next, to find the average cost of unlevered equity in the holiday gift industry we can use Modigliani-Miller Proposition II with corporate taxes, so:R S = R0 + (B/S)(R0– R B)(1 – t C).1340 = R0 + (.35)(R0– .05)(1 – .40)R0 = .1194 or 11.94%Now, we can use the Modigliani-Miller Proposition II with corporate taxes to re-lever the return on equity to account for this company’s debt-equity ratio. Doing so, we find:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .1194 + (.40)(.1194 – .05)(1 – .40)R S = .1361 or 13.61%Since the project is financed at the firm’s target debt-equity ratio, it must be discounted at t he company’s weighted average cost of capital. In a world with corporate taxes, a firm’s weighted average cost of capital equals:。

XXX《公司金融》在线测试

XXX《公司金融》在线测试公司金融》第01章在线测试剩余时间:38:29答题须知:1.本卷满分20分。

2.答完题后,请一定要单击下面的“交卷”按钮交卷,否则无法记录本试卷的成绩。

3.在交卷之前,不要刷新本网页,否则你的答题结果将会被清空。

第一题、单项选择题(每题1分,5道题共5分)1.下列不属于公司金融研究的内容是:A。

筹资决策B。

投资决策C。

股利决策D。

组织决策2.公司理财目标描述合理的是:A。

现金流量最大化B。

股东财富或利润最大化C。

资本利润率最大化D。

市场占有率最大化3.在公司的组织形式中,现代企业制度是指:A。

独资制B。

合伙制C。

公司制D。

股份制4.影响企业价值的两个基本因素是:A。

时间和利润B。

利润和成本C。

风险和报酬D。

风险和贴现率5.股东财富最大化目标和经理追求的目标之间总存在差异,理由是:A。

股东地域分散B。

所有权和控制权的分离C。

经理与股东年龄不同D。

以上答案均不对第二题、多项选择题(每题2分,5道题共10分)1.企业的组织形式主要有:A。

公司制B。

个体业主制C。

合伙制D。

盈利型E。

非盈利型2.公司金融管理的内容包括:A。

投资决策B。

融资决策C。

股利决策D。

资本预算决策3.在金融市场上,影响利率的因素主要有:A。

资金的供求市场B。

经济周期C。

通货膨胀D。

政府的财政和货币市场第三题、判断题(每题1分,5道题共5分)1.在个人独资企业中,独资人承担有限责任。

正确2.合伙企业本身不是法人,不缴纳企业所得税。

错误3.公司是以盈利为目的从事经营活动的组织。

正确4.股东财富最大化就是以公司股票的市场价格来衡量的。

错误5.在市场经济条件下,风险和报酬成反比,即风险越高,报酬越低。

错误交卷公司金融》第02章在线测试剩余时间:37:34答题须知:1.本卷满分20分。

2.答完题后,请一定要单击下面的“交卷”按钮交卷,否则无法记录本试卷的成绩。

3.在交卷之前,不要刷新本网页,否则你的答题结果将会被清空。

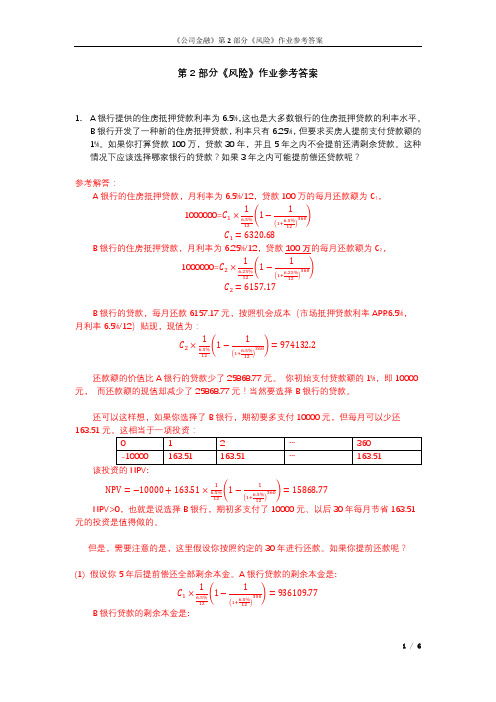

公司金融作业2参考答案

还款额的价值比 A 银行的贷款少了 25868.77 元。 你初始支付贷款额的 1%,即 10000 元, 而还款额的现值却减少了 25868.77 元!当然要选择 B 银行的贷款。 还可以这样想,如果你选择了 B 银行,期初要多支付 10000 元,但每月可以少还 163.51 元。这相当于一项投资: 0 -10000 该投资的 NPV: NPV = −10000 + 163.51 × 6.5% (1 −

2 ������������

=

������������������ ������������ ������������

=

0.8×30% 20%

= 1.2

2 / 6

《公司金融》第 2 部分《风险》作业参考答案

4. 资本市场线中,资产组合 M 是市场组合,资产组合 A 和 B 在直线上,资产组合 C 和 D 在曲线上。

12 (1+ 12 )

B 银行贷款的剩余本金是:

1 / 6

《公司金融》第 2 部分《风险》作业参考答案

1 ������2 × 6.25% (1 −

12

1

6.25% 300 (1+ 12 )

) = 933372.41

B 银行贷款的剩余本金比 A 银行少 2737.36 元。 如果选择 B 银行贷款并在 5 年后提前偿还剩余本金,相当于以下投资: 0 -10000 该投资的 NPV: NPV = −10000 + 163.51 × 6.5% (1 −

0.15*(0.36-0.1335) +0.6*(0.15-0.1335) +0.2*(-0.03-0.1335) +0.05*(-0.09-0.1335) =0.015703

浙大远程教育金融学离线作业及答案《金融学》课程作业及答案

浙大远程教育金融学离线作业及答案《金融学》课程作业及答案浙江大学远程教育学院《金融学》课程作业姓名:学号:年级:学习中心:—————————————————————————————说明:1、根据《金融学》课程的学科特点,未设置客观题。

由于金融学与实践联系较为紧密,因此在部分章节后设置了开放式学习题,要求学生在课外通过查阅相关资料,对金融的热点问题进行分析和思考,开放式学习题将作为考核中论述题的主要来源,且随着金融热点的变化而不断更新,可能会超出习题集的范围。

2、作业集的参考答案中部分题目以提供要点为限。

部分习题的详细答案请参见课件。

第一章:金融学导论与中国金融问题专题1、什么是金融创新?金融创新与金融监管的关系如何?试举一项你所了解的金融创新的例子答:一、什么是金融创新:金融创新是指变更现有的金融体制和增加新的金融工具,以获取现有的金融体制和金融工具所无法取得的潜在的利润,它是一个为盈利动机推动、缓慢进行、持续不断的发展过程。

具体的讲创新包括五种情形:(1)新产品的出现;(2)新工艺的应用;(3)新资源的开发;(4)新市场的开拓;(5)新的生产组织与管理方式的确立,也称为组织创新。

二、金融创新与金融监管的关系如何:1.金融监管刺激全融创新。

随着经济发展和金融环境的变化,过去的一些金融监管项目已经不再适应新的经济形势,而成为金融机构开展正常业务的障碍。

因此,金融机构为了求得自身的自由发展,总是千方百计绕开金融监管,在这个过程中就创造了许多新的金融工具。

这些新的金融工具极大地促进了金融领域乃至整个国民经济的发展。

2.金融创新促使金融监管不断变革。

金融创新的出现对传统金融监管体制提出了挑战。

一方面,由于传统货币政策的制定与执行要求对资产流量进行准确的测定,而新型金融工具使得这种测定失真,从而使传统的贴现率和准备金率等货币政策难以发挥作用。

另一方面,金融创新增加了金融监管的难度。

金融创新加剧了金融活动的不确定性,增大了金融风险,从而加大了金融监管的难度。

大工17秋《公司金融》在线作业3答案答案

大工17秋《公司金融》在线作业3答案答案大工17秋《公司金融》在线作业3-0001试卷总分:100得分:100一、单选题(共10道试题,共50分)1.以下各项中,不属于市盈率法优点的是()。

A.市盈率法比较直观,它将股票价格与当前公司盈利状况联系在一起B.市盈率易于计算并且容易得到C.市盈率能够作为公司风险性、成长性、资产盈利水平等特征的代表D.对于周期性公司的评估,常常出现较大的偏差正确答案:D2.某企业的应收账款周转期为30天,应付账款的平均付款天数为40天,平均存货期为50天,则该企业的现金周转期为()。

A.30天B.40天C.50天D.120天正确答案:B3.下列各项中,不属于稳健型短期投资策略的是()。

A.持有大量现金和短期证券B.保持高水平的存货投资C.放宽用条件,保持高额应收账款D.存货投资规模较小正确答案:DB.18%C.35.29%D.36.73%正确答案:D5.以下各项中,不属于实行现金扣头对企业的影响的是()。

A.缩短应收账款的均匀收账期B.增加应收账款成本C.提高资金周转速率D.减少企业的销售收入正确答案:B6.下列各项中,不属于无担保商业银行乞贷的四个基本要点的是()。

A.用限额B.周转贷协定C.利率期限D.补偿性余额正确答案:C7.在肯定规模内,下列不随现金持有量变动而变动的本钱是()。

A.机会本钱B.办理本钱C.短缺成本D.转换本钱正确答案:B8.下列各项中,不属于财务报表分析的基本程序的是()。

A.展望题目B.发现问题C.分析问题D.解决问题正确答案:A9.速动资产是流动资产扣除()后的数额。

A.泉币资金B.应收账款C.其他应收款D.存货正确答案:D10.某公司2012年度销售收入净额为6000万元。

年初应收账款余额为300万元,年末应收账款余额为500万元。

每年按360天计算,则该公司应收账款周转天数为()天。

A.15B.17C.22D.24正确答案:D二、多选题(共5道试题,共30分)1.下列各项中,属于激进型短期投资策略的是()。

公司金融参考答案

公司金融参考答案公司金融参考答案公司金融是一个复杂而又关键的领域,涉及到企业的资金运作、投资决策、财务管理等方面。

在这个竞争激烈的商业环境中,正确的金融策略和决策对于公司的发展至关重要。

本文将探讨一些常见的公司金融问题,并提供一些参考答案。

首先,让我们来看一下公司的资金运作。

资金是公司生存和发展的基础,因此,有效管理资金是至关重要的。

公司可以通过多种方式获得资金,包括债务融资和股权融资。

债务融资是指公司通过发行债券或贷款等方式来筹集资金,而股权融资则是指公司通过发行股票来融资。

在选择资金来源时,公司需要综合考虑成本、风险和可行性等因素。

其次,投资决策也是公司金融中的一个重要问题。

公司需要决定如何分配有限的资金来进行投资,以实现最大的回报。

在做出投资决策时,公司可以采用不同的方法,如净现值法、内部收益率法和投资回收期等。

净现值法是一种常用的投资评估方法,它通过计算项目现金流的现值与投资成本的差异来评估投资的可行性。

内部收益率法则是通过计算项目的内部收益率来评估投资的可行性。

投资回收期则是指项目投资所需时间来回收初始投资。

财务管理也是公司金融中的一个重要方面。

财务管理涉及到公司的资金流动、财务报表分析、风险管理等。

公司需要确保资金的流动性以满足日常运营需求,并通过财务报表分析来评估公司的财务状况和业绩。

此外,公司还需要进行风险管理,以应对可能出现的风险和不确定性。

在公司金融中,还有一些其他的问题也值得关注。

例如,公司如何制定财务目标和策略,如何管理现金流和资本结构,如何进行财务规划和预算等。

这些问题都需要公司认真思考和解决,以实现公司的长期发展目标。

总之,公司金融是一个复杂而又关键的领域,涉及到企业的资金运作、投资决策、财务管理等方面。

正确的金融策略和决策对于公司的发展至关重要。

本文提供了一些公司金融问题的参考答案,希望能够帮助读者更好地理解和应对公司金融挑战。

公司金融部考试题库及答案

公司金融部考试题库及答案一、单项选择题(每题2分,共10题)1. 公司金融中,以下哪项不是资本结构优化的目标?A. 最小化资本成本B. 最大化股东财富C. 提高公司债务比例D. 降低公司财务风险答案:C2. 在公司金融中,下列哪种融资方式不属于债务融资?A. 发行债券B. 银行贷款C. 发行股票D. 租赁融资答案:C3. 根据莫迪利亚尼-米勒定理,在没有税收的情况下,公司的资本结构对企业价值有何影响?A. 有正面影响B. 有负面影响C. 没有影响D. 影响不确定答案:C4. 公司进行股票回购的主要目的是什么?A. 增加股东权益B. 减少公司现金C. 提高每股收益D. 降低公司债务答案:C5. 以下哪项不是公司进行资本预算时考虑的现金流?A. 初始投资B. 营运现金流C. 残值D. 股东分红答案:D二、多项选择题(每题3分,共5题)1. 公司进行跨国并购时,可能面临的风险包括哪些?A. 政治风险B. 汇率风险C. 法律风险D. 市场风险答案:A、B、C、D2. 公司金融中,以下哪些因素会影响公司的资本成本?A. 无风险利率B. 市场风险溢价C. 公司财务杠杆D. 通货膨胀率答案:A、B、C3. 在公司金融中,以下哪些属于非公开市场融资方式?A. 私募股权B. 风险投资C. 公开发行股票D. 银行贷款答案:A、B4. 公司进行财务分析时,常用的比率分析包括哪些?A. 流动比率B. 资产负债率C. 净资产收益率D. 市盈率答案:A、B、C5. 公司进行项目投资决策时,常用的评估方法包括哪些?A. 净现值法B. 内部收益率法C. 回收期法D. 会计收益率法答案:A、B、C三、简答题(每题5分,共2题)1. 简述公司进行资本预算时,为何需要考虑货币的时间价值。

答案:在资本预算过程中,公司需要评估不同时间点的现金流。

由于货币具有时间价值,即一定量的货币在今天比在未来具有更高的价值,因此,在评估项目的投资回报时,必须将未来的现金流折现到当前价值,以反映资金的时间价值。

免费在线作业答案大工15秋《公司金融》在线作业1满分答案

大工15秋《公司金融》在线作业1满分答案一、单选题(共 10 道试题,共 50 分。

)1. 所有权和管理权实现分离的企业形式是()。

A. 个体业主制企业B. 一般合伙制企业C. 有限合伙制企业D. 公司制企业正确答案:D大众理财作业满分答案2. 现代公司金融管理的目标是以()最大化为标志的。

A. 公司价值B. 社会责任C. 税后利润D. 资本利润率正确答案:A3. 下列评价指标中,没有考虑货币时间价值的是()。

A. 净现值B. 投资回收期C. 内含报酬率D. 获利指数正确答案:B4. 在下列各项年金中,只有现值没有终值的年金是()。

A. 普通年金B. 即付年金C. 永续年金D. 先付年金正确答案:C5. 财务管理的目标是使股东财富最大化,而反映这一目标的最佳指标是()。

A. 每股盈余B. 税后净利润C. 股票市价D. 留存收益正确答案:C6. 现有甲、乙两个投资项目,其报酬率的期望值分别为15%和23%,标准差分别为30%和33%,那么()。

A. 甲项目的风险程度大于乙项目的风险程度B. 甲项目的风险程度小于乙项目的风险程度C. 甲项目的风险程度等于乙项目的风险程度D. 不能确定正确答案:A7. 财务经理解决如何在商品市场上进行实物资产投资,为公司未来创造价值的问题,属于()。

A. 投资决策B. 融资决策C. 股利决策D. 资本结构决策正确答案:A8. 下列选项中属于普通年金的是()。

A. 永续年金B. 预付年金C. 每期期末等额支付的年金D. 每期期初等额支付的年金正确答案:C9. 货币时间价值大小的影响因素是()。

A. 复利B. 单利C. 汇率D. 资金额正确答案:D10. 标准差测度的是()。

A. 总体风险B. 不可分散的风险C. 非系统风险D. 系统风险正确答案:A大工15秋《公司金融》在线作业1二、多选题(共 5 道试题,共 30 分。

)1. 下列各项中,属于年金形式的项目有()。

A. 零存整取储蓄存款的整取额B. 定期定额支付的养老金C. 年投资回收额D. 偿债基金E. 非定期购买股票正确答案:BCD2. 按利率变动与市场的关系,利率可分为()。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

浙江大学远程教育学院《公司金融》课程作业答案第一章公司金融学导论一、思考题1.现代企业有几种组织形式,各有什么特点?答案:企业的基本组织形式有三种,即个人独资企业、合伙企业和公司企业。

(1)个人独资企业是指由一个自然人投资,财产为投资人个人所有,投资人以其个人财产对企业债务承担无限责任的经营实体。

(2)合伙企业是由各合伙人订立合伙协议,共同出资,合伙经营,共享收益,共担风险,并对合伙企业债务承担连带无限责任的营利组织。

(3)不论个人独资企业还是合伙企业,都没有独立于企业所有者之外的企业财产,由于这个原因它们统称为自然人企业。

它们的优点在于,企业注册简便,注册资本要求少,经营比较灵活。

缺点,一个是资金规模比较小,抵御风险的能力低。

另一个是企业经营缺乏稳定性,受企业所有者个人状况影响很大。

(4)公司企业是具有法人地位的企业组织形势。

公司拥有独立的法人财产,独立承担经济责任。

相对于自然人企业,公司企业具有巨大优越性。

尽管公司这种企业组织形势具有优势,但是也有弊端,其弊端有:重复纳税。

公司的收益先要交纳公司所得税;税后收益以现金股利分配给股东后,股东还要交纳个人所得税。

内部人控制。

所谓内部人指具有信息优势的公司内部管理人员。

经理们可能为了自身利益而在某种程度上侵犯或者牺牲股东利益。

信息披露。

为了保护股东以及债权人的利益,公司经理人必须定期向股东和投资者公布公司经营状况,接受监督。

2.在股东财富最大化目标下,如何协调债权人、股东与经理人之间的利益冲突?答案:(1)现代公司制的一个重要特征是所有权与经营权的分离,虽然两权分离机制为公司筹集更多资金、扩大生产规模创造了条件,并且管理专业化有助于管理水平的提高,但是不可避免地会产生代理问题。

一方面股东与经理人的利益目标并不完全一致,经理人出于使自身效用最大化的活动可能会损害股东利益;另一方面,股东与公司债权人之间也存在利益冲突,为了追求财富最大化,股东可能要求经理采取不利于债权人利益的行动。

(2)为了使经理人按股东财富最大化的目标进行管理和决策,股东必须设计有效率的激励约束机制,其中以对经理人的激励为主,除了公司内部的激励机制外,公司外部资本市场和经理市场的存在也可以促使经理把公司股票价格最高化作为经营目标。

具体来讲,以下几个渠道可以在一定程度上缓解经理人对股东利益的侵犯:经理市场、经理人被解雇的威胁、公司被兼并的威胁、对经理的奖励--绩效股、财务信息公开制度。

(3)债权人为维护自己的利益,一是要求风险补偿,提高新债券的利率;二是在债券合同中加进许多限制性条款,如在企业债务超过一定比例时,限制企业发行新债券和发放现金股利,不得投资于风险很大的项目以免股东把风险转嫁到债权人身上;第三,分享权益利益。

债权人可以在购买债券的同时购买该公司的股票,或者债券附属的认股权证,或者可转换证券,从而使自己持有该公司部分权益。

二、单项选择题答案1. C.2.C.3. D.4.B.第二章公司财务报表一、基本概念答案1.流动比率:是指能在一年内变现的资产(流动资产)与一年内必须偿还的负债(流动负债)的比值。

2.速动比率:是指速动资产与流动负债的比值。

表示每1元流动负债有多少速动资产作为偿还的保证,进一步反映流动负债的保障程度。

3.市盈率:市盈率是普通股每股市价与每股盈余之比。

4.市净率:市净率是反映每股市价与每股净资产关系的比率。

二、思考题1.如何对企业偿债能力进行分析?答案:反映企业偿债能力的指标有:(1)流动比率:流动比率是指能在一年内变现的资产(流动资产)与一年内必须偿还的负债(流动负债)的比值。

一般而言,流动比率越高,公司的短期偿债能力也越强。

从理论上讲,流动比率接近于2比较理想。

(2)速动比率:是指速动资产与流动负债的比值。

影响速动比率的重要因素是应收账款的变现能力。

传统经验认为,速冻比率为1时是安全边际。

(3)应收账款周转率,也就是年度内应收账款转为现金的平均次数。

(4)现金比率是指企业的现金与流动负债的比例。

现金比率是衡量企业短期偿债能力的一个重要指标(5)资产负债率:资产负债率是综合反映企业偿债能力,尤其是反映企业长期偿债能力的重要指标。

它是指企业的负债总额与资产总额之间的比率。

2.如何对企业营运情况进行分析?答案:反映企业运营能力的指标有:(1)存货周转率:是公司在某一会计报告期内的主营业务成本和平均存货余额的比例,通过该项指标可以衡量公司存货是否适量,从而对公司商品的市场竞争力、公司的推销能力和管理绩效有一个基本的估计和判断。

同时它还是衡量公司短期偿债能力的一个重要参考指标。

一般来说,存货周转率越快,周转天数越少,公司就能获取更高的利润,并具备较强的短期偿债能力。

(2)固定资产周转率也叫固定资产利用率,是企业销售收入与固定资产净值的比率。

(3)总资产周转率是销售收入与平均资产总额的比率。

该项指标反映资产总额的周转速度。

周转越快,反映利用效果越好,销售能力越强,进而反映出企业的偿债能力和盈利能力令人满意。

(4)股东权益周转率是销售收入与平均股东权益的比值。

该指标说明公司运用所有者的资产的效率。

该比率越高,表明所有者资产的运用效率高,营运能力强。

(5)主营业务收入增长率是本期主营业务收入与上期主营业务收入之差与上期主营业务收入的比值。

主营业务收入增长率可以用来衡量公司的产品生命周期,判断公司发展所处的阶段。

3.利用现金流量表可以分析企业哪些事项?答案:(1)现金流量表是以现金为基础、遵循收付实现制原则而编制的,即以企业现金的收到或支付作为企业资产、负债和所有者权益进行计量、确认和记录的标准。

(2)利用现金流量表,可以分析企业的下列事项:第一、企业本期获取现金的能力和在未来会计期间内产生现金净流量的能力。

第二、企业的偿债能力、支付投资报酬能力和融资能力。

第三、企业的净收益与营业活动所产生的净现金流量发生差异的原因。

第四、企业在会计期间投资、融资活动等重要的经济活动情况以及对财务状况产生的影响。

第三章货币时间价值与风险收益一、基本概念答案:1.时间价值:货币的时间价值是指货币经历一定时间的投资和再投资所增加的价值,也称为资金的时间价值。

2.年金:年金是指在某一确定的时期里,每期都有一笔相等金额的收付款项。

年金实际上是一组相等的现金流序列:一般来说,折旧、租金、利息、保险金、退休金等都可以采用年金的形式。

3. 相关系数被用来描述组合中各种资产收益率变化的相互关系,即一种资产和另一种资产的收益率变化关系。

二、思考题1.答案:见教材第50页。

2.答案见教材第50-51页。

三、计算题教材57页练习题6、7、86.答案:设复利计息,则第五年年末的本利和为=本金*复利终值系数=10000*1.6105=16105元。

7.答案:设每年的偿还金额为A,则A=10000/年金现值系数=10000/4.3553=2296元。

8.答案:这个问题属于递延年金问题。

答案:现值=1000000*3.7908*0.6209=2353707元。

第四章公司资本预算一、基本概念答案1.现金流量:现金流量是指现金支出和现金收入的数量。

在此基础上,现金流入量减去现金流出量的差额机形成净现金流量。

2.静态投资回收期:是在不考虑资金时间价值的条件下,以项目生产经营期的资金回收补偿全部原始投资所需要的时间。

通常以年为单位,是反映项目资金回收能力的主要静态指标。

3.折现投资回收期:是指在考虑货币时间价值的条件下,以投资项目净现金流量的现值抵偿原始投资现值所需要的全部时间。

4.净现值:是在项目计算期内按设定的折现率或资金成本计算的各年净现金流量现值的代数和,记作NPV。

5.内部收益率:内部收益率可定义为使项目在寿命期内现金流入的现值等于现金流出现值的折现率,也就是使项目净现值为零的折现率,用IRR 表示。

6.盈亏平衡分析:盈亏平衡分析就是通过计算达到盈亏平衡状态的产销量、生产能力利用率、销售收入等有关经济变量,分析判断拟建项目适应市场变化的能力和风险大小的一种分析方法。

其中又以分析产量、成本和利润为代表,所以也俗称为“量本利”分析。

7.敏感性分析:敏感性分析是考察与投资项目有关的一个或多个主要因素发生变化时,对该项目经济效益指标影响程度的一种分析方法。

进行这种风险分析的目的在于:寻找敏感性因素,判断外部敏感性因素发生不利变化时投资方案的承受能力。

二、思考题:1.投资项目现金流量的构成。

答案:从现金流量的发生方向看,它可以包含如下几个部分:(1)现金流出量:包括固定资产投资、无形资产投资、递延资产投资、流动资产投资;(2)现金流入量包括:营业现金流入、回收固定资产残值和回收流动资金。

按照现金流量发生的投资阶段,又可划分为:(1)初始现金流量:开始投资时发生的现金流量。

如固定资产投资、流动资产垫支等,一般表现为现金流出。

(2)营业现金流量:投资项目投入使用后,由于生产经营所带来的现金流入和流出的数量。

营业现金净流量:营业现金净流量=营业现金收入-付现成本-所得税=税后净收入+折旧费(3)终结现金流量:投资项目终结时发生的现金流量。

如固定资产的残值收入,回收的流动资产垫资、停止使用的土地出卖收入等,一般表现为现金流入2.净现值法与内部收益率法的判断准则,两种方法有何区别?答案:(1)净现值法的使用原则:当NPV≥0时,投资项目在经济上是可行的;当NPV≤0时,项目不具备经济可行性。

这一原则是明确的,广泛适用于独立项目的投资决策。

(2)内部收益率的判断准则是:IRR 大于、等于筹资的资本成本,即IRR≥ic,项目可接受;若IRR 小于资本成本,即IRR<ic,则项目不可接受。

(3)二者的区别在于计算方法的不同:NPV是先给出折现率,再求净现值;IRR是先给出NPV=0,然后计算内部收益率;一个是绝对量指标,而另一个是相对指标。

尽管他们在经济意义上类似,但是IRR的使用受到来自技术因素方面的限制。

三、计算题:教材83-84页练习题:4答案:(1)设备的内含收益率:年金现值系数=8000/1260=6.3492,查表可知,当使用年限为8年时,6.3492对应的折现率介于5%与6%之间,使用插值法计算,内含收益率为5.85%。

(2)设备的使用年限,当内含收益率为10%时,年金现值系数6.3492对应的年限介于10和11之间,使用插值法计算,设备至少约使用10.6年。

6.答案:(1)当贴现率为10%时,计算两个项目的净现值。

项目A的净现值为:5×3.7908-15=3.954万元项目B的净现值:12×0.9091+2.5×(0.8264+0.7513+0.6830+0.6209)-15=3.11万元按照净现值法选择,项目A为最佳投资决策。

(2)计算两个项目的内部收益率:当净现值为0时,项目A的年金现值系数=15/5=3,当使用年限为5年时,3对应的折现率介于18%和20%之间,使用插值法计算其内部收益率为19.86%。