财务报表分析英文课件Chap5

财务报表分析 英文ppt课件

By ledger, complete P&L and B/S forecast by month

Includes Cost of Quality, Cost Savings and Economics projections

Final Results

Versus Versus Versus Versus While While

Current Profit Increase Current Profit Increase Increase Of Return On Investment Increase Liquidity Minimizing Capital Expenditures The Day-to-day Business Needs

($0.2) $0.5 $0.0 $0.5 $0.8 -0.8%

Other Inc/Exp Admin / Cap Charge

($2.0) ($4.0)

($1.8) ($4.0)

($0.2) $0.0

Operating Profit ROS %

$39.0 15.6%

$37.1 15.3%

$1.9 0.3%

N Tax Manager

North Asia

O Tax Manager

India

P Director of Finance North Asia (Team of 5)

Q Country Controller

India (Team of 5)

R Finance Manager (20%)

Taiwan

S Tax Manager Asia Pacific

财务报表分析英文课件Chap5

How to increase ROA?-2

The evolution of ROA in the U.S.

the graphs in the next few slides are from Penman and Nissim Review of Accounting Studies, 2019

4. The average ratio for other firms in the same industry (cross-section analysis)

Analysis of Profitability a. Return on assets (ROA): return to the firm

Accounts receivable turnover

• Measures how quickly a firm collects cash. • If A.R. turn over twice a year, then they average one half of a year in

collection. • Less time is preferred to more. • A high turnover is preferred to a low one. • The days of outstanding for account receivables: 365 days/accounts

COGS-to-Sales ratio Selling, General and administrative (SGA) expense-tosales ratio Etc.

By observing the time series and cross-section of each expense-to-sales ration, one can identify abnormal ratios and investigate the reasons, in order to control costs and expenses to increase PM

财务报表分析ChapPPT课件

净利

营业活动 = 现金流量 +

应计数

© The McGraw-Hill Companies, Inc., 2010

应计制—会计的基础

应计制会计的架构

收入认列-收入认列当 (1) 已赚得 (2) 不论是否已实现

费用配合-应与其对应的收入相配合 -产品成本 -期间成本

© The McGraw-Hill Companies, Inc., 2010

• 货币计量假设 – 会计主体在财务会计确认、计量和报告时均采用货币为 计量单位,反映会计主体生. 产经营活动价值方面的表现

1-16

第3节 制约企业报表编制的一般会计原则

客观性(objectivity)原则 相关性(relevance)原则 明晰性(clarity)原则 可比性(comparability)原则 实质重于形式(substance over form)原则 重要性(materiality)原则 谨慎(prudence)原则 及时性(timeliness)原则 权责发生制(accrual basis)原则

应采用最不乐观的看法

FASB

© The McGraw-Hill Companies, Inc., 2010

应计制会计-范例

范例说明

• 购买素面 T 恤及设备 $700 • 素面 T 恤每件 $5 • 彩绘 T 恤的固定设备成本 $100 • 彩绘 T 恤的变动成本每件 $0.75 • 售出 25 件 T 恤每件 $10,现金支付 • 售出 25 件 T 恤每件 $10,下周支付

–建造合同当期预期损失的原因和金额

• 所得税的会计处理方法

• 合并报表的说明

.

1-13

• 三、审计报告

– 注册会计师根据独立审计准则的要求,在实施了 必要审计程序后出具的,用于对被审计单位年度 财务报表发表审计意见的书面文件

财务报表分析英文课件

Examines the purchase and redemption of treasury stock and its impact on the financial statements

Income statement analysis

Revenue Recognition

Examining the methods and timelines of revenue recognition to ensure it complies with Generally Accepted Accounting Principles (GAAP)

Distinguishing between direct and indirect costs to better understand the impact of each on the capability of specific products or services

Direct vs. Indirect Costs

Investment in Property, Plant, and Equipment: This category includes cash outflows related to the purchase of fixed assets, such as property, plant, and equipment

财务报表分析-英文

Introduction and Basic Concepts

Business Partnership Vision Strategy Budget Forecast

Others Treasury M&A Risk Management Insurance Auditing Compliance Hedging ….

Introduction and Basic Concepts

Minimize Working Capital Maintain Strong Cash Flow

Pay Debts As They Are Due Increase Liquidity

Maintain Strong Financial Position

Introduction and Basic Concepts

导言及基本概念 Introduction and Basic Concepts Introduction Finance Organization Finance Activity Other topics

This training will allow you to understand: Finance Function Concept of Financial KPIs (Revenue, DM, DL, VOH, FOH, SG&A, OI, OCF, EBITDA, DOH, DSO, DPO, Incremental, etc.) BS, P&L and Cash Flow Statements Concepts of Financial Statement Evaluation and Investment Appraisal

财务分析报告英文版ppt课件

可编辑课件PPT

2

CHINT ELECTRICS Is China's largest production of

low voltage electric appliance manufacturing enterprise, the specialty is engaged in distribution appliances, control electric appliances, terminal apparatus, and power electronic and electric power supply low-voltage products development, production and sales. Chint is recognized for a famous Chinese trademark, chint brand universal type circuit breaker, plastic shell type breaker series product has been awarded "China famous brand product" title. The company in 2004 won the Chinese quality management of the highest award, the national quality management award

17.83% 0.48% 0.09% 18.41% 43.10%

12.03% 28.24% 2.98% 11.83% 55.06% 1.84% 56.90% 100.00%

Balance Sheet Vertical Common-size Analysis

企业财务会计分析(ppt 24页)(英文版)

Efficient Capital Markets

• Switches gears

• Past lectures decided how to spend money (invest)

• Today’s lecture deal with raising money (financing decisions)

180

130

80 Month

Level

Random Walk Theory

S&P 500 Five Year Trend? or

5 yrs of the Coin Toss Game?

230

180

130

80 nt Market Theory

Fundamental Analysts

Rights Issue - example

• YRU Corp currently has 9 million shares outstanding. The market price is $15/sh. YRU decides to raise additional funds via a 1 for 3 rights offer at $12 per share. If we assume 100% subscription, what is the value of each right?

Prospectus - Formal summary that provides information on an issue of securities.

Underpricing - Issuing securities at an offering price set below the true value of the security.

财务报表分析英文课件Cha

ROCE: return to common

Shareholders on7ly

Return on Assets (ROA)

ROA presents profitability independent of the source of financing – Does not consider leverage – Measure of how well the firm uses its assets to generate income – As if the firm is financed by equity alone

What to compare?

1. The planned ratio for the period

2. The corresponding ratio from a prior period (time-series analysis)

3. The corresponding ratio for another firm in the same industry (cross-section analysis)

as a whole

b. Return on common equity (ROCE): return to common shareholders only

c. Earnings per common share

.

6

Analysis of Profitability

ROA: return to .the firm

risk of investment alternatives, and the role of analysis in providing risk and return information.

财务报表分析 英文

Financial Statement AnalysisIntroductionFinancial statement analysis is a crucial tool for assessing the financial performance and stability of a company. By analyzing a company’s financial statements, investors and other stakeholders can gain insights into its profitability, liquidity, solvency, and overall financial health. This document provides an overview of financial statement analysis, including the different types of financial statements, key financial ratios used in analysis, and the importance of using a systematic approach for analyzing financial statements.Types of Financial StatementsFinancial statements are a collection of reports that provide a snapshot of a company’s financial position and performance over a specific period. The three main types of financial statements include:1. Balance SheetThe balance sheet is a statement that shows the financial position of a company at a given point in time. It provides information about a company’s assets, liabilities, and shareholders’ equity. The balance sheet is divided into two main se ctions: the left side shows the company’s assets, while the right side shows its liabilities and shareholders’ equity.2. Income StatementThe income statement, also known as the profit and loss statement, reports a company’s revenues, expenses, and net in come over a specific period. It provides insights into a company’s profitability and helps identify trends in its revenue and expenses. The income statement follows a simple equation: revenues minus expenses equal net income.3. Cash Flow StatementThe cash flow statement shows the inflows and outflows of cash in a company over a specified period. It provides information about a company’s operating, investing, and financing activities. The cash flow statement helps assess a company’s ability to generate cash and its liquidity.Key Financial RatiosFinancial ratios are used to analyze the relationships between different items in a company’s financial statements. They help evaluate a company’s financialperformance, efficiency, liquidity, and solvency. Some key financial ratios used in financial statement analysis include:1. Profitability RatiosProfitability ratios measure a company’s ability to generate profits. Common profitability ratios include gross profit margin, operating profit margin, and net profit margin.2. Liquidity RatiosLiquidity ratios assess a company’s ability to meet its short-term obligations. These ratios include the current ratio and quick ratio.3. Solvency RatiosSolvency ratios evaluate a company’s long-term financial stability and ability to meet its long-term obligations. Examples of solvency ratios include the debt-to-equity ratio and the interest coverage ratio.4. Efficiency RatiosEfficiency ratios measure a company’s ability to utilize its assets and resources effectively. Examples include the inventory turnover ratio and the accounts receivable turnover ratio.Systematic Approach for Financial Statement AnalysisTo conduct an effective financial statement analysis, it is important to follow a systematic approach. The key steps in this approach include:1. Gathering Financial StatementsCollect the company’s financial statements, including the balance sheet, income statement, and cash flow statement.2. Analyzing Financial RatiosCalculate the relevant financial ratios and analyze them to assess the company’s financial performance and condition.3. Comparing RatiosCompare the calculated financial ratios with industry averages or with the company’s historical performance to identify trends and benchmark the company’s performance.4. Conducting a Trend AnalysisAnalyze the company’s financial statements over multiple periods to identify any significant changes or trends in its financial performance.5. Making Informed DecisionsBased on the analysis of the financial statements and ratios, make informed decisions about the company’s financial health, investment potential, and future prospects.ConclusionFinancial statement analysis is an important tool for assessing a company’s financial performance and stability. By analyzing a comp any’s financial statements and calculating key financial ratios, investors and stakeholders can make informed decisions about the company’s financial health, stability, and investment potential. Following a systematic approach for financial statement analysis ensures a comprehensive evaluation and helps identify trends and benchmarks for comparison.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Year 4 $ 475

280 53 22 18 16 - 16 389 - 16 = 373 86 + 16 = 102 26 + 4.8 = 30.8 60 + 16 – 4.8 = 71.2

Horrigan Corporation ROA

Average total assets of this company in year 4 (520+650)/2 = 585,

as a whole

b. Re common shareholders only

c. Earnings per common share

Analysis of Profitability

ROA: return to the firm

The value of a firm to equity investors

risk

V = D1/(1+r) + D2/(1+r)2 + D3/(1+r)3 …….

profitability

The value of a firm to creditors

risk

V = I1/(1+r) + I2/(1+r)2 + I3/(1+r)3 + P/(1+r)3

Horrigan Corporation

Sales Revenue Less expense:

COGS Selling Administrative Depreciation Interest Total Next income before tax Income tax expense Next Income

profitability

Ii: interest revenues in period i P: return of principal

Financial Statement Analysis

1.Understand the relation between the expected return and

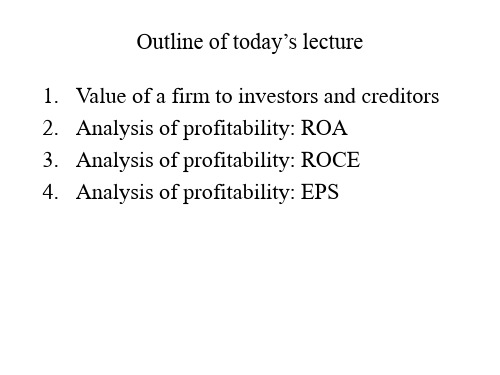

Outline of today’s lecture

1. Value of a firm to investors and creditors 2. Analysis of profitability: ROA 3. Analysis of profitability: ROCE 4. Analysis of profitability: EPS

Then ROA = 71.2/585 = 12.2%

Why add back interest income net of income tax savings in the numerator?

1) If all equity, the firm won’t pay $16 interest expense,

risk of investment alternatives, and the role of analysis in providing risk and return information.

2. Understand the usefulness of the rate of return on assets (ROA) as a measure of a firm’s operating profitability.

which increase net income by $16; 2) at 30% tax rate, government will collect an additional amount of $4.8 (16*30%) as tax, then the actual increase of net income is (16 – 4.8).

3. Understand the usefulness of the rate of return on common shareholders’ equity (ROCE) as a measure of profitability.

4. Understand the strengths and weaknesses of earnings per common share as a measure of profitability.

What to compare?

1. The planned ratio for the period

2. The corresponding ratio from a prior period (time-series analysis)

3. The corresponding ratio for another firm in the same industry (cross-section analysis)

4. The average ratio for other firms in the same industry (cross-section analysis)

Analysis of Profitability a. Return on assets (ROA): return to the firm

ROCE: return to common

Shareholders only

Return on Assets (ROA)

ROA presents profitability independent of the source of financing – Does not consider leverage – Measure of how well the firm uses its assets to generate income – As if the firm is financed by equity alone

Year 4 $ 475

280 53 22 18 16 389 86 26 60

Horrigan Corporation-assuming no debts

Sales Revenue Less expense:

COGS Selling Administrative Depreciation Interest Total Next income before tax Less Income tax expense Next Income