Sales Overview for Double-Take Availability for AIX -2011-2-23

英语作文-销售中的销售技巧与产品知识了解

英语作文-销售中的销售技巧与产品知识了解Effective Sales Techniques and Product Knowledge in Sales。

In the realm of sales, success hinges not just on persuasive communication but also on profound product knowledge. Sales professionals who master both these facets can significantly enhance their ability to close deals and build lasting client relationships. This article delves into the crucial skills and knowledge that elevate sales effectiveness, offering insights into how these elements synergize to drive results.Firstly, impeccable product knowledge forms the cornerstone of successful selling. When a salesperson thoroughly understands the features, benefits, and unique selling points of their offerings, they can articulate value propositions with clarity and confidence. This knowledge empowers them to address customer inquiries comprehensively, overcoming objections and positioning the product or service as the optimal solution. For instance, in technology sales, understanding specifications, compatibility, and performance benchmarks allows the salesperson to align customer needs precisely with product capabilities, fostering trust and credibility.Moreover, effective sales techniques complement product knowledge by structuring interactions for maximum impact. Active listening stands out as a foundational skill, enabling sales professionals to grasp client requirements, preferences, and pain points. By listening attentively, they can tailor their pitch to resonate deeply with the prospect's needs, presenting solutions that are not only relevant but also compelling. This personalized approach demonstrates empathy and enhances the likelihood of converting prospects into satisfied customers.Furthermore, the ability to communicate persuasively is pivotal in sales engagements. Clear and concise communication ensures that the benefits of the product or service are communicated effectively without overwhelming the prospect with unnecessary details. Using language that resonates with the prospect's industry-specific terminology or pain points can establish a shared understanding and reinforce the salesperson's expertise.In addition to verbal communication, non-verbal cues such as body language and tone of voice play crucial roles in conveying confidence and sincerity. A confident demeanor instills trust in the prospect, while sincerity fosters a genuine connection, paving the way for a more collaborative relationship. By maintaining a positive and engaging presence throughout the sales process, from initial contact to closing the deal, sales professionals can create a memorable and impactful experience for the client.Furthermore, adapting to different selling situations is essential for navigating varied client personalities and preferences. The ability to switch between consultative selling, where the emphasis is on problem-solving and relationship-building, and transactional selling, which focuses on efficient closure, demonstrates versatility and agility. This adaptive approach enables sales professionals to cater to diverse customer needs and preferences effectively, maximizing their chances of success in different sales scenarios.Lastly, continuous learning and self-improvement are indispensable for staying ahead in the dynamic field of sales. Keeping abreast of industry trends, competitor offerings, and evolving customer expectations allows sales professionals to offer informed recommendations and anticipate future needs. Embracing feedback and leveraging training opportunities further enhances skills and ensures ongoing professional growth.In conclusion, mastery of sales techniques and comprehensive product knowledge are indispensable for achieving sales success. By combining deep understanding of their offerings with refined communication skills and a customer-centric approach, sales professionals can build trust, drive engagement, and consistently deliver value to their clients. Continuous improvement and adaptability further cement their ability to thrive in competitive markets, ensuring sustained success and profitability.。

SAP01_SAP_Overview_Part3

Lesson:Sales Order ManagementLesson OverviewIn this lesson you will gain an understanding of the Sales Order processes and howSales Order Management is integrated within other solutions.Lesson ObjectivesAfter completing this lesson,you will be able to:•Outline the tasks associated with sales order management•Explain how SAP within mySAP ERP supports the key processes in sales order managementBusiness ExampleYour company,IDES,is selling products to various customers.Timely handlingand delivery of sales orders is key to their business success.Sales Order Process OverviewmySAP ERP provides superior insight into sales back-office processes,including:inquiries,quotations,order generation,contract,and billing cycle management.Businesses benefit from a complete overview of the customer life cycle,including order status,billing,payment,and credit management.In addition tothe back-office features,mySAP ERP also supports Internet sales,sales enteredthrough mobile devices such as handhelds,and basic call center functionality.The Sales Order Processing(or order to cash)scenario describes the completeprocess,starting with pre-sales activities,moving to the creation of the sales order,continuing with the sales order fulfillment,and ending with the invoicing of thesales order and the parallel process of the creation of the posting in financialaccounting.The basic sales order processing cycle for a service or material consists of thefollowing phases:Pre-Sales ActivitiesPre-sales activities can be inquiries or quotations entered in the system.These canthen be used as reference during the creation of a sales order.Sales Order Creation and Availability CheckThe sales order can adopt information from the pre-sales documents(a quotationor an inquiry).Sales scheduling agreements or sales contracts(long-term salesagreements)can also be created with reference to a sales order and are supportedby the sales process steps.During the creation of the sales order,the availability of the material can be checked to confirm the customer's requested delivery date.Figure45:Sales Order ManagementDelivery and Goods IssueAn outbound delivery is the basis for a process when the goods are physically moved as well as for the posting of the goods issue.Picking can be fulfilled through the use of the Warehouse Management system and transportation can be planned and carried out.BillingAs the final step in the sales process,an invoice is issued,which must also be reflected in accounting.Sales OrderDuring sales order creation,the system can carry out basic functions:•Monitoring sales transaction•Checking for availability•Transferring requirements to material requirements planning(MRP)•Scheduling delivery•Calculating pricing and taxes•Checking credit limits•Creating printed or electronically transmitted documentsFigure46:Sales OrderDepending on how the system is configured,these basic functions may be completely automated or may require some manual processing.The data resulting from these basic functions(for example,shipping dates,confirmed quantities, prices,and discounts)is stored in the sales document.The resulting data can be displayed by a user and,in some cases during subsequent processing,manually changed by the user.DeliveryShipping is an important part of the logistics chain.In shipping processing,all delivery procedure decisions can be made at the start of the process by:•Taking into account general business agreements with your customer •Recording special material requests•Defining shipping conditions in the sales orderThe result is an efficient and largely automatic shipping process in which manual changes are necessary only under certain circumstances.Figure47:Delivery and Goods IssueShipping FunctionsThe shipping module supports the following functions,which include but arenot limited to:•Deadline monitoring for reference documents due for shipment(sales orders and purchase orders,for instance)•Creating and processing outbound deliveries•Packing deliveries•Information support for transportation planning•Supporting foreign trade requirements•Printing and transmitting shipping documents•Processing goods issue•Deliveries currently in process•Activities that are still to be carried out•Identifying possible bottlenecksThe most commonly used document used to support delivery processed is the Outbound Delivery document.In its role as central object of the goods issue process,outbound delivery supports all shipping activities,including picking, packing,transportation,and goods issue.During the outbound delivery process, shipping-planning information is recorded,status of shipping activities is monitored,and data accumulated during shipping processing is documented. When the outbound delivery is created,the shipping activities,such as pickingor delivery scheduling,are initiated,and data that is generated during shipping processing is included in the delivery.Range of FunctionsAn outbound delivery can be created as follows:•With reference to a sales order•With reference to a stock transport order•With reference to a subcontract order•With reference to a project•Without any referenceDepending on your requirements,you can create outbound deliveries automatically or manually using worklists.You can make agreements with your customers for complete and partial deliveries and for order combinations.Outbound deliveries can be combined to form a single group of deliveries.A variety of warehouse and sales overview reports allow you to monitor created outbound deliveries and outstanding sales activities.Picking the DeliveryThe picking process involves taking goods from a storage location and staging the goods in a picking area where the goods will be prepared for shipping.Picking FunctionsSystem settings will allow picking to be carried out:•Automatically(during outbound delivery creation)•Routinely(at certain times)•Manually(via an employee request)A picking status is recorded in each delivery item for the purpose of scheduling and monitoring.This status indicates where the item is in the picking procedure. In the system standard settings,it is a prerequisite for a goods issue to be posted, that the items that are relevant,have been picked.Therefore,a delivery quantity must equal a picking quantity in the outbound delivery.The Warehouse Management system(WM)is fully integrated in the Logistics Execution System(LES).For example,you can create a Warehouse Management transfer order directly from the outbound delivery.The current status of the Warehouse Management process can also be monitored from the delivery or from the sales order.Goods Issue Posting FunctionsThe outbound delivery forms the basis of goods issue posting.The data required for goods issue posting is copied from the outbound delivery into the goods issue document,which cannot be changed manually.Any changes must be made in the outbound delivery itself.After goods issue is posted for an outbound delivery,the scope for changing the delivery document becomes very limited.This prevents any discrepancies between the goods issue document and the outbound delivery. In this way,you can be sure that the goods issue document is an accurate reflection of the outbound delivery.When you post goods issue for an outbound delivery,the following functions are carried out:•Warehouse stock of the material is reduced by the delivery quantity •Value changes are posted to the balance sheet account in inventory accounting •Requirements are reduced by the delivery quantity•The serial number status is updated•Goods issue posting is automatically recorded in the document flow •Stock determination is executed for the vendor's consignment stock•A worklist for the proof of delivery is generatedYou can post goods issues in the following ways:•Automatically(during outbound delivery creation)•Routinely(at certain times)•Manually(via an employee request)BillingBilling represents the final processing stage for a business transaction in sales order rmation on billing is available at every stage of order processing and delivery processing.Billing functions include:•Creation of invoices based on deliveries or services•Issue of credit and debit memos and pro forma invoices•Cancelling billing transactions•Comprehensive pricing functions•Issue rebates•Transfer billing data to financial accountingFigure48:BillingLike all parts of sales order processing in mySAP ERP,billing is integrated into the organizational structures.Thus,you can assign the billing transactions a specific sales organization,a distribution channel,and a division.Because billing has an interface to financial accounting,the organizational structures of the accounting department(the company codes as well as the sales organizations assigned to the company codes)are important.During a billing processing it is possible for you to create,change,and delete billing documents.It is possible to create billing documents:•With reference to a sales order document•With reference to a delivery document•With reference to external transactions•By having the system automatically process a billing due list as a background task•By manually processing from a worklist•By creating a billing document explicitly•By combining several sales order documents into a collective billing document•By billing one or more sales order documents with several billing documents (this is called an invoice split)•By creating an individual billing document for every sales document Billing and Financial AccountingThe system automatically posts the amounts to the appropriate accounts by means of account determination.Costs and revenue can be posted to the following accounts:•Customer accounts receivable•General ledger(for example,a cash clearing account)•Revenue•Sales deductions•Accruals(for rebate agreements)•Accrual account•Accrual clearing accountDocument FlowThe sales documents you create are individual documents,but they can also form part of a chain of interrelated documents.For example,you may recorda customer’s telephone inquiry in the system.The customer next requests a quotation,which you then create by referring to the inquiry.The customer later places an order on the basis of the quotation and you create a sales order with reference to the quotation.You ship the goods and bill the customer.All of these separate documents reference one another through document flow.Figure49:Document FlowAfter delivery of the goods,the customer claims credit for some damaged goods and you create a free-of-charge delivery with reference to the sales order.The entire chain of documents–the inquiry,the quotation,the sales order,the delivery, the invoice,and the subsequent delivery free of charge–creates a document flow, or history.The flow of data from one document into another reduces manual activity and makes problem resolution easier.Exercise8:Create a Sales OrderExercise ObjectivesAfter completing this exercise,you will be able to:•Create a sales orderBusiness ExampleA customer has faxed a sales order and it is your job,as a customer service representative,to enter the order into your system.Task:Create a sales order.ing the information provided in the table,create a standard order.Field DataOrder Type OR(Standard order)Sales organization1000(Germany Frankfurt)Distribution channel10(Final customer sales)Division00(Cross-division)ing the information provided in the table,continue creating the order.Record the sales order document.Field DataSold-to party Rohrer##(Rohrer AG Gr.##)Purch.order no.Group—##Req.deliv.date<Today+1week>Continued on next pageField Data Material R-F2##(Pump) Order quantity10 Sales orderSolution8:Create a Sales OrderTask:Create a sales order.ing the information provided in the table,create a standard order.Field DataOrder Type OR(Standard order)Sales organization1000(Germany Frankfurt)Distribution channel10(Final customer sales)Division00(Cross-division)a)From the SAP Easy Access menu,choose Logistics→Sales andDistribution→Sales→Order.b)Choose Create.c)Enter Order Type:OR.d)Enter Sales Organization:1000.e)Enter Distribution Channel:10.f)Enter Division:00.g)Choose Enter.ing the information provided in the table,continue creating the order.Record the sales order document.Field DataSold-to party Rohrer##(Rohrer AG Gr.##)Purch.order no.Group—##Req.deliv.date<Today+1week>Continued on next pageField DataMaterial R-F2##(Pump)Order quantity10Sales ordera)Enter Sold-to party:Rohrer##.b)Enter Purch.order no.:Group-##.c)Choose Enter.Hint:Make sure you are on the Sales tab on the order entryscreen.d)Enter Req.deliv.date:<Today+1week>.e)Choose Enter.f)Enter Material:R-F2##.g)Enter Order quantity:10.h)Choose Enter.Hint:If an information dialog box appears,choose Enter toconfirm that you have read the information.i)Choose Save and record the document number in the table provided.Hint:The system displays a message that the sales order hasbeen saved with the sales document number.This numberappears on the status bar on the bottom left-hand corner ofthe order window.j)Choose Exit to exit the screen and return to the SAP Easy Access menu.Exercise9:Create a DeliveryExercise ObjectivesAfter completing this exercise,you will be able to:•Create a delivery document with reference•Post the inventory goods issue with reference•View Document FlowBusiness ExampleYou have been notified that your customer's order is ready to ship.Task:Create a delivery document with reference to your customer's order.Post the delivery document in the system.Verify that the shipping documents were processed by using the sales document flow.Note:This exercise uses the sales order number created in the previousexercise.ing the information provided in the table,create a delivery document.Record the delivery document number.Field DataOrder<Sales order numbercreated in the previousexercise>If necessary,this ordernumber can be found by searchingfor Purchase order no.Group-## Shipping point1000(Shipping Point Hamburg) Selection Date<Today+1week>Delivery2.Post the goods issue for the delivery and view the document flow.Recordyour findings in the table provided.Continued on next pageDocument Document number Status Standard orderDeliveryWMS transfer orderGD goods issueSolution9:Create a DeliveryTask:Create a delivery document with reference to your customer's order.Post the delivery document in the system.Verify that the shipping documents were processed by using the sales document flow.Note:This exercise uses the sales order number created in the previousexercise.ing the information provided in the table,create a delivery document.Record the delivery document number.Continued on next pageField DataOrder<Sales order numbercreated in the previousexercise>If necessary,this ordernumber can be found by searchingfor Purchase order no.Group-## Shipping point1000(Shipping Point Hamburg) Selection Date<Today+1week>Deliverya)From the SAP Easy Access menu,choose Logistics→Sales andDistribution→Shipping and Transportation→Outbound delivery→Create→Single Document.b)Choose With Reference to Sales Order.c)Enter Shipping point:1000.d)Enter Selection date:<Today+1week>.e)If needed,enter the Order:<use the sales order numbercreated earlier>.Note:The sales order number should default.Hint:You can locate the sales order number in the system byusing the matchcode F4to search for the sales order by thePurchase order no.:Group-##.f)Choose Enter.g)Choose Save.Record the delivery document number in the tableprovided.2.Post the goods issue for the delivery and view the document flow.Recordyour findings in the table provided.Continued on next pageDocument Document number StatusStandard orderDeliveryWMS transfer orderGD goods issuea)From the SAP Easy Access menu,choose Logistics→Sales andDistribution→Shipping and Transportation→Outbound delivery→Change.b)Choose Single Document.Hint:The delivery document number should default.c)Choose the Post goods issue icon from the application toolbar.Hint:The document will be saved and the posting performed.This is indicated by the message in the message status bar.Hint:Do not back out of the Change Outbound Deliveryscreen!d)Choose Document flow.Record the documents in the table providedabove.e)Choose Exit to exit the screen.SAP01Lesson:Sales Order Management Exercise10:Create a Sales Order BillingDocumentExercise ObjectivesAfter completing this exercise,you will be able to:•Create a billing document with referenceBusiness ExampleThe customer received the ordered materials.Bill your customer by sending himan invoice.Task:Create a billing document.Verify that the billing document was created by usingthe sales document flow.ing the outbound delivery document created in the previous exercise,create a billing document.2.Display the document flow and record your findings in the table provided.Document Document number StatusStandard orderDeliveryInvoiceAccountingDocumentUnit4:Logistics SAP01 Solution10:Create a Sales Order BillingDocumentTask:Create a billing document.Verify that the billing document was created by usingthe sales document flow.ing the outbound delivery document created in the previous exercise,create a billing document.a)From the SAP Easy Access menu,choose Logistics→Sales andDistribution→Billing→Billing Document.b)Choose Create.c)Check the Document number.Hint:Your delivery document number should default so a userentry is not required.d)Choose Save.Hint:The document will be saved and the posting performed.This is indicated by the message in the message status bar.e)Choose Exit to exit the screen and return to the SAP Easy Accessmenu.2.Display the document flow and record your findings in the table provided.Continued on next pageSAP01Lesson:Sales Order ManagementDocument Document number StatusStandard orderDeliveryInvoiceAccountingDocumenta)From the SAP Easy Access menu,choose Logistics→Sales andDistribution→Billing→Billing Document.b)Choose Display.Hint:Your delivery document number should default,so auser entry is not required.Hint:You do not have to enter the document to view thedocument flow.c)Choose Display Document flow from the Application toolbar.Record your findings in the table provided.d)Choose Exit to exit the screen and return to the SAP Easy Accessmenu.Unit4:Logistics SAP01 Lesson SummaryYou should now be able to:•Outline the tasks associated with sales order management•Explain how SAP within mySAP ERP supports the key processes in sales order managementSAP01Lesson:Customer Relationship ManagementLesson:Customer Relationship ManagementLesson OverviewIn this lesson you will receive an overview of the mySAP Customer RelationshipManagement solution.Lesson ObjectivesAfter completing this lesson,you will be able to:•Outline the tasks associated with the customer relationship managementprocess•Explain how SAP supports the key processes in customer relationshipmanagement with the mySAP CRM applicationBusiness ExampleYour company,IDES,wants to give customers a number of contact options.Theywant to set up central customer management and are interested in implementingmySAP Customer Relationship Management.Customer Relationship ManagementNothing is more frustrating for a salesperson than not closing a deal because thenecessary information was not available.What has the customer already bought?How profitable is the customer?Can we deliver the required quantity?Nothing is more frustrating for customers than having to deal with a company thatdoes not meet their needs.Only satisfied customers will return in the future.Customer relationship management has become a decisive success factor.Thechallenge for large companies is to promote a local store mentality throughout alldepartments and all employees.Unit4:Logistics SAP01Figure50:mySAP CRMCustomer relationship management(CRM)is the concept of making the customerthe focus of a company and its business processes.It must be implemented as theprimary company philosophy and the strategies it promotes have to be adoptedwithin the company.The aim of all corporate activities must be to place customersat the center,and not view them as the means to an end(just to increase turnover).The principles of customer relationship management must predominate at alllevels of the company.CRM is intended to create and build upon long-termrelationships with customers during all phases of the business relationship.Thephases of a customer relationship include:•Approaching possible customers:A customer is interested in the company and its products(first contact).•Gaining the customer:The customer has a concrete intention to buy and the company receives an order.•Service:The company does everything to ensure that the customer issatisfied with the product or service purchased.•Keeping the customer:Specific and attentive customer support ensuresthat the customer is both a satisfied and loyal customer.The customer willremain true to your company,even if a competitor offers a similar product ata reduced rate.SAP01Lesson:Customer Relationship ManagementFigure51:Customer Relationship ManagementThe idea of customer relationship management is not new;local stores havealways acted in this way.As long as they were engaged in business with theircustomers,they maintained relationships with these customers.The owners of local stores know their customers well and are well acquainted withtheir particular needs and desires.They know which products to offer to whichcustomers and when,in order to ensure a successful sale.The local store ownersalso know when to give a customer's child a lollipop on their birthday.The challenge for large-scale enterprises is to transfer this local store mentalityto their company.Why should they do this?The Internet has changed our lives and the competitionis now only a mouse-click away.Nowadays,customers expect all channels ofbusiness communication to be fully integrated.Whatever channel of communication customers may be using,they expect realservice all the time,wherever they are.If one company does not offer this service,the customers simply go to a competitor.Companies need to rethink:Maintaining customer relationships has become adecisive success factor.The solution is mySAP CRM.mySAP CRM covers not only traditional salesprocesses.SAP Customer Relationship Management(SAP CRM),the cornerstoneof SAP's Customer Relationship Management solution(mySAP CRM),providescompanies with the customer-centric solutions they need to land,build,andmaintain profitable customer relationships.SAP CRM drives closed-loopcustomer interactions through all phases of the relationship lifecycle:engage,transact,fulfill,and service.SAP CRM supports all relevant channels:mobile,telephony,and the Internet.SAP CRM drives customer relationships in all CRMbusiness dimensions:operational,analytical,and collaborative.Traditional direct salesUnit4:Logistics SAP01 Typically,information within a company is not usefully collected.Wheninformation is passed on,it is often incomplete or inaccurate.Employee turnovermeans that vital customer information is often lost.Traditional direct sales is characterized by decentralized information about thecustomer.In some cases,only one employee has knowledge about the customerand the relevant contact information.Figure52:Traditional KnowledgeDirect Sales Using mySAP CRMmySAP CRM allows every employee who needs information about customercontacts to access all relevant information immediately.Field Sales and FieldServices enable field representatives to access ALL contact information in thefield using a laptop or other mobile devices.Analyzing this information gives thecompany a deeper understanding of its customers.As a result,the company canincrease its service package,process queries faster,strengthen relationships,andbenefit from increased customer loyalty.SAP01Lesson:Customer Relationship ManagementFigure53:Knowledge with mySAP CRMDepartments of an Enterprise Driving CustomerInteractionsDuring the different phases of customer interaction,various departments of acompany have to deal with the customer.This is reflected in the key capabilitiesof mySAP CRM.Unit4:Logistics SAP01Figure54:Key Capabilities of mySAP CRMMarketingMarketing in mySAP CRM includes the entire marketing process for extensivecustomer engagement.It delivers the critical capabilities of marketing planning,campaign management,e-marketing,lead management,marketing analytics,andcustomer segmentation in an easy,intuitive,and configurable interface.Initiativescan be designed and executed to meet specific corporate objectives–withassociated KPIs defined and measured to ensure bottom-line results.Marketing planningPlan all marketing activities at the enterprise,regional,field,product,or brandlevel to ensure success.Campaign managementDesign,optimize,execute,and manage all communications across theorganization.Lead managementCollaborate internally and with partners to qualify,transfer,and track leads,and toeliminate the time spent on poor leads.Closed-loop marketing analyticsGive your marketing professionals full visibility into the organization to improvethe planning,monitoring,and measuring of marketing initiatives.Customer segmentationDevelop highly targeted marketing segments without the need for IT involvement.PersonalizationOffer the right products to the right customers at the right time.Trade Promotion ManagementSupport both strategic and tactical marketing,including total sales volume planning.Implement,validate,and analyze sales-promotion tactics,such as features,displays,and temporary price reductions.SalesSales spans all customer sales channels,ensuring seamless,scalable customer transactions.It supplies organizations with Enterprise Sales,Telesales,Field Sales and E-Selling solutions to transact with customers anytime,anywhere.Sales planning and forecastingReport on and analyze all sales planning and forecasting activities. Organizational and territory managementDefine territories based on size,revenue,geography,products,product lines,and strategic accounts.Assign sales representatives for each territory and identify the prospects and products associated with each territory.Account and contact managementCapture,monitor,store,and track all critical information about customers, prospects,and partners.Activity managementSchedule and manage simple and complex tasks.Opportunity managementGive your channels complete visibility into each sales opportunity,so they can capture,manage,and monitor business contacts and account information. Quotation and order managementConfigure,price,and create quotes for customers,and generate follow-up activities,such as sales orders.Contract managementWork with customers to develop and revise customized contracts and long-term purchasing agreements.Incentive and commission managementDevelop,implement,and manage compensation plans.Track current performance, and measure the potential compensation of sales in the pipeline.。

英语作文-销售中的销售技巧与销售数据分析

英语作文-销售中的销售技巧与销售数据分析In the realm of sales, mastering the art of persuasion and understanding sales data analysis are two indispensable skills. Effective sales techniques coupled with insightful data analysis can significantly boost sales performance and contribute to overall business success. In this article, we will delve into various sales techniques and explore how data analysis can be utilized to enhance sales strategies.First and foremost, building rapport with customers is essential in sales. Establishing a connection based on trust and understanding can pave the way for successful transactions. Active listening is a fundamental aspect of this process. By attentively listening to customers' needs and concerns, sales professionals can tailor their approach accordingly, thereby increasing the likelihood of closing a sale.Moreover, the power of persuasion cannot be overstated in sales. Employing persuasive language and techniques can help sway hesitant customers towards making a purchase. Highlighting the unique selling points of a product or service and demonstrating how it addresses the customer's specific needs can be highly effective. Additionally, utilizing social proof, such as customer testimonials or case studies, can further reinforce the credibility of the offering.Furthermore, mastering the art of negotiation is crucial in sales. Negotiation skills enable sales professionals to navigate objections and reach mutually beneficial agreements with customers. It involves understanding the customer's perspective, identifying common ground, and effectively addressing any concerns or objections that may arise. By employing techniques such as framing, anchoring, and concessions, sales professionals can steer negotiations towards a favorable outcome.In addition to honing interpersonal skills, leveraging sales data analysis is paramount in optimizing sales strategies. By analyzing sales data, businesses can gain valuable insights into customer behavior, market trends, and product performance. This data-driven approach allows sales teams to identify opportunities for growth, refine targeting strategies, and allocate resources more effectively.For instance, analyzing sales trends can help identify peak selling periods, enabling businesses to adjust their marketing efforts accordingly. Similarly, examining customer demographics and preferences can inform product development and marketing messaging, ensuring alignment with target audience needs and preferences.Furthermore, sales data analysis can facilitate performance tracking and evaluation. By monitoring key performance indicators (KPIs) such as conversion rates, customer acquisition costs, and sales pipeline velocity, businesses can assess the effectiveness of their sales efforts and make data-driven decisions to optimize performance.In conclusion, mastering sales techniques and leveraging data analysis are essential components of successful sales strategies. By cultivating strong interpersonal skills, employing persuasive techniques, and harnessing the power of data, sales professionals can drive revenue growth, foster customer relationships, and achieve sustainable business success.。

销售产品方案英语

Introduction:At [Your Company Name], we are committed to delivering high-quality products that meet the diverse needs of our customers. Our latest product, [Product Name], is designed to revolutionize the market withits innovative features and exceptional performance. In this proposal, we will outline the sales strategy and marketing plan to ensure the successful launch and widespread adoption of [Product Name].1. Product Overview:[Product Name] is a [briefly describe the product's purpose and target market]. It is a [mention any unique features or technologies] that sets it apart from competitors. The product has undergone rigorous testingand has received positive feedback from early adopters.2. Target Market:Our target market for [Product Name] includes [list target demographics, industries, or customer segments]. This market has a significant unmet need for [describe the problem or pain point that [Product Name] solves]. By addressing this need, we aim to capture a substantial share of the market within the first year of launch.3. Sales Strategy:a. Channel Partnerships:- Establish strategic partnerships with leading distributors and retailers to ensure widespread availability of [Product Name].- Offer competitive pricing and incentives to encourage channel partners to promote and stock our product.b. Direct Sales:- Assign a dedicated sales team to engage with key customers and provide personalized support.- Organize sales meetings, trade shows, and product demonstrations to showcase the benefits of [Product Name].c. E-commerce:- Develop an online presence with a user-friendly website that highlights the features and benefits of [Product Name].- Implement targeted online advertising campaigns to drive traffic and generate leads.- Offer secure online purchasing options to facilitate easy transactions.4. Marketing Plan:a. Branding:- Develop a strong brand identity for [Product Name] through consistent messaging and visual elements.- Create compelling marketing materials, including brochures, flyers, and digital content, to educate potential customers about the product.b. Digital Marketing:- Leverage social media platforms to engage with the target audience and promote [Product Name].- Utilize SEO strategies to improve online visibility and drive organic traffic to the website.- Collaborate with influencers and bloggers to reach a broader audience and gain credibility.c. Public Relations:- Engage with industry publications and media outlets to secure feature articles and interviews.- Organize press releases and product launches to generate buzz and excitement around [Product Name].- Participate in industry events and conferences to network with potential customers and partners.5. Sales Goals and Targets:- Aim to achieve [specific sales targets, e.g., 100 units sold within the first month].- Monitor sales performance regularly and adjust the strategy as needed to meet targets.- Implement a customer feedback system to gather insights and continuously improve the product and sales approach.Conclusion:[Your Company Name] is confident in the success of [Product Name] due to its unique features, exceptional performance, and targeted marketing strategy. By leveraging a combination of channel partnerships, direct sales, and digital marketing, we aim to capture a significant market share and establish [Product Name] as a leading product in its category. We look forward to working with you to achieve these goals and deliver value to our customers.。

财务会计英语版课后答案

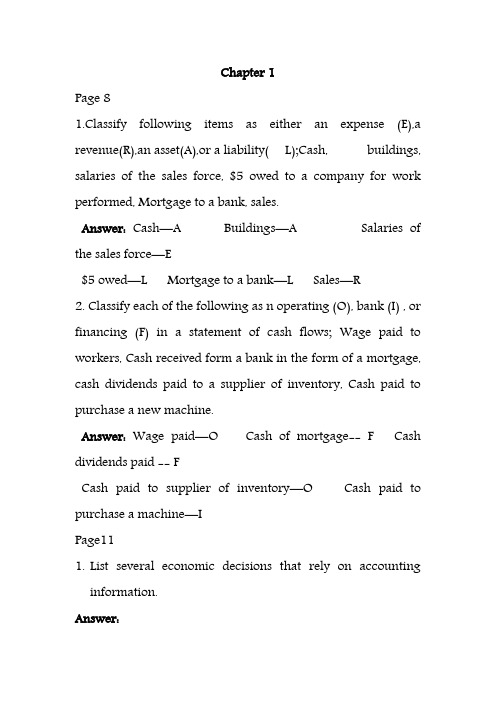

Chapter 1Page 81.Classify following items as either an expense (E),a revenue(R),an asset(A),or a liability( L);Cash, buildings, salaries of the sales force, $5 owed to a company for work performed, Mortgage to a bank, sales.Answer:Cash—A Buildings—A Salaries of the sales force—E$5 owed—L Mortgage to a bank—L Sales—R2. Classify each of the following as n operating (O), bank (I) , or financing (F) in a statement of cash flows; Wage paid to workers, Cash received form a bank in the form of a mortgage, cash dividends paid to a supplier of inventory, Cash paid to purchase a new machine.Answer:Wage paid—O Cash of mortgage-- F Cash dividends paid -- FCash paid to supplier of inventory—O Cash paid to purchase a machine—IPage111.List several economic decisions that rely on accounting information.Answer:·Whether to grant a loan·How much to pay for a share of common stock.·Whether to grant a rate increase to an electric utility·How much in damages the loser of a lawsuit must pay ·How much of a bonus to pay a plant manager·Whether to enter a new market2. Why do financial statements have footnotes, and what kinds of information might you find in them?Answer:Financial statements have footnotes because financial disclosure is a complex business. The notes tell us some of the specifics about the company environment , what accounting methods the company has used, what the accounting numbers might be if alternative methods had been used, and some of the major contingencies that are not formally included in the statement proper.Page 201.Describe the process of setting accounting standards. What are the roles of all the parties you mention?Answer:The FASB, a private, not-for-profit organization ,sets GAAP in the U.S. It publicly declares an agenda, promulgates "ExposureDrafts" of proposed standards, holds open meetings, and invites input from interested parties. The FASB has been delegated this authority by the SEC, a government agency with legal authority to determine GAAP.2.Think of an example, like the executive compensation example in the chapter, where incentives might exist to bias accounting numbers one way or another.Answer:There are other examples, but here is one that is different. A taxpayer has incentives to bias reported income downward in order to minimize income tax payments. However, it is important to understand that tax accounting rules are different from GAAP, and this book is about GAAP. Chapter 14 covers GAAP for taxes in more detail.Other examples include:·An entrepreneur seeking a loan from a bank or funding from a venture capitalist might have incentives to bias accounting numbers to look favorable.·A firm that is subject to scrutiny for earning excess profits(e.g.,an oil company)might have incentives to bias accounting numbers to look less favorable.·A utility subject to rate regulation might have an incentive tobias accounting numbers to look less favorable in order to gain more generous increases in its rates. (At this writing, there is a rather severe controversy about whether electric utilities in California are genuinely in financial difficulty and should be allowed to continue to impose large rate increase.)Chapter 2Page 381 Define assets, liabilities, and equities.Gave an example ofeach. How are assets valued? How are liabilities valued? Answer:An asset is a probable future economic benefit obtained or controlled by an entity as a result of a past transaction. Cash marketable securities, accounts receivable, inventories, prepaid expenses, patents, copyrights, trademarks, and property, plant and equipment are all examples of assets. A liability isa probable future sacrifice of economic benefits arisingfrom present obligations of an entity to transfer assets or provide services as a result of a past transaction or event.Accounts payable, accrued liabilities, unearned revenues, warranties, and bonds payable are all examples of liabilities.Accounting valuation of assets uses severaldifferent methods, including market value, expected realizable value, lower of cost or market, present value of future cash flows, and historical cost. Accounting valuation of liabilities is the expected amount that will be paid, perhaps adjusted for the time value of money.2. Explain what is meant by the entity concept. Answer:The entity is the person or organization about which accounting's financial history is being written.3 .A company signs a ten-year employee contract with a vicepresident. The salary is $500000 per year, guaranteed. Is this contract an asset? Would it appear on the balance sheet? Explain.Answer:The rights conveyed by the contrat may be an asset from an economic point of view, but they are not an asset under GAAP. The contract would not appear on the balance sheet as an asset, because GAAP does not record executory contracts, which are contracts that require future performance form both parties. That is ,GAAP views the contract as determining what services will be provided, no asset is recognized under GAAP.(Neither is a liability for payment recognized until services have beenperformed.)4 .A company purchased a parcel of land 10 years ago at a cost of $300000.The land has recently been appraised at $900000. At what value is the land carried in the balance sheet? How does the appraisal affect the carrying value in the balance sheet?Answer:The land is on the balance sheet at its historical cost of $300000.The carrying value of the land is unaffected by the appraisal.Page 421、Define debit and credit .What kind of balance ,debit or credit ,would you expect to find in the inventory T-account?In the Common Stock T-account?Answer:A debit is an entry on the left side of a T-account. A credit is an entry on the right side of a T-account. We would except to find a debit balance in Inventory, and credit balances in Bonds Payable and Common Stock. The reason is the convention that increases in assets are debits and increases in liabilities and equities are credits.2、If the trial balances, it means that you have analyzed all the effects of transactions correctly. True or false?Explain. Answer:False. A balanced means that the trial balance is consistent, not necessarily correct. For example. If an arbitrary entry is made that debits Cash and credits Common Stock for an equal amount, the trial balance will balance but it will be wrong. An accounting can receipt of cash and the issuance of common stock, but it alone can not make cash or additional common shares.3﹑Suppose Web sell leases a portion of its space to another company. Web sell’s accounts are debited and credited to record this transaction?Answer:Web sell would debit Cash and a liability, Rent Received in Advance, for the prepayment.Chapter 3Page 571. Define revenue and expense. How does one decide to list an item as revenue in an income statement? What is matching? Answer:Revenues are increases in net assets resulting from operationsover a period of time .Expense are decreases in net assets resulting from operations over a period of time .Revenue is recognized the earnings process is substantially complete , a transaction2. Give an example not found in the text , of an expense that is paid for in cash in a prior accounting period .In a subsequent accounting period.Answer:There are many allowable responses . An example is a patent that is purchased and paid for in one year and used in next .3. Give an example, not found in the text , of a revenue that is received in cash in a prior accounting period . In a subsequent accounting period .Answer:An example is a house painting contractor that receives payment for one-third of the contract price before beginning the painting .4. Explain why it is right to think of an asset as a cost and an expense as an expired cost .Answer:An asset is a future benefit . And there is an opportunity cost associated with not selling it for cash or exchanging it to settleChapter 6Page 120:1.The following table lists the adjustments and has an X in thecolumn indicating the approach:2. We first take adjustment for prepaid insurance and insurance expense. It would be easy to think of this adjustment as focusing on how much of the insurance coverage remained, as opposed to how much was used. In fact, the same type of logic could beused---computing a monthly rate for the coverage and applying that to the months reminding, instead of the months used.Now take adjustment for depreciation expense and accumulated depreciation. Estimating the value of the equipment at year end might be easy, for example, if there is a market for used equipment, or very difficult, for example, if the equipment was specially designed for Websell. Once a value estimate for the equipment at year end is obtained, depreciation expense would be the change in value over the year.Page 1231.$5000×(1+0.06)^10=$5000×1.79085=$8954.242.$5000×(1+0.06/2)^(10×2)=$5000×(1+0.03)^20=$5000×1.80611=$9030.563. $1000×(1.05)^3+$1000×(1.05)^2+$1000×(1.05)^1=$3310.134. ($1000×0.05/5)^13+$1000×(1+0.05/5)^10+$1000×(1+0.05/5)^5=($1000×(1.01)^15)+($1000×(1.01)^10)+($1000×(1.01)^5) =$1160.97+$1104.62+$1051.01=$3316.6Page 1241.x×.(1.07)^3=$3000 x=$3000/(1.07)^3=$2448.892. Calculate the present value at 10% of $1300 received two years from now. If that is greater than $1000, you are better off with the $1300 to be received in two years. If its present value is less that $1000, you better off with $1000 now. $1300/(1.10)^2=$1074.38Therefore, you are better off receiving $1300 two years from now.Another way to do this problem is to take the future value at 10% of $1000. At the end of two years, the $1000 would compound up to:$1000×(1.10)^2=$1210,Which is less than you would have at that point if you took the $1300.3.The most I would be willing to pay is the present value at 8% of the stream of $1000 payment:$1000/(1.08)^1+$1000/(1,08)^2+$1000/(1,08)^3=$925.926+857.339+793.832=$ 2577.1(rounded)Chapter 8Page 1681.Aging takes the balance in accounts receivable at the end of the year, and sorts it by how long ago the transaction occurredthat gave rise to that receivable. Experience has shown that “older” accounts have less likelihood of ever being collected. Percentages of likely uncollectibles for each category are applied to the totals in that category , and the results added to obtain an estimate of the allowance for uncollectibles required to value properly the estimated amount that will be collected from the accounts receivable. The bad debts expense then falls out as a “plug” in the allowance for uncollectibles.The percentage-of-sales method just estimates bad debt expense as a percent of sales, and plug the balance in the allowance account.2. Cash (118)Accounts receivable (118)12/31/2003(to recognize collection of cash from companies owing service co. from 2002 sales)Allow ance for doubtful accounts (7)Accounts receivable (7)12/31/2003(to write off accounts we know will not be collected) Accou nts receivable (125)Sales reven ue (125)12/31/2003(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2003, we would record.06×$125000=$7500 in bad debts expense.B ad debts expense………………………………………7.5 Allowan ce for doubtful accounts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accounts(10.5 is the “plug”,i.e., the number that drops out)Now we move to 2004, where events now proceed as expected . Collections are $117.5 thousand. Cash………………………………………………..117.5 Accounts receivable…………………………………117.512/31/2004(to recognize collection of cash form companies owing service co. from 2003 sales)Allowance for doubtful ac counts………………………7.5Accounts receivable………………………………….7.512/31/2004(to write off accounts we know will not be collected) Accounts receivable (125)Sales revenue (125)12/31/2004(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2004, we would record.06×$125000=$7500 in bad debts expense.Bad debts expense……………………………………7.5 Allowance for doubtful ac counts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)The allowance for doubtful accounts using the peentage-of-sales method looks like this:Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accountsOnly the entries recording bad debt expense are different using the aging method. Instead of the above entries recording bad debt expense, we would have the following analysis: Each year, we would adjust the balance in the allowance for doubtful accounts so that the net receivable ends up at $117500. That is, we would solve $125000-X=$117500,and find that the ending balance in the allowance for doubtful accounts must be $7500.Analyzing the account, we would determine that at 12/31/2003 we must add $4500 to the allowance for doubtful accounts: Bad debts expense………………………………..4.5 Allowanc e for doubtful accounts…………………….4.512/31/2004(to record bad debt expense in anticipation of not collecting 100% of receivables)At 12/31/2004, we must add $7500 to the allowance for doubtful accounts:Bad debts expense………………………………..7.5 Allowan ce for doubtful accounts…………………….7.512/31/2004(to record bad debt expense in anticipation of notcollecting 100% of receivables)Using aging, the allowance for doubtful accounts T-account looks like this:Method two: focus on the ending balance in the allowance for doubtful accounts.Allowance for doubtful accountsChapter 9Page 1831.LIFO is last-in first-out. It means that in computing ending inventoryand cost of goods sold, the cost of items sold is assigned in reverse chronological order of their purchase, beginning from the most regent items purchased in a period. FIFO is first-in, first-out .It means that in computing ending inventory and cost of goods sold, the cost of items sold is assigned in chronological order of their purchase, beginning from the goods on hand at the beginning of the period. Average costmeans that in computing ending inventory and cost of goods sold, the average unit cost of the beginning inventory and items purchased in a period is used to determine the cost of goods sold and remaining inventory.2.Yes, it is still a positive net present value project. In fact, its netpresent value is higher than when the purchase was made at$1.05 per unit, since the cash outflow is reduced but the cash inflow remains the same. The cash outflow on 12/31/01 when purchases are at $0.95 per unit is $114.This means the net cash flow at 12/31/01 is ($4) instead of ($16),and the NPV for Widget Company is:NPV=-100-$4/1.1+$10/ (1.1^2) +$144/ (1.1^3) =$12.82First, we redo the case of FIFO. The inventory T-account is:Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Net incomes are:Widget Incomes using FIFONow we redo the case of FIFO. First, the inventory T-account is: Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Netincomes are:Page 186To calculate the market-to-book ratios and accounting returns on equity: Market-to-book Ratios under Average CostAccounting Rates of Return under Average CostCollecting the results for FIFO from the chapter and these results for average cost, we have:Market-to-book Ratios under Various Cost Flow AssumptionAccounting Rates of Return under Various Cost Flow AssumptionAs is apparent, the market-to-book ratios and accounting rates of return for average cost are between for LIFO and FIFO.2. Because it has more recent costs on the balance sheet in the inventory account, FIFO has market-to-book ratios closer to 1regardless of whether prices rise or fall.Chapter 10Page 1961. The total profit on the transaction is the sales price of $880.00 less the original cost of $734.03:Sales price of securities $880.00Less : original cost ($735.03)Profit on transaction $144.97The cash flows were: $735.03 out on January1, 2001, and$880.00 in on January 3, 2003.There were profit in 2001, 2002, and 2003.In 2001, there was a profit of $81.17.In 2003,there was a profit of $5.00.2. The unadjusted book value of the security on December 31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing its carrying value by $3.83 is required to write it down to its market value: Unrealized loss on market value securities-trading ……3.83 Marketable securities –trading ………… 3.83 If the security were sold for $810.00 on January 3, 2003, the entry would be:Cash ………………………………810.00Marketable securities –trading ………………790.00Gain on marketable securities-trading …………20.001/03/2003(To record the sale of the Marketable securities—trading )Page 1981. When a securities is classified as trading security, profits or losses show up on the income statement in every period from when the security is purchased until when it is sold. when a security is classified as available-for-sale ,profits or losses only show up on the income statement in the period in which thesecurity is sold.2. the unadjusted book value of the security on December 31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing it’s carrying value by $3.83 is required to write it down to it’s market value. however unlike the trading security case ,the unrealized loss is an equity account ,not a temporary account:Unrealized loss on marketable securities-available-for-sale 3.38 Marketable securities –trading ………………3.83To record the sale of the security for $810.00 on January 3,2003: Cash ………810.00Unrealized gain on marketable securities-available-for-sale(58.80-3.83) ………54.97Marketable securities-trading …………790.00Realized gain on marketable securities-available-for-sale ……………74.9712/31/2002(To mark-to-market the Marketable securities—available-for-sale)Chapter 111.a. Under straight-line depreciation, the depreciation expense each year is$600-$100/5 years=$100 per year.b. Under double-declining balance depreciation, the depreciation expense each year is given in the following table:c. Under sum-of-year’-digits depreciation, the depreciation expense each year is given in the following table:Sum-of years’-digits depreciation2. Intangible assets are most often shown in one line that is cost net of amortization. Tangible assets are sometimes shown in three lines: cost , accumulated depreciation, and net .3. Economic depreciation is the change in the economicvalue of the asset. Economic depreciation can be appreciation when the asset increases in value. We seen this already with marketable debt securities, which sometimes increase in value because of unpaid interest4.It is easy and fulfills the requirement of GAAP to provide depreciation using a systematic and rational method. No GAAP depreciation method likely correctly reflects economic depreciation anyway ,so a simple expedient may be good enough.1.Sraight-line depreciation is $100 per year ($300/3 years).Double-declining balance depreciation is given in the following table:2.For straight-line depreciation,the entry is the same each year: Depreciation expense (100)Accumulateddepreciation (100)For double-declining balance depreciation,the entries are: Year1Depr eciation expense (200)Accu mulated depreciation (200)Year2Depreciation expense………………………………66.67 Acc umulated depreciation………………………66.67 Year3.declining balance because depreciation expense under straight-line is only $100,while under double-declining balance depreciation expense is $200.4.If the company buys one asset every year and each asset lasts three years,then in year 4 it will have three assets.Under straight-line depreciation,each of those assets generates a depreciation expense of $100;therefore total depreciation expense would be 3*$100,or $300.Under double-declining balance depreciation,totaldepreciation expense depends on the age of each asset.The company would have one asset in its first year of life,one in its second year of life,and one in its third year.Therefore,total depreciation expense would be:$200+$66.67+$33.33=$300,the same as under straight-line.Both depreciation methods give the same total depreciation because:1.Both methods fully depreciate the assets over their lives.2.The cost of the assets has remained constant.3.The company is in a steady state in which the number ofnew assets purchased in a period equals the number ofold assets being retired in that period.。

市场营销专业英语-经典

annual requirement purchasing arrangement 年度采购需求计划anticipatory positioning 预见性定位 anti —pollution legislation 反污染立法 anti-trust legislation 反托拉斯立法 Apple Computers 苹果电脑 area structure 地区结构aspiration/expectation level 渴望/期望水平 aspirations of consumers 消费者渴望 assurance 保证AT &T 美国电话电报公司ATM (automatic teller machine) 银行自动柜员机 attitudes of consumers 消费者态度audiences 受众 auto repair 汽车维修automation services 自动服务 automobile industry 汽车产业 autonomy 自主权availability 可获得性/供货能力 avante guardian 前卫派 Avon 雅芳awareness (产品)知晓度/知名度 Bbaby boomers 婴儿潮出生的一代人backward channels for recycling 回收的后向渠道 backward integration 后向垂直一体化 banner advertisements 横幅标语广告 bar codes 条形码 barter 实物交易basic physical needs 基本生理需要 Bausch & Lomb 博士伦BCG Grow-Share Matrix 波士顿增长—份额矩阵 before tests 事前测试Behavior Scan Information Resources Inc 。