Chapter 7 Financial Accounting

会计专业英语名词解释

会计专业英语名词解释Chapter 11. Accounting: Accounting is the process of identifying, measuring, recording, andcommunicating economic information to permit informed judgments and decisions by users of the information.2. Accrual basis accounting: Accrual basis accounting refers to an accounting methodthat records financial events based on economic activity rather than financial activity.Under accrual accounting, revenue is recorded when it is earned and realized, regardless of when actual payment is received. Similarly, expenses are matched with revenue regardless of when they are actually paid.3. Balance sheet: Balance sheet is the financial statement showing the financial positionof an entity by summarizing its assets, liabilities, and owner’s equity at one sp ecific date.4. Business entity: Business entity refers to an economic unit that controls resources,incurs obligations, and engages in business activities.5. CAS: Chinese Accounting Standards refer to the accounting concepts, measurementtechniques, and standards of presentation used in financial statements made by the PRC Financial Apartment.6. Cash basis accounting: Cash basis accounting is a method of bookkeeping thatrecords financial events based on cash flows and cash position. Revenue is recognized when cash is received and expense is recognized when cash is paid out.7. Conservatism: Conservatism states that when alternative accounting valuations areequally possible, the accountant should select the one that is least likely to overstate assets and income in the current period.8. Consistency: Consistency means that a company uses the same accountingprinciples and methods from year to year.9. Continuity: Continuity refers to an accounting assumption, also known as thegoing-concern assumption, that the company will continue to operate in the near future, unless substantial evidence to the contrary exists.10. Corporation: Corporation is a business organized as a separate legal entity understate corporation law and having ownership divided into transferable shares of stock.11. Cost principle: Cost principle is a widely used principle of accounting for assets at theiroriginal cost to the current owner.12. Financial accounting: Financial accounting refers to the development and use ofaccounting information describing the financial position of an entity and the results of its operations.13. Financial position: Financial position refers to the financial resources and obligationsof an organization, as described in a balance sheet.14. Financial reporting: Financial reporting refers to the process of periodically providing“general-purpose”financial information (such as financial statements) to persons outside the business organization.15. Financial statements: Financial statements refer to the four related accounting reportsthe summarize the current financial position of an entity and the results of its operations for the preceding year ( or other time period).16. Full disclosure principle: Full disclosure principle requires that circumstances andevents that make a difference to financial statement users be disclosed.17. Going-concern assumption: Go-concern assumption is an assumption by accountantsthat a business will operate indefinitely unless specific evidence to the contrary, such as impending bankruptcy, exists.18. Historical cost: The historical cost of an asset is the exchange price in the transactionin which the asset was acquired.19. Matching principle: Matching principle is an accounting principle that dictates thatexpenses be matched with revenue in the period in which efforts are made to generate revenue.20. Materiality: Materiality refers to the magnitude of an omission or misstatement ofaccounting information that, considering the circumstances, makes it likely that the judgment of a reasonable person relying on the information would have been influenced by the omission or misstatement.21. Market value: Market value is the estimated amount for which a property shouldexchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion,22. Net realizable value: The net realizable value of an asset is the amount of cash (or theequivalent) that could be obtained on the date of the balance sheet by selling the asset in its present condition, in an orderly liquidation.23. Income statement: Income statement is a financial statement indicating theprofitability of a business over a preceding time period.24. Partnership: Partnership is a business owned by two or more persons associated aspartners.25. Present value: The present value of an asset is the net amount of discounted futurecash inflows less the discounted future cash outflows relating to the asset.26. Proprietorship: Partnership is a business owned by one person.27. Relevance: Accounting information is relevant if it can make a difference in a decisionby helping users predict the outcomes of past, present, and future events or confirm or correct prior expectations. To be relevant, accounting information should have either predictive or feedback value, or both. In addition, it should be timely,28. Reliability: Reliable information is reasonably free from error and bias, and faithfullyrepresents what it is intended to represent. That is, to be reliable, information should be verifiable, neutral, and possess representational faithfulness,29. Revenue recognition principle: An accounting principle that dictates that revenue berecognized in the accounting period in which it is earned.30. Statement of cash flow: A financial statement summarizing the cash receipts and cashpayments of the business over the same time period covered by the income statement.31. Statement of owner’s equity: A financial statement explaining certain changes in theamount of the owner’s equity (investment) in the business.1. Asset: Assets mean the entire property of a person, association, corporation, or estateapplicable or subject to the payment of debts.2. Operating cycle: The operating cycle is the time span from when cash is used toacquire goods and service and until cash is received from the sale of goods and service.3. Cash: cash refers to an exchange medium launched into circulation which is availablefor any ordinary use and can be used to purchase goods or services or repay debts.4. Cash equivalents: Cash equivalents are short-term, highly liquid investments or otherassets that readily convertible to cash and sufficiently close to their due date.5. Internal control: Internal control means all policies and procedures used to protectassets, ensure reliable accounting, promote efficient operations, and urge adherence to company policies.Chapter 31. Receivables: Receivables refer to the monetary claims against business, individualsand other debtors.2. Accounts receivable: Accounts receivables are amounts due from customers for creditsales. This section begins by describing how accounts receivables occur. It includes receivables that occur when customers use credit cards issued by third parties and when a company gives credit directly to customers.3. Installment accounts receivables: Installment accounts receivables are amounts overan extended time period.4. Commercial discounts: Commercial discounts refer to a certain sum of moneydeducted from listed prices.5. Cash discounts: Cash discounts refer to a deduction from gross invoice price, whichare an inducement offered to the buyer to encourage the payments of goods within a specific period of time.6. The percentage-of-sale method: The percentage-of-sale method estimates somepercentage of credit sales would turn out to be uncollectible, in which the percentage of bad debts to credit sales should be properly estimated with the past experience. 7. The percentage-of-receivable method: The percentage-of-receivable methodestimates the uncollectible with a percentage of the ending balance of accounts receivables rather than credit sales.8. The aging method: The aging method analyzes the age structure of the accountbalance. In this method, an aging schedule is prepared, classifying the length of time that has passes since the sale that gave rise to them.9. The allowance method: The allowance method is the most usual way that companiesuse to record uncollectible accounts. In calculating uncollectible accounts, an account allowances for uncollectible receivable is set up.10. Promissory note: A promissory note is a written promise to pay a certain sum ofmoney on demand or at a fixed and determinable future time, generally over 30 or 60 days.1. Inventory: Inventory is the total amount if goods and/or materials contained in a storeor factory at any given.2. Product costs: Product costs are those costs that “attach”to the inventory. Suchcharges include freight charges on goods purchased, other direct costs of acquisition, and labor and other production costs incurred in processing the goods up to the time of sale.3. The perpetual inventory system: The perpetual inventory system requires thatseparate inventory ledger be maintained for each goods.4. The periodic inventory system: The periodic inventory system requires a companydetermines the quantity of inventory on hand only periodically, under which the cost of ending inventory is subtracted from the cost of goods available for sale, then the cost of goods sold are determined.5. The specific identification method: The specific identification method can be usedwhen units in the ending inventory can be identified as coming from specific purchases.6. The weighted average cost method: The weighted average cost method assumes thatthe goods available for sale have the same cost per unit. Under this method, the cost of goods available for sale is allocated on the basis of the weighted-average unit c0st.7. The first-in, first-out (FIFO) method: The first-in, first-out (FIFO) method is base on theassumption that the costs of the first items acquired should be assigned to the first item sold.Chapter 51. Accelerated depreciation: Accelerated depreciation is a method of depreciation thatcall for recognition of relatively large amounts if depreciation in the early years of an asset’s useful life and relatively small amounts in the later years.2. Depreciable value: Depreciable value is the amount of the acquisition cost to beallocated as depreciation over the total useful life of an asset. It is the difference between the total acquisition cost and the estimated residual value.3. Depreciation: Depreciation is the systematic allocation of the cost of an asset toexpress over the years of its estimated useful life.4. Fair market value: Fair market value is the value of an asset based on the price forwhich a company could sell the asset to an independent third party.5. Impairment: Impairment is a change in economic conditions which reduces theeconomic usefulness of an asset.6. Residual value: Residual value is the amount a company expects to receive fromdisposal of an asset at the end of its useful life.7. Useful life: Useful life refers to the shorter of the physical life or the economic life of anasset.1. Amortization: The systematic write-off to expense of the cost of an intangible assetover the period of its economic usefulness.2. Copyright: A grant by the state government covering the right to publish, sell, orotherwise control literary or artistic products for the life of the author plus 50 years. 3. Franchises: Agreements entered into by two parties in which, for a fee, one party (thefranchisor) gives the other party (the franchisee) rights to perform certain functions or sell certain products or services.4. Goodwill: The present value of expected future earnings of a business in excess of theearnings normally realized in the industry.5. Identifiable intangible asset: Intangibles that can be purchased or sold separately fromthe other assets of the company.6. Intangible assets: Those assets which are used in the operation of a business butwhich have no physical substance and are not current.7. Leases (or leaseholds): Intangible assets because a right to use the property is heldby the lessee.8. Patent: An exclusive right granted by the state government giving the owner control ofthe manufacturing, sale, or other use of an invention for a period of years from the date of filling.9. Research and development costs: Expenditures that may lead to patent, copy rights,new processes and new products.10. Trademarks: Distinctive identifications of a manufactured product or of a service,taking the form of a name, a sign, a slogan, a logo, or an emblem.Chapter 71. Available-for-sale securities: Securities that may be sold in the future.2. Consolidated financial statements: Financial statements that present the assets andliabilities controlled by the parent company and the aggregate profitability of the affiliated companies.3. Cost method: An accounting method in which the investment in common stock isrecorded at cost and revenue is recognized only when cash dividends are received.4. Debt investments: Investments in government and corporation bonds.5. Equity method: An accounting method in which the investment in common stock isinitially recorded at cost and the investment account is then adjusted annually to show the investor’s equity in the investee.6. Fair value: Amount for which a security could be sold in a normal market.7. Held-to-maturity securities: Debt securities that investor has the intent and ability tohold to maturity.8. Investment portfolio: A group of stocks in different corporations held for investmentpurposes.9. Long-term investments: Investments that are not readily marketable and thatmanagement does not intend to convert into cash within the next year or operating cycle, whichever is longer.10. Parent company: A company that owns more than 50% of the common stock ofanother entity.11. Short-term investments: Investments that are readily marketable and intend to convertinto cash within the next year or operating cycle, whichever is longer.12. Stock investments: Investments in the capital stock of corporations.13. Subsidiary (affiliated) company: A company in which more than 50% of its stock isowned by another company.14. Trading securities: Securities bought and held primarily for sale in the near term togenerate income on short-term price differences.Chapter 81. Amortization table: A schedule that indicates how installment payments are allocatedbetween interest expense and repayments of principal.2. Capital lease: A lease contract which, in essence, finances the eventual purchase bythe lessee of leased property. The lessor accounts for a capital lease as a sale of property; the lessee records an asset and a liability equal to the present value of the future lease payments. A capital lease is also called a financing lease.3. Commercial paper: Very short-term notes payable issued by financially strongcorporations. They are highly liquid from the investor’s point of view.4. Commitments: Contracts for the future transactions.5. Contra-liability account: A ledger account which is deducted from or offset against arelated liability account in the balance sheet; for example, Discount on Notes Payable.6. Convertible bond: One which may be changed at the option of the bondholder for aspecific number of shares of common stock.7. Deferred income taxes: Income taxes upon income which already has been reportedfor financial reporting purposes, but which will not be reported in income tax returns until future periods.8. Discount on notes payable: A contra-liability account representing any interestcharges applicable to future periods included in the face amount of a note payable.Over the life of the note, the balance of the Discount on Notes Payable account is amortized into Interest Expense.9. Deducted bond: Debenture bonds refer to an unsecured bond.10. Estimated liabilities: Liabilities which appear in financial statements at estimatedamounts.11. Long-term liabilities: Obligations that are not due for at least a year.12. Loss contingency: A possible loss, or expense, stemming from past events, that willbe resolved as to existence and amount by some future event.13. Mortgage bonds: Bonds secured by the pledge of specific assets.14. Operating lease: A lease contract which is in essence a rental agreement. The lesseehas the use of the leased property, but the lessor retains the usual risks and rewards of ownership. The periodic lease payments are accounted for as rent expense by the lessee and as rental revenue by the lessor.Chapter 91. Income: Income is defined as increases in economic benefits during the reportingperiod in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants. Income encompasses both revenue and gains.2. Revenue: Revenue is income that arises in the course of ordinary activities of anentity and is referred to by a variety of different names including sales, fees, interest, dividends and royalties.3. Gains: Gains represent other items that meet the definition of income and may, or maynot arise in the course of the ordinary activities of an entity.4. Accrued revenue: Accrued revenue is the revenue that has been earned but not yetcollected.5. Trade discounts: Trade discounts depend on the volume of the business or size oforder from the customer.6. Cash discounts: Cash discounts are offered to customers by some companies toencourage prompt payment of bills.7. Expenses: Expenses are outflows or using up of assets as part of operations of abusiness to generate sales.8. Employee expenses: Employee expenses are the entitlements which employeesaccumulate as a result of rendering their services to an employer.9. Depreciation (amortization): Depreciation is a periodic expense of operations and isassociated with the consumption or loss of service potential of non-current assets. 10. Bad (doubtful) debts expense: Bad debts expense is, in effect, a reduction of the“receivables” asset.11. Income taxes expense: Income taxes expense is the expense recognized in theaccounting records on an accrual basis that applies to income from continuing operations.12. Profit: Profit is the ultimate result of various operating activities of the enterprise in areporting period.13. Accounting policies: Accounting policies are the specific principles, bases,conventions, rules and practices adopted by an entity in preparing and presenting financial statements.14. Applicable profit: Applicable profit is assets that can be distributed to all kinds ofbeneficiaries.Chapter 101. Owner’s equity: Owner’s equity refers to the sources invested by owners or formed inthe course of the production and operation or other sourced shared by owners.2. Par value: The par value is an arbitrary dollar amount assigned to each share.3. Treasury stock: Treasury stock may be defined as shares of a corporation’s owncapital stock that have been issued and later reacquired by the issuing company but that have not been canceled or permanently retired.4. Capital reserve: Capital reserve refers to the capital which isn’t viewed as the paid-incapital or capital stock.5. Undistributed profit: Undistributed profit is the profit that is not distributed toshareholders but retained to the later years.Journal entries1. A company had the following transactions during January: Using the net method ofrecording purchases, prepare the journal entries to record these January transactions.Jan.2 Purchased merchandise, invoice price of $20 000, with terms 2/10, n/30.4 Received a credit memorandum for $4 000, the invoice price on merchandisereturned from the purchase of January 2.12 Purchased merchandise, invoice price of $15 000, with terms 3/15, n/30.26 Paid for the merchandise purchased on January 12.30 paid for the merchandise purchased on January 2.Answer:Jan.2 Merchandise …………………………………………………….19 600Accounts payable………………………………………………………19 6004 Accounts payable…………………………………………………3 920Merchandise………………………………………………………………3 92012 Merchandise……………………………………………………..14 550Accounts payable………………………………………………………14 55026 Accounts payable………………………………………………..14 550Cash……………………………………………………………………..14 55030 Accounts payable………………………………………………..15 680Expense (400)Cash………………………………………………………………………16 0802. The following series of transactions occurred during 2010 and 2011, when LinwoodCo. sold merchandise to John Moore. Linwood’s annual accounting period ends on December 31.10/01/2010 Sold $12 000 of merchandise to John Moore, terms 2/10, n/3011/15/2010 Moore reports that he cannot pay the account until the early next year. He agrees to exchange the account for a 120-day, 12% note receivable.12/31/2010 Prepared the adjusting journal entry to record accrued interest on the note.03/15/2011 Linwood receives a check from Moore for the maturity value (with interest) of the note.03/22/2011 Linwood receives notification that Moore’s check is being returned for nonsufficient funds (NSF).12/31/2011 Linwood writes off Moore’s account as uncollectible.Prepared Linwood Co.‘s journal entries to record the above transactions.The company uses the allowance method to account for its bad debt expenses.Answer:Oct.1, 2010 Accounts receivable—Moore……………………………..12 000Sales……………………………………………………………..12 000 Nov.15, 2010 Notes receivable……………………………………………12 000Accounts receivable—Moore........................................12 000 Dec.31,2010 Interest receivable (184)Interest revenue (184)($12 000 x 0.12 x 46/360 = $184)Mar.15, 2011 Cash…………………………………………………………..12 480Notes receivable………………………………………………...12 000Interest receivable (184)Interest earned (296)($12 000 x 0.12 x 74/360 = $296)Mar.22, 2011 Accounts receivable—Moore……………………………….12 480Cash…………………………………………………………….12 480 Dec.31, 2011 Allowance for doubtful accounts……………………………12 480Accounts receivable—Moore…………………………………12 4803. (a) A company purchased a patent on January 1, 2006, for $2 500 000. The patent’slegal life is 20 years but the company estimates that the patent’s useful life will only be5 years from the date of acquisition. On June 30, 2006, the company paid legal costsof $162 000 in successfully defending the patent in an infringement suit. Prepare the journal entry to amortize the patent at year end on December 31, 2006.(b) Suxia Company purchased a franchise from Yanyan Food Company for $400 000on January 1, 2006. The franchise is for an indefinite time period and gives Suxia Company the exclusive rights to sell Yanyan Wings in a particular territory. Prepare the journal entry to record the acquisition of the franchise and any necessary adjusting entry at year end on December 31, 2006.(c) Chenghe Company incurred research and development costs of $500 000 in 2006in developing a new product. Prepare the necessary journal entries during 2006 to record these events and any adjustments at year end on December 31, 2006.Answer:JOURNAL ENTRIES(a) December 31, 20×6Amortization Expense …………………………………………..518 000Patent………………………………………………………………… 518 000 (To record patent amortization.)$2 500 000 ÷ 5 years ……………………..$500 000$162 000 ÷ 54 months = …………………….$3 000$3 000×6……………………………………. $18 000$518 000(b) January 1, 20×6Franchise ………………………………………………………..400 000Cash………………………………………………………………. 400 000(To record acquisition of T astee Food franchise.)December 31, 20×6No amortization of the franchise is required since its life is indefinite.(c) 20×6Research and Development Expense……………………….. 500 000Cash………………………………………………………………. 500 000 (To record research and development expense for the Current year.)December 31—no entry.4. Suxia Company had the following transactions pertaining to short-term investments inequity securities.Jan.1 Purchased 900 shares of Chenghe Company stock for $9 450 cash plus brokerage fees of $ 270June.1 Received cash dividends of $0.50 per share on Chenghe Company stock.Sept.15 Sold 400 shares of Chenghe Company stock for $ 4 300 less brokerage fees of $100Dec.1 Received cash dividends of $0.50 per share on Chenghe Company stock.(a) Journalize the transactions.(b) Indicate the income statement effects of the transactions.Answer:(a) Jan. 1 Stock Investments……………………………………….. 9 720Cash..................................................................... 9 720 June 1 Cash (900 × $0.50) .. (450)Dividend Revenue (450)Sept. 15 Cash ($4 300 – $100)…………………………………. 4 200Loss on Sale of Stock Investments (120)Stock Investments (400 × ($9 720 ÷ 900)) ......................4 320 Dec. 1 Cash (500 × $0.50). (250)Dividend Revenue (250)(b) Dividend Revenue is reported under Other Revenues and Gains on theincome statement. Loss on Sale of Stock Investments is reported under Other Expenses and Losses on the income statement.5. Presented below are the three independent situations:(a) Henry Corporation purchased $ 400 000 of its bonds on June 30, 2005 at 102 andimmediately retired them. The carrying value of the bonds on the retirement date was $ 367 200. The bonds pay semiannual interest and the interest payment due on June 30, 2005 has been made and recorded.(b) Rose, Inc., purchased $600 000 of its bonds at 96 on June 30, 2005 andimmediately retired them. The carrying value of the bonds on the retirement date was $ 590 000. The bonds pay semiannual interest and the interest payment due on June 30, 2005 has been made and recorded.(c) Sealy Company has $200 000, 10%, 12-year convertible bonds outstanding.These bonds were sold at face value and pay semiannual interest on June 30 and December 31 of each year. The bonds are convertible into 80 shares of Sealy $ 5 par value common stock for each $ 1 000 par value bond. On December 31, 2005 after the bond interest has been paid, $ 50 000 par value of bonds were converted.The market value of Sealy’s common stock was $ 48 per share on December 31, 2005.Instruction: For each of the independent situations, prepare the journal entry to record the retirement or conversion of the bonds.Answer:(a) June 30 Bonds Payable……………………………………………. 400 000Loss on Bond Redemption……………………………….. 40 800Discount on Bonds Payable ………………………………………...32 800Cash …………………………………………………………………408 000($400 000 – $367 200 = $32 800)($400 000 × 102% = $408 000)(b) June 30 Bonds Payable……………………………………………. 600 000Discount on Bonds Payable………………………………………... 10 000Gain on Bond Redemption ………………………………………….14 000Cash………………………………………………………………… 576 000($600 000 – $590 000 =$10 000)($600 000 × 96% =$576 000)(c) Dec. 31 Bonds Payable………………………………………………. 50 000Common Stock…………………………………………………….. 20 000Paid-in Capital in Excess of Par …………………………………..30 000($5 × 80 × 50 =$20 000)6. Maia’s Bike Shop uses the perpetual inventory system and had the followingtransactions during the month of May:May 3 Sold merchandise to a customer on credit for $ 600, terms 2/10, n/30. The cost of the merchandise sold was $ 350.May 4 Sold merchandise to a customer for cash of $ 425. The cost of themerchandise was $ 250.May 6 Sold merchandise to a customer on credit for $ 1 300, terms 2/10, n/30. The cost of the merchandise sold was $ 750.May 8 The customer from May 3 returned merchandise with a selling price of $ 100.The cost of the merchandise returned was $ 55.May 15 The customer from May 6 paid the full amount due, less any appropriate discounts earned.May 31 The customer from May 3 paid the full amount due, less any appropriate discounts earned.Prepare the required journal entries that Maia’s Bike Shop must make to record these transactions.。

Financial Accounting-复式记账法

11. Performed a service by placing several advertisements for W. Department Stone and A & A Grocers. The earned fees of $7,000 and $9,000, respectively, will be collected next month. Dr. Accounts Receivables 16,000 Cr. Advertising Fees Earned 16,000 12. John Miller withdrew $8,000 from the business for personal living expenses. Dr. John Miller Withdraw 8,000 Cr. Cash 8,000

weeks’ 13. Paid the secretary two more weeks salary, $3,500. Dr. Office Wages Expenses 3,500 Cr. Cash 3,500 14. Paid the Utility bill, $500. Dr. Utility Fees Cr. Cash

(p46) Exercise 4 (p46) Translate the following into English 5, 现金 (cash) 5,000 应收账款(Accounts 3, 应收账款(Accounts receivable) 3,000 应收票据(Notes 1, 应收票据(Notes receivable) 1,000 10, 库存商品 (Merchandise Inventory) 10,000 办公用品(Office 1, 办公用品(Office Supplies) 1,500 资产合计(Total 20, 资产合计(Total Assets) 20,000

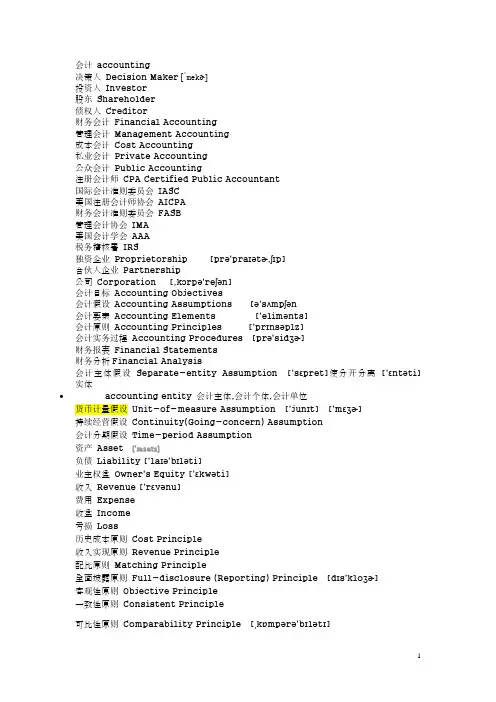

会计 accounting

会计accounting决策人Decision Maker[ˈmekɚ]投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师CPA Certified Public Accountant国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship [prə'praɪətɚ,ʃɪp]合伙人企业Partnership公司Corporation [,kɔrpə'reʃən]会计目标Accounting Objectives会计假设Accounting Assumptions [ə'sʌmpʃən会计要素Accounting Elements ['elimənts]会计原则Accounting Principles ['prɪnsəplz]会计实务过程Accounting Procedures [prə'sidʒɚ]财务报表Financial Statements财务分析Financial Analysis会计主体假设Separate-entity Assumption ['sɛpret]使分开分离['ɛntəti] 实体accounting entity 会计主体,会计个体,会计单位货币计量假设Unit-of-measure Assumption ['junɪt] ['mɛʒɚ]持续经营假设Continuity(Going-concern) Assumption会计分期假设Time-period Assumption资产Asset [ˈæsets]负债Liability ['laɪə'bɪləti]业主权益Owner's Equity ['ɛkwəti]收入Revenue ['rɛvənu]费用Expense收益Income亏损Loss历史成本原则Cost Principle收入实现原则Revenue Principle配比原则Matching Principle全面披露原则Full-disclosure (Reporting) Principle [dɪs'kloʒɚ]客观性原则Objective Principle一致性原则Consistent Principle可比性原则Comparability Principle [ˌkɒmpərə'bɪlətɪ]重大性原则Materiality Principle [məˌtɪrɪ'ælətɪ]稳健性原则Conservatism Principle [kənˈsɜ:rvətɪzəm]权责发生制Accrual Basis [əˈkruəl]现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning会计循环Accounting Procedure/Cycle会计信息系统Accounting information System帐户Ledger会计科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General Ledger明细分类帐Subsidiary Ledger试算平衡Trial Balance [ˈtraɪəl]现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐General Journal工作底稿Worksheet调整分录Adjusting entries结帐Closing entries(3)现金与应收账款,公司财务谈论公司目前现金及应收账款相关的英语专业术语词汇。

principles of financial accounting

risk of getting caught

Fails to see the criminal nature of the fraud or justifies the action

Must have soபைடு நூலகம்e pressure to commit fraud, like unpaid bills

International Standards

good and bad behavior.

Generally Accepted Accounting Principles (GAAP)

Financial accounting is governed by concepts and rules known as generally accepted accounting principles (GAAP). GAAP aims

to make information relevant, reliable, and comparable.

Relevant information affects decisions of users.

Reliable information is trusted by users.

Comparable information is helpful in contrasting

Ethics – A Key Concept

The goal of accounting is to provide useful information for decisions. For information to be useful, it must be trusted. This demands ethics in accounting. Ethics are beliefs that distinguish right from wrong. They are accepted standards of

中级财务会计习题(英文)

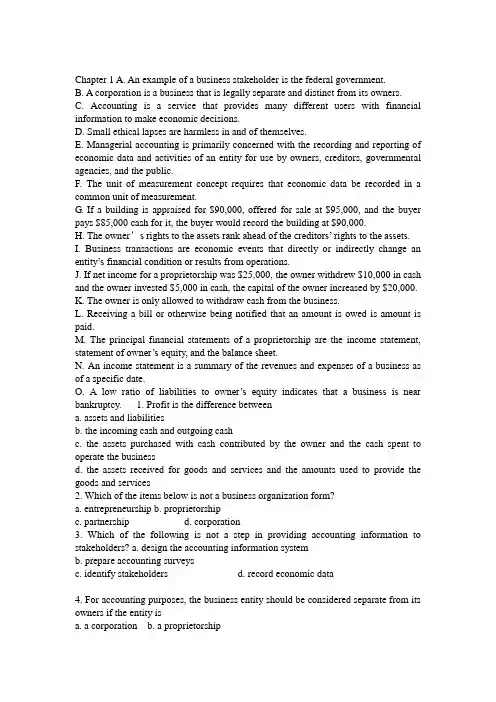

Chapter 1 A. An example of a business stakeholder is the federal government.B. A corporation is a business that is legally separate and distinct from its owners.C. Accounting is a service that provides many different users with financial information to make economic decisions.D. Small ethical lapses are harmless in and of themselves.E. Managerial accounting is primarily concerned with the recording and reporting of economic data and activities of an entity for use by owners, creditors, governmental agencies, and the public.F. The unit of measurement concept requires that economic data be recorded in a common unit of measurement.G. If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000.H. The owner’s rights to the assets rank ahead of the creditors’ rights to the assets.I. Business transactions are economic events that directly or indirectly change an entity’s financial condition or results f rom operations.J. If net income for a proprietorship was $25,000, the owner withdrew $10,000 in cash and the owner invested $5,000 in cash, the capital of the owner increased by $20,000. K. The owner is only allowed to withdraw cash from the business.L. Receiving a bill or otherwise being notified that an amount is owed is amount is paid.M. The principal financial statements of a proprietorship are the income statement, statement of owner’s equity, and the balance sheet.N. An income statement is a summary of the revenues and expenses of a business as of a specific date.O. A low ratio of liabilities to owner’s equity indicates that a business is near bankruptcy. 1. Profit is the difference betweena. assets and liabilitiesb. the incoming cash and outgoing cashc. the assets purchased with cash contributed by the owner and the cash spent to operate the businessd. the assets received for goods and services and the amounts used to provide the goods and services2. Which of the items below is not a business organization form?a. entrepreneurshipb. proprietorshipc. partnershipd. corporation3. Which of the following is not a step in providing accounting information to stakeholders? a. design the accounting information systemb. prepare accounting surveysc. identify stakeholdersd. record economic data4. For accounting purposes, the business entity should be considered separate from its owners if the entity isa. a corporationb. a proprietorshipc. a partnershipd. all of the above5. Which of the following is not a business transaction?a. make a sales offerb. sell goods for cashc. receive cash for services to be rendered laterd. pay for supplies6. The Reynolds Company estimated that the value of its land had increased from $10,000 to $16,000 and therefore wrote up the land account to $16,000. Which accounting concept(s) was (were) violated?a. cost conceptb. objectivity conceptc. all of the aboved. none of the above7. Goods purchased on account for future use in the business, such as supplies, are called a. prepaid liabilities b. revenuesc. prepaid expensesd. liabilities8. All of the following are financial statement(s) of a proprietorship except thea. statement of retained ear ningsb. statement of owner’s equityc. income statementd. statement of cash flowsChapter 2 A. A chart of accounts is a listing of accounts that make up the journal.B. Drawings are an example of an expense.C. To determine the balance in an account, always subtract credits from debits.D. The double-entry accounting system records each transaction twice.E. The increase side of all accounts is the normal balance.F. The journal is the book of original entry.G. Journalizing transactions using the double-entry bookkeeping system will eliminate fraud. H. The process of transferring the data from the journal to the ledger accounts is posting. I. The post reference notation used in the journal is the page number.J. When a business receives a bill from the utility company, no entry should be made until the invoice is paid.K. A proof of the equality of debits and credits in the ledger at the end of an accounting period is called a balance sheet.L. Even when a trial balance is in balance, there may be errors in the individual accounts. M. Posting a part of a transaction to the wrong account will cause the trial balance totals to be unequal.N. Horizontal analysis is used to compare the financial statements of the same company for different periods. 1. A group of related accounts that comprise a complete unit is called aa. Journalb. liability2.3.4.5.6. c. ledger d. transaction Which statement(s) concerning cash is (are) true? a. cash will always have more debits than credits b. cash will never have a credit balance c.cash is increased by debiting d. all of the above Which of the following types of accounts have a normal credit balance? a. assets and liabilities b. liabilities and expenses c. revenues and liabilities d. capital and drawing Which of the following entries records the receipt of cash from patients on account? a. Accounts Payable, debit; Fees Earned, credit b. Accounts Receivable, debit; Fees Earned, credit c. Accounts Receivable, debit; Cash, credit d. Cash, debit; Accounts Receivable, credit If the two totals of a trial balance are not equal, it could be due to a. failure to record a transaction b. recording the same erroneous amount for both the debit and the credit parts of a transaction c. an error in determining the account balances, such as a balance being incorrectly computed d. recording the same transaction more than once Which of the following errors, each considered individually, would cause the trial balance totals to be unequal?a. a transaction was not postedb. a payment of $96 for insurance was posted as a debit of $46 to Prepaid Insurance and a credit of $46 to Cashc. a payment of $311 to a creditor was posted as a debit of $3,111 to Accounts Payable and a debit of $311 to Accounts Receivabled. cash received from customers on account was posted as a debit of $140 to Cash and a credit of $140 to Accounts PayableChapter 3 1. The accrual basis of accounting requires revenue be recorded when cash is received from customers.2. The matching concept requires expenses be recorded in the same period that the related revenue is recorded.3. Adjusting entries are made at the end of an accounting period to adjust accounts on the balance sheet.4. The difference between deferred revenue and accrued revenue is that accrued revenue has been recorded and needs adjusting and deferred revenue has never been recorded.5. The systematic allocation of land’s cost to expense is called depreciation.6. The difference between the balance of a fixed asset account and the balance of its related accumulated depreciation account is termed the book value of the asset.7. If the adjustment for accrued salaries at the end of the period is inadvertently omitted, both liabilities and owner’s equity will be overstated for the period.8. The financial statements are prepared from the unadjusted trial balance.9. Vertical analysis compares each item in a statement with another item in the same statement.The correct: 2,6,91. Which account would normally not require an adjusting entry?a. Wages Expenseb. Accounts Receivablec. Accumulated Depreciationd. Smith, Capital2. What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid insurance account balance before adjustment, $15,500, and unexpired amounts per analysis of policies, $4,500?a. debit Insurance Expense, $4,500; credit Prepaid Insurance, $4,500b. debit Insurance Expense, $15,500; credit Prepaid Insurance, $15,500c. debit Prepaid Insurance, $11,500; credit Insurance Expense, $11,500d. debit Insurance Expense, $11,000; credit Prepaid Insurance, $11,0003. Depreciation Expense and Accumulated Depreciation are classified, respectively, asa. expense, contra assetb. asset, contra liabilityc. revenue, assetd. contra asset, expense4. If there is a balance in the unearned subscriptions account after adjusting entries are made, it represents a(n)a. deferralb. accrualc. drawingd. revenue5. What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid insurance account balance before adjustment, $15,500, and unexpired amounts per analysis of policies, $4,500?a. debit Insurance Expense, $4,500; credit Prepaid Insurance, $4,500b. debit Insurance Expense, $15,500; credit Prepaid Insurance, $15,500c. debit Prepaid Insurance, $11,500; credit Insurance Expense, $11,500d. debit Insurance Expense, $11,000; credit Prepaid Insurance, $11,0006. Depreciation Expense and Accumulated Depreciation are classified, respectively, asa. expense, contra assetb. asset, contra liabilityc. revenue, assetd. contra asset, expense7. If there is a balance in the unearned subscriptions account after adjusting entries are made, it represents a(n)a. deferralb. accrualc. drawingd. revenueMultiple choice: d d a aChapter 41. The most important output of the accounting cycle is the financial statements.2. A net loss is shown on the work sheet in the credit columns of both the Income Statement columns and the Balance Sheet columns.3. The difference between a classified balance sheet and one that is not classified is that the classified one has subheadings.4. Since the adjustments are entered on the work sheet, it is not necessary to record them in the journal or post them to the ledger.5. The post-closing trial balance will generally have fewer accounts than the trial balance.6. Solvency is essentially the ability of an organization to pay its bills.7. Working capital is current assets plus current liabilities.ANS:T F T F T T F1. The worksheeta. is an integral part of the accounting cycleb. eliminates the need to rewrite the financial statementsc. is a working paper that is requiredd. is used to summarize account balances and adjustments for the financial statements2. Which one of the fixed asset accounts listed below will not have a related contra asset account? a. Office Equipment b. Land c. Delivery Equipment d. Building3. Which of the accounts below would be closed by making a debit to the account?a. Unearned Revenueb. Fees Earnedc. Jeff Ritter, Drawingd. Rent Expense4. Which of the following accounts ordinarily appears in the post-closing trial balance?a. Bill Smith, Drawingb. Supplies Expensec. Fees Earnedd. Unearned Rent5. A fiscal yeara. ordinarily begins on the first day of a month and ends on the last day of the following twelfth monthb. for a business is determined by the federal governmentc. always begins on January 1 and ends on December 31 of the same yeard. should end at the height of the business’s annual operating cycle6. A current ratio of 4.3 means thata. there are $4.30 in current assets available to pay each dollar of current liabilitiesb. the company cannot pay its debts as they come duec. there are $4.30 in current assets for every $4.30 in current liabilitiesd. there are $4 in current assets for every $3 in current liabilitiesANS: dbbdaaChapter 61. In a merchandise business, sales minus operating expenses equals net income.2. In a perpetual inventory system, the Merchandise Inventory account is only used to reflect the beginning inventory.3. The single-step income statement is easier to prepare, but a criticism of this format is that gross profit and income from operations are not readily available.4. Under the perpetual inventory system, when a sale is made, both the retail and cost values are recorded.5. Sales Discounts is a revenue account with a credit balance.6. Discounts taken by the buyer for early payment of an invoice are credited to Cash Discounts by the buyer.7. If the ownership of merchandise passes to the buyer when the seller delivers the merchandise for shipment, the terms are stated as FOB destination.8. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with prepaid transportation costs of $100, is paid within 10 days, the amount of the purchases discount is $50.9. The adjusting entry to record inventory shrinkage would generally include a debit to Cost of Merchandise Sold. 1. The primary difference between a periodic and perpetual inventory system is that aa. periodic system determines the inventory on hand only at the end of the accounting periodb. periodic system keeps a record showing the inventory on hand at all timesc. periodic system provides an easy means to determine inventory shrinkaged. periodic system records the cost of the sale on the date the sale is made2. A sales invoice included the following information: merchandise price, $4,000; transportation, $300; terms 1/10, n/eom, FOB shipping point. Assuming that a credit for merchandise returned of $600 is granted prior to payment, that the transportation is prepaid by the seller, and that the invoice is paid within the discount period, what is the amount of cash received by the seller? a.$3,366 b.$3,400c.$3,666d.$3,9503. The net sales to asset s ratio measures a company’sa. working capitalb. net worthc. effective use of sales to support the purchase of new assetsd. effective use of assets to generate salesThe correct: 3,4,8,9 Multiple choice: a c dChapter 74. A customer’s c heck received in settlement of an account receivable is considered cash.5. If the balance in Cash Short and Over at the end of a period is a credit, it indicates that cash shortages have exceeded cash overages for the period.6. A voucher system is an example of an internal control procedure over cash payments.7. A remittance advice is the notification accompanying the check issued to a creditor that states the specific invoice being paid.8. The amount of the "adjusted balance" appearing on the bank reconciliation as ofa given date is the amount that is shown on the balance sheet for that date.9. When the petty cash fund is replenished, the petty cash account is credited for the total of all expenditures made since the fund was last replenished.10. Cash equivalents are short -term investments that will be converted to cash within 120 days.11. The doomsday ratio is almost always less than one.ANS:T F T T T F F T1. Credit memorandums from the banka. decrease a bank custom er’s accountb. are used to show a bank service chargec. show that a company has deposited a customer’s NSF checkd. show the bank has collected a note receivable for the customer2. Journal entries based on the bank reconciliation are required in the depositor’s accounts for a. outstanding checks b. deposits in transitc. bank errorsd. book errorsANS: d dChapter 81. Receivables from company owners and officers should be disclosed separately on the balance sheet.2. Since those responsible for receivables record keeping and credit approval do not handle cash, these duties do not need to be separated to maintain good internal control.3. Of the two methods of accounting for uncollectible receivables, the allowance method provides inadvance for uncollectible receivables.4. Although Allowance for Doubtful Accounts normally has a credit balance, it may have either a debit or a credit balance before adjusting entries are recorded at the end of the accounting period.5. At the end of a period, before the accounts are adjusted, Allowance for Doubtful Accounts has a debit balance of $2,000. If the estimate of uncollectible accounts determined by aging the receivables is $30,000, the current provision to be made for uncollectible accounts expense is $30,000.6. The due date of a 60-day note dated July 10 is September 10.7. If the maker of a note fails to pay the debt on the due date, the note is said to be dishonored.8. The discounting of a note receivable creates a contingent liability that continues in effect until the due date of the note. ANS: T F T T F F T T 1. Allowance for Doubtful Accounts has a debit balance of $500 at the end of the year (before adjustment), and uncollectible accounts expense is estimated at 3% of net sales. If net sales are $600,000, the amount of the adjusting entry to record the provision for doubtful accounts is a. $18,500 b. $17,500 c. $18,000 d. none of the above 2. On the balance sheet, the amount shown for the Allowance for Doubtful Accounts is equal to the a. Uncollectible accounts expense for the year b. total of the accounts receivables written-off during the year c. total estimated uncollectible accounts as of the end of the year d. sum of all accounts that are past due. 3. What is the type of account and normal balance of Allowance for Doubtful Accounts? a. Contra asset, credit b. Asset, debit c. Asset, credit d. Contra asset, debit 4. If the direct write-off method of accounting for uncollectible receivables is used, what general ledger account is credited to write off a customer’s account as uncollectible? a. Uncollectible Accounts Expense b. Accounts Receivable c. Allowance for Doubtful Accounts d. Interest Expense 5. A 90-day, 12% note for $10,000, dated May 1, is received from a customer on account. Thematurity value of the note isa. $10,000b. $10,300c. $450d. $9,550ANS: c c a b bChapter 91. 2. 3. 4. A business using the perpetual inventory system, with its detailed subsidiary records, does not need to take a physical inventory. Purchased goods in transit, shipped FOB destination, should be excluded from ending inventory. Unsold consigned merchandise should be included in the consignee’s inventory. Of the three widely used inventory costing methods (FIFO, LIFO, and average), the LIFO method of costing inventory is based on the assumption that costs are charged against revenues in the reverse order in which they were incurred.During inflationary periods, the use of the FIFO method of costing inventory will yield an inventory amount for the balance sheet approximating the current replacement cost.When using the FIFO inventory costing method, the most recent costs are assigned to the cost of goods sold.The use of the lower-of-cost-or-market method of inventory valuation increases net income for the period in which the inventory replacement price declined. Generally, the lower the number of days’ sales in inventory, the better.ANS: F F F T T F F TTaking a physical count of inventorya. is not necessary when a periodic inventory system is usedb. is a detective controlc. has no internal control relevanced. is not necessary when a perpetual inventory system is usedMerchandise inventory at the end of the year was inadvertently overstated. Which of the following statements correctly states the effect of the error on net income, assets, and owner’s equity?a. net income is overstated, assets are overstated, owner’s equity is understatedb. net income is overstated, assets are overstated, ow ner’s equity is overstatedc. net income is understated, assets are understated, owner’s equity is understatedd. net income is understated, assets are understated, owner’s equity is overstated Inventory costing methods place primary emphasis on assumptions abouta. flow of goodsb. flow of costsc. flow of goods or costs depending on the methodd. flow of valuesIf merchandise inventory is being valued at cost and the purchase price is steadily falling, which method of costing will yield the largest net income?a. average costb. LIFO 5. 6. 7. 8. 1. 2. 3. 4.c. FIFOd. weighted average 5. On the basis of the following data, what is the estimated cost of the merchandise inventory on October 31 by the retail method? Oct. 1 Merchandise Inventory $225,000 $324,500 Oct. 1-31 Purchases (net) 335,000 475,500 Oct. 1-31 Sales (net) 700,000 a. $372,000 b. $140,000 c. $100,000 d. $ 70,000 6. If the estimated rate of gross profit is 40%, what is the estimated cost of the merchandise inventory on June 30, based on the following data? June 1 Merchandise inventory $ 75,000 June 1-30 Purchases (net) 150,000 June 1-30 Sales (net) 135,000 a. $144,000 b. $140,000 c. $ 81,000 d. $ 54,500 7. Too much inventory on handa. reduces solvencyb. increases the cost to safeguard the assetsc. increases the losses due to price declinesd. all of the aboveANS: b b b b d a dChapter 10 1. The acquisition costs of property, plant, and equipment should include all normal, reasonable and necessary costs to get the asset in place and ready for use.2. Land acquired as a speculation is reported under Investments on the balance sheet.3. Standby equipment held for use in the event of a breakdown of regular equipment is reported as property, plant, and equipment on the balance sheet.4. As a company depreciates a piece of equipment, it cash flow goes up.5. All property, plant, and equipment assets are depreciated over time.6. The declining-balance method is an accelerated depreciation method.7. The cost of replacing an engine in a truck is an example of ordinary maintenance.8. The cost of new equipment is called a revenue expenditure because it will help generate revenues in the future.9. A gain can be realized when a fixed asset is discarded.10. When exchanging equipment, if the trade-in allowance is greater than the book value a loss results.11. The cost of a patent with a remaining legal life of 10 years and an estimated useful life of 7 years is amortized over 10 years.12. The method used to calculate the depletion of a natural resource is the straight line method.13. The higher the ratio of fixed assets to long-term liabilities the greater the margin of safety.ANS: T T T F F T F F F F F F T1. Factors contributing to a decline in the usefulness of a fixed asset may be divided into the following two categoriesa. salvage and functionalb. physical and functionalc. residual and salvaged. functional and residual2. Accumulated Depreciationa. is used to show the amount of cost expiration of intangiblesb. is the same as Depreciation Expensec. is a contra asset accountd. is used to show the amount of cost expiration of natural resources3. Equipment with a cost of $80,000, an estimated residual value of $5,000, and an estimated life of 15 years was depreciated by the straight-line method for 5 years. Due to obsolescence, it was determined that the useful life should be shortened by 5 years and the residual value changed to zero. The depreciation expense for the current and future years isa. $5,500b. $11,000c. $10,000d. $5,0004. A fixed asset with a cost of $42,000 and accumulated depreciation of $38,500 is traded for a similar asset priced at $60,000. Assuming a trade-in allowance of $5,000, the cost basis of the new asset isa. $58,000b. $58,500c. $60,000d. $61,5005. A machine with a cost of $65,000 has an estimated residual value of $5,000 and an estimated life of 4 years or 18,000 hours. What is the amount of depreciation for the second full year, using the declining-balance method at double the straight-line rate?a. $15,000b. $30,000c. $16,250d. $32,500ANS: b c b b cChapter 11 1. For a current liability to exist, the following two tests must be met. The liability must be due usually within a year and must be paid out of current assets.2. For an interest bearing note payable, the amount borrowed is equal to the face value of the note.3. The proceeds of a discounted note are equal to the face value of the note.4. Obligations that depend on past events and that are based on future transactions are contingent liabilities.5. The journal entry to record the cost of warranty repairs that were incurred during the current period, but related to sales made in prior years, includes a debit to Warranty Expense.6. Generally, all deductions made from an employee’s gross pay are required by law.7. FICA tax is a payroll tax that is paid only by employers.8. The higher the quick ratio, the more liquid a company is.ANS: T T F F F F F T1. On June 8, Acme Co. issued an $80,000, 6%, 120-day note payable to Still Co. Assume that the fiscal year of Acme Co. ends June 30. What is the amount of interest expense recognized by Acme in the current fiscal year?a. $293.33b. $400.00c. $391.11d. $1,600.002. Proceeds of $48,750 were received from discounting a $50,000, 90-day note at a bank. The discount rate used by the bank in computing the proceeds wasa. 6.25%b. 10.00%c. 10.26%d. 9.75%3. Pilgrim Company sells merchandise with a one year warranty. In 2005, sales consisted of 1,500 units. It is estimated that warranty repairs will average $10 per unit sold, and 30% of the repairs will be made in 2005 and 70% in 2006. In the 2005 income statement, Pilgrim should show warranty expense ofa. $4,500b. $10,500c. $15,000d. $0ANS: a b cChapter 12 1. A corporation is a separate entity for accounting purposes but not for legal purposes.2. Double taxation is a disadvantage of a corporation because the same party has to pay taxes twice on the income.3. The two main sources of stockholders’ equity are investments contributed by stockholders and net income retained in the business.4. The balance in retained earnings should be interpreted as representing surplus cash left over for dividends.5. Preferred stock with a preferential right to dividends in arrears is referred to asparticipating preferred.6. If 50,000 shares are authorized, 37,000 shares are issued, and 2,000 shares are reacquired, the number of outstanding shares is 39,000.7. When a corporation issues stock at a premium, it reports the premium as an other income item on the income statement.8. If 100 shares of treasury stock were purchased for $50 per share and then sold at $60 per share, $1,000 of income is reported in the income statement.9. Since a stock split changes information of a business, this transaction needs to be recorded.10. If 20,000 shares are authorized, 14,000 shares are issued, and 500 shares are held as treasury stock, a cash dividend of $1 per share would amount to $14,000.11. The declaration and issuance of a stock dividend does not affect the total amount of a corporation’s assets, liabilities, or stockholders’ equity.12. The dividend yield indicates the rate of return to stockholders in terms of cash dividend distributions.ANS: F F T F F F F F F F T T1. The outstanding stock is composed of 10,000 shares of $100 par, cumulative preferred $8 stock, and 50,000 shares of no-par common stock. Preferred dividends have been paid every year except for the preceding year and the current year. If $380,000 is to be distributed as a dividend for the current year, what total amount will be distributed to the common stockholders? a. $380,000b. $220,000c. $80,000d. $160,0002. A corporation issues 2,000 shares of common stock for $ 32,000. The stock has a stated value of $10 per share. The journal entry to record the stock issuance would include a credit to Common Stock fora. $20,000b. $32,000c. $12,000d. $2,0003. When common stock is issued in exchange for a noncash asset, the transaction should be recorded ata. the par value of the stock issuedb. the fair market value of the stockc. the fair market value of the asset acquiredd. the fair market value of the asset acquired or the fair market value of the stock, whichever canbe determined more objectively.4. Treasury stock that had been purchased for $5,400 last month was reissued this month for $7,500. The journal entry to record the reissuance would include a credit。

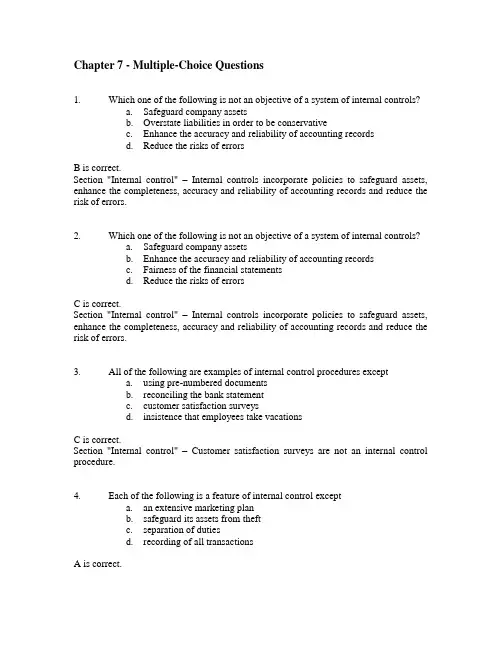

Chapter 7 - Multiple-Choice Questions