P13 Fin Acctg 3 Ques Nov 2015

财务会计专业英语 (10)

5.1

By reading the statement of cash flows, the reader might find answers to the following questions:

• Why did cash decrease for Home Depot when it reported net income for the period?

stock

5. Gain on the Sale of Automobile formerly used in the

business

6. The proceeds from the sale of the automobile in Item

#5.

7. An increase in the balance in a retailer's Merchandise

14. A decrease in the current asset account Prepaid

Insurance

15. A decrease in the current liability Income Taxes

Payable

16. The proceeds from issuing additional Common

$ 5,000 $60,000 $20,000

$85,000

Jan. 1, 2003 $-0-

-0$-0-

$-0$-0$-0-

$-0-

Steps in Preparation--2

Step 1. Determine the change in cash. Step 2. Determine the net cash flow from operating activities. Step 3. Determine net cash flows from investing and financing activities.

ACC00132-2015-2 Income Examples(1)

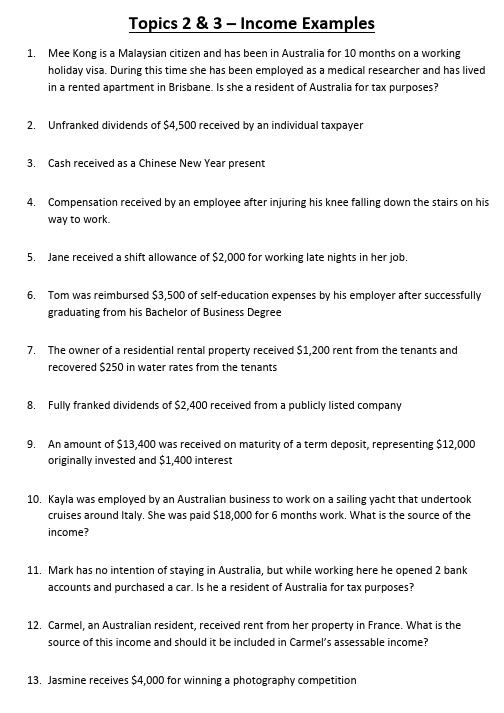

Topics 2 & 3 – Income Examples1.Mee Kong is a Malaysian citizen and has been in Australia for 10 months on a workingholiday visa. During this time she has been employed as a medical researcher and has lived in a rented apartment in Brisbane. Is she a resident of Australia for tax purposes?2.Unfranked dividends of $4,500 received by an individual taxpayer3.Cash received as a Chinese New Year presentpensation received by an employee after injuring his knee falling down the stairs on hisway to work.5.Jane received a shift allowance of $2,000 for working late nights in her job.6.Tom was reimbursed $3,500 of self-education expenses by his employer after successfullygraduating from his Bachelor of Business Degree7.The owner of a residential rental property received $1,200 rent from the tenants andrecovered $250 in water rates from the tenants8.Fully franked dividends of $2,400 received from a publicly listed company9.An amount of $13,400 was received on maturity of a term deposit, representing $12,000originally invested and $1,400 interest10.Kayla was employed by an Australian business to work on a sailing yacht that undertookcruises around Italy. She was paid $18,000 for 6 months work. What is the source of the income?11.Mark has no intention of staying in Australia, but while working here he opened 2 bankaccounts and purchased a car. Is he a resident of Australia for tax purposes?12.Carmel, an Australian resident, received rent from her property in France. What is thesource of this income and should it be included in Carmel’s assessable income?13.Jasmine receives $4,000 for winning a photography competition14.Phil received $6,500 from mowing lawns of his neighbours throughout the year. He did thison weekends for exercise and it was not part of his normal job as a builder.15.The owner of commercial premises was paid $10,000 by a tenant who failed to makenecessary repairs to the premises before the end of the lease16.Mary received $480 from the Australian Taxation Office, which represented interest on taxthat she paid early before the due date because she was going on a holiday for 6 months17.As Madeline had 3 children in child care, the government paid her $7,500 in child carebenefit to help cover the cost of her childcare18.Carter received $5,000 for being a member of the Army Reserves on weekends19.Sally received a scholarship of $6,000 to help with her study costs as a full time universitystudent20.Jack received $500,000 when he sold shares he had owned for 25 years21.Renee, and Australian resident, received a $600 dividend from a London company. What isthe source of the dividend and should it be included in Renee’s assessable income?22.Barry’s Bikes received $3,200 from a customer being payment of a debt that Barry hadpreviously written off as bad because the customer failed to pay the amount when it was due23.Jane received $396 in dividends from a company in Singapore. This was after foreign tax of$44 was withheld. What is the source of the income? How much will be assessable to Jane, assuming she is a resident of Australia for tax purposes?24.Alison received a $5,800 Carer’s Allowance from Centrelink25.Jim received a $10,600 Newstart Allowance from Centrelink. Of this total amount, $2,000was the supplementary amount26.A taxpayer received $15,000 for selling shares that were purchased 10 months ago27.Adam’s computer business was robbed 2 months ago with thieves taking $5,000 worth ofcomputer equipment. He has just received $4,500 from his insurance company28.Simon just sold his rental property and the sale contract includes a $450 reimbursementadjustment for rates on the property in his favour29.Amy received $6,000 compensation for injuries to her wrist after a motorcycle accident30.An employee taxpayer has just been made redundant from her job. She received $160,000from her employer, which consisted $10,000 for unused annual leave, $25,000 for unused long service leave and $125,000 as a bona fide redundancy31.A taxpayer received $5,000 from Care Australia for 5 months work she undertook in Nepalafter the earthquakes32.A taxpayer is an accountant for Ernst & Young in Australia, but worked in London for 6months of the year. He received $28,000 for the work he undertook in London33.A taxpayer receives $35,000 from his grandmother’s deceased estate34.A taxpayer received a foreign dividend of $1,500 after tax of $500 was withheld35.An employee taxpayer attended a conference in relation to his work and paid $400 foraccommodation expenses. When he returned from the conference his employerreimbursed him the $400。

ACCAF3中英文单词对照表

第一章1.资产asset2.负债liability3.所有者权益equity=capital=net asset4.收入income=revenue=sales5.费用expense6.厂房plant7.机器machine8.无形资产intangible asset9.非流动资产Non current asset(6 7 8属于9)10.库存现金petty cash11.银行存款cash12.应收账款trade receivable=A/R13.存货inventory14.流动资产current asset (10 11 12 13属于14)15.贷款loan16.应付账款trade payables=A/P17.预收账款advance from customers18.流动负债current liability(15 16 17属于18)19.实收资本share capital20.资本公积share premium21.留存收益Retained earnings=R/ES22.资产负债表statement of financial position=SOFP23.所有者权益变动表statement of changes in equity=SOCIE24.现金流量表statement of cash flow25.利润表statement of comprehensive income=SOCI第二章1.复式记账double-entry bookkeeping2. 借Debit3. 贷Credit4. 预付账款prepayment5. 利润profit第四章1.增值税value added tax=sales tax2.进项税额input tax3.销项税额output tax4.贸易折扣(商业折扣)trade discount5.现金折扣cash discount6. 不含税exclusive7. 含税inclusive 8. 交易事项Transaction9. 取走withdraw第五章1.现金petty cash=cash on hand2.支票cheque3.自动转账standing order/direct debt4.银行给你存款利息bank interest on deposit5.银行收取利息手续费bank charges6.银行收取利息bank interest on overdraft7.空头支票dishonored cheque8.未结清的款项,别人给我的uncleared lodgement9.未承兑的汇票unpresent cheque10.别人给我支票undrawn cheque11.公司业务错误business error12.银行业务错误bank error13.银行存款余额调节表bank reconciliation14.银行透支overdraft15.银行对账单bank statement16.现金账簿/银行存款日记账cash book17.总账control accounts =general ledger18.明细账individual ledger =personal ledger=subsidiary ledger=memo account19.应收账款总账receivable control account =receivable general ledger20.应收账款明细账receivable ledger=sales ledger21.坏账bad debt=irrecoverable debt22.毛利润gross profit23.一般性坏账准备general allowance24.特殊性坏账准备specific allowance25.可疑的坏账doubtful debt25.资产减值损失expense-bad debts written off26.坏账准备allowance for A/R第六章1 存货inventory2 先进先出first in first out3 特殊计价法specific identification4 加权平均法period average=weighted average5 移动加权平均法continuous average=continuous weighted average cost method=moving weighted average method6 成本historical cost7 可变现净值net realizable value8 资产减值损失-计提的存货跌价准备expense-inventory written-down9 永续盘存制perpetual inventory system10 实地盘存制periodic inventory system11 购货purchase12 数量quantity13 单价unit cost14 毛利润率gross profit margin第七章1 买价original purchase price2 场地准备费cost of site preparation3 运输费delivery and handling4 安装费installation5 员工培训费employee training6资本化后续支出capital expenditure7 费用化后续支出revenue expenditure8 直线法straight line method9 累计折旧accumulated depreciation10 原值original cost11 预计净残值estimated residual value12 预计使用寿命useful life13 余额递减法reducing balance method14 账面价值net book value=carrying value15 固定资产处置disposal of fixed asset16 固定资产清理disposal account17 研究性支出research cost18 开发性支出development cost19 不确定使用寿命indefinite useful life20 确定使用寿命finite useful life21累计摊销accumulated amortization22 每年的折旧depreciation for each year第八章1或有事项contingencies2.或有负债contingent liabilities3.现时义务present obligation4.或有资产contingent assets5.肯定的certain6.可能的probable7.或许的possible8.遥远的,渺茫的Remote9.预计负债provision第九章1.试算平衡trial Balance2.交易发生transaction occur3.复式记账Double entry4.结账Balance off5.期末调整Year End Adjustment6.错误Errors7.遗漏omission8.任命错误commission errors9.原则性错误errors of principle10.加总错误casting errors11.暂记账户suspense account第十章1.预付账款prepayment2.预提费用accruals3.其他应收款other receivable4.递延收入Deferred income5.到期expire6.欠款arrear7.租客Tenant8.财务报表financial statements9.资产负债表The Statement of Financial Position10.利润表The statement of comprehensive income11.所有者权益变动表The statement of change in equity第十一章1.现金流量表The statement of cash flow2.经营活动operating activities3.投资活动investing activities4.筹资活动financing activities5.直接法The direct method6.间接法indirect method7.付出利息Interest paid8.付出所得税Income tax paid9.付出红利Dividends paid第十二章1.资产负债表日后事项Events after the reporting period2.调整事项adjusting event3.非调整事项Non-adjusting event第十三章1.会计政策Accounting policy2.会计估计Accounting Estimate。

寺冈电子秤报错汇总

寺冈电子秤报错说明及故障排除方法大全一、故障排除:1.?秤的错误提示排除及错误显示说明0 PRINTER CASSETTEOPEN?装纸盒安装没有到位,请重新安装纸盒1 PAPER END?标签传感器检测到没有标签,请换新标签2 PLEASE PRESS FEED KEY?没有走纸,请按[走纸]键进行走纸3 PLEASE PEEL LABEL?剥离传感器被激活,请取走走出的标签4 CHANGE LABEL SWITCH?取出纸盒并将纸盒上的滑片拨到标签位置5 CHANGE RECEIPT SWITCH?取出纸盒并将纸盒上的滑片拨到收据位置6 NON PRINT?无手动打印7 UNIT PRICE OVERFLOW?单价溢出,请检查单价8 TOTAL PRICE OVERFLOW?累计后的总计溢出,请检查单价及价格9 NON LABEL?标签自由格式未设定,请设定自由格式或标准格式11 INSUFFICIENT SPACE?打印空间不够12 NON ADVERTISEMENT?没有该广告信息或编号存在13 READ FILE?读取文件出错,请检查电池开关是否正确或清除内存14 NON SHOP NAME?没有该店名数据或编号存在15 PRINTER HEAD NO CLOSE?打印头未合上,请闭合热敏打印头16 WRITE FILE?写入文件出错,内存问题,请清除内存17 NO MEMORY?内存不够,请扩展内存或删除无用的数据18 FILE DELETE ERROR?删除文件出错,内存问题19 DIFFERENT LABEL FORMAT?标签格式无效20 PLEASE REMOVE WEIGHT?固定价格的项目,请移去重物21 PLU NOT EXIST?没有该PLU数据或编号的存在22 TOTAL PRICE = 0?无该项目的总计,单价或重量为零23 WEIGH ITEM?乘法键不能用于称重的PLU24 CANNOT USE IN PRE-PACK?累加不允许用于预包装模式25 PRESET KEY NOT SET?预设键中无预设数据或PLU26 WEIGHT OVERFLOW?在打印时重量超出最大称量范围27 NEGATIVE TOTAL PRICE?打折后总价为负的,请检查设定的折扣28 TOTAL PRICE OVERFLOW?总价超出显示限制或打印限制的位数29 ILLEGAL OPERATION?操作步骤错误,请检查操作步骤30 QUANTITY = 0?当数量为0时无法打印,请输入数量值31 PLEASE SET TARE VALUE?当强制去皮为允许时,皮重值必须被设定或输入32 KEY INVALID?所按的键无效或没有确切的功能33 NUMBER INVALID?只有数字的输入或输入的数字无功能34 EXCEED MAX LIMIT?字符的最大数量已达到35 SIZE INVALID?无该字符尺寸存在,请检查下栽的数据文件36 MAIN GROUP NOT EXIST?无此项主组数据或编号存在37 PLU INVALID?当复制PLU时无此PLU数据38 DEPARTMENT NOT EXIST?没有该部门数据或编号存在39 TAX FILE NOT EXIST?无该税率数据或编号存在40 CLERK NOT EXIST?无该店员数据或编号存在41 PLEASE PRESS PLU KEY?请按?PLU (#)?键,保存某些步骤中的数据42 DATE INVALID?输入的日期格式错误,请输入正确的日期格式数据43 TIME INVALID?输入的时间格式错误,请输入正确的时间格式数据44 FUNCTION NOT EXIST?无此功能存在,请检查SPEC的设置45 KEY NOT ASSIGN?欲删除的预设键不存在46 KEY ALREADY ASSIGNED?预设键已被分配功能或PLU数据47 LOGO NOT EXIST?无该logo数据或编号存在48 LABEL INVALID?无此标签数据49 PLU NOT AVAILABLE?当用扫描仪扫描PLU号时无该PLU50 DATA INVALID?仅对U1使用,当使用FOR功能时数量设定错误51 QUANTITY OVERFLOW?数量数据超出限制范围52 NO LINK?当与FL-1发送或接收数据时,没有发现FL-1存在53 SYSTEM ERROR?当与FL-1发送或接收数据时数据出错54 VERIFY ERROR?当与FL-1上的数据进行比较时出错55 TIME ERROR?当打印时,日期和时间无效,请重新设置日期和时间56 BELOW MIN WEIGHT?当打印时重量低于最小称量57 REC CHOSEN USED IN MG?将要删除的记录被主组文件使用了58 REC CHOSEN USED IN PLU?将删除的记录被PLU数据使用了59 REC CHOSEN USED IN ADV60 REC CHOSEN USE IN SHOP61 ACC PRICE OVERFLOW?累加后的价格超出限定范围62 ACC QUANTITY OVERFLOW?累加后的数量超出限定范围63 PLEASE SET LABEL QTY?当打印数量功能启用时,请设定标签数量64 NOT PREPACK MODE?某些功能只能在预包装模式有效65 GRAND TOTAL OVERFLOW?总合计的价格超出范围66 ORG PRICE OVERFLOW?当使用折扣时,原来的价格超出范围67 INGREDIENT NOT EXIST?无该成份数据或标号存在68 SPECIAL MSG NOT EXIST?无此特殊信息或编号存在69 TEXT NOT EXIST?无此文本数据或编号存在70 CLERK ASSIGN?店员已分配,请选择另一店员71 NO PRINT AREA?某些功能在标签上无打印区域,如文本或成份等72 USER INGRE NOT EXIST?无此用户成份数据或编号存在73 INSUFF ADVERT SPACE?广告信息的打印区域不够74 DISCOUNT PRICE INVALID?目标价格不到固定折扣价75 PRINT INHIBITED?在预包装模式不能打印计重项目76 ORG UPRICE OVERFLOW?使用折扣时,原来的单价超出限制77 PLACE NOT EXIST?无产地数据或编号存在78 SELF SERVICE MODE?仅用于自助操作模式79 OFF LINE?客户机不能连接到主机80 DFS INIT ERROR81 COMM OFF82 BCC ERROR83 CODE ERROR84 RECEIVE OVERFLOW85 TIME OUT?时间溢出86 PLACE INSUFF SPACE?位置数据的打印区域不够87 NO ITEM CODE?无项目代码88 IMAGE NOT EXIST?无此图形数据或编号存在89 NOT IN USED90 EXCESS DATA?当更正数据时,无此数据被更正91 WEIGHT TOO LIGHT?称重检查功能92 WEIGHT TOO HEAVY?称重检查功能93 CLEAR ACCUMULATION?当流动店员清除交易数据时,店员累计没有结束94 POINT AND SHOP?仅使用于点和店的操作95 PLU NOT IN RANGE96 CLERK USED EXCEEDED97 NO FLAG CODE98 PLEASE REMOVE TARE99 NOT IN USED100 NOT IN USED101 SCROLL MSG NOT EXIST?无该滚动信息数据或编号的存在102 SCROLL SEQ NOT EXIST?无此滚动次序数据或编号存在103 SCROLL SEQUENCE IN USE?滚动次序被使用,请选择另一次序104 REC CHOSEN USE IN SCSQ?该滚动信息已用于滚动次序中105 CLERK FILE FULL?店员文件已满106 CLERK IN USE?流动店员时,通用的店员被同时调用107 NOT IN USED108 PRESET TARE ASSIGNED109 MACRO ALREADY ASSIGNED?110 NOT IN USED111 SERVER NO RESPONSE112 ETHERNET COM. ERROR?通信出错,请检查连接线和服务器(主机)113 NO PRICE PRINT114 NO DATA EXIST115 NO DATA116 INVALID END DATE117 INVALID END TIME118 PLEASE RE-SCAN119 NOT IN USED120 NOT IN USED121 NOT IN USED122 NOT IN USED123 NOT IN USED124 NOT IN USED125 NOT IN USED126 PASSWORD INCORRECT127 PLS CHECK BARCD CONFIG128 ACCESS DENIED!129 INVALID CUSTOMER NO.130 MAX CREDIT REACHED131 CUSTOMER LOCKED!132 CLERK NOT LOGIN133 INVALID BARCODE FORMAT134 NO TRACEABILITY RECORD2.?连网故障软件设置当设置完秤号后,应注意检查HOSTS文件,在Happy 2000的安装目录和Windows目录下都要有这个文件,它包含了所连接到网络上的秤的IP地址。

朗道多项生化定值质控

0843PAGE 1 OF 24LIQUID ASSAYED CHEMISTRY CONTROL PREMIUM PLUS - LEVEL 1 (LIQ CHEM ASY PREMIUM PLUS 1)Cat. No . LAL 4213 Lot No . 153UL Size : 12 x 5 ml Expiry : 2015-02INTENDED USEThis product is intended for in vitro diagnostic use, in the quality control of diagnostic assays. The Liquid Assayed Chemistry Control Premium Plus is for the control of accuracy.DEVICE DESCRIPTIONThe Liquid Assayed Chemistry Control Premium Plus is supplied at 3 levels, level 1, 2 and 3. Target values and ranges are supplied for the analytes listed in the values section at all three levels.SAFETY PRECAUTIONS AND WARNINGSFor in vitro diagnostic use only. Do not pipette by mouth. Exercise the normal precautions required for handling laboratory reagents.Human source material from which this product has been derived has been tested at donor level for the Human Immunodeficiency Virus (HIV 1, HIV 2) antibody, Hepatitis B Surface Antigen (HbsAg), and Hepatitis C Virus (HCV) antibody and found to be NON-REACTIVE. FDA approved methods have been used to conduct these tests.However, since no method can offer complete assurance as to the absence of infectious agents, this material and all patient samples should be handled as though capable of transmitting infectious diseases and disposed of accordingly.Health and Safety Data Sheets are available on request.STORAGE AND STABILITY OPENED: Store refrigerated (+2ºC to + 8ºC). Thawed serum is stable for 7 days at +2ºC to +8ºC, with the followingexceptions: Troponin T is stable for 3 days at +2ºC to +8ºC. Only the required amount of product should be removed. After use, any residual product should NOT BE RETURNED to the original vial.UNOPENED: Store frozen at -20ºC to -70ºC. Stable to expiration date printed on individual vials (see Limitations).LIMITATIONSFor Total Acid Phosphatase, the material should be stabilised by adding 1 drop (25 µl – 30 µl) of 0.7M Acetic acid solution to 1ml of the serum after thawing. After stabilisation, Total Acid Phosphatase is stable for 7 days at +2ºC to +8ºC. Bilirubin in the serum is light sensitive and it is recommended that the serum is stored in the dark.ALT, Total Acid Phosphatase, Alkaline Phosphatase, Total and Direct Bilirubin values may gradually decrease during the products shelf life.Bacterial contamination of the thawed serum will cause reductions in the stability of many components. The control should not be used as a calibration material.PREPARATION1. Allow the frozen control to thaw at room temperature (+15ºC to +25ºC) until completely thawed. Swirl the contents to ensurehomogeneity.2. Refer to the Control section of the individual analyser application.3. Refrigerate any unused material. Prior to reuse, mix contents thoroughly.MATERIALS PROVIDEDLiquid Assayed Chemistry Control Premium Plus - Level 1 12 x 5 mlMATERIALS REQUIRED BUT NOT PROVIDED NoneASSIGNED VALUESEach lot of serum is submitted to a number of external laboratories. Values are assigned from a consensus of results obtained by these laboratories and internal testing conducted at Randox Laboratories Ltd. With each batch, a control range is provided for individual parameters and each parameter method.If an instrument specific value is not available, refer to the Mean of all Instruments section. If necessary, contact Randox Laboratories – Customer Technical Services, Northern Ireland, Tel: +44 (0) 28 9445 1070 or email Technical.Services@29 Nov 13 rwPage 2 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 3 of 24 29/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 4 of 24 29/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 5 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 6 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 7 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 8 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 9 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 10 of 2429/11/2013___________________________________________________________________________________________________RANDOX Laboratories Ltd., 55 Diamond Road, Crumlin, Co. Antrim, United Kingdom, BT29 4QYTel: +44 (0) 28 9442 2413 Fax: +44 (0) 28 9445 2912Email: applications@ Website: Page 11 of 2429/11/2013___________________________________________________________________________________________________Page 12 of 2429/11/2013___________________________________________________________________________________________________Page 13 of 2429/11/2013___________________________________________________________________________________________________Page 14 of 2429/11/2013___________________________________________________________________________________________________Page 15 of 2429/11/2013___________________________________________________________________________________________________Page 16 of 2429/11/2013___________________________________________________________________________________________________Page 17 of 2429/11/2013___________________________________________________________________________________________________Page 18 of 2429/11/2013___________________________________________________________________________________________________Page 19 of 2429/11/2013___________________________________________________________________________________________________Page 20 of 2429/11/2013___________________________________________________________________________________________________Page 21 of 2429/11/2013___________________________________________________________________________________________________Page 22 of 2429/11/2013___________________________________________________________________________________________________Page 23 of 2429/11/2013___________________________________________________________________________________________________Page 24 of 2429/11/2013___________________________________________________________________________________________________。

Azithromycin Tablets(阿奇霉素片) USP40

C S= concentration of USP Azithromycin RS in the Sample solution: Nominally 1mg/mL of azithromycinStandard solution (mg/mL)in Mobile phase from NLT 20 Tablets, finely powdered.C U= nominal concentration of azithromycin in Sonicate and shake as needed to dissolve.Sample solution 1 (mg/mL)Chromatographic systemP= potency of azithromycin in USP Azithromycin(See Chromatography 〈621〉, System Suitability.) RS (µg/mg)Mode: LCF= conversion factor, 0.001mg/µg Detector: UV 210 nmWhere packaged in a multiple-unit container Column: 4.6-mm × 25-cm; 5-µm packing L1Calculate the percentage of the labeled amount of Column temperature: 50°azithromycin (C38H72N2O12) in the portion of Flow rate: 2mL/minAzithromycin for Oral Suspension taken:Injection volume: 100µLSystem suitabilityResult = (r U/r S) × (C S/C U) ×P×F× 100Sample:Standard solutionSuitability requirementsr U= peak response from Sample solution 2Tailing factor: NMT 2.0, Standard solutionr S= peak response from the Standard solution Relative standard deviation: NMT 2.0%, StandardC S= concentration of USP Azithromycin RS in the solutionStandard solution (mg/mL)AnalysisC U= nominal concentration of azithromycin in Samples:Standard solution and Sample solutionSample solution 2 (mg/mL)Calculate the percentage of the labeled amount of P= potency of azithromycin in USP Azithromycin azithromycin (C38H72N2O12) in the portion of Tablets RS (µg/mg)taken:F= conversion factor, 0.001mg/µgAcceptance criteria: 90.0%–110.0%Result = (r U/r S) × (C S/C U) ×P×F× 100PERFORMANCE TESTS rU= peak response of azithromycin from the•D ELIVERABLE V OLUME〈698〉: Meets the requirements Sample solution•U NIFORMITY OF D OSAGE U NITS〈905〉rS= peak response of azithromycin from the For single-unit containers Standard solutionAcceptance criteria: Meets the requirements CS= concentration of USP Azithromycin RS in theStandard solution (mg/mL)SPECIFIC TESTS CU= nominal concentration of azithromycin in the •P H 〈791〉Sample solution (mg/mL) For a solid packaged in single-unit containers:P= potency of USP Azithromycin RS (µg/mg)9.0–11.0, in the suspension constituted as directed in F= conversion factor, 0.001mg/µgthe labeling Acceptance criteria: 90.0%–110.0%For a solid packaged in multiple-unit containers:8.5–11.0, in the suspension constituted as directed in PERFORMANCE TESTSthe labeling•D ISSOLUTION〈711〉Medium: pH 6.0phosphate buffer; 900mL ADDITIONAL REQUIREMENTS Apparatus 2: 75 rpm•P ACKAGING AND S TORAGE: Preserve in tight containers.Time: 30 min•USP R EFERENCE S TANDARDS〈11〉Solution A: 4.4mg/mL of dibasic potassium phosphate USP Azaerythromycin A RS and 0.5mg/mL of sodium 1-octanesulfonate, adjusted 9-Deoxo-9a-aza-9a-homoerythromycin A;with phosphoric acid to a pH of 8.20 ± 0.056-Demethylazithromycin.Mobile phase: Acetonitrile, methanol, and Solution A C37H70N2O12734.96(9:3:8)USP Azithromycin RS Diluent: 17.5mg/mL of dibasic potassium phosphate.Adjust with phosphoric acid to a pH of 8.00 ± 0.05.Prepare a mixture of this solution and acetonitrile(80:20).Standard stock solution: Dissolve USP Azithromycin RS Azithromycin Tablets in Medium to obtain a solution having a known concen-tration of about (L/1000) mg/mL, where L is the Tablet DEFINITION label claim in mg.Azithromycin Tablets contain NLT 90.0% and NMT 110.0%Standard solution: Dilute the Standard stock solutionof the labeled amount of azithromycin (C38H72N2O12).with Diluent to obtain a solution having a known con-centration of about (L/2000) mg/mL, where L is the IDENTIFICATION Tablet label claim in mg.•A. The retention time of the major peak of the Sample Sample solution: Pass a portion of the solution under solution corresponds to that of the Standard solution, as test through a suitable filter of 0.45-µm pore size. Di-obtained in the Assay.lute a portion of the filtrate with Diluent to obtain asolution having a theoretical concentration of about ASSAY(L/2000) mg/mL, where L is the Tablet label claim in•P ROCEDURE mg, assuming complete dissolution.Buffer: Dissolve 4.6g of monobasic potassium phos-Chromatographic systemphate anhydrous in 900mL of water. Adjust with 1N(See Chromatography 〈621〉, System Suitability.)sodium hydroxide to a pH of 7.5, and dilute with waterto 1L.Mobile phase: Acetonitrile and Buffer (65:35)Standard solution: 1mg/mL of USP Azithromycin RS inMobile phase. Sonicate and shake as needed to dissolve.Mode: LC Standard stock solution: 0.4mg/mL of USP Azithro-Detector: UV 210 nm mycin RS in acetonitrile. Sonicate and shake as needed Column: 4.6-mm × 15-cm; 5-µm packing L1to dissolve.Column temperature: 50°Standard solution: 0.02mg/mL of azithromycin from Flow rate: 1.5mL/min Standard stock solution in Diluent AInjection volume: 50µL Sensitivity solution: 0.004mg/mL of azithromycin System suitability from Standard solution in Diluent ASample:Standard solution Sample stock solution: Nominally 14.3mg/mL of Suitability requirements azithromycin prepared as follows. Weigh and finely Tailing factor: NMT 2.0powder NLT 20 Tablets. Transfer nominally 1430mg of Relative standard deviation: NMT 2.0%azithromycin to a 100-mL volumetric flask. Add 75mL Analysis of acetonitrile, and sonicate for NLT 15 min. Shake by Samples:Standard solution and Sample solution mechanical means for NLT 15 min. Allow the solution Calculate the percentage of the labeled amount of to equilibrate to room temperature, dilute with acetoni-azithromycin (C38H72N2O12) dissolved:trile to volume, and mix.Sample solution: Nominally 4mg/mL of azithromycin Result = (r U/r S) × (C S/L) ×V× 100prepared as follows. Centrifuge an aliquot of the Samplestock solution for NLT 15 min. Transfer 7.0mL of the r U= peak response of azithromycin from the supernatant to a 25-mL volumetric flask, and dilute Sample solution with Diluent B to volume.r S= peak response of azithromycin from the Blank:Diluent AStandard solution Chromatographic systemC S= concentration of the Standard solution(See Chromatography 〈621〉, System Suitability.)(mg/mL)Mode: LCL= label claim (mg/Tablet)Detector: UV 210 nmV= volume of Medium, 900mL Column: 4.6-mm × 15-cm; 3.5-µm packing L1 Tolerances: NLT 80% (Q) of the labeled amount of Column temperature: 50°azithromycin (C38H72N2O12) is dissolved.Flow rate: 1.2mL/min•U NIFORMITY OF D OSAGE U NITS〈905〉: Meet the Autosampler temperature: 4°requirements Injection volume: 100µLSystem suitabilityIMPURITIES Samples:System suitability solution, Standard solution,•O RGANIC I MPURITIES and Sensitivity solutionProtect all solutions containing azithromycin from light.Suitability requirementsRefrigerate the Standard solution and the Sample solution Signal-to-noise ratio: NLT 10, Sensitivity solution after preparation and during analysis, using a refriger-Resolution: NLT 1.0 between desosaminylazithromy-ated autosampler set at 4°. The solutions must be ana-cin and azithromycin related compound F, System lyzed within 24 h of preparation.suitability solutionSolution A: Water and ammonium hydroxide Relative standard deviation: NMT 2.0%, Standard (2000:1.2). The pH of this solution is about 10.5.solutionSolution B: Acetonitrile, methanol, and ammonium hy-Analysisdroxide (1800:200:1.2)Samples:Sample solution and BlankMobile phase: See Table 1.Calculate the percentage of each impurity in the por-tion of Tablets taken:Table 1Result = (r U/r S) × (C S/C U) ×P×F1× (1/F2) × 100 Time Solution A Solution B(min)(%)(%)rU= peak response of each impurity from the 05446Sample solution205446r S= peak response of azithromycin from theStandard solution351090C S= concentration of USP Azithromycin RS in the35.15446Standard solution (mg/mL) 405446CU= nominal concentration of azithromycin in theSample solution (mg/mL) Buffer: 1.7g/L of monobasic ammonium phosphate inP= potency of USP Azithromycin RS (µg/mg) water. Adjust with ammonium hydroxide to a pH of 10.F1= conversion factor, 0.001mg/µg Diluent A: Methanol, acetonitrile, and BufferF2= relative response factor (see Table 2) (350:300:350)Acceptance criteria: See Table 2. The reporting level Diluent B: Methanol and Buffer (1:1)for impurities is 0.1%. Disregard any peaks in the Sam-System suitability stock solution: 0.1mg/mL each ofple solution that correspond to peaks in the Blank.USP Desosaminylazithromycin RS and USP AzithromycinRelated Compound F RS in acetonitrileSystem suitability solution: 0.028mg/mL each of USPDesosaminylazithromycin RS and USP Azithromycin Re-lated Compound F RS from System suitability stock solu-tion in Diluent ATable 2Table 2 (Continued)Relative Relative Acceptance Relative Relative AcceptanceRetention Response Criteria,Retention Response Criteria, Name Time Factor NMT (%)Name Time Factor NMT (%) Azithromycin N-ox-3-Deoxyazithro-ide a0.200.42 1.0mycin (azithro-——mycin B)h,l 1.143′-(N,N-Didemeth-yl)-3′-N-for-Any individual un-—mylazithromycin b0.29 1.7 1.0specified impurity h 1.00.23′-(N,N-Didemeth-Total impurities h—— 5.0yl)azithro-a(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10, mycin(ami-12,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylazinoyl)-β-D-xylo-hex-noazithromycin)c0.340.490.5opyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.Azithromycin related b(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-compound F d0.42 4.3 1.0methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3-formamido-3,4,6-trideoxy-β-D-xylo-hexopyra-Desosaminylazithro-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.mycin e0.46 1.10.5c(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-N-Demethylazithro-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3-amino-3,4,6-trideoxy-β-D-xylo-hexopyra-mycin f0.500.540.7nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.3′-De(dimethylami-d3′-(N-Demethyl)-3′-N-formylazithromycin; (2R,3S,4R,5R,8R,10R,11R,12S, no)-3′-oxoazithro-13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-methyl-α-L-ribo-hexopyra-mycin g0.87 1.4 1.0nosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3-(N-methyl)formamido-3,4,6-trideoxy-β-D-xylo-hexopyranosyl]oxy]-1-oxa-6-Azaerythromycin A h,i0.94——azacyclopentadecan-15-one.Azithromycin 1.0——e(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-2-Ethyl-3,4,10,13-tetrahydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3,4,6-trideoxy-3-dimethylamino-β-D-xylo-2-Desethyl-2-prop-——hexopyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one. ylazithromycin h,j 1.10f(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-3′-N-Demethyl-3′-N-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,[(4-methylphen-12,14-heptamethyl-11-[[3,4,6-trideoxy-3-methylamino-β-D-xylo-hexopyra-——nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.yl)sulfonyl]azithro-g(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3,3-dimethyl-α-mycin h,k 1.11L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-a(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-heptamethyl-11-[[3,4,6-trideoxy-3-oxo-β-D-xylo-hexopyranosyl]oxy]-1-oxa-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,6-azacyclopentadecan-15-one.12,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylazinoyl)-β-D-xylo-hex-h Process impurities that are controlled in the drug substance are not to be opyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.reported. They are listed here for information only. The unspecified impu-b(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-rities and total impurities limits do not include these impurities.methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,i9-Deoxo-9a-aza-9a-homoerythromycin A.12,14-heptamethyl-11-[[3-formamido-3,4,6-trideoxy-β-D-xylo-hexopyra-j(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.methyl-α-L-ribo-hexopyranosyl)oxy]-2-propyl-3,4,10-trihydroxy-3,5,6,8,10, c(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-12,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylamino)-β-D-xylo-hex-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,opyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one dihydrate.12,14-heptamethyl-11-[[3-amino-3,4,6-trideoxy-β-D-xylo-hexopyra-k(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10, d3′-(N-Demethyl)-3′-N-formylazithromycin; (2R,3S,4R,5R,8R,10R,11R,12S,12,14-heptamethyl-11-[[3-[N-(4-methylphenylsulfonyl)-N-methylamino]-3, 13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-methyl-α-L-ribo-hexopyra-4,6-trideoxy-β-D-xylo-hexopyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-nosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3-one.(N-methyl)formamido-3,4,6-trideoxy-β-D-xylo-hexopyranosyl]oxy]-1-oxa-6-l(2R,3R,4S,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-azacyclopentadecan-15-one.methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-4,10-dihydroxy-3,5,6,8,10,12, e(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-2-Ethyl-3,4,10,13-tetrahydroxy-3,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylamino)-β-D-xylo-hexopyra-5,6,8,10,12,14-heptamethyl-11-[[3,4,6-trideoxy-3-dimethylamino-β-D-xylo-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.hexopyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.f(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-ADDITIONAL REQUIREMENTSmethyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,•PACKAGING AND S TORAGE: Preserve in tight containers. 12,14-heptamethyl-11-[[3,4,6-trideoxy-3-methylamino-β-D-xylo-hexopyra-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.Store at controlled room temperature.g(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3,3-dimethyl-α-•USP R EFERENCE S TANDARDS〈11〉L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,14-USP Azithromycin RSheptamethyl-11-[[3,4,6-trideoxy-3-oxo-β-D-xylo-hexopyranosyl]oxy]-1-oxa-USP Azithromycin Related Compound F RS6-azacyclopentadecan-15-one.3′-(N-Demethyl)-3′-N-formylazithromycin;h Process impurities that are controlled in the drug substance are not to be(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dide-reported. They are listed here for information only. The unspecified impu-rities and total impurities limits do not include these impurities.oxy-3-C-methyl-3-O-methyl-α-L-ribo-hexopyra-i9-Deoxo-9a-aza-9a-homoerythromycin A.nosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10,12,j(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-14-heptamethyl-11-[[3-(N-methyl)formamido-3,4, methyl-α-L-ribo-hexopyranosyl)oxy]-2-propyl-3,4,10-trihydroxy-3,5,6,8,10,6-trideoxy-β-D-xylo-hexopyranosyl]oxy]-1-oxa-6-aza-12,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylamino)-β-D-xylo-hex-cyclopentadecan-15-one.opyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one dihydrate.C38H70N2O13762.97k(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-3,4,10-trihydroxy-3,5,6,8,10, USP Desosaminylazithromycin RS12,14-heptamethyl-11-[[3-[N-(4-methylphenylsulfonyl)-N-methylamino]-3,(2R,3S,4R,5R,8R,10R,11R,12S,13S,14R)-2-Ethyl-3,4,4,6-trideoxy-β-D-xylo-hexopyranosyl]oxy]-1-oxa-6-azacyclopentadecan-15-10,13-tetrahydroxy-3,5,6,8,10,12,14-heptamethyl-11 one.-[[3,4,6-trideoxy-3-dimethylamino-β-D-xylo-hexopyra-l(2R,3R,4S,5R,8R,10R,11R,12S,13S,14R)-13-[(2,6-Dideoxy-3-C-methyl-3-O-nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one. methyl-α-L-ribo-hexopyranosyl)oxy]-2-ethyl-4,10-dihydroxy-3,5,6,8,10,12,14-heptamethyl-11-[[3,4,6-trideoxy-3-(dimethylamino)-β-D-xylo-hexopyra-C30H58N2O9590.79nosyl]oxy]-1-oxa-6-azacyclopentadecan-15-one.Suitability requirementsResolution: NLT 2.0 between aztreonam and aztre-Aztreonamonam E -isomer, System suitability solutionTailing factor: NMT 2 for aztreonam, System suitabil-ity solutionRelative standard deviation: NMT 2.0%, Standard solution AnalysisSamples: Standard solution and Sample solutionCalculate the percentage of aztreonam (C 13H 17N 5O 8S 2)in the portion of Aztreonam taken:Result = (r U /r S ) × (C S /C U ) × P × F × 100C 13H 17N 5O 8S 2435.43r U = peak response from the Sample solution Propanoic acid, 2-[[[1-(2-amino-4-thiazolyl)-2-[(2-methyl-r S = peak response from the Standard solution 4-oxo-1-sulfo-3-azetidinyl)amino]-2-oxoethylidene]ami-C S= concentration of USP Aztreonam RS in theno]oxy]-2-methyl-, [2S -[2α,3β(Z )]]-;Standard solution (mg/mL)(Z )-2-[[[(2-Amino-4-thiazolyl)[[(2S ,3S )-2-methyl-4-oxo-C U = concentration of Aztreonam in the Sample1-sulfo-3-azetidinyl]carbamoyl]methylene]amino]oxy]-solution (mg/mL)2-methylpropionic acid [78110-38-0].P = potency of USP Aztreonam RS (µg/mg)F = unit conversion factor, 0.001mg/µgDEFINITIONAcceptance criteria: 92.0%–105.0% on the anhydrous Aztreonam, which may be anhydrous or hydrated, contains and solvent-free basisNLT 92.0% and NMT 105.0% of C 13H 17N 5O 8S 2, calculated on the anhydrous and solvent-free basis.IMPURITIESInorganic ImpuritiesIDENTIFICATION•R ESIDUE ON I GNITION 〈281〉: NMT 0.1%, the charred resi-•I NFRARED A BSORPTION 〈197K 〉: If a difference appears in due being moistened with 2mL of nitric acid and the IR spectra of the analyte and the standard, dissolve 5drops of sulfuric acidequal portions of the test specimen and the reference standard in equal volumes of methanol. [N OTE —To achieve a complete dissolution, it is suggested to use Delete the following:about 25mL of methanol for each 50mg of material,and stir the mixture for 40 min at room temperature.]••H EAVY M ETALS , Method II 〈231〉: NMT 30ppm •(Official 1-Evaporate the solutions to dryness under vacuum, and Jan-2018)dry at 40° for 4 h under vacuum. Perform the test on Organic Impurities the residues.•P ROCEDURE[N OTE —Store the System suitability solution , Standard so-ASSAYlution , and Sample solution at 5°, and protect from light •P ROCEDUREto prevent isomerization of aztreonam Z -isomer to az-[N OTE —Store the System suitability solution , Standard so-treonam E -isomer.]lution , and Sample solution at 5°, and protect from light Mobile phase, System suitability solution, Standard to prevent isomerization of aztreonam Z -isomer to az-solution, Sample solution, Chromatographic system,treonam E -isomer.]and System suitability: Proceed as directed in the Buffer: 6.8mg/mL of monobasic potassium phosphate Assay .in water. Adjust with 1M phosphoric acid to a pH of Analysis3.0.Samples: Standard solution and Sample solutionMobile phase: Methanol and Buffer (1:4)Calculate the percentage of each impurity in the por-System suitability solution: 1mg/mL of USP Aztre-tion of Aztreonam taken:onam RS and 1mg/mL of USP Aztreonam E -Isomer RS in Mobile phaseResult = (r U /r S ) × (C S /C U ) × P × F × 100Standard solution: 1mg/mL of USP Aztreonam RS in Mobile phaser U= peak response of each impurity from theSample solution: 1mg/mL of Aztreonam in Mobile Sample solutionphaser S = peak response of aztreonam from the StandardChromatographic systemsolution(See Chromatography 〈621〉, System Suitability .)C S = concentration of USP Aztreonam RS in theMode: LCStandard solution (mg/mL)Detector: UV 254 nmC U = concentration of Aztreonam in the SampleColumn: 3.9-mm × 30-cm; 10-µm packing L1solution (mg/mL)Flow rate: 1.5mL/min P = potency of USP Aztreonam RS (µg/mg)Injection size: 10µL F = unit conversion factor, 0.001mg/µg System suitabilityAcceptance criteriaSamples: System suitability solution and Standard Individual impurities: See Table 1.solution[N OTE —The relative retention times for aztreonam and aztreonam E -isomer are 1.0 and 1.8, respectively.]。

ACCA历年试卷-fr-2018-sepdec-sample-真题

ACCA历年试卷-fr-2018-sepdec-sample-真题Applied SkillsFinancial Reporting (FR)September/December 2018 – Sample QuestionsTime allowed: 3 hours 15 minutesThis question paper is divided into three sections:Section A – A LL 15 questions are compulsory and MUST be attempted Section B – A LL 15 questions are compulsory and MUST be attempted Section C – B OTH questions are compulsory and MUST be attemptedDo NOT open this question paper until instructed by the supervisor. Do NOT record any of your answers on the question paper.This question paper must not be removed from the examination hall.F RThe Association ofChartered CertifiedAccountantsFR ACCASection C – BOTH questions are compulsory and MUST be attemptedPlease write your answers to all parts of these questions on the lined pages within the Candidate Answer Booklet.31Duke Co is a retailer with stores in numerous city centres. On 1 January 20X8, Duke Co acquired 80% of the equity share capital of Smooth Co, a service company specialising in training and recruitment. This was the first time Duke Co had acquired a subsidiary.The consideration for Smooth Co consisted of a cash element and the issue of some shares in Duke Co to the previous owners of Smooth Co.Duke Co has begun to consolidate Smooth Co into its financial statements, but has yet to calculate the non-controlling interest and retained earnings. Details of the relevant information is provided in notes (i) and (ii).Extracts from the financial statements for the Duke group for the year ended 30 June 20X8 and Duke Co for the year ended 30 June 20X7 are provided below:Duke Group Duke Co30 June 20X8 30 June 20X7$’000 $’000Profit from operations 14,500 12,700Current assets 30,400 28,750Share capital 11,000 8,000Share premium 6,000 2,000Retained earnings Note (i) and (ii) 9,400Non-controlling interest Note (i) and (ii) NilLong-term loans 11,500 7,000Current liabilities 21,300 15,600The following notes are relevant:(i) The fair value of the non-controlling interest in Smooth Co at 1 January 20X8 was deemed to be $3·4m. Theretained earnings of Duke Co in its individual financial statements at 30 June 20X8 are $13·2m.Smooth Co made a profit for the year ended 30 June 20X8 of $7m. Duke Co incurred professional fees of $0·5m during the acquisition, which have been capitalised as an asset in the consolidated financial statements.(ii) The following issues are also relevant to the calculation of non-controlling interest and retained earnings:– At acquisition, Smooth Co’s net assets were equal to their carrying amount with the exception of a brand name which had a fair value of $3m but was not recognised in Smooth Co’s individual financial statements.It is estimated that the brand had a five-year life at 1 January 20X8.– On 30 June 20X8, Smooth Co sold land to Duke Co for $4m when it had a carrying amount of $2·5m.(iii) Smooth Co is based in the service industry and a significant part of its business comes from three large, profitable contracts with entities which are both well-established and financially stable.(iv) Duke Co did not borrow additional funds during the current year and has never used a bank overdraft facility.(v) The following ratios have been correctly calculated based on the above financial statements:20X8 20X7Receivables collection period 52 days 34 daysInventory holding period 41 days 67 daysOther than the recognition of the non-controlling interest and retained earnings, no adjustment is required to any of the other figures in the draft financial statements. All items are deemed to accrue evenly across the year.Required:(a) Calculate the non-controlling interest and retained earnings to be included in the consolidated financialstatements at 30 June 20X8.(6 marks)(b) Based on your answer to part (a) and the financial statements provided, calculate the following ratios for theyears ending 30 June 20X7 and 30 June 20X8:ratio;CurrentReturn on capital employed;Gearing(debt/equity).(4 marks)(c) Using the information provided and the ratios calculated above, comment on the comparative performanceand position for the two years ended 30 June 20X7 and 20X8.Note: Your answer should specifically comment on the impact of the acquisition of Smooth Co on your analysis.(10 marks) (20 marks)32The following extracts from the trial balance have been taken from the accounting records of Duggan Co as at 30 June 20X8:$’000 $’000Convertible loan notes (note (iv)) 5,000Cost of sales 21,700Finance costs (note (iv)) 1,240Investment income 120Operating expenses (notes (ii) and (v)) 13,520Retained earnings at 1 July 20X7 35,400Revenue (note (i)) 43,200Equity share capital ($1 shares) at 1 July 20X7 12,200T ax (note (iii)) 130The following notes are relevant:(i) Duggan Co entered into a contract where the performance obligation is satisfied over time. The total price on the contract is $9m, with total expected costs of $5m.Progress towards completion was measured at 50% at 30 June 20X7 and 80% on 30 June 20X8.The correct entries were made in the year ended 30 June 20X7, but no entries have been made for the year ended30 June 20X8.(ii) On 1 January 20X8, Duggan Co was notified that an ex-employee had started court proceedings against them for unfair dismissal. Legal advice was that there was an 80% chance that Duggan Co would lose the case and would need to pay an estimated $1·012m on 1 January 20X9.Based on this advice, Duggan Co recorded a provision of $800k on 1 January 20X8, and has made no further adjustments. The provision was recorded in operating expenses.Duggan Co has a cost of capital of 10% per annum and the discount factor at 10% for one year is 0·9091.(iii) The balance relating to tax in the trial balance relates to the under/over provision from the prior period. The tax estimate for the year ended 30 June 20X8 is $2·1m.In addition to this, there has been a decrease in taxable temporary differences of $2m in the year. Duggan Co pays tax at 25% and movements in deferred tax are to be taken to the statement of profit or loss.(iv) Duggan Co issued $5m 6% convertible loan notes on 1 July 20X7. Interest is payable annually in arrears. These bonds can be converted into one share for every $2 on 30 June 20X9. Similar loan notes, without conversion rights, incur interest at 8%. Duggan Co recorded the full amount in liabilities and has recorded the annual payment made on 30 June 20X8 of $0·3m in finance costs.Relevant discount rates are as follows:Present value of $1 in: 6% 8%year 0·943 0·9261years 0·890 0·8572(v) Duggan Co began the construction of an item of property on 1 July 20X7 which was completed on 31 March 20X8. A cost of $32m was capitalised. This included $2·56m, being a full 12 months’ interest on a $25·6m 10% loan taken out specifically for this construction. On completion, the property has a useful life of 20 years.Duggan Co also recorded $0·4m in operating expenses, representing depreciation on the asset for the period from31 March 20X8 to 30 June 20X8.(vi) It has been discovered that the previous financial controller of Duggan Co engaged in fraudulent financial reporting. Currently, $2·5m of trade receivables has been deemed to not exist and requires to be written off. Of this, $0·9m relates to the year ended 30 June 20X8, with $1·6m relating to earlier periods.(vii) On 1 November 20X7, Duggan Co issued 1·5 million shares at their full market price of $2·20. The proceeds were credited to a suspense account.Required:(a) Prepare a statement of profit or loss for Duggan Co for the year ended 30 June 20X8.(12 marks)(b) Prepare a statement of changes in equity for Duggan Co for the year ended 30 June 20X8.(5 marks)(c) Calculate the basic earnings per share for Duggan Co for the year ended 30 June 20X8.(3 marks)Note: All workings should be done to the nearest $’000.(20 marks)End of Question Paper。

14-雅培保护伞

保护伞导丝

导丝:

– BHW导丝平台, 3 cm的可视头端,可根据需要进行塑形 – 导丝头端为渐细镍钛合金内芯,导丝主体为不锈钢 – .014” 系统 – 190 cm 和300 cm 两种规格

– 可与Doc® 延长导丝相连接

AP2929161 Rev. A 3/09

Company Confidential © 2009 Abbott Laboratories

RX Accunet® 栓子保护装置

输送系统准备

AP2929161 Rev. A 3/09

Company Confidential © 2009 Abbott Laboratories

18

See Important Safety Information referenced within

辅助材料

• 8F 导引导管或 6F 导引鞘

– 最小内径= 0.085” / 2.2 mm

• .096” (2.44 mm) 旋转止血阀 • RX Acculink® 颈动脉支架系统和RX Accunet™ 栓子保护装置

• 球囊扩张导管

• 1,000 u/ 500 cc肝素生理盐水(无菌) • 10-20 cc 注射器 • Doc® 延长导丝

设计特点

AP2929161 Rev. A 3/09

Company Confidential © 2009 Abbott Laboratories

6

See Important Safety Information referenced within

最佳的栓子捕获能力 释放在迂曲血管

• 良好的柔顺性适应于各种复杂 的血管病变

12

See Important Safety Information referenced within

2015年ACCA考试模拟强化练习题(2)

2015年ACCA考试模拟强化练习题(2)1 Bravado,a public limited company,has acquired two subsidiaries and an associate. The draft statements of financial position are as follows at 31 May 2009:Bravado Message Mixted$m $m $mAssets:Non-current assetsProperty,plant and equipment 265 230 161Investments in subsidiariesMessage 300Mixted 128Investment in associate - Clarity 20Available-for-sale financial assets 51 6 5- - -764 236 166- - -Current assets:Inventories 135 55 73Trade receivables 91 45 32Cash and cash equivalents 102 100 8- - -328 200 113- - -Total assets 1,092 436 279- - -Equity and liabilities:Share capital 520 220 100Retained earnings 240 150 80Other components of equity 12 4 7- - -Total equity 772 374 187On 1 June 2007,Bravado acquired 6% of the ordinary shares of Mixted. Bravado had treated this investment as available-for-sale in the financial statements to 31 May 2008 but had restated the investment at cost on Mixted becoming a subsidiary. On 1 June 2008,Bravado acquired a further 64% of the ordinary shares of Mixted and gained control of the company. The consideration for the acquisitions was asfollows:Holding Consideration$m1 June 2007 6% 101 June 2008 64% 118- -70% 128- -Under the purchase agreement of 1 June 2008,Bravado is required to pay the former shareholders 30% of the profits of Mixted on 31 May 2010 for each of the financial years to 31 May 2009 and 31 May 2010. The fair value of this arrangement was estimated at $12 million at 1 June 2008 and at 31 May 2009 this value had not changed. This amount has not been included in the financial statements.At 1 June 2008,the fair value of the equity interest in Mixted held by Bravado before the business combination was $15 million and the fair value of the non-controlling interest in Mixted was $53 million. The fair value of the identifiable net assets at 1 June 2008 of Mixted was $170 million (excluding deferred tax assets and liabilities),and the retained earnings and other components of equity were $55 million and $7million respectively. There had been no new issue of share capital by Mixted since the date of acquisition and the excess of the fair value of the net assets is due to an increase in the value of property,plant and equipment (PPE)。

ACCA F1-F3模拟题及解析(5)

第1章 ACCA F1-F3模拟题及解析(5)1.A company's trial balance failed to agree, and a suspense account was opened for the difference. Subsequent checking revealed that discounts allowed of $13,000 had been credited to the discountsreceived account and an entry on the credit side of the cash book for the purchase of some machinerycosting $18,000 had not been posted to the plant and machinery account.Which two of the following journal entries would correct the errors?Debit Credit$ $1.Discounts allowed 13,000Discounts received 13,0002 Discounts allowed 13,000Discounts received 13,000Suspense account 26,0003 Suspense account 26,000Discounts allowed 13,000Discounts received 13,0004 Plant and machinery 18,000Suspense account 18,0005 Suspense account 18,000Plant and machinery 18,000A. 1 and4B. 2 and 5C. 2 and4D. 3 and52.A non-current asset was disposed of for $2,200 during the last accounting year. It had been purchased exactly three years earlier for $5,000, with an expected residual value of $500, andhad been depreciated on the reducing balance basis, at 20% per annum.The gain or loss on disposal was:A. $360 lossB. $150 lossC. $104 lossD. $200 profit3. Extracts from the accounting records of A, a company, relating to the year ended 31 December20X7 are as follows:Revaluation surplus $230,000Ordinary interim dividend paid $12,000Profit before tax $178,000Estimated tax liability for year $45,0008% £1 Preference shares $100,000Underprovision for tax in previous year $5,600Proceeds of issue of 2,000 £1 ordinaryShares $5,000Final ordinary dividend proposed after year end $30,000What is the total change reported in the statement of changes in equity for the year?A $312,400B $356,000C $348,000D $342,4004.ABC is engaged in the following research and development projects:Project 1 It is applying a new technology to the production of heat resistant fabric. The projectis intended to last for a further 18 months after which the fabric will be used in the productionof uniforms for the emergency services.Project 2 It is considering whether a particular substance can be used as an appetite suppressant.If this is the case, it is expected be sold worldwide in chemists and pharmacies.Project 3 It is developing a material for use in kitchens which is self cleaning and germ resistant.A competitor is currently developing a similar material and for this reason Geranium are unsure whether their project will be completed.The costs associated with which of these projects can be capitalised?A. Projects 1, 2 and 3B. Projects 1 and 2C. Project 1 onlyD. Projects 1 and 35.You are given the following incomplete and incorrect extract from the income statement of a company that trades at a mark up of 25% on cost:$ $Sales 174,258Less: cost of goods soldOpening inventory 12,274Purchases 136,527Closing inventory X(X)Gross profit XHaving discovered that the sales figure should have been $174,825andthat purchase returnsof$1,084and sales returnsof$1,146 have been omitted, the closing inventory should be:A. $8,662B. $8,774C. $17,349D. $17,4586. At I October 20X6, O's capital was structured as follows:$Ordinary shares of 25c 100,000Share premium 30,000On 10 January 20X7, in order to raise finance for expansion, there was a 1 for 4 rights issue at $1.15. The issue was fully taken up. This was followed by a 1 for 10 bonus issue on 1 June 20X7.What is the balance on the share premium account after these transactions?A. $17,500B. $21,250C. $107,500D. $120,0007. Jason performs an inventory count on 30 December 20X6 ahead of the 31 December year end. He counts 1,200 identical units, each of which cost $50. On 31 December, David sold 20 of the units for $48 each. What figure should be included in Jason's balance sheet for inventory at the year end?A. $60,000B. $59,000C. $57,600D. $56,6408. The following bank reconciliation statement has been prepared by an inexperienced bookkeeper at 31 December 20X5:$Balance per bank statement (overdrawn) 38,64019,270Add: lodgments not credited57,910Less: unpresented cheques14,260Balance per cash book 43,650What should the final cash book balance be when all the above items have been properly dealt with?A. $43,650 overdrawnB. $33,630 overdrawnC. $5,110 overdrawnD. $72,170 overdrawn9. Classify the following amounts as current or non-current in Albatross, a limited liability company's accounts:1. A sale has been made on credit to a customer. They have agreed to terms stating that payment is due in 18 months time.2. A bank overdraft facility of $30,000 is available under an agreement with the bank which extends 2 years.3. A company has bought a small number of shares in another company which it intends to trade.4. A bank loan has been taken out with a repayment date 5 years hence.Current Non-currentA 2 and3 1 and 4B 3 only 1,2 and 4C 1,2 and 3 4D 1 and 3 2 and 410. The following items have to be considered in finalising the financial statements of Q, a limited liability company:1.The company gives warranties on its products. The company's statistics show that about 5% of sales give rise to a warranty claim.2.The company has guaranteed the overdraft of another company. The likelihood of a liability arising under the guarantee is assessed as possible.What is the correct action to be taken in the financial statements for these items?Create a Disclose by note No actionprovision onlyA 1 2B 1 2C 1 and 2D 1 and 211. Which of the following statements are correct according to IAS 10 Events after the balance sheet date?1 Details of all adjusting events must be disclosed by note to the financial statements.2 A material loss arising from the sale, after the balance sheet date, of inventory valued at cost at the balance sheet date must be reflected in the financial statements.3 If the market value of investments falls materially after the balance sheet date, the details must be disclosed by note.4 Events after the balance sheet date are those that occur between the balance sheet date and the date when the financial statements are authorised for issue.A. l and 2 onlyB. 1,3 and 4C. 2 and 3 onlyD. 2,3 and 412.A credit entry of $450 on X's account in the books of Y could have arisen by:A.X buying goods on credit from YB.Y paying X $450C.Y returning goods to XD. X returning goods to Y.13.Inventories should be valued at the lower of cost and net realisable value. Which ONE of the following accounting concepts governs this?A. ComparabilityB. PrudenceC. Going concernD. Materiality14.ABC, a leasing apartment company, received cash totaling $838,600 from tenants during the year ended 31 December 20X6.Figures for rent in advance and in arrears at the beginning and end of the year were:31 December 20X5 31 December 20X6$ $Rent received in advance 102,600 88,700Rent in arrears (all subsequently received) 42,300 48,400What amount should appear in the company's income statement for the year ended 31 December 20X6 for rental income?A. $818,600B. $738,000C. $939,200D. $858,60015. Which of the following items could appear as items in a company's cash flow statement?1 A bonus issue of shares2 A rights issue of shares3 The revaluation of non-current assets4 Dividends paidA.All four itemsB. 1,3 and 4 onlyC. 2 and 4 onlyD. 2 and 3 only16. The Standards Advisory Council are responsible for:(1) issuing guidance in relation to emerging issues(2) advising the IASB on major standard-setting projectsA. 1 and2B. 1 onlyC. 2 onlyD. neither 1 nor two17. The trial balance of MHSB does not balance at the year end. What type of error may explain this?A. Extraction errorB. Error of commissionC. Compensating errorD. Error of original entry18. Ellen is registered for sales tax. During May, she sells goods with a tax exclusive price of $600 to Kyle on credit. As Kyle is buying a large quantity of goods, Erin reduces the price by 5%. She also offers a discount of another 3% if Kyle pays within 10 days. Kyle does not pay within the 10 days.If sales tax is charged at 17.5%, what amount should Ellen charge on this transaction?A. $96.60B. $101.85C. $99.75D. $105.0019. Which of the following statements is true?1. In a computerised system, all accounting personnel will have access to all records.2. The general ledger in a computerised system tends to take the same format as that in a manual system, i.e. a number of T accounts.A. Neither 1 nor 2B. Both 1 and 2C. 1 onlyD. 2 only20. Details of AIG's insurance policy are shown below:Premium for year ended 31 March 20X6 paid April 20X5. $10,800Premium for year ending 31 March 20X7 paid April 20X6 $12,000What figures should be included in the company's financial statements for the year ended 30 June 20X6?Income Statement Balance sheet$ $A. 11,100 9,000 prepaymentB. 11,700 9,000 prepaymentC. 11,100 9,000 accrual.D. 11,700 9,000 accrual21. A business' sales (receivables) ledger control account did not agree with the total of the balances on the receivables ledger. An investigation revealed that the sales day book had been overcast by $10. What effect will this have on the discrepancy?A. the control account should be credited with $10B. the control account should be debited with $10C. the ledger total should be decreased by $10D. the ledger total should be increased by $1022. A company's trial balance failed to agree, and a suspense account was opened for the difference. Subsequent checking revealed that discounts allowed of $13,000 had been credited to the discounts received account and an entry on the credit side of the cash book for the purchase of some machinery costing $18,000 had not been posted to the plant and machinery account.Which two of the following journal entries would correct the errors?Debit Credit$ $1 Discounts allowed 13,000Discounts received 13,0006 Discounts allowed 13,000Discounts received 13,000Suspense account 26,0007 Suspense account 26,000Discounts allowed 13,000Discounts received 13,0008 Plant and machinery 18,000Suspense account 18,0009 Suspense account 18,000Plant and machinery 18,000A. 1 and4B. 2 and 5C. 2 and4D. 3 and523. Which one of the following statements is correct?A. The prudence concept requires assets to be understated and liabilities to be overstated.B. To comply with the law, the legal form of a transaction must always be reflected in financial statements.C. If a non-current asset initially recognised at cost is revalued, the surplus must be credited in the income statement.D. In times of rising prices, the use of historical cost accounting tends to understate assets and overstate profits.24. A sales ledger control account showed a debit balance of $37,642. The individual customers' accounts in the sales ledger showed a total of $35,840. The difference could be due to:A. undercasting the sales day book by $1,802B. overcasting the sales returns day book by $1,802C. entering a cash receipt of $1,802 on the debit side of a customer's accountD. entering a cash discount allowed of $901 on the debit side of the control account.25. Where, in a company's financial statements complying with International accounting standards,should you find the proceeds of non-current assets sold during the period?A. Cash flow statement and balance sheetB. Statement of changes in equity and balance sheetC. Income statement and cash flow statementD. Cash flow statement only26. Which one of the following should be accounted for as capital expenditure?A. The cost of painting a building.B. The replacement of windows in a building.C. The purchase of a car by a garage for re-sale.D. Legal fees incurred on the purchase of a building.27. Lee and Ham are in partnership, trading as 'Furniture'. They have made a profit of $14,750 in the year ended 31 May 20X5.The partnership agreement provides for a salary of $12,000 to Lee and interest on capital at 3%. Remaining profits are shared in the ratio 1:4 At the start of the year, Lee had invested $10,000 in the business and Ham $20,000.What share of profit does Ham receive?A. $370B. $1,480C. $2,080D. $12,67028. The sales account is:A. credited with the total of sales made, including sales taxB. credited with the total of sales made, excluding sales taxC. debited with the total of sales made, including sales taxD. debited with the total of sales made, excluding sales tax.29.Inventory movements for product X during the last quarter were as follows:January Purchases 10 items at$19.80 eachFebruary Sales 10items at $30 eachMarch Purchases 20items at $24.50Sales 5 items at$30 eachOpening inventory at 1 January was 6 items valued at $15 each.Gross profit for the quarter, using the continuous weighted average cost method would be:A. $135.75B. $155.00C. $174.00D. $483.0030.The following information is available about a company's dividends:Sept 20X5 Final dividend for the year ended 30 June 20X5 paid $100,000(declared August 20X5)March 20X6 Interim dividend for the year ended 30 June 20X6 $40,000paidSept 20X6 Final dividend for the year ended 30 June 20X6 paid $120,000 (declared August 20X6)What figures, if any, should be disclosed in the company's income statement for the year ended 30 June 20X6 and its balance sheet at that date?Income statement Balance sheetA.$160,000 deduction $120,000B.$140,000 deduction NilC.Nil $120,000D.Nil Nil试题答案1.【答案】C2.【答案】A3.【答案】D4.【答案】C5.【答案】B6:【答案】C7:【答案】D8.【答案】B9.【答案】C10.【答案】A11 【答案】D12.【答案】D13.【答案】B14.【答案】D15.【答案】C16.【答案】C17.【答案】A18.【答案】A19.【答案】A20.【答案】A21.【答案】A22.【答案】C23.【答案】D24.【答案】D25.【答案】D26.【答案】D27.【答案】C28.【答案】B29.【答案】B30.【答案】略财经网络教育领导品牌_________________________________________________________________ 参与ACCA考试的考生可按照复习计划有效进行,另外高顿网校官网ACCA考试辅导高清课程已经开通,还可索取ACCA考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升复习备考效果。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

MODULE E PROFESSIONAL EXAMINATION 2 PAPER 13 - FINANCIAL ACCOUNTING 3

MONDAY 23rd NOVEMBER 2015 Time allowed - 3 hours SECTION A This question is compulsory

SECTION B Any THREE questions to be answered

(FOUR questions in all) Clear workings should be submitted with all your answers. All calculations should be made to the nearest $ (or $000) as appropriate.

You are allowed an additional 15 minutes reading time before the exam begins, during which you should read the question paper and, if you wish, make notes on the question paper. You are not allowed to open the exam script booklet and start writing or use your calculator during the reading time. 1

SECTION A Question ONE is compulsory and must be attempted

1. Stream is a public limited company and operates in a number of countries. The group’s main activity involves the manufacture of consumer goods. The following statements of comprehensive income for the year ended 31 October 2015 relate to the Stream Group:

Stream Rill Wadi $m $m $m Revenue 508 146 90

Cost of sales 396 83 46

Gross profit 112 63 44 Other income 27 9 2 Administrative costs (19) (11) (16) Finance costs (6) (8) (6) Other costs (44) (24) (10) ___ ___ ___ Profit before tax 70 29 14

Income tax expense (24) ___ (11) ___ (6) ___ PROFIT FOR THE YEAR 46 18 8

Other comprehensive income: Items that will not be reclassified to profit or loss (net of tax) Surplus on revaluation of property, plant and equipment Investments in equity instruments 13 7 ___ ___

__ Other comprehensive income for the year, net of tax 20 __-_ _-_

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 66 18 8

The following information is relevant to the preparation of the Stream Group’s statement of comprehensive income:

(i) Stream acquired 70% of the equity interests of Rill, a public limited company, on 1 November 2013 for a cash consideration of $99 million. At that date, the fair value of Rill’s identifiable net assets was $135 million and the fair value of the non-controlling interest in Rill was $57 million. For all acquisitions, it is group policy to measure non-controlling interests at fair value as at the date of acquisition. Stream entered into an arrangement with Rill before the acquisition that required Rill to restructure its manufacturing activities. The restructuring plan became effective upon the change in control. The fair value of Rill’s identifiable net assets included a liability of $5 million in connection with this plan.

The carrying value of Rill’s identifiable net asset as at the date of acquisition was $121 million. The excess of fair value over carrying value at that date was due to a parcel of land held for long-term capital appreciation.

Stream carried out an impairment test on goodwill on 31 October 2014 and found that the asset’s value had been reduced by 25%. However, due to an improvement in consumer confidence and thereby increases in the sale of goods and in asset values post recession, Stream calculated that the value of goodwill had increased by 50% over the year. Stream has included this increase in the above draft statement in ‘other income’. 2

(ii) On 31 October 2015, Stream disposed of 10% of the equity interests of Rill for a cash consideration of $20 million. The gain has been accounted for in the above statement in ‘other income’. Stream accounts for its investments in subsidiaries by electing to include gains and losses in other comprehensive income under IFRS9 Financial Instruments. The carrying value of the investment in Rill at 31 October 2014 was $80 million and had increased by $4 million before the disposal of the equity interest.

(iii) Stream gained control of Wadi, a public limited company, on 31 October 2013 when it acquired 55% of Wadi’s equity interests for a cash consideration of $89 million. At that date, the fair values of Wadi’s identifiable net assets and non-controlling interests were $109 million and $36 million respectively. Acquisition fees of $5 million were capitalised by Stream.

On 1 May 2015, Stream disposed of 36% of Wadi’s equity interest for a cash consideration of $64 million. Stream retained its representation on Wadi’s board of directors, provides Wadi with essential technological information and participates in Wadi’s policy-making processes. At the date of disposal, the fair value of Wadi’s identifiable net assets and non-controlling interests were $114 million and $43 million respectively. The fair value of the remaining equity interest in Wadi was $51 million. No entries have been made in the above financial statements concerning these transactions.