Accounting English(part2)

会计英语 Accounting English

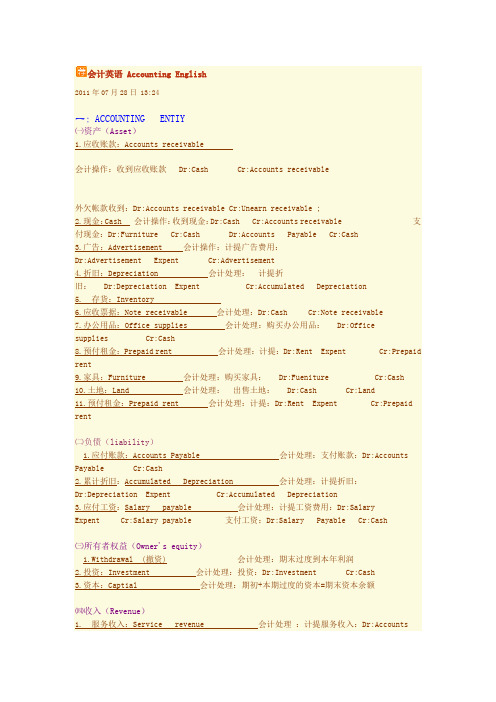

会计英语 Accounting English2011年07月28日 13:24一:ACCOUNTING ENTIY㈠资产(Asset)1.应收账款:Accounts receivable会计操作:收到应收账款 Dr:Cash Cr:Accounts receivable外欠帐款收到:Dr:Accounts receivable Cr:Unearn receivable ;2.现金:Cash 会计操作:收到现金:Dr:Cash Cr:Accounts receivable 支付现金:Dr:Furniture Cr:Cash Dr:Accounts Payable Cr:Cash3.广告:Advertisement 会计操作:计提广告费用:Dr:Advertisement Expent Cr:Advertisement4.折旧:Depreciation 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation5. 存货:Inventory6.应收票据:Note receivable 会计处理:Dr:Cash Cr:Note receivable7.办公用品:Office supplies 会计处理:购买办公用品: Dr:Officesupplies Cr:Cash8.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent9.家具:Furniture 会计处理:购买家具: Dr:Fueniture Cr:Cash10.土地:Land 会计处理:出售土地: Dr:Cash Cr:Land11.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent㈡负债(liability)1.应付账款:Accounts Payable 会计处理:支付账款:Dr:AccountsPayable Cr:Cash2.累计折旧:Accumulated Depreciation 会计处理:计提折旧:Dr:Depreciation Expent Cr:Accumulated Depreciation3.应付工资:Salary payable 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable 支付工资:Dr:Salary Payable Cr:Cash㈢所有者权益(Owner's equity)1.Withdrawal (撤资) 会计处理:期末过度到本年利润2.投资:Investment 会计处理:投资:Dr:Investment Cr:Cash3.资本:Captial 会计处理:期初+本期过度的资本=期末资本余额㈣收入(Revenue)1. 服务收入:Service revenue 会计处理:计提服务收入:Dr:Accountsreceivable Cr:Service renenue收到:Dr:Cash Cr:Accounts receivable Dr:Unearned Servicerenenue Cr:Service renenue2.保险收入:Commission revenue 会计处理:计提:Dr:Unearned commission revenue Cr:Commission revenue3.销售收入:Sales revenue 会计处理:现金收到:Dr:Cash Cr:Sales revenue销售收入赊账处理:Dr:Accounts receivable Cr:Sales revenue㈤费用(Expent)1.公用事业费用:Utilities Expent2.租金费用:Rent Expent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent3.工资费用:Salary Expent 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable4.办公费用:Supplies Expend 会计处理:计提:Dr:Supplies Expent Cr:Supplies5.折旧费用:Depreciation Expent 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation㈥过户:Dr:Income Summary Cr:费用类科目Dr:收入类科目 Cr:Income SummaryDr:Withdrawal Cr:Income SummaryDr:Income Summary Cr:Captial二:THE ACCOUNTING CYCLEA→→→→→→→→→↓↓Transaction source document→Joural→Ledger→Worksheet→Finacial statementsB→→→Closing→→→→↓↓Analyzing→Recording→Posting→Adjusting→Preparing三:存货(Inventory)---会计处理1.购买存货:Dr:Purchase Cr:Cash OR Accounts Payable2.购货折扣与退回折让:Dr:Accounts Payable Cr:CashPurchase DiscountsPurchase returns and allowances3.Purchase(Dr) ---Purchase Discounts(Cr)---Purchase returnsand allowances(Cr) =Net purchase(Dr)4.运输成本:Dr:Freight In Cr :Cash5.销售折扣与销售折让、退回:Dr:Sales DiscountSales Returnsand allowancesCr:Accounts receivable6.Sales revenue (Cr) ---Sales Discount (Dr)--- Sales Returnsand allowances(Dr)=Net Sales (Cr)7.Beginning inventory(Dr)+Net purchase(Dr)+Freight In =Cost of inventory ---Ending inventory=Cost of goods sold。

会计英语UnitTwo

►2 Attention: ►material means important enough to

influence the decisions of statement users. ► Large/ small/ differ significantly/ nature

十二 Substance over form

►

Assets: lowest

► Liabilities: highest

十一 Materiality convention

►1 Definition: record and report separately only those transactions which are material.

五 Objectivity convention

the accounting records and reports be base upon objectivity evidence.

六 Relevance

► if accounting information is to be of any use, it must be relevant for its intended use.

transactions from its own viewpoint. ►3 In other words, the business is viewed as

会计英语第2章

Objectives

1. Explain why accounts are used to record After studying this and summarize the effects of transactions chapter, you should on financial statements. be able to: 2. Describe the characteristics of an account. 3. List the rules of debit and credit and the normal balances of accounts. 4. Analyze and summarize the financial statement effects of transactions.

Each financial statement item, called an account, is included in the ledger.

A group of accounts for a business entity is called a ledger.

A list of the accounts in a ledger is called a chart of accounts.

Major Account Classifications

Owner’s equity is the owner’s right to the assets of the business. Revenues are increases in owner’s equity as a result of selling services or products. Expenses are the using up of assets or consuming of services to generate revenue.

Accounting English 15章加期末复习

External users: creditors 债权人,government

agencies 政府机构,customers ,顾客labor unions

工会, and competitors对手

❖ 1.4 Accounting Principles and Concepts

Generally Accepted Accounting

C5

Principles

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

❖ Common examples of expenses: office rent, salaries of employees, telephone services, many types of taxes.

Expanded Accounting

ties + Equity

"四不准":

❖ 1.不准旷课; ❖ 2.不准迟到或早退; ❖ 3.不准睡觉或玩手机(手机应设为静

音); ❖ 4.不准带早点到教室吃。

职业技能考试:

❖ 会计英语主要是要学生掌握会计术语的一些英 文说法和做法,主要是对西方会计的一些常规 了解,拓展学生的就业方向和渠道,以下考试 和会计课程直接挂钩:

( 3.2 和3.3 是重点)

Chapter 4 :financial statements(4.2是 重点)

chapter 5 : adjusting and closing procedures(5.1,5.2,5.5是重点)

会计英语2ppt课件

asset).

Adjusting Entry

Recognize portion

of asset consumed as

expense, and

Reduce balance of

asset account.

完整最新ppt

8

Entries to prepaid expenses…

Chapter 2-2

Accounting Cycle (Cont.)

完整最新ppt

1

• Before financial statements can be prepared, the accounts must be reviewed to ensure they reflect the correct balances; adjustments will be needed to adjust prepayments and unearned amounts, and to record amortization and accruals.

Cash basis accounting does not make adjustments; revenues are recorded when cash is received and expenses are recorded when cash is paid.

The cash basis of accounting is not generally accepted.

Jan. 1

Dec. 31

On January 1, Webb, Co. purchased a one-

year insurance policy for $2,400.

accountingenglish2 (2)PPT课件

2020/11/12

4

Learning Objectives

After studying this chapter, you should be able to:

1. Explain four major financial statements

2. Describe how to understand and use the balance sheet

Review of Chapter 3

Question 1. Is the following statement true or false?

Explain your answer.

Debit means decrease and credit means increase.

2020/11/12

1

Sheet

Point in time

2020/11/12

Period of time

Point in time

6

Financial statements are a central feature of accounting. They are the primary means of communicating important accounting information to users.

Four major financial statements are used to communicate the required information about a business.

2020/11/12

7

One is the balance sheet, which shows the financial position at either the beginning or the ending of the accounting period.

会计英语2

Words

Assume [ə'sju:m] / Assumption [ə'sʌmpʃn] To assume is to suppose or believe something is true

(sometimes wrongly) . It also means to take over, usually responsibilities and duties, such as with a job, or to take on a look or attitude。

Words

Liquidate['likwideit]: To liquidate a company is to close it down and sell all its assets, usually because it is in debt.

liquidation [ˌlikwi'deiʃn] The company closed down operations and began liquidating

April. p11

Words

Accrual basis p13/ Cash basis Cash basis is to recognize the

economic transactions once the entitiy receive the cash inflows or incur the cash outflows.

会计英语 Unit Two

►2

十四 Matching princiexpenses incurred in earning revenue should be recognized in the same period the revenue is recognized. ► 2 As a result, most matching is not directly to revenue, but is instead to time periods.

五 Objectivity convention

the accounting records and reports be base upon objectivity evidence.

六 Relevance

►

if accounting information is to be of any use, it must be relevant for its intended use.

►

十一 Materiality convention

►1

Definition: record and report separately only those transactions which are material.

►2

Attention: ► material means important enough to influence the decisions of statement users. ► Large/ small/ differ significantly/ nature

一 Accounting Entity convention

►1

Definition: ► the smallest unit of activity with a selfcontained accounting system. ► 2 Characteristic: ► each accounting entity interprets transactions from its own viewpoint. ► 3 In other words, the business is viewed as an entity separate from its owners, creditors, or other stakeholders.

会计英语(西方会计学)chapter2-accounting cycle

0.Adjustments

Adjustments

Paid (or received) cash before expense (or revenue) recognized Paid (or received) cash after expense (or revenue) recognized

Prepaid expenses

Dollar amount of debits and credits

2. Post to the Ledger

GENERAL JOURNAL

Date 2014 Dec. 1 Cash Description PR Debit 12,000 Amy. Schneider, Capital The investment of the owner Dec. 2 Supplies Cash 1 Identify the debit account Purchased store supplies for cash 2,500

Asset

Unadjusted Balance Credit Adjustment

Expense

Debit Adjustment

E.g.: On 1/1/2013, Amy’s enterprise paid $2,400 for insurance for 2-years. The enterprise recorded the expenditure as Prepaid Insurance on 1/31/2013. What adjustment is required?

T型账户

复式记账法

Part1: Introduction

分析经济事项

(调整事项)

大学课程《会计英语》PPT课件:Chapter 2 Unit 2

Events

Events refer to those happenings that affect an entity’s accounting equation and can be reliably measured.

Examples of events: changes in the market value of certain assets and liabilities, and natural events such as floods and fires that destroy assets and create losses.

Assets - Liabilities = Owners’ Equity

Owners’ Equity

Owners’ equity has two parts: contributed capital or invested capital and retained earnings.

Contributed capital refers to the amount that stockholders invest in the company.

式记账原理

Accounting is an Information system

The inputs of the accounting system are business transactions and events.

The transformation process is the set of rules and methods that accountants use to record, classify, and summarize the inputs.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Types of assets

Examples: Cash short term investment短期投资 (marketable securities有价证券) notes receivable 应收票据 accounts receivable 应收账款 Supplies 物料用品

Types of assets

Business entity concept

So far we have spoken of assets of a business. You may have wondered whether an intangible entity, such as a business, can own assets or have liabilities in its own name. There are two aspects to this question: the strict legal position and the convention adopted by accountants.

Answer 3

Investment --mortgage 抵押 notes receivables (due in 6 years) Plant Asset --store equipment --building ---furniture & fixtures ---office machine ---office equipment Intangible Asset ---goodwill 商誉 ---patents 专利

Answer 3

Current Asset ---Cash in bank --First National City Bonds ---accounts receivables --- notes receivables (due in 90 days) ---petty cash ---merchandise --factory supplies

More examples

Office furniture Cash

Question 2:

Test your ability to assign specific to various categories.

traveler’s check, tables, truck, computer, adding machine, lamp, pencils, type paper, chairs, stationery, wrapping paper, automobiles, coins, money in bank, desk blotters, light bulbs, desk, pens, currency, and showcases.

Notes receivable 应收票据

In some cases, promisory notes may be received from the credit customers in exchange for the merchandise soled or the serviced performed. A promisory note is a written promise to pay a certain sum of money on demand or at a fixed and determinable future time.

For example

Suppose that C sells goods on credit to D for $6,000 on terms that the debt must be settled within two months of the invoice date 1 October. If D does not pay the $6,000 until 30 November, D will be a debtor of C for $6,000 from 1 October until 30 November.

Accounts receivable 应收账款

Amounts owed by debtors are called trade accounts receivable, sometimes abbreviated to “accounts receivable” or “receivables”.

Accounting English (2)

College of Foreign Studies Jinan University

Accounting elements

Assets 资产 Liabilities 负债 Owner’s equity 所有者权益 Revenues 收入 Expenses 费用 Net earnings ( or Net loss) 净收益/净损

Question 3:

Place each of these assets in the appropriate column of the following form: Cash in bank, office equipment, First National City bonds, patents, accounts receivables, Office supplies, notes receivables (due in 90 days), building, office machines, furniture and fixtures, mortgage notes receivables (due in 6 years), store equipment, petty cash, good will, factory supplies, and merchandise. Current Asset Investment Plant Asset Intangible Asset

Notes receivable 应收票据

An interest bearing note is the note on which an annual interest rate is specified explicitly.

Determining the money value of assets Cost principle: The cost assigned to the asset includes not only the purchase price, but also transportation charges, installation charges, and any other costs associated with placing the asset into use by the organization. Business entity concept 企业实体概念 企业实体概念: The assets that the business owns are separate and apart from the assets that the owner may personally own.

Inventories 存货

Types of assets

Note: any money, regardless of its actual form, would be known and categorized as cash.

Types of assets

Non-current assets 固定资产 --long-term investment --those economic resources that are held for operational purposes 经营目的

Cash Furniture & Fixtures Delivery Equipment Office Supplies Office Equipment

Answer 2

Cash ---Traveler’s check, coins, money in bank, currency Furniture & Fixtures ---tables, chairs, desk, showcase Delivery Equipment -truck, automobile Office Supplies ---type paper, stationery, wrapping paper desk blotters, pens, pencils Office Equipment -type writer, adding machine, lamp, light bulbs

Types of assets

Examples: plant and equipment 厂房设备 natural resources 自然资源 intangible assets 无形资产

More examples

Factories Office buildings Warehouses Delivery vans Lorries Computer equipment

Accounting elements

A good understanding of these accounting elements will be a good start in learning financial accounting.

What Are Assets?

The economic resources that are owned or controlled by any business organization and can be expressed in monetary units are known as assets. Two requirements:

Business entity concept