投资协议条款清单

经典版投资协议条款范文5篇

经典版投资协议条款范文5篇篇1甲方(投资方):__________乙方(融资方):__________根据公平、平等、互利的原则,为明确甲乙双方的投资合作关系,确保双方的权利与义务,经充分协商,达成如下投资协议条款:一、投资概述1. 投资目的:用于乙方项目__________的开发与运营。

2. 投资金额:甲方投资总额为人民币______万元。

3. 投资方式:甲方以现金或银行转账方式支付投资款项。

二、投资条款1. 投资期限:本协议签订之日起至项目结束或双方协商确定的终止日期。

2. 利润分配:乙方按照项目盈利情况,向甲方分配利润,具体分配比例和方式另行约定。

3. 资金管理:投资款项应专款专用,乙方需设立专用账户,并向甲方提供详细的资金使用情况报告。

4. 股权结构:甲方投资后,在乙方公司持有的股权比例为____%,乙方应完成相应的股权变更手续。

三、项目运营与管理1. 乙方负责项目的日常运营与管理,应建立健全公司治理结构,确保项目顺利进行。

2. 重大决策:对于项目的重大决策,需经甲乙双方共同商议并达成一致意见。

3. 财务报告:乙方应定期向甲方提供财务报表及审计报告,确保财务透明。

4. 项目风险:双方应共同承担项目风险,具体风险分担比例根据项目投资比例确定。

四、合作期限与终止1. 合作期限:本协议自签订之日起生效,合作期限为_____年。

2. 终止事由:合作期限届满、双方协商一致或其他法定事由出现时,本协议终止。

3. 资产处置:合作终止时,应对项目资产进行清算,按照股权比例分配剩余资产。

五、违约责任1. 若任何一方违反本协议的约定,应承担违约责任,并赔偿对方因此造成的损失。

2. 若因违约导致本协议提前终止,违约方应承担违约责任并赔偿对方因此产生的损失。

六、争议解决1. 对于本协议的履行过程中产生的争议,甲乙双方应首先友好协商解决。

2. 协商不成的,任何一方均有权向有管辖权的人民法院提起诉讼。

七、其他条款1. 本协议未尽事宜,由甲乙双方另行协商补充。

投资条款清单模板范本

编号:_____________投资条款清单甲方:________________________________________________乙方:___________________________签订日期:_______年______月______日本清单旨在规定投资方与被投资方(目标公司)及目标公司的原股东有关投资事项的主要合同条款,其中“保密条款”、“排他性条款”、“费用分担”和“争议解决条款”一经签署即具有法律约束力。

本清单其他条款在投资方完成尽职调查并获得投资委员会批准,并以书面(包括电子邮件)通知目标公司后,便对各方具有法律约束力。

各方应尽最大努力根据本清单的规定达成、签署正式的投资协议。

正式签署的投资协议与本清单不一致的,以正式签署的投资协议为准。

原股东(甲方):甲方之一: (自然人)身份证号码:甲方之二: (法人)住所:营业执照注册号码:组织机构代码:法定代表人:投资方(乙方):乙方:住所:法定代表人:目标(标的)公司(丙方):营业执照注册号码:组织机构代码:住所:法定代表人:(以下“甲方之一”、“甲方之二”合称“甲方”,“甲方”、“乙方”合称“双方”,甲方、乙方、丙方合称“各方”)备注:(1)请根据投资项目的具体情况填写。

(2)若有优先股、可转换债券的按照具体项目再商谈具体条款。

(3)条款清单中有涉及“实际控制人”、“董监高”的投资项目,请根据具体项目的实际情况予以加列或者删除。

以下无正文签约各方:(签字盖章)原股东(甲方):甲方之一: (自然人)住所:身份证号码:联系电话:甲方之二: (法人)住所:法定代表人:职务:联系电话:传真:投资方(乙方):乙方:住所:法定代表人:职务:联系电话:委托代理人或授权代表:传真:目标(标的)公司(丙方):营业执照注册号码:组织机构代码:住所:法定代表人:职务:联系电话:传真:。

投资条款清单TERM

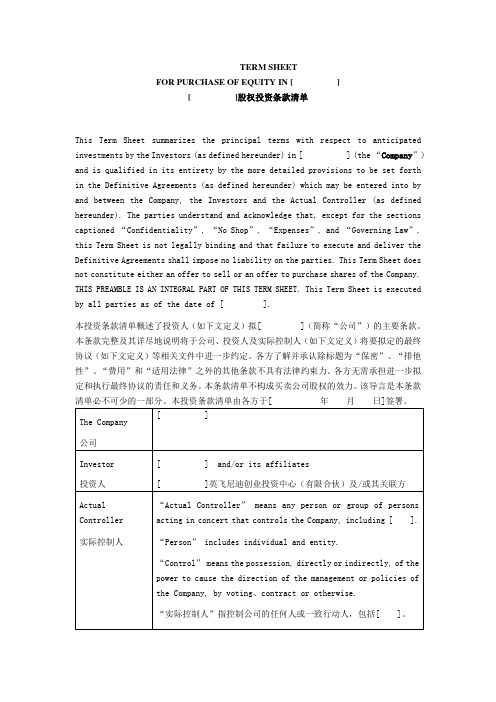

TERM SHEETFOR PURCHASE OF EQUITY IN [ ][ ]股权投资条款清单This Term Sheet summarizes the principal terms with respect to anticipated investments by the Investors (as defined hereunder) in [ ] (the “Company”) and is qualified in its entirety by the more detailed provisions to be set forth in the Definitive Agreements (as defined hereunder) which may be entered into by and between the Company, the Investors and the Actual Controller (as defined hereunder). The parties understand and acknowledge that, except for the sections captioned “Confidentiality”, “No Shop”, “Expenses”, and “Governing Law”, this Term Sheet is not legally binding and that failure to execute and deliver the Definitive Agreements shall impose no liability on the parties. This Term Sheet does not constitute either an offer to sell or an offer to purchase shares of the Company. THIS PREAMBLE IS AN INTEGRAL PART OF THIS TERM SHEET. This Term Sheet is executed by all parties as of the date of [ ].本投资条款清单概述了投资人(如下文定义)拟[ ](简称“公司”)的主要条款。

投资条款清单

投资条款清单投资人创始人【】年【】月【】日本投资条款清单(简称“本清单”)由xxxxxxxxxxxxxxxxxxxxxxx (有限合伙)(简称“投资人”)与【】(简称“创始人”)共同签署。

本清单总结了投资人拟投资【】公司的主要条款,仅为双方确认投资意向所用。

在双方确认并签署具有法律约束力的最终投资协议之前,除“保密”、“费 用”、“排他性”、“适用法律及争议解决”等条款中所述内容外,本清单其他条款对投资人、创始人均不具有法律约束力。

A. xxxxxxxxxxxxxxxxxxxxxxx (有限合伙)。

B. 【】。

【】是一家依据中华人民共和国法律依法设立并有效存续的有限责任公司,注册资本人民币【】万元,主营业务为【】。

公司设立完成后,投资人拟以溢价增资方式向公司投资。

公司投资后估值为人民币【】万元,投资人投资人民币【】万元(简称“投资款”),取得增资完成后公司【】%的股权(简称“本轮融资”)。

与公司主营业务【】有关的事项。

交割日为各方签署正式投资协议后,投资人向公司汇入投资款之日。

本轮融资完成后,公司股权结构如附表一所示。

本清单中投资人承担其投资义务,需取决于以下先决条件的实现:(i)投资人对尽职调查的结果满意; (ii) 最终的法律文件(包括但不限于投资协议、结合本轮融资修订和重述的公司章程、股东会决议等)令投资人满意;(iii) 公司已取得交易所必需的所有资质、证照及其他政府审批C. 公司D. 公司估值及投资意向E. 投资款使用F. 交割日G. 股权结构H. 交割条件创始人及公司的陈述与保证股权成熟优先购买权领售权 (如适用) (iv) 公司已经与关键管理层和人员(由投资人选定)签订格式和内容令投资人满意的劳动合同; (v) 公司创始人承诺自本条款清单签订之日起全职在公司工作; (vi) 其他投资人惯常要求的条件。

I. 创始人及公司须在正式投资协议中就投资和公司法律、财务及运营事项做出通常的陈述与保证。

投资条款清单

投资条款清单(声明:1、本声明文字可在下载后自行删除;2、合同生成过程中的提示,仅是基于通常情况下合同条款的示范,不能视为是米律的指导意见;3、在线生成的合同文本及具体条款,不是标准及最终法律文本,仅供参考,米律不建议直接使用,建议根据实际情况,在法律专业人士的指导下进行修改后再使用,米律就在线生成的合同不承担任何法律责任。

)本条款清单(下称“本清单”)由投资人与被投资公司(下称“公司”)及公司创始股东和共同签署。

本主要条款是基于公司提供的商业计划书以及其他相关信息而做出,除“保密及排他性”的条款外,其他条款对各方均无任何约束力。

被投资公司:,一家成立于的有限责任公司。

投资人:投前估值:人民币万元。

投资金额:人民币万元。

投资方式:投资人投资上述金额,取得本次增资后充分稀释基础上公司%的股权。

投资人权利:1、创始股东股权成熟。

创始股东股权自正式增资(投资)协议签署之日起分4年成熟,每年成熟 25%。

若创始股东主动从公司离职,或因自身原因不能履行职务,或因故意、重大过失被解职,创始股东应以人民币壹元的价格强制转让给其余创始股东和投资人。

2、创始股东股权锁定。

公司在合格资本市场首次公开发行股票(下称“IPO”) 前,未经投资人书面同意,创始股东不得以转让、赠与、质押、置换等任何方式进行处分,因公司实施股权激励计划的除外。

3、优先认购权。

公司如需要进一步融资,则投资人有权基于其持股比例享有相应的优先认购权。

4、优先购买权和共同出售权。

在公司IPO前,未经投资人事先书面同意,现有股东不得出售其持有的公司股权。

若投资人同意现有股东向第三方提议出售其全部或一部分股权,其应首先允许投资人自行选择:以和拟受让方同等的条件购买全部或部分该等股权,或以和拟受让方为购买股权而提出的同等条件等比例地出售投资人持有的股权。

5、股东的知情权与检查权。

投资人享有对公司的法定知情权,及对公司的检查权。

6、投资人清算优先权。

若公司发生任何清算、解散或终止情形,在公司依法付清清算费用、职工工资和劳动保险费用,缴纳所欠税款,清偿公司债务后,投资人有权优先于公司的其他股东取得相当于投资款 120 %的金额,以及对应的未分配利润,剩余部分由全体股东按各自股权比例进行分配。

投资条款清单模板

方合称“各方”)

备注:

(1)请根据投资项目的具体情况填写。

(2)若有优先股、可转换债券的按照具体项目再商谈具体条款。

(3)条款清单中有涉及“实际控制人”、“董监高”的投资项目,请根据具体项目的实际情况予以加列或者删除。

以下无正文

签约各方:(签字盖章)

原股东(甲方):

甲方之一: (自然人)

住所:

身份证号码:

联系电话:

甲方之二: (法人)

住所:

法定代表人:职务:联系电话:

传真:

投资方(乙方):

乙方:

住所:

法定代表人:职务:联系电话:

委托代理人或授权代表:

传真:

目标(标的)公司(丙方):

营业执照注册号码:

组织机构代码:。

投资协议条款清单(Term Sheet)- 反稀释条款

投资协议条款清单(Term Sheet)- 反稀释条款作者: 桂曙光Term Sheet - Anti-DilutionTraditionally, the anti-dilution provision is used to protect investors in the event a company issues equity at a lower valuation then in previous financing rounds. There are two varieties: weighted average anti-dilution and ratchet based anti-dilution. Standard language is as follows:Anti-dilution Provisions: The conversion price of the Series A Preferred will be subject to a [full ratchet / broad-based / narrow-based weighted average] adjustment to reduce dilution in the event that the Company issues additional equity securities (other than shares (i) reserved as employee shares described under the Company’s option pool,, (ii) shares issued for consideration other than cash pursuant to a merger, consolidation, acquisition, or similar business combination approved by the Board; (iii) shares issued pursuant to any equipment loan or leasing arrangement, real property leasing arrangement or debt financing from a bank or similar financial institution approved by the Board; and (iv) shares with respect to which the holders of a majority of the outstanding Series A Preferred waive their anti-dilution rights) at a purchase price less than the applicable conversion price. In the event of an issuance of stock involving tranches or other multiple closings, the antidilution adjustment shall be calculated as if all stock was issued at the first closing. The conversion price will also be subject to proportional adjustment for stock splits, stock dividends, combinations, recapitalizations and the like.Full ratchet means that if the company issues shares at a price lower than the Series A, then the Series A price is effectively reduced to the price of the new issuance. One can get creative and do "partial ratchets" (such as "half ratchets" or "two-thirds ratchets") which are a less harsh, but rarely seen.While full ratchets came into vogue in the 2001 – 2003 time frame whendown-rounds were all the rage, the most common anti-dilution provision is based on the weighted average concept, which takes into account the magnitude of the lower-priced issuance, not just the actual valuation. In a "full ratchet world" if the company sold one share of its stock to someone for a price lower than the Series A, all of the Series A stock would be repriced to the issuance price. In a "weighted average world," the number of shares issued at the reduced price are considered in the repricing of the Series A. Mathematically (and this is where the lawyers get to show off their math skills – although you’ll notice there are no exponents or summation signs anywhere) it works like this (note that despite the fact one is buying preferred stock, the calculations are always done in as-if-converted to common stock basis):NCP = OCP * ((CSO + CSP) / (CSO + CSAP))Where:•NCP = new conversion price•OCP = old conversion price•CSO = common stock outstanding•CSP = common stock purchasable with consideration received by company (i.e. "what the buyer should have bought if it hadn’t been a ‘down round’ issuance") •CSAP = common stock actually purchased in subsequent issuance (i.e., "what the buyer actually bought")Recognize that we are determining a "new conversion price" for the Series A Preferred . We are not actually issuing more shares (you can do it this way, but it’s a silly and unnecessarily complicated approach that merely increases the amount the lawyers can bill the company for the financing). Consequently, "anti-dilution provisions" generate a "conversion price adjustment" and the phrases are often used interchangeably.Got it? I find it’s best to leave the math to the lawyers.You might note the term "broad-based" in describing weighted average anti-dilution. What makes the provision a broad-based versus narrow-based is the definition of "common stock outstanding" (CSO). A broad-based weighted average provision includes both the company’s common stock outstanding (including all common stock issuable upon conversion of its preferred stock) as well as the number of shares of common stock which could be obtained by converting all other options, rights, and securities (including employee options). A narrow-based provision will not include these other convertible securities and limit the calculation to only currently outstanding securities. The number of shares and how you count them matter – make sure you are agreeing on the same definition (you’ll often find different lawyers arguing over what to include or not include in the definitions – again – this is another common legal fee inflation technique).In our example language, we’ve included a section which is generally referred to as "anti-dilution carve outs" (the section (other than shares (i) … (iv)). These are the standard exceptions for share granted at lower prices for which anti-dilution does not kick in. Obviously - from a company (and entrepreneur) perspective - more exceptions are better – and most investors will accept these carve-outs without much argument.One particular item to note is the last carve out: (iv) shares with respect to which the holders of a majority of the outstanding Series A Preferred waive theiranti-dilution rights. This is a carve out that started appearing recently which we have found to be very helpful in deals where a majority of the Series A investors agree to further fund a company in a follow-on financing, but the price will be lower than the original Series A. In this example, several minority investors signaled they were not planning to invest in the new round, as they would have preferred to "sit back" and increase their ownership stake via the anti-dilution provision. Having thelarger investors (the majority of the class) "step up" and vote to carve the financing out of the anti-dilution terms was a huge bonus for the company common holders and employees who would have suffered the dilution of additional anti-dilution from investors who were not continuing to participate in financing the company. This approach encourages the minority investors to participate in the round in order to protect themselves from dilution.Occasionally, anti-dilution will be absent in a Series A term sheet. Investors love precedent (e.g. the new investor says "I want what the last guy got, plus more"). In many cases anti-dilution provisions hurt Series A investors more than prior investors if you assume the Series A price is the low watermark for the company. For instance, if the Series A price is $1.00, the Series B price is $5.00, and the Series C price is $3.00, then the Series B is benefited by an anti-dilution provision at the expense of the Series A. However, our experience is that anti-dilution is usually requested despite this as Series B investors will most likely always ask for it and – since they do – the Series A proactively asks for it anyway.In addition to economic impacts, anti-dilution provisions can have control impacts. First, the existence of an anti-dilution provision incents the company to issue new rounds of stock at higher valuations because of the ramifications of anti-dilution protection to the common stock holders. In some cases, a company may pass on taking an additional investment at a lower valuation (although practically speaking, this only happens when a company has other alternatives to the financing). Second, a recent phenomenon is to tie anti-dilution calculations to milestones the investors have set for the company resulting in a conversion price adjustment in the case that the company does not meet certain revenue, product development or other business milestones. In this situation, the anti-dilution adjustments occur automatically if the company does not meet in its objectives, unless this is waived by the investor after the fact. This creates a powerful incentive for the company to accomplish its investor-determined goals. We tend to avoid this approach, as blindly hitting pre-determined (at the time of financing) product and sales milestones is not always best for the long-term development of a company, especially if these goals end up creating a diverging set of goals between management and the investors as the business evolves.Anti-dilution provisions are almost always part of a financing, so understanding the nuances and knowing which aspects to negotiate is an important part of the entrepreneur’s toolkit. We advise you not to get hung up in trying to eliminate anti-dilution provisions – rather focus on (a) minimizing their impact and (b) building value in your company after the financing so they don’t ever come into play.。

投资协议条款清单(Term Sheet)- 股权给付

投资协议条款清单(Term Sheet)- 股权给付作者: 桂曙光Term Sheet - VestingWhile vesting is a simple concept, it can have profound and unexpected implications. Typically, stock and options will vest over four years - which means that you have to be around for four years to own all of your stock or options (for the rest of this post, I'll simply refer to the equity as "stock" although exactly the same logic applies to options.) If you leave the company earlier than the four year period, the vesting formula applies and you only get a percentage of your stock. As a result, many entrepreneurs view vesting as a way for VCs to "control them, their involvement, and their ownership in a company" which, while it can be true, is only a part of the story.A typical stock vesting clause looks as follows:Stock Vesting: All stock and stock equivalents issued after the Closing to employees, directors, consultants and other service providers will be subject to vesting provisions below unless different vesting is approved by the majority (including at least one director designated by the Investors) consent of the Board of Directors (the "Required Approval"): 25% to vest at the end of the first year following such issuance, with the remaining 75% to vest monthly over the next three years. The repurchase option shall provide that upon termination of the employment of the shareholder, with or without cause, the Company or its assignee (to the extent permissible under applicable securities law qualification) retains the option to repurchase at the lower of cost or the current fair market value any unvested shares held by such shareholder. Any issuance of shares in excess of the Employee Pool not approved by the Required Approval will be a dilutive event requiring adjustment of the conversion price as provided above and will be subject to the Investors' first offer rights.The outstanding Common Stock currently held by _________ and ___________ (the "Founders") will be subject to similar vesting terms provided that the Founders shall be credited with [one year]of vesting as of the Closing, with their remaining unvested shares to vest monthly over three years. Industry standard vesting for early stage companies is a one year cliff and monthly thereafter for a total of 4 years. This means that if you leave before the first year is up, you don't vest any of your stock. After a year, you have vested 25% (that's the "cliff"). Then - you begin vestingmonthly (or quarterly, or annually) over the remaining period. So - if you have a monthly vest with a one year cliff and you leave the company after 18 months, you'll have vested 37.25% of your stock.Often, founders will get somewhat different vesting provisions than the balance of the employee base. A common term is the second paragraph above, where the founders receive one year of vesting credit at the closing and then vest the balance of their stock over the remaining 36 months. This type of vesting arrangement is typical in cases where the founders have started the company a year or more earlier then the VC investment and want to get some credit for existing time served.Unvested stock typically "disappears into the ether" when someone leaves the company. The equity doesn't get reallocated - rather it gets "reabsorbed" - and everyone (VCs, stock, and option holders) all benefit ratably from the increase in ownership (or - more literally - the reverse dilution.") In the case of founders stock, the unvested stuff just vanishes. In the case of unvested employee options, it usually goes back into the option pool to be reissued to future employees.A key component of vesting is defining what happens (if anything) to vesting schedules upon a merger. "Single trigger" acceleration refers to automatic accelerated vesting upon a merger. "Double trigger" refers to two events needing to take place before accelerated vesting (e.g., a merger plus the act of being fired by the acquiring company.) Double trigger is much more common than single trigger. Acceleration on change of control is often a contentious point of negotiation between founders and VCs, as the founders will want to "get all their stock in a transaction - hey, we earned it!" and VCs will want to minimize the impact of the outstanding equity on their share of the purchase price. Most acquires will want there to be some forward looking incentive for founders, management, and employees, so they usually either prefer some unvested equity (to help incent folks to stick around for a period of time post acquisition) or they'll include a separate management retention incentive as part of the deal value, which comes off the top, reducing the consideration that gets allocated to the equity ownership in the company. This often frustrates VCs (yeah - I hear you chuckling "haha - so what?") since it puts them at cross-purposes with management in the M&A negotiation (everyone should be negotiating to maximize the value for all shareholders, not just specifically for themselves.) Although the actual legal language is not very interesting, it is included below.In the event of a merger, consolidation, sale of assets or other change of control of the Company and should an Employee be terminated without cause within one year after such event, such person shall be entitled to[one year] of additional vesting. Other than the foregoing, there shall be no accelerated vesting in any event."Structuring acceleration on change of control terms used to be a huge deal in the 1990's when "pooling of interests" was an accepted form of accounting treatment as there were significant constraints on any modifications to vesting agreements. Pooling was abolished in early 2000 and - under purchase accounting - there is no meaningful accounting impact in a merger of changing the vesting arrangements (including accelerating vesting). As a result, we usually recommend a balanced approach to acceleration (double trigger, one year acceleration) and recognize that in an M&A transaction, this will often be negotiated by all parties. Recognize that many VCs have a distinct point of view on this (e.g. some folks will NEVER do a deal with single trigger acceleration; some folks don't care one way or the other) - make sure you are not negotiating against and "point of principle" on this one as VCs will often say "that's how it is an we won't do anything different."Recognize that vesting works for the founders as well as the VCs. I've been involved in a number of situations where one or more founders didn't work out and the other founders wanted them to leave the company. If there had been no vesting provisions, the person who didn't make it would have walked away with all their stock and the remaining founders would have had no differential ownership going forward. By vesting each founder, there is a clear incentive to work your hardest and participate constructively in the team, beyond the elusive founders "moral imperative." Obviously, the same rule applies to employees - since equity is compensation and should be earned over time, vesting is the mechanism to insure the equity is earned over time.Of course, time has a huge impact on the relevancy of vesting. In the late 1990's, when companies often reached an exit event within two years of being founded, the vesting provisions - especially acceleration clauses - mattered a huge amount to the founders. Today - as we are back in a normal market where the typical gestation period of an early stage company is five to seven years, most people (especially founders and early employees) that stay with a company will be fully (or mostly) vested at the time of an exit event.While it's easy to set vesting up as a contentious issue between founders and VCs, we recommend the founding entrepreneurs view vesting as an overall "alignment tool" - for themselves, their co-founders, early employees, and future employees. Anyone who has experienced an unfair vesting situation will have strong feelings about it - we believe fairness,a balanced approach, and consistency is the key to making vesting provisions work long term in a company.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

XX有限公司与XX有限公司投资意向书草案

项目

条款

1.被投资方

XX有限公司及其直接或间接拥有或控制的任何子公司、分公司或关联公司以下简称“目标公司”

2.投资方

XX

3.投资方式与金额

目标公司现有股东拟对外转让其持有的部分股权,共计股,每股定价为 元,合计元以下简称“老股转让安排”,其中XX同意认购股,合计元人民币;

交易各方各自承担为本次投资发生的费用,包括但不限于尽职调查费用、律师费用等;

16.保密性条款

双方另行签订保密协议;

17.法律及司法管辖权选择条款

本条款清单受中国法律管辖,由此引起的纠纷,协议各方同意将其提交至中国国际经济贸易仲裁委员会进行仲裁

18.非约束条款

本意向书不对投资者、目标公司及目标公司现有股东构成针对本意向书题述事宜的有法律约束力的协议;各方之间有法律约束力的协议尚有赖于投资者对目标公司完成尽职调查并对尽职调查结果满意,各方取得所有必要的目标公司批准及各方协商、批准、签署并交付最终交易协议;

本投资意向书于2017年 月 日签署:

签署人:_ห้องสมุดไป่ตู้___________________

姓名:

职务:

2由被投资公司及现有股东以连带责任对投资人作出赔偿,在此种情况下,被投资公司及现有股东应共同及连带的赔偿投资人因该等损害所发生的任何损失、损害、责任、成本或支出,包括但不限于合理的诉讼/仲裁费用和律师费,使投资人的权益恢复至违约事件未发生时的状态;

11.一票否决权

12.回购条款

股东及被投资公司特此同意并承诺,若被投资公司未按照本协议约定时间完成合格上市申报或合格上市,现有股东及被投资公司严重违反交易文件项下的有关约定或交易文件项下的承诺、陈述及/或保证,则投资人有权但无义务要求现有股东及/或被投资公司回购其届时持有的被投资公司全部或部分股份;

若目标公司向证监会申报上市材料的,则相关条款解除;但若目标公司的上市申报被不予受理、被否决、被劝退或者主动撤回的,且发生在业绩承诺期内,即xx年xx月xx日前,则估值调整条款自动恢复,并视为自始有效;若被不予受理、被否决、被劝退或主动撤回发生在业绩承诺期外,则估值调整条款不再恢复;注:估值调整条款另行商定;

具体交易结构以最终投资协议为准;

4.估值

本次交易完成之日,目标公司的投前估值为人民币x亿元;

5.老股出让资金用途

本次融资用于清理三类账户,便于公司申报IPO;

6.首次公开发行

7.业绩承诺及估值调整

目标公司xx年、xx年、xx年三年经审计税后净利润合计不低于人民币xx亿元其中xx年x亿元,xx年x亿元,xx年x亿元以下简称“承诺净利润”,如果目标公司未实现承诺净利润的x%,则目标公司对投资人进行现金或者股份补偿,补偿方式另行约定;

14.交割条件和程序

交割完成前按惯例至少需要完成以下事项,包括但不限于:相关方签署增资协议、股东协议、修订后的目标公司章程及其他交易性文件以下简称“交易协议”生效,本次投资及交易协议获得所有相关的目标公司内部的、交易协议中所要求的有关方和/或相关监管机关的批准与同意,及交易协议约定的其他交割条件;

15.费用

投资人行使上述的回购权,现有股东及/或被投资公司应在约定时日内自行回购或指定第三方购买投资人要求出售的被投资公司股份并足额支付回购价款/股份转让价款各现有股东对回购价款/股份转让价款的足额支付承担连带责任;

各方同意,在任何情况下,前述相关回购约定的回购价款/股份转让价款以下简称“回购价款”应为投资人届时要求回购的股份所对应的原始投资金额加上年化12%的收益率计算后所得的最终金额,具体计算公式如下:

回购价款=被回购的股份所对应的原始投资金额ⅹ1+12%ⅹN

其中,N为计息期间,即自相应原始投资金额支付被投资公司的公司账户之日含至投资人根据本条款约定收到全部回购价款之日/365;

13.陈述和保证

在交易协议中将就投资和目标公司法律、财务及运营事宜做出惯例的陈述与保证,包括但不限于目标公司截至交割日的财务和运营条件、知识产权、重大合同与承诺及监管合规性等;

8.优先认购权

目标公司新增注册资本或者发行股份时,投资者有权按照其股权比例享有优先认购权;

9.反稀释权

如果目标公司进行再次增资,则该等增资对目标公司的投前估值不应低于本次投资完成后的目标公司估值;

10.违约条款

被投资公司及现有股东中任何一方出现违约,则投资人有权选择:

1由现有股东对被投资公司进行赔偿,在此种情况下,现有股东应赔偿被投资公司因该等损害所发生的任何损失、损害、责任、成本或支出,包括但不限于合理的诉讼/仲裁费用和律师费;