管理会计作业Homework [Dec 21]

管理会计练习题作业答案

第一部分《管理会计》作业答案习题一解: a=2600-7.5×230=875y=a+bx=875+7.5x习题二解:依题意,选择的高低点坐标分别为(31,84 560)和(25,71 000) ∵b=(84560-71000)/(31-25)=2260(元/件) a=84 560—31×2 260=14 500(元) 或=71 000—25×2 260=14 500(元)∴A 产品的成本性态模型为:y=14 500+2 260x5.7=7023014002600=b解:∴y=a+bx=-535.5948+8.4891x当机器工时为150千时时,电费总支出数为 y=-535.5948+8.4891×150=737.77(百元)习题四(1)b=40000/=0.4 则在高点生产量下: 变动成本=×0.4=56000(元) 固定成本=84000(元)混合成本=-56000-84000=64000(元) 然后将高低点生产量下的混合成本列出如下:低点 高点生产量混合成本 50000 64000∴ a=50000-0.35×=15000(元) 混合成本公式为:y=15000+0.35x (2)当生产能量为小时时,混合成本:y=15000+0.35×=67500(元) 固定成本:84000(元) 变动成本:0.4×=60000(元)制造费用总额=84000+60000+67500=(元)()()()4891.8=1180114500×123590×1180340000×12==222∑∑∑∑∑x x n y x xyn b 5948.535=121180×4891.83590=•=x b ∑∑n y a 35.0=10000014000050000640000=b(1)按完全成本计算法编制的收益表:(2)按变动成本法编制的收益表:习题六(1)按完全成本计算法总成本=8000+5000+8000=21000(元)单位成本=21000/1200=17.5(元/件)(2)按变动成本计算法总成本=8000+5000=13000(元)单位成本=13000/1200=10.8(元/件)(3)①按完全成本法计算营业净利润营业收入=900×50=45000(元)营业成本=0+21000-17.5*(1200-900)=15750(元)营业毛利=45000-15750=29250(元)营业净利润=29250-(2000+3000)=24250(元)②按变动成本计算法计算营业净利润变动成本=10.8×900+2000=11720(元)贡献边际=45000-11720=33280(元)固定成本=8000+3000=11000(元)营业净利润=33280-11720=22280(元)习题七解:(1)单位变动成本=(6000+4000)/2000+0.4+0.2=5.6(元/件)单价=5.6/(1-60%)=14(元/件)(2)完全成本法下的单位产品成本=(6000+4000)/2000+0.4+2000/2000 =6.4(元/件)变动成本法下的单位产品成本=(6000+4000)/2000+0.4=5.4(元/件)(3)依题意,编制的利润表见下表。

管理会计小组作业

务支持和决策依据。

价值创造

管理会计将更加注重价值创造,通 过财务管理和决策分析为企业创造 更多的经济价值和社会价值。

智能化发展

随着信息技术的发展,管理会计将 逐步实现智能化,运用人工智能、 机器学习等技术提高工作效率和准 确性,降低人工成本。

战略成本管理

要点一

1. 分析企业内外部环境

了解企业的市场地位、竞争对手、客户需求等信息,以及 企业内部的优势和劣势。

要点二

2. 确定企业战略目标

根据内外部环境分析结果,确定企业的长期发展目标和短 期经营目标。

战略成本管理

3. 进行成本动因分析

分析影响企业成本的因素,包括结构性成本动因和执行性成本动因。

数据整合与共享

管理会计信息化能够实现企业 内部各部门之间的数据整合与 共享,加强信息沟通和协作, 促进企业决策的科学性和及时 性。

实时监控与分析

管理会计信息化能够实时收集 、处理和分析财务数据,为企 业提供及时、准确的财务信息 ,帮助企业及时发现问题、调 整经营策略。

管理会计国际化

全球视野

管理会计国际化要求企业具备全 球视野,关注国际市场和跨国经 营,运用国际通用的会计准则和 财务管理理念,提升企业的国际

管理会计小组作业

目

CONTENCT

录

• 管理会计概述 • 管理会计的基本理论 • 管理会计的实践应用 • 管理会计的新发展 • 管理会计案例分析

01

管理会计概述

管理会计的定义与特点

定义

管理会计是企业管理的重要组成部分,主要服务于企业内部决策 和管理,通过加工、整理、运用财务和非财务信息,帮助管理者 制定经营计划、做出决策、控制经营活动,促进企业实现战略目 标。

电科21春《管理会计学》在线作业3【标准答案】

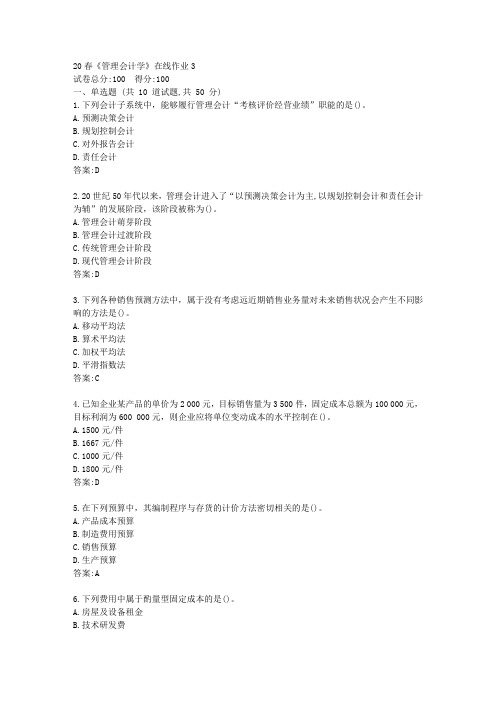

20春《管理会计学》在线作业3

试卷总分:100 得分:100

一、单选题 (共 10 道试题,共 50 分)

1.下列会计子系统中,能够履行管理会计“考核评价经营业绩”职能的是()。

A.预测决策会计

B.规划控制会计

C.对外报告会计

D.责任会计

答案:D

2.20世纪50年代以来,管理会计进入了“以预测决策会计为主,以规划控制会计和责任会计为辅”的发展阶段,该阶段被称为()。

A.管理会计萌芽阶段

B.管理会计过渡阶段

C.传统管理会计阶段

D.现代管理会计阶段

答案:D

3.下列各种销售预测方法中,属于没有考虑远近期销售业务量对未来销售状况会产生不同影响的方法是()。

A.移动平均法

B.算术平均法

C.加权平均法

D.平滑指数法

答案:C

4.已知企业某产品的单价为2 000元,目标销售量为3 500件,固定成本总额为100 000元,目标利润为600 000元,则企业应将单位变动成本的水平控制在()。

A.1500元/件

B.1667元/件

C.1000元/件

D.1800元/件

答案:D

5.在下列预算中,其编制程序与存货的计价方法密切相关的是()。

A.产品成本预算

B.制造费用预算

C.销售预算

D.生产预算

答案:A

6.下列费用中属于酌量型固定成本的是()。

A.房屋及设备租金

B.技术研发费。

管理会计学作业题1答案

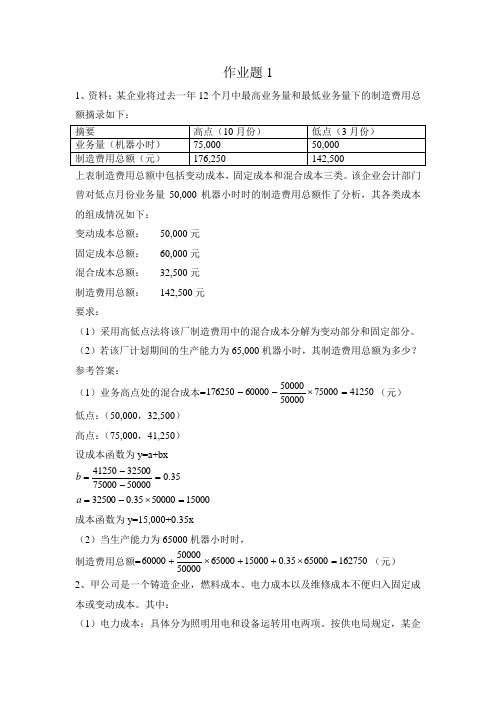

作业题11、资料:某企业将过去一年12个月中最高业务量和最低业务量下的制造费用总额摘录如下:上表制造费用总额中包括变动成本,固定成本和混合成本三类。

该企业会计部门曾对低点月份业务量50,000机器小时时的制造费用总额作了分析,其各类成本的组成情况如下:变动成本总额: 50,000元 固定成本总额: 60,000元 混合成本总额: 32,500元 制造费用总额: 142,500元 要求:(1)采用高低点法将该厂制造费用中的混合成本分解为变动部分和固定部分。

(2)若该厂计划期间的生产能力为65,000机器小时,其制造费用总额为多少? 参考答案:(1)业务高点处的混合成本=4125075000500005000060000176250=⨯--(元) 低点:(50,000,32,500) 高点:(75,000,41,250) 设成本函数为y=a+bx35.050000750003250041250=--=b150005000035.032500=⨯-=a成本函数为y=15,000+0.35x(2)当生产能力为65000机器小时时, 制造费用总额=1627506500035.01500065000500005000060000=⨯++⨯+(元) 2、甲公司是一个铸造企业,燃料成本、电力成本以及维修成本不便归入固定成本或变动成本。

其中:(1)电力成本:具体分为照明用电和设备运转用电两项。

按供电局规定,某企业的变压器维持费为50,000元/月,每度电费1.6元,用电额度每月20,000度,超额用电按正常电费的1.5倍计价。

正常情况下,每件产品平均用电2度。

照明用电每月2,000度。

(2)燃料成本。

燃料用于铸造工段的熔炉,具体分为点火(耗用木柴和焦炭)和熔化铁水(耗用焦炭)两项操作。

假设企业按照最佳的操作方法进行生产,每次点火要使用木柴0.1吨、焦炭1.5吨,熔化1吨铁水要使用焦炭0.15吨,铸造每件产品需要铁水0.01吨;每个工作日点火一次,全月工作22天,木柴每吨价格为10,000元,焦炭每吨价格为18,000元。

奥鹏吉大21年春季《管理会计》在线作业一_4.doc

1.中原公司有一台机器,其原价为80 000元,现欲处理,有以下两个方案可供选择:①外地晨光机器厂拟出价56 000元购买,但需中原公司支付拆卸、包装及运输费用共计12 000元。

②本市黄河机器厂拟租用这台机器10年,每年愿出租金8 000元,但需中原公司每年支付该机器的维修费和保险费1 000元。

假定租赁期满,该机器无残值;该公司的资金成本率为12%。

哪个方案较为有利()。

A.方案①B.方案②【参考答案】: A2.某企业生产经营一种产品,基期销售价格为60元/件,单位变动成本36元/件,销售量为1 000件,固定成本为20 000元。

则其营业杠杆系数为()。

A.4B.5C.6D.7【参考答案】: C3.某企业有A,B两个投资方案。

二者均为一次性投资20万元,资金成本率为12%,项目寿命5年。

A方案每年现金净流量8万元;B方案的年现金净流量分别是10万元、9万元、7.5万元、7万元和6万元。

用净现值法、内含报酬率法进行评价,哪个方案较优()。

A.A方案B.B方案【参考答案】: B4.某工厂有20 000件残次品,总成本为36 000元,该工厂可以0.90元/件的价格将这些残次品当做废料出售,也可花费22 000元的成本加以修复后,再以3.50元/件的价格售出。

该工厂应做出何种选择。

()A.直接出售B.修复后出售【参考答案】: B5.已知产品销售单价为24元,保本销售量为150件,销售额可达4800元,则安全边际率为()。

A.33.33%B.25%C.50%D.20%【参考答案】: B6.某企业于第六年初开始每年等额支付一笔设备款,其金额为2万元,连续支付5年,年利率为10%。

若现在一次付清应付()元。

A.50000B.51782.3C.51780D.52000【参考答案】: B7.在标准成本控制下的成本差异是指()。

A.实际成本与标准成本的差异B.实际成本与计划成本的差异C.预算成本与标准成本的差异D.实际成本与预算成本的差异【参考答案】: A8.管理会计的相关从业资格()。

管理会计英文版课后习题答案

第二章产品成本计算Exercises2–1(指教材上的第2章练习第1题,下同)1. Part #72A Part #172CSteel* $ 12.00 $ 18.00Setup cost** 6.00 6.00Total $ 18.00 $ 24.00*($1.00 ⨯ 12; $1.00 ⨯ 18)**($60,000/10,000)Steel cost is assigned by calculating a cost per ounce and then multiplying this by the ounces used by each part:Cost per ounce = $3,000,000/3,000,000 ounces= $1.00 per ounceSetup cost is assigned by calculating the cost per setup and then dividing this by the number of units in each batch (there are 20 setups per year):Cost per setup = $1,200,000/20= $60,0002. The cost of steel is assigned through the driver tracing using thenumber of ounces of steel, and the cost of the setups is assigned through driver tracing also using number of setups as the driver.3. The assumption underlying number of setups as the driver is thateach part uses an equal amount of setup time. Since Part #72A uses double the setup time of Part #172C, it makes sense to assign setup costs based on setup time instead of number of setups. This illustrates the importance of identifying drivers that reflect the true underlying consumption pattern. Using setup hours [(40 ⨯ 10) + (20 ⨯10)], we get the following rate per hour:Cost per setup hour = $1,200,000/600= $2,000 per hourThe cost per unit is obtained by dividing each part’s total setup costs by the number of units:Part #72A = ($2,000 ⨯ 400)/100,000 = $8.00Part #172C = ($2,000 ⨯ 200)/100,000 = $4.00Thus, Part #72A has its unit cost increased by $2.00, while Part #172C has its unit cost decreased by $2.00.problems2–51. Nursing hours required per year: 4 ⨯ 24 hours ⨯ 364 days* = 34,944*Note: 364 days = 7 days ⨯ 52 weeksNumber of nurses = 34,944 hrs./2,000 hrs. per nurse = 17.472Annual nursing cost = (17 ⨯ $45,000) + $22,500= $787,500Cost per patient day = $787,500/10,000 days= $78.75 per day (for either type of patient)2. Nursing hours act as the driver. If intensive care uses half of thehours and normal care the other half, then 50 percent of the cost is assigned to each patient category. Thus, the cost per patient day by patient category is as follows:Intensive care = $393,750*/2,000 days= $196.88 per dayNormal care = $393,750/8,000 days= $49.22 per day*$525,000/2 = $262,500The cost assignment reflects the actual usage of the nursing resource and, thus, should be more accurate. Patient days would be accurate only if intensive care patients used the same nursing hours per day as normal care patients.3. The salary of the nurse assigned only to intensive care is a directlytraceable cost. To assign the other nursing costs, the hours of additional usage would need to be measured. Thus, both direct tracing and driver tracing would be used to assign nursing costs for this new setting.2–61. Bella Obra CompanyStatement of Cost of Services SoldFor the Year Ended June 30, 2006 Direct materials:.............................................................................. Beginninginventory .............................................................. $ 300,000.............................................................................. Add: Purchases 600, .............................................................................. Materials available $ 900, .............................................................................. Less: Endinginventory .............................................................. 450,000*Direct materials used .......................................... $ 450,000 Direct labor .......................................................... 12,000,0 Overhead .............................................................. 1,500,00 Total service costs added .................................. $ 13,950,0 Add: Beginning work in process ....................... 900,000 Total production costs ........................................ $ 14,850,0 Less: Ending work in process ........................... 1,500,00 Cost of services sold .......................................... $ 13,350,0 *Materials available less materials used2. The dominant cost is direct labor (presumably the salaries of the 100professionals). Although labor is the major cost of providing manyservices, it is not always the case. For example, the dominant costfor some medical services may be overhead (e.g., CAT scans). Insome services, the dominant cost may be materials (e.g., funeralservices).3. Bella Obra CompanyIncome StatementFor the Year Ended June 30, 2006 Sales ..................................................................... $ 21,000,0 Cost of services sold .......................................... 13,350,0 Gross margin ....................................................... $ 7,650,00 Less operating expenses:.............................................................................. Selling expenses $ 900, .............................................................................. Administrativeexpenses ............................................................................................................................... 750,000.............................................................. 1,650,000Income before income taxes .............................. $ 6,000,00 4. Services have four attributes that are not possessed by tangibleproducts: (1) intangibility, (2) perishability, (3) inseparability, and (4)heterogeneity. Intangibility means that the buyers of services cannotsee, feel, hear, or taste a service before it is bought. Perishabilitymeans that services cannot be stored. This property affects thecomputation in Requirement 1. Inability to store services means thatthere will never be any finished goods inventories, thus making thecost of services produced equivalent to cost of services sold.Inseparability simply means that providers and buyers of servicesmust be in direct contact for an exchange to take place.Heterogeneity refers to the greater chance for variation in theperformance of services than in the production of tangible products.2–71. Direct materials:Magazine (5,000 ⨯ $0.40) $ 2,000Brochure (10,000 ⨯ $0.08) 800 $ 2,800 Direct labor:Magazine [(5,000/20) ⨯ $10] $ 2,500Brochure [(10,000/100) ⨯ $10] 1,000 3,500 Manufacturing overhead:Rent $ 1,400Depreciation [($40,000/20,000) ⨯ 350*] 700Setups 600Insurance 140Power 350 3,190 Cost of goods manufactured $ 9,490*Production is 20 units per printing hour for magazines and 100units per printing hour for brochures, yielding monthly machinehours of 350 [(5,000/20) + (10,000/100)]. This is also monthly laborhours, as machine labor only operates the presses.2. Direct materials $ 2,800Direct labor 3,500Total prime costs $ 6,300Magazine:Direct materials $ 2,000Direct labor 2,500Total prime costs $ 4,500Brochure:Direct materials $ 800Direct labor 1,000Total prime costs $ 1,800Direct tracing was used to assign prime costs to the two products.3. Total monthly conversion cost:Direct labor $ 3,500Overhead 3,190Total $ 6,690Magazine:Direct labor $ 2,500 Overhead:Power ($1 ⨯ 250) $ 250Depreciation ($2 ⨯ 250) 500Setups (2/3 ⨯ $600) 400Rent and insurance ($4.40 ⨯ 250 DLH)* 1,100 2,250 Total $ 4,750 Brochure:Direct labor $ 1,000 Overhead:Power ($1 ⨯ 100) $ 100Depreciation ($2 ⨯ 100) 200Setups (1/3 ⨯ $600) 200Rent and insurance ($4.40 ⨯ 100 DLH)* 440 940 Total $ 1,940 *Rent and insurance cannot be traced to each product so the costsare assigned using direct labor hours: $1,540/350 DLH = $4.40 perdirect labor hour. The other overhead costs are traced according totheir usage. Depreciation and power are assigned by using machine hours (250 for magazines and 100 for brochures): $350/350 = $1.00 per machine hour for power and $40,000/20,000 = $2.00 per machine hour for depreciation. Setups are assigned according to the time required. Since magazines use twice as much time, they receive twice the cost: Letting X = the proportion of setup time used for brochures, 2X + X = 1 implies a cost assignment ratio of 2/3 for magazines and 1/3 for brochures.Exercises3–11. Resource Total Cost Unit CostPlastic1$ 10,800 $0.027Direct labor andvariable overhead28,000 0.020Mold sets320,000 0.050Other facility costs410,000 0.025 Total $ 48,800 $0.12210.90 ⨯ $0.03 ⨯ 400,000 = $10,800; $10,800/400,000 = $0.0272$0.02 ⨯ 400,000 = $8,000; $8,000/400,000 = $0.023$5,000 ⨯ 4 quarters = $20,000; $20,000/400,000 = $0.054$10,000; $10,000/400,000 = $0.0252. Plastic, direct labor, and variable overhead are flexible resources;molds and other facility costs are committed resources. The cost of plastic, direct labor, and variable overhead are strictly variable. The cost of the molds is fixed for the particular action figure being produced; it is a step cost for the production of action figures in general. Other facility costs are strictly fixed.3–3High (1,400, $7,950); Low (700, $5,150)V = ($7,950 – $5,150)/(1,400 – 700)= $2,800/700 = $4 per oil changeF = $5,150 – $4(700)= $5,150 – $2,800 = $2,350Cost = $2,350 + $4 (oil changes)Predicted cost for January = $2,350 + $4(1,000) = $6,350problems3–61. High (1,700, $21,000); Low (700, $15,000)V = (Y2– Y1)/(X2– X1)= ($21,000 – $15,000)/(1,700 – 700) = $6 per receiving orderF = Y2– VX2= $21,000 – ($6)(1,700) = $10,800Y = $10,800 + $6X2. Output of spreadsheet regression routine with number of receivingorders as the independent variable:Constant 4512.98701298698 Std. Err. of Y Est. 3456.24317476605 R Squared 0.633710482694768 No. of10ObservationsDegrees of8 FreedomX Coefficient(s) 13.3766233766234Std. Err. of Coef. 3.59557461331427V = $13.38 per receiving order (rounded)F = $4,513 (rounded)Y = $4,513 + $13.38XR2 = 0.634, or 63.4%Receiving orders explain about 63.4 percent of the variability in receiving cost, providing evidence that Tracy’s choi ce of a cost driver is reasonable. However, other drivers may need to beconsidered because 63.4 percent may not be strong enough to justify the use of only receiving orders.3. Regression with pounds of material as the independent variable:Constant 5632.28109733183 Std. Err. of Y Est. 2390.10628259277 R Squared 0.824833789433823 No. of10ObservationsDegrees of8 FreedomX Coefficient(s) 0.0449642991356633Std. Err. of Coef. 0.0073259640055344V = $0.045 per pound of material delivered (rounded)F = $5,632 (rounded)Y = $5,632 + $0.045XR2 = 0.825, or 82.5%Pounds of material delivered explains about 82.5 percent of the variability in receiving cost. This is a better result than that of the receiving orders and should convince Tracy to try multiple regression.4. Regression routine with pounds of material and number of receiving orders as the independent variables:Constant 752.104072925631 Std. Err. of Y Est. 1350.46286973443 R Squared 0.951068418023306 No. of10ObservationsDegrees of7 FreedomX Coefficient(s) 0.0333883151096915 7.14702865269395 Std. Err. of Coef. 0.00495524841198368 1.68182916088492 V1= $0.033 per pound of material delivered (rounded)V2= $7.147 per receiving order (rounded)F = $752 (rounded)Y = $752 + $0.033a + $7.147bR2= 0.95, or 95%Multiple regression with both variables explains 95 percent of thevariability in receiving cost. This is the best result.5–21. Job #57 Job #58 Job #59Balance, 7/1 $ 22,450 $ 0 $ 0Direct materials 12,900 9,900 35,350Direct labor 20,000 6,500 13,000Applied overhead:Power 750 600 3,600Material handling 1,500 300 6,000Purchasing 250 1,000 250 Total cost $ 57,850 $ 18,300 $ 58,2002. Ending balance in Work in Process = Job #58 = $18,3003. Ending balance in Finished Goods = Job #59 = $58,2004. Cost of Goods Sold = Job #57 = $57,850problems5–31. Overhead rate = $180/$900 = 0.20 or 20% of direct labor dollars.(This rate was calculated using information from the Ladan job;however, the Myron and Coe jobs would give the same answer.)2. Ladan Myron Coe Walker WillisBeginning WIP $ 1,730 $1,180 $2,500 $ 0 $ 0 Direct materials 400 150 260 800 760 Direct labor 800 900 650 350 900 Applied overhead 160 180 130 70 180 Total $ 3,090 $2,410 $3,540 $ 1,220 $ 1,840 Note: This is just one way of setting up the job-order cost sheets.You might prefer to keep the detail on the materials, labor, andoverhead in beginning inventory costs.3. Since the Ladan and Myron jobs were completed, the others muststill be in process. Therefore, the ending balance in Work in Process is the sum of the costs of the Coe, Walker, and Willis jobs.Coe $3,540Walker 1,220Willis 1,840Ending Work in Process $6,600Cost of Goods Sold = Ladan job + Myron job = $3,090 + $2,410 = $5,5004. Naman CompanyIncome StatementFor the Month Ended June 30, 20XXSales (1.5 ⨯ $5,500) ................................................................... $8,250 Cost of goods sold ................................................................... 5,500 Gross margin ............................................................................ $2,750 Marketing and administrative expenses ................................ 1,200 Operating income ..................................................................... $1,550 5–201. Overhead rate = $470,000/50,000 = $9.40 per MHr2. Department A: $250,000/40,000 = $6.25 per MHrDepartment B: $220,000/10,000 = $22.00 per MHr3. Job #73 Job #74Plantwide:70 ⨯ $9.40 = $658 70 ⨯ $9.40 = $658Departmental:20 ⨯ $6.25 $ 125.00 50 ⨯ $6.25 $ 312.5050 ⨯ $22 1,100.00 20 ⨯ $22 440.00$ 1,225.00 $ 752.50Department B appears to be more overhead intensive, so jobs spending more time in Department B ought to receive more overhead. Thus, departmental rates provide more accuracy.4. Plantwide rate: $250,000/40,000 = $6.25Department B: $62,500/10,000 = $6.25Job #73 Job #74Plantwide:70 ⨯ $6.25 = $437.50 70 ⨯ $6.25 = $437.50Departmental:20 ⨯ $6.25 $ 125.00 50 ⨯ $6.25 $ 312.5050 ⨯ $6.25 312.50 20 ⨯ $6.25 125.00$ 437.50 $ 437.50 Assuming that machine hours is a good cost driver, the departmental rates reveal that overhead consumption is the same in each department. In this case, there is no need for departmental rates, anda plantwide rate is sufficient.5–41. Overhead rate = $470,000/50,000 = $9.40 per MHr2. Department A: $250,000/40,000 = $6.25 per MHrDepartment B: $220,000/10,000 = $22.00 per MHr3. Job #73 Job #74Plantwide:70 ⨯ $9.40 = $658 70 ⨯ $9.40 = $658Departmental:20 ⨯ $6.25 $ 125.00 50 ⨯ $6.25 $ 312.5050 ⨯ $22 1,100.00 20 ⨯ $22 440.00$ 1,225.00 $ 752.50 Department B appears to be more overhead intensive, so jobs spending more time in Department B ought to receive more overhead. Thus, departmental rates provide more accuracy.4. Plantwide rate: $250,000/40,000 = $6.25Department B: $62,500/10,000 = $6.25Job #73 Job #74Plantwide:70 ⨯ $6.25 = $437.50 70 ⨯ $6.25 = $437.50Departmental:20 ⨯ $6.25 $ 125.00 50 ⨯ $6.25 $ 312.5050 ⨯ $6.25 312.50 20 ⨯ $6.25 125.00$ 437.50 $ 437.50 Assuming that machine hours is a good cost driver, the departmental rates reveal that overhead consumption is the same in each department. In this case, there is no need for departmental rates, anda plantwide rate is sufficient.5–51. Last year’s unit-based overhead rate = $50,000/10,000 = $5This year’s unit-based overhead rate = $100,000/10,000 = $10Last Year This Year Bike cost:2 ⨯ $20 $ 40 $ 403 ⨯ $12 36 36Overhead:5 ⨯ $5 255 ⨯ $10 50Total $101 $126P rice last year = $101 ⨯ 1.40 = $141.40/dayPrice this year = $126 ⨯ 1.40 = $176.40/dayThis is a $35 increase over last year, nearly a 25 percent increase. No doubt the Carsons are not pleased and would consider looking around for other recreational possibilities.2. Purchasing rate = $30,000/10,000 = $3 per purchase orderPower rate = $20,000/50,000 = $0.40 per kilowatt hourMaintenance rate = $6,000/600 = $10 per maintenance hourOther rate = $44,000/22,000 = $2 per DLHBike Rental Picnic Catering Purchasing$3 ⨯ 7,000 $21,000$3 ⨯ 3,000 $ 9,000 Power$0.40 ⨯ 5,000 2,000$0.40 ⨯ 45,000 18,000 Maintenance$10 ⨯ 500 5,000$10 ⨯ 100 1,000 Other$2 ⨯ 11,000 22,000 22,000 Total overhead $50,000 $50,000 3. This year’s bike rental overhead rate = $50,000/10,000 = $5Carson rental cost = (2 ⨯ $20) + (3 ⨯ $12) + (5 ⨯ $5) = $101Price = 1.4 ⨯ $101 = $141.40/day4. Catering rate = $50,000/11,000 = $4.55* per DLHCost of Estes job:Bike rental rate (2 ⨯ $7.50) $15.00Bike conversion cost (2 ⨯ $5.00) 10.00Catering materials 12.00Catering conversion (1 ⨯ $4.55) 4.55Total cost $41.55*Rounded5. The use of ABC gives Mountain View Rentals a better idea of thetypes and costs of activities that are used in their business. Adding Level 4 bikes will increase the use of the most expensive activities, meaning that the rental rate will no longer be an average of $5 per rental day. Mountain View Rentals might need to set a Level 4 price based on the increased cost of both the bike and conversion cost.分步成本法6–11. C utting Sewing PackagingDepartment Department Department Direct materials $5,400 $ 900 $ 225 Direct labor 150 1,800 900 Applied overhead 750 3,600 900 Transferred-in cost:From cutting 6,300From sewing 12,600 Total manufacturing cost $6,300 $12,600 $14,625 2. a. Work in Process—Sewing ................. 6,300Work in Process—Cutting .......... 6,300b. Work in Process—Packaging ............ 12,600Work in Process—Sewing .......... 12,600c. Finished Goods ................................... 14,625Work in Process—Packaging ..... 14,6253. Unit cost = $14,625/600 = $24.38* per pair6–21. Units transferred out: 27,000 + 33,000 – 16,200 = 43,8002. Units started and completed: 43,800 – 27,000 = 16,8003. Physical flow schedule:Units in beginning work in process 27,000Units started during the period 33,000 Total units to account for 60,000 Units started and completed 16,800Units completed from beginning work in process 27,000Units in ending work in process 16,200 Total units accounted for 60,0004. Equivalent units of production:Materials Conversion Units completed 43,800 43,800 Add: Units in ending work in process:(16,200 ⨯ 100%) 16,200(16,200 ⨯ 25%) 4,050 Equivalent units of output 60,000 47,850 6–31. Physical flow schedule:Units to account for:Units in beginning work in process 80,000 Units started during the period 160,000 Total units to account for 240,000 Units accounted for:Units completed and transferred out:Started and completed 120,000From beginning work in process 80,000 200,000 Units in ending work in process 40,000 Total units accounted for 240,000 2. Units completed 200,000Add: Units in ending WIP ⨯ Fraction complete(40,000 ⨯ 20%) 8,000 Equivalent units of output 208,0003. Unit cost = ($374,400 + $1,258,400)/208,000 = $7.854. Cost transferred out = 200,000 ⨯ $7.85 = $1,570,000Cost of ending WIP = 8,000 ⨯ $7.85 = $62,8005. Costs to account for:Beginning work in process $ 374,400Incurred during June 1,258,400Total costs to account for $ 1,632,800Costs accounted for:Goods transferred out $ 1,570,000Goods in ending work in process 62,800 Total costs accounted for $ 1,632,8006–31、Units t0 account for:Units in beginning work in process(25% completed) 10000 Units started during the period 70000 Total units to account for 80000 Units accounted forUnits completed and transferred outStarted and completed 50000From beginning work in process 10000 60000 Units in ending work in process(60% completed) 20000 Total units accounted for 80000 2、60000+20000×60%=72000(units ) 3、Unit cost for materials:4900035100056000020000+=+($/unit )Unit cost for convension:2625787351.136000012000+=+($/unit )Total unit cost:5+1.13=6.13($/unit )4、The cost of units of transferred out:60000×6.13=367800($)The cost of units of ending work in process:20000×5+20000×20%×1.13=113560($)作业成本法4–21. Predetermined rates:Drilling Department: Rate = $600,000/280,000 = $2.14* per MHrAssembly Department: Rate = $392,000/200,000= $1.96 per DLH*Rounded2. Applied overhead:Drilling Department: $2.14 ⨯ 288,000 = $616,320Assembly Department: $1.96 ⨯ 196,000 = $384,160Overhead variances:Drilling Assembly Total Actual overhead $602,000 $ 412,000 $ 1,014,000 Applied overhead 616,320 384,160 1,000,480 Overhead variance $ (14,320) over $ 27,840 under $ 13,520 3. Unit overhead cost = [($2.14 ⨯ 4,000) + ($1.96 ⨯ 1,600)]/8,000= $11,696/8,000= $1.46**Rounded4–31. Yes. Since direct materials and direct labor are directly traceable toeach product, their cost assignment should be accurate.2. Elegant: (1.75 ⨯ $9,000)/3,000 = $5.25 per briefcaseFina: (1.75 ⨯ $3,000)/3,000 = $1.75 per briefcaseNote: Overhead rate = $21,000/$12,000 = $1.75 per direct labor dollar (or 175 percent of direct labor cost).There are more machine and setup costs assigned to Elegant thanFina. This is clearly a distortion because the production of Fina isautomated and uses the machine resources much more than thehandcrafted Elegant. In fact, the consumption ratio for machining is0.10 and 0.90 (using machine hours as the measure of usage). Thus,Fina uses nine times the machining resources as Elegant. Setupcosts are similarly distorted. The products use an equal number of setups hours. Yet, if direct labor dollars are used, then the Elegant briefcase receives three times more machining costs than the Finabriefcase.3. Overhead rate = $21,000/5,000= $4.20 per MHrElegant: ($4.20 ⨯ 500)/3,000 = $0.70 per briefcaseFina: ($4.20 ⨯ 4,500)/3,000 = $6.30 per briefcaseThis cost assignment appears more reasonable given the relativedemands each product places on machine resources. However, oncea firm moves to a multiproduct setting, using only one activity driverto assign costs will likely produce product cost distortions. Productstend to make different demands on overhead activities, and thisshould be reflected in overhead cost assignments. Usually, thismeans the use of both unit- and nonunit-level activity drivers. In thisexample, there is a unit-level activity (machining) and a nonunit-levelactivity (setting up equipment). The consumption ratios for each(using machine hours and setup hours as the activity drivers) are asfollows:Elegant FinaMachining 0.10 0.90 (500/5,000 and4,500/5,000)Setups 0.50 0.50 (100/200 and 100/200)Setup costs are not assigned accurately. Two activity rates areneeded—one based on machine hours and the other on setup hours:Machine rate: $18,000/5,000 = $3.60 per MHrSetup rate: $3,000/200 = $15 per setup hourCosts assigned to each product:Machining: Elegant Fina$3.60 ⨯ 500 $ 1,800$3.60 ⨯ 4,500 $ 16,200Setups:$15 ⨯ 100 1,500 1,500Total $ 3,300 $ 17,700Units ÷3,000 ÷3,000Unit overhead cost $ 1.10 $ 5.904:Elegant Unit overhead cost:[9000+3000+18000*500/5000+3000/2]/3000=$5.1 Fina Unit overhead cost:[3000+3000+18000*4500/5000+3000/2]/3000=$7.94–51. Deluxe Percent Regular PercentPrice $900 100% $750 100%Cost 576 64 600 80Unit gross profit $324 36% $150 20% Total gross profit:($324 ⨯ 100,000) $32,400,000($150 ⨯ 800,000) $120,000,000 2. Calculation of unit overhead costs:Deluxe gularUnit-level:Machining:$200 ⨯ 100,000 $20,000,000$200 ⨯ 300,000 $60,000,000 Batch-level:Setups:$3,000 ⨯ 300 900,000$3,000 ⨯ 200 600,000 Packing:$20 ⨯ 100,000 2,000,000$20 ⨯ 400,000 8,000,000 Product-level:Engineering:$40 ⨯ 50,000 2,000,000$40 ⨯ 100,000 4,000,000 Facility-level:Providing space:$1 ⨯ 200,000 200,000$1 ⨯ 800,000 800,000 Total overhead $25,100,000 $73,400,000 Units ÷100,000 ÷ 800,000 Overhead per unit $251 $91.75Deluxe Percent Regular Percent Price $900 100% $750.00 100% Cost 780* 87*** 574.50** 77*** Unit gross profit $120 13%*** $175.50 23%*** Total gross profit:($120 ⨯ 100,000) $12,000,000($175.50 ⨯ 800,000) $140,400,000*$529 + $251**$482.75 + $91.753. Using activity-based costing, a much different picture of the deluxeand regular products emerges. The regular model appears to be more profitable. Perhaps it should be emphasized.4–61. JIT Non-JITSales a$12,500,000 $12,500,000Allocation b750,000 750,000a$125 ⨯100,000, where $125 = $100 + ($100 ⨯0.25), and 100,000 is the average order size times the number of ordersb0.50 ⨯ $1,500,0002. Activity rates:Ordering rate = $880,000/220 = $4,000 per sales orderSelling rate = $320,000/40 = $8,000 per sales callService rate = $300,000/150 = $2,000 per service callJIT Non-JIT Ordering costs:$4,000 ⨯ 200 $ 800,000$4,000 ⨯ 20 $ 80,000 Selling costs:$8,000 ⨯ 20 160,000$8,000 ⨯ 20 160,000 Service costs:$2,000 ⨯ 100 200,000$2,000 ⨯ 50 100,000 T otal $1,160,000 $340,0 0For the non-JIT customers, the customer costs amount to $750,000/20 = $37,500 per order under the original allocation. Using activity assignments, this drops to $340,000/20 = $17,000 per order, a difference of $20,500 per order. For an order of 5,000 units, the order price can be decreased by $4.10 per unit without affecting customer profitability. Overall profitability will decrease, however, unless the price for orders is increased to JIT customers.3. It sounds like the JIT buyers are switching their inventory carryingcosts to Emery without any significant benefit to Emery. Emery needs to increase prices to reflect the additional demands on customer-support activities. Furthermore, additional price increases may be needed to reflect the increased number of setups, purchases, and so on, that are likely occurring inside the plant. Emery should also immediately initiate discussions with its JIT customers to begin negotiations for achieving some of the benefits that a JIT supplier should have, such as long-term contracts. The benefits of long-termcontracting may offset most or all of the increased costs from the additional demands made on other activities.4–71. Supplier cost:First, calculate the activity rates for assigning costs to suppliers: Inspecting components: $240,000/2,000 = $120 per sampling hourReworking products: $760,500/1,500 = $507 per rework hourWarranty work: $4,800/8,000 = $600 per warranty hourNext, calculate the cost per component by supplier:Supplier cost:Vance Foy Purchase cost:$23.50 ⨯ 400,000 $ 9,400,000$21.50 ⨯ 1,600,000 $ 34,400,000Inspecting components:$120 ⨯ 40 4,800$120 ⨯ 1,960 235,200Reworking products:$507 ⨯ 90 45,630$507 ⨯ 1,410 714,870Warranty work:$600 ⨯ 400 240,000$600 ⨯ 7,600 4,560,000 Total supplier cost $ 9,690,430 $ 39,910,070 Units supplied ÷400,000 ÷1,600,000 Unit cost $ 24.23* $ 24.94**RoundedThe difference is in favor of Vance; however, when the price concession is considered, the cost of Vance is $23.23, which is less than Foy’s component. Lumus should accept the contractual offer made by Vance.4–7 Concluded2. Warranty hours would act as the best driver of the three choices.Using this driver, the rate is $1,000,000/8,000 = $125 per warranty hour. The cost assigned to each component would be:Vance Foy。

管理会计作业

一、资料Adam公司生产某电子产品,下表显示了该公司在刚刚结束的年度中的数据。

Adam公司电子产品成本要求:1、本年中,一个不相关的市场潜在客户提出用$82000购买1000件该电子产品。

它不被包括在已售出的100 000件产品中。

固定的销售佣金率已被支付。

总裁拒绝了这个订单,因为“它低于我们$97的单位成本”。

你认为呢?2、一个供应商提出以单价$13.50生产本公司当年所需的100 000个塑料壳。

如果Adam公司外购而不是自制塑料壳,将对营业收益产生什么影响?假定外购壳子,就可以避免分摊到壳子上的$350 000可分属固定成本。

3、公司以单价$13.50外买壳子,并用腾出来的空间生产高端产品。

假设不包括壳子和10%的销售佣金,能够生产(并出售除100 000台普通产品之外)20 000件高端产品,单位变动成本是$90。

额外的20 000个塑料壳也可以以每个$13.50外购。

高端产品的售价是$130。

所有与塑料壳生产有关的固定成本都将继续,因为这些成本主要是与使用的制造设备有关。

如果Adam购买塑料壳并且生产和销售高端产品,营业收益会是多少?二、资料:某公司现有闲置资金400 000元,对如何有效地运用这笔资金,公司经理要求各有关部门提供决策资料。

市场部门将收集到的资料经过初步筛选,提供以下信息供公司管理层进行投资决策所用:1、目前国内销售市场上中档消毒碗柜紧缺,预计今后十五年内总需求量为6 000 000台。

目前国内的年生产能力为200 000台,而且品种单一,功能不全。

公司有生产中档消毒碗柜的技术能力,且力量雄厚,不仅可以保证产品质量,而且能改进功能,提高对顾客的吸引力。

2、生产消毒碗柜需新建生产车间用厂房一幢,新增生产流水线一条。

新建车间厂房预计投资155 000元,可使用十五年,十五年后报废残值约为 5 000元。

购建生产流水线有以下两个方案可供选择:(1)从国内市场上订购生产流水线并请设备安装公司施工安装,投资额为210 000元。

《管理会计》(高起专)作业答案(1)

《管理会计》作业答案一、单选题1-5.DDDBC 6-10.BCAAA 11-15.ACADD 16-20.ADBDB21-25.BBDDD 26-30.BADAA 31-35.BCCAB 36-40.BDCDB41-45.BBBDA 46-50.BAACC 51-55.CBCCC 56-60.DCBCC61-65.DACDC 66-70.DCACA 71-75.CDAAA 76-80.CADAA 81-85.DCACA 86-90.BABBD 91-95.DBBAB 96-100.CBDDC 101-105.DCDCB 106-110.BCDCD 111-115.CABBC 116-120.CADBC二、多选题1.A,B,C,E2.B,D,E3.A,B,D4.B,C,E5.B,D6.A,B,C,D,E7.C,D8.C,D,E9.A,B,C,D,E 10.A,C,D,E 11.B,C 12.C,D,E 13.A,B,C,D,E 14.A,C,D 15.B,C,D,E 16.A,B,C,D,E 17.A,B,C,D,E 18.A,B,C,D,E 19.A,D 20.A,D 21.C,D 22.A,D 23.A,B,C,D,E 24.C,D 25.A,C,D,E 26.A,C,E 27.A,B,C 28.A,E 29.A,C,E 30.A,B,C,D 31.A,B,C,D 32.B,C,D 33.A,B,C,E 34.B,C,E 35.A,C,E 36.A,C,E 37.A,B,C,D 38.A,C 39.A,B,C,D,E 40.B,C 41.A,B 42.A,C 43.A,D 44.A,B,D 45.A,D,E 46.C,D 47.A,B,C,D,E 48.A,C,D,E 49.C,E 50.A,C,D 51.B,D,E 52.D,E 53.A,B,C,E 54.A,C,E 55.A,C,D,E 56.B,C,D 57.A,E 58.B,C,E 59.B,D,E 60.C,D 61.A,D,E 62.A,B,C,D,E 63.A,B,C,D 64.A,B 65.A,B,C,D 66.A,B,D 67.B,C,E 68.C,E 69.A,B,C,D,E 70.B,C,D,E 71.D,E 72.A,B,C,D 73.A,B,C,E 74.A,B,E 75.B,C,E 76.A,B,D 77.B,D 78.A,B,D 79.A,C,D,E 80.A,C,D,E 81.B,C,D 82.A,B,D,E 83.A,B,C,D 84.B,D,E 85.B,C,D 86.A,C 87.B,C,E 88.B,C 89.B,C,E 90.B,C,D,E 91.A,B,E 92.A,B,D,E 93.A,B,C,D 94.A,C,D 95.A,C,E 96.C,E 97.A,C,D 98.A,B,C,D,E 99.A,B,C,D 100.A,B,C,E101.D,E 102.A,B,C 103.A,D 104.A,B,C,D,E 105.A,B,E 106.B,C,E 107.C,D,E 108.D,E 109.A,B,C,D,E 110.A,C,D,E 111.A,B,C,E 112.A,B,C 113.A,B,C 114.B,C,D,E 115.A,C,D 116.A,C,E 117.A,C,E 118.A,B,C,D,E 119.A,B,D 120.A,B,C,E 三、判断题1-5.√√×√×6-10.×××√√11-15.×√×√√16-20.√√√×√21-25.√×××√26-30.××√××31-35.××√×√36-40.×√√√√41-45.√√×××46-50.×××√×51-55.×√√××56-60.×××√×四、简答题1.答:二者的相同点如下:(1)总体目标相同;(2)均属于企业管理的一个组成部分;(3)具有相同的管理职能;(4)采用的分析方法相同;(5)工作主体相同。

奥鹏吉大21年春季《管理会计》在线作业二_2.doc

1.管理会计的相关从业资格()。

A.注册会计师(CPA)B.会计师C.注册管理会计师(CMA)D.主任会计师【参考答案】: C2.Stellar Systems公司的微处理器部门出售给组装部门一个计算机组件,用于组装完整的系统。

微处理器部门没有剩余生产能力。

这个计算机组件制造成本为10 000美元,它能以13 500美元卖到外部市场。

要求采用一般内部转移定价规则计算这个计算机组件的内部转移价格是()元。

A.13500B.13000C.15000D.14000【参考答案】: A3.某公司生产经营A,B两种产品,固定成本为60 000元,其中A产品专属部分12 000元。

两种产品都是对甲材料进行加工,A产品单位甲材料标准用量为50公斤,B产品单位甲材料标准用量为70公斤。

A产品售价为45元/件,单位变动成本25元/件;B产品售价为88元/件,单位变动成本为60元/件。

假定对A,B 两种产品的固定成本按材料的单位标准耗用量分配,企业的综合保本点为()元。

A.150000B.160000C.170000D.180000【参考答案】: B4.某公司于一年前购置机床一台,估计尚可使用10年,将来使用期满有残值2 000元。

最近市场上有一种新型机床,其售价为50 000元,购进后可使每年的销售收入从100 000增加到115 000元,每年的变动成本将从原来的86000增加到91 800元。

该项新型机床的使用寿命为10年,期未有残值2 000元。

假定该公司原有机床的账面价值为32 000元,将其立刻出售,可得价款10 000元。

该公司的资金成本率为18%。

根据上述分析,采用净现值法并结合差量分析,该公司售旧换新是否可行(不考虑折旧)。

()A.可行B.不可行【参考答案】: A5.某企业生产经营一种产品,基期销售价格为60元/件,单位变动成本36元/件,销售量为1 000件,固定成本为20 000元。

则其营业杠杆系数为()。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Beijing Normal University, Zhuhai

Management Accounting Homework

Page 1 of 3

Beijing Normal University, Zhuhai

Management Accounting

Homework

Instruction to students:

1) You should submit the homework on December 21, 2011 (Wednesday) directly to

me during the lecture meeting.

2) The homework must be submitted either by writing on paper or type on computer

and print it out.

3) Please write clearly your name, student number, and the class you registered on the

left top corner of the submitted homework.

4) Answer ALL questions.

5) Write clearly the question number you are answering.

6) You are required to write clearly the steps involved to arrive at your final answers.

Marks are allocated to the steps in developing the answer.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Question 1

Brightside Limited makes and sells only 2 products, PS and PT, the unit selling

prices being $24.00 and $50.00 respectively. The products are made using the same

production facilities. Variable costs are $16.80 for PS and $30.00 for PT. Fixed

costs are budgeted as $129,600 for the year. Annual production and sales are

budgeted as 5,000 units of PS and 5,600 units of PT.

Required

Calculate the break-even point in sales value in total and for each product for the

budget year. (20 marks)

Beijing Normal University, Zhuhai

Management Accounting Homework

Page 2 of 3

Question 2

Hawkins Limited makes 2 products, Model T and Model S, in one department. Selling

prices are $110 per unit of Model T and $160 per unit of Model S. The budgeted

production and sales units for 2011 are 2,000 units of Model T and 800 units of Model

S, and there were no stocks of either product at the beginning of 2011.

Material costs are expected to be $25 and $40 for a unit of Model T and Model S

respectively. Production hours for one unit are 4 hours and 6 hours for Model T and

Model S respectively. Direct workers are paid $9.00 per hour, and budgeted overheads

for 2011 are:

$

Variable overheads

47,360

Fixed overheads

87,040

134,400

Required

(a) Calculate the budgeted overhead absorption rate per direct labour hour for 2011.

(4 marks)

(b) Prepare a product cost for (i) one unit of Model T, and (ii) one unit of Model S.

(12 marks)

(c) Calculate the budgeted variable overhead absorption rate per direct labour hour for

2011. (2 marks)

(d) For (i) one unit of Model T, and (ii) one unit of Model S, prepare a product cost to

show the variable cost and contribution. (16 marks)

(e) Calculate the budgeted total contribution made by each product, and the budgeted

profit for the company. (6 marks)

Beijing Normal University, Zhuhai

Management Accounting Homework

Page 3 of 3

Question 3

Opshon Ltd commenced business on 1 January 2011 to produce a special type of

portable polishing machine. The budget was to make and sell 25,000 machines during

each quarter, giving the following budgeted profit and loss account:

$$

Sales750,000

Less:Production cost of sales

Direct materials275,000

Direct labour75,000

Variable factory overheads50,000

Fixed factory overheads100,000 500,000

Production profit250,000

Less:Fixed selling and administration overheads160,000

Net profit90,000

During the quarter ended 31 March 2011, 24,500 machines were made and 22,800 were

sold at the budgeted selling price. Actual costs were incurred on the same basis as the

budgeted cost structure.

Required

Prepare separate profit and loss accounts for the quarter ended 31 March 2011:

(a) using absorption costing (20 marks)

(b) using marginal costing (20 marks)