会计分录口诀

会计记账口诀

会计记账口诀

1. 记账就像数星星,借贷两方要分清,借方是那收债的狼,贷方像那还钱的羊。

2. 会计记账别发慌,有借有贷像阴阳,借方好比大胃口,贷方恰似粮入仓。

3. 记账犹如走迷宫,借贷规则要记浓,借方是那吞金兽,贷方如同散财童。

4. 会计记账不简单,借贷就像两座山,借方像那高坡难,贷方恰似缓坡坦。

5. 记账好似分楚汉,借贷两边界限严,借方如同楚霸王,贷方恰似汉刘邦。

6. 会计记账有妙方,借贷平衡像双桨,借方像那破浪舟,贷方恰似顺风浪。

7. 记账如同捉迷藏,借贷关系不能忘,借方像那捉人的猫,贷方恰似躲的鼠。

8. 会计记账心莫乱,借贷犹如正反瓣,借方像那凸出面,贷方恰似凹入湾。

9. 记账就像分黑白,借贷分明才不哀,借方像那黑包公,贷方恰似白脸怪。

10. 会计记账如打仗,借贷双方摆战场,借方像那进攻兵,贷方恰似防御墙。

11. 记账仿若理丝线,借贷清楚才顺坦,借方像那乱麻团,贷方恰似梳理杆。

12. 会计记账别胡猜,借贷如同天地开,借方像那高耸天,贷方恰似厚实地。

13. 记账犹如玩跷跷,借贷平衡不能跑,借方像那沉下砣,贷方恰似翘起角。

14. 会计记账要细心,借贷就像善恶分,借方像那恶之魔,贷方恰似善之神。

15. 记账好似排兵阵,借贷有序才安稳,借方像那先锋将,贷方恰似后援军。

16. 会计记账别懵懂,借贷好像水火冲,借方像那熊熊火,贷方恰似汪汪洪。

17. 记账仿佛分昼夜,借贷分明不纠结,借方像那黑夜幕,贷方恰似白昼光。

18. 会计记账有门道,借贷如同左右脚,借方像那左脚迈,贷方恰似右脚跷。

借贷科目口诀

借贷科目口诀

借贷科目口诀是会计学中的一个记忆方法,用于记住各种账户在借方和贷方的增减规则。

以下是常用的借贷科目口诀:

1. 资产类账户:

- 借:增加资产,减少负债

- 贷:减少资产,增加负债

2. 负债类账户:

- 借:减少负债,增加资产

- 贷:增加负债,减少资产

3. 所有者权益类账户:

- 借:增加所有者权益(包括资本、利润等)

- 贷:减少所有者权益

4. 收入类账户:

- 借:减少收入

- 贷:增加收入

5. 费用类账户:

- 借:增加费用

- 贷:减少费用

这些口诀可以帮助记忆常见的借贷规则,但在实际应用中,还需要根据具体情况和会计准则进行分析和处理。

同时,建议结合学习会计原理和实操经验,加深对借贷规则的理解和记忆。

初级会计实务巧记顺口溜

初级会计实务巧记顺口溜

以下是一些初级会计实务的巧记顺口溜:

1、借贷记账法口诀:借增贷减是资产,权益和它正相反。

成本资产总相同,细细记牢莫弄乱。

损益账户要分辨,费用收入不一般。

收入增加贷方看,减少借方来结转。

2、会计信息质量要求口诀:三可一相关,始终谨记。

可靠性、可理解性、可比性、相关性、实质重于形式、重要性、谨慎性、及时性。

3、权责发生制VS 收付实现制口诀:权责发生制看“事”不看“钱”,收付实现制看“钱”不看“事”。

这些顺口溜可以帮助初学者更好地记忆和理解初级会计实务的相关知识点。

但请注意,顺口溜只是辅助记忆的工具,真正掌握和理解会计知识还需要结合教材和实际案例进行深入学习。

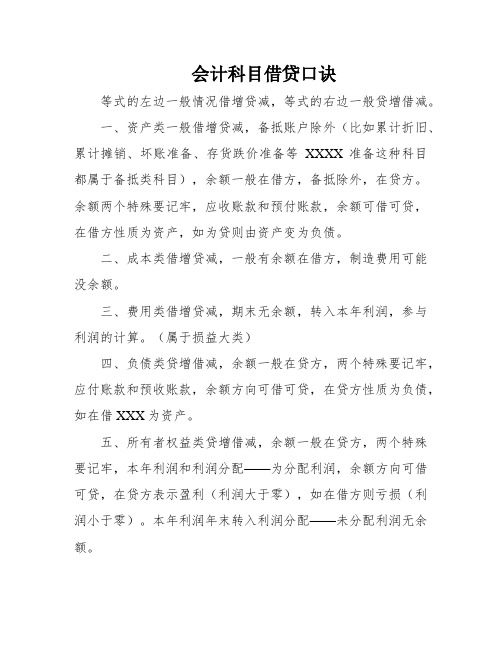

会计科目借贷口诀

会计科目借贷口诀

等式的左边一般情况借增贷减,等式的右边一般贷增借减。

一、资产类一般借增贷减,备抵账户除外(比如累计折旧、累计摊销、坏账准备、存货跌价准备等XXXX准备这种科目都属于备抵类科目),余额一般在借方,备抵除外,在贷方。

余额两个特殊要记牢,应收账款和预付账款,余额可借可贷,在借方性质为资产,如为贷则由资产变为负债。

二、成本类借增贷减,一般有余额在借方,制造费用可能没余额。

三、费用类借增贷减,期末无余额,转入本年利润,参与利润的计算。

(属于损益大类)

四、负债类贷增借减,余额一般在贷方,两个特殊要记牢,应付账款和预收账款,余额方向可借可贷,在贷方性质为负债,如在借XXX为资产。

五、所有者权益类贷增借减,余额一般在贷方,两个特殊要记牢,本年利润和利润分配——为分配利润,余额方向可借可贷,在贷方表示盈利(利润大于零),如在借方则亏损(利润小于零)。

本年利润年末转入利润分配——未分配利润无余额。

六、收入类贷增借减,期末无余额,转入今年利润,参与利润的计算。

(属于损益大类)。

7、损益类无余额,期末转入今年利润

资产=负责+所有者权益

利润=收入-费用

资产+费用=负责+所有者权益+收入。

会计借贷记账法口诀

会计借贷记账法口诀如何让学习者理解并掌握借贷记账法的相关知识点是会计教学工作中的一个重要环节。

下面店铺就为大家解开会计借贷记账法口诀,希望能帮到你。

会计借贷记账法口诀复试记账很简单,一笔分录记两边;关键分清借和贷(这句可以不要的,完全出于工整的考虑),左边是借右边贷;资产费用在借方,权益收入反过来。

“一笔分录记两边”揭示的是复式记账的特点;“左边是借右边贷”强调,借和贷都是纯粹的记账符号,是账户的两个方位;“资产费用在借方”揭示的是资产和费用两大类账户的账户结构,也就是说,对于这二类账户,他们增加,就要在账户的借方登记,而减少,就要记到相反的方向,即贷方。

这是基于综合的会计恒等式的基本判断。

会计借贷记账法的主要优点其优点主要有以下几方面:(1) 有利于分析经济业务,加强经济管理;(2) 有利于防止和减少记账差错;(3) 在账户设置上较为灵活;(4) 有利于会计电算化。

会计的基础课程始于借方和贷方。

借方在帐簿的左侧,贷方在帐簿的右侧。

在这里,要牢记一条不变的定律:“借方=贷方”,换句话说,在任何交易中,都必须同时登记到帐簿的左右两侧,其原则如下:(1)资产增加时,记入左侧;资产减少时,记入右侧。

(2)负债增加时,记入右侧;负债减少时,记入左侧。

(3)所有者权益增加时,计入右侧;所有者权益减少时,计入左侧。

(4)成本增加时,计入左侧;成本减少时,计入右侧。

(5)收入增加时,计入右侧;收入减少时,计入左侧。

(6)费用增加时,计入左侧;费用减少时,计入右侧。

会计等式为:资产=负债+所有者权益。

利润分配之前为:资产+费用=所有者权益+负债+收入。

可以看出,借和贷两个符号规定了相反的含义:借对于会计等式左边的账户是表示资产费用类账户的增加,对于会计等式右边的账户表示负债,所有者权益,收入类账户的减少。

贷正好相反。

因此有了上述的记账规则。

借贷记账法是以借贷为记账符号的一种复式记账法。

借贷记账法的账户基本结构分为左、右两方,左方称之为借方,右方称之为贷方。

借贷会计记账法口诀

借贷会计记账法口诀借贷记账法的存在已有几百年的历史,传入到中国也有近二百年的历史,它的存在有一定的历史原因与理论基础。

下面店铺就为大家解开借贷会计记账法口诀,希望能帮到你。

借贷会计记账法口诀借贷记账法下的记账规矩是基础会计学习的入门规律,咱们普通把账户辨别为资产、欠债、全部者权益、本钱、损益五大类。

资产、本钱类账户普通都是借方登记增加,贷方登记变少;欠债、全部者权益账户(两者兼并称为权益)普通都是借方登记变少,贷方登记增加;损益类账户则需求辨别是开销类还是收入类去分离登记,收入与开销之间的登记也是相反的。

为便于初学者理解,进步其学习兴趣,编写了以下口诀,并命名其为记账规矩之歌。

记账规矩之歌借增贷减是资产,权益跟它正相反。

损益账户要分辨,开销收入不普通。

收入增加贷方看,变少借方来结转。

会计核算有七种根本核算办法,即:设置会计科目(设置账户)、复式记账、填制跟考核证据、登记账簿、本钱核算、财产清查、编制会计报表。

咱们也可以把七种办法总结成为以下的口诀:会计核算办法七,设置科目属第一。

复式记账最神秘,家庭理财知识ppt填审证据不容易。

登记账簿要仔细,本钱核算讲效益。

财产清核对账实,编制报表工作齐。

利用口诀理解记忆跨期摊提账户的账务处理跨期摊提账户主要包括待摊开销跟预提开销账户。

待摊开销实际是先付费后分摊的开销,主要属于资产性质。

预提开销实际是先预计后付费的开销,主要属于欠债性质。

他们的共同点是收益期是若干个会计时期(月)。

他们的核算规律可以联合以下的口诀举行理解记忆。

待摊预提之歌待摊预提都跨期,权责发生来摊提。

先花货币是待摊,后掏腰包走预提。

支付待摊借方记,贷方资金来放弃。

摊销需从贷方转,借走开销进损益。

预提开销贷方提,四费借方来对应。

付费借方减预提,现金存款别忘掉。

这个口诀可以这样解释:第一句指出依照账户的用途跟结构举行分类,待摊开销跟预提开销都属于跨期摊提开销,两者核算的基础都是权责发生制。

第二句指出了两者在资金耗费工夫先后的差别。

会计背诵顺口溜口诀超级实用

会计背诵顺口溜口诀超级实用会计背诵顺口溜口诀超级实用一、资产负债表相关资产总计占资产负债表,其中有流动与非流动。

流动资产方,货币、应收款,存货、预付款。

非流动资产方,长期投资好,固定资产真才华,无形资产别纠结,合计就得到啦。

减去流动负债,那么剩下的就是净资产啦。

二、成本费用表相关成本费用表别犯愁,费用分类要注意。

办公费、销售费,研发费你也需。

营业外收入记一笔,利润表来一趟。

这几笔加总得出的利润,会让你心情很愉快。

三、利润表相关利润表上有两大类,营业收入和营业成本。

减下来好运行,就得到了毛利润。

再减去其他费用,是不是心情愉快?光是这些还不够,税费减下来不亏损。

这么一做利润分析,公司运营可不太易。

四、现金流量表相关现金流量表,重中之重,涵盖了一切要紧事。

经营、投资和筹资,平衡了资金的流动性。

经营活动带动流入,投资筹资顺带赚钱。

可是真的不太容易,要格外小心谨慎。

五、会计科目的记账要领借贷记账别搞混,借方右记贷方左。

资产负增借贷双生,再加上收入费用。

借、借、借;贷、贷、贷,对账平方能睡得香。

六、会计原则大讲堂会计原则知识多,规矩要遵守够。

真实性和公允性,谁都不能妥协。

持续经营和货币计量,忘记它们不行。

核算一个符号的平衡,这是玩会计的基本功。

七、审计大师的嘱咐审计大师有心情,找准问题替解决。

材料真实,可靠性好,工作底稿有据有。

准确表达,审计报告准点上。

对于审计问题不明白,果断去咨询才能开。

八、会计准则的变动会计准则更新,要跟上节奏。

政策变动,要快速学习和调整。

规范操作,文明待客,不踩准则的雷区。

会计岗位的责任重,成为规范的守护者。

以上是会计背诵顺口溜口诀,帮助你记忆轻松又有效。

会计不再难理解,口诀帮你轻松上手。

记住这些要点,助你在会计道路上走得更远。

会计分录口诀(Accountingentriesformula)

会计分录口诀(Accounting entries formula)The bookkeeping rules under debit and credit bookkeeping are the basic rules of basic accounting learning, and one of the most basic knowledge points that need profound memory and understanding by students. We usually divide accounts into five categories: assets, liabilities, owners' rights, costs, profits and losses. The cost of assets, generally accounts debit registered, credit registration reduced; liabilities, owners' equity accounts (two combined called interests) are generally reduced credit debit registered, registration; profit and loss account is needed to distinguish the expense or revenue to registration, registration is between income and expenses the opposite. For beginners to understand and improve their learning interest, I wrote the following formulas, and named it as "the song of accounting rules".The song of accounting rulesBy increasing loans minus assets, equity and it is the opposite.The total cost of assets, carefully remember mo.The profit and loss account has to distinguish the expense from the income.The increase in credit shows that borrowers are less likely to carry over.Accounting has seven basic accounting methods, namely: the setting of accounting subjects (accounts), double entry, fill and check the documents, registration books, cost accounting,inventory, accounting statements. We can also put the seven methods into the following formula:Accounting method seven, setting subject is the first.Double entry bookkeeping is the most mysterious, and it is not easy to fill in the voucher.Registration books should be careful, cost accounting, efficiency.Property inventory reconciliation, preparation of statements, work qi.The understanding of memory span formula amortization account accounting cross amortization account includes prepaid expenses and accrued expenses account. Prepaid expenses are actually paid after the cost of sharing, mainly belonging to the nature of assets. Accrued expenses are actually pre paid expenses, mainly in the nature of liabilities. What they have in common is that the earnings period is a number of accounting periods (months). The accounting rules they can be combined with the following formula to understand memory.A song waiting to accrueAccrued accruals are intertemporal and accrual basis is raised.First, to spend money is to be spread, and then pay out withholding.Pay the deferred debit note, the credit fund to give up. Amortization should be transferred from credit to expense. The accrued expense, the credit, the four fee, the debit. Pay debit deduction, cash deposit don't forget.This formula can be explained:The first sentence points out that according to the use and structure of accounts, the prepaid expenses and accrued expenses are all amortized expenses, and the basis of the two accounting is accrual basis". The second sentence points out the difference between the two funds in the time order. The third part of the corresponding prepaid expenses in the time of payment of the accounting entries, namely "borrow: prepaid expenses": Bank deposits". The fourth sentence corresponds to the cost of the allocation of prepaid expenses, namely, "borrow": management cost credit: prepaid expenses". In fact, the debit of this entry may be the manufacturing expense, or the management fee, and so on, mainly the period cost, so it is "profit and loss"". In the fifth sentence, the accounting entries of the accrued expenses at the time of extraction are as follows: "borrowing: management expenses: withholding expenses"". Its debit is mainly manufacturing costs, management fees, financial costs, operating expenses, so it is "four fees."". The sixth sentence is the accounting of the accrued expenses at the time of payment, namely "borrowing: withholding expenses: bank deposits."". Of course, the bank account in the above accounting entries can also be cash, andthe two are monetary funds.Using formulas understanding memory long-term equity investment accounting cost accounting method of dividend formulaBefore that year, the cost goes down.When the year is divided, the interest is counted.In the next year, they will be compared.Dividend net profit reduction,Judgment of difference."The year before, direct cost": for example, in January 1st 96 for long-term equity investment accounting by cost method, in May 2nd 96 declared by the investee companies 95 annual dividend distribution, so the investment enterprises will all offset the cost of investment."The year that year, interest count:" if in examples in May 2nd 96 dividend, including this year, then calculate the investment belongs to the part before the investment and belongs to the part of the former to offset the cost of investment, which included investment income. Of course, in this case, the test maker generally assumes an average monthly profit distribution.After the year, see "compare: 97 years later is not evendeclared dividend, then we can compare two values: first, is the cumulative dividend investment enterprises according to the proportion from the invested enterprise share (as at the end of this year); second, is in accordance with the proportion of investment enterprises enjoy the cumulative net profit by investment enterprise. Then judge:1, the former accumulates dividends = the latter accumulates net profit, and returns the previously reduced investment cost.2, the former and the latter will reduce the cost of investment by the difference between the former accumulated dividends and the latter accumulated net profits, which had already reduced the cost of investment. The dividends should be included in the dividends receivable, and the difference between the dividends receivable and the reduction costs should be included in the investment income.3, the former "the latter, do not offset the cost, if we have offset the cost, will all return, will not pay attention to (the cumulative dividend cumulative net profit was - - the latter to offset the cost of investment) the difference between the recovery, regardless of the difference is greater than, less than previously reduced cost amount. #p# paging Title #e#The whole process is based on the difference between accumulated dividends and accumulated net profits, so as to judge whether there is excessive distribution, so as to determine whether to reduce the investment cost or to restore the investment cost. If we can not determine the change of investment cost, we can not determine the size of investmentincome.Examples are as follows: suppose the cost of investment that was previously reduced is 10000, and the cumulative dividend that has been collected before is 10000.The distribution value is 30000Cumulative dividend 1000030000 = 40000Cumulative net profit of 40000Dividends receivable 30000Long term equity investment 10000Credit: investment income 40000The assigned value of 50000 cumulative dividend cumulative net profit 1000050000 = 60000 40000 difference 20000Dividends receivable 50000Credit: long term equity investment 10000 (2000010000)Investment income 40000The assigned value 250000, have cumulative dividend10000+25000 = 35000, the cumulative net profit margin 40000 - 5000 even number - 5000-10000 = - 15000 is not in accordance with the difference between the cost of recovery, or restorethe original has offset the full amount of the cost (not to exceed this amount)Dividends receivable 25000Long term equity investment 10000Credit: investment income 35000If the assigned value of 150000 points, has cumulative dividend cumulative net profit of 40000 10000+15000, the number of difference - 15000 - 15000 - 10000, even if the same = - 25000 is not in accordance with the difference between the cost of recovery, or restore the original has offset the full amount of 10000 of the cost (not to exceed this amount). If the undistributed dividend of the invested unit is negative in the current period, even if the initial investment cost should be negative, the current investment rights and interests and the initial investment cost will not be recognized.Understanding memory using formulas of the cash flow statement method of cash flow statement is the accounting exam very troubling content,Absent-minded is the most prone to errors in the preparation of cash flow statement. The following formula basically summarizes all the preparation process of the cash flow statement. How to understand the specific content of formulas, we elaborate on the formula behind.See income, find receivable, not pay tax separate walk.See cost payable, inventory change without negligence.The cost is adjusted first, and the difference is left behind.There are exceptions to the financial costs. Pay attention to the classification.Income tax, you directly transfer, outside the business to find fixed assets.Bad debts, depreciation, amortization, where to counter offset?.How much to pay for employees, separate treatment, classification thinking.Explanation: the first sentence according to the sales of goods and services received cash, because of the direct method is based on the profit table operating income for the starting point, so we see the operating income, to find receivables (accounts receivable, bills receivable etc.). Uncollected taxes to separate accounts (value-added tax to receive money as a cash flow) that should be part of the tax shall be collected include accounts receivable in, if the actual cash is not credited should pay tax, in addition, the discount, discount for bills receivable will produce discount (included in financial expenses) for antiregulation. For example: the amount of notes receivable is 100 thousand yuan (if it happened in March), and the discount rate is 10 thousand yuan in May. However, from the beginning of the end of the final report,notes receivable have not changed, but you can not do without cash flow adjustment, because the actual cash flow is 90 thousand yuan.The phrase "see the cost of inventory changes for deal with negligence" in "tell you to buy goods to pay cash when looking for deal with subjects, considering the inventory at the beginning of the period, the final value change, whether related to this project, the relevant adjustment.In the first sentence, the "expenses are first adjusted, and the difference is left behind" refers to the adjustment of the amount of "management expenses" and "operating expenses"". And the back of the 6 content only tune back. These 6 items are: bad debt preparation, deferred expenses, accumulated depreciation, amortization of intangible assets, payable to management personnel, payable to the welfare of management personnel (without any adjustment of operating expenses)There is an exception to the financial cost, which is the discount rate mentioned above.Article 5 "income tax and transfer business for fixed assets" income tax carryforwards, operating income, operating expenses, are from the fixed assets, the loss of the nature, to find the fixed assets.Article 6 sentence refers to the project does not affect cash flow, then you can come back to reverse.Article 7 sentence payments to employees, and cash payments forworkers is a special project, the need for a separate accounting.In general, there are three items to note: (1) 2 items need to be adjusted when the cash received from selling goods is calculated. Cash received from discount interest and payable tax in financial expense. 5 items need to be adjusted in the cash payment of purchase commodity. Accumulated depreciation, payable wages, payable welfare benefits, deferred expenses, payable taxes (input tax). (3) 6 items need to be adjusted in the calculation of the cash paid for other business activities. Provision for bad debts, deferred expenses, accumulated depreciation, payable to management personnel, payable to management, welfare, amortization of intangible assets.You can refer to the law of indirect accounting which I sum up for you. Profit and loss related items (Item 9) adjusted net profit. Fixed assets (4 items): impairment provision, depreciation, disposal loss, scrap loss. Intangible assets (1 items): amortization of intangible assets. Financial expense: the financial expense reflecting the investment in the current period, excluding discount interest (as we have already mentioned above, discount rate is a special financial expense),We must pay attention to the actual problem Investment loss, accrued expenses and deferred expenses. The profit and loss of the item (four): inventory, deferred taxes, business accounts receivable and payable, these adjustments can be applied to balance "assets = Liabilities + equity" when the owners' equity increases, reduced net profit; when the owner's equity is reduced, the increase in net profit, in order to achieve theaccrual system of net profit to cash flow from operating activities, the removal does not affect the cash flow change project. For example: if the increase in depreciation of fixed assets, the assets and liabilities unchanged reduce equity reduced, because depreciation does not affect cash flow, so take this part to net income increase, the other are modeled on the treatment.Six, use rhymes to understand memory fill balance sheet itemsIn the preparation of the balance sheet, fill in the "accounts receivable, prepayments, accounts payable, accounts receivable in advance of the four projects, to distinguish the corresponding list of debit or credit balance to calculate the list. I've summed up four formulas for students, as follows:1, the amount of assets receivable accounts receivable = "accounts receivable" detail account debit balance + "accounts receivable" detail account debit balance (assuming not to consider bad debt preparation)2, the amount of pre receivable account receivable of the debt is equal to the credit balance of the account receivable of the account receivable and the credit balance of the subsidiary account of the pre receivable account3, the amount of assets prepaid account amount = "prepaid accounts" detail account debit balance + payable accounts detailed account debit balance4, the amount of debt payable account amount = "accountspayable" detailed account credit balance + prepaid account detail account credit balanceLater found that students understand the four formula is not very comprehensive, calculation or error prone, I summed up the following "Five" formulas based on the four formula, to help students to enhance memory:Two collect and close, debit and credit go separately.Two pay and one pay, each goes his own way.It should be said that the first sentence used with the formula 1, 3, second, 4. can be matched with the formula of 2 such students fill in the project will greatly improve the accuracy of. For example, an enterprise only sets up accounts receivable and accounts payable, but does not set up accounts of prepayments and accounts receivable. The "accounts receivable" account is two a detailed account is a debit and credit balances were 400 and 700, "accounts payable" account also has two subsidiary account, the balance is 500 and 600 respectively, the debit credit, according to the formula can quickly calculate the "accounts receivable" and "prepayment", "accounts payable, accounts of the four project amount were 400, 500, 600, 700.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计分录口诀

会计分录口诀是一种记忆技巧,用于帮助记忆会计分录的规则和要点。

下面是一个常用的会计分录口诀:

借方增减负债权,贷方增减所有权。

借贷相等保平衡,会计分录两端正。

先借后贷分录列,借记在左贷记右。

资产负债者要借方,负债资产正贷方。

费用收入贷方记,借记收入正明白。

借贷方向归纳出,会计工作不迷糊。

这个口诀主要强调会计分录的基本原则,即借贷相等保平衡、借贷方向的确定和如何处理不同种类的账户。

通过反复使用和操练,可以帮助记忆和运用会计分录的规则。

好的,这是另外一个常用的会计分录口诀:

“增减对称同方向,同类错位当注意。

”

这个口诀强调了会计分录的对称性和方向性,以及在处理同一类账户时的注意事项。

具体解释如下:

- 借方和贷方的金额增减应该是对称的,即借方增加时贷方也

要增加,借方减少时贷方也要减少。

- 借方和贷方应该是同方向的,即在相同的经济事项下,如果

增加了借方,贷方也要增加,如果减少了借方,贷方也要减少。

- 对于同一类账户(例如资产账户、负债账户、权益账户等),借贷方向要相反。

例如,对于资产账户来说,借方表示增加,贷方表示减少。

这个口诀可以帮助记忆会计分录时的对称性、方向性以及同一类账户的处理方法。

通过不断练习和应用,可以提高记忆和运用会计分录的准确性和效率。

当资产增加,借方要记,

当负债增加,贷方要记。

当费用增加,贷方要记,

当收入增加,借方要记。

这是另一个简单的会计分录口诀,强调了资产、负债、费用和收入四种账户的分录规则。

其中,“增加”指的是账户余额增加,需要用借方或贷方来记录。

此外,还有一些其他的会计分录口诀:

- 营运成本借方记,费用和个人贷方走。

- 折旧和摊销也是贷,借方资产减少来。

- 应付账款借方记,付款和个人贷方走。

- 损益调整借贷对,借负益贷收益。

这些口诀都是为了方便记忆不同情况下的会计分录规则和方向,但仍需结合实际情况和会计知识进行正确的分录和处理。