公司理财考试复习题

公司理财原版题库Chap010

Chapter 10Return and Risk: The Capital-Assets-Pricing Model Multiple Choice Questions1. When a security is added to a portfolio the appropriate return and risk contributions areA) the expected return of the asset and its standard deviation.B) the expected return and the variance.C) the expected return and the beta.D) the historical return and the beta.E) these both can not be measured.Answer: C Difficulty: Medium Page: 2552. When stocks with the same expected return are combined into a portfolioA) the expected return of the portfolio is less than the weighted average expected return of thestocks.B) the expected return of the portfolio is greater than the weighted average expected return of thestocks.C) the expected return of the portfolio is equal to the weighted average expected return of thestocks.D) there is no relationship between the expected return of the portfolio and the expected return ofthe stocks.E) None of the above.Answer: C Difficulty: Easy Page: 2613. Covariance measures the interrelationship between two securities in terms ofA) both expected return and direction of return movement.B) both size and direction of return movement.C) the standard deviation of returns.D) both expected return and size of return movements.E) the correlations of returns.Answer: B Difficulty: Medium Page: 258-259Use the following to answer questions 4-5:GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows:State of Economy Probability GenLabs ReturnsDepression .05 -50%Recession .10 -15Mild Slowdown .20 5Normal .30 15%Broad Expansion .20 25Strong Expansion .15 404. The expected return on GenLabs is:A) 3.3%B) 8.5%C) 12.5%D) 20.5%E) None of the above.Answer: C Difficulty: Medium Page: 256Rationale:E(r) = .05(-.5) + .10(-.15) + .2(.05) + .3(.15) + .2(.25) + .15(.40) = .125 = 12.5%5. The variance of GenLabs returns isA) .0207B) .0428C) .0643D) .0733E) None of the above.Answer: B Difficulty: Medium Page: 256-257Rationale:.05(-.50 - .125)2 + .1(-.15 - .125)2 + .2(.05 - .125)2 + .3(.15 - .125)2 + .2(.25 - .125)2 + .15(.40 - .125)2 = .04286. The standard deviation of GenLabs returns isA) .0845B) .2069C) .3065D) .3358E) None of the above.Answer: B Difficulty: Medium Page: 256-257Rationale:.05(-.50 - .125)2 + .1(-.15 - .125)2 + .2(.05 - .125)2 + .3(.15 - .125)2 + .2(.25 - .125)2 + .15(.40 - .125)2 = .0428(.0428) = .20697. The correlation between two stocksA) can take in positive values.B) can take on negative values.C) cannot be greater than 1.D) cannot be less than -1.E) All of the above.Answer: E Difficulty: Medium Page: 260-2618. If the correlation between two stocks is –1, the returnsA) generally move in the same direction.B) move perfectly opposite one another.C) are unrelated to one another as it is < 0.D) have standard deviations of equal size but opposite signs.E) None of the above.Answer: B Difficulty: Medium Page: 2609. Stock A has an expected return of 20%, and stock B has an expected return of 4%. However, therisk of stock A as measured by its variance is 3 times that of stock B. If the two stocks arecombined equally in a portfolio, what would be the portfolio's expected return?A) 4%B) 12%C) 20%D) Greater than 20%E) Need more information to answer.Answer: B Difficulty: Medium Page: 262Rationale:Rp = 20(.5) + 4(.5) = 12%Use the following to answer questions 10-14:Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:Economy Idaho Slopes Dakota SteppesStrong Downturn -10% 2%Mild Downturn - 4% 7%Slow Growth 4% 6%Moderate Growth 12% 4%Strong Growth 20% 4%10. The mean expected returns of Idaho Slopes and Dakota Steppes areA) 4.0%; 6.0%B) 4.4%; 4.6%C) 5.5%; 5.8%D) 10.0%; 6.0%E) None of the aboveAnswer: B Difficulty: Medium Page: 256Rationale:IS = (-10%-4%+4%+12%+20%)/5 = 4.4%DS = (2%+7%+6%+4%+4%)/5 = 4.6%11. The variances of Idaho Slopes and Dakota Steppes areA) .0145; .00038B) .011584; .000304C) .006454; .000154D) .0008068; .000193E) None of the aboveAnswer: B Difficulty: Hard Page: 256-257Rationale:2IS = .2 = 0.0115842DS = .2 = .00030412. The covariance between the Idaho Slopes and Dakota Steppes returns isA) .00187B) .00240C) .00028D) .000056E) None of the aboveAnswer: C Difficulty: Hard Page: 258-259Rationale:ISDS = = .0002813. If Idaho Slopes and Dakota Steppes are combined in a portfolio with 50% invested in each, theexpected return and risk would be?A) 4.5%; 0%B) 4.5%; 5.48%C) 5.0%; 0%D) 5.625%; 37.2%E) 8.0%; 8.2%Answer: B Difficulty: Hard Page: 261-262Rationale:Rp = .5(.044) + .5(.046) = .045 = 4.5%p = .5 = .05477 = 5.48%14. The correlation between stocks A and B is theA) covariance between A and B divided by the standard deviation of A times the standarddeviation of B.B) standard deviation A divided by the standard deviation of B.C) standard deviation of B divided by the covariance between A and B.D) variance of A plus the variance of B dividend by the covariance.E) None of the above.Answer: A Difficulty: Medium Page: 26015. A portfolio is entirely invested into Buzz's Bauxite Boring Equity, which is expected to return 16%,and Zum's Inc. bonds, which are expected to return 8%. Sixty percent of the funds are invested in Buzz's and the rest in Zum's. What is the expected return on the portfolio?A) 6.4%B) 9.6%C) 12.8%D) 24.2%E) Need additional information.Answer: C Difficulty: Medium Page: 262Rationale:R p = .60(R Buzz)+.40(R Zum) = .60(16%) + .40(8%) = 12.8%16. You have plotted the data for two securities over time on the same graph, ie., the month return ofeach security for the last 5 years. If the pattern of the movements of the two securities rose and fell as the other did, these two securities would haveA) no correlation at all.B) a weak negative correlation.C) a strong negative correlation.D) a strong positive correlation.E) one can not get any idea of the correlation from a graph.Answer: D Difficulty: Easy Page: 26017. If the covariance of stock 1 with stock 2 is -.0065, then what is the covariance of stock 2 with stock1?A) -.0065B) +.0065C) greater than +.0065D) less than -.0065E) Need additional information.Answer: A Difficulty: Medium Page: 258-25918. If you have a portfolio of two risky stocks which turns out to have no diversification benefit. Thereason you have no diversification is the returnsA) are too small.B) move perfectly opposite of one another.C) are too large to offset.D) move perfectly with one another.E) are completely unrelated to one another.Answer: D Difficulty: Easy Page: 26419. A portfolio will usually containA) one riskless asset.B) one risky asset.C) two or more assets.D) no assets.E) None of the above.Answer: C Difficulty: Easy Page: 26120. The variance of Stock A is .004, the variance of the market is .007 and the covariance between thetwo is .0026. What is the correlation coefficient?A) .9285B) .8542C) .5010D) .4913E) .3510Answer: D Difficulty: Medium Page: 260Rationale:Standard deviation of B = .06325, Standard deviation of the market = .08366CORR = COV/(SDA)(SDM) = .0026/(.06325)(.08366) = .491321. If the correlation between two stocks is +1, then a portfolio combining these two stocks will have avariance that isA) less than the weighted average of the two individual variances.B) greater than the weighted average of the two individual variances.C) equal to the weighted average of the two individual variances.D) less than or equal to average variance of the two weighted variances, depending on otherinformation.E) None of the above.Answer: C Difficulty: Medium Page: 26422. The opportunity set of portfolios isA) all possible return combinations of those securities.B) all possible risk combinations of those securities.C) all possible risk-return combinations of those securities.D) the best or highest risk-return combination.E) the lowest risk-return combination.Answer: C Difficulty: Medium Page: 26723. A portfolio has 50% of its funds invested in Security One and 50% of its funds invested in SecurityTwo. Security One has a standard deviation of 6. Security Two has a standard deviation of 12. The securities have a coefficient of correlation of .5. Which of the following values is closest toportfolio variance?A) .0027B) .0063C) .0095D) .0104E) One must have covariance to calculate expected value.Answer: B Difficulty: Medium Page: 262Rationale: Var. = .52(.06)2 + .52(.12)2 + 2(.5)(.5)(.5)(6)(12) = .0009 + .0036 + .0018 = .006324. A portfolio has 25% of its funds invested in Security C and 75% of its funds invested in Security D.Security C has an expected return of 8% and a standard deviation of 6. Security D has an expected return of 10% and a standard deviation of 10. The securities have a coefficient of correlation of .6.Which of the following values is closest to portfolio return and variance?A) .090; .0081B) .095; .001675C) .095; .0072D) .100; .00849E) Cannot calculate without the number of covariance terms.Answer: C Difficulty: Medium Page: 261-262Rationale:E(R) = .25(.08) + .75(.10) = .095 = 9.5%Variance = .252(.06)2 + .752(.10)2 + 2(.25)(.75)(.06)(.60)(.10) = .007225. When many assets are included in a portfolio or index the risk of the portfolio or index will beA) greater than the risk of the securities because the correlations are greater than 1.B) equal to the risk of the securities because the correlations are equal to 1.C) less than the risk of the securities because the correlations are usually less than 1.D) unaffected by the risk of securities because their correlations are less than 1.E) None of the above.Answer: C Difficulty: Medium Page: 26426. The efficient set of portfoliosA) contains the portfolio combinations with the highest return for a given level of risk.B) contains the portfolio combinations with the lowest risk for a given level of return.C) is the lowest overall risk portfolio.D) Both A and BE) Both A and C.Answer: D Difficulty: Medium Page: 26727. Diversification can effectively reduce risk. Once a portfolio is diversified the type of riskremaining isA) individual security risk.B) riskless security risk.C) risk related to the market portfolio.D) total standard deviations.E) None of the above.Answer: C Difficulty: Easy Page: 27428. For a highly diversified equally weighted portfolio with a large number of securities, the portfoliovariance isA) the average covariance.B) the average expected value.C) the average variance.D) the weighted average expected value.E) the weighted average variance.Answer: A Difficulty: Medium Page: 273-27429. A well-diversified portfolio has negligibleA) expected return.B) systematic risk.C) unsystematic risk.D) variance.E) Both C and D.Answer: C Difficulty: Easy Page: 27430. The CML is the pricing relationship betweenA) efficient portfolios and beta.B) the risk-free asset and standard deviation of the portfolio return.C) the optimal portfolio and the standard deviation of portfolio return.D) beta and the standard deviation of portfolio return.E) None of the above.Answer: C Difficulty: Medium Page: 27931. The SML is the equilibrium pricing relationship forA) efficient portfolios.B) single securities.C) inefficient portfolios.D) All of the above.E) None of the above.Answer: D Difficulty: Easy Page: 285-28632. A typical investor is assumed to beA) a fair gambler.B) a gambler.C) a single security holder.D) risk averse.E) risk neutral.Answer: D Difficulty: Medium Page: 27533. You've owned a share of stock for 6 years. It returned 5% in 3 of those years and -5% in the other3. What was the variance?A) 0B) .0015C) .0030D) .0150E) .0400Answer: C Difficulty: Medium Page: 256-257Rationale:VAR= {(5-0)2 + (5-0)2 +(5-0)2 + (5-0)2 +(5-0)2 + (5-0)2/5 - 3034. The total number of variance and covariance terms in portfolio is N2. How many of these would be(including non-unique) covariance's?A) NB) N2C) N2 - ND) N2 - N/2E) None of the above.Answer: C Difficulty: Medium Page: 27235. Total risk can be divided intoA) standard deviation and variance.B) standard deviation and covariance.C) portfolio risk and beta.D) systematic risk and unsystematic risk.E) portfolio risk and covariance.Answer: D Difficulty: Easy Page: 27436. Beta measuresA) the ability to diversify risk.B) how an asset covaries with the market.C) the actual return on an asset.D) the standard of the assets' returns.E) All of the above.Answer: B Difficulty: Medium Page: 28337. The dominant portfolio with the lowest possible risk measures isA) the efficient frontier.B) the minimum variance portfolio.C) the upper tail of the efficient set.D) the tangency portfolio.E) None of the above.Answer: B Difficulty: Medium Page: 26638. The measure of beta associates most closely withA) idiosyncratic risk.B) risk-free return.C) systematic risk.D) unexpected risk.E) unsystematic risk.Answer: C Difficulty: Easy Page: 26939. An efficient set of portfolios isA) the complete opportunity set.B) the portion of the opportunity set below the minimum variance portfolio.C) only the minimum variance portfolio.D) the dominant portion of the opportunity set.E) only the maximum return portfolio.Answer: D Difficulty: Medium Page: 27040. A stock with a beta of zero would be expected to have a rate of return equal toA) the risk-free rate.B) the market rate.C) the prime rate.D) the average AAA bond.E) None of the above.Answer: A Difficulty: Medium Page: 28541. The combination of the efficient set of portfolios with a riskless lending and borrowing rate resultsinA) the capital market line which shows that all investors will only invest in the riskless asset.B) the capital market line which shows that all investors will invest in a combination of theriskless asset and the tangency portfolio.C) the security market line which shows that all investors will invest in the riskless asset only.D) the security market line which shows that all investors will invest in a combination of theriskless asset and the tangency portfolio.E) None of the above.Answer: B Difficulty: Medium Page: 27842. According to the CAPMA) the expected return on a security is negatively and non-linearly related to the security's beta.B) the expected return on a security is negatively and linearly related to the security's beta.C) the expected return on a security is positively and linearly related to the security's variance.D) the expected return on a security is positively and non-linearly related to the security's beta.E) the expected return on a security is positively and linearly related to the security's beta.Answer: E Difficulty: Easy Page: 28243. The diversification effect of a portfolio of two stocksA) increases as the correlation between the stocks declines.B) increases as the correlation between the stocks rises.C) decreases as the correlation between the stocks rises.D) Both A and C.E) None of the above.Answer: A Difficulty: Medium Page: 26644. The elements along the diagonal of the Variance / Covariance matrix areA) covariances.B) security weights.C) security selections.D) variances.E) None of the above.Answer: D Difficulty: Medium Page: 27245. The elements in the off-diagonal positions of the Variance / Covariance matrix areA) covariances.B) security selections.C) variances.D) security weights.E) None of the above.Answer: A Difficulty: Medium Page: 27246. The separation principle states that an investor willA) choose any efficient portfolio and invest some amount in the riskless asset to generate theexpected return.B) choose an efficient portfolio based on individual risk tolerance or utility.C) never choose to invest in the riskless asset because the expected return on the riskless asset islower over time.D) invest only in the riskless asset and tangency portfolio choosing the weights based onindividual risk tolerance.E) All of the above.Answer: D Difficulty: Medium47. The beta of a security is calculated byA) dividing the covariance of the security with the market by the variance of the market.B) dividing the correlation of the security with the market by the variance of the market.C) dividing the variance of the market by the covariance of the security with the market.D) dividing the variance of the market by the correlation of the security with the market.E) None of the above.Answer: A Difficulty: Medium Page: 28348. If investors possess homogeneous expectations over all assets in the market portfolio, when risklesslending and borrowing is allowed, the market portfolio is defined toA) be the same portfolio of risky assets chosen by all investors.B) have the securities weighted by their market value proportions.C) be a diversified portfolio.D) All of the above.E) None of the above.Answer: D Difficulty: Medium Page: 28049. A portfolio contains two assets. The first asset comprises 40% of the portfolio and has a beta of 1.2.The other asset has a beta of 1.5. The portfolio beta isA) 1.35B) 1.38C) 1.42D) 1.50E) 1.55Answer: B Difficulty: Medium Page: 287Rationale:βp = .4(1.2)+.6(1.5)=1.3850. A portfolio contains four assets. Asset 1 has a beta of .8 and comprises 30% of the portfolio. Asset2 has a beta of 1.1 and comprises 30% of the portfolio. Asset3 has a beta of 1.5 and comprises 20%of the portfolio. Asset 4 has a beta of 1.6 and comprises the remaining 20% of the portfolio. If the riskless rate is expected to be 3% and the market risk premium is 6%, what is the beta of theportfolio?A) 0.80B) 1.10C) 1.19D) 1.25E) 1.40Answer: C Difficulty: Hard Page: 287Rationale:βp = .3(.8)+.3(1.1)+.2(1.5)+.2(1.6)=1.1951. The characteristic line is graphically depicted asA) the plot of the relationship between beta and expected return.B) the plot of the returns of the security against the beta.C) the plot of the security returns against the market index returns.D) the plot of the beta against the market index returns.E) None of the above.Answer: C Difficulty: Medium Page: 281-28252. Recent research by Fama and French calls into questions the CAPM because they findA) average security returns are negatively related to the firm P/E and M/B ratios.B) P/E and M/B are only two of several factors explaining average returns.C) a weak relationship between average returns and beta for 1941 to 1990 and no relationshipfrom 1963 to 1990.D) Both A and C.E) Both B and C.Answer: D Difficulty: Hard Page: 29553. Further study to evaluate the Fama-French results and the CAPM are needed becauseA) P/E and M/B may be two of a large set of factors which were found due to hindsight bias.B) A positive relationship is found over the period 1927 to 1990 indicating more than 50 years ofdata are necessary for proper CAPM testing.C) Annual data based estimates of beta show positive relationships to average returns, whilemonthly betas do not.D) All of the above.E) None of the above.Answer: D Difficulty: Hard Page: 295-296Essay Questions54. Given the following data:Year Returns – Ink, Inc. Returns – S & P 500 1 10% 15% 2 0% -2% 3 -5% -2% 4 15 10% 5 5% 0%Calculate the covariance between Ink and the S&P 500.Difficulty: Hard Page: 258-259 Answer:R I IRR I - IR R SP SP R R SP –SP R.10 .05 .05 .15 .042.108 .00 .05 -.05 -.02 .042 -.062 -.05 .05 -.10 -.02 .042 -.062 .15 .05 .10 .10 .042 .058 .05.05.00 .00 .0421-.042(R I - I R ) x (R SP –SP R ).05 x.108 .0054 -.05 x -.062 .0031 -.10 x -.062 .0062 .10 x .058 .00580 x -.402.0205/5=.004155. A portfolio is made up of 75% of stock 1, and 25% of stock 2. Stock 1 has a variance of .08, andstock 2 has a variance of .035. The covariance between the stocks is -.001. Calculate both the variance and the standard deviation of the portfolio. Difficulty: Medium Page: 262 Answer: σ² = (.75)²(.08) + (.25)²(.035) + 2(.25)(.75)(-.001) = .0468 σ = .216356. Illustrate and explain the impact of adding securities to a portfolio assuming the securities are ofaverage correlation with each other. Difficulty: Medium Page: 274Answer:As N increases, portfolio risk decreases. As N gets large, portfolio risk approaches the market risk.For details please refer to the text Figure 10.7 page 274.57. Given the following information on 3 stocks:Stock A Stock B Stock C T-Bills Market PortExp. Return .19 .15 .09 .07 .18Variance .0200 .1196 .0205 .0000 .0064Covariance withMkt Portfolio .007 .0045 .0013 .0000 .0064Using the CAPM, calculate the expected return for Stock's A, B, and C. Which stocks would you recommend purchasing?Difficulty: Hard Page: 285-287Answer:B A = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903B B = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473B C = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0.923Indifferent on A as .1903 = .19.Would buy B as .15 > .1473.Would not buy C as .09 < .0923.58. Returns for the IC Company and for the S&P 500 Index over the previous 4-year period are givenbelow:Year IC Co. S & P 5001 30% 17%2 0% 20%3 -8% 7%4 0% 5%What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?Difficulty: Medium Page: 259Answer:Average return is 22/4 = 5.5% for IC and 49/4 = 12.25% for the S&P.After 4 years $1.00 in IC grows to $1.00(1.30)(.92) = 1.196 = $1.20.For n=4σIC = 14.52, σSP = 6.38, σIC,SP = 46.125, determining ( r IC,SP ) =0.498For n-1 = 3σIC = 16.76 σSP = 7.37 σIC,SP = 61.50 determining (r IC,SP ) =. 49859. Draw and explain the relationship between the opportunity set for a two asset portfolio when thecorrelation is: [Choose from -1, -.5, 0, +.5, and +1] Difficulty: Hard Page: 267-268 Answer: ∙ Opportunity set is made up of a portfolio of two asset combinations with weights from (0,100) to (100,0). ∙ Upper point--maximum return portfolio, 100% in highest return sec. ∙ Inflection point--minimum variance portfolio ∙ See diagram, pg. 267MRPStd. DeviationRpOpportunity SetBetween the MVP (Minimum Variance Portfolio) andthe MRP (Maximum Return Portfolio) is the efficient set of portfolios.60. The diagram below represents an opportunity set for a two asset combination. Indicate the correctefficient set with labels; explain why it is so. Difficulty: Hard Page: 267-268 Answer: ∙ Efficient set is portion of opportunity set that dominates. ∙ Provides maximum return for given risk or converse.MRPStd. DeviationRpOpportunity SetA is on the efficient frontier with the best return to risk combination. Portfolioson the frontier dominate all other portfolios. A dominates both B and C. B has a higher standard deviation for the same return while C has a lower return for the same standard deviation.ABCXX。

对外经贸大学公司理财试卷

对外经济贸易大学《公司理财》期末考试试卷(参考答案完美版)学号:姓名:成绩:案例1:(50分)Ragan Thermal Systems公司9年前由Carrington和Genevieve Ragan两兄妹创建。

公司生产和安装商务用的采暖通风与空调系统(HV AC)。

Ragan公司因拥有能提高系统能源适用效率的私人技术,正处于高速增长阶段。

目前,公司由两兄妹平等地共同拥有。

他们之间的最初协议是每人拥有50,000股公司股票,如果某一方要出股票,那么这些股票必须按某一折扣价提供给对方。

尽管此时两兄妹不打算出售股票,但他们希望对手中股票的注:EPS:每股盈利,DPS:每股股利,Stock Price:每股价格,ROE:权益资本回报率,R:必要报酬率Expert hld的EPS为负,原因在于去年会计冲销,如果不进行冲销,那么该公司的EPS为2.34美元。

去年,Ragan公司的EPS为4.32美元,并且向两兄妹各支付了54000美元。

目前,公司的ROE为25%。

两兄妹相信,公司的必要报酬率为20%。

根据公司增长率计算公式,公司增长率g = ROE × b,其中b为再投资比率。

1.假设公司会保持目前的增长率,那么公司股票的每股价值是多少?2.为了验证他们的计算,两兄妹雇了Josh Schlessman为顾问。

Josh研究发现,Ragan公司的技术优势只能再持续5年,然后,公司的增长率将降为行业平均水平。

另外,Josh认为,公司所使用的必要报酬率太高,他认为使用行业的平均必要报酬率更合适。

在Josh 的假设下,公司的股票价格应该是多少?解题提示:股价P0 = D1 / (R – g)答案1、增长率g =ROE*Retention ratio=0.25*(4.32-54000/50000)/4.32=0.1875 股价P =D1/(R-g)=D0(1+g)/(R-g)=1.08*(1+0.1875)/(0.2-0.1875)=102.6答案3、Industry Payout Ratio=(0.16+0.52+0.54)/(0.82+1.32+2.34)=0.2723 Industry Retention Ratio=1-0.2723=0.7277Industry ROE=0.13行业平均增长率Industry g (gi)=0.7277*0.13=0.0946D1 =D0(1+g) =1.08*(1+0.1875)=1.2825 折现P1= D1/1+0.1167=1.1485 D2 =D0(1+g)^2 =1.08*(1+0.1875)^2 折现P2=D2/(1+0.1167)^2=1.2213D3 =D0(1+g)^3 =1.08*(1+0.1875)^3 折现P3=D3/(1+0.1167)^3=1.2987D4 =D0(1+g)^4 =1.08*(1+0.1875)^4 折现P4=D4/(1+0.1167)^4=1.3811D5 =D0(1+g)^2 =1.08*(1+0.1875)^5 折现P5=D5/(1+0.1167)^5=1.4686D6 =D5(1+gi) = D5(1+0.0946) = 2.7916Value in year 5 = D6/Ri-gi = D6/(0.1167-0.0946) =126.30折现PV5 =126.30/(1+0.1167)^5 = 72.73每股价值PV= P1+P2+P3+P4+P5+PV5 = 79.25案例2:(50分)Cheek产品公司(CPI)在53年前由Joe Cheek创建,其最初销售如薯片和快餐。

公司理财期末考试试题开卷

公司理财期末考试试题开卷### 公司理财期末考试试题一、选择题(每题2分,共10分)1. 公司的财务杠杆效应是指:- A. 公司使用债务融资来增加股东的回报率- B. 公司通过增加资产来提高利润- C. 公司通过减少成本来提高利润- D. 公司通过增加销售来提高利润2. 资本资产定价模型(CAPM)中,β系数代表的是: - A. 资产的期望回报率- B. 资产的无风险回报率- C. 资产的系统性风险- D. 资产的非系统性风险3. 以下哪项不是公司财务报表的一部分?- A. 资产负债表- B. 利润表- C. 现金流量表- D. 产品目录4. 公司进行股票回购的主要目的通常是为了:- A. 增加公司的市场竞争力- B. 增加公司的资产总额- C. 提高每股收益(EPS)- D. 降低公司的负债比率5. 以下哪项不是影响公司资本成本的因素?- A. 公司的财务风险- B. 市场的利率水平- C. 公司的经营风险- D. 公司的行业地位二、简答题(每题10分,共20分)1. 请简述公司进行现金管理时需要考虑的主要因素。

2. 描述一下公司在进行资本预算时,如何评估一个投资项目的净现值(NPV)。

三、计算题(每题15分,共30分)1. 假设一家公司的税前利润为100万元,税率为25%,公司的债务利息为20万元,债务成本为10%。

请计算该公司的税后利润和企业价值增加值(EVA)。

2. 某公司计划进行一项投资,初始投资为500万元,预计该项目的年现金流入为120万元,持续5年。

假设公司的资本成本为10%,计算该项目的净现值(NPV)。

四、案例分析题(每题20分,共20分)某公司目前考虑发行新股来筹集资金,用于偿还现有债务和进行新的投资。

公司现有债务总额为5000万元,年利率为8%,公司希望通过发行新股筹集的资金来偿还这笔债务。

公司计划发行的股票数量为500万股,每股发行价格为10元。

请分析:- 公司发行新股后,财务杠杆的变化。

江苏高等教育自学考试公司理财真题

江苏高等教育自学考试公司理财真题The following text is amended on 12 November 2020.2015年4月江苏省高等教育自学考试 07524公司理财一、单项选择题(每小题1分.共25分)在下列每小题的四个备选答案中选出一个正确答案,并将其字母标号填入题干的括号内。

1.公司财务管理内容不包括( )A.长期投资管理 B.长期融资管理C.营运资本管理 D.业绩考核管理2.股东通常用来协调与经营者之间利益的方法主要是( )A.约束和激励 B.解聘和激励 C.激励和接收 D.解聘和接收3.假设以10%的年利率借的30000元,投资于某个寿命为10年的项目,为使该投资项目成为有利的项目,每年至少应收回的现金数额为( )(提示:(P/A,10%,10) =A.3000元 B.4882元 C.5374元 D.6000元4.甲公司平价发行5年期的公司债券,债券票面利率为10%,每半年付息一次,到期一次偿还本金。

该债券的有效年利率是( )C. 10. 25% . 5%5.-般来说,无法通过多样化投资来予以分散的风险是( )A.系统风险 B.非系统风险 C.总风险 D.公司特有风险6.证券j的风险溢价可表示为( )-rf B.j×(r m-r f) +×(r m - r f) ×r f7.可以被称为“表外融资”的是( )A.融资租赁 B.经营租赁 C.长期借款 D.新股发行8.收益性和风险性均较高的营运资本融资政策是( )A.折中型融资政策 B.激进型融资政策C.稳健型融资政策 D.混合型融资政策9.某公司上年销售收入为1000万元,若下一年产品价格会提高5%,公司销售量增长10%,所确定的外部融资占销售收入增长百分比为25%,则相应外部资金需要量为( )A. 25万元 B.25. 75万元 C.万元 D.38. 75万元10.下列各项中,不属于投资项目现金流出量的是( )A.经营付现成本 B.固定资产折旧费用C.固定资产投资支出 D.以前垫支的营运成本11.折旧具有抵税作用,由于计提折旧而减少的所得税额的计算公式为( )A.折旧额×所得税税率B.折旧额×(1-所得税税率)C.(经营付现成本十折旧率)×所得税税率D.(净利润十折旧率)×所得税税率12.存货模式下,与收益持有量成正比例关系的是( )A.现金周转期 B.现金交易成本 C.现金总成本 D.现金机会成本13. MM公司所得税模型认为,在考虑公司所得税的情况下,公司价值会随着负债比率的提高而增加,原因是( )A.财务杠杆的作用 B.总杠杆的作用C.利息可以抵税 D.利息可以税前扣除14.如果将考虑公司所得税的MM模型和CAPM模型结合起来,可以得到负债公司的股本成本等于( )A.无风险利率十经营风险溢价B.货币时间价值十经营风险溢价C.无风险利率十经营风险溢价十财务风险溢价D.无风险利率十经营风险溢价十财务风险溢价十总风险溢价15.如果BBC公司无负债时的公司价值为1000万元,经测算,该公司最佳资本结构为负债比率40%,因此准备采用股转债的方式将公司的资本结构调整为最佳资本结构,该公司所得税税率为25%。

公司理财期末考试题(A卷)

《公司理财》期末考试题(A 卷)一、判断题(共10分,每小题1分)1. 在终值与利率一定的情况下,计息期越多,复利现值就越小。

( )2. 在企业财务关系中最为重要的关系是指企业与作为社会管理者的政府有关部门、社会公众之间的关系。

( )3. 单利与复利是两种不同的计息方法,单利终值与复利终值在任何时候都不可能相等。

( )4. 发行普通股股票可以按票面金额等价发行,也可以偏离票面金额按溢价、折价发行。

( )5. 在个别资本成本一定的情况下,企业综合资本成本的高低取决于资金总额。

( )6. 某一投资方案按10%的贴现率计算的净现值大于零,那么,该方案的内含报酬率大于10%。

( )7. 就风险而言,从大到小的排列顺序为:金融证券、公司证券、政府证券。

( ) 8. 存货ABC 控制法中,C 类物资是指数量少、价值低的物质。

( ) 9. 只要公司拥有足够现金,就可以发放现金股利。

( )10.利润中心必然是成本中心,投资中心必然是利润中心,所以投资中心首先是成本中心,但利润中心并不一定都是投资中心。

( )二、单项选择题(共15分,每小题1分)1. 作为企业财务管理目标,每股利润最大化目标较之利润最大化目标的优点在于( )。

A 考虑了资金的时间价值 B 考虑了投资风险价值C 反映了创造利润与投入资本之间的关系D 能够避免企业的短期行为 2. 随单价的变动而同方向变动的是( )。

A 保本量B 保利量C 变动成本率D 单位边际贡献 3. 在期望值不同时,比较风险的大小,可采用( )。

…………………………………………………………………………………………………………………………………………………………………………………………………密……………………………封………………………………………线………………………………………A 标准差B 标准差系数C 期望值D 概率 4. 普通股每股净资产反映了普通股的( )。

公司理财考试题

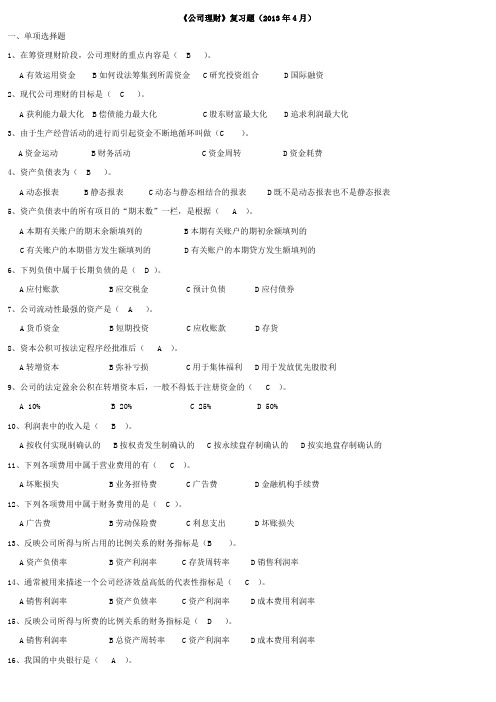

《公司理财》复习题(2013年4月)一、单项选择题1、在筹资理财阶段,公司理财的重点内容是( B )。

A有效运用资金 B如何设法筹集到所需资金 C研究投资组合 D国际融资2、现代公司理财的目标是( C )。

A获利能力最大化 B偿债能力最大化 C股东财富最大化 D追求利润最大化3、由于生产经营活动的进行而引起资金不断地循环叫做(C )。

A资金运动 B财务活动 C资金周转 D资金耗费4、资产负债表为( B )。

A动态报表 B静态报表 C动态与静态相结合的报表 D既不是动态报表也不是静态报表5、资产负债表中的所有项目的“期末数”一栏,是根据( A )。

A本期有关账户的期末余额填列的 B本期有关账户的期初余额填列的C有关账户的本期借方发生额填列的 D有关账户的本期贷方发生额填列的6、下列负债中属于长期负债的是( D )。

A应付账款 B应交税金 C预计负债 D应付债券7、公司流动性最强的资产是( A )。

A货币资金 B短期投资 C应收账款 D存货8、资本公积可按法定程序经批准后( A )。

A转增资本 B弥补亏损 C用于集体福利 D用于发放优先股股利9、公司的法定盈余公积在转增资本后,一般不得低于注册资金的( C )。

A 10%B 20%C 25%D 50%10、利润表中的收入是( B )。

A按收付实现制确认的 B按权责发生制确认的 C按永续盘存制确认的 D按实地盘存制确认的11、下列各项费用中属于营业费用的有( C )。

A坏账损失 B业务招待费 C广告费 D金融机构手续费12、下列各项费用中属于财务费用的是( C )。

A广告费 B劳动保险费 C利息支出 D坏账损失13、反映公司所得与所占用的比例关系的财务指标是(B )。

A资产负债率 B资产利润率 C存货周转率 D销售利润率14、通常被用来描述一个公司经济效益高低的代表性指标是( C )。

A销售利润率 B资产负债率 C资产利润率 D成本费用利润率15、反映公司所得与所费的比例关系的财务指标是( D )。

《公司理财》期末试卷A(含答案)

《公司理财》期末试卷A(含答案)第 2 页XXXX 学 院2015 /2016 学年第 2学期考试试卷( A )卷课程名称:公司理财 适用专业/年级:2014级会计电算化本卷共 5 页,考试方式: 闭卷 ,考试时间: 90 分钟一、单项选择题 (本题共12小题,每题2分,共24分)1.以下企业组织形式当中创立最容易维持经营固定成本最低的是( ) 。

A.个人独资企业 B.合伙制企业 C.有限责任公司 D.股份有限公司 2.公司的目标不包括以下( )。

A.生存目标 B.发展目标 C.盈利目标 D.收购目标3.资产负债率主要是反映企业的( )指标。

A.盈利能力 B.长期偿债能力 C.发展能力 D.营运能力4.企业的财务报告不包括( )。

A.现金流量表B.财务状况说明书C.利润分配表D.比较百分比会计报表 5.资产负债表不提供( )等信息。

A.资产结构B.负债水平C.经营成果D.资金来源情况6.某校准备设立永久性奖学金,每年计划颁发36000元资金,若年复利率为12%,该校现在应向银行存入( )元本金。

A .450000 B .300000 C .350000 D .3600007.债券投资中,债券发行人无法按期支付利息或本金的风险称为( )专业班级: 姓 名: 学 号:密 封装 订第3页第4页5.影响资金时间价值大小的因素主要包括()。

A.单利B.复利C.资金额D.利率和期限6.下列选项中,()可以视为年金的形式。

A.直线法计提的折旧 B.租金C.利滚利 D.保险费二、计算分析题(本题共3小题,第1题18分,第二题20分,第三题20分,共58分)1.某公司有一项付款业务,有甲乙两种付款方式可供选择。

甲方案:现在支付15万元,一次性结清。

乙方案:分5年付款,1-5年各年初的付款分别为3、3、4、4、4万元,年利率为10%。

已知:(F/A,10%,1)=(P/A,10%,1)=0.9091 (P/A,10%,3)=2.4869要求:按现值计算,选出较优方案并说明理由。

成人教育 《公司理财》期末考试复习题及参考答案

公司理财练习题A一、名词解释1、β系数1、股利政策3、资本结构4、杜邦分析法二、问答题1、证券市场线的走势受那些因素的影响?2、企业项目投资的现金流量分为几个部分?各部分的构成是什么?3、发行普通股筹资的利弊分别是什么?4、公司制企业的特点有哪些?5、企业的主营业务利润由几个部分构成,各个组成部分又包含什么内容?三、计算题1、在一项合约中,你可以有两种选择:1)从现在起的6年后收到25000元;2)从现在起的12年后收到50000元。

求:在年利率为多少时两种选择对你而言没有区别?(保留到小数点后4位)2、公司目前的资本结构为长期资本总额600万元,其中债务200万元,普通股股本400万元,每股面值100元,4万股全部发行在外,目前市场价每股300元。

债务利息10%,所得税率33%。

公司欲追加筹资200万元,有两筹资方案:甲:全部发行普通股,向现有股东配股,4配1,每股股价200元,配发一万股;乙:向银行贷款200万元,因风险增加银行要求的利息率为15%。

根据会计人员的测算,追加筹资后销售额可望达到800万元,变动成本率为50%,固定成本180万元。

求1)两方案的每股利润无差别点。

2)哪种方案为较优方案。

3同方公司的β为1.55,无风险收益率为10%,市场组合的期望收益率为13%。

目前公司支付的每股股利为2美元,投资者预期未来几年公司的年股利增长率为8%。

求:1)该股票期望收益率为多少?(保留到小数点后4位)2)确定的收益率下,该股票每股市价是多少?(保留整数)4、公司目前的资本结构为长期资本总额600万元,其中债务200万元,普通股股本400万元,每股面值100元,4万股全部发行在外,目前市场价每股300元。

债务利息10%,所得税率33%。

公司欲追加筹资200万元,有两筹资方案:甲:全部发行普通股,向现有股东配股,4配1,每股股价200元,配发一万股;乙:向银行贷款200万元,因风险增加银行要求的利息率为15%。

罗斯公司理财题库全集

Chapter 15Long-Term Financing: An Introduction Multiple Choice Questions1. The book capital of a corporation is determined by:A. the sum of the capital in excess of par and the retained earnings.B. the par value of preferred stock.C. the sum of the treasury stock and the preferred stock.D. the number of shares issued multiplied by the par value of each share.E. the market price of the company's debt.2. Retained earnings are:A. the amount of cash that the firm has saved up.B. the difference between the net income earned and the dividends paid.C. the difference between the market price of the stock and the book value.D. the amount of stock repurchased.E. None of the above.3. The book value of the shareholders' ownership is represented by:A. the sum of the par value of common stock, the capital surplus and the accumulated retained earnings.B. the total assets minus the net worth.C. the sum of the preferred stock, debt and the capital surplus.D. the sum of the total assets minus the current liabilities.E. None of the above.4. Shares of stock that have been repurchased by the corporation are called:A. treasury stock.B. undistributed capital stock.C. retained equity.D. capital surplus shares.E. None of the above.5. The market value of the ownership of the firm equals:A. the market price of the stock times the number of shares outstanding.B. the sum of the market price of the bonds and the stock.C. the par value of the stock times the number of shares outstanding.D. the market price of the stock minus the retained earnings.E. None of the above.6. A grant of authority allowing someone else to vote shares of stock that you own is called:A. a power-of-share authorization.B. a proxy.C. a share authority grant (SAG).D. a restricted conveyance.E. None of the above.7. Unsecured corporate debt is called a(n):A. indenture.B. debenture.C. bond.D. mortgage.E. None of the above.8. A standard arrangement for the orderly retirement of long-term debt calls for the corporation to make regular payments into a(n):A. custodial account.B. sinking fund.C. retirement fund.D. irrevocable trustee fund.E. None of the above9. Debt that may be extinguished before maturity is referred to as:A. sinking-fund debt.B. debentures.C. callable debt.D. indenture debt.E. None of the above.10. If a long-term debt instrument is perpetual, it is called a(n):A. secured debt issue.B. subordinated debt issue.C. consol.D. capital debt issue.E. indenture.11. The amount of loan a person or firm borrows from a lender is the:A. creditor.B. indenture.C. debenture.D. principal.E. amortization.12. The written agreement between a corporation and its bondholders is called:A. the collateral agreement.B. the deed.C. the indenture.D. the deed of conveyance.E. None of the above.13. If cumulative voting is permitted:A. the total number of votes a shareholder has is equal to the number of shares owned.B. the total number of votes a shareholder has is equal to the number of shares owned times the average number of years the shareholder has owned the shares.C. the total number of votes a shareholder has can be calculated as the number of shares owned times the number of directors to be elected.D. the total number of votes a shareholder has is equal to the number of shares times the number of board meetings the shareholder has attended.E. None of the above.14. The market-to-book value ratio is implies growth and success when it is:A. greater than 0.B. less than 10.C. less than 0.D. less than 1.E. greater than 1.15. There are 3 directors' seats up for election. If you own 1,000 shares of stock and you can cast 3,000 votes for a particular director, this is illustrative of:A. cumulative voting.B. absolute priority voting.C. sequential voting.D. straight voting.E. None of the above.16. If you own 1,000 shares of stock and you can cast only 1,000 votes fora particular director, then the stock features:A. cumulative voting.B. absolute priority voting.C. sequential voting.D. straight voting.E. None of the above.17. If a group other than management solicits the authority to vote shares to replace management, a _____ is said to occur.A. proxy fightB. stockholder derivative actionC. tender offerD. vote of confidenceE. None of the above.18. Shareholders usually have which of the following right(s)A. To elect board members, the authorizing of new shares and other matters of great importance to shareholders such as being acquired.B. To share proportionally in regular and liquidating dividends.C. To share proportionally in any new stock sold.D. All of the above.E. None of the above.19. Different classes of stock usually are issued to:A. maintain ownership control by holding the class of stock with greater voting rights.B. pay less in dividends between the classes of stock.C. fool investors into thinking that equity is equity and there is no difference in control or value features.D. extract perquisites without the other class of stockholders knowing.E. None of the above.20. Which of the following statements is falseA. Creditors do not have voting power.B. Payment on interest on debt in considered an expense, while payment of dividends is a return on capital.C. Unpaid debt is a liability of the firm, and if not paid, can result in liquidation of the firm. Unpaid common stock dividends cannot force liquidation.D. One of the costs of issuing equity is the possibility of financial distress, while no financial distress is associated with debt.E. None of the above.21. Corporations try to create hybrid securities that look like equity but are called debt because:A. debt interest expense is tax deductible.B. bankruptcy costs are eliminated or reduced.C. these securities have lower risk than debt.D. Both A and C.E. Both A and B.22. Technically speaking, a long-term corporate debt offering that features a specific attachment to corporate property is generally called:A. a debenture.B. a bond.C. a long-term liability.D. a preferred liability.E. None of the above.23. If a firm retires or extinguishes a debt issue before maturity, the specific amount they pay is:A. the amortization amount.B. the call price.C. the sinking fund amount.D. the spread premium.E. None of the above.24. If a debenture is subordinated, it:A. has a higher priority status than specified creditors.B. is secondary to equity.C. must give preference to the specified creditor in the event of default.D. has been issued because the company is in default.E. None of the above.25. Not paying the dividends on a cumulative preferred issue may result in:A. preferred dividend arrears that can be eliminated by the common shareholders only after common dividends are paid.B. voting rights are granted to preferred stockholders if preferred dividends are in arrears.C. no payment of dividends to common shareholders.D. Both A and B.E. Both B and C.26. Preferred stock has both a tax advantage and a tax disadvantage. These two are:A. in default there are no taxes and dividends are taxed in corporate hands at 70%.B. corporate dividends are taxed on 30% of the dividends received and expenses are deductible.C. dividends are not a tax-deductible expense but are 70% exempt from corporate taxation.D. dividends are fully tax deductible but are not equity capital.E. None of the above.27. Preferred stock may be desirable to issue for which of the following reason(s)A. If there is no taxable income, preferred stock does not impose a tax penalty.B. The failure to pay preferred dividends, cumulative or noncumulative, will not cause bankruptcy.C. Preferred dividends are not tax deductible and therefore will not provide a tax shield but will reduce net income.D. Both B and C.E. Both A and B.28. Preferred stock may exist because:A. losses before income taxes prevent a company from enjoying the tax advantages of debt interest while there is no tax advantage for preferred dividends.B. an advantage exists for the firm; preferred shareholders can not force the company into bankruptcy because of unpaid dividends.C. corporations get a 70% tax exemption on preferred dividends received.D. All of the above.E. None of the above.29. The written agreement between a corporation and its bondholders might contain a prohibition against paying dividends in excess of current earnings. This prohibition is an example of a(n):A. maintenance of security provision.B. collateral restriction.C. affirmative indenture.D. restrictive covenant.E. None of the above.30. What percentage of the dividends received by one corporation from another is taxableA. 15%B. 30%C. 34%D. 70%E. 100%31. Which of the following statements about preferred stock is trueA. Unlike dividends paid on common stock, dividends paid on preferred stock are a tax-deductible expense.B. Unpaid dividends on preferred stock are a debt of the corporation.C. If preferred dividends are non-cumulative, then preferred dividends not paid in a particular year will be carried forward to the next year.D. There is no difference in the voting rights of preferred and common stockholders.E. None of the above.32. If a debt issue is callable, the call price is generally ____ par.A. greater thanB. less thanC. equal toD. unrelated toE. It varies widely based on the risk of the firm.33. There was an upward trend in the ratio of the book value of debt to the book value of debt and equity throughout the 1990s. Some of this was due to the repurchasing of stock. The market value ratio of debt to debt and equity exhibited no upward trend. This can be explained by:A. the change in the accounting rules of the period.B. the difference between tax accounting and accounting for financial accounting purposes.C. a large increase in the market value of equity that was greater than the increase in debt.D. All of the above.E. None of the above.34. Based on historical experience, which of the following best describes the "pecking order" of long-term financing strategy in the .A. Long-term debt first, new common equity, internal financing last.B. Long-term debt first, internal financing, new common equity last.C. Internal financing first, new common equity, long-term borrowing last.D. Internal financing first, long-term borrowing, new common equity last.E. None of the above.35. Financial deficits are created when:A. profits and retained earnings are greater than the capital-spending requirement.B. profits and retained earnings are less than the capital-spending requirement.C. profits and retained earnings are equal to the capital-spending requirement.D. All of the above.E. None of the above.36. Financial economists prefer to use market values when measuring debt ratios because:A. market values are more stable than book values.B. market values are a better reflection of current value than historical value.C. market values are readily available and do not have to be calculated like book values.D. market values are more difficult to calculate which makes financial economists more valuable.E. None of the above.37. Corporate financial officers prefer to use book values when measuring debt ratios because:A. book values are more stable than market values.B. debt covenant restriction are usually expressed in book value terms.C. rating agencies measure debt ratios in book values terms.D. All of the above.E. None of the above.38. Rockwell Corporation had net income of $150,000 for the year ending 2008. The company decided to payout 40% of earnings per share as a dividend. Rockwell has 120,000 shares issued and outstanding. What are the retained earnings for 2008A. $40,000B. $60,000C. $90,000D. $150,000E. None of the above39. Nelson Company had equity accounts in 2008 as follows:Projected income is $150,000 and 40% of this amount will be paid out immediately as dividends. What will the ending retained earnings account beA. $90,000B. $92,000C. $122,000D. $210,000E. $242,00040. Holden Bicycles has 1,000 shares outstanding each with a par value of $. If they are sold to shareholders at $10 each, what would the capital surplus beA. $100B. $900C. $9,900D. $10,000E. $11,00041. The Lory Bookstore used internal financing as a source of long-term financing for 80% of its total needs in 2008. The company borrowed an additional 27% of its total needs in the long-term debt markets in 2008. What were Lory's net new stock issues in that yearA. -20%B. -7%C. 7%D. 20%E. 27%42. David's Building Equipment (DBE) had net income of $200,000 for the year ending 2008. The company decided to payout 30% of earnings per share as a dividend. DBE has 50,000 shares issued and outstanding. What are the retained earnings for 2008A. $60,000B. $140,000C. $150,000D. $200,000E. None of the above.43. Alexandra Investments had equity accounts in 2008 as follows:Projected income is $200,000 and 20% of this amount will be paid out immediately as dividends. What will the ending retained earnings account beA. $160,000B. $250,000C. $270,000D. $410,000E. $470,00044. Michael's Motor Scooters has 1,000 shares outstanding each with a par value of $. If they are sold to shareholders at $5 each, what would the capital surplus beA. $4,400B. $4,500C. $4,750D. $4,950E. $5,00045. Calhoun Computech used internal financing as a source of long-term financing for 80% of its total needs in 2008. The company borrowed an additional 15% of its total needs in the long-term debt markets in 2008. What were Calhoun's net new stock issues, in percentage terms, for 2008A. -10%B. -5%C. 5%D. 10%E. 15%Essay QuestionsInformation on shareholder's equity as currently shown on the books of the Eaton Corporation is given as:46. From this information, calculate Eaton's book value per share.47. Rework the shareholder's equity as it appears on the books if the company issues 40,000 new shares of common at $70 per share.48. Preferred Stock, as a hybrid security, presents somewhat of a puzzle as to why they are issued. What elements give rise to the puzzle and how is it explained49. Different countries have different sources of funds. For example, in the United States, internally generated funds count for over 4/5 of all funds while in Japan, it is about ½ with externally generated funds making up the remainder. The disparities are less in the United Kingdom and Germany, with about 2/3 of funds coming from internal sources. Discuss this disparity and why it might exist.Chapter 15 Long-Term Financing: An Introduction Answer KeyMultiple Choice Questions1. The book capital of a corporation is determined by:A.the sum of the capital in excess of par and the retained earnings.B.the par value of preferred stock.C.the sum of the treasury stock and the preferred stock.D.the number of shares issued multiplied by the par value of each share.E.the market price of the company's debt.Difficulty level: EasyTopic: BOOK CAPITALType: DEFINITIONS2. Retained earnings are:A.the amount of cash that the firm has saved up.B.the difference between the net income earned and the dividends paid.C.the difference between the market price of the stock and the book value.D.the amount of stock repurchased.E.None of the above.Difficulty level: EasyTopic: RETAINED EARNINGSType: DEFINITIONS3. The book value of the shareholders' ownership is represented by:A.the sum of the par value of common stock, the capital surplus and the accumulated retained earnings.B.the total assets minus the net worth.C.the sum of the preferred stock, debt and the capital surplus.D.the sum of the total assets minus the current liabilities.E.None of the above.Difficulty level: MediumTopic: BOOK VALUEType: DEFINITIONS4. Shares of stock that have been repurchased by the corporation are called:A.treasury stock.B.undistributed capital stock.C.retained equity.D.capital surplus shares.E.None of the above.Difficulty level: EasyTopic: TREASURY STOCKType: DEFINITIONS5. The market value of the ownership of the firm equals:A.the market price of the stock times the number of shares outstanding.B.the sum of the market price of the bonds and the stock.C.the par value of the stock times the number of shares outstanding.D.the market price of the stock minus the retained earnings.E.None of the above.Difficulty level: EasyTopic: MARKET VALUE OF EQUITYType: DEFINITIONS6. A grant of authority allowing someone else to vote shares of stock that you own is called:A. a power-of-share authorization.B. a proxy.C. a share authority grant (SAG).D. a restricted conveyance.E.None of the above.Difficulty level: EasyTopic: PROXYType: DEFINITIONS7. Unsecured corporate debt is called a(n):A.indenture.B.debenture.C.bond.D.mortgage.E.None of the above.Difficulty level: EasyTopic: DEBENTUREType: DEFINITIONS8. A standard arrangement for the orderly retirement of long-term debt calls for the corporation to make regular payments into a(n):A.custodial account.B.sinking fund.C.retirement fund.D.irrevocable trustee fund.E.None of the aboveDifficulty level: EasyTopic: SINKING FUNDType: DEFINITIONS9. Debt that may be extinguished before maturity is referred to as:A.sinking-fund debt.B.debentures.C.callable debt.D.indenture debt.E.None of the above.Difficulty level: EasyTopic: CALLABLE DEBTType: DEFINITIONS10. If a long-term debt instrument is perpetual, it is called a(n):A.secured debt issue.B.subordinated debt issue.C.consol.D.capital debt issue.E.indenture.Difficulty level: EasyTopic: CONSOL OR PERPETUAL DEBTType: DEFINITIONS11. The amount of loan a person or firm borrows from a lender is the:A.creditor.B.indenture.C.debenture.D.principal.E.amortization.Difficulty level: EasyTopic: LOAN PRINCIPALType: DEFINITIONS12. The written agreement between a corporation and its bondholders is called:A.the collateral agreement.B.the deed.C.the indenture.D.the deed of conveyance.E.None of the above.Difficulty level: EasyTopic: INDENTUREType: DEFINITIONS13. If cumulative voting is permitted:A.the total number of votes a shareholder has is equal to the number of shares owned.B.the total number of votes a shareholder has is equal to the number of shares owned times the average number of years the shareholder has owned the shares.C.the total number of votes a shareholder has can be calculated as the number of shares owned times the number of directors to be elected.D.the total number of votes a shareholder has is equal to the number of shares times the number of board meetings the shareholder has attended.E.None of the above.Difficulty level: EasyTopic: CUMULATIVE VOTINGType: CONCEPTS14. The market-to-book value ratio is implies growth and success when it is:A.greater than 0.B.less than 10.C.less than 0.D.less than 1.E.greater than 1.Difficulty level: MediumTopic: MARKET-TO-BOOK RATIOType: CONCEPTS15. There are 3 directors' seats up for election. If you own 1,000 shares of stock and you can cast 3,000 votes for a particular director, this is illustrative of:A.cumulative voting.B.absolute priority voting.C.sequential voting.D.straight voting.E.None of the above.Difficulty level: EasyTopic: CUMULATIVE VOTINGType: CONCEPTS16. If you own 1,000 shares of stock and you can cast only 1,000 votes fora particular director, then the stock features:A.cumulative voting.B.absolute priority voting.C.sequential voting.D.straight voting.E.None of the above.Difficulty level: EasyTopic: STRAIGHT VOTINGType: CONCEPTS17. If a group other than management solicits the authority to vote shares to replace management, a _____ is said to occur.A.proxy fightB.stockholder derivative actionC.tender offerD.vote of confidenceE.None of the above.Difficulty level: EasyTopic: PROXY FIGHTType: CONCEPTS18. Shareholders usually have which of the following right(s)A.To elect board members, the authorizing of new shares and other matters of great importance to shareholders such as being acquired.B.To share proportionally in regular and liquidating dividends.C.To share proportionally in any new stock sold.D.All of the above.E.None of the above.Difficulty level: EasyTopic: SHAREHOLDER RIGHTSType: CONCEPTS19. Different classes of stock usually are issued to:A.maintain ownership control by holding the class of stock with greater voting rights.B.pay less in dividends between the classes of stock.C.fool investors into thinking that equity is equity and there is no difference in control or value features.D.extract perquisites without the other class of stockholders knowing.E.None of the above.Difficulty level: MediumTopic: CLASSES OF STOCKType: CONCEPTS20. Which of the following statements is falseA.Creditors do not have voting power.B.Payment on interest on debt in considered an expense, while payment of dividends is a return on capital.C.Unpaid debt is a liability of the firm, and if not paid, can result in liquidation of the firm. Unpaid common stock dividends cannot force liquidation.D.One of the costs of issuing equity is the possibility of financial distress, while no financial distress is associated with debt.E.None of the above.Difficulty level: MediumTopic: COSTS OF LONG TERM FINANCINGType: CONCEPTS21. Corporations try to create hybrid securities that look like equity but are called debt because:A.debt interest expense is tax deductible.B.bankruptcy costs are eliminated or reduced.C.these securities have lower risk than debt.D.Both A and C.E.Both A and B.Difficulty level: MediumTopic: HYBRID SECURITIESType: CONCEPTS22. Technically speaking, a long-term corporate debt offering that features a specific attachment to corporate property is generally called:A. a debenture.B. a bond.C. a long-term liability.D. a preferred liability.E.None of the above.Difficulty level: EasyTopic: BONDType: CONCEPTS23. If a firm retires or extinguishes a debt issue before maturity, the specific amount they pay is:A.the amortization amount.B.the call price.C.the sinking fund amount.D.the spread premium.E.None of the above.Difficulty level: EasyTopic: CALLABLE DEBTType: CONCEPTS24. If a debenture is subordinated, it:A.has a higher priority status than specified creditors.B.is secondary to equity.C.must give preference to the specified creditor in the event of default.D.has been issued because the company is in default.E.None of the above.Difficulty level: MediumTopic: SUBORDINATED DEBENTUREType: CONCEPTS25. Not paying the dividends on a cumulative preferred issue may result in:A.preferred dividend arrears that can be eliminated by the common shareholders only after common dividends are paid.B.voting rights are granted to preferred stockholders if preferred dividends are in arrears.C.no payment of dividends to common shareholders.D.Both A and B.E.Both B and C.Difficulty level: MediumTopic: PREFERRED STOCK AND DIVIDENDSType: CONCEPTS26. Preferred stock has both a tax advantage and a tax disadvantage. These two are:A.in default there are no taxes and dividends are taxed in corporate hands at 70%.B.corporate dividends are taxed on 30% of the dividends received and expenses are deductible.C.dividends are not a tax-deductible expense but are 70% exempt from corporate taxation.D.dividends are fully tax deductible but are not equity capital.E.None of the above.Difficulty level: MediumTopic: PREFERRED STOCKType: CONCEPTS27. Preferred stock may be desirable to issue for which of the following reason(s)A.If there is no taxable income, preferred stock does not impose a tax penalty.B.The failure to pay preferred dividends, cumulative or noncumulative, will not cause bankruptcy.C.Preferred dividends are not tax deductible and therefore will not provide a tax shield but will reduce net income.D.Both B and C.E.Both A and B.Difficulty level: ChallengeTopic: PREFERRED STOCKType: CONCEPTS28. Preferred stock may exist because:A.losses before income taxes prevent a company from enjoying the tax advantages of debt interest while there is no tax advantage for preferred dividends.B.an advantage exists for the firm; preferred shareholders can not force the company into bankruptcy because of unpaid dividends.C.corporations get a 70% tax exemption on preferred dividends received.D.All of the above.E.None of the above.Difficulty level: MediumTopic: PREFERRED STOCKType: CONCEPTS29. The written agreement between a corporation and its bondholders might contain a prohibition against paying dividends in excess of current earnings. This prohibition is an example of a(n):A.maintenance of security provision.B.collateral restriction.C.affirmative indenture.D.restrictive covenant.E.None of the above.Difficulty level: EasyTopic: RESTRICTIVE COVENANTType: CONCEPTS30. What percentage of the dividends received by one corporation from another is taxableA.15%B.30%C.34%D.70%E.100%Difficulty level: EasyTopic: TAXABLE CORPORATE DIVIDENDSType: CONCEPTS31. Which of the following statements about preferred stock is trueA.Unlike dividends paid on common stock, dividends paid on preferred stock are a tax-deductible expense.B.Unpaid dividends on preferred stock are a debt of the corporation.C.If preferred dividends are non-cumulative, then preferred dividends not paid in a particular year will be carried forward to the next year.D.There is no difference in the voting rights of preferred and common stockholders.E.None of the above.Difficulty level: MediumTopic: PREFERRED STOCKType: CONCEPTS32. If a debt issue is callable, the call price is generally ____ par.A.greater thanB.less thanC.equal toD.unrelated toE.It varies widely based on the risk of the firm.Difficulty level: EasyTopic: CALLABLE DEBTType: CONCEPTS33. There was an upward trend in the ratio of the book value of debt to the book value of debt and equity throughout the 1990s. Some of this was due to the repurchasing of stock. The market value ratio of debt to debt and equity exhibited no upward trend. This can be explained by:A.the change in the accounting rules of the period.B.the difference between tax accounting and accounting for financial accounting purposes.C. a large increase in the market value of equity that was greater than the increase in debt.D.All of the above.E.None of the above.Difficulty level: EasyTopic: DEBT FINANCING TRENDSType: CONCEPTS。

公司理财期末考试复习

公司理财期末考试复习金融10-1 乐云201005001608第1章公司理财导论1、公司治理(笔记)1)并购交易2)职业经理人市场3)投资者法律保护4)政治与金融;政治的质量5)文化与金融6)金融分析师7)发达的中介机构8)新闻媒体第4章折现现金流量估价1、复利:FV=(1+)2、永续年金:PV= 永续增长年金:PV=年金:PV=[1-]FV= [(1+r)-1]增长年金:PV=[1—()]第5章净现值和投资评价的其他方法1)净现值法则:接受净现值大于0的项目,拒绝净现值为负的项目2)回收期法(适用于小型企业)优点:决策过程简单缺点:回收期决策标准确定的主观臆断、无视回收期后的现金流量、忽略了货币时间价值。

3)内部收益法(适用条件:未来现金流是正值)例:NPV=—100+ (NPV取0时,R=?)若内部收益率大于折现率,项目可以接受;若内部收益率小于折现率,项目不可以接受。

缺点:内部收养法忽略了“规模问题"4)盈利指数法盈利指数(PI)=初始投资所带来的的后续现金流量的现值/初始投资若PI〉1,则可行。

5)平均会计回收法AAR=平均净收益/平均投资的账目价值优点:会计信息通常是可得到的容易测算缺点:忽略了时间价值,依赖账面价值。

第6章投资决策(老师没有讲)1、实际利率=1+名义利率/1+通货膨胀—1第7章风险分析、实物期权和资本预算1、敏感性分析1)计算NPV,需知条件:期初成本、未来现金流、贴现率2)敏感分析法提供了在不同假设下的NPV,从而有利于经理更好地察觉项目的风险。

3)敏感分析法只在同一时间修正一个变量,而在现实中,许多变量很有可能是联合变动的。

2、场景分析法1)在不同场景下项目的表现。

2)操作性不强3、盈亏平衡法1)计算出项目盈亏平衡时所应实现的销售量2)帮助经理了解项目在亏损前做出错误的预测的危害性3)适用于工业4、实物期权1)拓展期权2)放弃期权3)择机期权5、决策树是对项目中的隐含期权和实物期权进行评估的方法。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

公司理财复习题(小小)注:本人在百忙之中经过几天几夜整理,只求考试过关,难免有差错和漏洞.红色部分为不知道答案部份.请各位同学再汇总一下.并在群中分享,谢谢!1.企业组织形态中的单一业主制和合伙制有哪四个主要的缺点?这两种企业组织形态相对公司形态而言,有哪些优点?答:单一业主制企业的缺点虽然单一业主制有如上的优点,但它也有比较明显的缺点。

一是难以筹集大量资金。

因为一个人的资金终归有限,以个人名义借贷款难度也较大。

因此,单一业主制限制了企业的扩展和大规模经营。

二是投资者风险巨大。

企业业主对企业负无限责任,在硬化了企业预算约束的同时,也带来了业主承担风险过大的问题,从而限制了业主向风险较大的部门或领域进行投资的活动。

这对新兴产业的形成和发展极为不利。

三是企业连续性差。

企业所有权和经营权高度统一的产权结构,虽然使企业拥有充分的自主权,但这也意味着企业是自然人的企业,业主的病、死,他个人及家属知识和能力的缺乏,都可能导致企业破产。

四是企业内部的基本关系是雇佣劳动关系,劳资双方利益目标的差异,构成企业内部组织效率的潜在危险。

合伙制企业的缺点然而,合伙制企业也存在与单一业主制企业类似的缺陷。

一是合伙制对资本集中的有限性。

合伙人数比股份公司的股东人数少得多,且不能向社会集资,故资金有限。

二是风险性大。

强调合伙人的无限连带责任,使得任何一个合伙人在经营中犯下的错误都由所有合伙人以其全部资产承担责任,合伙人越多,企业规模越大,每个合伙人承担的风险也越大,合伙人也就不愿意进行风险投资,进而妨碍企业规模的进一步扩大。

三是合伙经营方式仍然没有简化自然人之间的关系。

由于经营者数量的增加,在显示出一定优势的同时,也使企业的经营管理变得较为复杂。

合伙人相互间较容易出现分歧和矛盾,使得企业内部管理效率下降,不利于企业的有效经营。

单一业主制企业的优点单一业主制企业是企业制度序列中最初始和最古典的形态,也是民营企业主要的企业组织形式。

其主要优点为:一是企业资产所有权、控制权、经营权、收益权高度统一。

这有利于保守与企业经营和发展有关的秘密,有利于业主个人创业精神的发扬。

二是企业业主自负盈亏和对企业的债务负无限责任成为了强硬的预算约束。

企业经营好坏同业主个人的经济利益乃至身家性命紧密相连,因而,业主会尽心竭力地把企业经营好。

三是企业的外部法律法规等对企业的经营管理、决策、进入与退出、设立与破产的制约较小。

合伙制企业的优点合伙制作为一种联合经营方式,在经营上具有的主要优点有:一是出资者人数的增加,从一定程度上突破了企业资金受单个人所拥有的量的限制,并使得企业从外部获得贷款的信用能力增强、扩大了企业的资金来源。

这样不论是企业的内部资金或外部资金的数量均大大超过单一业主制企业,有利于扩大经营规模。

二是由于风险分散在众多的所有者身上,使合伙制企业的抗风险能力较之单一业主制企业大大提高。

企业可以向风险较大的事业领域拓展,拓宽了企业的发展空间。

三是经营者即出资者人数的增加,突破了单个人在知识、阅历、经验等方面的限制。

众多的经营者在共同利益驱动下,集思广益,各显其长,从不同的方面进行企业的经营管理,必然会有助于企业经营管理水平的提高。

2.公司组织形态有哪些主要优点?举出至少两条公司组织的优点。

(见第一题答案)3.在公司组织形态中存在代理关系的主要原因是什么?在这种背景下,可能产生什么问题?答:股东与管理层之间的关系称为代理关系。

只要一个人(委托人)雇佣另外一个人(代理人)代表他的利益,就会存在这种代理关系.例如,当你离开学校时,你或许会雇佣某人(代理人)卖掉你的汽车.在所有这种关系中,委托人和代理人的利益都有冲突的可能.这种冲突称为代理问题.4. 股票价值最大化的目标会与诸如避免不道德或违法行为等其他目标发生冲突吗?特别是,你是否认为像客户和职工的安全、环境和良好的社会等主题符合这一框架,或者它们本来就被忽视了?试着用一些具体情况来说明你的答案。

答:1:公司股票价值的最大化目标与不道德,违法等情况是不发生冲突的。

更确切的来说是因时而论的,比如说这次经济危机中万科房子降价,相对于已购房产的客户是不道德的,但就事实和大的环境而论也是不可避免的,这就是自然法则,要生存要实现公司价值最大化,股票价值最大化,就不得不做出的让步,从长远的方向来说是好的。

2:客户和职工的安全、良好的生态环境和社会环境是绝对符合这一框架的。

它们与公司价值的最大化,公司股票价值的最大化是相辅相成的。

仍以万科为例:在这次经济危机中,万科该撤项的撤,该降价的降。

在这一过程中,肯定会伤害到已购房产客户和员工的感情!但是我们把目光投向更远的方向去看,就是万科存活下来了,之后更树立了良好的社会形象。

5. 流动性衡量的是什么?解释一家企业面临高流动性和低流动性时的取舍。

答:流动性指的是资产转换成现金的速度和难易程度。

流动性包含两个层面,转换的难易程度和价值的损失。

只要把价格降得足够低,任何资产都能迅速转换成现金。

因而流动性高的资产是指那些很快脱手而且没有重大价值损失的资产。

流动性低的资产则是那些不大幅度降价就无法迅速转换成现金的资产。

6.假设一个公司在特定时期来自资产的现金流量为负值,它是不是一定就是一种好的迹象或者坏的迹象?7. 假设一个公司在多年经营中经营现金流量为负值,它是不是一定就是一种好的迹象或者坏的迹象?(同6题一样,原题)8. 企鹅冰球(Penguin Pucks)公司的流动资产为5 000美元,固定资产净值为23 000美元,流动负债为4 300美元,长期债务为13 000美元。

该企业股东权益的价值是多少?净营运资本是多少?9. Papa Roach Exterminators公司的销售收入为527 000美元,成本为280 000美元,折旧费为38 000美元,利息费用为15 000美元,税率为35%。

该企业的净利润是多少?假设企业支付了48 000美元的现金股利,新增的留存收益是多少?假设企业发行在外的普通股股数为30 000股,EPS是多少?每股股利是多少?10. 请解释一个企业的流动比率等于0.50意味着什么。

如果这家企业的流动比率为1.50,是不是更好一些?如果是15.0呢?解释你的答案。

答:流动比率是流动资产对流动负债的比率,用来衡量企业流动资产在短期债务到期以前,可以变为现金用于偿还负债的能力。

一般而言,流动比率的高低与营业周期很有关系:营业周期越短,流动比率就越低;反之,则越高。

一个企业的流动比率等于0.50,即流动比率小于1,说明资金流动性差,意味着净营运资本(流动资产减去流动负债)是负债,这在一个健康的企业里是很少见的;1.5<流动比率<2,资金流动性一般;流动比率为15,意味着资金流动性好。

11. 请全面解释下列财务比率能够提供企业的哪些方面的信息:a. 速动比率;b. 现金比率;c. 总资产周转率;d. 权益乘数;答:A、速动比率,又称“酸性测验比率”,是指速动资产对流动负债的比率。

它是衡量企业流动资产中可以立即变现用于偿还流动负债的能力。

速动资产包括货币资金、短期投资、应收票据、预付账款、应收账款、其他应收款项等,可以在较短时间内变现。

而流动资产中存货、1年内到期的非流动资产及其他流动资产等则不应计入。

速动比率的高低能直接反映企业的短期偿债能力强弱,它是对流动比率的补充,并且比流动比率反映得更加直观可信。

如果流动比率较高,但流动资产的流动性却很低,则企业的短期偿债能力仍然不高。

B、现金比率=(货币资金+有价证券)÷流动负债现金比率通过计算公司现金以及现金等价资产总量与当前流动负债的比率,来衡量公司资产的流动性。

现金比率是速动资产扣除应收帐款后的余额。

速动资产扣除应收帐款后计算出来的金额,最能反映企业直接偿付流动负债的能力。

现金比率一般认为20%以上为好。

但这一比率过高,就意味着企业流动负债未能得到合理运用,而现金类资产获利能力低,这类资产金额太高会导致企业机会成本增加。

C、总资产周转率是考察企业资产运营效率的一项重要指标,体现了企业经营期间全部资产从投入到产出的流转速度,反映了企业全部资产的管理质量和利用效率。

通过该指标的对比分析,可以反映企业本年度以及以前年度总资产的运营效率和变化,发现企业与同类企业在资产利用上的差距,促进企业挖掘潜力、积极创收、提高产品市场占有率、提高资产利用效率、一般情况下,该数值越高,表明企业总资产周转速度越快。

销售能力越强,资产利用效率越高。

总资产周转率(次)=主营业务收入净额/平均资产总额X100%。

D、权益乘数又称股本乘数,是指资产总额相当于股东权益的倍数。

权益乘数较大,表明企业负债较多,一般会导致企业财务杠杆率较高,财务风险较大,在企业管理中就必须寻求一个最优资本结构,以获取适当的 EPS/CEPS,从而实现企业价值最大化。

权益乘数=资产总额/股东权益总额即=1/(1-资产负债率).12.计算流动性比率SDJ公司的净营运资本为1 320美元,流动负债为4 460美元,存货为1 875美元。

它的流动比率是多少?速动比率是多少?答:流动比率=流动资产/流动负债=1320/4460=0.30倍;速动比率=流动负债—存货/流动负债=4460—1875/4460=0.58倍13. 计算获利能力比率Timber Line公司的销售收入为2 900万美元,资产总额为3 700万美元,债务总额为1 300万美元。

如果利润率为9%,净利润是多少?ROA是多少?ROE是多少?答:利润率=净利润/销售收入=》净利润=9%*2900=261万美元;资产报酬率(ROA)=净利润/资产总额=261/3700=7%;权益报酬率(ROE)=净利润/权益总额=261/1300=20%。

14. 杜邦恒等式假如Roten Rooters公司的权益乘数为1.75,总资产周转率为1.30,利润率为8.5%,它的ROE是多少?答:权益报酬率(ROE)=利润率*总资产周转率*权益乘数=8.5%*1.30*1.75=19%.15. 杜邦恒等式Forester防火公司的利润率为9.20%,总资产周转率为1.63,ROE为18.67%。

该企业的债务权益率是多少?答: 权益报酬率(ROE)=利润率*总资产周转率*权益乘数=>18.67%=9.20%*1.63*权益乘数=>权益乘数=18.67%/9.2%*1.63=1.24.;权益乘数=1/1-资产负债率=1.24 =》资产负债率=19%,;债务权益率=19/81=23.45%16.你认为为什么大多数长期财务计划的制定都从销售收入预测开始?换句话说,为什么未来的销售收入是关键的输入因素?答:销售预测是指对未来特定时间内,全部产品或特定产品的销售数量与销售金额的估计。