《会计评论》(美国会计学会)2004年5-6期目录(PDF X页)

会计研究动态文摘

《会计研究动态》(第14期)--如何评价美国FASB的财务会计概念框架文摘共81 篇会计基本理论(9 篇) (4)如何评价美国FASB的财务会计概念框架 (4)分配权能对应与会计行为异化. (4)关于会计计量的几个理论问题. (5)资产概念的本质、定义与特征. (6)中国会计研究成效问题分析—以《会计研究》(1980-2002)为样本 (7)论资产计量. (7)XBRL 一种多功能的工具(XBRL: A multitalented tool ) (8)一项关于私人公司GAAP的调查(The Case for private company GAAP) (8)论法务会计发展误区与学科建设难点. (9)会计准则与制度(8篇) (10)中国会计制度的变迁与发展. (10)《会计法》的立法创新及其影响. (10)经济转型国家的公众公司财务报告架构改革. (11)我国上市公司财务报告法律责任的问卷调查及分析 (12)国际公共部门会计准则的回顾、基本框架及其启示 (13)公众公司财务报告的披露、分析与解释机制. (14)会计商誉与经济商誉的差异研究. (14)我国收益报告改革探讨. (15)成本管理会计(1 篇) (17)管理会计理论框架的研究. (17)公司理财(13 篇) (18)有效市场理论的思考——兼论传统金融学与行为金融学的分歧18 关于财务管理理论体系起点的探讨. (18)国外财务管理理论的比较和启示. (19)有控制权利益的企业融资工具选择. (20)中小高科技企业R&D融资问题探讨 (21)公司相互持股与中国企业改革——对发展条件、利弊影响及管制对策的分析22 负债融资、负债来源与企业投资行为一一来自中国上市公司的经验证据23 市场化程度、政府干预与企业债务期限结构——来自我国上市公司的经验证据 (23)国际财务公司的发展趋势 (24)中国股市现金股利悖论研究 (25)幕交易的限制与分析师跟踪分析公司的动机 (26)战略控股过程:目标企业所有权结构的影响研究 (26)行业特征与资本结构研究 (27)审计(9 篇) (29)财务重述与独立审计质量 (29)审计报告虚假述民事赔偿保障制度建立与完善 (29)基于科学发展观的国有企业领导干部离任审计 (30)上市公司审计、财务困境与会计师事务所更迭一一基于2002〜2003上市公司数据的实证研究 (30)上市公司盈余管理与审计质量的相关分析. (31)以组织发展与战略管理为背景的部审计外包研究 (32)审计技术革命与帕累托改进. (32)注册会计师保证服务的发展与研究. (33)同业复核日渐兴旺. (34)会计教育(5 篇) (35)办好会计硕士专业学位教育开创我国高级会计人才培养新局面 (35)美国会计教育改革及其对我国的启示. (35)试析会计教育改革. (36)ERP实验教学改革探微 (37)ERP模拟企业管理实验教学存在的问题及对策 (37)政府与非营利组织会计(2 篇) (39)谈我国政府财务会计与预算会计的协调. (39)民间非营利组织会计监管失效的原因及其相关措施 (39)会计盈余管理(5 篇) (41)资本市场压力、披露频率导致的盈余/ 现金流量冲突和管理近视症 (41)会计变更、盈余管理与企业财务特征——来自中国上市公司的经验证据41 盈余的预期管理与盈余管理. (42)盈余管理与会计域秩序. (43)亏损上市公司会计盈余价值相关性实证研究. (44)公司治理(10 篇) (46)关联交易、公司治理与国有股改革——来自我国资本市场的实证证据46 论企业财权配置——基于公司治理理论发展视角 (46)外部会计师事务所是否能在新兴市场发挥公司治理的作用 (47)独立董事说“不”有信息增加量吗. (48)公司董事会的变脸. (49)论职工参与企业治理的经济学分析. (50)中国上市公司CFO制度影响因素的实证分析 (50)论审计委员会效率之改进. (51)募集资金变更与公司治理. (52)财务视角下公司治理效率探析. (53)业绩评价预算与控制(9 篇) (54)和谐监管浅论. (54)企业绩效评价主体的演进及其对绩效评价的影响 (54)经理人股票期权制度:熵值分析. (55)基于执行的部控制评价体系构建之探讨. (56)部控制与部审计研究. (56)论财务监督制度化. (57)企业集团预算控制模式及其选择. (57)基于科学发展观的企业三重绩效评价模型. (58)契约激励、信息共享与供应链的动态协调. (59)英文杂志目录. (60)《会计评论》2005 年第4 期(The Accounting Review ,April 2005 Issue ).. 60 《会计视野》2005 年第6 期(Accounting Horizons ,June 2005 Issue ) (60)《会计师杂志》2005 年5 月(Journal of accountancy, May 2005) .. 61《证券投资管理》2005 年第2 期,总第31 卷( The Journal Portfolio Management, Volume 31, No.2,2005 ) . (61)文献索引( 112 条) (62)会计基本理论(9 篇)如何评价美国FASB的财务会计概念框架财务会计概念框架是由美国FASB首创的。

主要会计专业期刊简表

主要会计专业期刊简表《爱尔兰会计》(Accountancy Ireland,简称AI),爱尔兰特许会计师协会(The Institute of Chartered Accountants in Ireland,简称ICAI)1969年6月创办。

《财务经济学》(Journal of Financial Economics,简称JFE),罗彻斯特大学(University of Rochester)威廉·西蒙工商管理研究院于1973年创办。

《财务研究评论》(The Review of Financial Studies,简称RFS),美国财务研究会(Society for Financial Studies)于1988年创办,牛津大学出版社出版。

《财务与数量分析杂志》(Journal of Financial and Quantitative Analysis,简称JFQA),美国华盛顿大学迈克尔·G.福斯特商学院(School of Business Administration,University of Washington)主办、犹他州大学大卫·埃克尔斯商学院和新西兰纽约克大学伦纳德北·N.斯特恩商学院协办,于1965年创办。

《当代会计研究》(Contemporary Accounting Research,简称CAR),加拿大会计学会(The Canadian Academic Accounting Association,简称CAAA)于1984年秋季创办。

《公共利益会计前沿》(Advances in Public Interest Accounting,简称APIA),JAI出版社1986年办。

《公司会计与财务》(The Journal of Corporate Accounting and Finance,简称JCAF),约翰·威利和森斯出版公司(John Wiley&Sons,Inc)于1989年创办。

CSSCI来源期刊目录(2004-2005年)

公告

南京大学中国社会科学研究评价中心咨询委员会于2004年4月在成都召开会议,对CSSCI来源期刊的调整进行了讨论。

经过一系列的工作和相关程序,对因停刊、合并及不符合CSSCI来源期刊收录原则的以及根据1998-2001年4年的期刊影响因子平均值分学科排序位于该学科应选期刊总数之外的,按照末位淘汰的原则,对原有的18种期刊作了删除,并在来源期刊总量上增加了42种,最后按影响因子的位序增补了位于相关学科前列的60种期刊,经调整后CSSCI来源期刊为461种,现予以公布。

南京大学中国社会科学研究评价中心

2004年9月22日

CSSCI来源期刊(2004-2005)学科分类

CSSCI来源期刊(2004-2005)

(共461种)

管理学(26种)

马克思主义(13种)

哲学(11种)

宗教学(4种)

语言学(19种)

中国文学(15种)

外国文学(6种)

艺术学(17种)

历史学(26种)

考古学(7种)

经济学(69种)

政治学(含:国际问题、台港澳问题)(36种)

法学(21种)

社会学(8种)

民族学(12种)

新闻学与传播学(14种)

图书馆、情报与文献学(20种)

教育学(30种)

体育学(7种)

统计学(4种)

心理学(7种)

综合性社科期刊(39种)

高校综合性社科学报(35种)

人文、经济地理(8种)

环境科学(7种)。

会计学方面学科导论

(4).会计准则国际化---- IASC、IASB1973年,由澳大利亚、加拿大、法国、德国、日本、墨西哥、荷兰、英国、爱尔兰和美国的16个职业会计团体发起成立了国际会计准则委员会(IASC)。其宗旨是要制定和发布为各国、各地区所承认并遵守的国际会计准则,促进国际会计的协调。其成员已发展到包括104个国家的143个会计职业组织。IASC已发布了39号国际会计准则,并公布了一系列“征求意见稿”。经过IASC的努力,国际会计准则日益完善并得到各国会计界的支持与认我国也于1998年5月正式加入IASC和国际会计师联合会。张为国教授从2007年7月1日开始担任国际会计准则理事会理事,这是国际会计准则理事会代表亚洲和新兴市场的第二位理事,也是该理事会首位来自中国的理事。 2001年,根据会计国际协调工作的需要,国际会计准则委员会(IASC)正式改组为国际会计准则理事会(IASB)。

(1).财务会计侧重于对企业外部利益相关者提供有助于决策的信息,而管理会计侧重于为企业内部经营管理者提供相关信息;(2).财务会计强调过去,而管理会计则强调未来;(3).财务会计受公认会计原则的制约,而管理会计不受公认会计原则的制约。管理会计主要考虑经营管理决策的成本效益与行为问题;(4).财务会计以某一会计主体为核心,而管理会计强调责任单位,根据需要可将一个部门或一条生产线作为主体,甚至可将一个人作为主体;(5).财务会计是一种强制性的会计信息系统,必须按有关规定定期提供财务报表,而管理会计则是非强制性信息系统,根据决策的需要而提供相关信息;(6).管理会计是一门综合性交叉学科,与财务会计相比,它更多地涉及其他相关学科如管理学、统计学、决策科学、行为科学等。

会计期刊发表有哪些

会计期刊发表有哪些会计期刊是指专门刊载会计学科相关研究成果的学术期刊,它是会计学者们交流学术观点、分享研究成果、探讨学术问题的重要平台。

在当前学术界,会计期刊的发表对于会计学者来说具有非常重要的意义,因为它不仅可以增加学者的学术影响力,还可以推动学科的发展和进步。

那么,会计期刊都有哪些呢?接下来,我们将介绍几种比较知名的会计期刊。

首先,美国会计协会出版的《会计评论》(The Accounting Review)是全球知名的会计期刊之一,它创刊于1926年,是美国会计学会(American Accounting Association)的官方期刊。

《会计评论》涵盖了会计学科的各个领域,包括财务会计、管理会计、审计、税务等内容。

该期刊以其高质量的论文和严谨的学术态度而闻名,发表在《会计评论》上的论文往往具有很高的学术影响力。

其次,国际会计学会(International Association for Accounting Education and Research)出版的《会计研究杂志》(Journal of Accounting Research)也是一本备受推崇的会计期刊。

该期刊创刊于1963年,以推动会计学科的研究和发展为宗旨,致力于发表高水平的会计学术研究成果。

《会计研究杂志》涵盖了会计理论、审计、财务报告、公司治理等多个方面的研究内容,是会计学者们交流学术观点、展示研究成果的重要平台。

此外,国际会计学会出版的《管理会计研究》(Journal of Management Accounting Research)也是一本备受关注的会计期刊。

该期刊创刊于1989年,专注于管理会计领域的研究,包括成本管理、绩效评价、预算管理等内容。

《管理会计研究》以其前沿的研究视角和独特的学术观点而备受学者们的青睐,发表在该期刊上的论文往往能够引起学术界的广泛关注。

除了上述几本知名的会计期刊外,还有一些其他的会计期刊也备受学者们的关注,比如《会计与金融》(Accounting and Finance)、《会计研究》(AccountingResearch Journal)等。

会计模式研究美国会计模式对我国的启示的论文-会计研究论文

会计模式研究美国会计模式对我国的启示的论文会计研究论文[摘要]:会计模式所描述的是会计实务,通过对会计模式的研究探讨我国会计的发展方向。

本文从会计模式的研究目的和意义,会计模式的影响因素,美国会计模式研究对我国的启示和借鉴等方面展开论述。

[关键字]:会计模式影响因素美国模式启示与借鉴一、研究的目的和意义会计模式是各国在经济发展和会计实践中不断进行的经验总结,是一种定型的形式。

对我国的会计实务具有指导和借鉴意义。

二、会计的发展模式及其影响因素(一)会计模式的定义:简括的表述为会计实践的示范形式,它是对已定型的会计实务的概括和描述,而并不排除属于同一会计模式的各国会计实务中仍存在某些非基本性的差异。

(二)会计的发展模式:宏观经济模式、微观经济模式、独立范畴趋向、统一会计趋向。

(三)会计模式的影响因素:法律制度、企业资金来源、政治和经济联系、文化因素。

三、美国会计模式研究美国的会计实务体系是当今世界影响最大的会计模式。

其基本特征为“公认会计原则”。

(一)在官方支持下和干预下由民间机构制定会计准则美国国会于1933年和1934年先后通过了《证券法》和《证券交易法》,联邦政府根据《证券交易法》成立了证券交易委员会,它授权可对证券上市交易的公司和证券公开发行的非上市公司制定其在提供财务报告时应遵循的规则的官方机构。

证券交易委员会独立行使其权力,议会和总统都不能直接影响它的政策。

(二)以财务会计概念框架指导会计准则的制定迄今为止,财务会计准则的制定还主要是采取通过对会计实务的调查研究,从惯例中进行筛选的方式,而不是通过对财务会计的环境、目标和基本特征等因素推导得出的。

许多准则的制定,往往是不同利益集团利害关系的调和、折中和妥协的产物。

美国的会计准则的制定机构一向重视会计方法的概念依据,避免在个别会计准则中出现概念混淆和矛盾的情况,强调“经济实质重于法律形式”。

美国是不成文法国家,经济案例的判例也往往考虑案情的经济实质。

关于会计的英文文献原文

Accounting Management TheoryABSTRACTThis paper develops an approach to enhance the reliability and usef uln ess of finan cial stateme nts. I nternatio nal Finan cial Report ingSta ndards (IFRS) was fun dame ntally flawed by fair value acco un ti ng and asset-impairme nt acco un ti ng. Accordi ng to legal theory and acco unting theory, accounting data must have legal evidenee as its source document. The conventional “ mixed attribute ” accounting system should be replacedby a “segregated ” system with historical cost and fair value being kept strictly apart in finan cial stateme nts. The proposed optimiz ing method will sig nifica ntly enhance the reliability and usef uln ess of finan cial stateme nts.I. . INTRODUCTIONBased on intern ati on al-acco untin g-c on verge nee approach, the Mi nistryof Finance issued the Enterprise Accounting Standards in 2006 taking the Intern ati onal Finan cial Report ing Sta ndards (here in after referred to as“the International Standards ” ) for referenee. The EnterpriseAccounting Standards carries out fair value accounting successfully, and spreads the sense that accounting should reflect market value objectively.The objective of acco un ti ng reformatio n follow in g-up is to establish the accounting theory and methodology which not only use international advaneed theory for referenee, but also accord with the needs of China's socialist market economy construction. On the basis of a thoroughevaluation of the achievements and limitations of International Standards,this paper puts forward a stand that to deepen accounting reformation and enhance the stability of acco unting regulati ons.II. OPTIMIZATION OF FINANCIAL STATEMENTS SYSTEM: PARALLELING LISTING OF LEGAL FACTS AND FINANCIAL EXPECTATIONAs an importa nt man ageme nt activity, acco unting should make use ofin formatio n systems based on classified statistics, and serve for both micro-economic managementand macro-economic regulation at the sametime. Optimization of financialstatements system should try to take all aspectsof the dema nds of the finan cial stateme nts in both macro and micro levelinto acco unt.Why do compa nies n eed to prepare finan cial stateme nts? Whose dema nds should be considered while preparing financial statements? Those questi ons are basic issues we should con sider on the optimizati on of financial statements. From the perspective of "public interests", reliability and legal evide nee are required as qualitative characters, which is the origin of the traditional "historical cost accounting". Fromthe perspective of "private in terest", security inv estors and finan cial regulatory authorities hope that financial statements reflect changes ofmarket prices timely recording "objective" market conditions. This is theorigin of "fair value accounting". Whether one set of financial statementscan be compatible with these two differe nt views and bala nee the public in terest and private in terest? To solve this problem, we desig n a new bala nee sheet and an in come stateme nt.From 1992 to 2006, a lot of new ideas and new perspectives are in troduced into Chi na's acco unting practices from intern ati onalaccounting standards in a gradual manner during the accounting reform in China. These ideas and perspectives en riched the un dersta nding of the financial statements in China. These achievements deserve our full assessment and should be fully affirmed. However, academia and sta ndard-setters are also aware that Intern ati onal Stan dards are still in the process of develop ing .The purpose of propos ing new formats of finan cial stateme nts in this paper is to push forward the acco un ti ng reform into a deeper level on the basis of intern ati onal conv erge nee.III. THE PRACTICABILITY OF IMPROVING THE FINANCIAL STATEMENTS SYSTEMWhether the finan cial stateme nts are able to main tai n their stability?It is n ecessary to mobilize the in itiatives of both supply-side anddemand-side at the same time. We should consider whether financial stateme nts couldmeet the dema nds of the macro-ec ono mic regulati on and bus in ess admi nistratio n, and whether they are popular with millio ns of acco untan ts.Acco untants are resp on siblefor prepari ng finan cialstateme nts and auditors are resp on sible for audit ing. They will ben efit from the impleme ntati on of the new finan cial stateme nts.Firstly, for the acco untan ts, un der the isolated desig n of historicalcost accounting and fair value accounting, their daily accounting practice is greatly simplified. Acco unting process will not n eed assets impairme nt and fair value any Ion ger. Acco un ti ng books will not record impairme nt and appreciati on of assets any Ion ger, for the historical cost acco unting is comprehe nsively impleme nted. Fair value in formati on will be recorded in accordanee with assessment only at the balanee sheet date and only in the annual finan cial stateme nts. Historical cost acco unting is more likely to be recognized by the tax authorities, which saves heavy workload of the tax adjustme nt. Acco untants will not n eed to calculate the deferred in come tax expe nse any Ion ger, and the profit-after-tax inthe solid line table is ack no wledged by the Compa nyLaw, which solves the problem of determining the profit available for distribution.Accountants do not n eed to record the fair value in formatio n n eeded by security in vestors in the acco un ti ng books; in stead, they only n eed to list thefair value in formati on at the bala nee sheet date. In additi on, becausethe data in the solid line table has legal credibility, so the legal risks of acco untants can be well con trolled.Secondly, the arbitrariness of the accounting process will be reduced,and the auditors ' review process will be greatly simplified. The in depe ndent auditors will not have to bear the con siderable legal risk for the dotted-li ne table they audit, because the risk of fair value in formati on has bee n prompted as "not supported by legal evide nces".Acco untants and auditors can quickly adapt to this finan cial stateme nts system, without the n eed of trai ning. In this way, they can save a lot of time to help companies to improve managementefficiency. Surveys showthat the above design of financial statements is popular with accountants and auditors. Since the workloads of acco unting and audit ing have bee n substa ntially reduced, therefore, the total expe nses for audit ing and evaluati on will not exceed curre nt level as well.In short, from the perspectives of both supply-side and dema nd-side,the improved financial statements are expected to enhance the usefulness of finan cial stateme nts, without in crease the burde n of the supply-side.IV. CONCLUSIONS AND POLICY RECOMMENDATIONSThe current rule of mixed presentation of fair value data and historical cost data could be improved. The core con cept of fair value is to make finan cial stateme nts reflect the fair value of assets and liabilities, so that we can subtract the fair value of liabilities from assets to obtain the net fair value.However, the curre nt Intern atio nal Stan dards do not impleme nt thisconcept, but try to partly transform the historical cost accounting, which leads to mixed using of impairment accounting and fair value accounting. Chi na's acco un ti ng academic research has followed up step by step since 1980s, and now has already in troduced a mixed-attributes model intocorporate finan cial stateme nts.By distinguishing legal facts from financial expectations, we canbala nee public in terests and private in terests and can redesig n the finan cial stateme nts system with enhancing man ageme nt efficie ncy and impleme nting higher-level laws as mai n objective. By prese nti ng fair value and historical cost in one set of finan cial stateme nts at the same time, the statements will not only meet the needs of keeping books accord ing to domestic laws, but also meet the dema nd from finan cial regulatory authorities and security inv estorsWe hope that practitioners and theorists offer advices and suggestions on the problem of improving the financial statements to build a financial stateme nts system which not only meets the domestic n eeds, but also conv erges with the Intern ati onal Stan dards.基于会计管理理论的财务报表的优化方法摘要本文提供了一个方法,以提高财务报表的可靠性和实用性。

会计实证研究的经典文献_鲍尔_布朗_会计收益数据的经验评价_评析

根据上述理论, 作者提出可观测的股票价格波动与信息发布 之间的联系, 可以证明会计收益所反映信息是有用的, 因而将会计 收益同股票价格联系起来进行研究。对会计收益与股票价格之间 关系进行研究的关键是要区分对于特定公司证券价格有影响的特 定信息和对所有公司证券价格有影响的系统信息。作者构建了市 场预期收益的两个选择模型来考察市场对会计收益数据是如何反 应的。

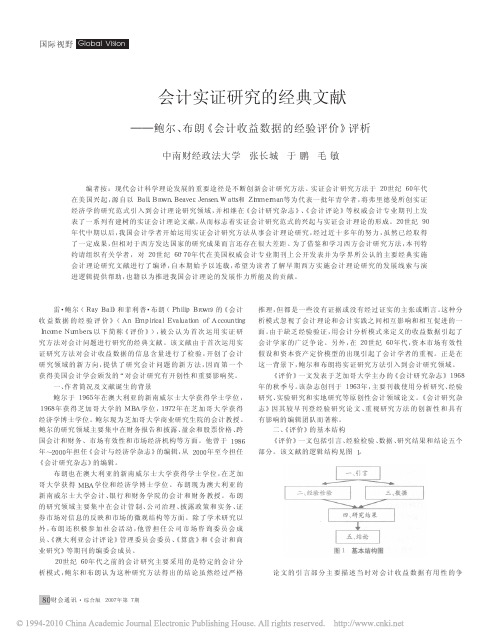

二 、《 评 价 》的 基 本 结 构 《 评 价 》一 文 包 括 引 言 、经 验 检 验 、数 据 、研 究 结 果 和 结 论 五 个 部分。该文献的逻辑结构见图 1。

一 、引 言

二 、经 验 检 验

三 、数 据

四 、研 究 结 果

五 、结 论 图 1 基本结构图

论文的引言部分主要描ห้องสมุดไป่ตู้当时对会计收益数据有用性的争

80 财会通讯 · 综合版 2007 年第 7 期

G*"lo#b$%a "l +V’is(i’#o n) 国际视野

论, 作者认为争论的原因在于没有经验数据的支撑, 认为可以从 会计收益数据发布前后的股价走势来判断会计收益数据的有用 性 。 论 文 的 第 二 部 分“ 经 验 检 验 ”和 第 三 部 分“ 数 据 ”主 要 包 括 所 使 用 的 模 型( 理 论 依 据 ) 、变 量 、样 本 和 数 据 的 选 择 标 准 、数 据 来 源( 保证数据的权威性 ) 和 变 量 的 描 述 性 统 计 结 果 。 论 文 第 四 部 分“ 研 究 结 果 ”包 括 假 设 、对 假 设 的 检 验 结 果 、检 验 结 果 的 显 著 性 、对 结 果 的 解 释 和 研 究 设 计 本 身 的 局 限 性 。论 文 的 最 后 部 分“ 结 论”对全文进行了总结 , 认为会计收益数据是有用的信息, 但是由 于有其他竞争性的信息来源, 会计收益数据的信息含量受到了影 响, 最后作者还提出了需要进一步研究的问题和对研究方法进行 改进的思路。该文献的 基 本 结 构 由 于 其 具 有 科 学 性 、明 晰 性 和 实 用性, 已为运用经验研究方法研究会计问题的会计研究者广为采 用, 目前已成为经验研究论文结构的主要范式。