Week 3 MBA 503- Managerial Decision Making Final Fall 2012

欧洲商学院MBA课程人力资源管理之员工管理

领导型的职业发展

General Management

Operations

Business development

Sales

Market research

管理他人的两项基本技能

Creating Energy

Motivation

Channeling Energy

Leadership

Goal setting

Strategies are only as good as the people to implement them 计划再好也 要靠人来执行

怎么判断一个人是否是最合适 某个岗位的人呢?

Job Activities

1 The person does the job well

Personality

•Simulating

The announcement •Action

情况处理技能

Coaching skills

Reading the traffic lights

•Developing people

•Direction & Control

•Decide on the appropriate decision strategy

你有两个助手,都能做第二件事。原则上你 可以让他们两个中的任何一个去做第二件事。

琐事只能你自己做,并且你只有时间做两件 事中的一样。

小测验

你面临的问题是先做那件工作?

– A:你选择那个技术问题,希望稍后能挤出 时间来处理那堆琐事

– B:你选择那堆琐事,让你的一个助手来做 另外一件更富有挑战性的事

好的事情马上就会到来,一切都是最 好的安 排。下 午12时54分0秒 下午12时54分 12:54:0020.10.27

美国帕克大学介绍版

美国帕克大学MBA帕克大学一年制MBA班是帕克大学专为中国精英开设的创新型MBA硕士学位班,课程为期一年,全程脱产在美国本土学习。

通过考核者将获得中美认可的MBA硕士学位。

该课程旨在进一步加强国际文化交流、开辟文化合作的新境界。

希望学员在美国进行为期一年的学习后,能够全面开拓思维视野,革新企业经营理念,成为国际型、复合型、实用型的杰出高端人才。

MBA班授课地点在美国密苏里州的帕克大学帕克维尔主校区,该校区有近三分之一的学生为国际学生,分别来自120多个国家。

帕克大学在对国际学生的教学与管理上有着长期而丰富的经验。

帕克大学一年制MBA班无论从课程设置还是从授课方式上,都充分考虑到亚洲学生的特点与需要。

本课程不设TOEFL、GMAT要求,但需要有一定的英语基础。

学员入学后先接受一个月的英语强化培训,接着进行11个月的MBA课程学习。

除了英语培训和MBA常规课程外,帕克大学还为学员提供两次美国商界精英人士讲座,两次美国著名公司参观访问以及组织“美国西海岸房地产、经济、教育考察团”。

帕克大学MBA 班每年招生两次,为5月份春季班、9月份秋季班。

招生信息报名条件:拥有中国教育部认可的本科学历者拥有中国教育部认可的大专学历并有三年以上工作经验者有大学或相当学历的英语水平、能全脱产一年在美国本土学习报名方式:申请材料:本科或专科毕业证、成绩单、银行存款证明、护照复印件、英文个人简历1-2页申请流程:到当地报名点报名、递交报名材料----统一邮寄资料到帕克大学----帕克大学签发录取通知书----学生签证----汇款----入学报到。

收费标准:入学申请费、报名费及资格审查费共RMB3千元美国帕克大学学费、在美国英语培训费共计RMB16.8万元商学院与工商管理硕士(MBA)专业帕克大学商学院是美国最大的商学院之一。

学院的使命是以对社会负责的方式,为学生提供高质量的、创新性的、以应用为基础的教育。

帕克大学商学院是美国进步最快的商学院之一。

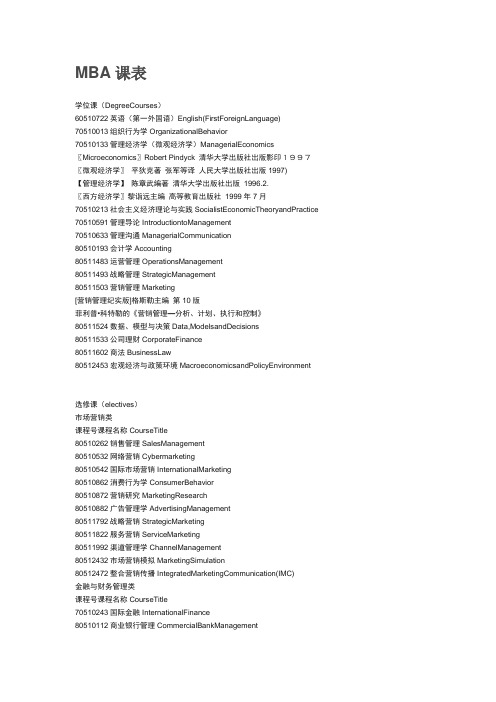

清华大学MBA课程表

MBA课表学位课(DegreeCourses)60510722英语(第一外国语)English(FirstForeignLanguage) 70510013组织行为学OrganizationalBehavior70510133管理经济学(微观经济学)ManagerialEconomics 〖Microeconomics〗Robert Pindyck 清华大学出版社出版影印1997〖微观经济学〗平狄克著张军等译人民大学出版社出版1997)【管理经济学】陈章武编著清华大学出版社出版1996.2.〖西方经济学〗黎诣远主编高等教育出版社1999年7月70510213社会主义经济理论与实践SocialistEconomicTheoryandPractice 70510591管理导论IntroductiontoManagement70510633管理沟通ManagerialCommunication80510193会计学Accounting80511483运营管理OperationsManagement80511493战略管理StrategicManagement80511503营销管理Marketing[营销管理纪实版]格斯勒主编第10版菲利普•科特勒的《营销管理—分析、计划、执行和控制》80511524数据、模型与决策Data,ModelsandDecisions80511533公司理财CorporateFinance80511602商法BusinessLaw80512453宏观经济与政策环境MacroeconomicsandPolicyEnvironment选修课(electives)市场营销类课程号课程名称CourseTitle80510262销售管理SalesManagement80510532网络营销Cybermarketing80510542国际市场营销InternationalMarketing80510862消费行为学ConsumerBehavior80510872营销研究MarketingResearch80510882广告管理学AdvertisingManagement80511792战略营销StrategicMarketing80511822服务营销ServiceMarketing80511992渠道管理学ChannelManagement80512432市场营销模拟MarketingSimulation80512472整合营销传播IntegratedMarketingCommunication(IMC)金融与财务管理类课程号课程名称CourseTitle70510243国际金融InternationalFinance80510112商业银行管理CommercialBankManagement80510122投资银行业务InvestmentBankOperation80510312投资学TheoryofInvestment亚当.史密斯的《金钱游戏》希尔《像大亨般思考》墨基尔《漫步华尔街》罗威斯坦《巴菲特:美国资本家的特质》林区《征服股海》索罗斯《超越指数》施伯伦《专业投机原理》《股市大亨/新股市大亨》《金融怪杰》《论凯因斯》《股票作手回忆录》葛拉汉《智慧型股票投资人》费雪《非常潜力股》甘氏《华尔街浮沉二十五载》《股价趋势》伯恩斯坦《与天为敌》《战胜道琼斯》《放空巧术》《统计会说谎》高伯瑞《1929股市大崩盘》《混乱中的困惑》《异常大众妄想与群体疯狂》来源:(/s/blog_44c2e3510100f7vb.html) - 清华MBA管理课程课表_求索_新浪博客80510342国际贸易InternationalTrade董瑾主编:《国际贸易理论与实务(修订版)》,北京理工大学出版社,2001年。

浙江大学MBA课程设置(MBA Courses)

32

2

管理統計學(Business Statistics)

32

2

人力資源管理(Human Resource Management)

32

2

入學導向(Orientation)

16

1

文獻閱讀與論文導寫(Literature ReadingandDissertation Guide)

16

1

MBA必修課小計(Subtotal Required Courses Credits)

8

MBA選修課

(Electives)

管理溝通(Managerial Communication)

32Байду номын сангаас

2

企業倫理(Business Ethics)

32

2

商法(Business Law)

32

2

國際貿易理論與實務(International Trade)

32

2

物流與供應鏈管理(Logistics and Supply Chain)

32

2

宏觀經濟學(Macroeconomics)

32

2

房地產經營管理(Real Estate Management)

32

2

客戶關係管理(Customer Relationship Management)

32

2

創新管理(Innovation Management)

48

3

戰略管理(Strategic Management)

48

3

MBA核心課小計(Subtotal Core Courses Credits)

24

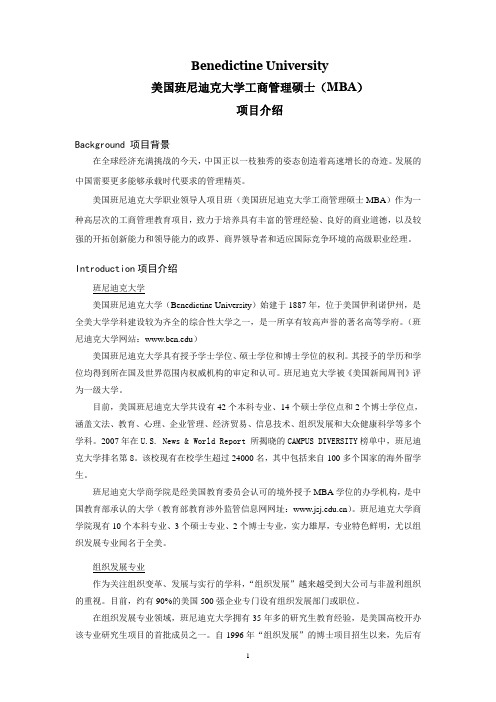

班尼迪克MBA项目介绍

Benedictine University美国班尼迪克大学工商管理硕士(MBA)项目介绍Background 项目背景在全球经济充满挑战的今天,中国正以一枝独秀的姿态创造着高速增长的奇迹。

发展的中国需要更多能够承载时代要求的管理精英。

美国班尼迪克大学职业领导人项目班(美国班尼迪克大学工商管理硕士MBA)作为一种高层次的工商管理教育项目,致力于培养具有丰富的管理经验、良好的商业道德,以及较强的开拓创新能力和领导能力的政界、商界领导者和适应国际竞争环境的高级职业经理。

Introduction项目介绍班尼迪克大学美国班尼迪克大学(Benedictine University)始建于1887年,位于美国伊利诺伊州,是全美大学学科建设较为齐全的综合性大学之一,是一所享有较高声誉的著名高等学府。

(班尼迪克大学网站:)美国班尼迪克大学具有授予学士学位、硕士学位和博士学位的权利。

其授予的学历和学位均得到所在国及世界范围内权威机构的审定和认可。

班尼迪克大学被《美国新闻周刊》评为一级大学。

目前,美国班尼迪克大学共设有42个本科专业、14个硕士学位点和2个博士学位点,涵盖文法、教育、心理、企业管理、经济贸易、信息技术、组织发展和大众健康科学等多个学科。

2007年在U.S. News & World Report 所揭晓的CAMPUS DIVERSITY榜单中,班尼迪克大学排名第8。

该校现有在校学生超过24000名,其中包括来自100多个国家的海外留学生。

班尼迪克大学商学院是经美国教育委员会认可的境外授予MBA学位的办学机构,是中国教育部承认的大学(教育部教育涉外监管信息网网址:)。

班尼迪克大学商学院现有10个本科专业、3个硕士专业、2个博士专业,实力雄厚,专业特色鲜明,尤以组织发展专业闻名于全美。

组织发展专业作为关注组织变革、发展与实行的学科,“组织发展”越来越受到大公司与非盈利组织的重视。

目前,约有90%的美国500强企业专门设有组织发展部门或职位。

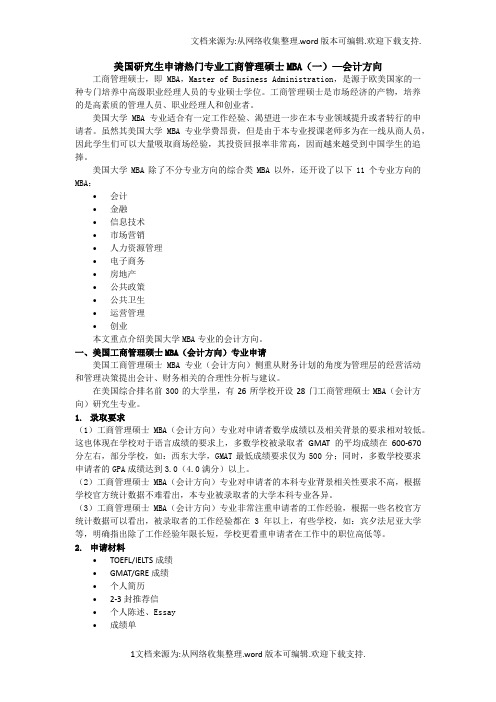

美国MBA(会计方向)

美国研究生申请热门专业工商管理硕士MBA(一)—会计方向工商管理硕士,即MBA,Master of Business Administration,是源于欧美国家的一种专门培养中高级职业经理人员的专业硕士学位。

工商管理硕士是市场经济的产物,培养的是高素质的管理人员、职业经理人和创业者。

美国大学MBA专业适合有一定工作经验、渴望进一步在本专业领域提升或者转行的申请者。

虽然其美国大学MBA专业学费昂贵,但是由于本专业授课老师多为在一线从商人员,因此学生们可以大量吸取商场经验,其投资回报率非常高,因而越来越受到中国学生的追捧。

美国大学MBA除了不分专业方向的综合类MBA以外,还开设了以下11个专业方向的MBA:•会计•金融•信息技术•市场营销•人力资源管理•电子商务•房地产•公共政策•公共卫生•运营管理•创业本文重点介绍美国大学MBA专业的会计方向。

一、美国工商管理硕士MBA(会计方向)专业申请美国工商管理硕士MBA专业(会计方向)侧重从财务计划的角度为管理层的经营活动和管理决策提出会计、财务相关的合理性分析与建议。

在美国综合排名前300的大学里,有26所学校开设28门工商管理硕士MBA(会计方向)研究生专业。

1.录取要求(1)工商管理硕士MBA(会计方向)专业对申请者数学成绩以及相关背景的要求相对较低。

这也体现在学校对于语言成绩的要求上,多数学校被录取者GMAT的平均成绩在600-670分左右,部分学校,如:西东大学,GMAT最低成绩要求仅为500分;同时,多数学校要求申请者的GPA成绩达到3.0(4.0满分)以上。

(2)工商管理硕士MBA(会计方向)专业对申请者的本科专业背景相关性要求不高,根据学校官方统计数据不难看出,本专业被录取者的大学本科专业各异。

(3)工商管理硕士MBA(会计方向)专业非常注重申请者的工作经验,根据一些名校官方统计数据可以看出,被录取者的工作经验都在3年以上,有些学校,如:宾夕法尼亚大学等,明确指出除了工作经验年限长短,学校更看重申请者在工作中的职位高低等。

清华大学经济管理学院MBA课程表

罗斯,伦道夫 W.

威斯特菲尔德,

朱玉杰

杰弗利 F.杰富著, 吴世农,沈艺峰,

王志强等译,《公

司理财》(原书第

6版),机械工业

王以华/于增彪/宋学宝

无

陈涛涛/焦捷/段志蓉

待定

吴贵生/王毅

无

朱岩/黄京华/毛波

无

Philip Kotler &

Kevin Lane

赵平

Keller,营销管 理,13版,中文

版,中国人民大学

钱小军 陈国权

刘丽文著,《生产 与运作管理》,第 三版,清华大学出

版社,2007。 1.金占明著,《战

略管理》,第3 版,清华大学出版 2.(美)迈克尔· 波特著,陈小悦 译,《竞争战略 》,华夏出版社。 3.(美)迈克尔· 波特著,陈小悦 译,《竞争优势 》,华夏出版社。

无 范健主编,《商法 》,第二版,高等 教育出版社(北 京),北京大学出

待定

以教师讲义和阅读 资料为主

姜彦福、张帏等编 著,《创业管理学 》,清华大学出版 社,2005年7月份

出版。

46

公司成长管理

47

项目投融资决策

48

供应链管理

49

公司财务案例

Байду номын сангаас

50

公司综合风险管理

51

国际金融

52

投资学

53

证券投资学

54

企业文化与管理

55

战略人力资源管理

56

消费行为学

57

国际企业管理(MBA)

guidemanagerialcommunication理沟通指南第七版清华大学出版社28管理思维与沟通下29会计学30营销管理31管理思维与沟通下32领导力开发与组织行为下33管理思维与沟通下34领导力开发与组织行为下自编讲义35伦理与企业责任随堂发资料36伦理与企业责任随堂发资料37伦理与企业责任随堂发资料38伦理与企业责任随堂发资料39管理研究方法论自编讲义40广告管理学41积极心理学42企业的兴衰中外企业发展史简析待定43中国资本市场与公司财务44中外著名企业管理研究45创业管理managerialcommunication理沟通指南第七版清华大学出版社夏冬林主编会计学清华大学出版社第三版

Managerial Economics Chapter 01

GWMBA Short Quiz-- Chapter 11. Economic profitA. Is a theoretical measure of a firm's performance and has little value in real world decision making.B. Can be calculated by subtracting implicit costs of using owner-supplied resources from the firm's total revenue.C. Is negative when costs exceed revenues.D. Is generally larger than accounting profit.2. Consider a firm that employs some resources that are owned by the firm. When accounting profit is zero, economic profitA. Must also equal zero.B. Is sure to be positive.C. Must be negative and shareholder wealth is reduced.D. Cannot be computed accurately, but the firm is breaking even nonetheless.3. Suppose Marv, the owner-manager of Marv's Hot Dogs, earned $72,000 in revenue last year. Marv's explicit costs of operation totaled $36,000. Marv has a Bachelor of Science degree in mechanical engineering and could be earning $30,000 annually as mechanical engineer.A. Marv's implicit cost of using owner-supplied resources is $36,000.B. Marv's economic profit is $36,000.C. Marv's implicit cost of using owner-supplied resources is $30,000.D. Marv's economic profit is $6,000.E. Both c and d.4. The principal-agent problem arises whenA. The principal and the agent have different objectives.B. The principal cannot enforce the contract with the agent or finds it too costly to monitor the agent.C. The principal cannot decide whether the firm should seek to maximize the expected future profits of the firm or maximize the price for which the firm can be sold.D. Both a and b.E. Both a and c.5. Moral hazardA. Occurs when managers pursue maximization of profit without regard to the interests of society in general.B. Exists when either party to a contract has an incentive to cancel the contract.C. Occurs only rarely in modern corporations.D. Is the cause of principle-agent problems.6. When a firm earns less than a normal profit,A. The revenues generated cannot pay all explicit costs and the opportunity cost of using owner-supplied resources.B. Accounting profit is negative.C. Economic profit is zero.D. Normal profit is negative.E. All of the above.7. Economic profit is the best measure of a firm's performance becauseA. Normal profit is generally too difficult to measure.B. Economic profit fully accounts for all sources of revenue.C. Only explicit costs influence managerial decisions since, in general, only explicit costs can be subtracted from revenue for the purposes of computing taxable profit.D. The opportunity cost of using ALL resources is subtracted from total revenue.8. Which of the following is an example of an implicit cost for a firm?A. The value of time worked by the owner.B. Any wages and salaries paid to employed.C. Forgone rent on property owned by firm.D. Both a and c.E. All of the above.9. During a year of operation, a firm collects $450,000 in revenue and spends $100,000 on labor expense, raw materials, rent, and utilities. The firm's owner has provided $750,000 of her own money instead of investing the money and earning a 10% annual rate of return.a. The explicit opportunity costs of using market-supplied resources are ______________. The implicit opportunity costs of using owner-supplied resources are ______________. Total economic cost is______________.b. The firm earns economic profit of ______________.c. The firm's accounting profit is ______________.d. If the owner could earn 15% annually on the money she has invested in the firm, the economic profit of the firm would be ______________ (when revenue is $450,000).GWMBA Short Quiz-- Chapter 1 Key1. Economic profita. Is a theoretical measure of a firm's performance and has little value in real world decision making.b. Can be calculated by subtracting implicit costs of using owner-supplied resources from the firm's total revenue.C. Is negative when costs exceed revenues.d. Is generally larger than accounting profit.Thomas - Chapter 01 #22. Consider a firm that employs some resources that are owned by the firm. When accounting profit is zero, economic profita. Must also equal zero.b. Is sure to be positive.C. Must be negative and shareholder wealth is reduced.d. Cannot be computed accurately, but the firm is breaking even nonetheless.Thomas - Chapter 01 #53. Suppose Marv, the owner-manager of Marv's Hot Dogs, earned $72,000 in revenue last year. Marv's explicit costs of operation totaled $36,000. Marv has a Bachelor of Science degree in mechanical engineering and could be earning $30,000 annually as mechanical engineer.a. Marv's implicit cost of using owner-supplied resources is $36,000.b. Marv's economic profit is $36,000.c. Marv's implicit cost of using owner-supplied resources is $30,000.d. Marv's economic profit is $6,000.E. Both c and d.Thomas - Chapter 01 #84. The principal-agent problem arises whena. The principal and the agent have different objectives.b. The principal cannot enforce the contract with the agent or finds it too costly to monitor the agent.c. The principal cannot decide whether the firm should seek to maximize the expected future profits of the firm or maximize the price for which the firm can be sold.D. Both a and b.e. Both a and c.Thomas - Chapter 01 #115. Moral hazarda. Occurs when managers pursue maximization of profit without regard to the interests of society in general.b. Exists when either party to a contract has an incentive to cancel the contract.c. Occurs only rarely in modern corporations.D. Is the cause of principle-agent problems.Thomas - Chapter 01 #126. When a firm earns less than a normal profit,A. The revenues generated cannot pay all explicit costs and the opportunity cost of using owner-supplied resources.b. Accounting profit is negative.c. Economic profit is zero.d. Normal profit is negative.e. All of the above.Thomas - Chapter 01 #237. Economic profit is the best measure of a firm's performance becausea. Normal profit is generally too difficult to measure.b. Economic profit fully accounts for all sources of revenue.c. Only explicit costs influence managerial decisions since, in general, only explicit costs can be subtracted from revenue for the purposes of computing taxable profit.D. The opportunity cost of using ALL resources is subtracted from total revenue.Thomas - Chapter 01 #248. Which of the following is an example of an implicit cost for a firm?a. The value of time worked by the owner.b. Any wages and salaries paid to employed.c. Forgone rent on property owned by firm.D. Both a and c.e. All of the above.Thomas - Chapter 01 #279. During a year of operation, a firm collects $450,000 in revenue and spends $100,000 on labor expense, raw materials, rent, and utilities. The firm's owner has provided $750,000 of her own money instead of investing the money and earning a 10% annual rate of return.a. The explicit opportunity costs of using market-supplied resources are ______________. The implicit opportunity costs of using owner-supplied resources are ______________. Total economic cost is______________.b. The firm earns economic profit of ______________.c. The firm's accounting profit is ______________.d. If the owner could earn 15% annually on the money she has invested in the firm, the economic profit of the firm would be ______________ (when revenue is $450,000).a. $100,000; $75,000; $175,000.b. $275,000.c. $350,000.d. $237,500.Thomas - Chapter 01 #36GWMBA Short Quiz-- Chapter 1 SummaryCategory # of QuestionsThomas - Chapter 01 9。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

What choices does a manager make with respect to Accounting? Is it limited to policies? Also decides on estimates & disclosure

Enron, Worldcom- examples of direct manipulation of accounting information to deceive- outside of the rules Flexibility of GAAP with Professional judgment leads to legal earnings management.

Recognition that a previously recorded Accounts receivable will not provide a future benefit due to the fact we will not collect it, or will we??? Didn’t the rules of revenue recognition require us to determine if collection is reasonably assured???

Situation #

Situation 1

Fiscal 2010 Fiscal 2011 Fiscal 2012

Rogers receives Rogers ships large order from order to customer corp customer and receives cash Receives large order from customer Receives large order Ships order Receives cash on delivery Ships order Receives cash from customer

Situation 2

Situation 3

When do we record the revenue and why?

Performance has occurred The amount of revenue can be reasonable measured Collection of payment is reasonably assured Sounds easy?

Net cash provided by operating activities Net cash used for investing activities Net cash provided by financing activities Net decrease in cash Cash balance, December 31, 2005 Cash balance, December 31, 2006

Common methods of Bad Debt calculation

1) Direct Write Off 2) % of Sales 3) Aging of A/R balances

Subject

Revenue Recognition

Policies

When to recognize revenue?

Estimates

Bad Debts Returns Discounts

Other

Inventory

Valuation- FIFO,LIFO, average cost What is included in inventory cost?

Operating

–day to day

Investing

– Long term assets

Long term liabilities shareholders

Financing-

and transactions

Cash Flow Statement (Indirect Method) For the Year Ended December 31, 2006 (In thousands)

Rules vs Guidelines? Government vs Self Policing? Professional judgment? Do laws against speeding and theft stop those activities? Be vigilant- consider the source/objectives of all information If it doesn’t make sense, question it!

Is there a difference between revenue and the receipt of cash?

Is timing important?

Must there be agreement between the two parties as to whether or not something is earned?

industry risk customers contracts ownership demands need for financing moral/ethical considerations taxation

Accounts receivable balances Accounting for returns/discounts Bad debt expense & allowance for doubtful accounts

GAAP says that we record Revenue when it is earned

What happens when revenue is earned? Assets increase Revenues increase

The big question is: When is revenue earned??

Even in the US, GAAP allows for flexibility in the choice of:

Accounting Policies- more than 1 allowable option Accounting Estimates- professional judgment Disclosure- no required wording

GAAP Auditors Report- fair representation Fraudulent Activities Basic Financial Analysis

◦ Management by exception ◦ Expectations/Comparisons

Interconnection between Accounts

Meet investors expectations Maintain stock price Meet budget goals Obtain best terms for loans Avoid violation of debt covenants Obtain grants from government Minimize taxes Generally influence decisions arising out of accounting information

Amortization Method Capitalization policies

Leases When to recognize liabilities

Write-downs of obsolete and damaged inventory, Net Realizable Value

Useful lives, Write downs and write offs Salvage values

Warranty provisions Pensions Accruals

Capital Assets

Liabilities

Assets vs Expenses

Other

Capitalization policies

Expensing assets Classifications Long/Short term, ordinary, unusual, extraordinary Disclosure of contingencies

Defn: “Amounts owed to an entity by customers for goods and services provided on credit”

John Friedlan, Financial Accounting, 2nd edition, McGraw Hill, 2007

Management InfluenceGoals/Motivations/Objectives Earnings Management Generally Accepted Accounting Principles (GAAP) Inter-connection between Accounts Revenue Recognition and Accounts Receivable

$ 68 (255) 167 $ (20) 42 $ 22

Free cash flow is the amount of cash available from operations after paying for planned investments in capital, equipment, and other long-term assets. Free cash flow = Net cash flow from operating activities – Cash outflow earmarked for investments in capital, equipment (long term assets) and required dividends