会计学原理英文名词解释

大学一年级下学期会计学原理-会计学原理名词解释

名词解释1.Accounting: An information and measurement system that identifies, records, and municatesrelevant, reliable, and parable information about an organization’s business activities.(P2)2.Double-entry bookkeeping: each transaction affect, and are recorded in, at least two accounts. It alsomeans the total amount debited must equal the total amount credited for each transaction.(P32) 3.Business entity assumption: a business is accounted for separately from other business entities,including its owner.(P7)4.Going-concern assumption: accounting information reflects a presumption that the business willcontinue operating instead of being closed or sold.(P7)5.Moary unit assumption: we can express transactions and events in moary, or money, units.(P7)6.Time period assumption: the life of pany can be divided into time periods, such as month and years,and that useful reports can be prepared for those periods.(P7)7.Revenue recognition principle: provides guidance on when a pany must recognize revenue.(1.Revenue is recognized when earned. 2. Proceeds from selling products and services need not be incash. 3. revenue is measured by the cash received plus the cash value of any other items received.) (P7)8.Matching principle: a pany must record its expenses incurred to generate the revenue reported. (P7)9.Full-disclosure principle: a pany to report the details behind financial statements that would impactusers’ decisions.(P7)10.Consistency concept: a pany use the same accounting methods period after period so that financialstatements are parable across periods-----the only exception is when a change from one method to another will improver its financial statements.(P152)11.Conservatism constraint: the use of the less optimistic amoun t when more than one estimate of theamount to be received or paid exists and these estimates are about equally likely.(P153)12.Materiality constraint: an amount can be ignored if its effect on the financial statements isunimportant to users’ business decisions.(P232)13.Asset: resources owned or controlled by a pany and that have expected future benefits.(P29)14.Current Asset: cash and other resources that are expected to be sold, collected or used within oneyear or the pany’s operating cycle, whichever is longer(P97)15.Liability: a probable future payment of assets or services that a pany is presently obligated to makeas a result of past transactions or events. (P281)16.Current liability: also called short-term liabilities, are obligations due within one year or the pany’scycle, whichever is longer.(P282)17.Long-term liability: a pany’s obligations not expected to be paid within the longer of one year or thepany’s operating cycle.(P282)18.Equity: the owner’s claim on a pany’s assets. (P31)19.Retained Earning: the cumulative ine (and loss) not distributed as dividends to itsstockholders.(P348)20.Gross Profit: also called gross margin, which equals sales less cost of goods sold.(P113)sales = Sales – Sales discounts – Sales returned and allowances简答1.Steps involved in Accounting cycle (P95)Step 1 analyze transactionsStep 2 JournalizeStep 3 postStep 4 prepare unadjusted trial balanceStep 5 adjustStep 6 prepare adjusted trial balanceStep 7 prepare statementsStep 8 closeStep 9 prepare post-closing trail balance(step 10 reverse)2.Introduce basic financial statement(P14)1.ine statement——describes a pany’s revenues and expenses along with the resulting ine or lossover a period of time due to earning activities.2.statement of owner’s equity——explains changes in equity from ine ( or loss) and from anyowner investments and withdrawals over a period of time.3.balance sheet——describes a pany’s financial position (types and amounts of assets, liabilitiesand equity) at a point of time.3.Accrual basis VS cash basis (P60)Accrual basis accounting uses the adjusting process to recognize revenues when earned and expenses when incurred ( matched with revenues) .Matching principleCash basis accounting recognizes revenues when cash is received and records expenses when cash is paid.4.Principles of internal control (P202)1.Establish responsibilities2.maintain adequate records3.separate recordkeeping from custody of assets4.divide responsibility for related transactions5.perform regular and independent reviews5.Principles of cash control (P205)1.handling cash is separate from recordkeeping of cash2.cash receipts are promptly deposited in a bank3.cash disbursements are made by check..6.Capital expenditures VS revenue expenditures (P252)Capital expenditures are additional costs of plant assets that provide benefits extending beyond the current period. They are debited to asset accounts and reported on the balance sheet. Capital expenditures increase or improve the type or amount of service an asset provides.Revenue expenditures are additional costs of plant assets that do not materially increase the asset’s life or productive capabilities. They are recorded as expenses and deducted from revenues in the current period’s ine statement.7.advantages and disadvantages of corporation (P345)Advantages: 1.separate legal entity2. limited liability of stockholders3. transferable ownership rights4. continuous life5. lack of mutual agency for stockholders6. ease of capital accumulationDisadvantages: 1. government regulation2.corporate taxation------------------------- 赠予------------------------【幸遇•书屋】你来,或者不来我都在这里,等你、盼你等你婉转而至盼你邂逅而遇你想,或者不想我都在这里,忆你、惜你忆你来时莞尔惜你别时依依你忘,或者不忘我都在这里,念你、羡你念你袅娜身姿羡你悠然书气人生若只如初见任你方便时来随你心性而去却为何,有人为一眼而愁肠百转为一见而不远千里晨起凭栏眺但见云卷云舒风月乍起春寒已淡忘如今秋凉甚好几度眼迷离感谢喧嚣把你高高卷起砸向这一处静逸惊翻了我的万卷和其中的一字一句幸遇只因这一次被你拥抱过,览了被你默诵过,懂了被你翻开又合起被你动了奶酪和心思不舍你的过往和过往的你记挂你的现今和现今的你遐想你的将来和将来的你难了难了相思可以这一世。

会计学原理重要术语

第三章1、会计假设(AccountingPostulates)会计信息产生和加工的基本前提条件。

2、会计主体(AccountingEntity)会计主体又称为经济主体,每个企业或独立核算的单位都是独立于业主和其他单位的会计主体。

3、持续经营(GoingConcern)除非有相反的确切证据,否则,认为一个经营主体将持续它的经营活动直到实现其经营目标为止。

4、会计分期(TimePeriod)人为地将企业的生产经营活动过程划分至一定的期间,通常是以日历年度作为划分标准的。

5、货币计量(Monetaryunit)其规定了会计信息系统主要提供的是可以用货币计量的信息。

这个假设有两层含义:第一,以货币(通常为主体所在国的法定货币)为计量单位;第二,假定作为计量单位的货币,其购买力是稳定的。

6、会计目标(AccountingObjective)也称为会计目的,指的是会计活动应达到的境地或标准。

7、受托责任(Accoutability)是由于委托关系的建立而发生的,委托关系建立后,作为一个委托人,就要以最大的善意、最经济有效的办法、最严格地按照当事人的意志来完成委托人所托付的任务。

8、会计报表(AccountingReport)是以日常会计核算资料为主要依据,按照一定的格式加以汇总、整理,用来总括地反映企业财务状况、经营成果和现金流量的一种书面文件。

会计报表是日常会计核算的定期总结,可以为报表的使用者提供综合、系统的财务信息。

9、资产负债表(theBalanceSheet)是反映企业在某一特定日期的财务状况的报表,又称为“财务状况表”,其主要作用在于提供企业在某一时日关于资产、负债、所有者权益及其相互关系的静态信息。

10、利润表(theIncomeStatement)又叫损益表,是用来反映企业一定时期经营活动业绩的会计报表。

11、现金流量表(theCashFlowStatement)是以现金为基础编制的财务状况变动表,它反映企业一定期间内现金和现金等价物的流入和流出,表明企业获得现金和现金等价物的能力。

会计专业专业术语中英文对照

会计专业专业术语中英文对照一、会计与会计理论会计accounting决策人Decision Maker投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师CPA Certified Public Accountant国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业Partnership公司Corporation会计目标Accounting Objectives会计假设Accounting Assumptions会计要素Accounting Elements会计原则Accounting Principles会计实务过程Accounting Procedures财务报表Financial Statements财务分析Financial Analysis会计主体假设Separate-entity Assumption货币计量假设Unit-of-measure Assumption持续经营假设Continuity(Going-concern) Assumption会计分期假设Time-period Assumption资产Asset负债Liability业主权益Owner's Equity收入Revenue费用Expense收益Income亏损Loss历史成本原则Cost Principle收入实现原则Revenue Principle配比原则Matching Principle全面披露原则Full-disclosure (Reporting) Principle 客观性原则Objective Principle一致性原则Consistent Principle可比性原则Comparability Principle重大性原则Materiality Principle稳健性原则Conservatism Principle权责发生制Accrual Basis现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning二、会计循环会计循环Accounting Procedure/Cycle会计信息系统Accounting information System帐户Ledger会计科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General Ledger明细分类帐Subsidiary Ledger试算平衡Trial Balance现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐General Journal工作底稿Worksheet调整分录Adjusting entries结帐Closing entries三、现金与应收账款现金Cash银行存款Cash in bank库存现金Cash in hand流动资产Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单Bank statement银行存款调节表Bank reconciliation statement 在途存款Outstanding deposit在途支票Outstanding check应付凭单Vouchers payable应收帐款Account receivable应收票据Note receivable起运点交货价F.O.B shipping point目的地交货价F.O.B destination point商业折扣Trade discount现金折扣Cash discount销售退回及折让Sales return and allowance 坏帐费用Bad debt expense备抵法Allowance method备抵坏帐Bad debt allowance损益表法Income statement approach资产负债表法Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息票据Interest bearing note不带息票据Non-interest bearing note出票人Maker受款人Payee本金Principal利息率Interest rate到期日Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee com四、存货存货Inventory商品存货Merchandise inventory产成品存货Finished goods inventory在产品存货Work in process inventory原材料存货Raw materials inventory起运地离岸价格F.O.B shipping point目的地抵岸价格F.O.B destination寄销Consignment寄销人Consignor承销人Consignee定期盘存Periodic inventory永续盘存Perpetual inventory购货Purchase购货折让和折扣Purchase allowance and discounts 存货盈余或短缺Inventory overages and shortages 分批认定法Specific identification加权平均法Weighted average先进先出法First-in, first-out or FIFO后进先出法Lost-in, first-out or LIFO移动平均法Moving average成本或市价孰低法Lower of cost or market or LCM 市价Market value重置成本Replacement cost可变现净值Net realizable value上限Upper limit下限Lower limit毛利法Gross margin method零售价格法Retail method成本率Cost ratio五、长期投资长期投资Long-term investment长期股票投资Investment on stocks长期债券投资Investment on bonds成本法Cost method权益法Equity method合并法Consolidation method股利宣布日Declaration date股权登记日Date of record除息日Ex-dividend date付息日Payment date债券面值Face value, Par value债券折价Discount on bonds债券溢价Premium on bonds票面利率Contract interest rate, stated rate市场利率Market interest ratio, Effective rate普通股Common Stock优先股Preferred Stock现金股利Cash dividends股票股利Stock dividends清算股利Liquidating dividends到期日Maturity date到期值Maturity value直线摊销法Straight-Line method of amortization实际利息摊销法Effective-interest method of amortization 六、固定资产固定资产Plant assets or Fixed assets原值Original value预计使用年限Expected useful life预计残值Estimated residual value折旧费用Depreciation expense累计折旧Accumulated depreciation帐面价值Carrying value应提折旧成本Depreciation cost净值Net value在建工程Construction-in-process磨损Wear and tear过时Obsolescence直线法Straight-line method (SL)工作量法Units-of-production method (UOP)加速折旧法Accelerated depreciation method双倍余额递减法Double-declining balance method (DDB)年数总和法Sum-of-the-years-digits method (SYD)以旧换新Trade in经营租赁Operating lease融资租赁Capital lease廉价购买权Bargain purchase option (BPO)资产负债表外筹资Off-balance-sheet financing最低租赁付款额Minimum lease payments七、无形资产无形资产Intangible assets专利权Patents商标权Trademarks, Trade names著作权Copyrights特许权或专营权Franchises商誉Goodwill开办费Organization cost租赁权Leasehold摊销Amortization八、流动负债负债Liability流动负债Current liability应付帐款Account payable应付票据Notes payable贴现票据Discount notes长期负债一年内到期部分Current maturities of long-term liabilities 应付股利Dividends payable预收收益Prepayments by customers存入保证金Refundable deposits应付费用Accrual expense增值税value added tax营业税Business tax应付所得税Income tax payable应付奖金Bonuses payable产品质量担保负债Estimated liabilities under product warranties 赠品和兑换券Premiums, coupons and trading stamps或有事项Contingency或有负债Contingent或有损失Loss contingencies或有利得Gain contingencies永久性差异Permanent difference时间性差异Timing difference应付税款法Taxes payable method纳税影响会计法Tax effect accounting method递延所得税负债法Deferred income tax liability method 九、长期负债长期负债Long-term Liabilities应付公司债券Bonds payable有担保品的公司债券Secured Bonds抵押公司债券Mortgage Bonds保证公司债券Guaranteed Bonds信用公司债券Debenture Bonds一次还本公司债券Term Bonds分期还本公司债券Serial Bonds可转换公司债券Convertible Bonds可赎回公司债券Callable Bonds可要求公司债券Redeemable Bonds记名公司债券Registered Bonds无记名公司债券Coupon Bonds普通公司债券Ordinary Bonds收益公司债券Income Bonds名义利率,票面利率Nominal rate实际利率Actual rate有效利率Effective rate溢价Premium折价Discount面值Par value直线法Straight-line method实际利率法Effective interest method到期直接偿付Repayment at maturity提前偿付Repayment at advance偿债基金Sinking fund长期应付票据Long-term notes payable抵押借款Mortgage loan十、业主权益权益Equity业主权益Owner's equity股东权益Stockholder's equity投入资本Contributed capital缴入资本Paid-in capital股本Capital stock资本公积Capital surplus留存收益Retained earnings核定股本Authorized capital stock实收资本Issued capital stock发行在外股本Outstanding capital stock库藏股Treasury stock普通股Common stock优先股Preferred stock累积优先股Cumulative preferred stock非累积优先股Noncumulative preferred stock完全参加优先股Fully participating preferred stock部分参加优先股Partially participating preferred stock非部分参加优先股Nonpartially participating preferred stock 现金发行Issuance for cash非现金发行Issuance for noncash consideration股票的合并发行Lump-sum sales of stock发行成本Issuance cost成本法Cost method面值法Par value method捐赠资本Donated capital盈余分配Distribution of earnings股利Dividend股利政策Dividend policy宣布日Date of declaration股权登记日Date of record除息日Ex-dividend date股利支付日Date of payment现金股利Cash dividend股票股利Stock dividend拨款appropriation十一、财务报表财务报表Financial Statement资产负债表Balance Sheet收益表Income Statement帐户式Account Form报告式Report Form编制(报表)Prepare工作底稿Worksheet多步式Multi-step单步式Single-step十二、财务状况变动表财务状况变动表中的现金基础SCFP.Cash Basis(现金流量表)财务状况变动表中的营运资金基础SCFP.Working Capital Basis (资金来源与运用表)营运资金Working Capital全部资源概念All-resources concept直接交换业务Direct exchanges正常营业活动Normal operating activities财务活动Financing activities投资活动Investing activities十三、财务报表分析财务报表分析Analysis of financial statements比较财务报表Comparative financial statements趋势百分比Trend percentage比率Ratios普通股每股收益Earnings per share of common stock股利收益率Dividend yield ratio价益比Price-earnings ratio普通股每股帐面价值Book value per share of common stock资本报酬率Return on investment总资产报酬率Return on total asset债券收益率Yield rate on bonds已获利息倍数Number of times interest earned债券比率Debt ratio优先股收益率Yield rate on preferred stock营运资本Working Capital周转Turnover存货周转率Inventory turnover应收帐款周转率Accounts receivable turnover流动比率Current ratio速动比率Quick ratio酸性试验比率Acid test ratio十四、合并财务报表合并财务报表Consolidated financial statements吸收合并Merger创立合并Consolidation控股公司Parent company附属公司Subsidiary company少数股权Minority interest权益联营合并Pooling of interest购买合并Combination by purchase权益法Equity method成本法Cost method十五、物价变动中的会计计量物价变动之会计Price-level changes accounting一般物价水平会计General price-level accounting货币购买力会计Purchasing-power accounting统一币值会计Constant dollar accounting历史成本Historical cost现行价值会计Current value accounting现行成本Current cost重置成本Replacement cost物价指数Price-level index国民生产总值物价指数Gross national product implicit price deflator (or GNP deflator) 消费物价指数Consumer price index (or CPI)批发物价指数Wholesale price index货币性资产Monetary assets货币性负债Monetary liabilities货币购买力损益Purchasing-power gains or losses资产持有损益Holding gains or losses未实现的资产持有损益Unrealized holding gains or losses。

会计英语名词解释

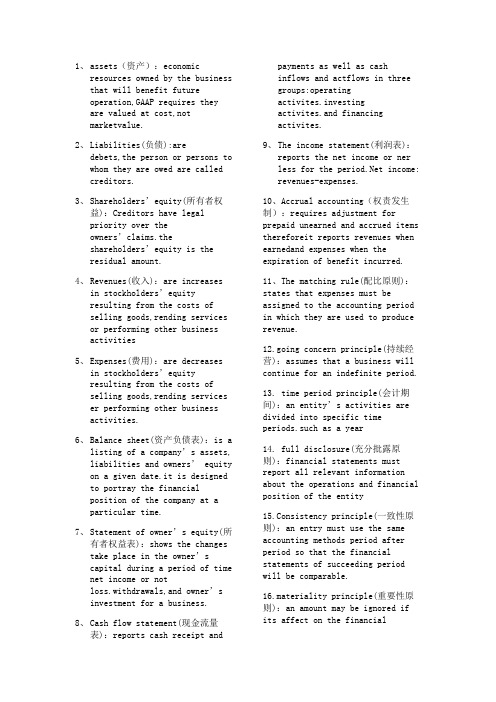

1、assets(资产):economicresources owned by the business that will benefit futureoperation,GAAP requires theyare valued at cost,notmarketvalue.2、Liabilities(负债):aredebets,the person or persons to whom they are owed are calledcreditors.3、Shareholders’equity(所有者权益):Creditors have legalpriority over theowners’claims.theshareholders’equity is theresidual amount.4、Revenues(收入):are increasesin stockholders’equityresulting from the costs ofselling goods,rending servicesor performing other businessactivities5、Expenses(费用):are decreasesin stockholders’equityresulting from the costs ofselling goods,rending serviceser performing other businessactivities.6、Balance sheet(资产负债表):is alisting of a company’s assets, liabilities and owners’ equity on a given date.it is designedto portray the financialposition of the company at aparticular time.7、Statement of owner’s equity(所有者权益表):shows the changestake place in the owner’scapital during a period of time net income or notloss.withdrawals,and owner’sinvestment for a business.8、Cash flow statement(现金流量表):reports cash receipt andpayments as well as cashinflows and actflows in threegroups:operatingactivites.investingactivites.and financingactivites.9、The income statement(利润表):reports the net income or nerless for the income: revenues-expenses.10、Accrual accounting(权责发生制):requires adjustment for prepaid unearned and accrued items thereforeit reports revenues when earnedand expenses when the expiration of benefit incurred.11、The matching rule(配比原则):states that expenses must be assigned to the accounting period in which they are used to produce revenue.12.going concern principle(持续经营):assumes that a business will continue for an indefinite period.13. time period principle(会计期间):an entity’s activities are divided into specific time periods.such as a year14. full disclosure(充分批露原则):financial statements must report all relevant information about the operations and financial position of the entity15.Consistency principle(一致性原则):an entry must use the same accounting methods period after period so that the financial statements of succeeding period will be comparable.16.materiality principle(重要性原则):an amount may be ignored if its affect on the financialstatements is not important to its users.17.conservatism principle(稳健性原则):the least optimistic estimate should be selected when two estimates of amounts to be received or paid are aboutequality likely;it is better to understate than over values.18.busniness entity principle(会计主体):each entity must keep accounting records and people reports that are distinct from those of the owner and any other entity.19.。

《会计学原理》慕课模块术语中英文对照表 (1)

王德宏《会计学原理》慕课英汉对照会计术语表模块一Accounting 会计/会计学Accounting equation 会计等式,即资产=负债+所有者权益American Accounting Association (AAA) 美国会计协会(本课程讲授者就是AAA的会员) Assets 资产,与负债相对Auditors 审计师/核数师Balance sheet 资产负债表,即综合反映企业中资产、负债和所有者权益的会计报表Bookkeeping 记账Business entity assumption 会计主体假设Code of Ethics 职业道德守则Common stock 普通股,与优先股相对Connected transaction 关联交易,也称related party transactionCorporation 公司制企业Cost principle 成本原则Equity 权益Ethics 职业道德Events 事项Expanded accounting equation 扩展会计等式,即将所有者权益再进行细分后的会计等式Expenses 费用,与收入相对External transactions 外部交易,与内部交易相对External users 外部使用者,与内部使用者相对Financial accounting 财务会计,主要用于外部使用者Financial Accounting Standards Board (FASB) (美国)财务会计准则委员会Full disclosure principle 充分披露原则Generally Accepted Accounting Principles (GAAP) 公认会计准则Going concern assumption 持续经营假设Income statement 利润表,也称损益表,主要用于报告企业的收入、费用以及利润或损失Internal transactions 内部交易,与外部交易相对Internal users 内部使用者,与外部使用者相对International Accounting Standards Board (IASB) 国际会计准则委员会International Financial Reporting Standards (IFRS) 国际财务报告准则Liabilities 负债,与资产相对Managerial accounting 管理会计,主要用于内部使用者Matching principles 配比原则Monetary unit assumption 货币计量假设Net income 净利润,出现在收入大于费用时Net loss 净损失,出现在收入小于费用时Owner, Capital 所有者资本Owner investment 所有者投资Owner withdrawal 所有者提取,例如所有者撤资和发给所有者的红利(dividends)等Partnership 合伙制企业Proprietorship 独资企业Recordkeeping 记账Related party transaction 关联交易,也称connected transactionRevenue recognition principle 收入确认原则Revenues 收入,与费用相对Sarbanes-Oxley Act 萨班斯-奥克斯利法案,美国安然事件后颁布的要求企业进行更加严格的财务报告的法案Securities and Exchange Commission (SEC) (美国)证券交易委员会Shareholders 股东Shares 股份Sole proprietorship 独资企业,本课程中专指一人制独资企业Statement of cash flows 现金流量表,用于报告企业的现金流入流出状况Statement of owner’s equity所有者权益表,也称所有者权益变动表,用于报告企业中所有者权益的变动情况,是资产负债表中所有者权益项目的深入说明Stock 股票Stockholders 股东Time period assumption 会计分期假设Withdrawals 提取模块二Account 账户Account balance 账户余额Balance column account 三栏式账户,主要特点是能够反映账户余额Chart of accounts 会计科目表Compound journal entry 复式日记账分录Credit 贷方Creditors 债权人Debit 借方Debtors 债务人Double entry accounting 复式记账General journal 普通日记账General ledger 总分类账,简称总账Journal 日记账,也称流水账Journalizing 登记日记账,即将会计原始凭证分录到日记账中Ledger 分类账Posting 过账,本课程中指将日记账登记到三栏式账户Posting reference (PR) 过账索引,本课程中指将三栏式账户与日记账相互关联的编号Source documents 会计原始凭证T-account T型账户Trial balance 试算平衡表,即统一列出各个分类账的余额,主要用于查找记账差错和后续会计处理(例如账务调整、期末关账和制作会计报表等)模块三Accounting period 会计期间,例如一个会计季度或会计年度Accrual basis accounting 权责发生制会计,也称应计制会计,是现代企业会计制度的基础Accrued expenses 预提费用,是权责发生制的一种体现Accrued revenues 应计收入,是权责发生制的一种体现Accumulated depreciation 累计折旧,是各个会计期间发生的折旧的累加Adjusted trial balance 经过账务调整后的试算平衡表,是权责发生制的一种体现Adjusting entry 调整分录,用于账务调整Annual financial statements 年度财务报表Book value 账面价值,与市场价值相对Cash basis accounting 收付实现制会计,也称现金制会计,与权责发生制会计相对Contra account 备抵账户,一类特殊账户Depreciation 折旧Fiscal year 会计年度,既可能与日历年度一致(中国等多数国家)也可能不一致(例如部分美国企业)Interim financial statements 中期财务报表,简称中报,指上半年的财务报表Natural business year 自然营业年度,大多数情况下与日历年度一致Plant assets 厂房设备资产,也称固定资产(fixed assets)Prepaid expenses 待摊费用,属于资产科目(将来会转变为费用) ,是权责发生制的一种体现Straight line depreciation method 直线折旧法,最常用和最简单的一种折旧方法Unadjusted trial balance 未经账务调整的试算平衡表Unearned revenue 预收账款,也称递延收入,属于负债科目(将来会转变为收入) ,是权责发生制的一种体现模块四Accounting cycle 会计循环,指一个会计期间内的各个会计处理过程Classified balance sheet 分类资产负债表,指将会计科目按照某种特点分组后列出的资产负债表,便于会计报表使用者阅读和分析。

会计学原理(英文)

《会计学原理(英文)》教学大纲王燕祥编写工商管理专业课程教学大纲610 目录Chapter 1 Accounting in Action 第一章会计实践活动 (613)学习目标 (613)Teaching and homework hours 教学与作业时间 (613)Reading and References 学生必读和参考书目 (613)Chapter 2 The Recording Process 第二章记录过程 (615)学习目标 (615)Teaching and homework hours 教学与作业时间 (615)Reading and References 学生必读和参考书目 (615)Chapter 3 Adjusting the Accounts 第三章调整账户 (617)学习目标 (617)Teaching and homework hours 教学与作业时间 (617)Reading and References 学生必读和参考书目 (617)Chapter 4 Completion of the Accounting Cycle 第四章完成会计循环 (619)学习目标 (619)Teaching and homework hours 教学与作业时间 (619)Reading and References 学生必读和参考书目 (619)Chapter 5 Accounting for Merchandising Operations 第五章商品经营活动的会计核算 (621)学习目标 (621)Teaching and homework hours 教学与作业时间 (621)Reading and References 学生必读和参考书目 (621)Chapter 6 Inventories 第六章存货 (623)学习目标 (623)Teaching and homework hours 教学与作业时间 (624)Reading and References 学生必读和参考书目 (624)Chapter 7 Accounting Information Systems 第七章会计信息系统 (626)学习目标 (626)Teaching and homework hours 教学与作业时间 (626)Reading and References 学生必读和参考书目 (626)Chapter 8 Internal Control and Cash 第八章内部控制和现金 (628)学习目标 (628)Teaching and homework hours 教学与作业时间 (628)Reading and References 学生必读和参考书目 (628)Chapter 9 Accounting for Receivables 第九章应收款项的会计核算 (630)学习目标 (630)Teaching and homework hours 教学与作业时间 (630)Reading and References 学生必读和参考书目 (630)Chapter 10 Plant Assets, Natural Resources, and Intangible Assets 第十章厂场资产、自然资源和无形资产 (632)会计学原理(英文)学习目标 (632)Teaching and homework hours 教学与作业时间 (632)Reading and References 学生必读和参考书目 (633)Chapter 11 Current Liabilities and Payroll Accounting 第十一章流动负债和工资的核算 (634)学习目标 (634)Teaching and homework hours 教学与作业时间 (634)Reading and References 学生必读和参考书目 (634)Chapter 12 Accounting Principles 第十二章会计原则 (636)学习目标 (636)Teaching and homework hours 教学与作业时间 (636)Reading and References 学生必读和参考书目 (636)Chapter 13 Accounting for Partnerships 第十三章合伙企业的会计核算 (638)学习目标 (638)Teaching and homework hours 教学与作业时间 (638)Reading and References 学生必读和参考书目 (638)Chapter 14 Corporations: Organization and Capital Stock Transactions 第十四章公司:组织和股本交易 (640)学习目标 (640)Teaching and homework hours 教学与作业时间 (640)Reading and References 学生必读和参考书目 (640)Chapter 15 Corporations: Dividends, Retained Earnings, and Income Reporting 第十五章股利、保留盈余和收益报告 (642)学习目标 (642)Teaching and homework hours 教学与作业时间 (642)Reading and References 学生必读和参考书目 (642)Chapter 16 Long-Term Liabilities 第十六章长期负债 (644)学习目标 (644)Teaching and homework hours 教学与作业时间 (644)Reading and References 学生必读和参考书目 (644)Chapter 17 Investments 第十七章投资 (646)学习目标 (646)Teaching and homework hours 教学与作业时间 (646)Reading and References 学生必读和参考书目 (646)Chapter 18 The Statement of Cash Flows 第十八章现金流量表 (648)学习目标 (648)Teaching and homework hours 教学与作业时间 (648)Reading and References 学生必读和参考书目 (648)Chapter 19 Financial Statement Analysis 第十九章财务报表分析 (650)学习目标 (650)Teaching and homework hours 教学与作业时间 (650)Reading and References 学生必读和参考书目 (650)Chapter 20 Managerial Accounting 第二十章管理会计 (652)611工商管理专业课程教学大纲612 学习目标 (652)Teaching and homework hours 教学与作业时间 (652)Reading and References 学生必读和参考书目 (652)Chapter 21 Job Order Cost Accounting 第二十一章分批成本法 (654)学习目标 (654)Teaching and homework hours 教学与作业时间 (654)Reading and References 学生必读和参考书目 (654)Chapter 22 Process Cost Accounting 第二十二章分步成本法 (656)学习目标 (656)Teaching and homework hours 教学与作业时间 (656)Reading and References 学生必读和参考书目 (657)Chapter 23 Cost-V olume-Profit Relationships 第二十三章本量利分析 (658)学习目标 (658)Teaching and homework hours 教学与作业时间 (658)Reading and References 学生必读和参考书目 (659)Chapter 24 Budgetary Planning 第二十四章编制预算 (660)学习目标 (660)Teaching and homework hours 教学与作业时间 (660)Reading and References 学生必读和参考书目 (660)Chapter 25 Budgetary Control and Responsibility Accounting 第二十五章预算控制和责任会计 662 学习目标 (662)Teaching and homework hours 教学与作业时间 (662)Reading and References 学生必读和参考书目 (662)Chapter 26 Performance Evaluation through Standard Costs 第二十六章利用标准成本进行业绩评价 (664)学习目标 (664)Teaching and homework hours 教学与作业时间 (664)Reading and References 学生必读和参考书目 (664)Chapter 27 Incremental Analysis and Capital Budgeting 第二十七章增量分析和资本预算 (666)学习目标 (666)Teaching and homework hours 教学与作业时间 (667)Reading and References 学生必读和参考书目 (667)会计学原理(英文)Chapter 1 Accounting in Action第一章会计实践活动STUDY OBJECTIVESAfter studying this chapter you should be able to:1.Explain what accounting is.2.IDENTIFY THE USERS AND USES OF ACCOUNTING.3.UNDERSTAND WHY ETHICS IS A FUNDAMENTAL BUSINESS CONCEPT.4.EXPLAIN THE MEANING OF GENERALLY ACCEPTED ACCOUNTING PRINCIPLESAND THE COST PRINCIPLE.5.EXPLAIN THE MEANING OF THE MONETARY UNIT ASSUMPTION AND THE ECONOMIC ENTITY ASSUMPTION.6.STATE THE BASIC ACCOUNTING EQUATION AND EXPLAIN THE MEANING OF ASSETS, LIABILITIES, AND OWNER’S EQUITY.7.ANALYZE THE EFFECT OF BUSINESS TRANSACTIONS ON THE BASIC ACCOUNTING EQUATION.8.Understand what the four financial statements are and how they are prepared.学习目标学完本章之后,学生应该能够达到以下目标:1.解释什么是会计。

会计专业外语名词解释

会计专业外语名词解释专业英语名词解释Capital structure 资本结构The makeup of the liabilities and stockholders' equity side of the balance sheet, especially the ratio of debt to equity and the mixture of short and long maturities.Contingent claim 未定权益A claim that can be made only if one or more specified outcomes occur. In the words of finance theory, debt and equity securities are contingent claims on the total firm value.Sole proprietorship 独资企业A business owned by a single individual. A sole proprietor pays no corporate income tax but has unlimited liability for business debts and obligations.Partnership 合伙企业Shared ownership among two or more individuals, some of whom may, but do not necessarily, have limited liability with respect to obligations of the group. See: General partnership, limited partnership, and master limited partnership.Corporation 公司;法人A legal entity that is separate and distinct from its owners. A corporation is allowed to own assets, incur liabilities, and sell securities, among other things.income trust 信托An income trust is an investment that may hold equities, debt instruments, royalty interests or real properties. The trust can receive interest, royalty or lease payments from an operating entity carrying on a business, as well as dividends and a return of capitalAgency costs 代理成本The costs of resolving the conflicts of interest between managers and shareholders are special types of costs called agency costsSet of Contracts Perspective 组合同角度The belief that different stakeholders in the corporation have different interests that often, or always, conflict. For example, managers may be concerned about the company's ability to make a long-term profit while shareholders (especially traders) may consider primarily short term gains. Likewise, management may be interested in reducing expenses, while the union representing employees are most concerned with increasing members' wages and benefits.Stakeholder 利益相关者Any party that has an interest in an organization. Stakeholders of a company include stockholders, bondholders, customers, suppliers, employees, and so forth.Financial institution 金融机构An enterprise such as a bank whose primary business and function is to collect money from the public and invest it in financial assets such as stocks and bonds, loans and mortgages, leases, and insurance policies.Financial market 金融市场An organized institutional structure or mechanism for creating and exchanging financial assets. Money Market 货币市场Money Market are the markets for trading of highly liquid, short-term assets and securities Capital markets 资本市场Capital markets are the markets for long-term debt and shares of stock.Primary market 一级市场Where a newly issued security is first offered by the corporation.Secondary market 二级市场The market in which securities are traded after they are initially offered in the primary market. Most trading occurs in the secondary market.Listing 上市Stocks that trade on an organized exchange are said to be listed on that exchange.Foreign exchange market 外汇市场Largely banks that serve firms and consumers who may wish to buy or sell various currencies. Capital budgeting 资本预算The process of choosing the firm's long-term assets.Capital gains资本收益When a stock is sold for a profit, the capital gain is the difference between the net sales price of the securities and their net cost, or original basis. If a stock is sold below cost, the difference is a capital loss.Net Working Capital 净营运资本Cash and short-term assets expected to be converted to cash within a year less short-term liabilitiesSocially responsible investing社会责任投资Any investment philosophy that recommends investment decisions based upon a decision's ethical implications for individuals and companies,such funds screen and select securities based on social or environmental criteria.。

会计学原理专业英语词汇对照(第一二章)

会计学原理专业英语词汇对照第一章:必知词汇accounting会计recordkeeping or bookkeeping簿记shareholders股东board of directors董事会auditors审计suppliers供应商creditor债权人ethics职业道德GAAP公认会计原则(美国)SEC证券交易委员会(美国)FASB财务会计准则委员会(美国)IASB国际会计准则理事会(国际)IFRS国际财务报告准则(国际)Relevant相关Reliable可靠Comparable可比Principles原则The measurement principle/ the cost principle计量原则/ 成本原则The revenue recognition principle收入确认原则The expense recognition principle/ the matching principle支出确认原则/配比原则Sale on credit/ on account 赊销Purchase on credit/on account赊购The full disclosure principle充分披露原则Assumptions假设The going-concern assumption持续经验假设The monetary unit assumption货币计量假设The time period assumption会计分期假设The business entity assumption会计主体假设Sole proprietorship独资企业Unlimited liability无限责任Partnership合伙企业Corporation公司Double taxation双重课税Expanded accounting equation扩展会计等式Assets资产Liabilities负债Owners, equity 所有者权益Net assets净资产Owners, capital所有者资本Owners, withdrawals所有者提取/所有者抽回投资Expenses费用Revenue收入Net income净利润Net loss净损失Income statement利润表Statement of owners, equity所有者权益表/所有者权益变动表Balance sheet资产负债表Statement of cash flows现金流量表第二章:必知词汇(上文有的不再重复)Accounting books/books会计帐簿Source documents原始凭证Account账户General ledger总分类账Ledger分类账Account receivable应收账款Note receivable应收票据Prepaid accounts/ prepaid expenses预付账款/待摊费用Account payable应付账款Note payable应付票据Unearned revenue预收账款Accrued liabilities应计负债Increase增加Decrease减少Chart of accounts会计科目表T-account T形账户Debit借方(Dr.)Credit贷方(Cr.)Account balance账户余额Normal balance正常余额Double entry accounting 复式记账法Journalizing登记日记账Journal日记账General journal普通日记账Journal entry日记账分录Posting过账Balance column account三栏式账户PR(posting reference)过账索引Trial balance试算平衡表Unadjusted statements调整前的财务报表必记口诀:有借必有贷,借贷必相等。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

《会计学原理》名词解释1.Accounting: is an information and measurement system thatidentifies records and communicates relevant reliable and comparable information about an organization’s business activities.(P2)2.Managerial accounting: is the area of accounting that servesthe decision-marking needs of internal users.(P4)3.Events: refer to happenings that affect an entity’saccounting equation and can be reliably measured.(P11) 4.External user: of accounting information are not directlyinvolved in running the organization.(P3)5.Internal user: of accounting information are those directlyefficiency and effectiveness of an organization.(P4)6.Ethics: are beliefs that distinguish right from wrong. Theyare accepted standards of good and bad behavior.(P5)7.Cost principle: means that accounting information is basedon actual cost.(P7)8.Revenue recognition principle: provides guidance on when acompany must recognize revenue.(P7)9.Matching principle: prescribes that a company must recordsits expenses incurred to generate the revenue reported.(P7) 10.Going-concerning assumption: means that accountinginformation reflects a presumption that the business will continue operating instead of being closed or sold.(P7) 11.Audit: through review of an organization’s accountingrecords and accounting reports and return make by the analysis. income:amount a business earns after paying allexpenses and costs associated with its sales and revenues.(P15)13.Income statement: describes a company’s revenues andexpenses along with the resulting net income or loss overa period time due to earnings activities.(P14)14.Statement of owner’s equity: explains changes in equityfrom net income (or loss) and from any owner investments and withdrawals over a period of time.(P14)15.Balance sheet: describ es a company’s financialposition (types and amounts of assets liabilities and equity) at a point in time.(P15)16.Statement of cash flows: identifies cash inflows(receipts) and cash outflows (payments) over a period of time.(P15)17.Owner’s withdrawals account: the account used to recordthe transfers of assets from a business to its owner. (P31)18.Liabilities: is what a company owes its no owners(creditors) in future payments, products, or services.(P10)19.Accounting equation: Assets=Liabilities + Equity.(P10)20.Accrued expense: refer to costs that are incurred in aperiod but are both unpaid and unrecorded.(P66)21.Operating cycle: is the time span from when cash is usedto acquire goods and services until cash is received from the sale of goods and services. (P96)22.Shareholders (investors): are the owners of acorporation. (P3)23.Current radio: a ratio used to help evaluate a company’sability to pay its debts in the near future.24.Merchandise inventory: refers to products that a companyowns and intends to sell.(P113)25.Cash discount: reduction in a receivable or payable ifit is paid within the discount period. sellers can grant a cash discount to discourage buyers to pay earlier(P137) 26.Gross profit: also called Gross margin, which equals netsales cost of goods sold.(P137)27.Credit period: the amount of time allowed before fullpayment is due.(P137)28.Acid-test ratio: a ratio used to assets a company’sability to pay its current liabilities; defined by current liabilities.29.Selling expense: include the expenses of promoting salesby displaying and advertising merchandise, making sales, and delivering goods to customers.(P124)30.General and administrative expense: support a company’soverall operations and include expenses related to accounting, human resource management, and financial management.(P124)31.Time period assumption: presumes that the life of acompany can be divided into time periods, such as months and years, and that useful reports can be prepared for those periods.(P7)32.Account receivable: are held by a seller and decreasedby customers to sellers.(P29)33.Prepaid account (also called prepaid expenses): areassets that represent prepayments of future expenses (not current expenses). (P29)34.Unearned revenue: refers to a liability that is settledin the future when a company delivers its products or services.(P30)35.Accrued liabilities: is the company’s debt owed. Forexample, salaries payable, taxes payable, and interest payable and so on.(P31)36. Purchase discount: purchaser’s description of a cashdiscount received from a supplier of goods.(P137)37.Sales discount: seller’s description of a cash discountgranted to buyers in return for early payment.(P137)38.Trade discount: reduction below list or catalog price hatis negotiated in setting the price of goods.(P137)39.FOB shipping point (FOB factory): means the buyer acceptsownership when the goods depart the seller’s place of business.(P117)40.FOB destination: means ownership of goods transfers tothe buyer when the goods arrive at the buyer’s place of business. (P117)41.Credit terms: for a purchase include the amounts andtiming of payments from a buy to a seller.(P114)42.Current assets: are cash and other resources that areexpected to be sold, collect, or used within one year or the company’s operating cycle, whichever is longer.(P97) 43.Plant assets: refers to long-term tangible assets usedto produce and sell products and services.(P98)44.Long-term investment: notes receivable and investmentsin stocks and bonds are long-term assets when they are expected to be held for more than the longer of one year or the operating cycle.(P98)45.Intangible assets: are long-term resources that benefitbusiness operations, usually lack physical form, and have uncertain benefits. (P98)46.Current liabilities: are obligations due to be paid orsettled within one year or the operating cycle, whichever is longer.(P98)47.Long-term liabilities: are obligations not due withinone year or the operating cycle, whichever is longer.(P98) 48.Accounting cycle: refers to the steps in preparingfinancial statements.(P95)49.Temporary (or nominal) accounts: accumulate data relatedto one accounting period.(P91)50.Permanent (or real) accounts: report on activitiesrelated to one or more future accounting periods.(P91)。