会计学基础英文课件 (6)

国际会计学课件cha6 Foreign Currency Accounting

• To record foreign currency tranctions.

• The expanded scale of international investment increases the need to transfer accounting information from one country to users in others.

• *6.Foreign currency . • A currency other than the currency of the country being referred to; A currency other than the reporting currency of the enterprise being referred to. • 外币:特定国家的非本国货币;特定企业的非报告货 币. • *7.Foreign currency financial statement. Financial statement that employ foreign currency as the unit of measure. • 外币财务报表:以外币作为计量单位的财务报表.

• 2.Indirect exchange rate (quote) • (Receivable Quote 应收法) • It is the reciprocal(倒数)of the direct quote, the price of a unit of domestic currency in terms of the foreign currency. It would take approximately 0.1639 U.S dollar to acquire 1 Chinese yuan .

基础会计学四单元课件英文版PPT课件

Salaries payable

Unearned consulting revenue

C. Taylor, Capital

C. Taylor, Withdrawals

200

Consulting revenue

Rental revenue

Depreciation expense-Equipment

375

Debit

Cash

$ 4,350

Accounts receivable

1,800

Supplies

8,670

Prepaid insurance

2,300

Equipment

26,000

Accumulated depreciation-Equip.

Accounts payable

Salaries payable

8,670

Prepaid insurance

2,300

Equipment

26,000

Accumulated depreciation-Equip.

Accounts payable

Salaries payable

Unearned consulting revenue

C. Taylor, Capital

balance columns

4 Extend adjusted trial balance amounts to the F/S

columns

5 Total F/S columns, compute net income or loss, and

complete the worksheet

4-7

Unearned consulting revenue

会计学英语电子版ppt课件

15

Operating Activities

Primary activity of business

Selling goods Providing services Manufacturing Cost of Sales Advertising Paying employees Paying utilities

3. Explain the three principal types of business activity.

4. Describe the content and purpose of each of the financial statements.

3

Study Objectives

5. Explain the meaning of assets, liabilities, and stockholders’ equity, and state the basic accounting equation.

6. Describe the components that supplement the financial statements in an annual report.

4

111 Forms of Business Organization

Sole proprietorship Partnership Corporation

11

Users of Financial Information

External Users Ask?

12

311

Types of Business Activity

《会计学基础》(第二版)配套课件 第六章案例分析答案

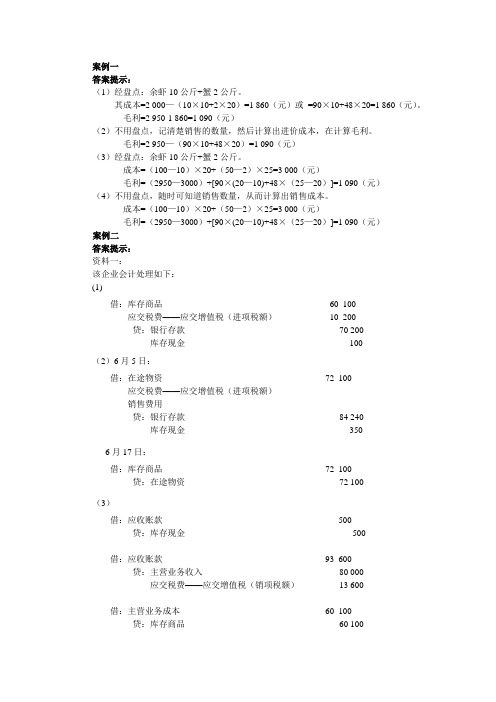

案例一答案提示:(1)经盘点:余虾10公斤+蟹2公斤。

其成本=2 000—(10×10+2×20)=1 860(元)或=90×10+48×20=1 860(元)。

毛利=2 950-1 860=1 090(元)(2)不用盘点,记清楚销售的数量,然后计算出进价成本,在计算毛利。

毛利=2 950—(90×10+48×20)=1 090(元)(3)经盘点:余虾10公斤+蟹2公斤。

成本=(100—10)×20+(50—2)×25=3 000(元)毛利=(2950—3000)+[90×(20—10)+48×(25—20)]=1 090(元)(4)不用盘点,随时可知道销售数量,从而计算出销售成本。

成本=(100—10)×20+(50—2)×25=3 000(元)毛利=(2950—3000)+[90×(20—10)+48×(25—20)]=1 090(元)案例二答案提示:资料一:该企业会计处理如下:(1)借:库存商品60 100应交税费——应交增值税(进项税额)10 200贷:银行存款70 200库存现金100(2)6月5日:借:在途物资72 100应交税费——应交增值税(进项税额)销售费用贷:银行存款84 240库存现金350 6月17日:借:库存商品72 100贷:在途物资72 100(3)借:应收账款500贷:库存现金500借:应收账款93 600贷:主营业务收入80 000应交税费——应交增值税(销项税额)13 600借:主营业务成本60 100贷:库存商品60 100(4)6月23日:借:应收账款500 贷:库存现金500借:应收账款87 750 贷:主营业务收入75 000 应交税费——应交增值税(销项税额) 2 750借:主营业务成本72 100 贷:库存商品72 1006月25日:借:银行存款87 750 贷:应收账款87 750资料二:借:库存商品——电视250 000 应交税费——应交增值税(进项税额)34 000贷:应付账款234 000 商品进销差价50 000借:库存商品——食品150 000 应交税费——应交增值税(进项税额)17 000贷:应付账款117 000 商品进销差价50 000借:库存商品——日用百货300 000 应交税费——应交增值税(进项税额)34 000贷:应付票据234 000 商品进销差价100 000借:银行存款620 000 贷:主营业务收入620 000借:主营业务成本620 000 贷:库存商品620 000借:主营业务收入贷:应交税费——应交税费(销项税额)借:商品进销差价贷:主营业务成本。

会计英语—基础会计

depreciation expense

折旧费用

post-closing trial balance

结账后试算平衡

可编辑ppt

26

prepaid expense 待摊费用

insurance policies 保险,保单

income summary 收益汇总,本年利润

miscellaneous expenses

杂项费用,其他费用

可编辑ppt

27

revenue earned 已实现收入

unearned revenue 预收账款(未实现收

入)

可编辑ppt

28

Chapter 7

可编辑ppt

29

financial statement 财务报表

income statement 利润表

可编辑ppt

17

credit 贷方

source document 原始凭证

permanent accounts 永久性账户

temporary account 临时性账户

可编辑ppt

18

journalizing 记日记账

book of original entry

原始分录的记录

14

net income 净收益

net loss 净损失

expense 费用

revenue 收入

可编辑ppt

15

Chapter 4

可编辑ppt

16

account 账户

T-account T形账户

double-entry accounting

复式记账制

debit 借方

accounting period 会计分期

《英文版基础会计学》PPT课件

Seek different chance to maximize his own interests;

When we define human being as REMM, we have to solve the fundamental issue:

The value must be fundamental and the society could not go without;

Another way to explain: Darwinism;

Natural selection and the fittest survive;

6

The Nature of Firm

business;

DEB: the symbol of accounting science;

18

The Evolution of Accounting

From Bookkeeping to Financial Accounting

Capital market: accounting information is widely circulated;

Decision making: much more complicated;

Management Accounting is “invented”;

21

The Evolution of Accounting

From commodity market to capital market; The developing of capital market raises two

REMMs have to find efficient ways to develop and maintain trust;

大学课程《会计英语》PPT课件:Chapter 6 Unit 1

1. Plant And Equipment 固定资产 2.Trade In 以旧换新 3.Betterments 改造投资 4.Additions 扩建 5.Disposal Of Plant And Equipment 固定资

产处置 6.Property Taxes 财产税

Continued

Only reasonable and necessary expenditures should be included.

Determining the Cost of Assets

Purchased for Cash

Cost is most easily determined when an asset is purchased for cash. The cost of the asset is then equal to the cash outlay necessary in acquiring the asset plus any expenditures for freight, insurance while in transit, installation, trial runs and any other costs necessary to make the asset ready for use.

AccountingBasics英语会计基础教学课件期末复习

If using ageing method

ADJUST for any existing balance in impairment account

Overview | ASSETS ~ Inventories

Dividends

EVERYONE wants it!!! So, we need internal control procedures. A fundamental internal control procedure for cash is the bank

reconciliation statement. In Week 5, our example was Friends Ltd. Key items in a bank reconciliation

Chapters…remember these ones???

Chapter 6 - Inventories – FIFO/LIFO/WA Chapter 7 - Accounting information systems Chapter 8 - Internal control and cash Chapter 9 - Accounting for receivables Chapter 11 - Current liabilities Chapter 10 - Non-current assets (PPE) Chapter 16 - Non-current liabilities Chapter 14 - Share capital Chapter 15 - Dividends & retained earnings Chapter 19 - Financial statement analysis Chapter 18 - Cash flow statements Chapter 20 - Management accounting Chapter 23 - Budgeting

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Income Statement Balance Sheet

Inventory Systems

Perpetual Method

Gives a continual record of the amount of inventory on hand. When an item is sold it is recorded in the Cost of Goods Sold account.

• • The operating cycle of merchandise companies involves the purchase and subsequent sale of merchandise inventory. Purchase of inventory can either on account or by cash.

9

Inventory Systems

• Perpetual provides a continuous record of: – The amount of inventory on hand. – Cost of goods sold to date.

• Periodic requires a physical count of goods to determine:

15

Purchase Discounts

• Purchase discount is a deduction from the invoice price granted to induce early payment of the amount due. Example – 2/10, n30

Terms Time

Example

MarCo, Inc. offers a 20% trade discount on orders of 100 units or more of their popular product Racer. Each Racer has a list price of $5.00.

Quantity sold 100 Price per unit $ 5.00 Total 500 Less 20% discount (100) Invoice price $ 400

4

Reporting Financial Performance

• Service organizations sell time to earn revenue.

– Examples: accounting firms, law firms, and plumbing services

Revenues

Cost of Goods Available for Sale

Less: Ending Inventory Measured at end of period by physical inventory count

Cost of Good Sold

Computed as a residual amount at end of period

At the end of accounting period

Cost of Goods Sold XX No entry Inventory (beginning) XX Purchases XX Inventory (ending) XX Cost of goods Sold XX

13

Merchandise Purchases

Oct.31

Due

Purchase

16

Purchase Discounts

2/10,n/30

Discount Percent Number of Days Discount Is Available

Otherwise, Net (or All) Is Due

Credit Period

17

Purchase Discounts

Measured at every sale based on perpetual record

11

Comparison of Periodic and Perpetual Systems

Transaction Periodic XX Perpetual Inventory XX Accounts Payable XX

Net Sales

-

Cost of Goods Sold

=

Gross Profit

-

Expenses

=

Net Income

6

Operating Cycle of Merchandise Companies

• Begins with the purchase of merchandise and ends with the collection of cash from the sale of merchandise.

2

Introduction

• Scandals in stock market occur now and then. Among them, financial frauds or income manipulation are common. Income manipulation typically starts from making up sales revenues as well as purchases, for example, GuangXia (Yinchuan). • In this lesson you are required to think about,

• Assume the purchase of $4,000 inventory on October 1 was on the terms 2/10,n30. Case 1-Discount taken

Oct.11 Accounts Payable 4,000 Inventory 80 Cash 3,920 2% x (5,000 - 1,000) = 80

Oct.1

Discount Period = 10 days

Credit Period = 30 days

Oct.11

(Full amount minus 2% discount) due between Oct.1 and Oct.11 Full amount due anytime between Oct.12 and Oct.31

12

Comparison of Periodic and Perpetual Systems

Transaction Merchandise retuned by customer Periodic Sales Returns & Allow. XX Accounts Receivable XX Perpetual Sales Returns & Allow. XX Accounts Receivable XX Inventory XX Cost of Goods Sold XX

– The amount of inventory on hand. – Cost of goods sold.

10

Comparison of Perpetual and Periodic Systems

Source of Information Equation Beginning Inventory Add: Purchases Equals: Periodic System Carried over from prior period Accumulated in the Purchases account Perpetual System Carried over from prior period Accumulated in the inventory account Perpetual record updated at every sale

Periodic Method

Requires updating the inventory account only at the end of the period. Acquisition of merchandise inventory is recorded in a temporary Purchases account.

Case 2-Discount not taken

Oct.31 Accounts Payable Cash

Oct. 1 Inventory 5,000 Accounts Payable /cash Purchased inventory. 5,000

14

Trade Discounts

Trade discounts are used by manufacturers and wholesalers to change selling prices without republishing their catalogs.

Lesson 6 Accounting for Merchandising Activities

Task Team of FUNDAMNTAL ACCOUNTING

School of Business, Sun Yat-sen University

Outline

• • •

•

•

•

•

Merchandising activities Operating cycle of merchandising companies Merchandising cost accounts Inventory systems Merchandise purchases Sales transactions Adjusting and closing entries

Cash Sale