《国际经济学》教师手册及课后习题答案(克鲁格曼,第六版)imch07

国际经济学课后练习题答案

增加所导致的,对该国贸易品需求的增加会使该国贸 易品价格上涨,导致实际价格总水平上升,实际汇率 升值。另外,贸易品部门劳动生产率的提高会导致实 际汇率升值,而这个实际汇率的升值对出口部门是有 利的。

•4/11/2020

课后练习题第3题

·当非贸易品的价格相对于贸易品价格上升时,非

•4/11/2020

·E. 没有发生市场交易,无需记入经常项目或金融

项目。

· F. 这种离岸交易不会记入美国的国际收支账户。

•4/11/2020

课后练习题第4题

·电话录音机的购买对于纽约州应记入经常项目的

借方(进口了产品),对于新泽西州而言,要记 入经常项目的贷方(出口了产品)。

·那当么新记泽入西纽公约司州将金所融得项的目支的票贷存方入(纽资约本州流的入银)行,时,

另一部分是收益,则是伦敦银行对这笔存款支付的10% 的利息。

因此,在伦敦银行存款的年收益率是-8%+10%=2%

•4/11/2020

第5题

· a. 实际收益率=25%-10%=15% · b. 实际收益率=20%-10%=10% · c. 实际收益率=2%-10%=-8%

•4/11/2020

第6题

际货币需求量的减少,价格水平同比例上升,导 致实际货币供应量减少,从M/P1到M/P2,利率恢 复到实际货币需求量减少到以前的水平。同时, 持续的货币需求减少会使外汇市场有本币贬值的 预期,导致了外国资产的本币收益率提高。汇率 从E1到E2,到E4.

•4/11/2020

•4/11/2020

Chapter 14 第2题

贸易品支出的增加会导致实际汇率升值。

·外国转向对本国出口产品的需求,会导致对本国

国际经济学第六版中文版克鲁格曼课后习题答案

指导手册伴随克鲁格曼& Obstfeld国际经济学:理论和政策第六版第一章介绍组织章国际经济是什么呢?贸易收益的贸易的模式保护主义国际收支汇率的决心国际政策协调国际资本市场国际经济学:贸易和资金章概述本章的目的是提供概述,国际经济的主题,并提供一种指导组织的文本。

它是相对容易的讲师激励研究国际贸易和金融。

报纸的头版,杂志的封面,导致电视新闻广播的报道预示着美国经济的相互依存与世界其他国家的。

这种相互依存关系可能也会被学生通过他们购买进口的各种各样的商品,他们的个人观测的影响由于国际竞争的混乱,和他们的经验通过出国旅行。

理论的学习国际经济学生成一个理解许多关键事件,塑造我们的国内和国际环境。

在最近的历史,这些事件包括成因及后果的巨额经常账户赤字的美国;显著升值的美元在1980年代的前半期后跟其快速折旧在第二个一半的1980年代,拉丁美洲债务危机的1980年代和墨西哥危机在1994年末;和不断上升的压力,保护不受外国竞争的行业广泛表达了在1980年代后期和更为强烈拥护在1990年代的前半期。

最近,金融危机始于东亚在1997年和年蔓延到世界各地的许多国家,经济和货币联盟在欧洲已经强调了w第二章劳动生产率和比较优势:李嘉图模型组织章比较优势的概念一个单因素经济生产可能性相对价格和供应贸易在单因素的世界箱:比较优势在实践:贝比鲁斯的情况确定相对价格在贸易贸易收益的一个数值例子箱:非贸易的损失相对工资误解的比较优势生产力和竞争力穷人劳动力参数剥削箱:工资反映生产力?比较优势与许多商品设置模型相对工资和专业化确定相对工资与Multigood模型增加运输成本和非贸易商品经验证据在李嘉图模型摘要章概述李嘉图模型的介绍了国际贸易理论。

这个最基本的模型的贸易涉及两个国家,两种商品,和一个生产要素、劳动。

在相对劳动生产率差异各国引起国际贸易。

这李嘉图模型,简单,产生重要的见解关于比较优势和从交易中获利。

这些观点有必要的基础提出了更复杂的模型在后面的章节。

国际经济学克鲁格曼课后习题答案章完整版

国际经济学克鲁格曼课后习题答案章集团标准化办公室:[VV986T-J682P28-JP266L8-68PNN]第一章练习与答案1.为什么说在决定生产和消费时,相对价格比绝对价格更重要?答案提示:当生产处于生产边界线上,资源则得到了充分利用,这时,要想增加某一产品的生产,必须降低另一产品的生产,也就是说,增加某一产品的生产是有机会机本(或社会成本)的。

生产可能性边界上任何一点都表示生产效率和充分就业得以实现,但究竟选择哪一点,则还要看两个商品的相对价格,即它们在市场上的交换比率。

相对价格等于机会成本时,生产点在生产可能性边界上的位置也就确定了。

所以,在决定生产和消费时,相对价格比绝对价格更重要。

2.仿效图1—6和图1—7,试推导出Y商品的国民供给曲线和国民需求曲线。

答案提示:3.在只有两种商品的情况下,当一个商品达到均衡时,另外一个商品是否也同时达到均衡?试解释原因。

答案提示:4.如果生产可能性边界是一条直线,试确定过剩供给(或需求)曲线。

答案提示:5.如果改用Y商品的过剩供给曲线(B国)和过剩需求曲线(A国)来确定国际均衡价格,那么所得出的结果与图1—13中的结果是否一致?6.答案提示:国际均衡价格将依旧处于贸易前两国相对价格的中间某点。

7.说明贸易条件变化如何影响国际贸易利益在两国间的分配。

答案提示:一国出口产品价格的相对上升意味着此国可以用较少的出口换得较多的进口产品,有利于此国贸易利益的获得,不过,出口价格上升将不利于出口数量的增加,有损于出口国的贸易利益;与此类似,出口商品价格的下降有利于出口商品数量的增加,但是这意味着此国用较多的出口换得较少的进口产品。

对于进口国来讲,贸易条件变化对国际贸易利益的影响是相反的。

8.如果国际贸易发生在一个大国和一个小国之间,那么贸易后,国际相对价格更接近于哪一个国家在封闭下的相对价格水平?答案提示:贸易后,国际相对价格将更接近于大国在封闭下的相对价格水平。

克鲁格曼国际经济学的教师手册

*

The External Balance Problem of the United States Worldwide Inflation and the Transition to Floating Rates Summary

Macroeconomic Policy Goals in an Open Economy

Copyright © 2003 Pearson Education, Inc.

*

Macroeconomic Policy Goals in an Open Economy

External Balance: The Optimal Level of the Current Account External balance has no full employment or stable prices to apply to an economy’s external transactions. An economy’s trade can cause macroeconomic problems depending on several factors: The economy’s particular circumstances Conditions in the outside world The institutional arrangements governing its economic relations with foreign countries

Macroeconomic Policy Goals in an Open Economy International Macroeconomic Policy Under the Gold Standard, 1870-1914 The Interwar Years, 1918-1939 The Bretton Woods System and the International Monetary Fund Internal and External Balance Under the Bretton Woods System Analyzing Policy Options Under the Bretton Woods System

克鲁格曼国际经济学课后答案

克鲁格曼国际经济学课后答案【篇一:克鲁格曼《国际经济学》(国际金融)习题答案要点】lass=txt>第12章国民收入核算和国际收支1、如问题所述,gnp仅仅包括最终产品和服务的价值是为了避免重复计算的问题。

在国民收入账户中,如果进口的中间品价值从gnp中减去,出口的中间品价值加到gnp中,重复计算的问题将不会发生。

例如:美国分别销售钢材给日本的丰田公司和美国的通用汽车公司。

其中出售给通用公司的钢材,作为中间品其价值不被计算到美国的gnp中。

出售给日本丰田公司的钢材,钢材价值通过丰田公司进入日本的gnp,而最终没有进入美国的国民收入账户。

所以这部分由美国生产要素创造的中间品价值应该从日本的gnp中减去,并加入美国的gnp。

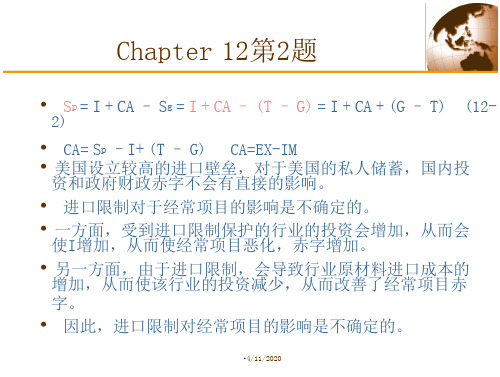

2、(1)等式12-2可以写成ca?(sp?i)?(t?g)。

美国更高的进口壁垒对私人储蓄、投资和政府赤字有比较小或没有影响。

(2)既然强制性的关税和配额对这些变量没有影响,所以贸易壁垒不能减少经常账户赤字。

不同情况对经常账户产生不同的影响。

例如,关税保护能提高被保护行业的投资,从而使经常账户恶化。

(当然,使幼稚产业有一个设备现代化机会的关税保护是合理的。

)同时,当对投资中间品实行关税保护时,由于受保护行业成本的提高可能使该行业投资下降,从而改善经常项目。

一般地,永久性和临时性的关税保护有不同的效果。

这个问题的要点是:政策影响经常账户方式需要进行一般均衡、宏观分析。

3、(1)、购买德国股票反映在美国金融项目的借方。

相应地,当美国人通过他的瑞士银行账户用支票支付时,因为他对瑞士请求权减少,故记入美国金融项目的贷方。

这是美国用一个外国资产交易另外一种外国资产的案例。

(2)、同样,购买德国股票反映在美国金融项目的借方。

当德国销售商将美国支票存入德国银行并且银行将这笔资金贷给德国进口商(此时,记入美国经常项目的贷方)或贷给个人或公司购买美国资产(此时,记入美国金融项目的贷方)。

最后,银行采取的各项行为将导致记入美国国际收支表的贷方。

《国际经济学》克鲁格曼(第六版)习题答案imsect4

OVERVIEW OF SECTION IV: INTERNATIONAL MACROECONOMIC POLICYPart IV of the text is comprised of five chapters:Chapter 18 The International Monetary System, 1870-1973Chapter 19 Macroeconomic Policy and Coordination Under Floating Exchange Rates Chapter 20 Optimum Currency Areas and The European ExperienceChapter 21 The Global Capital Market: Performance and Policy ProblemsChapter 22 Developing Countries: Growth, Crisis, and ReformSECTION OVERVIEWThis final section of the book, which discusses international macroeconomic policy, provides historical and institutional background to complement the theoretical presentation of the previous section. These chapters also provide an opportunity for students to hone their analytic skills and intuition by applying and extending the models learned in Part III to a range of current and historical issues.The first two chapters of this section discuss various international monetary arrangements. These chapters describe the workings of different exchange rate systems through the central theme of internal and external balance. The model developed in the previous section provides a general framework for analysis of gold standard, reserve currency, managed floating, and floating exchange-rate systems.Chapter 18 chronicles the evolution of the international monetary system from the gold standard of 1870 - 1914, through the interwar years, and up to and including the post-war Bretton Woods period. The chapter discusses the price-specie-flow mechanism of adjustment in the context of the discussion of the gold standard. Conditions for internal and external balance are presented through diagrammatic analysis based upon the short-run macroeconomic model of Chapter 16. This analysis illustrates the strengths and weaknesses of alternative fixed exchange rate arrangements. The chapter also draws upon earlier discussion of balance of payments crises to make clear the interplay between "fundamental disequilibrium" and speculative attacks. There is a detailed analysis of the Bretton Woodssystem that includes a case study of the experience during its decline beginning in the mid-1960s and culminating with its collapse in 1973.Chapter 19 focuses on recent experience under floating exchange rates. The discussion is couched in terms of current debate concerning the advantages of floating versus fixed exchange rate systems. The theoretical arguments for and against floating exchange rates frame two case studies, the first on the experience between the two oil shocks in the 1970s and the second on the experience since 1980. The transmission of monetary and fiscal shocks from one country to another is also considered. Discussion of the experience in the 1980s points out the shift in policy toward greater coordination in the second half of the decade. Discussion of the 1990s focuses on the strong U.S. economy from 1992 on and the extended economic difficulties in Japan. Finally, the chapter considers what has been learned about floating rates since 1973. The appendix illustrates losses arising from uncoordinated international monetary policy using a game theory setup.Europe’s switch to a single currency, the euro, is the subject of Chapter 20, and provides a particular example of a single currency system. The chapter discusses the history of the European Monetary System and its precursors. The early years of the E.M.S. were marked by capital controls and frequent realignments. By the end of the 1980s, however, there was marked inflation convergence among E.M.S. members, few realignments and the removal of capital controls. Despite a speculative crisis in 1992-3, leaders pressed on with plans for the establishment of a single European currency as outlined in the Maastricht Treaty which created Economic and Monetary Union (EMU). The single currency was viewed as an important part of the EC 1992 initiative which called for the free flow within Europe of labor, capital, goods and services. The single currency, the euro, was launched on January 1, 1999 with eleven original participants. These countries have ceded monetary authority to a supranational central bank and constrained their fiscal policy with agreements on convergence criteria and the stability and growth pact. A single currency imposes costs as well as confers benefits. The theory of optimum currency areas suggests conditions which affect the relative benefits of a single currency. The chapter provides a way to frame this analysis using the GG-LL diagram which compares the gains and losses from a single currency. Finally, the chapter examines the prospects of the EU as an optimal currency area compared to the United States and considers the future challenges EMU will face.The international capital market is the subject of Chapter 21. This chapter draws an analogy between the gains from trade arising from international portfolio diversification andinternational goods trade. There is discussion of institutional structures that have arisen to exploit these gains. The chapter discusses the Eurocurrency market, the regulation of offshore banking, and the role of international financial supervisory cooperation. The chapter examines policy issues of financial markets, the policy trilemma of the incompatibility of fixed rates, independent monetary policy, and capital mobility as well as the tension between supporting financial stability and creating a moral hazard when a government intervenes in financial markets. The chapter also considers evidence of how well the international capital market has performed by focusing on issues such as the efficiency of the foreign exchange market and the existence of excess volatility of exchange rates.Chapter 22 discusses issues facing developing countries. The chapter begins by identifying characteristics of the economies of developing countries, characteristics that include undeveloped financial markets, pervasive government involvement, and a dependence on commodity exports. The macroeconomic analysis of previous chapters again provides a framework for analyzing relevant issues, such as inflation in or capital flows to developing countries. Borrowing by developing countries is discussed as an attempt to exploit gains from intertemporal trade and is put in historical perspective. Latin American countries’ problems with inflation and subsequent attempts at reform are detailed. Finally, the East Asian economic miracle is revisited (it is discussed in Chapter 10), and the East Asian financial crisis is examined. This final topic provides an opportunity to discuss possible reforms of the world’s financial architecture.。

克鲁格曼国际贸易 答案imch07

CHAPTER 7INTERNATIONAL FACTOR MOVEMENTSChapter OrganizationInternational Labor MobilityA One-Good Model without Factor MobilityInternational Labor MovementExtending the AnalysisCase Study: Wage Convergence in the Age of Mass MigrationCase Study: Immigration and the U.S. EconomyInternational Borrowing and LendingIntertemporal Production Possibilities and TradeThe Real Interest RateIntertemporal Comparative AdvantageBox: Does Capital Movement to Developing Countries Hurt Workers in High-Wage Countries?Direct Foreign Investment and Multinational FirmsThe Theory of Multinational EnterpriseMultinational Firms in PracticeCase Study: Foreign Direct Investment in the United StatesBox: Taken for a Ride?SummaryAppendix: More on Intertemporal TradeCHAPTER OVERVIEWThis chapter introduces an additional aspect of economic integration, international factor movements. Most notably, this refers to labor and financial capital mobility across countries. An important point emphasized in Chapter 7 is that many of the same forces which trigger international trade in goods between countries will, if permitted, trigger international flows of labor and finances. Students may find this analysis especially interesting in that it sheds light on issues which may involve them personally, such as motives for the 19th and early 20th century waves of emigration to land-abundant but labor-scarce America from land-scarce andlabor-abundant Europe and China. Other, more current examples of international factor mobility include the international capital flows associated with the debt crisis of the 1980s, and intertemporal substitution motives behind United States borrowing and foreign direct investment inflows and outflows in the 1980s and 1990s.The chapter proceeds in three main sections. First, a simple model of international labor mobility is presented. Next, intertemporal production and consumption decisions are analyzed in the context of international borrowing and lending. Finally, the role of multinational corporations is discussed.To demonstrate the forces behind international labor mobility, the chapter begins with a model which is quite similar to that presented in Chapter 3. In each country of the world, the real return to labor equals its marginal product in perfectly competitive markets in each of two countries which produce one good using two factors of production. Labor relocates until the marginal products are equal across countries. While the redistribution of labor increases world output and provides overall gains, it also has important income distribution effects. Workers in the originally high wage country are made worse off since wages fall with the inflow of additional workers, and workers in the originally low wage country are made better off. One case study in the text helps illustrate the effects on both source and destination countries and another focuses on the American experience with immigration. It would be interesting for an instructor to discuss the resistance of groups within the United States to migrant farm workers from Mexico and immigration from other low wage countries such as Haiti.An analysis of international capital movements involves the consideration of intertemporal trade. The important point here is that the real rate of interest differs across countries and international factor movements provide gains to both borrowers and lenders. The analysis presented here is analogous to that in Chapter 5; instead of choosing between consumption of goods at any point in time, the analysis focuses on a one good world where the choice at a point in time is between future and present consumption. An intertemporal production possibilities frontier replaces the PPF and the intertemporal price line replaces the relative price line. Analysis of the gains from intertemporal trade, the size of borrowing and lending, and the effects of taxes on capital transfers follow. The appendix presents this model in greater detail.The final issue addressed in this chapter concerns direct foreign investment and multinational firms. Direct foreign investment differs from other capital transfers in that it involves the acquisition of control of a company. The theory of multinational firms is not well developed. Important points of existing theory are that decisions concerning multinationals are based upon concerns involving location and internalization. Location decisions are based upon barriers to trade and transportation costs. Internalization decisions focus on vertical integration and technology transfers. Multinationals facilitate shifts such that factor prices move in the direction which free trade would cause. The income distribution effects of direct foreign investment are politically charged and in other chapters are discussed in further detail.The political dimension of international factor movements differs from that of international trade. Class discussion on these distinctions could focus on who wins and who loses from each and, more specifically, issues such as the role of multinationals or the responsibility of host countries to guest workers. For example, one interesting topic for discussion is the effects of labor mobility as a component of integration within the European Union. (This topic is developed further in Chapter 20.)ANSWERS TO TEXTBOOK PROBLEMS1. The marginal product of labor in Home is 10 and in Foreign is 18. Wages are higherin Foreign, so workers migrate there to the point where the marginal product in both Home and Foreign is equated. This occurs when there are 7 workers in each country, and the marginal product of labor in each country is 14.2. There is no incentive to migrate when there is factor price equalization. This occurswhen both countries produce both goods and when there are no barriers to trade (the problem assumes technology is the same in the two countries). A tariff by country A increases the relative price of the protected good in that country and lowers its relative price in the country B. If the protected good uses labor relatively intensively, the demand for labor in country A rises, as does the return to labor, and the return to labor in the country B falls. These results follow from the Stolper-Samuelson theory, which states that an increase in the price of a good raises the return to the factor used intensively in the production of that good by more than the price increase. These international wage differentials induce migration from country B to country A.3. The analysis of intertemporal trade follows directly the analysis of trade of two goods.Substitute "future consumption" and "present consumption" for "cloth" and "food."The relevant relative price is the cost of future consumption compared to present consumption, which is the inverse of the real interest rate. Countries in which present consumption is relatively cheap (which have low real interest rates) will "export"present consumption (i.e. lend) to countries in which present consumption is relatively dear (which have high real interest rates). The equilibrium real interest rate after borrowing and lending occur lies between that found in each country before borrowing and lending take place. Gains from borrowing and lending are analogous to gains from trade--there is greater efficiency in the production of goods intertemporally.4. Foregoing current consumption allows one to obtain future consumption. There willbe a bias towards future consumption if the amount of future consumption which can be obtained by foregoing current consumption is high. In terms of the analysis presented in this chapter, there is a bias towards future consumption if the real interest rate in the economy is higher in the absence of international borrowing or lending than the world real interest rate.a. The large inflows of immigrants means that the marginal product of capital will rise asmore workers enter the country. The real interest rate will be high, and there will be a bias towards future consumption.b. The marginal product of capital is low and thus there is a bias towards currentconsumption.c. The direction of the bias depends upon the comparison of the increase in the price ofoil and the world real interest rate. Leaving the oil in the ground provides a return of the increase in the price of oil whereas the world real interest rate may be higher or lower than this increase.d. Foregoing current consumption allows exploitation of resources, and higher futureconsumption. Thus, there is a bias towards future consumption.e. The return to capital is higher than in the rest of the world (since the country's rate ofgrowth exceeds that of the rest of the world), and there is a bias toward future consumption.5. a. $10 million is not a controlling interest in IBM, so this does not qualify as directforeign investment. It is international portfolio diversification.b. This is direct foreign investment if one considers the apartment building a businesswhich pays returns in terms of rents.c. Unless particular U.S. shareholders will not have control over the new Frenchcompany, this will not be direct foreign investment.d. This is not direct foreign investment since the Italian company is an "employee," butnot the ones which ultimately control, the company.6. In terms of location, the Karma company has avoided Brazilian import restrictions. Interms of internalization, the firm has retained its control over the technology by not divulging its patents.FURTHER READINGSRichard A. Brecher and Robert C. Feenstra. "International Trade and Capital Mobility between Diversified Economies." Journal of International Economics14 (May, 1983), pp. 321-339.Richard E. Caves. Multinational Enterprises and Economic Analysis.Cambridge: Harvard University Press, 1982.Wilfred J. Ethier. "The Multinational Firm," Quarterly Journal of Economics 101 (November 1986), pp.805-833.Irving Fisher. The Theory of Interest. New York: Macmillan, 1930.Edward M. Graham and Paul R. Krugman. Foreign Direct Investment in the United States. Washington, D.C.: Institute for International Economics,1989.Charles P. Kindleberger. American Business Abroad.New Haven: Yale University Press, 1969.Charles P. Kindleberger. Europe's Postwar Growth: The Role of Labor Supply. Cambridge: Harvard University Press, 1967.G.D.A. MacDougall. "The Benefits and Costs of Private Investment from Abroad: A Theoretical Approach." Economic Record, 36 (1960), pp. 13-35.Robert A. Mundell. "International Trade and Factor Mobility." American Economic Review, 47 (1957), pp. 321-335.Jeffrey Sachs. "The Current Account and Macroeconomic Adjustment in the 1970's." Brookings Papers on Economic Activity, 1981.。

《国际经济学》克鲁格曼(第六版)习题答案imsect3

OVERVIEW OF SECTION III: EXCHANGE RATES AND OPEN ECONOMY MACROECONOMICSSection III of the textbook is comprised of six chapters:Chapter 12 National Income Accounting and the Balance of PaymentsChapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Chapter 14 Money, Interest Rates, and Exchange RatesChapter 15 Price Levels and the Exchange Rate in the Long RunChapter 16 Output and the Exchange Rate in the Short RunChapter 17 Fixed Exchange Rates and Foreign Exchange InterventionSECTION III OVERVIEWThe presentation of international finance theory proceeds by building up an integrated model of exchange rate and output determination. Successive chapters in Part III construct this model step by step so students acquire a firm understanding of each component as well as the manner in which these components fit together. The resulting model presents a single unifying framework admitting the entire range of exchange rate regimes from pure float to managed float to fixed rates. The model may be used to analyze both comparative static and dynamic time path results arising from temporary or permanent policy or exogenous shocks in an open economy.The primacy given to asset markets in the model is reflected in the discussion of national income and balance of payments accounting in the first chapter of this section. Chapter 12 begins with a discussion of the focus of international finance. The discussion then proceeds to national income accounting in an open economy. The chapter points out, in the discussion on the balance of payments account, that current account transactions must be financed by financial account flows from either central bank or noncentral bank transactions. A case study uses national income accounting identities to consider the link between government budget deficits and the current account.Observed behavior of the exchange rate favors modeling it as an asset price rather than as a goods price. Thus, the core relationship for short-run exchange-rate determination in the model developed in Part III is uncovered interest parity. Chapter 13 presents a model inwhich the exchange rate adjusts to equate expected returns on interest-bearing assets denominated in different currencies given expectations about exchange rates, and the domestic and foreign interest rate. This first building block of the model lays the foundation for subsequent chapters that explore the determination of domestic interest rates and output, the basis for expectations of future exchange rates and richer specifications of the foreign-exchange market that include risk. An appendix to this chapter explains the determination of forward exchange rates.Chapter 14 introduces the domestic money market, linking monetary factors to short-run exchange-rate determination through the domestic interest rate. The chapter begins with a discussion of the determination of the domestic interest rate. Interest parity links the domestic interest rate to the exchange rate, a relationship captured in a two-quadrant diagram. Comparative statics employing this diagram demonstrate the effects of monetary expansion and contraction on the exchange rate in the short run. Dynamic considerations are introduced through an appeal to the long run neutrality of money that identifies a long-run steady-state value toward which the exchange rate evolves. The dynamic time path of the model exhibits overshooting of the exchange-rate in response to monetary changes.Chapter 15 develops a model of the long run exchange rate. The long-run exchange rate plays a role in a complete short-run macroeconomic model since one variable in that model is the expected future exchange rate. The chapter begins with a discussion of the law of one price and purchasing power parity. A model of the exchange rate in the long-run based upon purchasing power parity is developed. A review of the empirical evidence, however, casts doubt on this model. The chapter then goes on to develop a general model of exchange rates in the long run in which the neutrality of monetary shocks emerges as a special case. In contrast, shocks to the output market or changes in fiscal policy alter the long run real exchange rate. This chapter also discusses the real interest parity relationship that links the real interest rate differential to the expected change in the real exchange rate. An appendix examines the relationship of the interest rate and exchange rate under a flexible-price monetary approach.Chapter 16 presents a macroeconomic model of output and exchange-rate determination in the short run. The chapter introduces aggregate demand in a setting of short-run price stickiness to construct a model of the goods market. The exchange-rate analysis presented in previous chapters provides a model of the asset market. The resulting model is, in spirit, very close to the classic Mundell-Fleming model. This model is used to examine the effects of avariety of policies. The analysis allows a distinction to be drawn between permanent and temporary policy shifts through the pedagogic device that permanent policy shifts alter long-run expectations while temporary policy shifts do not. This distinction highlights the importance of exchange-rate expectations on macroeconomic outcomes. A case study of U.S. fiscal and monetary policy between 1979 and 1983 utilizes the model to explain notable historical events. The chapter concludes with a discussion of the links between exchange rate and import price movements which focuses on the J-curve and exchange-rate pass-through. An appendix to the chapter compares the IS-LM model to the model developed in this chapter. A second appendix considers intertemporal trade and consumption demand. A third appendix discusses the Marshall-Lerner condition and estimates of trade elasticities.The final chapter of this section discusses intervention by the central bank and the relationship of this policy to the money supply. This analysis is blended with the previous chapter's short-run macroeconomic model to analyze policy under fixed rates. The balance sheet of the central bank is used to keep track of the effects of foreign exchange intervention on the money supply. The model developed in previous chapters is extended by relaxing the interest parity condition and allowing exchange-rate risk to influence agents' decisions. This allows a discussion of sterilized intervention. Another topic discussed in this chapter is capital flight and balance of payments crises with an introduction to different models of how a balance of payments or currency crisis can occur. The analysis also is extended to a two-country framework to discuss alternative systems for fixing the exchange-rate as a prelude to Part IV. An appendix to Chapter 17 develops a model of the foreign-exchange market in which risk factors make domestic-currency and foreign-currency assets imperfect substitutes.A second appendix explores the monetary approach to the balance of payments. The third appendix discusses the timing of a balance of payments crisis.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

HAPTER 7INTERNATIONAL FACTOR MOVEMENTSChapter OrganizationInternational Labor MobilityA One-Good Model without Factor MobilityInternational Labor MovementExtending the AnalysisCase Study: Wage Convergence in the Age of Mass MigrationCase Study: Immigration and the U.S. EconomyInternational Borrowing and LendingIntertemporal Production Possibilities and TradeThe Real Interest RateIntertemporal Comparative AdvantageBox: Does Capital Movement to Developing Countries Hurt Workers in High-Wage Countries?Direct Foreign Investment and Multinational FirmsThe Theory of Multinational EnterpriseMultinational Firms in PracticeCase Study: Foreign Direct Investment in the United StatesBox: Taken for a Ride?SummaryAppendix: More on Intertemporal TradeCHAPTER OVERVIEWThis chapter introduces an additional aspect of economic integration, international factor movements. Most notably, this refers to labor and financial capital mobility across countries. An important point emphasized in Chapter 7 is that many of the same forces which trigger international trade in goods between countries will, if permitted, trigger international flows of labor and finances. Students may find this analysis especially interesting in that it sheds light on issues which may involve them personally, such as motives for the 19th and early 20th century waves of emigration to land-abundant but labor-scarce America from land-scarce andlabor-abundant Europe and China. Other, more current examples of international factor mobility include the international capital flows associated with the debt crisis of the 1980s, and intertemporal substitution motives behind United States borrowing and foreign direct investment inflows and outflows in the 1980s and 1990s.The chapter proceeds in three main sections. First, a simple model of international labor mobility is presented. Next, intertemporal production and consumption decisions are analyzed in the context of international borrowing and lending. Finally, the role of multinational corporations is discussed.To demonstrate the forces behind international labor mobility, the chapter begins with a model which is quite similar to that presented in Chapter 3. In each country of the world, the real return to labor equals its marginal product in perfectly competitive markets in each of two countries which produce one good using two factors of production. Labor relocates until the marginal products are equal across countries. While the redistribution of labor increases world output and provides overall gains, it also has important income distribution effects. Workers in the originally high wage country are made worse off since wages fall with the inflow of additional workers, and workers in the originally low wage country are made better off. One case study in the text helps illustrate the effects on both source and destination countries and another focuses on the American experience with immigration. It would be interesting for an instructor to discuss the resistance of groups within the United States to migrant farm workers from Mexico and immigration from other low wage countries such as Haiti.An analysis of international capital movements involves the consideration of intertemporal trade. The important point here is that the real rate of interest differs across countries and international factor movements provide gains to both borrowers and lenders. The analysis presented here is analogous to that in Chapter 5; instead of choosing between consumption of goods at any point in time, the analysis focuses on a one good world where the choice at a point in time is between future and present consumption. An intertemporal production possibilities frontier replaces the PPF and the intertemporal price line replaces the relative price line. Analysis of the gains from intertemporal trade, the size of borrowing and lending, and the effects of taxes on capital transfers follow. The appendix presents this model in greater detail.The final issue addressed in this chapter concerns direct foreign investment and multinational firms. Direct foreign investment differs from other capital transfers in that it involves the acquisition of control of a company. The theory of multinational firms is not well developed. Important points of existing theory are that decisions concerning multinationals are based upon concerns involving location and internalization. Location decisions are based upon barriers to trade and transportation costs. Internalization decisions focus on vertical integration and technology transfers. Multinationals facilitate shifts such that factor prices move in the direction which free trade would cause. The income distribution effects of direct foreign investment are politically charged and in other chapters are discussed in further detail.The political dimension of international factor movements differs from that of international trade. Class discussion on these distinctions could focus on who wins and who loses from each and, more specifically, issues such as the role of multinationals or the responsibility of host countries to guest workers. For example, one interesting topic for discussion is the effects of labor mobility as a component of integration within the European Union. (This topic is developed further in Chapter 20.)ANSWERS TO TEXTBOOK PROBLEMS1. The marginal product of labor in Home is 10 and in Foreign is 18. Wages are higherin Foreign, so workers migrate there to the point where the marginal product in both Home and Foreign is equated. This occurs when there are 7 workers in each country, and the marginal product of labor in each country is 14.2. There is no incentive to migrate when there is factor price equalization. This occurswhen both countries produce both goods and when there are no barriers to trade (the problem assumes technology is the same in the two countries). A tariff by country A increases the relative price of the protected good in that country and lowers its relative price in the country B. If the protected good uses labor relatively intensively, the demand for labor in country A rises, as does the return to labor, and the return to labor in the country B falls. These results follow from the Stolper-Samuelson theory, which states that an increase in the price of a good raises the return to the factor used intensively in the production of that good by more than the price increase. These international wage differentials induce migration from country B to country A.3. The analysis of intertemporal trade follows directly the analysis of trade of two goods.Substitute "future consumption" and "present consumption" for "cloth" and "food."The relevant relative price is the cost of future consumption compared to present consumption, which is the inverse of the real interest rate. Countries in which present consumption is relatively cheap (which have low real interest rates) will "export"present consumption (i.e. lend) to countries in which present consumption is relatively dear (which have high real interest rates). The equilibrium real interest rate after borrowing and lending occur lies between that found in each country before borrowing and lending take place. Gains from borrowing and lending are analogous to gains from trade--there is greater efficiency in the production of goods intertemporally.4. Foregoing current consumption allows one to obtain future consumption. There willbe a bias towards future consumption if the amount of future consumption which can be obtained by foregoing current consumption is high. In terms of the analysis presented in this chapter, there is a bias towards future consumption if the real interest rate in the economy is higher in the absence of international borrowing or lending than the world real interest rate.a. The large inflows of immigrants means that the marginal product of capital will rise asmore workers enter the country. The real interest rate will be high, and there will be a bias towards future consumption.b. The marginal product of capital is low and thus there is a bias towards currentconsumption.c. The direction of the bias depends upon the comparison of the increase in the price ofoil and the world real interest rate. Leaving the oil in the ground provides a return of the increase in the price of oil whereas the world real interest rate may be higher or lower than this increase.d. Foregoing current consumption allows exploitation of resources, and higher futureconsumption. Thus, there is a bias towards future consumption.e. The return to capital is higher than in the rest of the world (since the country's rate ofgrowth exceeds that of the rest of the world), and there is a bias toward future consumption.5. a. $10 million is not a controlling interest in IBM, so this does not qualify as directforeign investment. It is international portfolio diversification.b. This is direct foreign investment if one considers the apartment building a businesswhich pays returns in terms of rents.c. Unless particular U.S. shareholders will not have control over the new Frenchcompany, this will not be direct foreign investment.d. This is not direct foreign investment since the Italian company is an "employee," butnot the ones which ultimately control, the company.6. In terms of location, the Karma company has avoided Brazilian import restrictions. Interms of internalization, the firm has retained its control over the technology by not divulging its patents.FURTHER READINGSRichard A. Brecher and Robert C. Feenstra. "International Trade and Capital Mobility between Diversified Economies." Journal of International Economics14 (May, 1983), pp. 321-339.Richard E. Caves. Multinational Enterprises and Economic Analysis.Cambridge: Harvard University Press, 1982.Wilfred J. Ethier. "The Multinational Firm," Quarterly Journal of Economics 101 (November 1986), pp.805-833.Irving Fisher. The Theory of Interest. New York: Macmillan, 1930.Edward M. Graham and Paul R. Krugman. Foreign Direct Investment in the United States. Washington, D.C.: Institute for International Economics,1989.Charles P. Kindleberger. American Business Abroad.New Haven: Yale University Press, 1969.Charles P. Kindleberger. Europe's Postwar Growth: The Role of Labor Supply. Cambridge: Harvard University Press, 1967.G.D.A. MacDougall. "The Benefits and Costs of Private Investment from Abroad: A Theoretical Approach." Economic Record, 36 (1960), pp. 13-35.Robert A. Mundell. "International Trade and Factor Mobility." American Economic Review, 47 (1957), pp. 321-335.Jeffrey Sachs. "The Current Account and Macroeconomic Adjustment in the 1970's." Brookings Papers on Economic Activity, 1981.。