30外国税制 程黎 范信葵 (3)

国际税收学的基本概念

税收管辖权与税种的关系

商品税的税收管辖权

地域税收管辖权

所得税的税收管辖权

综合所得税制下:居民(公民)管辖权和(或)地 域管辖权

分类所得税制下:单一的地域管辖权

财产税的税收管辖权

一般财产税 :居民(公民)管辖权和/或地域管辖 权

特别财产税 :单一的地域管辖权

公民/居民税收管辖权的确立

国家税收管辖权

税收管辖权的原则和类型 公民/居民税收管辖权的确立 地域税收管辖权的确立

税收管辖权的原则和类型

税收管辖权的原则 税收管辖权的类型 税收管辖权的具体实施情况 税收管辖权与税种的关系

税收管辖权的原则

属人原则

以人(包括自然人和法人)的国籍和住所为 标准,确定国家行使管辖权范围的原则

国际税收协调

所得税和财产税方面:国际税收协定范本 OECD范本和联合国范本

商品税方面:关贸总协定

国际税收分配--国际税收协调的结果

跨国商品、所得和财产课税中 的重复征税

跨国所得课税中的重复征税 对同一纳税人的同一课税对象(例)

跨国财产课税中的重复征税 对同一纳税人的同一课税对象(例)

跨国商品课税中的重复征税 对不同纳税人的同一课税对象(例)

所得税重复课税

财产税重复课税

商品税重复课税

国际税收协调如何导致国际税收分配

跨国所得课税 例

跨国财产课税 例

跨国商品课税 国内商品税 关税

国际税收的概念

关于国际税收概念的主要观点

国际税收体现的是一种怎样的关系? 涉外税收和国际税收的关系如何?

国际税收的本质是国家之间的税收分配关系 国际税收与涉外税收的关系 国际税收的概念:两个或两个以上国家的政府

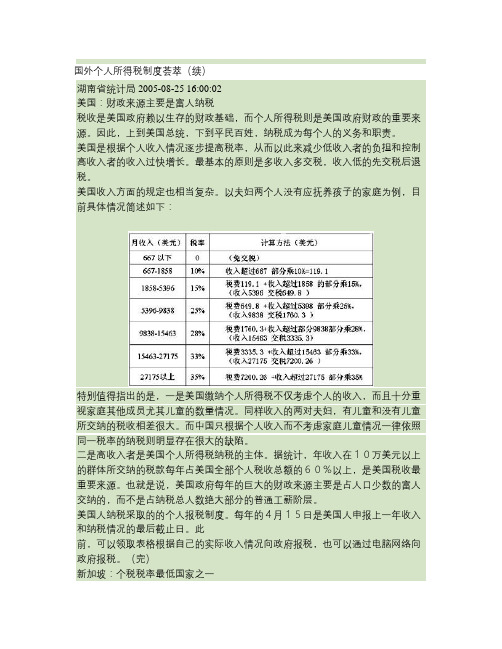

国外个人所得税制度荟萃(续)(精)

国外个人所得税制度荟萃(续)湖南省统计局 2005-08-25 16:00:02美国:财政来源主要是富人纳税税收是美国政府赖以生存的财政基础,而个人所得税则是美国政府财政的重要来源。

因此,上到美国总统,下到平民百姓,纳税成为每个人的义务和职责。

美国是根据个人收入情况逐步提高税率,从而以此来减少低收入者的负担和控制高收入者的收入过快增长。

最基本的原则是多收入多交税,收入低的先交税后退税。

美国收入方面的规定也相当复杂。

以夫妇两个人没有应抚养孩子的家庭为例,目前具体情况简述如下:特别值得指出的是,一是美国缴纳个人所得税不仅考虑个人的收入,而且十分重视家庭其他成员尤其儿童的数量情况。

同样收入的两对夫妇,有儿童和没有儿童所交纳的税收相差很大。

而中国只根据个人收入而不考虑家庭儿童情况一律依照同一税率的纳税则明显存在很大的缺陷。

二是高收入者是美国个人所得税纳税的主体。

据统计,年收入在10万美元以上的群体所交纳的税款每年占美国全部个人税收总额的60%以上,是美国税收最重要来源。

也就是说,美国政府每年的巨大的财政来源主要是占人口少数的富人交纳的,而不是占纳税总人数绝大部分的普通工薪阶层。

美国人纳税采取的的个人报税制度。

每年的4月15日是美国人申报上一年收入和纳税情况的最后截止日。

此前,可以领取表格根据自己的实际收入情况向政府报税,也可以通过电脑网络向政府报税。

(完)新加坡:个税税率最低国家之一新加坡拥有较为完善的个人所得税征收体系,其中新加坡国内税务局是该国最大的税收机构,负责评估、收取和实施在税收法令下的各种课税。

新加坡是个人所得税税率最低的国家之一,其实行的是13级超额累进税率,也就是以前一年的收入扣除适当项目后,以累计式征税。

每年的4月15日之前,所有应纳税者必须将前一年的各项收入如实填入税务申报登记表中,并及时上报国内税务局。

新加坡的税制是按收入来源地征税的。

新加坡目前的税率为0%至22%。

须纳税的项目包括:在新加坡赚取的收入;以及在新加坡收到的海外收入;属非居民的个人在新加坡所收到的海外收入不需要在新加坡缴税。

《外国税制》程黎 范信葵 chapter VII

2. Main taxes

-

National Taxes

Taxes on income

Individual income taxCorporation tax

Taxes on gifts and inheritances

Taxes on properties

Gift tax Inheritance tax -

❖ 2.1.6. Filing of returns and payment of taxes

❖ Corporate income tax returns are required to be filed within two months after the end of each accounting period and taxes paid thereon, unless an extension is applied for and approved by the tax office. A onemonth extension. if applied, is automatically approved. A final return must be accompanied by financial statements and supportings Municipal inhabitants’ tax

国外财税制度双语课程教学大纲

《国外财税制度》(双语)课程教学大纲一、课程总述本课程大纲是以2015年财政本科专业人才培养方案为依据编制的。

二、教学时数分配三、单元教学目的、教学重难点和内容设置Chapter 1 Government At A Glance【Objectives】By learning this chapter, students are going to know more of American government expenditure and revenue. What’s more, they’er supposed to explore and find the datas about the government public finance via internet resources if necessary.【Key points】Federal Government, State and Local Governments, the Size of Government, Budget, Government Expenditures, Government Revenues【Contents】1. Legal Framework2.Unified Budgeternment Expenditureernment RevenueChapter 3 Welfare Economics【Objectives】By learning this chapter, students are supposed to grasp the basic framework of normative analysis, including the two fundamental theorems of welfare economics and the cases when there are market failures.【Key points】Welfare economics, Pareto efficient, Pareto improvement, the first fundamental theorem of welfare economics, fairness, the first fundamental theorem of welfare economics, market failure, government intervention【Contents】1.Welfare economics2.The first fundamental theorem of welfare economics3.Fairness and the second fundamental theorem of welfare economics4.Market failure5.Buying into welfare economicsChapter 7 Education【Objectives】The chapter provides students with a chance to look into the US educational institutions and its fiscal problems concerning education. By comparing the educational practices between China and the US, students will be able to better understand why governments intervene into the field of education.【Key points】public education, government intervention, public good, externality, commodity egalitarianism, charter schools, school voucher, school accountability 【Contents】1.Justifying government intervention in education2.What can government intervention in education accomplish?3.New directions for public educationChapter 9 The Health Care Market【Objectives】The chapter would introduce the unique aspects of the health care market and justify government intervention in the health care provision.【Key points】Health care market, private insurance, social insurance, insurance premium, expected value, actuarially fair insurance premium, expected utility, risk smoothing, risk premium, loading fee, risk pooling, adverse selection, asymmetric information, death spiral, moral hazard, paternalism【Contents】1.The role of insurance2.The role of risk pooling3.Adverse selection in the health insurance market4.Insurance and moral hazard5.Other information problems in the health care market6.Do we want efficient provision of health care?Chapter 10 Government and the Health Care Market 【Objectives】The chapter would discuss the practices of US health care, including private health insurance and the main forms of government provision of health insurance, i.e. Medicare and Medicaid. By analyzing the challenges facing the health care system, proposals as to reform the system are brought about.【Key points】Private health insurance, Employer-provided health insurance, job lock, cost-based reimbursement, fee-for-service, managed care, capitation-based reimbursement, Medicare, hospital insurance, supplementary medical insurance, prospective payment systems, retrospective payment system, Medicaid, health care reform【Contents】1.Private health insuranceernment provision of health insurance: Medicare and Medicaid3.Health care reformChapter 17 The Personal Income Tax【Objectives】This chapter introduces the US personal income tax system. By learning it, students are supposed to learn how to calculate the personal income tax according to the five steps. Detailed explanation will be given as to prove the complexity of tax system.【Key points】adjusted gross income, taxable income, exemption, deductions, rate schedule, capital gain(loss), realized capital gain, unrealized capital gain, imputed rent, lock-in effect, individual retirement account, Roth IRA, 401(k) plan, Keogh Plan, education savings account, itemized deduction, standard deduction, tax credit, tax expenditure, tax reform act of 1986 【Contents】1.Basic structure2.Defining income3.Excludable reforms of money income4.Exemptions and deductions5.Rate structure6.Taxes and inflation7.The alternative minimum tax8.Choice of unit and the marriage tax9.State income taxes10.Politics and tax reform。

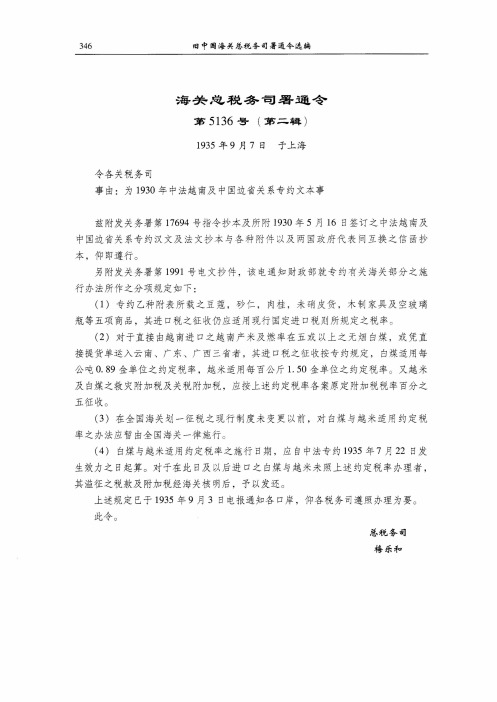

为1930年中法越南及中国边省关系专约文本事

346旧中国海关总税务司署通令选编

海关总税务司署通令

第5136号(第二辑)

1935年9月7日于上海

令各关税务司

事由:为1930年中法越南及中国边省关系专约文本事

兹附发关务署第17694号指令抄本及所附1930年5月16日签订之中法越南及中国边省关系专约汉文及法文抄本与各种附件以及两国政府代表间互换之信函抄本,仰即遵行。

另附发关务署第1991号电文抄件,该电通知财政部就专约有关海关部分之施行办法所作之分项规定如下:

(1)专约乙种附表所载之豆蔻,砂仁,肉桂,未硝皮货,木制家具及空破璃瓶等五项商品,其进口税之征收仍应适用现行国定进口税则所规定之税率。

(2)对于直接由越南进口之越南产米及燃率在五或以上之无烟白煤,或凭直接提货单运入云南、广东、广西三省者,其进口税之征收按专约规定,白煤适用每公吨0. 89金单位之约定税率,越米适用每百公斤1. 50金单位之约定税率。

又越米及白煤之救灾附加税及关税附加税,应按上述约定税率各案原定附加税税率百分之五征收。

(3)在全国海关划一征税之现行制度未变更以前,对白煤与越米适用约定税率之办法应暂由全国海关一律施行。

(4)白煤与越米适用约定税率之施行日期,应自中法专约1935年7月22日发 生效力之日起算。

对于在此日及以后进口之白煤与越米未照上述约定税率办理者,其溢征之税款及附加税经海关核明后,予以发还。

上述规定已于1935年9月3日电报通知各口岸,仰各税务司遵照办理为要。

此令。

总税务司

梅乐和。

第一章 国际税收导论

三、国际税收与国家税收的关系

联系 区别

四、国际税收的研究范围

广义研究范围 所得税、财产税、商品税的国际税收协调 狭义研究范围 所得税和财产税的国际税收协调

第二节 国际税收问题的 产生

一、国际税收问题的产生

1.商品课税国际税收问题(关税,消费税,销售 税)

就商品课税的国际协调而言,国际协调的目的是为了促 进国际贸易的发展,而关税是国际贸易发展的主要障碍, 因此,关税是当初商品课税协调的主要对象。 商品课税的国际协调历史正是从关税开始的,而且在很长 的历史时期内,关税一直是商品课税国际协调活动的唯一 领域,直到二战后,国内商品税的国际协调活动才开始出 现。

4、《全球经济中的转让定价策略》 税总科研所译 中国财政经济出版 社1997年 5、《International Taxation》肯森、布卢姆著中信出版社2003年 《国际税收大全》雷维编朱明熙等译 西南财经大学出版社1991年

参考杂志:

《涉外税务》《税收译丛》《国际税讯》《national tax journal》 《international tax and public finance 》《journal of public economics》《international tax review》《intertax》

增值税国际协调已经开始进行并有不断扩大的趋 势。

目前国际社会规定统一由商品的进口国课征增值税,出口 国对商品出口前已经负担的税收,给予退税(出口退税)。 如,南部非洲共同体14国拟定了一份《谅解备忘录》, 决定在2004年以后在成员国之间进行间接税(包括消费 税和增值税)的跨国协调。欧盟也在成员国范围内尝试增 值税和消费税的协调工作。

外国税制第一章

Comparison of Taxation Systems

所得税为主体

稳定可靠的财政收入:直接税,不易转嫁/ 税源稳定 更能实现公平:累进税率,纳税扣除,抵免和再分配 促进宏观经济稳定:Automatic Stabilizer

Michael J.Boskin and Charles E.Mclure, Jr, World Tax Reform: Case Studies of Developed and Developing Countries, International Center for Economic Growth, 1990

复合税制模式下税种的分类

两大税系:Direct tax, Indirect tax 三大税系:Income tax, Consumption tax, Property tax

OECD分类

1000所得、利润和资本利得税 2000社会保障缴款 3000对薪金和劳动力课税 4000财产税 5000商品和劳务税 6000其他税

Roger Gordon and Wei Li,Tax structures in developing countries: Many puzzles and a possible explanation,Journal of Public Economics, 1990

Thomas Piketty & Emmanuel Saez, 2019. "How Progressive is the U.S. Federal Tax System? A Historical and International Perspective," Journal of Economic Perspectives, American Economic Association, vol. 21(1), pages 3-24

国际税收基础之涉外税制

2.1 税收国民待遇原则 2.2 涉外税收负担原则 2.3 国际税收惯例 2.4 我国涉外税收制度

学习目的和要求:

通过本章学习,要求学生掌握税收国民待遇原 则的实质及内容,把握税收负担原则的三项内 容,了解国际税收管理在国际税收中的体现, 熟悉我国涉外税收制度的变革及现存的体系及 内容。

3、税收饶让的应用。

三、防范国际避税的惯例

完善国内税制 国际避税地监控 转让定价的调整 其他措施等

四、应用国际税收协定的惯例

税收协定优先于国内税法。

五、实施外交税收豁免的惯例

《维也纳外交管辖公约》《维也纳领事关系公约》

六、利用仲裁方式的国际惯例

2.4 我国涉外税制制度

一、我国涉外税收制度改革的原则

二、内容

1、全面优惠原则,两套税制 2、特定优惠原则,一套税制

特定项目优惠:利息所得、技术转让和技术服务所得、 外资企业的营业利润所得、国家急需发展的部门和行业 等。

特定地区优惠:经济落后地区、经济特区、出口加工区、 自由贸易区等。

对外国投资者的特定所得实行税收优惠举例

根据韩国1984年颁布的《引进外商投资法》,并非所有的外商投资企业在韩 国都可以享受税收优惠,只有符合特定条件的外商投资企业才能享受税收优惠, 如在高科技项目的外商投资企业以及设在自由出口地区的外商投资企业可以享 受免征所得税或对固定资产提取额外折旧额。

企业的主要财产、会计账簿、公司印章、董事2及以上的有投票权的董事或高层管理人员经常居住于中国境内

我国判定实际管理机构的四条标准,要求在判定企业的实际管理机构是否位于中 国境内时,必须考察企业的最高决策机构和人员(董事会和有投票权的董事)以 及日常管理机构和人员(总经理部和高层管理人员)是否同事在中国境内。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

❖ There are other taxes which are less important or specific to certain industries such as IPT (insurance premium tax) and PRT (petroleum revenue tax) and duties on such items as tobacco, alcohol and petrol.

Tax system

❖ The main taxes in the UK are: * income tax * corporation tax * capital gains tax * NIC (National Insurance contributions, a payroll levy) * inheritance tax (on gifts and death transfers) * VAT (Value Added Tax - the main indirect tax) * stamp duty (a duty on certain transfers of assets, primarily

A pie chart showing the projected constituents of UK taxation receipts for the tax year 2010-2011

Explanation

❖ Income tax forms the bulk of revenues collected by the government. The second largest source of government revenue is National Insurance Contributions. The third largest source of government revenues is value added tax (VAT), and the fourthlargest is corporation tax.

❖ Calendar year - A calendar tax year is 12 consecutive months beginning January 1 and ending December 31.

❖ Fiscal year - A fiscal tax year is 12 consecutive months ending on the last day of any month except December. A 52-53-week tax year is a fiscal tax year that varies from 52 to 53 weeks but does not have to end on the last day of a month.

Overview

❖ Taxation in the United Kingdom may involve payments to a minimum of two different levels of government: The central government (HM Revenue and Customs) and local government.

Chapter V

in the United Kingdom

Words and phrases

❖ 1. Domicile ❖ 2. Residence ❖ 3. HM Revenue and Customs ❖ 4. double tax treaty ❖ 5.fiscal year ❖ 6. tax year ❖ 7. personal allowance

❖ A “tax year” is an annual accounting period for keeping records and reporting income and expenses. An annual accounting period does not include a short tax year. The tax years you can use are:

❖ A fiscal year (or financial year, or sometimes budget year) is a period used for calculating annual ("yearly") financial statements in businesses and other organizations. In many jurisdictions, regulatory laws regarding accounting and taxation require such reports once per twelve months, but do not require that the period reported on constitutes a calendar year (i.e., January through December). Fiscal years vary between businesses and countries. Fiscal year may also refer to the year used for income tax reporting.

❖ Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty.

❖ Local government revenues come primarily from grants from central government funds, business rates in England and Wales, Council Tax and increasingly from fees and charges such as those from on-street parking.