India Auto EY report Oct 2009

期望——2009 Acura RL

低 对 行 人 的伤 害程 度

系统

,

该 系 统 在 车 辆遭 遇 后 部 碰 撞 时 可 以

。

0 9 款 讴 歌 R L不 论 外 形 还 是 性 能 都是 相

起 到 保 护 头 颈 的作 用

全性

.

为了进

一

步增加安

当不 错 的

.

想 必 讴 歌 对 其 也 是 充 满期 望

.

。

每

一

辆 0 9 款 讴 歌 R L都 配 备 乘 员 安 全

重视后排乘客

。

不 过 后 排 手 动 的遮 阳 帘就

。

显 得 不 够档次 了

动 力 方 面 是 0 9 款 讴 歌 R L 值 得 炫 耀 的地 方

。

因 为 它搭载 了

一

款 新 开 发 的3 7 L V 6

.

耀蕊

维普资讯

TE C

!

(智 能 可 变气 门正 时及 气 门升 程 电

( 超级 4 轮 驱 动 力 自 由控 制 系 统 )

。

弹 簧 和 更 大 直 径 的稳 定 杆 从 而 为 车 辆 提 供

经 过 升 级 的S H A W D 能 提 供

—

一

种传统

它是

.

一

了 良 好 的乘 坐 舒 适 性

。

轮驱 动 系统所 没 有 的重 要 功 能

(蕴含

“

,

安全 方 面

.

0 9 款 讴 歌R L采 用讴 歌 独创

52

撞 击 能 量 向 驾驶 室 的传 导

.

从 而 起 到 有效

篷鼐 群

;S e

p 2008

.

维普资讯

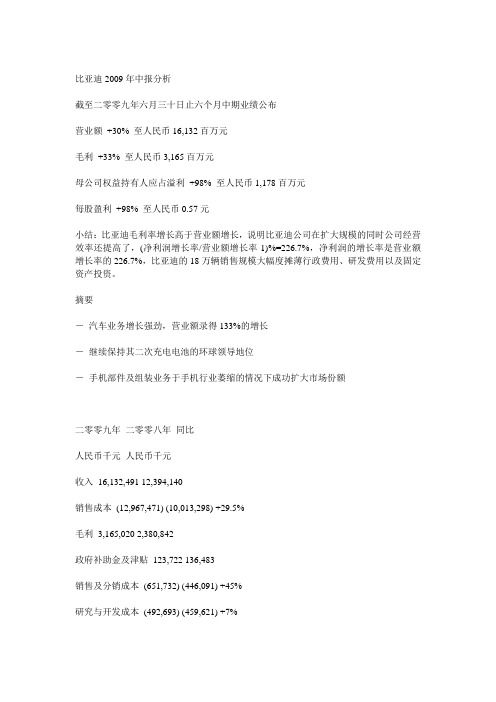

比亚迪2009年中报分析

比亚迪2009年中报分析截至二零零九年六月三十日止六个月中期业绩公布营业额+30% 至人民币16,132百万元毛利+33% 至人民币3,165百万元母公司权益持有人应占溢利+98% 至人民币1,178百万元每股盈利+98% 至人民币0.57元小结:比亚迪毛利率增长高于营业额增长,说明比亚迪公司在扩大规模的同时公司经营效率还提高了,(净利润增长率/营业额增长率-1)%=226.7%,净利润的增长率是营业额增长率的226.7%,比亚迪的18万辆销售规模大幅度摊薄行政费用、研发费用以及固定资产投资。

摘要-汽车业务增长强劲,营业额录得133%的增长-继续保持其二次充电电池的环球领导地位-手机部件及组装业务于手机行业萎缩的情况下成功扩大市场份额二零零九年二零零八年同比人民币千元人民币千元收入16,132,491 12,394,140销售成本(12,967,471) (10,013,298) +29.5%毛利3,165,020 2,380,842政府补助金及津贴123,722 136,483销售及分销成本(651,732) (446,091) +45%研究与开发成本(492,693) (459,621) +7%行政开支(665,130) (722,310) -8%其它开支(16,218) (60,723)融资成本(150,610) (212,512)小结:销售成本同比增长+29.5%,跟营业额增长基本同步,销售及分销成本成本+45%,高于营业额的增长,但是瑕不掩瑜,研究与开发成本是492,693,同比增长+7%,比亚迪重视研发,研发是比亚迪未来高速增长的基础,行政开支同比减少-8%二零零九年二零零八年同比人民币千元人民币千元流动资产存货4,273,266 6,915,535 -39%应收贸易账款及票据7,068,877 5,566,164 +26%预付款项、按金及其它应收款327,356 711,959现金及等同现金项目2,054,808 1,701,397流动资产总值13,728,279 14,899,779流动负债应付贸易账款及票据7,195,306 6,848,714 +5%其它应付款项及预提费用1,714,962 1,530,035预收客户账款1,887,355 1,271,930流动负债总额13,750,129 14,395,207流动资产/(负债)净值(21,850) 504,572小结:销售额增加,存货减少39%,比亚迪就是未来的中国Dell,应收贸易帐款和票据+26%,小于销售额的增长,应付贸易账款及票据+5%,公司还款及时,可以积累信誉。

印度2008-09年度总体经济及货币发展报告摘要

印度2008-09年度總體經濟及貨幣發展報告摘要駐印度經濟組撰980423 一、2008-09年度印度經濟發展概述2008年全球經濟及財金情勢急劇惡化,部份先進國家經濟成長面臨有史以來最大跌幅,許多大型國際金融機構亦陷入危機,所造成的震波自2008年第4季起漸擴及印度在內的新興市場國家,全球經濟全面走入衰退。

印度經濟在服務、出口等主要產業紛受衝擊下,亦失去過去數年的快速成長動能,成長所繫的民間消費及投資活動亦漸減緩,企業利潤紛紛下滑。

幸該年9月起印度政府及時祭出各項財政、貨幣、擴大內需等措施,RBI亦放寬金融業的資金管理,加上印度金融體系相當穩健保守,農村需求尚稱暢旺,以及低通膨及高外匯存底(至2009年4月10日止為2,530億美元),使印度經濟在金融海嘯下不致受到嚴重打擊。

二、經濟成長2008年第3季起工業及服務業成長明顯趨緩,印度中央統計局估計該季經濟成長5.3%,低於上年同期的8.9%;2008-09年度的經濟成長率約介於6.5%-6.6%,低於RBI 原預估的7%;2009-10年度預估經濟成長率約為6%。

三、各產業情形(一)農業:各類農作物產量約2億2,790萬公噸,低於上年同期的2億3,080萬公噸,惟以本年降雨情形而言,尚稱滿意;(二)工業生產:至2月底止成長2.8%,低於上年同期的8.8%;其中製造業成長2.8%,低於上年同期的9.3%,電力成長2.4%,低於上年同期的6.6%;(三)基礎建設:至2月底止成長3%,低於上年同期的5.8%;(四)對外貿易:由於全球貿易量減少,2008-09年度第3季(10-12月)印度對外貿易亦面臨2001年來首度負成長,該季進口亦因國際原油價格下跌及國內需求減少而僅略成長8.8%,至2009年2月底貿易赤字為1,138億美元,較上年同期的822億美元增加38.4%;(五)個人貸款(包括房貸、信用卡、就學貸款、耐久財貸款等):至2009年2月止個人貸款總額為5兆5,539億盧比(約1,110億美元),較上年同期成長8.5%,低於過去的13%;其中房貸額為2兆7,237億盧比,較上年成長7.5%,低於2007-08年的成長13%及2006-07年的成長26%;信用卡亦僅成長8%,低於2007-08年的成長51%及2006-07年的成長46%。

阿尔斯通2009年报

GROUP ACTIVITYOverview• Group general organisation• Main events of fiscal year 2008/09• General comments on activity and results• OutlookSector review• Power Sectors• Transport Sector• Corporate & OthersOperating and financial review• Income statement• Balance sheet• Liquidity and capital resources• Use of non-GAAP financial indicatorsOverviewGROUP GENERAL ORGANISATIONAlstom serves the power generation market through its Power Sectors, and the rail transport market through its Transport Sector. Alstom designs, supplies and services a complete range of technologically advanced products and systems for its customers, and possesses a unique expertise in systems integration and through-life maintenance and service. In fiscal year 2008/09, orders amounted to €24.6 billion and sales to €18.7 billion. On 31 March 2009, the backlog amounted to €45.7 billion.Alstom believes the power and transport markets in which the Group operates are sound, offering:• solid long-term growth prospects based on customers’ needs to expand essential infrastructure systems in developing economies and to replace or modernise them in the developed world; and• attractive opportunities to serve the existing installed base.Alstom believes it can capitalise on its long-standing expertise in these two markets to achieve competitive differentiation. Alstom is strategically well positioned for the following reasons: • Alstom has global reach, with a presence in around 70 countries worldwide;• Alstom is a recognised technology leader in most of its fields of activity, providing best-in-class technology; and• the Group benefits from one of the largest installed bases of equipment in power generation and rolling stock, which enables it to develop its service activities.An international network coordinates the presence of Alstom throughout the world. This network supports the Sectors in their business development and sales.On 31 March 2009, Alstom had a total of approximately 81,500 employees worldwide.MAIN EVENTS OF FISCAL YEAR 2008/09Alstom pursues its growth and improves once again its profitabilityIn fiscal year 2008/09, Alstom achieved very good results, driven by commercial successes on the dynamic power and transport markets and by an overall proper execution of the projects in backlog. The Group set a new record in orders intake at €24.6 billion, a 5% increase on an actual basis (6% on an organic basis) compared to last year. Fuelled by these commercial successes, the backlog reached €45.7 billion at the end of March 2009 (an increase of 16% on an actual and an organic basis), the equivalent of 29 months of sales.Sales also grew to €18.7 billion, representing an annual increase of 11% an actual basis (10% on an organic basis) as a result of the execution of the Group’s large backlog.Continuously improving since 2004/05, operating income increased by 19% at €1,536 million during fiscal year 2008/09 (18% on an organic basis). Translating both the quality of the orders received and the attention paid to project execution, operating margin rose to 8.2% (7.7% in 2007/08).During fiscal year 2008/09, net profit (Group share) after a 25% tax expense, increased 30% at €1,109 million due to an improved operational performance and a turned positive financial income. Earnings per share (basic) reached €3.9 versus €3.0 last year.During the past fiscal year, Alstom generated €1,479 million of free cash flow, a notable performance – including the high capital expenditure programmes launched in 2007/08 – which results from a good operational performance and a favourable evolution of the Group’s working capital.Strong assets to face the challenging environmentLong-term market drivers remain promisingFrom liquidity shortages, the financial crisis rapidly turned into a global economic downturn bringing companies new challenges. A base of financially sound customers, a wide portfolio of activities and a broad geographic coverage are in this context, among the Group’s strongest assets.Regarding Power, Alstom’s long-term market drivers remain positive. In the emerging markets, the need for power generation infrastructure together with the search for energy independence should continue to fuel an already large demand whereas in the industrialised countries, the ageing fleet should support the service and retrofit markets. In addition, more and more stringent environmental regulations should sustain the development of clean energy solutions such as hydro, wind and nuclear, foster the demand for higher technological contents to ensure a better efficiency of the thermal power plants and drive the need for replacement. In the short term, the financing constraints as well as a downward revision of end markets may drive a decrease of the demand for new power market as some new projects may be postponed. The service market should however be less volatile.Regarding Transport, fast-growing urbanisation and the need for environment-friendly mobility should continue to pledge mass transportation means such as metros, tramways, inter city andhigh speed trains. In addition, short-term demand is expected to be supported by stimulus packages put in place in a number of countries.A secured backlog in volume and in qualityAt 31 March 2009, the Group backlog reached €45.7 billion, representing 29 months of sales. The high volume and quality of this backlog give Alstom strong visibility to prepare for and face, if necessary, an extended slowdown in demand.State-owned and large utilities account today for 80% of Alstom Power Sectors customer base, and 90% of Transport Sector’s. This proportion should minimise the Group’s sensitivity to financial risks impacting its customer base. In this respect, no project cancellation or deferral has been recorded so far.A sound financial performanceAt the end of fiscal year 2008/09, Alstom showed a steady liquidity position with net cash strengthened at €2.1 billion and gross cash amounting to €2.9 billion, after the reimbursement, during the period either at maturity or in anticipation of €559 million of bonds. As of 31 March 2009, the total outstanding bonds amounted to €275 million in nominal value (vs. €834 million at 31 March 2008). In terms of bonds and guarantees, Alstom also benefits from an €8 billion committed syndicated line and €13.5 billion of bilateral lines (€2.4 billion and €5.1 billion being respectively undrawn).Preparing the futureInitiatives taken in an uncertain global contextUncertainties created by the recent economic downturn have prompted Alstom to take the following specific actions:- a programme focusing on the strict control of S&A (Selling & Administrative) expenses was set up in December 2008, and actions deployed at the Group’s unit level. Short-term specific actions have also been taken to limit IT, travel and consulting expenses. Lastly, specific attention will continue to be paid to the efficiency of support functions;- future capital expenditures will be strictly prioritised, without questioning the ongoing major projects aiming at developing and reinforcing the industrial base in key markets (Wuhan Boiler Company new factory in China, Chattanooga steam turbines facility in the United States or Elblag foundry in Poland).Streamlining of Power organisationIn March 2009, Alstom announced a reorganisation of its activities related to power generation consisting in the merger of the two Sectors, Power Systems (plants, equipments and retrofit) and Power Service (after-sales, from service to renovation and spare parts). The set-up of a single Power Sector will improve the commercial performance of the Group and optimise its engineering and production means. This new Sector will be organised around six activities (Thermal Systems, Thermal Products, Thermal Services, Hydro, Wind and Energy Management).A strong and optimised industrial baseThe Group’s capital expenditures for the fiscal year 2008/09 (excluding capitalised development costs) amounted to €499 million, an increase of 33% year on year.Market oriented, major ongoing Power capital expenditure projects include:- to address the American market, the construction of a new facility in Chattanooga (Tennessee, United States of America) to manufacture steam turbines for nuclear and thermal applications, gas turbines, generators and related equipments;- to address the Chinese and export markets, the construction in Wuhan city outskirts (Hubei Province, China) of a new facility following the acquisition of 51% of Wuhan Boiler Company in 2007. This factory will be Alstom’s largest utility boilers manufacturing site and should be operational by the end of 2009;- the building of a foundry in Elblag (Poland), aiming at increasing the production capacity of key components for turbines.In Transport Sector, the capital expenditure programmes were focused on the upgrade and expansion of the European manufacturing base for rolling stock (very high speed trains, tramways and components). The main investments have been made in France, Germany, Italy and Poland.Joint ventures and partnerships to reinforce the strategic positioningIn 2008/09, Alstom continued to deploy its growth strategy by finalising joint venture agreements and entering into promising partnerships.- during the first half of 2008/09, Alstom finalised the creation of a joint venture with JSC Atomenergomash, part of the Russian Federal Agency for Atomic Energy responsible for the development of the national nuclear programme, to provide the turbine islands of Russian nuclear power plants based on Alstom’s half-speed technology ARABELLE™. In September 2008, Alstom Atomenergomash LLC signed an agreement with Atomenergoproekt for the engineering of the turbine generator package and turbine hall equipment for the Seversk nuclear power plant in Siberia, recording a first success on the Russian market;- in November 2008, Alstom and Bharat Forge Ltd (BFL), a global leader in manufacturing and metal forming, signed a shareholders’ agreement to create a joint venture company based in India (the agreement is subject to Government and regulatory approvals). The new company will manage the whole process from engineering and manufacturing to selling and commissioning state-of-the-art 600 MW to 800 MW supercritical steam turbine islands in India;- in March 2009, Alstom and Transmashholding (TMH), the main rolling stock manufacturer in Russia, signed a strategic agreement. This agreement follows a Letter of Intent announced inOctober 2008, according to which Alstom Transport will support the modernisation of TMH manufacturing sites and the development of a new generation of rolling stock equipment adapted to the Russian market. Alstom and TMH have also committed to creating a joint venture, held in equal parts, for the development of new models of rolling stock which will be based on Alstom Transport and TMH’s latest technologies. Finally, Alstom will acquire 25% (+ 1 share) of the capital of TMH holding company at a price that will be defined according to the financial results of TMH over the 2008-2011 period.Shaping the future through innovationResearch & DevelopmentIn order to maintain its technological leadership, Alstom pursued the acceleration of its Research and Development (R&D) programmes over the last fiscal year. R&D expenditures (gross costs) amounted to €621 million versus €561 million in 2007/08. After capitalisation and amortisation of development costs, R&D expenditures as per the income statement, reached €586 million compared to €554 million last year, representing 3.1% of sales. Alstom’s flagship R&D programmes - for Power, the development of CO2 capture technologies and for Transport the AGV TM, the last generation of very high speed trains - accomplished significant progresses in 2008/09.In 2008/09, Alstom continued to pave the way for CO2 capture solutions, focusing on oxy-combustion and post-combustion processes. During fiscal year 2008/09, the Group entered the following technological partnerships:- an agreement with TransAlta Corporation, a Canadian power generation company, to develop a large scale CO2 capture and storage facility in Alberta, Canada;- a Memorandum of Understanding (MoU) with PGE Elektrownia Belchatow S.A. for the development and implementation of Carbon Capture and Storage (CCS) technology at the Belchatow power plant in Poland;- a joint development and commercialisation agreement with the Dow Chemical Company to develop advanced amine technology for CO2 capture that will be used in the design and construction of a pilot plant in West Virginia, USA.In addition, Alstom became this year a founding member of the Global Carbon Capture and Storage Institute (GCCSI), created under the initiative of the Australian government. This framework will allow Alstom to promote research in this field and set up demonstration projects.To date, Alstom has started operation at three CO2 capture pilot projects, with EPRI and We Energies in Wisconsin, USA, E.ON in Sweden and Vattenfall in Germany.Inaugurated in September 2009, Vattenfall’s Schwarze Pumpe is the first pilot plant based on Alstom’s oxy-combustion technology in the world.Other initiatives contributed to strengthen the competitive edge of Alstom’s Power products:- the creation of a Global Technology Centre for hydroelectricity in Vadodara (India), will secure together with Hydro’s Global Technology Centre in Grenoble (France), Alstom Hydro’s leadership on the entire range of hydro turbines;- R&D efforts in wind business have been focused on the development of the new 3 MW wind turbine, put in operation this year;- performance improvement of GT13TM and GT26TM gas turbines, as well as the upgrade of GT24TM remained a focus point;- lastly, Alstom Power Energy Management Business (EMB) announced its collaboration with Microsoft to deliver the next generation of high-performance information technology (IT) solutions for the power industry.While promoting environment-friendly solutions, the Transport Sector continued to develop its advanced technology in its product range:- the AGV TM ran dynamic tests in the Czech Republic before its first dynamic tests in France at 360 kph, the commercial speed it has been designed for. The AGV TM technology is based on articulated carriages and a distributed drive system. The first trains will be delivered starting from 2010;- in tramways, the prototype for a new platform aiming at broadening the CITADIS TM range will complete testing phase in Germany end of April 2009;- regarding regional trains, the first 24 CORADIA TM CONTINENTAL trains have been delivered to their customers and the CORADIA TM NORDIC X61, a product for regional traffic in Northern Europe, successfully completed its first test runs in Salzgitter (Germany);- in signalling, the Group delivered its state-of-the-art URBALIS TM evolution system on the Beijing Line 2 and the Beijing Airport Link, right on time for the Olympic Games;- finally, Alstom dedicated significant part of its Research and Development efforts to promote sustainable rail transport by developing trains featuring low energy consumption, reduced weight, hybrid or bi-modes traction and low noise pollution.“I Nove You” programmeAs a must to differentiate from the competition and to optimise processes, innovation is at the heart of Alstom’s strategy. At Group level, the “I Nove You” programme initiated last year aims at three major objectives: create a favorable environment for innovation and innovative people within the Alstom community, enhance cross-fertilisation and support ongoing efforts to leverage innovations developed outside of the Group.A reinforced Corporate ResponsibilityA caring Human Resources managementDuring fiscal year 2008/09, the Group continued to drive its headcount increase. At the end of March 2009, total headcount reached 81,500 people, including 11,000 new recruitments over the period to support the Group’s development on key markets and to ensure the execution of its growing backlog. Alstom focused its recruitment particularly in Europe (57%) and Asia/Pacific (22%). This policy may be adapted pending future market development.Care for people remained a key factor as the Group further developed its training programmes. The number of “Alstom University” training sessions delivered has doubled compared to last year, and five “Alstom University” regional campuses are operational around the world.“Environment, Health and Safety” (EHS) continuous improvementThrough continuous efforts to improve employees’ health and safety, the number of work-related incidents has been greatly reduced (-35% for 2008/09 compared to the same period a year before). The Group is committed to pursuing its efforts on training and communication to improve employees’ awareness and to minimise risks. In addition, as part of EHS policy, a new emphasis has been put on CO2 reduction on Alstom sites.Employee Sharing ProgrammeFollowing the success met by the previous programmes, a third employee stock purchase scheme was announced in January 2009 in 22 countries with the same objectives: encouraging employees’ contribution to the Group’s performance while enlarging and stabilising the shareholding base. In line with past references, close to 30% of the employees participated into this programme. The number of additional shares represented around 0.4% of the Group’s share capital.The Board of Directors also approved a new Long Term Incentive Plan based on the grant of conditional stock options and the free attribution of performance shares, depending on the Group’s performance in 2010/11; this plan could represent approximately 0.4% of the share capital.Alstom Foundation for the EnvironmentThe Alstom Foundation, created in November 2007, will devote €1 million per year to support projects in the field of environmental protection. The Foundation has rewarded the first eleven projects this year. One of the most significant initiatives rewarded will establish a new conservation programme protecting the biodiversity in a national park of China’s Yunnan Province. Other selected projects promoted actions in Argentina, North Korea, India, Switzerland, USA, Indonesia, Malaysia, Philippines, South Africa and France.GENERAL COMMENTS ON ACTIVITY AND RESULTSConsolidated Key Financial FiguresThe following table sets out, on a consolidated basis, some of the key financial and operating figures:General comments on activityver fiscal year 2008/09, power and transport markets showed a very strong activity creating nd observed in 2007/08 was confirmed this year with a he transport market has been very dynamic in 2008/09. With fast-growing urbanisation, the Orders received and backlogenefiting from favourable markets, Alstom achieved a strong commercial performance in fiscal O numerous opportunities for Alstom.Regarding Power, the favorable tre balanced demand for all technologies, both for the installed and the new base markets. Thermal continued to lead the market, not only supported by the high demand for coal in Asia and Europe, but also by an active gas market bringing new projects namely in Europe, Africa and the Middle East. Rising environmental concerns and enforcement of green regulations continued to call for the development of clean sources of energy and their substitution for polluting equipment. Consequently, demand for renewables such as hydro and wind kept on growing, and nuclear confirmed its strong potential. The market for retrofit and upgrade solutions was also fostered by a continuing demand for energy efficiency.T need for mobility and respect for the environment were again the key leading factors of a high demand for transportation means. The market for very high speed, regional trains and metros remained strong while demand for tramways continued to progress.B year 2008/09, booking a record level of €24.6 billion orders, a 5% increase compared to last year on an actual basis and 6% on an organic basis. At the end of March 2009, the Group’s backlogamounted to €45.7 billion, a 16% increase year on year, representing the equivalent of 29 months of sales.The combined Power Sectors booked €16.5 billion orders over fiscal year 2008/09, recording a 3% customers’ confidence in Alstom technology and know-how, Power Systems recorded stom confirmed its position as a leading supplier by booking an order for the Alstom continued to strengthen its global presence in renewables. In ncy as well as ageing of the installed base brought also successes eizing the opportunities of the growing service market, Power Service booked €4.6 billion orders fiscal year 2008/09, Transport realised major commercial achievements across its product the rise over the high level of the previous year on an actual basis (4% on an organic basis). Power Systems orders intake reached a new peak level with €11.9 billion, an increase of 3 % compared to previous year (on actual and organic bases), representing 48% of the Group’s total orders received.Illustrating major successes for coal and gas-fuelled power plants turnkey contracts including GT26TM -based combined-cycle power plants in Africa (the first on the continent), the Netherlands, Spain and Indonesia. Orders for equipment supply (turbines and generators) to oil or coal-based power plants were received, including key contracts in Saudi Arabia, South Africa, the Netherlands and Germany, where Alstom will supply the most advanced clean coal technology to an existing power plant.In nuclear, Al engineering and procurement of the complete turbine island for the first nuclear power plant in China to use the EPR technology. Orders for nuclear equipment retrofit were also recorded in South Africa and France.Over the last fiscal year, hydro business, the Group booked large projects in South and Central America (Brazil, Panama), Europe (Portugal, Turkey) and Asia (India, China). Eighteen months after the acquisition of Ecotècnia and the creation of its Wind business activity, Alstom smoothly pursues its expansion on the European wind market.Lastly, search for energy efficie for Alstom with hydro power plant upgrades in Africa and Norway, boiler repowering in Germany and modernisation of equipment for a gas-fuelled plant in the Netherlands.S in 2008/09, a 4% increase compared to last year on an actual basis (5% on an organic basis). The main Operation and Maintenance (O&M) contracts included projects in Algeria, Tunisia, the United Arab Emirates, the Netherlands and Spain. In addition to a record number of small and medium sized orders, Power Service signed contracts for power plants upgrade in Turkey, Hungary and France.In range, booking orders at €8.1 billion, an increase of 9% (11% on an organic basis) compared to last year, which was already an exceptional year. Historic markets (France, the United Kingdom, Germany) with new products (CORADIA TM CONTINENTAL, AGV TM ) and maintenance contracts (the United Kingdom, Italy) have driven the increase. In new markets, tramway turnkey solutions have been sold, demonstrating the continuous success of Alstom’s CITADIS TM product range. Alstom’s leading position in very high speed was confirmed with the first order received for AGV TM in Italy, whereas in high speed Alstom continued to demonstrate its know-how, booking several orders in Europe including a record contract for the extension of a PENDOLINO TM fleet and associated maintenance for the line between London and Glasgow in the United Kingdom. Alstom also benefited from the modernisation of European networks and fleets, winning severalprojects for regional trains in Germany, Sweden, France and Luxemburg as well as for locomotives in France, the Netherlands and Germany.Alstom was served by a the strong demand in mass transit, booking numerous turnkey projects Sales upported by the smooth execution of a growing backlog, the Group’s sales once again ower Systems achieved €9.2 billion sales, accounting for 49% of the Group’s total sales in ower Service generated €3.8 billion sales in fiscal year 2008/09, increasing by 6% the previous fiscal year 2008/09, Transport recorded sales at €5.7 billion, a 3% growth year on year on an Income from operationscome from operations reached €1,536 million in fiscal year 2008/09, representing a 19% ll Sectors contributed to the Group’s income from operations and operating margin growth. Power Systems commercial performance drove an increase of income from operations by 45% on based on the Group’s CITADIS TM tramway products in North Africa and Middle East, and recoding metro contracts in Asia, South and Central America and North America, where the New York Municipality confirmed option for additional subway cars. Signalling projects, namely for Santiago de Chile and Sao Paulo metros, as well as orders for infrastructure (Romania) and maintenance for main lines fleets (Switzerland) also contributed to Transport Sector’s high level of orders intake in 2008/09.S established a record at €18.7 billion, showing an 11% increase year on year on an actual basis (10% on an organic basis).P 2008/09, and representing a 19% increase year on year on an actual basis (16% on an organic basis). Main contracts contributing to sales over the period included gas-based power plant projects in Europe (the United Kingdom, Ireland, the Netherlands, France), the United Arab Emirates, Algeria, Brazil and Australia, boilers projects in Poland, Bulgaria and Germany as well as hydro projects in India and Brazil.P figure on an actual basis and by 8% on an organic basis.In actual basis (5% on organic). Significant main lines contracts traded during the year included high speed trains (TGV 1) in France, regional trains in France, Spain and Germany, several projects for locomotives in France and Germany as well as a maintenance contract in the United Kingdom and signalling projects executed in Belgium and Italy. Traded mass transit contracts covered metro projects in the USA (New York City, Atlanta), Spain (Barcelona), Brazil (Sao Paulo), Hungary (Budapest) and Singapore and the delivery of a tramway turnkey system in Algeria (Algiers).In increase compared to last year on an actual basis (18% on an organic basis). The operating margin rose from 7.7% to 8.2%, driven by the good quality of the orders in hand, a proper execution of the backlog and continuous cost controlling.A1TGV is a trademark of the SNCFan actual basis (42% on an organic basis) from €415 million in 2007/08 to €600 million in 2008/09, Power Service improved income from operations to €648 million from €592 million a year earlier (9% on an actual basis and 7% on an organic basis), representing 17.0% of sales in fiscal year 2008/09. Transport’s income from operations was €408 million, stable versus last year, at 7.2% of sales.Net profit (Group share) N grew from €852 million to €1,109 million year-on-year. This 30% crease in one year mainly stemmed from a strong increase of income from operations. Free cash flow (as defined in paragraph “Use of non-GAAP financial indicators”) reached 1,479 million in fiscal year 2008/09, compared to €1,635 million for the previous year. Switching from net debt to net cash in 2007/08, the Group’s net cash position increased by more an €1 billion over last fiscal year to €2,051 million. This record surge includes €233 million rders by region of destinationT ders received by region of destination: e total orders booked by the Group over the period (48% in 2008/09 compared to 50% last year). he Transport Sector achieved major commercial successes booking the first order for the supplyet profit (Group share)inFree cash flow€Supported by the increase of net income and a further improvement of working capital, the large free cash flow generation includes the Group’s continuous investment efforts in R&D and capital expenditures.Net cashth dividends paid during the year (vs. €117 million last year).Key geographical figuresGeographical analysis of ohe table below sets out the geographical breakdown of orWith €11.7 billion for the year ended at 31 March 2009, Europe still accounted for almost half of th T and maintenance of the AGV TM in Italy for an Italian private operator, the supply and maintenance of PENDOLINO TM trains in the United Kingdom and regional trains in Germany and。

brochure_20090320132901

2009亚洲柴油车排放论坛暨亚洲AdBlue 论坛11-12 May 五月十一日至十二日13 May 五月十三日Keynote speakers include:AdBlue ForumAsia’s largest independent forum for diesel emissions business strategy 亚洲最大的柴油车排放企业策略论坛The global economic outlook for the Asian diesel emissions industry• 给亚洲汽车工业的全球经济视野领域将逆势成长?Asian and global legislative updates and forecasts• legislation?亚洲及全球的法规讯息更新及预测有效达到越趋严格的排放标准?Fuel quality challenges and opportunities in Asia• 燃油品质挑战及亚洲的机会Assessing advanced emission reduction technologies and on board • diagnostics讨论先进的排放减量科技AdBlue infrastructure development in Asia• 亚洲的AdBlue基础建设发展投资机会?MArTin MAodong FAng 方茂东Executive Director, Committee of Vehicle Emission Control (CVEC) 秘书长,机动车污染防治委员会Xu JiAn 许健Vice President, Volkswagen group China 副总裁, 大众汽车中国KirAn VAirAgKAr 奇让发拉戈卡尔General Manager, Mahindra & Mahindra Ltd., india总经理, 马亨德拉汽车公司,印度rudi Von MEisTEr 万如意General Manageriveco Fiat China Co. Ltd., China 大中华区总经理, 依维柯中国ZhAng JiAnrong 张建荣Deputy Chief Engineer, sinopec, research institute of Petroleum Processing, China 副总工程师,中国石化石油化工研究院KArL-hEinZ KusTErMAnn 卡尔-汉兹.库斯特尔曼Vice President, Engineering , BMW China 工程副总裁,BMW 中国dr PAuL grEEning 保罗格瑞宁博士Director Emissions & Fuels, ACEA – European Automobile Manufacturer’s Association 排放和燃油部主任,欧洲汽车制造商协会PETEr CArrAChEr 彼得卡拉克尔Technical Director, iveco, China科技总监, 上汽依维柯红岩商用车公司27diesel emissions ConFerenCeAssociate sponsor 联合赞助商:Lunch sponsor 午餐赞助商:Silver sponsor 白银赞助商:Endorsers 合作单位:A selection of companies speaking 贵宾主讲人公司:Hosted by:Media partners 媒体合作伙伴:Simultaneous translation English/Chinese available at the conference会议将提供同步传声英/中文翻译• LATEST DiESEL EMiSSiOnS LEGiSLATiOnS – learn about the latestdevelopments in Asian diesel emission regulation by meeting directly with key legislators.• inSiGHTFuL DiESEL FuEL quALiTy DiSCuSSiOnS – hear casestudies, analysis and panel discussion from leading industry experts that will enable you to identify the crucial fuel quality issues which significantly affect diesel emissions.• ADVAnCED DiESEL EMiSSiOnS REDuCTiOn TECHnOLOGy – find out which are the most cost-effective and fuel-efficient technologies for meeting emissions limits in Asia.• GROWinG BuSinESS OPPORTuniTiES – discover investment opportunities in Asian markets for diesel emissions reduction equipment which continue to grow despite the global economic slowdown.• ExCELLEnT nETWORKinG OPPORTuniTy – network with Asian truck manufacturers to better evaluate the opportunities for increased sales.• 最新的柴油车排放法规——了解最新的亚洲柴油车排放法规发展,透过与立法者的直接会面。

国际橡胶研究组织预测2009年橡胶消费

大 幅度下 降 , 到 每 吨 20 跌 70元 左 右 , 使许 多 制糖 致 企业 陷入严 重亏损 。 3月初 开始 , 从 食糖 价格 开始 止 跌 回升 , 目前 价格在 每 吨 30 6o元左 右 。

一

1 一 4

殖。

麦 克雷 雷 大 学兽 医专 业 D v aa s 教 授表 ai K b aa d 示 :过 去 的 五 十 年 中 ,乌 干 达 的 气 温 已上 升 摄 氏

0203度 ,加 快 了各 种农 作 物 与动 物疾 病 的传 播 。 .— .

另 外农 民大量使 用 化肥造 成 土地 贫瘠 。

( 郑淑 娟 译  ̄/ ww.o h lz . m/0 9 0 - / w f s pa ac 2 0 - , r o 4

国际橡胶研究组织 预测 20 年橡胶消费 09

20 0 9年 3月 2 4日,国 际橡 胶研 究组 织秘 书长 声 称 ,0 8年 全球 天然 橡 胶及 合 成橡 胶 的总 消费量 20

迫 于 以上 原 因 。政 府派 遣 一支 以研 究香蕉 为 主

有 关人 士认 为 。我 国 2 0 0 8跨 2 0 蔗糖榨季 0 9年 食糖 减产 , 食糖 价格 有可 能 进一 步攀 升。 如果市场 对 食糖 的需求 不 出现 较大 幅度 滑坡 ,下半 年甘蔗种 植 面积不 出现大 面积 增加 。今 年 的食 糖价格 还将有所 攀升 。

2009年中美轮胎特保案分析

2009年中美轮胎特保案分析王帅中澳一班 09070534轮胎特保案是指美国国际贸易委员会于2009年6月29日提出建议,对中国输美乘用车与轻型卡车轮胎连续三年分别加征55%、45%和35%的从价特别关税。

根据程序,2009年9月11日,美国总统巴拉克·奥巴马决定对中国轮胎特保案实施限制关税为期三年。

2010年12月13日,WTO驳回中国提出的美国对其销美轮胎征收反倾销惩罚性关税的申诉,仲裁小组表示美国在2009年9月对中国销美轮胎采取“过渡性质保护措施”征收惩罚性关税未违反WTO规定。

2011年9月5日,世界贸易组织(WTO)裁定中国败诉。

此案是奥巴马时代美国首起对华特保案,也是针对中国的最大特保案,可能导致其他国家和地区抵制中国产品。

该案也是奥巴马对华贸易政策的风向标。

2009年4月20日,美国钢铁工人联合会向美国国际贸易委员会提出申请,对中国产乘用车轮胎发起特保调查。

其在诉状中声称,从中国大量进口轮胎损害了当地轮胎工业的利益;若不对中国轮胎采取措施,到2009年年底还会有三千名美国工人失去工作。

事件起源于2009年6月29日,美国国际贸易委员会(ITC)以中国轮胎扰乱美国市场为由,建议美国将在现行进口关税的基础上,对中国输美乘用车与轻型卡车轮胎连续三年分别加征55%、45%和35%的从价特别关税。

根据美国调查程序,在8月7日的听证会后,美国总统将于9月17日前作出是否采取措施的最终决定。

与此同时,中国也对次时间进行了反击。

中华人民共和国商务部2009年9月13日毅然做出决定,对美国部分进口汽车产品和肉鸡产品启动反倾销和反补贴立案审查程序。

中国政府2009年9月14日正式就美国限制中国轮胎进口的特殊保障措施启动了世界贸易组织争端解决程序。

中国常驻世贸组织代表团在一项声明中说,中方当日正式就美相关措施提出世贸组织争端机制框架内的磋商要求。

中方要求与美方磋商,是行使世贸组织成员权利的正当举动,是维护自身利益的切实行动。

中美轮胎特保案

第六部分: 中国出口企业面临的问题和挑战

1. 中国出口企业如何避免卷入贸易摩擦。 2. 中国出口企业如何有效应对贸易摩擦。 3. 中国出口企业应对贸易摩擦的力度是否够分量、方式

是否欠佳。 4. 中国出口企业如何摆脱WTO窘境。 5. 中国出口企业该如何根除贸易风险。

第七部分:

对中国出口企业存在的问题和面 临的挑战,我们提出几点建议

第二部分:中美双方争论焦点聚焦

美国方面

中国方面

◆ 造成美国就业萎缩

美国钢铁业工会称,在过去的5 年间,由于中国轮胎大量进入 美国市场,导致美国轮胎业失 去去了大约5000个工作岗位, 损害了美国工业的利益。

要求奥巴马政府更严格执行贸 易法规,对中国产轮胎进入美 国市场征收3年制裁关税。

◆ 将使中美损失庞大就业

2,2009年8月17日和18日中国商务部副部长钟山就轮 胎特保案与先后与美国国务院、财政部、贸易代表办公 室、商务部以及白宫国家安全委员会官员进行了交涉与 磋商,未果。

3,2009年9月11日,奥巴马宣布对中国轮胎采取 特保措施:对中国制轮胎征收3年特别关税。

美国新的轮胎关税政策将于2009年9月26日开始 生效。根据WTO规则,相关国家可以直接援引美国的制 裁方案对中国轮胎实施制裁。

4.此案遭到专家学者的反对。

参加夏季达沃斯年会的专家学者,包括世贸组织官员、美国研究机构研 究员、墨西哥前总统和泰国贸易代言人,对此案作出反应,认为此举是贸易 保护行为,不利于世界贸易增长,无助于国际社会共同应对金融危机。

第四部分:

特保案—燕尾服下的狼牙棒

———看美国总统奥巴马

凭借高超的演讲技巧、俊朗的绅士风度和充满亲和力的微笑,美国首 位非洲裔总统奥巴马在世界范围内掀起了一场不小的时代潮流。于是,当 人们问,2009年的流行是什么?“力量”、“含蓄”和“平民”成为了主 要的用词。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Dear reader,I am pleased to bring forth the latest issue of Auto Track, Ernst & Y oung’s newsletter on the IndianThe journey of change in the global automotive industry continues. China has overtaken US as the biggestautomotive market in the world with an annual estimate of 12 million light vehicle sales for 2009 as against10.5 million in the US. Europe’s leading car manufacturer Volkwagen is hair’s-breath-close to General Motors inglobal volumes and is all set to gain no.2 position after T oyota.The Indian automotive industry has performed well in the first half of the current fiscal posting a growth ofmore than 15% in the domestic markets. Activity level was high in the recently concluded festive season and as I write, there is anexpectation that the growth story will continue in the month of October also.India’s contribution to the global automotive industry needs a special mention and accolades. Reportedly, there are only two-carcompanies globally which have posted profits in Q1FY10, Honda and Suzuki and both of these companies have attributed this to theperformance of their Indian JVs, Hero Honda and Maruti Suzuki respectively. Another key aspect has been the increasing export ofcars from India which now stands larger than China’s. Between India and China, Indian automotive industry is reportedly considereda better place to invest given a 100% FDI allowance as against the strict rule of necessity of a local JV partner in China. In anotherdevelopment, China’s largest car maker Shanghai automotive Industry Corporation is contemplating a collaboration with GM India Forewordto produce light commercial vehicles in latter’s plant in T alegaon located in Maharashtra. GM tying up with Reva, India’s first electriccar company, to produce an electric variant for one of its existing products, is a point in case for India’s growing engineering andtechnology capabilities.The general sense of optimism is increasing with each month passing. Rising financial markets and increase in foreign capital inflowsare positive signals for the Indian economy which is showing signs of revving up, again. And this is great news for the commercial vehicleindustry which is so heavily dependant on the level of economic activity. There has been a significant improvement from the slumpwitnessed in Q3FY09. Sales for Light Commercial Vehicle (LCVs) have already started to pick-up and have secured a handsome growth of20% for Apr-Sep09 over same period last year. But the entire industry is not out of the woods completely. Medium & Heavy CommercialVehicle (MHCV) are still down y-o-y so are the CV exports.The Indian CV industry has a huge potential. This industry has been dominated by domestic players, however is attracting a lot of internationalplayers. The capacities are being added and the international players are expected to contribute heavily towards this growth in capacity.In this edition of Auto-track, we take a look at how the CV industry has been performing, how competitive scenario is shaping up, what are thevarious trends emerging and the way forward.I look forward to your feedback and comments.Rakesh BatraAutomotive Sector LeaderErnst & Y oung, IndiaRakesh.Batra@Ernst & Y oung’s Auto-track October 20092 (4)555678 (10)1313131415161718212231. Industry growth patternsa). Spectacular growth between FY03and FY07The Indian CV industry witnessed spectacular growthbetween FY03 and FY07, growing at a CAGR of more than 25%. A favourable macroeconomic environment, increased industrial activity and easy financing, among others reasons, were significant drivers of growth in the domestic market. Trend in total CV sales (domestic + exports)Source: SIAM, EY analysis-300,000-200,000-100,0000100,000200,000300,000400,000500,000600,000-40%-20%0%20%40%60%80%DomesticExportsDomestic growthExports growthExports accounted for approximately 10% of the total volumes.In 2004, the rule commonly known as Golden Pass, under which trucks were allowed to carry more load than the law sanctioned on the payment of meager penal charges, was withdrawn. This led to a spurt in the growth of CVs in the goods carrier segment.b). Growth slowed in FY08 and fell in FY09A corrective period followed the five-year phase that witnessed growth of more than 25%. In FY08, easyfinancing, which was a significant growth driver , declined significantly. The interest rate began to increase, thereby impacting borrowing cost and subsequently the total cost of ownership. With as many as 90 out of 100 vehicles being sold on finance, the liquidity crunch came as a big blow. Non-banking finance companies (NBFCs) virtually stopped lending to first-time users and small-fleet operators. T otal creditdisbursement in the CV industry is estimated to have declined by 33% in FY09 over FY08.The global slowdown adversely impacted both global anddomestic demand in FY09. Industrial activity plummeted, and GDP growth projections were reduced with every subsequent revision. The third quarter of FY09 saw the worst for the Indian automotive industry in recent times, with CV sales falling by 48% in the domestic market. Exports also slumped by 40% in the same period.Despite some revival in consumer demand toward the end of FY09, industrial activity remained sluggish, with negative growth in the Industrial Index of Industrial Production (IIP) in the fourth quarter of FY09. The sales volume in this quarter , however , improved sequentially over the third quarter.Correlation between IIP and CV sales-55101520A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -A u g -D e c -A p r -i n p e r c e n t a g e10203040506070i n '000 u n i t sIIP (% change)T otal CV demandSource: CRIS INFAC, EY analysis5Ernst & Y oung’s Auto-track October 2009During FY09, CVs de-grew by 22% and exports declined by 28%. Although all segments were impacted, higher tonnage vehicles were worse hit. The MHCV segment de-grew by 33% as compared to a 7% decline in LCVs in the domestic market.Within the domestic HCV segment, a slowdown inconstruction and mining and delays in awarding licenses and construction projects affected the sales of tippers and dumpers, which contribute around 30% of total heavy truck sales.While considering classifications based on load, thepassenger carrier (bus) segment, which is considered to be non-cyclical, witnessed a 7% y-o-y decline in domestic sales during FY09. In contrast, the goods carrier segment, which constitutes more than 80% of total CV sales, was down 24% y-o-y.Goods carriers: segment-wise domestic sales trend (FY09)50002500045000LCVMHCV U n i t sSource: SIAMPassenger carriers: segment-wise domestic sales trend (FY09)U n i t sSource: SIAMLCVMHCVc). Government stimulus packageFollowing the economic downturn and a sharp decline in sales volume, the government initiated measures to help revive sales in the CV industry. The government’s stimulus package featured two primary components:1. Government grant for buses: Under the JawaharlalNehru Urban Renewal Mission (JNNURM), thegovernment agreed to provide a 50% subsidy of the cost of new buses purchased till 31 December 2009 for urban transportation. T otal funds allocated to state governments were INR42,000 million. It is estimated that6Ernst & Y oung’s Auto-track October 2009Source: SIAMCV: FY10 growth trends in domestic market (y-o-y)P e r c e n t a ge -60%-40%-20%0%20%40%MHCVLCVCVUnder the Jawaharlal Nehru Urban Renewal Mission, the government has allocated Rs. 42,000 million to the cost of new buses purchased till 31 December 2009.around 10,400 buses, equivalent to approximately four months of sales, have already been ordered underthe scheme. This is significantly lower than the total grant which could potentially cover 60,000 buses based on theanalysis below.Source: EY analysis2. Government grant for trucks: T o create surplus demandfor trucks, the government launched the following initiatives:R educing excise duty on CVs from 10% to 8% • Depreciating 50% on CVs purchased till•30 September 2009Directing public sector banks to increase funding to•NBFCs to help revive CV demandd). A rebound in FY10FY10 has begun on a positive note. Increased industrial activity in the first half of FY10, along with variousgovernment benefits provided to boost sales, have yielded positive results. LCVs have started growing, posting a y-o-y increase of 20% in the first six months of FY10. T otal CVs, however, fell by 1% due to significant de-growth in MHCVs.Source: SIAMWhile the domestic markets have seen some respite, the export markets are still not out of the woods due to a more severe slowdown in the global markets. For the first sixmonths of FY10, exports have declined by 36% as compared to same period last year .7Ernst & Y oung’s Auto-track October 2009e). OutlookShort-term outlookConsidering the strong correlation between CV sales and economic activity, FY10 may prove to be a tough year for CVs. While we expect that the economy is likely to start looking up after the first half of FY10, we do not expect the recovery to immediately translate into higher sales of CVs. Moreover, exports are likely to be under severe pressureSources: JD Power , CIA World Factbook, Global Insight, EY analysisNote: numbers have been estimated from various sources using the latest available data and should be considered as indicative. The bubble size indicates the expected growth in industrial production.(10,000)Paved roads/total landdue to the slowdown in the global markets, which is not expected to recover in the short term. LCVs are expected to outperform MHCVs in both the domestic and export markets.Long-term outlookCurrently, India has the lowest MHCV penetration among the BRIC economies and a higher-than-average paved road penetration. Both are reflective of the significant opportunity share for the CV industry in India. However , there are a fewer number of expressways in India as compared to its peers. This will have to be increased to boost CV industry growth.There are a fewer number ofto boost CV industry growth.8Ernst & Y oung’s Auto-track October 2009While we expect that the economy is likely tostart looking up after the first half of FY10,we do not expect the recovery to immediatelytranslate into sales of CVs at levels prior to FY09.9Ernst & Y oung’s Auto-track October 20092. Competitive landscape: international presence to increase sevenfoldSharing more than 90% of the total market collectively, local players such as T ata Motors, Ashok Leyland, M&M and Eicherhave traditionally dominated the CV industry.CVs: market share trend6%4%4%0%25%50%75%100%DomesticInternationalconsumer needs and a low-cost product CVs: domestic market share in MHCV segment for FY09Eicher 7.4%T 61.9%0.1%Source: SIAMCVs: domestic market share in LCV segment for FY09Source: SIAMT 59.91%4.49%10Ernst & Y oung’s Auto-track October 2009Growth opportunities lured various international players such as Mazda, Volvo and T etra Vectra. Despite entering the Indian market more than five years ago, they have not been able to garner a sizable market share. New players such as Daimler , Piaggio, MAN AG and Hino have entered the CV industry recently.Capacity additionThe Indian CV industry currently has the capacity toproduce 0.85 million units. Actual production in FY09 was 0.42 million, signifying low plant capacity utilization. From 0.38 million units currently, the domestic market is estimated to reach 1 million units by FY20.CVs: share of total installed capacity90 %T otal: 0.85 millionT otal: 1.5 million20082013Source: EY analysis, industry articles and press releases via Dow Jones FactivaT o tap the industry’s potential, significant capacity additions are expected. It is anticipated that international players will contribute more than 70% of the incremental capacity. As such, their share in total industry capacity is projected to increase to 37% in the medium term from the current 10%.In the Indian market, collaborating with a local player has been a time-tested strategy to gain quick access to local intelligence and to understand the complexities of dealing with various regulatory and statutory authorities. Apart from leveraging the advantages of an already established distribution network, associating with a local player increases brand awareness.CVs: comparative market size (India = 100)200400600800100012001400160018002000IndiaUS China Japan France Mexico South KoreaBrazil Thailand UK GermanySource: SIAM, CRIS INFACNote: Data for FY08 for India and for CY07 for all other countries11Ernst & Y oung’s Auto-track October 2009E = Expected once operation commenceOther possible entrantsCollaborating with an overseas partner is beneficial to Indian players as well, since it provides them with access to better technology and a wider product range, thereby facilitating diversification.Ashok Leyland is planning to enter the LCV segment with Nissan.•Force Motors, primarily an LCV player , entered the MHCV segment with MAN AG.•M&M, which ranks second in the LCV segment, is planning to enter the MHCV space with Navistar .•12Ernst & Y oung’s Auto-track October 20093. Emerging trendsSource: SIAM, EY analysis0%20%40%60%80%100%S h a r eSCV LCVMHCVCVs: composition of SCV and three-wheeler salesb). Alternative fuelsDiesel has been one of the traditional fuels used for CVs. However , the focus is gradually shifting toward CNG as a result of growing concerns around rising pollution and climate change. Both customers (owing to the lower running costs of CNG) and manufacturers (owing to CNG’s pollution-reducing nature) are becoming increasingly inclined toward CNG. As the number of cities the CNG distribution network covers is expected to increase from 30 to 250 by 2018, CNG vehicle are expected to increase.The following are among the initiatives players have taken in the CNG segment:M&M launched a CNG version of its Maxi Truck LCV in •June 2009.Ashok Leyland has announced its plans to launch a •CNG HCV.In association with Australia’s Eden Energy, Ashok•Leyland has developed a hythane (blend of natural gas and hydrogen)-powered, 92-KW engine.T ata Motors has announced its plans to develop a hybrid•bus, which is expected to run on CNG or a diesel-electric engine combination.13Ernst & Y oung’s Auto-track October 20094. Positive trends for the CV industrya). Sustained levels of investment in varioussectors of the economyThe sustained level of additional investments in various sectors consuming CVs is expected to increase activity in these sectors. This, in turn, will positively impact CV demandin the next two three years. Source: CRIS INFACFor instance, India’s organized retail sector is under-penetrated and has been growing at close to 30% annually in the past few years, with the exception of a slowdown in FY09. Players in this sector have plans to increase their presence significantly in tier-2 and tier-3 cities. As LCVs are largely used for the redistribution of consumption goods, enhanced presence in smaller cities is expected to increase the demandfor LCVs.b). Freight transportation by road isexpected to increaseUntil 2007, both India’s GDP and IIP witnessed robustgrowth. This resulted in increased road freight movement in the country. Although the railway network is heavily targetingTrend in the share of road in total freight movementSource: BMI40455055602006200720082009f 2010f 2011f 2012f 2013fShare of road in total freight movement (%)the movement of commercial goods at present, it is expected that the share of freight movement by road will increase. An increase in freight availability boosts the demand for trucks, primarily heavy trucks used to transport manufactured goods and agricultural produce.T o complement this trend, the government has been increasing its allocation for road infrastructure. Oneparticular milestone has been the construction of the Golden Quadrilateral, an expressway that connects all four metros in India. The expressway is 97% complete. Such initiatives are expected to reduce transportation time and increase competition for the railways.c). Other changesGovernment has taken positive steps to introduce new•emission and safety standards for commercial vehicle industry which is expected to enhance the road safety and will be more beneficial for the environment.There has been a notable increase in professional third-•party transportation and supply chain services ( 3PL) which will be more conducive for the growth of the CV industry.Fleet owner are increasingly focused on lowering of total•cost of ownership i.e. Rs./tonne km for the entire life of asset, instead of intial purchase price of the asset .14Ernst & Y oung’s Auto-track October 20095. Industry challenges). Driver tr ining: Except the basic requirementsassociated with a driver’s license, no fixed standards of training are required to drive a CV in India. The shortage of trained drivers is one of the major challenges the CV industry is facing.b). Spare part availability: Traveling across the countryby road entails passing through many small andinaccessible villages, which have neither proper service stations nor spare parts. India is a geographically vastcountry with diverse terrains and territories, and the regular availability of spare parts is a major challenge for vehicle manufacturers.c). Regional transport offices (RTOs): While travelingbetween states, a fair amount of time is lost insubmitting documents and obtaining clearances at RTOs. Untrained personnel at non-computerized offices, along with bureaucracy and corruption, are the main factors driving this trend.d). Fuel dulter tion: Prevalent more in non-urban areas,fuel adulteration leads to the non-optimal performanceExcept the basic requirementsassociated with a driver’s license, no fixed standards of training are requiredto drive a CV in India.of a vehicle, and may lead to breakdowns and anunproductive increase in journey time. In a sample test conducted with fuel from various petrol stations, the Environmental Pollution Control Authority (EPCA) found that 8.7% of the total sample was adulterated. This number is expected to be higher in smaller cities and rural areas.e). Lower use of technology: While some playersrecently started installing technologies such as GPS in vehicles, Indian vehicle manufacturers typically do not fully leverage different technologies as compared to developed countries.15Ernst & Y oung’s Auto-track October 20091.Acquisitions and alliancesAlliances17Ernst & Y oung’s Auto-track October 20092. Key projects announced18Ernst & Y oung’s Auto-track October 200919Ernst & Y oung’s Auto-track October 200920Ernst & Y oung’s Auto-track October 2009India: EY Automotive Index (EY AX) and BSE SensexNote: EYAX is a market capitalization weighted index comprising 20 automotive companies selected on the basis of their existing market cap. It consists of the large market cap companies in each of the four automotive industry segments(passenger cars, CVs, two- and three-wheelers and auto components).85100115130145160May 2009June 2009July 2009August 2009September 2009BSE Sensex EYAXRegional and world automotive indicesSource: “History Wizard,” Bloomberg, accessed 16 September 2009Note:DJUSAP: Dow Jones US Automobiles & Parts IndexP1ATO: Dow Jones Asia/Pacific Automobiles & Parts IndexMXWO0AC: Morgan Stanley Capital International World Auto and Auto Components Index MXWO: Morgan Stanley Capital International World IndexMXEU0AC: Morgan Stanley Capital International Europe Auto and Auto Components Index9095100105110115120125130135140May 2009June 2009July 2009August 2009September 2009P1ATO Index MXWO0AC Index MXEU0AC IndexMXWO IndexDJUSAP Index3. Global market movesErnst & Y oung Center for Business Knowledge (CBK) research •and analysis“Has the CV industry bottomed out?,” Avendus Research, 28 •February 2009, via Thomson Research.“Automobiles,” Edelweiss, 3 July 2009, via Thomson Research.•“Auto & Auto Parts,” Nomura, 24 February 2009, via Thomson •Research.“Bajaj to use KTM alliance to roll out bigger bikes (plans to•utilise the partnership for jointly manufacturing complex, high-end and powerful engines),” 26 May 2009, Indian BusinessInsight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Bajaj Auto to raise stake in Austria’s KTM,” 14 July 2009,•Business Standard, via Dow Jones Factiva, © 2009 BusinessStandard Ltd.“Hero steps out from Daimler JV (because of tough economic •conditions and a lull in commercial vehicle sales in India),” 26April 2009, Indian Business Insight, via Dow Jones Factiva, ©2009 Informatics (India) Ltd.“JBM to buy European firm for Rs 300 crore,” 16 June 2009, •Business Standard, via Dow Jones Factiva,© 2009 Business Standard Ltd.Sohini Das, “M&M may buy out partner in Mahindra South•Africa,” 11 June 2009, Business Standard, via Dow JonesFactiva, © 2009 Business Standard Ltd.“T ata Motors may buy Thonburi stake in Thai truck JV,” 10•August 2009, Business Standard, via Dow Jones Factiva, ©2009 Business Standard Ltd.“Sumitomo Metal to make car engine parts in India via joint•venture,” 18 May 2009, Kyodo News, via Dow Jones Factiva, © 2009 Kyodo News.“Chery, Great Wall mull to enter Indian car market,” 1 May•2009, Auto China, via Dow Jones Factiva, © 2009 China DailyInformation Company.“Fiem Industries enters into an agreement with Japanese firm,”•11 May 2009, The Press Trust of India Limited, via Dow JonesFactiva, © 2009 Asia Pulse Pty Limited.“Japanese firm gets nod to form JV with Kailash Vahan Udyog,”•9 June 2009, The Press Trust of India Limited, via Dow JonesFactiva, © 2009 Asia Pulse Pty Limited.“Magna Seating, Krishna Group establish joint venture in India,”•6 August 2009, Datamonitor News and Comment, via DowJones Factiva, © 2009 Datamonitor plc.“Modi Rubber back in tyre biz, after 8 years,” 13 June 2009,•Business Standard, via Dow Jones Factiva,© 2009 ElsevierEngineering Information.Sindhu Bhattacharya, “Setco to make clutches for cars,” 23 May•2009, DNA - Daily News & Analysis, via Dow Jones Factiva, ©2009. Diligent Media Corporation Ltd.“Japan’s T achi-S, Lear to build carseat plants in India, Thailand,”•27 July 2009, Asia Pulse, via Dow Jones Factiva, © 2009 AsiaPulse Pty Limited.“TRF forms joint venture to make auto components•(at the T ata Motors vendor park in Lucknow),” 3 June 2009,Indian Business Insight, via Dow Jones Factiva,© 2009 Informatics (India) Ltd.“Allison Transmission India to export parts (is setting up a plant•in India, which it plans to make an export hub for automatictransmission parts),” 1 June 2009, Indian Business Insight, viaDow Jones Factiva, © 2009 Informatics (India) Ltd.“Country’s 2nd electric car unit near Chennai,” 13 July 2009,•Business Standard, © 2009 Business Standard Ltd. via DowJones Factiva, © 2009 Business Standard Ltd.“Bosch Automotive unit on stream,” 27 May 2009,•The Hindu, via Dow Jones Factiva, © 2009 Kasturi & Sons Ltd.“Bridgestone Invests 2.6 bil. Rupees in Indian Tyre Plant•Expansion,” 24 July 2009, IHS Global Insight Daily Analysis, viaDow Jones Factiva, © 2009, IHS Global Insight Limited.“Jagdish Khattar’s Carnation Auto to invest Rs 1,000 cr in•expansion,” 2 June 2009, United News of India (UNI).“Cummins Rs 750-cr project near Pune,” 27 June 2009,•T endersinfo, via Dow Jones Factiva.“Mercedes-Benz India plans to invest E700 million to increase•truck production,” 6 August 2009, Datamonitor News andComment, via Dow Jones Factiva, © 2009 Datamonitor plc.“Mercedes-Benz spending on car factory, dealers,” 1 July 2009,•Just-Auto, via Dow Jones Factiva, © 2009 Aroq Limited.“Falcon Tyres plans to raise Rs 100 cr for expansion,” 23 July•2009, Business Line (The Hindu), via Dow Jones Factiva, ©2009 The Hindu Business Line.“Fiat India to raise $510 mn loan,” 21 July 2009,•The Economic Times (MCT) (India), via Dow Jones Factiva, ©McClatchy - Tribune Information Services.“GM Exec: Expect T o Start India Engine Plant By Early 2010,”•2 June 2009, Dow Jones International News, via Dow JonesFactiva, © 2009 Dow Jones & Company, Inc.“Hindustan Motors revamps auto component unit,” 25 July•2009, Business Line (The Hindu), via Dow Jones Factiva,©2009 The Hindu Business Line.“Honda Siel to set up engine plant in India,” 15 June 2009,•Auto Business News, via Dow Jones Factiva, © 2009, ElectronicNews Publishing.“Hyundai to start diesel engine production by next year-end,” 8•July 2009, Business Line (The Hindu), via Dow Jones Factiva, ©2009 The Hindu Business Line.“Solvay to have presence in India,” 19 June 2009, Indian•Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“JK Tyre looks to set up radial unit in TN,” 3 August 2009, The •Economic Times, via Dow Jones Factiva, © 2009 The Times of India Group.“Leo Fasteners to expand capacity,” 12 August 2009, •The Economic Times, via Dow Jones Factiva, © 2009 The Times of India Group.“Lucas Indian Service enters organised car accessories market,” • 4 June 2009, Business Line (The Hindu), via Dow Jones Factiva, © 2009 The Hindu Business Line.“India’s Mahindra to invest $420 mln in expansion,” 28 May •2009, Reuters News, via Dow Jones Factiva, © 2009 Reuters Limited.“Magna International to set up facility in India (an integrated •manufacturing unit),” 31 May 2009, Indian Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Mann + Hummel Bosch setting up 2nd plant in Himachal,” 4 •June 2009, Business Line (The Hindu), via Dow Jones Factiva, © 2009 The Hindu Business Line.“Maruti Suzuki to set up stockyards in India,” 5 May 2009, Auto •Business News, via Dow Jones Factiva, © 2009 Electronic News Publishing.“Suzuki makes Haryana hub of its investment in India,” 11 •August 2009, United News of India (UNI), via Dow Jones Factiva, 2009, © HT Media Limited.“Maruti to invest Rs 2K cr to drive up output,” 28 July 2009, •The Economic Times, via Dow Jones Factiva,© 2009 The Times of India Group.“Govt clears Michelin’s Rs11k crore FDI proposal to set up•factory,” 10 July 2009, Indian Business Insight,via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Mitsui Chemicals to Decide in 2010 on PP-compound Plant in •Brazil / India,” 8 July 2009, Japan Chemical Web, via Dow Jones Factiva, © 2009 The Chemical Daily Co., Ltd.“MUNJAL SHOWA L TD (a new plant to manufacture shock •absorbers),” 26 April 2009, Indian Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Oeitker opens its lone manufacturing facility in India,” 18 May •2009, The Press Trust of India Limited, via Dow Jones Factiva, © 2009 Asia Pulse Pty Limited.“Peugeot to set up car plant in India,” 5 June 2009, Auto •Business News, via Dow Jones Factiva, © 2009 Electronic News Publishing“Peugeot plans to enter Indian market,” 8 June 2009, Auto •Business News, via Dow Jones Factiva, © 2009 Electronic News Publishing.‘The Statesman (India): Piaggio to make 2-wheelers in India,” 5 •July 2009, The Statesman , via Dow Jones Factiva, © 2009 The Statesman (India).Boby Kurian and S Sanandkumar , “Popular Vehicles may get Rs •110-cr PE funding,” 27 April 2009, The Economic Times, via Dow Jones Factiva, © 2009 The Times of India Group.“Reva Electric Car Company Planning New Plant in India,” 22 July•2009, IHS Global Insight Daily Analysis, via Dow Jones Factiva, © 2009 IHS Global Insight Limited.Sindhu Bhattacharya, “Setco to make clutches for cars,” 23 May•2009, DNA – Daily News & Analysis, via Dow Jones Factiva, © 2009 Diligent Media Corporation Ltd.“SKF’s new unit in Haridwar (to manufacture ball bearings with•an investment of Rs150 crore),” 10 May 2009, Indian Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Sumitomo to Build Steel Processing Center In India,” 2 May•2009, Nikkei Report, via Dow Jones Factiva, © 2009. Nihon Keizai Shimbun, Inc.“Update: T ata Motors Invests INR10 Bln In New Truck Range,”•28 May 2009, Dow Jones International News, via Dow Jones Factiva, © 2009 Dow Jones & Company, Inc.“T ata Motors to set up truck unit in Myanmar (with the support•of the Government of India),” 31 May 2009, Indian Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.Nandini Sen Gupta, “T ata Motors readies 8,000-crore capex,”•14 August 2009, The Economic Times, via Dow Jones Factiva, © 2009 The Times of India Group.“T oyota Kirloskar to invest INR8bn in Bangalore,” 26 June•2009, Auto Business News, via Dow Jones Factiva, © 2009 Electronic News Publishing.“Vibgyor Group to invest Rs800 crore in new ventures,” 10 July•2009, Indian Business Insight, via Dow Jones Factiva, © 2009 Informatics (India) Ltd.“Volkswagen’s Pune plant gets Rs 920 crore from IFC,” 7•August 2009, Indian Express, via Dow Jones Factiva, © Indian Express Pty. Ltd。