8投资学第八章习题答案

金德环《投资学》课后习题答案

金德环《投资学》课后习题答案习题答案第一章习题答案第二章习题答案练习题1:答案:(1),公司股票的预期收益率与标准差为:Er,,,,,,,0.570.350.2206,,,,,,,,A1/2222,, ,0.5760.3560.22068.72,,,,,,,,,,,,,,A,,(2),公司和,公司股票的收益之间的协方差为:Covrr,0.5762510.50.3561010.5,,,,,,,,,,,,,,,,,AB ,,,,,,0.22062510.590.5,,,,(3),公司和,公司股票的收益之间的相关系数为:Covrr,,,,90.5AB ,,,,,0.55AB,8.7218.90,,AB练习题2:答案:如果,,,的投资投资于,公司,余下,,,投资于,公司的股票,这样得出的资产组合的概率分布如下:钢生产正常年份钢生产异常年份股市为牛市股市为熊市概率 0.5 0.3 0.2 资产组合收益率(,) ,, ,., -2.5 得出资产组合均值和标准差为:Er=0.516+0.32.5+0.2-2.5=8.25,,,,,,,,,,组合1/22222,, ,=0.516-8.25+0.32.5-8.25+0.2-2.5-8.25+0.2-2.5-8.25=7.94,,,,,,,,组合,,1/22222,=0.518.9+0.58.72+20.50.5-90.5=7.94,,,,,,,,,,,,,,,组合,,练习题3:答案:尽管黄金投资独立看来似有股市控制,黄金仍然可以在一个分散化的资产组合中起作用。

因为黄金与股市收益的相关性很小,股票投资者可以通过将其部分资金投资于黄金来分散其资产组合的风险。

练习题4:答案:通过计算两个项目的变异系数来进行比较:0.075 CV==1.88A0.040.09 CV==0.9B0.1考虑到相对离散程度,投资项目B更有利。

练习题5:答案:R(1)回归方程解释能力到底如何的一种测度方法式看的总方差中可被方程解释的方差所it2,占的比例。

投资学习题解答

精选2021版课件

28

第六章 投资风险与投资组合

1.假定某资产组合中包含A、B、C三种 股票,股份数分别为150、200、50,每 股初始市场价分别为20元、15元和30元, 若每股期末的期望值分别为30元、25元 和40元,计算该资产组合的期望收益率。

精选2021版课件

29

第六章 投资风险与投资组合

解:

(1)预期现金流为 0.5×70000+0.5×200000=135000美元。 风险溢价为8%,无风险利率为6%,要求的

回报率为14%。 因此,资产组合的现值为: 135000/1.14=118421美元

精选2021版课件

36

第六章 投资风险与投资组合

(2) 如果资产组合以118421美元买入,给 定预期的收入为135000美元,而预期的收 益率E(r)推导如下:

假定某种无风险资产收益率为6其中风险资产的收益率为9该风险资产收益率的方差为20如果将这两种资产加以组合请计算该资产组合的风险价48第七章证券市场的均衡与价格决定49第七章证券市场的均衡与价格决定3

第四章 证券市场及期运行

1.某钢铁股份有限公司股票的价格信息 为:买方报价16元,卖方报价17元。

某投资者已作出17元限价买入指令。分析该 指令的含义并判断该指令是否会被执行。

12/1.06+112/(1.08472*1.08472)=106.51 由n=2, FV=100, PV=106.51, PMT=12, 则有:

TM=8.333% (2)f2 =[(1+s2) (1+s2)/(1+s1)]-1 =(1.08472*1.08472/1.06)-1=0.11=11%

(2)第二年的远期利率是多少?

国家开放大学《投资学》章节测试题参考答案

国家开放大学《投资学》章节测试题参考答案第一章导论一、单项选择题。

1.投资和投机的本质区别表现在()。

A. 交易动机B. 交易对象C. 交易时间D. 交易方式2.狭义的投资是指()。

A. 实物投资B. 证券投资C. 风险投资D. 创业投资3.投资风险与收益之间呈()。

A. 同比例变化B. 不确定性C. 反方向变化D. 同方向变化4.区分直接投资和间接投资的基本标志是在于()。

A. 投资者是否拥有控制权B. 投资者的投资渠道C. 投资者的投资方式D. 投资者的资本数量二、多项选择题。

5.一项投资活动至少要包括以下()方面。

A. 投资客体B. 投资主体C. 投资目的D. 投资渠道E. 投资主体6.投资的特征有()。

A. 经济性B. 时间性C. 风险性D. 收益性E. 安全性7.实物投资的特点有()。

A. 投资回收期较长B. 与生产过程紧密联系C. 流动性较差D. 与经营过程紧密联系E. 投资变现速度较慢8.金融投资包含以下()投资形式。

A. 外汇B. 汇票C. 股指期货D. 彩票E. 存款第二章投资的经济关系一、单项选择题。

1.总产出通常用()来衡量。

A. 国家生产总值B. 物价指数C. 国民生产总值D. 国内生产总值2.假设新增投资为100,边际消费倾向为0.8,那么由此新增投资带来的收入的增量为()。

A. 80B. 675C. 125D. 5003.用来衡量通货膨胀的程度的指标是()。

A. 城市居民消费价格指数B. 工业品出产价格指数C. 固定资产投资价格指数D. 消费价格指数二、多项选择题。

4.投资的供给效应对经济增长的作用表现为()。

A. 重置投资B. 乘数效应C. 加速效应D. 净投资5.经济周期通常可以分为()阶段。

A. 平静B. 扩张C. 爆发D. 衰退6.失业可以分为()。

A. 自愿失业B. 隐蔽性失业C. 非自愿失业D. 显性失业第三章项目投资估值理论一、单项选择题。

1.单利计算法忽略了()的时间价值。

威廉夏普 投资学课后习题答案解析第八章

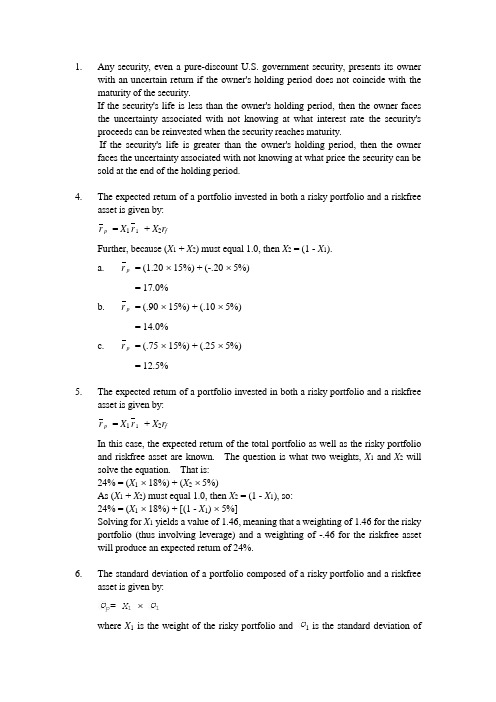

1. Any security, even a pure-discount U.S. government security, presents its ownerwith an uncertain return if the owner's holding period does not coincide with the maturity of the security.If the security's life is less than the owner's holding period, then the owner faces the uncertainty associated with not knowing at what interest rate the security's proceeds can be reinvested when the security reaches maturity.If the security's life is greater than the owner's holding period, then the owner faces the uncertainty associated with not knowing at what price the security can be sold at the end of the holding period.4. The expected return of a portfolio invested in both a risky portfolio and a riskfreeasset is given by:= X1r1+ X2r fpFurther, because (X1 + X2) must equal 1.0, then X2 = (1 - X1).a. r p = (1.20 ⨯ 15%) + (-.20 ⨯ 5%)= 17.0%b. r p = (.90 ⨯ 15%) + (.10 ⨯ 5%)= 14.0%c. r p = (.75 ⨯ 15%) + (.25 ⨯ 5%)= 12.5%5. The expected return of a portfolio invested in both a risky portfolio and a riskfreeasset is given by:= X1r1+ X2r fpIn this case, the expected return of the total portfolio as well as the risky portfolio and riskfree asset are known. The question is what two weights, X1 and X2 will solve the equation. That is:24% = (X1⨯ 18%) + (X2⨯ 5%)As (X1 + X2) must equal 1.0, then X2 = (1 - X1), so:24% = (X1⨯ 18%) + [(1 - X1) ⨯ 5%]Solving for X1 yields a value of 1.46, meaning that a weighting of 1.46 for the risky portfolio (thus involving leverage) and a weighting of -.46 for the riskfree asset will produce an expected return of 24%.6. The standard deviation of a portfolio composed of a risky portfolio and a riskfreeasset is given by:=X1⨯1pwhere X1 is the weight of the risky portfolio and 1 is the standard deviation ofthe risky portfolio. As X1 = (1 - weight of the riskfree asset), then:a. X1 = 1 - (-.30) = 1.30, thus:= 1.30 ⨯ 20%p= 26.0%b. X1 = 1 - .10 = .90, thus:= .90 ⨯ 20%p= 18.0%c. X1 = 1 - .30 = .70, thus:= .70 ⨯ 20%= 14.0%p7. The standard deviation of a portfolio invested in a risky portfolio and a riskfreeasset is given by:= X1⨯1pAs the standard deviation of Oyster's total portfolio is 20%, solving for the proportion invested in the risky portfolio (X1) gives:20% = X1⨯ 25%X1= .80The expected return of a portfolio invested in both a risky portfolio (with proportion X1) and a riskfree asset with proportion X2 or (1 - X1) is:r p = (.80 ⨯ 12%) + [(1 - .80) ⨯ 7%]= 11.0%8. Both Hick and Patsy are correct. Borrowing at the riskfree rate to invest more thanone's initial wealth in a risky portfolio is equivalent to purchasing the risky portfolio on margin. Further, borrowing at the riskfree rate is equivalent to takinga short position in the riskfree asset and investing the proceeds of the short sale inthe risky portfolio.9. The efficient set becomes all the portfolios that can be constructed through acombination of a single risky portfolio and lending or borrowing at the riskfree rate.The efficient set will therefore consist of all portfolios along a ray emanating from the riskfree asset, tangent to the curved Markowitz efficient set (that is, the efficient set without riskfree borrowing or lending), and continuing on out into risk-return space. The tangency point represents the optimal combination of risky assets for the investor.10. Riskfree borrowing and lending permits the investor to create any combination ofportfolios allocated between a risky portfolio (contained in the feasible set of risky portfolios) and the riskfree asset. These combinations lie on rays emanating from the riskfree asset. The more a ray is tilted to the northwest, the more desirable is the associated set of portfolios to the investor.Because the feasible set of risky portfolios is concave, the ray combining the riskfree asset and a risky portfolio, tilted as far as possible to the northwest, mustbe tangent to the feasible set of risky portfolios at only one point. This ray is the efficient set under riskfree borrowing and lending. All other portfolios in the feasible set of risky portfolios (including the "old"efficient set) will lie to the south and/or east of this "new" efficient set and, therefore, are dominated by the portfolios of the new efficient set. That is, these other portfolios offer less expected return and/or more risk than the portfolios lying on the efficient set generated under riskfree borrowing and lending.12. The feasible set now becomes the area between two rays, each emanating from theriskfree asset. The ray to the northwest is the efficient set. The ray to the southeast will connect the riskfree asset and generally the lowest expected return asset. Any combination of risk and return between these two rays can be created by appropriately combining a risky portfolio with riskfree borrowing or lending.13. The efficient set will be the same for both investors because it representsinvestment opportunities, not preferences. (Of course, the two investors may have different expectations regarding available expected returns and risks.)The more risk-averse investor's indifference curves will be more steeply slopedthan the indifference curves of the less risk-averse investor.The optimal portfolio of the more risk-averse investor will lie to the southwest ofthe less risk-averse investor's optimal portfolio. Both optimal portfolios, of course, will lie on the efficient set. The more risk-averse investor's optimal portfolio likely will lie to the southwest of the tangency portfolio, implying lending at the riskfree rate. Conversely, the less risk-averse investor's optimal portfolio likely will lie to the northeast of the tangency portfolio, implying borrowing at the riskfree rate.14. a. The riskfree asset has a zero variance and has zero covariance with otherassets. Thus, examining the variance-covariance matrix, the third security must be the riskfree asset.b. r p = (X 1 ⨯ r 1) + (X 2 ⨯ r 2)= (.50 ⨯ 10.1%) + (.50 ⨯ 7.8%)= 9.0%σσp i n i j ij j n X X =⎡⎣⎢⎤⎦⎥==∑∑1112/= (X 1X 1 11 +X 2X 2 22 + 2X 1X 2 12)½= {[(.50)² ⨯ 210] + [(.50)² ⨯ 90]+ (2) ⨯ (.50) ⨯ (.50) ⨯ (60)}½= [52.5 + 22.5 + 30]½ = [105]½ = 10.2% c. r tp = (.75 ⨯ r p ) + (.25 ⨯ r 3) = (.75 ⨯ 9.0%) + (.25 ⨯ 5.0%)= 8.0%= .75 ⨯p= .75 ⨯ 10.2%tp= 7.7%15. The efficient set would be composed of the southwest portion of the curvedMarkowitz efficient set (that is, the efficient set without riskfree borrowing or lending) up to the tangency portfolio (when both riskfree borrowing and lending are permitted), where it would then become a ray emanating from the tangency portfolio and extending out into risk-return space. If this ray were extended to the southwest, it would intersect the return axis at the riskfree rate.16. The effect is to increase both expected return and risk.The investor is leveraging his or her invested position. Since the optimal risky portfolio has a higher expected return than the riskfree asset, the expected return on the leveraged risky portfolio is higher than that of the unleveraged portfolio.However, because the risky portfolio's return is variable, the leveraged risky portfolio's return is more variable and hence more risky than the return on the unleveraged risky portfolio.17. Your optimal risky portfolio would not change (assuming the feasible investmentopportunities did not change). It would remain the only risky portfolio lying on the efficient set. However, your allocations to the riskfree asset and the risky portfolio would change as your risk preferences changed. As you became less risk averse, you would decrease (increase) your riskfree lending (borrowing) and move to the northeast along the efficient set.18. The efficient set becomes divided into three segments. The first segment is astraight line between the lending rate on the return axis and tangent to the curved Markowitz efficient set (that is, the efficient set without riskfree borrowing or lending). The second segment lies to the northeast of the first. It is a straight line tangent to the curved Markowitz efficient set, extending northeast into risk-return space. While this line does not extend to the return axis, if it did it would intersect the axis at the borrowing rate. The third segment lies between the first two. It is the portion of the curved Markowitz efficient set that lies between the two tangency portfolios.。

《投资学》课后习题参考答案

习题参考答案第2章答案:一、选择1、D2、C二、填空1、公众投资者、工商企业投资者、政府2、中国人民保险公司;中国国际信托投资公司3、威尼斯、英格兰4、信用合作社、合作银行;农村信用合作社、城市信用合作社;5、安全性、流动性、效益性三、名词解释:财务公司又称金融公司,是一种经营部分银行业务的非银行金融机构。

其最初是为产业集团内部各分公司筹资,便利集团内部资金融通,但现在经营领域不断扩大,种类不断增加,有的专门经营抵押放款业务,有的专门经营耐用消费品的租购和分期付款业务,大的财务公司还兼营外汇、联合贷款、包销证券、不动产抵押、财务及投资咨询服务等。

信托公司是指以代人理财为主要经营内容、以委托人身份经营现代信托业务的金融机构。

信托公司的业务一般包括货币信托(信托贷款、信托存款、养老金信托、有价证券投资信托等)和非货币信托(债权信托、不动产信托、动产信托等)两大类。

保险公司是一类经营保险业务的金融中介机构。

它以集合多数单位或个人的风险为前提,用其概率计算分摊金,以保险费的形式聚集资金建立保险基金,用于补偿因自然灾害或以外事故造成的经济损失,或对个人因死亡伤残给予物质补偿。

四、简答1、家庭个人是金融市场上的主要资金供应者,其呈现出的主要特点如下:(1)投资目标简单;(2)投资活动更具盲目性(3)投资规模较小,投资方向分散,投资形式灵活。

企业作为非金融投资机构,其行为呈现出了以下的显著特点:(1)资金需求者地位突现;(2)投资目标的多元化;(3)投资比较稳定;(4)短期投资交易量大。

2、商业银行在经济运行中主要的职能如下:(1)信用中介职能;(2)支付中介职能;(3)调节媒介职能;(4)金融服务职能;(5)信用创造职能;总的来说,商业银行业务可以归为以下三类:(1)负债业务:是指资金来源的业务;(2)资产业务:是商业银行运用资金的业务;(3)中间业务和表外业务:中间业务指银行不需要运用自己的资金而代客户承办支付和其他委托事项,并据以收取手续费的业务第3章答案:一、选择题1、D2、D3、B二、填空题1、会员制证券交易所和公司制证券交易所、会员制、公司制。

投资学教程(上财版)第8章习题集

《投资学》第8章习题集一、判断题1、债券的发行期限是债券发行时就确定的债券还本期限。

()2、一组信用质量相同、但期限不同的债券的到期收益率和剩余期限的关系用图形描画出来的曲线,就是收益率曲线。

()3、隆起收益率曲线的含义是:随着债券剩余期限长度的减少,债券到期收益率先上升后降低。

()4、利率期限结构研究的是其他因素相同、期限不同债券的收益率和到期期限之间的关系()5、附息债券的价值就等于剥离后的若干个零息债券的价值之和。

()6、无偏预期理论认为,远期利率是人们对未来到期收益率的普遍预期。

()7、在流动性偏好理论下,长期利率一般都比短期利率高。

()8、市场分割理论认为,投资者一般都会比较固定地投资于*个期限的债券,这就形成了以期限为划分标识的细分市场。

()9、简单的说,久期是债券还本的加权平均年限。

()10、附息债券的久期等于其剩余期限。

()11、修正久期可以反映债券价格对收益率变动的敏感程度。

()12、其他条件不变时,债券的到期日越远,久期也随之增加,但增加的幅度会递减。

()13、其他条件不变,到期收益率越高,久期越长。

()14、随着收益率变动幅度的增加,用久期来测算债券价格变化的精确度在减小。

()15、一般而言,债券价格与利率的关系并不是线性的。

()16、凸性系数是债券价格对收益率的一阶导数除以2倍的债券价格。

()17、久期与债券价格相对于收益率的一阶导相关,因此称为一阶利率风险。

()18、当收益率(利率)变动较小时,债券价格的变动近似线性,只需要考虑凸性。

()19、债券组合管理大致可以分为两类:消极的债券组合管理和积极的债券组合管理。

()20、有效债券市场是指债券的当前价格能够充分反映所有有关的、可得信息的债券市场。

()21、如果债券市场是有效的,投资者将找不到价格被错估的债券,也不必去预测市场利率的变化。

()22、常见的消极的债券组合管理包括:免疫组合和指数化投资。

()23、市场利率变动对债券投资收益的影响包括:影响债券的市场价格,影响债券利息的再投资收益。

投资学习题习题及答案

第一章投资环境1.假设你发现一只装有100亿美元的宝箱。

a.这是实物资产还是金融资产?b.社会财富会因此而增加吗?c.你会更富有吗?d.你能解释你回答b、c时的矛盾吗?有没有人因为这个发现而受损呢?a. 现金是金融资产,因为它是政府的债务。

b. 不对。

现金并不能直接增加经济的生产能力。

c. 是。

你可以比以前买入更多的产品和服务。

d. 如果经济已经是按其最大能力运行了,现在你要用这1 0 0亿美元使购买力有一额外增加,则你所增加的购买商品的能力必须以其他人购买力的下降为代价,因此,经济中其他人会因为你的发现而受损。

nni Products 是一家新兴的计算机软件开发公司,它现有计算机设备价值30000美元,以及由Lanni的所有者提供的20000美元现金。

在下面地交易中,指明交易涉及的实物资产或(和)金融资产。

在交易过程中有金融资产的产生或损失吗?nni公司向银行贷款。

它共获得50000美元的现金,并且签发了一张票据保证3年内还款。

nni公司使用这笔现金和它自有的20000美元为其一新的财务计划软件开发提供融资。

nni公司将此软件产品卖给微软公司(Microsoft),微软以它的品牌供应给公众,Lanni公司获得微软的股票1500股作为报酬。

nni公司以每股80元的价格卖出微软的股票,并用所获部分资金还贷款。

a. 银行贷款是L a n n i公司的金融债务;相反的,L a n n i的借据是银行的金融资产。

L a n n i获得的现金是金融资产,新产生的金融资产是Lanni 公司签发的票据(即公司对银行的借据)。

b. L a n n i公司将其金融资产(现金)转拨给其软件开发商,作为回报,它将获得一项真实资产,即软件成品。

没有任何金融资产产生或消失;现金只不过是简单地从一方转移给了另一方。

c. L a n n i公司将其真实资产(软件)提供给微软公司以获得一项金融资产—微软的股票。

由于微软公司是通过发行新股来向L a n n i支付的,这就意味着新的金融资产的产生。

投资学8~9章课后习题

投资学课后作业 第八章 指数模型3. 其他条件保持不变,公司特定风险越大,积极组合所占的比重越小,投资者会偏向于投资指数组合。

4.因为我们已经用市场指数表示了市场收益溢价,剩下的当然是非市场收益溢价。

当市场收益溢价为0时,α所表示的就是非市场收益溢价。

对于积极投资者而言,找到非零的α,代表夏普比率会相对其他投资组合更大,即相同的风险,收益会更高,所以积极型投资者更容易被α值大的股票吸引。

其他条件保持不变,α变大,夏普比率变大。

5.a.估计60个期望值、60个方差、C 602=1770个协方差b.单指数模型公式R i =αi +βi ∗R M +e i σ2=βi 2σM 2+σ2(e i ) 需要估计60个期望值、60个βi 、60个σ2(e i )、1个βi 2σM 2、1个R M6.a. σi2=βi 2σM 2+σ2(e i ),带入数值,解得σA=34.78%,σB=47.93%b.E r p =0.3∗E r A +0.45∗E r B +0.25∗r f ,代入数值,得E r p =14% β=0.3∗βA +0.45∗βB+0.25∗βf ,带入数值,得β=0.78σ2=βi 2σM2+σ2 e ,其中,βi 2σM2=0.782∗0.222=0.0294,σ2 e =0.32∗σ2 e A +0.452∗σ2 e B ,带入数值,得σ2 e =0.0405, σ2=0.0699,σ=26.44%7.从图中我们可以看到A 的回归线比较平缓,散点离回归线比较远,说明A 的特定风险大;B 的回归线比较陡峭,说明B 的系统风险大,散点比较接近回归线,模拟的比较好,。

a. A 的特定风险大b. B 的系统风险大c. Bd. Ae. B 8. a. A b. A c. A d.-0.2% 9. σi2=βi 2σM2+σ2e i =βi 2σM2R2, 带入数值,得σA =31.3%,σB=69.28%10. βA 2σM2=0.72∗0.22=1.96%,σ2 e A =9.797%−1.96%=7.837%,同理,得βB 2σM2=5.76% σ2 e B =4.22%11.Cov R A ,R B =βA βB σM2, 代入数值,得Cov R A ,R B =3.36%,ρ=Cov R A,R B,带入数值,得ρ=0.155σAσB12. Cov R A,R M=βAβMσM2, 代入数值,得Cov R A,R M=2.8%,同理,得Cov R M,R B=4.8%13.组合P的方差σp2=0.62∗σA2+0.42∗σB2+0.6∗0.4∗σAσB,带入数值,得σp2=0.1282 σP=35.8%βP=0.6∗0.7+0.4∗1.2=0.9, βP2σM2=3.24%,σ2e P=9.58%, Cov R P,R M=0.3614.基本思想与13题一样,这里就不再列出式子而直接写答案了:标准差为21.55%,与市场的协方差为0.3,非系统风险2.40%,系统风险19.15%16.αA=0.11−0.06−0.8∗0.12−0.06=0.02αB=0.14−0.06−1.5∗0.12−0.06=−0.01,通过比较,我会选择α大的股票17.a.b.α=-(0.61*1.6%+1.13*4.4%+1.69*3.4%+1.7*4.0%)=-16.9% β=2.08最优组合是指数组合的权重为1.047c.夏普比率为0.3662,积极组合的贡献为0.0184d.投资于短期国债的比例为0.5685,投资于股票组合的比例为(1-0.5685)第九章 资本资产定价模型8. 贴现率i=r f +β(r M −r f ),带入数值,得i=22.4% NPV= (CI −CO )t (1+i)t100,带入数值,得NPV=18.09美元,当NPV<=0时,i<=0.3573, 则β最大为3.47 9.a.各为2和0.3b.期望收益率各为18%和9%c.整体经济的证券市场线的斜率为1,纵坐标截距为6%d.每只股票的截距分别为-0.06和0.003e.8.7%10.不可能,因为A 的β比B 的要大,但是A 的收益却比B 的要小,这样的组合是无效的。

投资学课后习题及答案

投资学课后习题及答案投资学课后习题及答案投资学练习导论习题1证券投资是指投资者购买_______、________、________等有价证券以及这些有价证券的_______以获取________、_________及________的投资行为和投资过程,是直接投资的重要形式。

(填空)2 ____是投资者为实现投资目标所遵循的基本方针和基本准则。

(单选) A证券投资政策 B证券投资分析 C证券投组合 D评估证券投资组合的业绩3 一般来说,证券投资与投机的区别主要可以从________等不同角度进行分析。

(多选) A 动机 B对证券所作的分析方法 C投资期限 D投资对象E风险倾向4在证券市场中,难免出现投机行为,有投资就必然有投机。

适度的投机有利于证券市场发展(判断)第一至第四章习题1在股份有限公司利润增长时,参与优先股股东除了按固定股息率取得股息外,还可以分得___________。

(填空)2 累积优先股是一种常见的、发行很广泛的优先股股票。

其特点是股息率______,而且可以 ________计算。

(填空)3________不是优先股的特征之一。

(单选)A约定股息率 B股票可由公司赎回 C具有表决权 D优先分派股息和清偿剩余资产。

4 股份有限公司最初发行的大多是_____,通过这类股票所筹集的资金通常是股份有限公司股本的基础。

(单选) A特别股 B优先股 CB股 D普通股5 当公司前景和股市行情看好、盈利增加时,可转换优先股股东的最佳策略是_______ 。

(单选)A转换成参与优先股 B转换成公司债券 C转换成普通股 D转换成累积优先股6 下列外资股中,不属于境外上市外资股的是________。

(单选)A H股 BN股 CB股 DS股7 股份制就是以股份公司为核心,以股票发行为基础,以股票交易为依托。

(判断) 8 可赎回优先股是指允许拥有该股票的股东在一个合理的价格范围内将资金赎回。

(判断) 9________是指在管理层和股东之间发生冲突的可能性,它是由管理层在利益回报方面的控制以及管理人员的低效业绩所产生的问题。

投资学课后练习答案(贺显南版)

投资学练习答案导论2.A3.ABCDE4.正确第一至第四章习题1.公司剩余盈利2.固定、累积3.C4.D5.C6.C7.正确8.错误9.A 11.C 12.C 13.D14.AD 15.B 16A 17.B 18.D 20.C 21.B22.A 23.D 24.B 26.A 29.C 30.C 31.A32.C 33.错误 34.正确 35.正确 36.错误 37.C38.A 39.B 40.B第五章习题1.D2.AC3.AB4.BCD5.正确6.正确7.ABCD8.正确9.E 10.D 11.B 12.E13.D 14.C 17.C第六章练习8.D 10.B 12.B 13.A 14.C第七章练习1.B2.C3.C4.C5.D 8.C 9.B12.B 13.D 14.C 15.B 17.E 18.B 19.B 22.C 23.B 24.B 25E26.A 27.B 28.A 33错误 34.A 35.A第八章练习2.B3.A4.B5.D6.D7.C8.A9.B12.C 13.C 14.D 16.C 17.C 18.D19.B 23.B 25.D 27.C投资学第九章习题答案1.不做2.不做3.C4.不做5.不做6.3%7.不做8.B9. C 10.D 11. D 12.C 13.D 14.C 15.A 16.C 17.(答案为0.75) 18.D 19.C 20.B21.不做投资学第十章至第十一章习题答案1.相关系数为02. B3. B4. C5.错6.错7. B8. E9. A10.对11.D投资学第十二章至第十三章习题答案1.不做2.高于票面值因为10%大于8%3.具体看课本公式(老师只是讲公式没有给出确切得答案)4.贴现贴现率5.反方向6.C7.C8.对9.对10.不做11.折价平价溢价12.不做13.不做14.不做15.A16.C17.C18.具体看书本323页19.具体看课本325页20.看课本319至32021.不做22.不做第十四章至十五章习题答案1.先行同步滞后2.不做3.开拓拓展成熟衰落4.资产负责表损益表现金流量表5. C6.宏观分析行业分析公司分析7. A8. B9. A10.D11.D12.A13.A14.对15.对十七章注意事项: 注意技术分析得三大假设假设1. 市场行为涵盖一切信息假设2.价格沿趋势运动假设3.历史会重演。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1. 收入资本化法,又称股息贴现模型,通过将未来各期的收入贴现到当前价值,然后加总,

得到普通股的内在价值。

2. 买卖股票的资本利得对股票的内在价值没有影响。

因为资本利得是不同投资者之间利益

的转移,而转移的原因就是股票内在价值发生了变化。

3. 利用股息贴现模型进行投资分析有两个途径:一是NPV 法,选取合适的贴现率,求出

股票的净现值,若NPV 大于零,该股票有投资价值;若NPV 小于零,该股票没有投资价值。

二是IRR 法,求出一个特殊的贴现率使得NPV 等于零,该贴现率就是内部收益率,若内部收益率大于该股票风险水平相对应的贴现率,则该股票具有投资价值;反之亦然。

4. 见P235 前三句。

5. 区别:三阶段模型有两个平稳期,一个渐变期;H 模型有一个渐变期,一个平稳期。

三

阶段模型的现金流贴现计算比较复杂;H 模型有一个简单的公式就可以计算出股票的现值,以及计算内部收益率。

联系:H 模型是在三阶段增长模型的基础上提出的,是对三阶段模型的简化处理

6. 见P243 第一、二两段

7. 见P245 最后两段

8. 见P244-245 (1)(1)g ROE b PM ATO L b =×−=×××−

9. 市盈率与市场组合收益率,贝塔系数,贴现率是负相关的;与股息增长率,股东权益收

益率,总资产收益率,税后净利润率和总资产周转率是正相关的;与无风险资产收益率,派息率和杠杆比率的关系不确定。

详情请看 P246的图标。

10. 两个模型的判断原则,都是计算一个理论值,与实际值进行比较;区别在于股息贴现模

型侧重于长期的评价;而市盈率模型更侧重于短期的评价。