IAS 16 国际会计准则16号 固定资产PPE

关于企业会计准则第16号——固定资产的会计处理

关于企业会计准则第16号——固定资产的会计处理企业会计准则第16号(以下简称“准则16号”)是关于固定资产的会计处理的规定。

在企业会计中,固定资产是指企业持有并用于生产经营活动的长期有形资产。

准则16号对固定资产的计量、确认、评估和报告进行了详细的规定,下面将从准则16号的重要内容和会计处理的流程等方面进行阐述。

准则16号规定了固定资产的计量原则。

在购置固定资产时,企业应按实际购买价格计量,并包括直接相关的购置成本。

准则16号还额外规定了一些特殊情况下的计量方法,如自建固定资产、交换固定资产和政府补助等。

准则16号规定了固定资产的确认原则。

企业应当将满足以下条件的固定资产确认为资产:(1)对于购置的固定资产,其成本可以可靠地计量,并且能够带来未来经济利益;(2)购置的固定资产已经属于企业,并且能够控制其使用;(3)相关的经济利益有可能流入企业。

当固定资产不符合上述条件时,则不应确认为资产。

准则16号规定了固定资产的评估原则。

固定资产应当按照成本模式或公允价值模式进行评估。

在成本模式下,固定资产应当以其历史成本减去累计折旧计量。

在公允价值模式下,固定资产应当以其公允价值计量,且公允价值变动计入当期损益。

企业可以根据实际情况选择对固定资产采用成本模式或公允价值模式进行评估,但需在财务报表中明确披露采用的评估模式。

准则16号规定了固定资产的报告要求。

企业应当在财务报表中明确分列固定资产的种类和金额,并披露固定资产的重要政策、计量基准和折旧方法等信息。

对于可能对固定资产价值产生重大影响的情况,如重大修理、变卖、报废等,企业应当及时披露相关的信息。

在会计处理中,企业应按照准则16号的规定进行固定资产的计量、确认、评估和报告。

具体步骤可以概括为:首先,企业应记录固定资产的购置成本,包括直接相关的费用。

其次,企业应根据准则16号的规定,将固定资产确认为资产,或者在不满足确认条件时,不予确认。

然后,企业应根据所采用的评估模式,计量固定资产的历史成本、累计折旧或公允价值。

国际会计资料准则第16号之不动产厂房和设备

国际会计资料准则第16号之不动产厂房和设备国际会计准则第16号(IAS16)是国际会计准则理事会(IASB)规定的关于不动产、厂房和设备的会计准则。

该准则规定了企业应如何计量、报告和披露不动产、厂房和设备的相关信息,以确保相关资产能够准确地反映在企业的财务报表中。

IAS16要求企业对不动产、厂房和设备进行初始计量,即以成本减去累积折旧和累积减值损失的金额进行计量。

这些成本包括购买资产的价格、直接相关的成本(如安装费用和物流费用)以及与资产可投入使用状态相关的贷款利息。

有时,如果资产是以非货币支付的方式获得的,准则还规定了如何计算这些成本。

IAS16还规定了企业应如何对不动产、厂房和设备进行折旧和减值测试。

折旧是指企业应该根据资产的预计使用寿命和估计的残余价值,在资产的预计使用寿命内按适当的方法计算每年的减值金额。

减值测试是指企业应当周期性地评估资产的可回收金额是否低于其账面价值,如果是,则需要计提减值损失。

当不动产、厂房和设备出售或报废时,企业需要将其摊销或净额列示在财务报表中相应的资产和负债科目中,并将其带来的收益或亏损计入利润表中。

同时,IAS16还规定了对于租赁资产的计量和披露要求。

在财务报表披露方面,IAS16要求企业应提供对不动产、厂房和设备的披露信息,包括资产的计量基础、主要假设和估计、资产的使用寿命和残余价值、折旧方法、资产的净残值额、资产的累积折旧额以及减值损失的计提等。

总而言之,IAS16为企业提供了对不动产、厂房和设备的计量、报告和披露的一系列准则,以确保企业能够适当地处理这些重要的资产,使其财务报表能够准确地反映企业的财务状况和业绩。

这有助于提高企业的透明度和可比性,使投资者和利益相关方能够更好地理解和评估企业的价值。

国际会计准则第16号之不动产厂房和设备

国际会计准则第16号之不动产厂房和设备国际会计准则第16号(IAS16)是一个被国际会计准则理事会(IASB)制定的会计准则,规定了如何会计处理与不动产、厂房和设备相关的事项。

该准则的核心目标是确保企业以一种准确、一致和可比较的方式报告和披露这些资产,以便用户能够做出有关企业财务状况和绩效的明智决策。

根据IAS16,不动产、厂房和设备是具有以下特征的有形资产:具有实体形态,用于生产货物、出租给他人或供企业经营,使用寿命超过一年。

该准则要求企业在其财务报表中对这些资产进行准确的计量和分类。

首先,根据IAS16,不动产、厂房和设备应该以其成本计量。

成本包括购买时支付的现金、现金等价物、或者在购买时发生的权益性交换的公平价值。

成本还应包括与获取和将资产准备为其预期用途相关的直接和间接费用,如安装、运输和测试费用。

其次,一旦资产被准备好以供使用,企业应将其按照成本模型或再评估模型进行会计处理。

在成本模型下,资产的会计价值为其成本减去已计提的累计折旧和累计减值损失。

在再评估模型下,资产的会计价值可以根据其公平价值重新确定,并将其反映在财务报表中。

另外,IAS16还规定了资产的折旧会计处理方法。

资产的折旧是指其使用寿命内的价值递减过程。

企业应采用合适的方法将该递减过程在其预期使用寿命中进行分配,以便反映准确的资产价值。

常用的折旧方法包括直线法、减值余价法或双倍余价法。

企业应根据其自身情况选择适当的折旧方法,并在财务报表中披露。

此外,当资产发生损值时,IAS16要求企业进行减值测试,并在需要时对其进行减值计提。

资产的减值损失是指其账面价值超过其可收回金额的差额。

企业应根据相关准则进行减值测试,例如比较资产的账面价值和预计的现金流量,以确定是否需要计提减值损失。

最后,IAS16还要求企业在财务报表中对不动产、厂房和设备相关的信息进行充分披露。

披露内容包括但不限于其会计政策、会计余额、折旧方法、减值测试方法等。

这些披露可以帮助用户更好地理解和评估企业对这些资产的处理和管理情况。

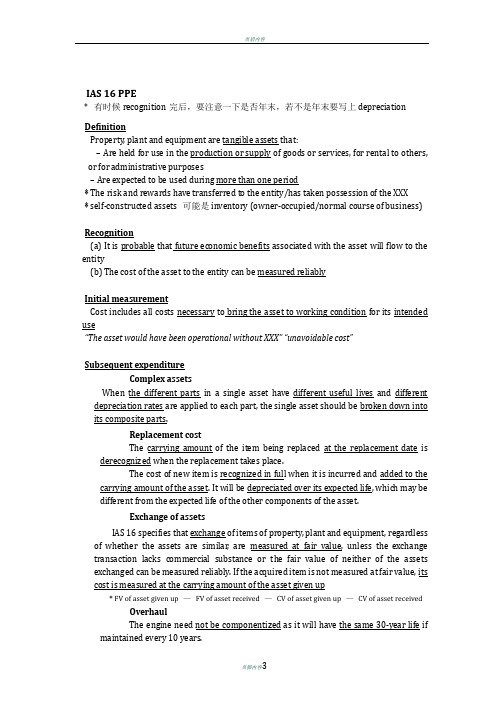

ACCA SBR IAS 16 PPE 笔记

IAS 16 PPE* 有时候recognition完后,要注意一下是否年末,若不是年末要写上depreciationDefinitionProperty, plant and equipment are tangible assets that:– Are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes– Are expected to be used during more than one period* The risk and rewards have transferred to the entity/has taken possession of the XXX* self-constructed assets 可能是inventory (owner-occupied/normal course of business)Recognition(a) It is probable that future economic benefits associated with the asset will flow to the entity(b) The cost of the asset to the entity can be measured reliablyInitial measurementCost includes all costs necessary to bring the asset to working condition for its intended use“The asset would have been operational without XXX” “unavoidable cost”Subsequent expenditureComplex assetsWhen the different parts in a single asset have different useful lives and different depreciation rates are applied to each part, the single asset should be broken down into its composite parts.Replacement costThe carrying amount of the item being replaced at the replacement date is derecognized when the replacement takes place.The cost of new item is recognized in full when it is incurred and added to the carrying amount of the asset. It will be depreciated over its expected life, which may be different from the expected life of the other components of the asset.Exchange of assetsIAS 16 specifies that exchange of items of property, plant and equipment, regardless of whether the assets are similar, are measured at fair value, unless the exchange transaction lacks commercial substance or the fair value of neither of the assets exchanged can be measured reliably. If the acquired item is not measured at fair value, its cost is measured at the carrying amount of the asset given up* FV of asset given up —FV of asset received —CV of asset given up —CV of asset received OverhaulThe engine need not be componentized as it will have the same 30-year life if maintained every 10 years.Where an asset requires regular overhauls in order to continue to operate, the cost of the overhaul is treated as an additional component and depreciated over the period to the next overhaul.The cost should be capitalized when the overhaul is to be undertaken.Subsequent measurementCost modelThe asset is carried at cost less accumulated depreciation and impairment loss.Revaluation modelThe asset is carried at a revalued amount, being its fair value at the date of revaluation less subsequent depreciation and impairment loss.The revised IAS 16 makes clear that the revaluation model is available only if the fair value of the item can be measured reliably.Scopea)If an item is revalued, the entire class of assets to which that asset belongsshould be revalued.b)All the items within a class should be revalued at the same time, to preventselective revaluation and to avoid disclosing a mixture of costs and values from different dates in the financial statements.FrequencyThe frequency of valuation depends on the volatility of the fair values of individual items of property, plant and equipment. The more volatile the fair value, the more frequently revaluations should be carried out.Depreciation accountingDepreciable amounta)The depreciable amount of an item of property, plant and equipmentshould be allocated on a systematic basis over its useful life.b)The depreciation charge for each period should be recognized as anexpense unless it is included in the carrying amount of another asset.Depreciation methodReflect the pattern in which the asset’s economic benefits are consumedStraight lineReducing balance (最后一年是balance figure)The depreciation method should be reviewed at each financial year end and, if the pattern of consumption of benefits has changed, the depreciation method should be changed prospectively as a change in estimate under IAS 8.The change in depreciation method is a change in accounting estimate and the depreciation charge for the current and future periods should be adjusted.Residual valueResidual value is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.The residual value of an asset may increase to an amount equal to or greaterthan the asset’s carrying amount. If it does, the asset’s depreciation charge should be zero until its residual value subsequently decreases below the asset’s carrying amount.At least at each financial year endChanges are changes in accounting estimates and are accounted for prospectively as adjustments to future depreciation.Useful lifeAt least at each financial year endDepreciation charge for the current and future periods should be adjusted if expectations have changed significantly from previous estimates.Changes are changes in accounting estimates and are accounted for prospectively as adjustments to future depreciation.Factors are considered in determining the useful life of an asset:* 若要改变life,should be reasonable and supported by evidencea) Expected use of the assetb) Expected physical wear and tearc) Technical or commercial obsolescence arising from changes or improvements inproduction, or from market demand or the product or service output of the assetd) Legal or similar limits on the use of the asset, such as the expiry dates of relatedleasesBeginning and Cessation of depreciationBegin when it is available for useCease at the earlier date of the asset is classified as HFS and the date that the asset is derecognizedDepreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated. However, under usage methods of depreciation the depreciation charge can be zero while there is no productionOther:One asset has been replaced after only XX year earlier than expected. In this case, any remaining net book value of the old engine and overhaul cost should be expensed immediately.。

国际财务报告准则第16 号

《国际财务报告准则第16 号——租赁》新变化Note on 2018-01-122016 年1月,国际会计准则委员会(IASB) 发布了《国际财务报告准则第16 号——租赁》(IFRS 16),并将于2019 年1 月1 日生效,届时将替换现行的《国际会计准则第17 号——租赁》(IAS 17)。

IFRS 16 相对于IAS 17 变化较大,其指导原则在于要求承租人将租赁入表。

“新准则”下无论融资租赁还是经营租赁,承租人均须确认使用权资产和租赁负债。

IFRS 16 规定,租赁负债的计量是付款义务即租金和租赁期结束时预计支付款项之和的现值,这与IAS 17 下融资租赁负债的计量基本一致。

然而,使用权资产是一个崭新的概念,既非有形资产也非无形资产,对于其应当如何计量呢?按照IFRS 16,使用权资产的确认金额应为租赁负债加上初始直接费用等。

在确认资产和负债的基础上,对使用权资产计提折旧、负债则按照摊余成本法计算利息支出,这与现行IAS 17 下融资租赁的计量也是一致的。

另一方面,对于出租人而言,IFRS 16 要求仍将企业所发生的租赁业务分类为融资租赁和经营租赁,相应的会计处理也基本不变,由此可以看出,IFRS 16 实施后,主要影响的是承租人的经营租赁业务,其会计处理将发生较大变化(基本可看作视同融资租赁业务)。

IFRS 16 对租赁的认定是承租人从可识别资产获得经济利益并主导资产的使用,重点在于“主导资产使用”或“控制资产”,大致包括三个要素:一是出租人无实质可替换权,二是承租人有对使用方式和目的的决策权,三是承租人有操作决策权。

根据IFRS 16 提供的案例,如出租人有大量标的物可随意替换出租给客户的租赁物,且替换成本较低,则出租人有实质可替换权,不构成租赁;如客户对船舶的目的地不具决策权,则客户丧失对使用方式和目的的决策权,不构成租赁;或者虽然客户可决定船舶目的地,但无权操作船舶,则客户丧失操作决策权,也不构成租赁。

国际会计准则第16号

国际会计准则第1 6 号正体中文版草案不动产、厂房及设备总召集人国立政治大学会计系教授郑丁旺覆审委员国立台湾大学会计系教授杜荣瑞惠众联合会计师事务所执业会计师卢联生初审委员淡江大学会计系教授颜信辉翻译单位会计研究发展基金会(仅准则部分对外征求意见,有意见者请于99 年5 月20 日前,将意见以电子邮件方式寄至tifrs@.tw)财团法人中华民国会计研究发展基金会国际会计准则翻译覆审项目委员会征求意见函国际会计准则第16 号不动产、厂房及设备A部分财团法人中华民国会计研究发展基金会国际会计准则翻译覆审项目委员会翻译国际会计准则第16 号正体中文版草案A1国际会计准则第16号不动产、厂房及设备本版纳入截至2009 年12 月31 日发布之国际财务报导准则对本准则所作之修正。

国际会计准则委员会(IASC)于1993 年12 月发布国际会计准则第16 号「不动产、厂房及设备」,并取代国际会计准则第16 号「不动产、厂房及设备之会计」(1982 年3 月发布)。

国际会计准则第16 号于1998 年修订,另于2000 年作进一步之修正。

常务解释委员会制定下列三个与国际会计准则第16 号有关之解释:_ 解释公告第6 号「修改现有软件之成本」(1998 年5 月发布)_ 解释公告第14 号「不动产、厂房及设备:项目减损或损失之补偿」(1998 年12 月发布)_ 解释公告第23 号「不动产、厂房及设备:重大检修成本」(2000 年7 月发布)。

国际会计准则理事会(IASB)于2001 年4 月决议,依据旧章程所发布之所有准则及解释于修正或撤销前仍应适用。

国际会计准则理事会(IASB)于2003 年12 月发布修订之国际会计准则第16 号,并取代解释公告第6 号、解释公告第14 号及解释公告第23 号。

其后,国际会计准则第16 号已被下列国际财务报导准则修正:_ 国际财务报导准则第2 号「股份基础给付」(2004 年2 月发布)_ 国际财务报导准则第3 号「企业合并」(2004 年3 月发布)_ 国际财务报导准则第5 号「待出售非流动资产及停业单位」(2004 年3 月发布)_ 国际财务报导准则第6 号「矿产资源探勘及评估」(2004 年12 月发布)_ 国际会计准则第23 号「借款成本」(2007 年3 月修订)*_ 国际会计准则第1 号「财务报表之表达」(2007 年9 月修订)*_ 国际财务报导准则第3 号「企业合并」(2008 年1 月修订)†_ 「国际财务报导准则之改善」(2008 年5 月发布)。

国际会计准则第16号—不动产厂房和设备

国际会计准则第16号—不动产厂房和设备根据IAS16,不动产、厂房和设备是指企业用于出租给其他方或自用于生产、出售货物或提供服务的具有物质性的长期资产。

这包括土地、建筑物、设备、机器和车辆等。

IAS16要求企业对不动产、厂房和设备进行初始计量。

初始计量时,企业应以成本为基础,包括购买成本、直接相关的运输费用和安装费用。

如果企业通过金融租赁方式获得资产,则应将租赁资产按公允价值初始计量。

另外,企业还应考虑任何与资产采购相关的贷款利息。

对于不动产、厂房和设备的后续计量,IAS16提供了两种选择:成本模式和重新评估模式。

在成本模式下,企业应将不动产、厂房和设备按成本减少折旧或摊销,并进行减值测试。

减值测试应在每个会计期间结束时进行,以确定是否需要调整资产的帐面价值。

在重新评估模式下,企业可以选择按公允价值重新评估其不动产、厂房和设备。

重新评估后的公允价值减去累计折旧后的金额将被调整账面价值。

公允价值的变动将计入其他综合收益。

不论采用哪种模式,企业都应在每个会计期间结束时进行减值测试。

如果资产的账面价值超过可收回金额,则应进行减值损失的计提。

另外,对于处置资产,企业应按照资产的账面价值,减去预计出售费用后的净额,计提处置损失或计入投资收益。

在披露方面,根据IAS16,企业应披露其不动产、厂房和设备的账面价值、累计折旧、重新评估模式下的公允价值以及减值准备。

此外,企业还应披露计量政策、折旧方法和使用的假设。

总的来说,国际会计准则第16号规定了企业在计量、披露和报告不动产、厂房和设备方面的要求。

企业应根据其选择的计量模式按照规定的方法对资产进行计量,并及时披露相关信息。

这些规定有助于提高企业财务报告的透明度和比较性,使投资者和其他利益相关方能够更好地了解企业的资产状况和绩效。

(注:本文只是对国际会计准则第16号的简要介绍,具体操作和适用范围应根据个体企业的具体情况和国家的会计准则进行分析和应用。

《国际会计准则第16号:固定资产》简介

《国际会计准则第16号:固定资产》简介

朱海林

【期刊名称】《中国注册会计师》

【年(卷),期】1994(000)008

【摘要】本准则是国际会计委员会于1993年修订的准则之一,属于财务报表可比性项目.它替代了1981年颁布的国际会计准则第16号“固定资产”以及国际会计准则第4号“折旧会计”中涉及固定资产折旧的有关规定,定于1995年1月1日起生效.本准则适用于所有固定资产的会计处理.但不适用于(1)森林和类似再生性自然资源;(2)矿产权、矿产的勘探开采、石油、天然气和类似的非再生资源.另外,本准则不考虑在应用反映价格变动影响的综合制度过程中所涉及的某些方面的特殊问题,有关规定可参考国际会计准则第15号“反映价格变动影响的资料”以及国际会计准则第29号“恶性通货膨胀中的财务报告”.

【总页数】4页(P28-31)

【作者】朱海林

【作者单位】财政部会计司准则组

【正文语种】中文

【中图分类】F234.5

【相关文献】

1.浅析国际会计准则第16号与德国商法典--固定资产的后续计量(历史成本计量法) [J], 牛晓璠

2.基于我国固定资产准则与国际会计准则比较的探讨 [J], 苟勇

3.基于我国固定资产准则与国际会计准则比较的探究 [J], 史彩霞

4.我国固定资产准则与国际会计准则的比较 [J], 何帆

5.中国会计准则与国际会计准则的比较——以固定资产的会计处理为例 [J], 陈天波

因版权原因,仅展示原文概要,查看原文内容请购买。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2013IAS 16 Property, Plant and Equipmentas issued at 1 January 2013. Includes IFRSs with an effective date after 1 January 2013 but not the IFRSs they will replace.This extract has been prepared by IFRS Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of the financial statements can discern information about an entity’s investment in its property, plant and equipment and the changes in such investment. The principal issues in accounting for property, plant and equipment are the recognition of the assets, the determination of their carrying amounts and the depreciation charges and impairment losses to be recognised in relation to them.Property, plant and equipment are tangible items that:(a)are held for use in the production or supply of goods or services, for rental to others, or for administrativepurposes; and(b)are expected to be used during more than one period.The cost of an item of property, plant and equipment shall be recognised as an asset if, and only if:(a)it is probable that future economic benefits associated with the item will flow to the entity; and(b)the cost of the item can be measured reliably.Measurement at recognition: An item of property, plant and equipment that qualifies for recognition as an asset shall be measured at its cost. The cost of an item of property, plant and equipment is the cash price equivalent at the recognition date. If payment is deferred beyond normal credit terms, the difference between the cash price equivalent and the total payment is recognised as interest over the period of credit unless such interest is capitalised in accordance with IAS 23.The cost of an item of property, plant and equipment comprises:(a)its purchase price, including import duties and non-refundable purchase taxes, after deducting tradediscounts and rebates.(b)any costs directly attributable to bringing the asset to the location and condition necessary for it to becapable of operating in the manner intended by management.(c)the initial estimate of the costs of dismantling and removing the item and restoring the site on which it islocated, the obligation for which an entity incurs either when the item is acquired or as a consequence of having used the item during a particular period for purposes other than to produce inventories during that period.Measurement after recognition: An entity shall choose either the cost model or the revaluation model as its accounting policy and shall apply that policy to an entire class of property, plant and equipment.Cost model: After recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses.Revaluation model: After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluations shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period.If an asset’s carrying amount is increased as a result of a revaluation,the increase shall be recognised in other comprehensive income and accumulated in equity under the heading of revaluation surplus. However, the increase shall be recognised in profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognised in profit or loss. If an asset’s carrying amount is decreased as a result of a revaluation,the decrease shall be recognised in profit or loss. However, the decrease shall be recognised in other comprehensive income to the extent of any credit balance existing in the revaluation surplus in respect of that asset.Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. Depreciable amount is the cost of an asset, or other amount substituted for cost, less its residual value. Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately. The depreciation charge for each period shall be recognised in profit or loss unless it is included in the carrying amount of another asset. The depreciation method used shall reflect the pattern in which the asset’s future economic benefits are expected to be consumed by the entity.The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.To determine whether an item of property, plant and equipment is impaired, an entity applies IAS 36 Impairment of Assets.The carrying amount of an item of property, plant and equipment shall be derecognised:(a)on disposal; or(b)when no future economic benefits are expected from its use or disposal.。