【财务管理英文课件】Accounts Receivable and Inventory Management

合集下载

《ACCA考试之财务管理 FINANCIAL MANAGEMENT》课件PPT 5 Managing working capital

8

1.1 The basic EOQ formula

Key term

The economic order quantity (EOQ) is the optimal ordering quantity for an item of inventory which will minimize costs (order set-up + holding costs). Let D = usage in unit for one period (the demand)

4

1 Managing inventory

Fast forward

An economic order quantity can be calculated as a guide to minimizing costs in managing inventory level. Bulks discounts can however mean that a different order quantity minimizing inventory costs.

I * Q* U 2

2Co D U CH

16

1.3 Uncertainties in demand and lead times: a re-order level system

Fast forward

Uncertainties in demand and lead times taken to fulfill orders mean that inventory will be ordered once it reaches a re-order level Re-order level = maximum usage × maximum lead time

1.1 The basic EOQ formula

Key term

The economic order quantity (EOQ) is the optimal ordering quantity for an item of inventory which will minimize costs (order set-up + holding costs). Let D = usage in unit for one period (the demand)

4

1 Managing inventory

Fast forward

An economic order quantity can be calculated as a guide to minimizing costs in managing inventory level. Bulks discounts can however mean that a different order quantity minimizing inventory costs.

I * Q* U 2

2Co D U CH

16

1.3 Uncertainties in demand and lead times: a re-order level system

Fast forward

Uncertainties in demand and lead times taken to fulfill orders mean that inventory will be ordered once it reaches a re-order level Re-order level = maximum usage × maximum lead time

财务会计与财务管理知识学(PPT 60页)

(一)利息收入金额,按照他人使用本企业货币 资金的时间和实际利率计算确定;

(二)使用费收入金额,按照有关合同或协议约 定的收费时间和方法计算确定;

2. Revenue Measurement

◆商品销售收入的计量

一般地,商品销售收入=商品销售数量×单价。 但应注意以下几点:

◆商业折扣(Trade discount):标价×商业折 扣率=成交价。商业折扣不影响销售收入的计 量。

收入确认的具体标准

——按不同经营业务

〈3〉委托销售(代销)——委托方只有在 受托方卖出货物之后才能确认收入,受 托方卖出货物的具体标志是将“代销清 单”交给委托方。〈4〉预收货款销售 (订货销售)——无论是全部预收还是 部分预收,都应该在交付商品时确认收 入。

收入确认的具体标准

——按不同经营业务

经营的开展,利润不断地得以实现。 <2>但实际上,很难“客观”地给出这样地对

应关系,因为,经营循环是一个连续不断的过 程;如果一定要为经营过程的“每一时点”确 认收入、费用从而利润,就会很“主观”。

收入确认为什么成为问题?(续)

◆不同经营业务的经营循环过程有着不同 的特征,因此,它们很难以“统一”的 尺度作为收入确认的依据。

收入确认的具体标准 ——按不同经营业务

◆一些特殊情形下的具体确认标志:

〈1〉商品须经比较“复杂”的安装程序时—— 通常须待安装完毕时再确认;〈2〉附有退货 条件的商品销售——如果企业不能合理地确定 退货的可能性,则在售出商品退货期满时确认 收入;如果能够对退货的可能性做出合理估计 的,在发出商品时将估计不会发生退货的部分 确认为收入。

建造合同收入的确认:

合同结果能可靠估计时

完工百分比法

合同结果不能可靠估计时

(二)使用费收入金额,按照有关合同或协议约 定的收费时间和方法计算确定;

2. Revenue Measurement

◆商品销售收入的计量

一般地,商品销售收入=商品销售数量×单价。 但应注意以下几点:

◆商业折扣(Trade discount):标价×商业折 扣率=成交价。商业折扣不影响销售收入的计 量。

收入确认的具体标准

——按不同经营业务

〈3〉委托销售(代销)——委托方只有在 受托方卖出货物之后才能确认收入,受 托方卖出货物的具体标志是将“代销清 单”交给委托方。〈4〉预收货款销售 (订货销售)——无论是全部预收还是 部分预收,都应该在交付商品时确认收 入。

收入确认的具体标准

——按不同经营业务

经营的开展,利润不断地得以实现。 <2>但实际上,很难“客观”地给出这样地对

应关系,因为,经营循环是一个连续不断的过 程;如果一定要为经营过程的“每一时点”确 认收入、费用从而利润,就会很“主观”。

收入确认为什么成为问题?(续)

◆不同经营业务的经营循环过程有着不同 的特征,因此,它们很难以“统一”的 尺度作为收入确认的依据。

收入确认的具体标准 ——按不同经营业务

◆一些特殊情形下的具体确认标志:

〈1〉商品须经比较“复杂”的安装程序时—— 通常须待安装完毕时再确认;〈2〉附有退货 条件的商品销售——如果企业不能合理地确定 退货的可能性,则在售出商品退货期满时确认 收入;如果能够对退货的可能性做出合理估计 的,在发出商品时将估计不会发生退货的部分 确认为收入。

建造合同收入的确认:

合同结果能可靠估计时

完工百分比法

合同结果不能可靠估计时

会计学(第21版)课件:Receivables

Uncollectible Receivables

The Allowance Method

▪ This method is consistent with the matching principle.

▪ Management makes an estimate each year of the portion of accounts receivable that may not be collectible.

Customer

Ashby & Co. B. T. Barr Brock Co.

$101,000 ($105,000 – $4,000), is called the net realizable value (NRV).

The adjusting entry reduces receivables to the NRV and matches uncollectible expenses

6. Describe the nature and characteristics of promissory notes.

7. Journalize the entries for notes receivable transactions.

8. Prepare the Current Assets presentation of receivables on the balance sheet.

Receivables

Accounting, 21st Edition

Warren Reeve Fess

Some of the action has been automated, so click the mouse when you see this lightning bolt in the lower right-hand

财务专业英语ppt课件

E1-2 Divide into groups as instructed by your professor and discuss the following:

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

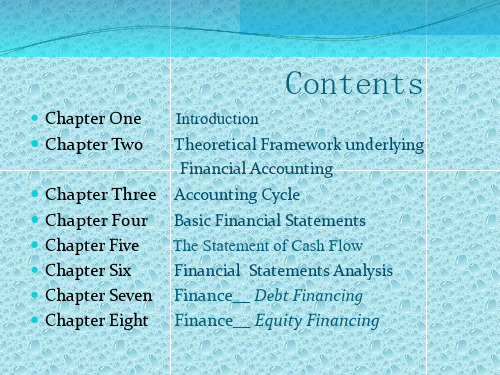

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

Chapter 10 Accounts Receivable and Inventory Management 应收帐款和存货管理 财务管理(双语版) 教学课件

假定,无缺货成本,订货无+购置成本(单价一定时,与经济订货量无关)

=平均存货量×单位储存成本+每次订货成本×订货次数

TC(Q)=Q/2*C+O*S/Q

Q* 2O S C

3.Order Point 订货点 通常发出订单到收到存货之间有一段时滞---交货期(lead time) Order Point(OP)=Lead time ×Daily usage 再订货点=订货提前期×每日耗用量 4.Safety Stock 安全存货量(保险储备) 为防止需求量(耗用量)和交货期的不确定性而持有的存货 Order Point(OP)=(Average lead time ×Average daily

The optimal policy is the one that provides the greatest incremental benefit.最优的政策应是能提供最大增量收益的政策.

4.Collection Policy and Procedure收帐政策和程序

收帐费用越高,坏帐比率越低,平均收帐期就越短.

Trade-off the level of expenditures with the reduction in the cost of baddebt losses and savings due to the reduction in investment in receivables.

二、Inventory management and control 存货管理与 控制

Chapter 10 Accounts Receivable and Inventory Management 应收帐款和存货管理

3.Credit terms 信用条件(信用期间(credit period)、现金折扣

Module 2 财务会计入门英文版 PPT 21

LO 3: Journalising

Journalizing – Simple journal entries.

On September 1, stockholders invested $15,000 cash in exchange for ordinary shares, and Softbyte purchased computer equipment for $7,000 cash.

Record of increases and decreases in a specific asset, liability, equity, income, or expense item.

Account Name

Debit / Dr.

Credit / Cr.

Debit = “Left” Credit = “Right”

LO 4: The Ledger

Chart of Accounts

Illustration 2-18

LO 4: The Ledger

Standard Form of Account

➢ T-account form used in accounting textbooks. ➢ Ledger form used in practice.

1 600

Service Revenue

1 600

31 Cash

900

Accounts Receivable

900

Required

(a) Post the transactions to T accounts.

(b) Prepare a trial balance as at 31 August 2011.

财务管理英文版.ppt

210

Total Equity $1,139

Total Liab/Equitya,b $2,169

a. Note, Assets = Liabilities + Equity.

b. What BW owed and ownership position.

c. Owed to suppliers for goods and services.

d. Unpaid wages, salaries, etc.

e. Debts payable < 1 year. f. Debts payable > 1 year. g. Original investment. h. Earnings reinvested.

Basket Wonders’ Income Statement

Financial Statement Analysis

Financial Statements A Possible Framework for Analysis Balance Sheet Ratios Income Statement and Income

Statement/Balance Sheet Ratios Trend Analysis Common-Size and Index Analysis

Ⅰ.Primary Types of Financial Statements

Balance Sheet

A summary of a firm’s financial position on a given date that shows total assets = total liabilities + owners’ equity. Income Statement

财务管理学英文课件 (1)

10-1

u Credit and Collection Policies

u Analyzing the Credit Applicant

u Inventory Management and Control

10-2

Possible Cash Discount

(1) Average Collection Period

10-10

is considering changing its

credit period from

(which has resulted

in 12 A/R “Turns” per year) to

(which is

expected to result in 6 A/R “Turns” per year).

(20% opp. cost) x $24,000 =

Profits > Required pre-tax return

10-8

Quality of Trade Account

Possible Cash Discount

(1) Average Collection Period

(2) Bad-debt Losses

-- The period of time

during which a cash discount can be taken for

early payment. For example,

allows a

cash discount in the first 10 days from the

invoice date.

($2,000,000 sales) / (12 Turns) = $166,667

10-13

u Credit and Collection Policies

u Analyzing the Credit Applicant

u Inventory Management and Control

10-2

Possible Cash Discount

(1) Average Collection Period

10-10

is considering changing its

credit period from

(which has resulted

in 12 A/R “Turns” per year) to

(which is

expected to result in 6 A/R “Turns” per year).

(20% opp. cost) x $24,000 =

Profits > Required pre-tax return

10-8

Quality of Trade Account

Possible Cash Discount

(1) Average Collection Period

(2) Bad-debt Losses

-- The period of time

during which a cash discount can be taken for

early payment. For example,

allows a

cash discount in the first 10 days from the

invoice date.

($2,000,000 sales) / (12 Turns) = $166,667

10-13

《财务会计英语》PPT课件

完整版课件ppt

9

Time-Period Concept

A fiscal year ends on a date other than December 31. Most retailers, including Wal-Mart and J.C.Penney, use a fiscal year that ends on January 31 because the low point in their business activity falls after Christmas.

完整版课件ppt

5

Under accrual accounting, cash transactions are recorded as well as noncash transactions such as: ➢Purchases of inventory on account ➢Sales on account ➢Depreciation expense ➢Accrual of expenses incurred but not yet paid ➢Usage of prepaid rent, insurance, and supplies

➢ A fiscal year ends on a date other than December 31.Interim financial statements are usually prepared for periods such as a month, a quarter, or semiannual period.

完整版课件ppt

15

Closing accounts

Debit each revenue account for its credit balance and credit Retained Earnings for the sum of the revenues. Credit each expense account for its debit balance. Debit retained earnings for the sum of the expenses . Credit the dividends account for its debit balance. Debit Retained Earnings.

英文版财务会计51页PPT

Copyright © 2007 Prentice-Hall. All rights reserved

14

Going Concern Concept

• Assumes that the entity will remain in operation for the foreseeable future

Copyright © 2007 Prentice-Hall. All rights reserved

28

Exercise 1-17

5

Ethics

• Audit

– Examination of company’s financial situation – Performed by independent accountants

• Sarbanes-Oxley Act

– Criminal offense to falsify financial statements

• AICPA – Code of Professional Conduct for Accountants

• IMA – Standards of Ethical Conduct

Copyright © 2007 Prentice-Hall. All rights reserved

7

Types of Business Organizations

Copyright © 2007 Prentice-Hall. All rights reserved

2

Decision Makers

• Individuals • Businesses • Investors • Creditors • Taxing Authorities

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

to ?/10, net 60.

Current annual credit sales of $5 million are expected to be maintained.

The firm expects 30% of its credit customers (in dollar volume) to take the cash discount and thus increase A/R turns to 8.

early payment. For example, ? / 10 allows a cash discount in the first 10 days from the

invoice date.

Cash Discount -- A percent (%) reduction in sales or purchase price allowed for early payment of invoices. For example, ? / 10?allows the customer to take a 2% cash discount during the cash discount period.

Firm Collection Program

Credit Standards

Credit Standards -- The minimum quality of credit worthiness of a credit applicant

that is acceptable to the firm.

$333,333 - $166,667 = $166,666

Total investment in add. receivables

$33,334 + $166,666 = $200,000

Req. pre-tax return on add. investment

(20% opp. cost) x $200,000 = $40,000

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

(2) Bad-debt Losses

10-9

Length of Credit Period

Firm Collection Program

Credit Terms

($5 contribution) x (4,800 units) = $24,000

Additional receivables

($120,000 sales) / (4 Turns) = $30,000

Investment in add. receivables

($2

10-5

Example of Relaxing Credit Standards

Basket Wonders is not operating at full capacity and wants to determine if a relaxation of their credit standards will enhance profitability.

10-13

Example of Relaxing the Credit Period

New receivable level

($2,000,000 sales) / (6 Turns) = $333,333

Investment in add. receivables (original sales)

Ignoring any additional bad-debt losses that may arise, should Basket Wonders

relax their credit standards?

10-7

Example of Relaxing Credit Standards

Profitability of additional sales

relax their credit period?

10-12

Example of Relaxing the Credit Period

Profitability of additional sales

($5 contribution)x(10,000 units) = $50,000

Additional receivables

($250,000 sales) / (6 Turns) = $41,667

Investment in add.

($20/$25) x ($41,667) =

receivables (new sales) $33,334

Previous receivable level

($2,000,000 sales) / (12 Turns) = $166,667

invoice date.

10-10

Example of Relaxing the Credit Period

Basket Wonders is considering changing its credit period from net 30 (which has resulted in

12 A/R turns per year) to net 60 (which is expected to result in 6 A/R turns per year).

10-17

Example of Introducing a Cash Discount

The before-tax opportunity cost for each dollar of funds died-up?in additional receivables is 20%.

(2) Bad-debt Losses

10-15

Length of Credit Period

Firm Collection Program

Credit Terms

Cash Discount Period -- The period of time during which a cash discount can be taken for

10-11

Example of Relaxing the Credit Period

The before-tax opportunity cost for each dollar of funds died-up in additional receivables is 20%.

Ignoring any additional bad-debt losses that may arise, should Basket Wonders

The firm is currently producing a single product with variable costs of $20 and selling price of $25. Relaxing credit standards is not expected to affect current customer payment habits.

10-14 Yes! Profits > Required pre-tax return

Credit and Collection Policies of the Firm

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

The firm is currently producing a single product with variable costs of $20 and a selling price of $25.

Additional annual credit sales of $250,000 from new customers are forecasted, in addition to the current $2 million in annual credit sales.

Req. pre-tax return on add. investment

(20% opp. cost) x $24,000 = $4,800

Yes! Profits > Required pre-tax return

10-8

Credit and Collection Policies of the Firm

10-2

Credit and Collection Policies of the Firm

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

(2) Bad-debt Losses

10-3

Length of Credit Period

Credit Period -- The total length of time over which credit is extended to a customer to

pay a bill. For example, net 30?requires full payment to the firm within 30 days from the

Why lower the firm’s credit standards?

The financial manager should continually lower the firm’s credit standards as long as

profitability from the change exceeds the extra costs generated by the additional

Current annual credit sales of $5 million are expected to be maintained.

The firm expects 30% of its credit customers (in dollar volume) to take the cash discount and thus increase A/R turns to 8.

early payment. For example, ? / 10 allows a cash discount in the first 10 days from the

invoice date.

Cash Discount -- A percent (%) reduction in sales or purchase price allowed for early payment of invoices. For example, ? / 10?allows the customer to take a 2% cash discount during the cash discount period.

Firm Collection Program

Credit Standards

Credit Standards -- The minimum quality of credit worthiness of a credit applicant

that is acceptable to the firm.

$333,333 - $166,667 = $166,666

Total investment in add. receivables

$33,334 + $166,666 = $200,000

Req. pre-tax return on add. investment

(20% opp. cost) x $200,000 = $40,000

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

(2) Bad-debt Losses

10-9

Length of Credit Period

Firm Collection Program

Credit Terms

($5 contribution) x (4,800 units) = $24,000

Additional receivables

($120,000 sales) / (4 Turns) = $30,000

Investment in add. receivables

($2

10-5

Example of Relaxing Credit Standards

Basket Wonders is not operating at full capacity and wants to determine if a relaxation of their credit standards will enhance profitability.

10-13

Example of Relaxing the Credit Period

New receivable level

($2,000,000 sales) / (6 Turns) = $333,333

Investment in add. receivables (original sales)

Ignoring any additional bad-debt losses that may arise, should Basket Wonders

relax their credit standards?

10-7

Example of Relaxing Credit Standards

Profitability of additional sales

relax their credit period?

10-12

Example of Relaxing the Credit Period

Profitability of additional sales

($5 contribution)x(10,000 units) = $50,000

Additional receivables

($250,000 sales) / (6 Turns) = $41,667

Investment in add.

($20/$25) x ($41,667) =

receivables (new sales) $33,334

Previous receivable level

($2,000,000 sales) / (12 Turns) = $166,667

invoice date.

10-10

Example of Relaxing the Credit Period

Basket Wonders is considering changing its credit period from net 30 (which has resulted in

12 A/R turns per year) to net 60 (which is expected to result in 6 A/R turns per year).

10-17

Example of Introducing a Cash Discount

The before-tax opportunity cost for each dollar of funds died-up?in additional receivables is 20%.

(2) Bad-debt Losses

10-15

Length of Credit Period

Firm Collection Program

Credit Terms

Cash Discount Period -- The period of time during which a cash discount can be taken for

10-11

Example of Relaxing the Credit Period

The before-tax opportunity cost for each dollar of funds died-up in additional receivables is 20%.

Ignoring any additional bad-debt losses that may arise, should Basket Wonders

The firm is currently producing a single product with variable costs of $20 and selling price of $25. Relaxing credit standards is not expected to affect current customer payment habits.

10-14 Yes! Profits > Required pre-tax return

Credit and Collection Policies of the Firm

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

The firm is currently producing a single product with variable costs of $20 and a selling price of $25.

Additional annual credit sales of $250,000 from new customers are forecasted, in addition to the current $2 million in annual credit sales.

Req. pre-tax return on add. investment

(20% opp. cost) x $24,000 = $4,800

Yes! Profits > Required pre-tax return

10-8

Credit and Collection Policies of the Firm

10-2

Credit and Collection Policies of the Firm

Quality of Trade Account

(1) Average Collection Period

Possible Cash Discount

(2) Bad-debt Losses

10-3

Length of Credit Period

Credit Period -- The total length of time over which credit is extended to a customer to

pay a bill. For example, net 30?requires full payment to the firm within 30 days from the

Why lower the firm’s credit standards?

The financial manager should continually lower the firm’s credit standards as long as

profitability from the change exceeds the extra costs generated by the additional