MANAGERIAL ACCOUNTING chapter 10 1,2,3,4,5,6,7,19,22,27 and 30(problem solution 管理会计

Managerial Accounting

THE HELLER SCHOOL FOR SOCIAL POLICY AND MANAGEMENTBRANDEIS UNIVERSITYHS 251fManagerial AccountingSpring 2007Brenda AndersonOffice: Golding 20, Sachar 13Phone: 781-736-8423Email: banders@Course Description: The purpose of this course is to provide a general introduction to the concepts, problems and issues related to managerial accounting. Managerial accounting predominantly addresses the internal use of economic information regarding the resources used in the process of producing goods and providing services. Internal users of accounting information are all of those individuals that are involved in the business decision-making process of the economic entity. In the course, you will become acquainted with some of the conventional methods of internal reporting used in planning, control and decision-making. Fundamental aspects of cost behavior and cost accounting will also be discussed, but always from the perspective of the manager who must make decisions rather than the accountant who prepares the information.Management Discipline Skills and Competencies: Upon completion of this course, the student will be able to (1) understand the nature of product and service cost measurement and behavior, (2) analyze costs using cost/volume/profit analysis, (3) employ a number of cost allocation techniques and (4) analyze a variety of short term business problems (outsourcing, special orders, etc.) using differential cost approaches.Readings:Garrison, Noreen and Brewer, Managerial Accounting, 11th Edition (McGraw Hill/ Irwin) Course Requirements:Quiz 20%Exam 65%Class Participation 15%Students are expected to attend all class sessions and to actively participate in class discussions. Class participation involves being regularly engaged in the discussion/lecture and making a positive contribution by asking thoughtful questions, sharing relevant experiences, requesting clarification and making comments. All forms of participation should be conducted in a manner that is respectful of fellow students and the professor.Provisions for Feedback: Performance feedback will be provided to students in the form of grades and written comments on exams. The reading and assignment schedule presented in this syllabus is a tentative schedule and is subject to change.Academic Integrity: Academic integrity is central to the mission of educational excellence at Brandeis University. Each student is expected to turn in work completed independently, except when assignments specifically authorize collaborative effort. It is not acceptable to use the words or ideas of another person- be it a world-class philosophers or your lab partner - without proper acknowledgement of that source. This means that you must use footnotes and quotation marks to indicate the sources of any phrases, sentences, paragraphs or ideas found in published volumes, on the internet, or created by another student. Violations of university policies on academic integrity, described in Section 3 of Rights and Responsibilities, may result in failure in the course or on the assignment, and could end in suspension from the University. If you are in doubt about the instructions for any assignment in this course, you must ask for clarification.Notice: If you have a documented disability on record at Brandeis University and require accommodations, please bring it to the instructor’s attention prior to the second meeting of the class. If you have any questions about this process, contact Beth Mann, disabilities coordinator for the Heller School at bmann@.Course ScheduleDate Session Assignment1/17 1 Introduction to Management Decision Making andUnderstanding Cost Behavior in an OrganizationReadings: Chapters 1, 2E2-1, E2-2, E2-7, P2-26, P2-27 (1&2only), P2-29Case: C2-301/24 2 Allocating Common Costs to Products and Services: How Much Does It Really Cost to Produce a Product or Provide a Service?Reading: Chapter 2&3E3-2, E3-3, E3-6, P3-20, P3-24, P3-27, P3-29, P3-30Case Assignment: Walking Hand in Hand*1/31NO CLASS – BRANDEIS MONDAY2/7 3Overhead Cost Allocation/ Intro. to CVP AnalysisReading: Chapter 5E5-4, E5-5, E5-6, P5-14, P5-16Case Assignment: Child’s Play*2/14 4Analyzing the Cost, Volume, Profit RelationshipQUIZReading: Chapter 6E6-3, E6-4, E6-5, E6-7, E6-9, P6-19, P6-22, P6-232/21NO CLASS – UNIVERSITY RECESS2/26 LAST DAY TO DROP MODULE I CLASSES2/28 5 Differential Cost AnalysisReading: Chapter 13E13-3, E13-4, E13-5, E13-6, E13-7, P13-17, P13-20,P13-18Case Assignment: Happy Homes3/7 6Differential Cost AnalysisReading: Chapter 13P13-22, P13-233/14 7 FINAL EXAM*Cases to be distributed by professor。

管理会计课件 英文

1 - 11 1-11 - 11111111h11111ythtr

The Nature of Planning and Controlling

Management Process Internal Accounting System

Budgets, Special Reports

Other information systems

Mayfair Starbucks Store, March 31, 20X1

Sales Less: Ingredients Store labor Other labor Utilities, etc. Total expenses Operating income

Budget $50,000

22,000 12,000 6,000 4,500 $44,500 $ 5,500

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 1 - 14 1-11 - 14111111h11111ythtr

Budget: quantitative expression of a plan of action

Performance reports: compare actual results with budgeted amounts provide feedback by comparing results with plans highlight variances

Actual $50,000

24,500 11,600 6,050 4,500 $46,650 $ 3,350

Variance 0

$2,500 U 400 F 50 U 0 $2,150 U $2,150 U

agp0107管理会计

Managerial Decision Making

C管ha理pte决r 7策的制定 第7章

After studying chapter 7, you should be able to:学习第7章后,你应该能够:

Understand ethical standards 理解伦理标准

•Fundamental Concepts 基础概念

After studying chapter 2, you should be able to:学习第2章后,你应该能够:

Master the concept of cost. 掌握成本概念

管理决策的制定 第3章(续)

Describe how managers use cost behavior patterns. 描述管理者如何使用成本习性模式

Understand how analysts estimate cost behavior using engineering methods and account analysis. 理解分析家使用工程方法与会计分析来估计成 本习性

Variable costs and fixed costs. 可变成本与固定成本

Short run and long run. 短期运营与长期运营

Define relevant range.明确相关范围 Identify capacity costs, committed costs, and

discretionary costs. 识别资本成本,承诺成本,以及可随意支配成本

Understand the nature of various cost behavior patterns. 理解不同成本习性模式的本质

管理会计第14版(charles 查尔斯)英文影印版课后答案

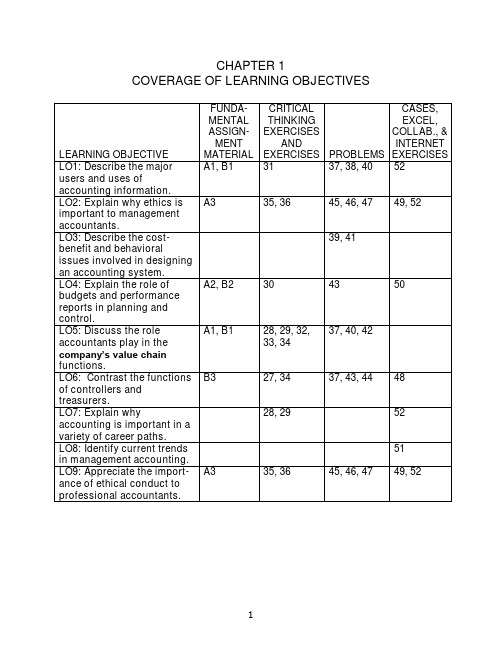

COVERAGE OF LEARNING OBJECTIVESManagerial Accounting and the Business Organization1-A1 (10-15 min.)Because the accountant's duties are often not sharply defined, some of these answers could be challenged:1. Attention directing and problem solving. Budgeting involves makingdecisions about planned activities -- hence, aiding problem solving.Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has ascorekeeping dimension.2. Problem solving. Helps a manager assess the impact of a decision.3. Scorekeeping. Reports on the results of an operation. Could also beattention direction if scrap is an area that might require management decisions.4. Attention directing. Focuses attention on areas that need attention.5. Attention directing. Helps managers learn about the informationcontained in a performance report.6. Scorekeeping. The statement merely reports what has happened.7. Problem solving. The cost comparison is apparently useful becausethe manager wishes to decide between two alternatives. Thus, it aids problem solving.8. Attention directing. Variances point out areas where results differfrom expectations. Interpreting them directs attention to possiblecauses of the differences.9. Problem solving. Aids a decision about where the parts should bemade.10. Scorekeeping. Determining a depreciation schedule is simply anexercise in preparing financial statements to report the results ofactivities.1. Budgeted Actual DeviationsAmounts Amounts or Variances Room rental $ 140 $ 140 $ 0Food 800 1,008 208UEntertainment 600 600 0Decorations 220 190 30FTotal $1,760 $1,938 $178U2. Because of the management by exception rule, room rental andentertainment require no explanation. The actual expenditure forfood exceeded the budget by $208. Of this $208, $150 is explained by attendance of 15 persons more than budgeted (at a budget of $10 per person) and $58 is explained by expenditures above $10 per person.Actual expenditures for decorations were $30 less than the budget. If all desired decorations were purchased, the decorations committee should be commended for their savings.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard:1. The General Mills manager must respect the confidentiality standard.He or she should not disclose any information about the new cereal.2. Roberto must address his level of competence for the assignment. Ifhis supervisor knows his level of expertise and wants an analysisfrom a “layperson” point of view, he should do it. However, if thesupervisor expects an expert analysis, Roberto must admit his lackof competence.3. The objectivity standard should cause Helen to decline to omit theinformation from her budget. It is relevant information, and itsomission may mislead readers of the budget.Because the accountant’s duties are often not sharply defined, some of these answers could be challenged:1. Scorekeeping. Records events.2. Scorekeeping. Simply recording of what has happened.3. Problem solving. Helps a manager decide between alternatives.4. Attention directing. Directs attention to the use of overtime labor.5. Problem solving. Provides information to managers for decidingbetween alternatives.6. Attention directing. Directs attention to why nursing costs increased.7. Attention directing. Directs attention to areas where actual resultsdiffered from the budget.8. Problem solving. Helps the vice-president to decide which course ofaction is best.9. Scorekeeping. Records costs in the department to which theybelong.10. Scorekeeping. Records actual overtime costs.11. Attention directing. Directs attention to stores with either high or lowratios of advertising expenses to sales.12. Attention directing. Directs attention to causes of returns of the drug.13. Attention directing or problem solving, depending on the use of theschedule. If it is to identify areas of high fuel usage it is attentiondirecting. If it is to plan for purchases of fuel, it is problem solving. 14. Problem solving. Provides information for deciding between twoalternative courses of action.15. Scorekeeping. Records items needed for financial statements.1 & 2. Budget Actual VarianceSales $75,000 $74,860 $ 140UCosts:Fireworks $35,000 $39,500 $4,500ULabor 15,000 13,000 2,000FOther 8,000 8,020 20UProfit $17,000 $14,340 $2,660U3. The cost of fireworks was $4,500 ÷ $35,000 = 13% over budget. Didfireworks suppliers raise their prices? Did competition cause retailprices to be lower than expected? There should be someexplanation for the extra cost of fireworks. Also, the labor cost was$2,000 ÷ $15,000 =13% below budget. It would be useful to discover why this cost was saved. Both sales and other costs were very close to budget.1-B3 (10 - 15 min.)1. Treasurer. Analysts affect the company's ability to raise capital,which is the responsibility of the treasurer.2. Controller. Advising managers aids operating decisions.3. Controller. Advice on cost analysis aids managers' operatingdecisions.4. Controller. Divisional financial statements report on operations.Financial statements are generally produced by the controller'sdepartment.5. Treasurer. Financing the business is the responsibility of thetreasurer.6. Controller. Tax returns are part of the accounting process overseenby the controller.7. Treasurer. Insurance, as with other risk management activities, isusually the responsibility of the treasurer.8. Treasurer. Allowing credit is a financial decision.1-1 Decision makers within and outside an organization use accounting information for three broad purposes:1. Internal reporting to managers for planning and controllingoperations.2. Internal reporting to managers for special decision-making and long-range planning.3. External reporting to stockholders, government, and other interestedparties.1-2 The emphasis of financial accounting has traditionally been on the historical data presented in the external reports. Management accounting emphasizes planning and control purposes.1-3 The branch of accounting described in the quotation is management accounting.1-4 Scorekeeping is the recording of data for a later evaluation of performance. Attention directing is the reporting and interpretation of information for the purpose of focusing on inefficiencies of operation or opportunities for improvement. Problem solving presents a concise analysis of alternative courses of action.1-5 GAAP applies to publicly issued annual financial reports. Internal accounting reports are not restricted by GAAP.1-6 Yes, but it covers more than that. The Foreign Corrupt Practices Act applies to all publicly-held companies and covers the quality of internal accounting control as well as bribes and other matters.1-7 Users cannot easily observe the quality of accounting information. Thus, they rely on the integrity of accountants to be sure the information is accurate. Information that is unreliable is worthless, so if accountants do not have a reputation for integrity, the information they produce will not have value.1-8 Three examples of service organizations are banks, insurance companies, and public accounting firms. Such organizations tend to be labor intensive, have outputs that are difficult to define and measure, and have both inputs and outputs that are difficult or impossible to store.1-9 Two considerations are cost-benefit balance and behavioral effects. Cost-benefit balance refers to how well an accounting system helps achieve management's goals in relation to the cost of the system. The behavioral consideration specifies that an accounting system should be judged by how it will affect the behavior (that is, decisions) of managers.1-10 Yes. The act of recording events has become as much a part of operating activities as the act of selling or buying. For example, cash receipts and disbursements must be traced, and receivables and payables must be recorded, or else gross confusion would ensue.1-11 A budget is a prediction and guide; a performance report is a tabulation of actual results compared with the budget; and a variance reconciles the differences between budget and actual.1-12 No. Management by exception means that management spends more effort on those areas that seem to be out of control and less on areas that are functioning as planned. This method is an efficient way for managers to decide where to put their time and effort.1-13 No. There is no perfect system of automatic control, nor does accounting control anything. Accounting is a tool used by managers in their control of operations.1-14 Information that is relevant for decisions about a product depends on the product's life-cycle stage. Therefore, to prepare and interpret information, accountants should be aware of the current stage of a product's life cycle.1-15 The six functions are: (1) research and development – generation and experimentation with new ideas; (2) product and service process design – detailed design and engineering of products; (3) production – use of resources to produce a product or service; (4) marketing - informing customers of the value and features of products or services; (5) distribution – delivering products or services to customers; and (6) customer service –support provided to customers.1-16 No. Not all of the functions are of equal importance to the success of a company. Measurement and reporting should focus on those functions that enable a company to gain and maintain a competitive edge.1-17 Line managers are directly responsible for the production and sale of goods or services. Staff managers have an advisory function – they support line managers.1-18 Management accountants are the information specialists, even in non-hierarchical companies. However, in such companies they are more directly involved with managers and are often parts of cross-functional teams.1- 19 A treasurer is concerned mainly with the company's financial matters, the controller with operating matters. In large organizations, there are sufficient activities associated with both financial and operating matters to justify two separate positions. In a small organization the same person might be both treasurer and controller.1-20 The four parts of the CMA examination are: (1) economics, finance, and management, (2) financial accounting and reporting, (3) management reporting, analysis, and behavioral issues, and (4) decision analysis and information systems.1-21 This is not true. About one-third of CEOs come from finance or accounting backgrounds. Accounting is excellent preparation for top management positions because accountants are often exposed to many parts of the company early in their careers.1-22 Changes in technology are affecting how accountants operate. They must be able to account for e-commerce transactions efficiently and safely, they often must integrate their accounting systems into ERP systems, and an increasing number are beginning to use XBRL to communicate information electronically.1-23 The essence of the just-in-time philosophy is the elimination of waste, accomplished by reducing the time products spend in the production process and trying to eliminate the time spent in processes that do not add value to the product.1-24 Moving tools and products that are in process from one location to another in a plant is an activity that does not add value to the product. So changing the plant layout to eliminate wasted movement and time improves production efficiency.1-25 The four major responsibilities are: (1) competence - develop knowledge; know and obey laws, regulations, and technical standards; and perform appropriate analyses, (2) confidentiality - refrain from disclosing or using confidential information, (3) integrity - avoid conflicts of interest, refuse gifts that might influence actions, recognize limitations, and avoid activities that might discredit the profession, and (4) objectivity - communicate information fairly, objectively, and completely, within confidentiality constraints.1-26 Standards do not always provide the needed guidance. Sometimes an action borders on being unethical, but it is not clearly an ethical violation. Other times two ethical standards conflict. In situations such as these, accountants must make ethical judgments.1-27 (5-10 min.)Typical activities associated with the treasurer function include:❑Provision of capital❑Investor relations❑Short-term financing❑Banking and custody❑Credits and collections❑Investments❑Risk managementTypical activities associated with the controller function include:❑Planning for control❑Reporting and interpreting❑Evaluating and consulting❑Tax administration❑Government reporting❑Protection of assets❑Economic appraisal1-28 (5-10 min.)Activities 2, 4, 5, and 6 are primarily associated with marketing decisions. The management accountant would assist in these decisions as follows: Boeing Company’s pricing decision requires cost data relevant to the new method of distributing spare parts. will need to know the costs of the advertising program as well as the additional costs of other value chain functions resulting from increased sales. TexMex Foods will need to know the incremental revenues and incremental costs associated with the special order. Target Stores needs to know the impact on both revenues and costs of closing one of its stores.Activities 1, 7, and 8 are primarily associated with production decisions. The management accountant would assist in these decisions as follows. Porsche Motor Company needs an analysis of the costs associated with purchasing the part compared to the costs of making the part. Dell will need to know the costs of the training program and the savings associated with increased efficiencies in the setup and changeover activities. General Motors needs to know the costs and salvage values of the replacement equipment, the proceeds of the sale of the old equipment, and the operating savings associated with the use of the new equipment.1-30 (5 min.)1. Management 4. Management 7. Financial2. Management 5. Management3. Financial 6. Financial1. Performance ReportBudget Actual Variance Explanation Revenues $220,000 $228,000 $8,000 F Additional salesfrom newproducts* Advertising cost 15,000 16,500 (1,500) U New advertisingCampaignNet $6,500 F* From the New Products Report, seven new products were added. This exceeded the plan to add six.2.Factors that may not have been considered include:a.The costs of new products may have exceeded their price.b.Customer satisfaction with new products may not have been partof the new products report.petitors’ reactions to the Starbucks store’s actions may nothave been anticipated.d.External uncontrollable factors such as increases in operatingcosts, adverse weather, changes in the overall economy, newcompetitors entering the market, or key employee turnover mayhave decreased efficiency.1-32 (5 min.)1. Line, support 3. Staff, marketing 5. Staff, support2. Staff, support 4. Line, marketing 6. Line, productionMicrosoft is a company that most students will know and have some understanding of what functions its managers perform. Nevertheless, this may not be an easy exercise for those who have little knowledge of how companies operate.Research & development – Because software companies must continually come out with new products and upgrades to their current products this is a critical function for Microsoft. More than one-fourth of Microsoft’s operating expenses are devoted to R&D.Design of products, services, or processes – For Microsoft the design and R&D process probably overlap considerably. Product design is critical; process design is probably not. One essential part of design is beta testing – that is, field testing of new software. This quality-control step is essential to prevent customer dissatisfaction with new products.Production – Microsoft produces disks and CD-ROMs and the manuals and packaging to go with them. However, they are increasingly delivering software over the Internet, which takes an initial process design and then few resources. It is not likely a major focus for Microsoft.Marketing – Microsoft spends more on sales and marketing than on any other operating expense. Increasing competition in software sales makes marketing essential to the company’s future. This function includes advertising and direct marketing activities, but it also includes activities of the company’s sales force. Distribution – This function is becoming simpler for Microsoft as it delivers more and more software over the Internet. Although the company must stay abreast of competitors in delivery methods, this is not likely to create a major competitive advantage or disadvantage for Microsoft.Customer service – Customer service is important, but Microsoft tries to minimize its costs in this area by product design – making things work right without needing deep computer expertise. Still, poor customer service can severely impact a company, so Microsoft must attend to it.Support functions – Most of the time these are not a major focus. There is one exception recently for Microsoft. Legal support has been front and center. The very future of the company was based on court judgments for which good legal support was essential.The management accountant's major purpose is to provide information that helps line managers in making decisions regarding the planning and controlling of operations. The accountant supplies information for scorekeeping, attention directing, and problem solving. In turn, managers use this and other information for routine and non-routine decisions and for evaluating subordinates and the performance of sub-parts of the organization. Management accountants must walk a delicate line between (1) making sure that managers are properly using the pertinent information and (2) making sure that the managers, not the accountants, are doing the actual managing.1-35(5 min.)Other costs of a poor ethical environment include legal costs and costs due to high employee turnover. Other benefits of a good ethical environment include low employee turnover, low loss from internal theft, and improved customer satisfaction resulting from better quality and service (that result from a more productive work environment).1-36(5 min.)There are numerous examples.“You understand how important it is to record this sale before year end, don’t you?”“Doing it this way is common for all companies in our business, so don’t worry!”“Trust me, the inventory is at the warehouse.”This problem can form the basis of an introductory discussion of the entire field of management accounting.1. The focus of management accounting is on helping internal users tomake better decisions, whereas the focus of financial accounting ison helping external users to make better decisions. Managementaccounting helps in making a host of decisions, including pricing,product choices, investments in equipment, making or buying goods and services, and manager rewards.2. Generally accepted accounting standards or principles affect bothinternal and external accounting. However, change in internalaccounting is not inhibited by generally accepted principles. Forexample, if an organization wants to account for assets on the basisof replacement costs for internal purposes, no outside agency canprohibit such accounting. Of course, this means that organizationsmay have to keep more than one set of records. There is nothingimmoral or unethical about having multiple sets of books, but theyareexpensive. Accounting data are commodities, just like butter or eggs.Innovations in internal accounting systems must meet the samecost-benefit tests that other commodities endure. That is, theirperceived increases in benefits must exceed their perceivedincreases in costs. Ultimately, benefits are measured by whetherbetter decisions are forthcoming in the form of increased net profitsor cost savings.3. Budgets, the formal expressions of management plans, are a majorfeature of management accounting, whereas they are not asprominent in financial accounting. Budgets are major devices forcompelling and disciplining management planning.4. An important use of management accounting information is theevaluation of performance, which often takes the form of comparisonof actual results against budgets, providing incentives and feedback to improve future decisions.5.Accounting systems have an enormous influence on the behavior ofindividuals affected by them. Management accounting is moreconcerned with the likely behavioral effects of various accountingalternatives that may be adopted than is financial accounting.1-38(10 min.)The main point of this question is that cost information is crucial for decisions regarding which products and services should be emphasized or de-emphasized. The incentives to measure costs precisely are far greater when flat fees are being received instead of reimbursements of costs.Note, too, that nonprofit organizations and profit-seeking organizations have similar desires regarding management accounting. Accountability is now in fashion for many purposes, including justification of prices, cost control, and response to criticisms by investors (whether they be donors, taxpayers, or others).When somebody's money is at stake, accounting systems get much love and attention. In a survey of 550 hospitals, hospital financial executives said that improved cost accounting systems "are crucial to responding to changes in hospital payment mechanisms and that better cost information is essential for more profitable and efficient operations." Hospitals will increasingly identify costs by product (type of case), not just by departments.1-39 (10 min.)Paperwork and systems often seem to become ends in themselves. However, the rationale that should underlie systems design is the cost-benefit philosophy or approach that is implied in the quotation. The aim is to get the managers and their subordinates collectively to make better decisions under one system versus another system -- for a given level of costs.Marks & Spencer should look at each of the management accounting reports it produces with an eye toward how it helps managers make better decisions. Does it provide needed scorekeeping? Does it direct attention to aspects of operations that might need altering? Does it provide information for specific management decisions? These types of questions will help identify the benefit of the information in the report.Then the company must consider the cost – not just the cost of collecting the data and preparing the reports, but the cost of educating managers to use the information and the cost of the time to read, digest, and act on the information. Too much information may be costly because it makes it time-consuming (and thus costly) to sift through the reams of information to find the few items that are important. And one cost may be the loss of important information because the total volume of information makes it too difficult to ferret out the important items.1-40(10 min.) Financial information is important in all companies. But how managers get and use financial information can differ depending on the culture and philosophies of the company.Top executives of a company often represent a functional area that is critical to the comparative economic advantage of the company. If technology is crucial, engineers generally hold important executive positions. If marketing differentiates the company from others, marketing executive s usually dominate. But regardless of the source of a company’s competitive advantage, its success will eventually be measured in economic terms. They must attend to financial aspects to thrive and often even to survive.Management accountants must work with the dominant managers in any organization. The modern trend toward use of cross-functional teams places management accountants at the center of the action regardless of what type of managers and executives dominate. Most companies realize that there is a financial dimension to almost every major decision, so they want the financial experts, management accountants, involved in the decisions. But to be accepted as an important part of these teams, the management accountants must know how to help managers in various functional areas. In General Mills, if accountants can’t talk the language of marketing, they will not have great influence. In ArvinMeritor, if they do not understand the information needs of engineers they will not provide value.1-41(10-15 min.)1. Boeing's competitive environment and manufacturing processeschanged greatly during the 1990s. An accounting system that served them well in their old environment would not necessarily be optimal in the 2000s. Boeing's management probably thought that changes in the accounting system were necessary to produce the kind of information necessary to remain competitive.2. A cost-benefit criterion was probably used. Boeing's management maynot have quantified the costs and the benefits, but they certainlyassessed whether the new system would help decisions enough towarrant the cost of the system.Many of the benefits of a better accounting system are hard to measure.They affect many strategic decisions of an organization. Withoutaccurate product costs, management will find it difficult to assess the consequences of their decisions. An accurate accounting system will help to price airplanes and other products competitively.3. More accurate product costs will usually result in better managementdecisions. But if the cost of the accounting system that produces the more accurate costs is too high, it may be best to forego the increased accuracy. The benefit of better decisions must exceed the added cost of the system for a change to be desirable.1-42(10 min.)1. There are many possible activities for each function of Nike's valuechain. Some possibilities are:Research and development -- Determining changes in customers'tastes and preferences for shoes and sportswear to come up withnew products (maybe the next "Air Jordans").Product and service process design -- Design a shoe to meet theincreasing demands of competitive athletes.Production -- Determine where to produce products and negotiatecontracts with the companies producing them.Marketing -- Signing prominent athletes to endorse Nike's products.Distribution -- Select the best locations for warehouses fordistribution to retail outlets.Customer service -- Formulate return policies for products thatcustomers perceive to be defective.2. Accounting information that aids managers' decisions includes:Research and development -- Trends in sales for various products, to determine which are becoming more and less popular.Product and service process design -- Production costs of variousshoe designs.Production -- Measure total costs, including both purchase cost and transportation costs, for production in various parts of the world.Marketing -- The added profits generated by the added sales due toproduct endorsements.Distribution -- Storage and shipping costs for different alternativewarehouse locations.Customer service -- The net cost of returned merchandise, to becompared with the benefits of better customer relations.。

财务会计Managerial Accounting-CN

提取。

• 现金等价物是期限少于三个月的短期、高流动性的金融工具;它们可 以迅速转换成现金。

• 公司的现金流分为三类:经营、投资和融资。

• 经营活动通常涉及向顾客提供商品和服务有关的交易。它们反映了 损益表上的典型和经常性交易的现金流影响。经营现金流入,比如 说:客户的收入和从投资中获得的利息和股息。营运现金流出包括支 付给员工和供应商的款项以及利息和税金。

Section 2 Cash flow Statement

第二节 现金流量表

• 请记住,应计利润(来自损益表的净收入)并不一定反映现金流。 许多收入和支出交易没有直接的现金流效应。

• 现金流量表提供了关于公司流动资产和财务灵活性的信息(通过改变 现金流的数量和时间来应对意外事件的能力)。

• 现金及现金等价物

• 投资活动通常涉及收购和处置非流动资产产生的现金流。现金流出 产生于购买(投资)房地产、厂房和设备、发放贷款和收购其他公

司的投资。现金流入来自于处置财产、厂房和设备;收取贷款(利

息除外);以及出售投资。

• 融资活动包括获得和偿还融资产生的现金流。现金流入来自所有者 的出资(向股东发行股票以换取现金)和贷款。现金流出产生于支

资本

提款

收入

支出

借记

贷记

借记

贷记

贷记Biblioteka 借记借记贷记

(千美元)

净销售额 销售成本 毛利 销售,一般费用及行政费用 营业收入 其他收入 利息支出 所得税前收入 所得税准备金 净收入

Altron公司 损益表

截至2019年1月3日年度

会计学原理(英文)

《会计学原理(英文)》教学大纲王燕祥编写工商管理专业课程教学大纲610 目录Chapter 1 Accounting in Action 第一章会计实践活动 (613)学习目标 (613)Teaching and homework hours 教学与作业时间 (613)Reading and References 学生必读和参考书目 (613)Chapter 2 The Recording Process 第二章记录过程 (615)学习目标 (615)Teaching and homework hours 教学与作业时间 (615)Reading and References 学生必读和参考书目 (615)Chapter 3 Adjusting the Accounts 第三章调整账户 (617)学习目标 (617)Teaching and homework hours 教学与作业时间 (617)Reading and References 学生必读和参考书目 (617)Chapter 4 Completion of the Accounting Cycle 第四章完成会计循环 (619)学习目标 (619)Teaching and homework hours 教学与作业时间 (619)Reading and References 学生必读和参考书目 (619)Chapter 5 Accounting for Merchandising Operations 第五章商品经营活动的会计核算 (621)学习目标 (621)Teaching and homework hours 教学与作业时间 (621)Reading and References 学生必读和参考书目 (621)Chapter 6 Inventories 第六章存货 (623)学习目标 (623)Teaching and homework hours 教学与作业时间 (624)Reading and References 学生必读和参考书目 (624)Chapter 7 Accounting Information Systems 第七章会计信息系统 (626)学习目标 (626)Teaching and homework hours 教学与作业时间 (626)Reading and References 学生必读和参考书目 (626)Chapter 8 Internal Control and Cash 第八章内部控制和现金 (628)学习目标 (628)Teaching and homework hours 教学与作业时间 (628)Reading and References 学生必读和参考书目 (628)Chapter 9 Accounting for Receivables 第九章应收款项的会计核算 (630)学习目标 (630)Teaching and homework hours 教学与作业时间 (630)Reading and References 学生必读和参考书目 (630)Chapter 10 Plant Assets, Natural Resources, and Intangible Assets 第十章厂场资产、自然资源和无形资产 (632)会计学原理(英文)学习目标 (632)Teaching and homework hours 教学与作业时间 (632)Reading and References 学生必读和参考书目 (633)Chapter 11 Current Liabilities and Payroll Accounting 第十一章流动负债和工资的核算 (634)学习目标 (634)Teaching and homework hours 教学与作业时间 (634)Reading and References 学生必读和参考书目 (634)Chapter 12 Accounting Principles 第十二章会计原则 (636)学习目标 (636)Teaching and homework hours 教学与作业时间 (636)Reading and References 学生必读和参考书目 (636)Chapter 13 Accounting for Partnerships 第十三章合伙企业的会计核算 (638)学习目标 (638)Teaching and homework hours 教学与作业时间 (638)Reading and References 学生必读和参考书目 (638)Chapter 14 Corporations: Organization and Capital Stock Transactions 第十四章公司:组织和股本交易 (640)学习目标 (640)Teaching and homework hours 教学与作业时间 (640)Reading and References 学生必读和参考书目 (640)Chapter 15 Corporations: Dividends, Retained Earnings, and Income Reporting 第十五章股利、保留盈余和收益报告 (642)学习目标 (642)Teaching and homework hours 教学与作业时间 (642)Reading and References 学生必读和参考书目 (642)Chapter 16 Long-Term Liabilities 第十六章长期负债 (644)学习目标 (644)Teaching and homework hours 教学与作业时间 (644)Reading and References 学生必读和参考书目 (644)Chapter 17 Investments 第十七章投资 (646)学习目标 (646)Teaching and homework hours 教学与作业时间 (646)Reading and References 学生必读和参考书目 (646)Chapter 18 The Statement of Cash Flows 第十八章现金流量表 (648)学习目标 (648)Teaching and homework hours 教学与作业时间 (648)Reading and References 学生必读和参考书目 (648)Chapter 19 Financial Statement Analysis 第十九章财务报表分析 (650)学习目标 (650)Teaching and homework hours 教学与作业时间 (650)Reading and References 学生必读和参考书目 (650)Chapter 20 Managerial Accounting 第二十章管理会计 (652)611工商管理专业课程教学大纲612 学习目标 (652)Teaching and homework hours 教学与作业时间 (652)Reading and References 学生必读和参考书目 (652)Chapter 21 Job Order Cost Accounting 第二十一章分批成本法 (654)学习目标 (654)Teaching and homework hours 教学与作业时间 (654)Reading and References 学生必读和参考书目 (654)Chapter 22 Process Cost Accounting 第二十二章分步成本法 (656)学习目标 (656)Teaching and homework hours 教学与作业时间 (656)Reading and References 学生必读和参考书目 (657)Chapter 23 Cost-V olume-Profit Relationships 第二十三章本量利分析 (658)学习目标 (658)Teaching and homework hours 教学与作业时间 (658)Reading and References 学生必读和参考书目 (659)Chapter 24 Budgetary Planning 第二十四章编制预算 (660)学习目标 (660)Teaching and homework hours 教学与作业时间 (660)Reading and References 学生必读和参考书目 (660)Chapter 25 Budgetary Control and Responsibility Accounting 第二十五章预算控制和责任会计 662 学习目标 (662)Teaching and homework hours 教学与作业时间 (662)Reading and References 学生必读和参考书目 (662)Chapter 26 Performance Evaluation through Standard Costs 第二十六章利用标准成本进行业绩评价 (664)学习目标 (664)Teaching and homework hours 教学与作业时间 (664)Reading and References 学生必读和参考书目 (664)Chapter 27 Incremental Analysis and Capital Budgeting 第二十七章增量分析和资本预算 (666)学习目标 (666)Teaching and homework hours 教学与作业时间 (667)Reading and References 学生必读和参考书目 (667)会计学原理(英文)Chapter 1 Accounting in Action第一章会计实践活动STUDY OBJECTIVESAfter studying this chapter you should be able to:1.Explain what accounting is.2.IDENTIFY THE USERS AND USES OF ACCOUNTING.3.UNDERSTAND WHY ETHICS IS A FUNDAMENTAL BUSINESS CONCEPT.4.EXPLAIN THE MEANING OF GENERALLY ACCEPTED ACCOUNTING PRINCIPLESAND THE COST PRINCIPLE.5.EXPLAIN THE MEANING OF THE MONETARY UNIT ASSUMPTION AND THE ECONOMIC ENTITY ASSUMPTION.6.STATE THE BASIC ACCOUNTING EQUATION AND EXPLAIN THE MEANING OF ASSETS, LIABILITIES, AND OWNER’S EQUITY.7.ANALYZE THE EFFECT OF BUSINESS TRANSACTIONS ON THE BASIC ACCOUNTING EQUATION.8.Understand what the four financial statements are and how they are prepared.学习目标学完本章之后,学生应该能够达到以下目标:1.解释什么是会计。

11ManagerialAccounting-Student_财务管理_经管-文档资料

Quantity Variance

Difference between actual quantity and standard quantity

Price Variance

Difference between actual price and standard price

11-12

Quantity and Price Standards

Price Variance

Materials price variance Labor rate variance VOH rate variance

11-14

A General Model for Variance Analysis

(1) Standard Quantity Allowed for Actual Output, at Standard Price

Setting Direct Materials Standards

Standard Price per Unit

Standard Quantity per Unit

Final, delivered cost of materials, net of discounts.

Summarized in a Bill of Materials.

Amount

Direct Labor

Direct Material

Standard

Manufacturing Overhead

Type of Product Cost

11-4

Variance Analysis Cycle

11-5

Setting Standard Costs

Should we use ideal standards that require employees to work at 100 percent

10ManagerialAccounting-Student_财务管理_经管-PPT文档资料

10-14

How a Flexible Budget Works

To

a budget, we need to know that:

Total variable costs change in direct proportion to changes in activity.

Total fixed costs remain

10-33

Performance Reports in Non-Profit Organizations

Non-profit organizations may receive funding from sources other than the sale of goods and services, so

F = Favorable variance that occurs when actual costs are less than budgeted costs.

10-11

Deficiencies of the Static Planning Budget

Larry’s Actual Results Compared with the Planning Budget

50 lawns × $75 per lawn

50 lawns × $30 per lawn

10-32

A Performance Report Combining Activity and Revenue and Spending Variances

$43,000 actual - $41,250 budget

Performance evaluation is difficult when actual activity

Managerial Accounting Study Guide

Managerial Accounting Study GuideDisclaimer: This guide does not include all the material that will be covered on the exam. However, the listed items will direct your attention to the main ideas that will be the source for multiple-choice questions. Some of the multiple choice questions may take the form of small calculation problems.Chapter 1:1. Managerial accounting reports provide decision-making information for internal users. The reports need not follow GAAP, and the reports often focus on the future.2. The controller is the top management accountant in a company.3. Under Total Quality Management, a business strives to improve performance in conjunction with goal setting.Chapter 2:1. Manufacturing or product costs have three components: direct materials, direct labor, and manufacturing overhead. Know what it included in each component.2. Direct costs are costs that can be traced conveniently and economically to a cost object. Indirect costs are not traced directly to a certain cost object.3. Selling and general/administration costs are nonmanufacturing or period costs that are reported on the Income Statement. These costs are used to generate revenues during the current period.4. A manufacturer has three inventory accounts: Raw Materials, Work-in-Process, and Finished Goods. These inventory accounts are assets that are reported on the Balance Sheet.5. A cost object is any product, service, or department which receives allocated costs to determine its cost.6. Sunk costs are past costs that are not relevant for present decision-making purposes.7. The cost of goods manufacturing is the cost of the items that are completed and transferred to Finished Goods during a period.8. Review the cost of goods manufactured formula on page 65 and the cost of goods formula on page 63.Chapter 3:1. There are two basic product-costing systems: job order costing and process costing.2. A job order costing system is used by a manufacturer who produces unique or special-order products.3. Process costing system is used by a manufacturer in a continuous flow or assembly line environment.4. Product costs flow from Raw Materials to Work-in-Process to Finished Goods to Cost of Goods Sold.5. Direct material costs, direct labor costs, and manufacturing overhead costs are added toa Work-in-Process account during production.6. A job order cost card is used in a job order costing system to record the direct materials, direct labor, and overhead costs associated with a specific job. The product unit cost is the total job cost divided by the number of units produced.7. Overhead is allocated or assigned or applied to jobs using an estimated overhead allocation rate.8. Most companies prepare an estimated allocation rate. This estimated overhead allocation rate is called the predetermined overhead rate. It is usually calculated for a year’s time period.9. Predetermined Overhead Rate = Estimated Factory Overhead/Estimated Allocation Base.10. The selected allocation base should be associated with the overhead costs. Common allocation bases are direct labor hours, direct labor costs, and machine hours.11. Usually, the amount of applied overhead will not equal the actual overhead at the end of the year since the applied overhead is based on estimates.12. If the applied overhead is greater than the actual overhead, the difference is called overapplied overhead. If the actual overhead is larger, the difference is called underapplied overhead.18. A just-in-time (JIT) manufacturing system works to reduce the inventory levels of a manufacturer.Chapter 4:1. Cost allocation is the process of assigning indirect costs.2. A cost pool is the total of costs that is allocated by an allocation base (activity driver). The individual costs in a cost pool should be similar or homogeneous.3. An allocation rate is calculated by dividing the budgeted cost pool by the estimated activity driver rate (allocation base). The allocated cost is determined by multiplying the actual usage of the allocation base by the allocation rate.4. Traditional cost allocation systems have used one or two cost pools that have used production volume allocation bases.5. Since the traditional cost allocation systems have used few pools and production bases, product prices are often not accurate.6. Activity-based costing uses many cost pools with different allocation bases. The cost pool rate is the pool costs divided by the cost driver (activity or allocation base).7. When an activity-based costing system is implemented, the accuracy of costing is improved. Usually, the costs of high volume products decrease while the costs of low volume products increase.Chapter 5:1. A process costing system does not use job cost cards.2. In a process cost system, the product costs flow through multiple departments3. Direct materials, direct labor, and overhead costs for each department are accumulated in that department's Work-in-Process account.4. Costs flow from one department’s Work-in-Process account to the next department’s Work-in-Process account. These costs are called transferred-in costs.5. Conversion costs include direct labor and manufacturing overhead costs.6. A process costing system uses equivalent units to calculate an average unit cost.7. Equivalent units measure production in terms of whole units. Know how to calculate equivalent units.8. A production cost report provides information summarizing the units for which departments are accountable and the costs charged to the departments. In particular, it reconciles the units and the costs and calculates cost per equivalent unit.Chapter 6:1. Variable costs are costs that change in total with the level of business activity. The variable cost per unit remains constant.2. Fixed costs are costs that do not change in total with the level of business activity. However, the fixed cost per unit varies inversely with changes in the level of business activity.3. Mixed costs contain both fixed and variable cost components.4. The high-low method can be used to estimate the variable and fixed costs in a mixed cost.5. Full costing (absorption costing) is required by GAAP. Direct labor, direct materials, variable manufacturing overhead, and fixed manufacturing overhead are included in the cost of inventory.6. Variable costing is used internally for decision-making purposes. Direct labor, direct materials, and variable manufacturing overhead are included in the inventory costs.7. The treatment of fixed manufacturing overhead is the only difference between full and variable costing. Fixed manufacturing overhead is an expense on the income statement in the period incurred under variable costing.8. When the units produced equals the units sold, the net income under full costing equals the net income under variable costing.9. When the units produced are greater than the units sold, the net income under full costing is greater than the net income under variable costing.10. When the units produced are less than the units sold, the net income under full costing is less than the net income under variable costing.11. A variable costing income statement reports the contribution margin. A full costing income statement reports the gross margin.12. The full costing method can be used by managers to manipulate performance results. Chapter 7:1. The break-even point is the number of units that must be sold or amount of sales revenue that must generated to have no profit or no loss. In other words, the net income is zero.2. The profit equation is: Profit = Sales less Total Variable Costs less Total Fixed Costs.3. The margin of safety is the difference between the expected sales and the break-even sales.4. The contribution margin per unit is equal to the sales price per unit less the variable costs per unit.5. The breakeven in units is equal to the Total Fixed Costs divided by the contribution margin in units. Know how to calculate the breakeven point.6. The required number of units that must be sold in order to achieve a specified profit level (operating income) is equal to the sum of the Total Fixed Costs plus the Operating Income (Profit Level) divided by the contribution margin in units. Know how to calculate the sales in units to achieve a desired profit level.7. An increase in fixed costs or variable costs will increase the break-even point. An increase in sales price will decrease the break-even point.8. Operating leverage refers to the cost structure of the business. A business with high percentage of fixed costs is considered to have a high operating leverage.Chapter 8:1. Decision making is based on incremental analysis which investigates incremental revenues and incremental costs. Incremental costs are often called differential costs or relevant costs.2. Incremental analysis investigates the differences in revenues and costs for different decision alternatives.3. Sunk costs are not relevant in the decision-making process. Avoidable costs are relevant costs in the decision-making process.4. Opportunity costs are the benefits that are lost when one alternative is chosen over another alternative.5. Common costs are costs that are not directly traceable to a product line or department. Instead, these costs are allocated to the individual product lines or departments. If one product line or department is dropped, the common costs are allocated to the remaining product lines or departments.6. A product line should be dropped only when the total net income of a business will increase if the product line is eliminated. Usually the product line should be retained if contribution margin is greater than the avoidable costs (cost savings).7. Products should be processed further when the incremental revenue from the additional processing is greater than the additional costs of the additional processing. The joint costs are sunk costs in an additional processing decision.8. When there is a resource constraint, a business should strive for the highest contribution margin per unit of the constraint.9. A supplier or vendor is paid for the cost of production plus a fixed amount (or percentage of cost) under a cost-plus contract.Chapter 9:1. A budget is a formal document that outlines a financial plan for achieving goals. A business is not required to prepare budgets.2. Budgets are used to increase communication and coordination and to evaluate performance.3. When budgets are prepared using zero-based budgeting, all budgeted amounts are justified for each budget period.4. The master budget is a collection budgets such the sales budget, the production budget, and the direct materials budget.5. The sales or revenue budget is the first budget prepared in the master budget sequence.6. For a manufacturer, the production budget is the second budget prepared. Productionin units is equal to the budgeted sales in units plus the desired ending inventory in units less the beginning inventory in units. Know how to calculate a production budget.7. After the production budget is prepared, direct materials and direct labor budgets are prepared. Know how to calculate direct materials purchases and direct labor requirements.8. Cash collections (receipts) and cash payments (disbursements) budgets provide information for determining the cash balance, the amount of excess cash for investment, and the amount of cash available for capital acquisitions. Know how to calculate cash receipts from sales and cash disbursements for purchases.9. A budget variance is the difference between the budgeted and actual amount.Chapter 10:1. A decentralized business gives decision-making authority to the mangers of its subunits.2. Two advantages of decentralization are better information at the manager level and quicker response time at the manager level. Additionally, decentralization motivates and trains managers.3. Two disadvantages of decentralization are a duplication of activities at the different subunits and a lack of goal congruence.4. Under responsibility accounting, managers are responsible for the revenues and costs that are under their control. A manager should be accountable for only controllable costs.5. The subunits of a business often are referred to as responsibility centers. Three common responsibility centers are cost centers, profit centers, and investment centers.6. A manager of a cost center is responsible for controlling costs in that subunit. A manager of a profit center is responsible for generating revenues and controlling costs. A manager of an investment center is responsible for investing assets, generating revenues, and controlling costs.7. The return on investment (ROI) is used to evaluate the performance of investment centers. ROI is a better than income as a performance measure for an investment center because it compares the amount of income to the amount of investment.8. However, ROI evaluation can lead to underinvestment when managers reject projects that have returns greater than the required return but that will lower the ROI. Evaluation in terms of profit can lead to overinvestment.9. ROI is income divided by total assets (invested capital). Know how to calculate ROI.10. ROI can be separated into a sales margin component and capital (investment) turnover component.11. Sales margin is income divided by sales. Know how to calculate profit margin.12. Capital (Investment) turnover is sales divided by total assets (invested capital). Know how to calculate the capital turnover.13. Residual income is the net operating income less the required profit.Know how to calculate residual income.14. The balanced scorecard is another method to evaluate performance. The balanced scorecard considers financial, customer, internal process and growth measures.15. Flexible budgets can be adjusted for various activity or production levels16. Managers use the principle of management by exception to investigate the difference between projected results and actual results. Under management by exception, minor differences are not investigated.Chapter 11:1. Standards are costs that a business sets as goals. Standards can be set for direct materials, direct labor, and manufacturing overhead.2. Attainable standards are goals that can be reached with reasonable effort. Attainable standards are not set on perfect performance.3. A budgeted cost can be calculated by multiplying the standard cost by the number of budgeted units.4. Generally, manufacturers set standards for price and quantity for direct materials andfor rate and efficiency for direct labor.5. Cost variances are the difference between the standard cost and the actual cost.6. If the actual cost is greater than the standard cost, the variance is unfavorable. If the actual cost is less than the standard cost, the variance is favorable.7. A volume variance results from an actual production that is different from the estimated production level.8. Different departments have responsibility for the different variances. For example, the Purchasing Department usually would be responsible for the direct materials price variance.Chapter 12:1. Capital expenditures decisions also are called capital budgeting decisions or capital investment decisions. These decisions involve the acquisition of long-term assets.2. Both the net present value method and the internal rate of return method use the time value of money in the evaluation of capital investments.3. The net present value method is the sum of the present values of the cash inflows and cash outflows from an investment.4. A positive net present value indicates that the rate of return is greater than the required rate of required.5. The internal rate of return is the rate of return that results in a net present value of zero.6. If the internal rate of return is greater than the required rate of return (the cost of capital), the investment should be accepted.7. The payback period is the length of time needed to recover the cost of an investment. Know how to calculate the payback period8. The payback method does not use the time value of money and does not consider cash flows after the payback date.Chapter 14:1. Financial statement analysis provides information for decision-making. The information can be used to control operations, to assess the appearance of the company toinvestors or creditors, and to assess the financial condition of vendors, customers, and business partners.2. The Balance Sheet reports assets, liabilities, and owners’ equity. The Income Statement reports revenues and expenses. The Statement of Cash Flows reports cash inflows and outflows from operating, investing, and financing activities.3. Horizontal analysis computes the change in each financial statement item both indollar amount and percentage change. Using comparative financial statements, the amount of change is divided by the base year amount to determine the percentage change.4. Vertical Analysis highlights the relationship between the items on a financial statement on a percentage basis. On the balance sheet, total assets (or total stockholders' equity and liabilities) are set at 100%. Net sales or net revenue is set at 100% on the income statement. All items on a statement are divided by the 100% standard for that statement. Thus, a common-size statement is produced.5. Earnings per share is a profitability ratio. Earnings per share is calculated by dividing the net income less preferred dividends by the number of shares of outstanding common Stock6. Another profitability ratio, the price-earnings ratio, is the multiple of earnings that an investor pays for the stock. Earnings per share is calculated by dividing the market price per share divided by the earnings per share.7. Gross profit (gross margin) is equal to net sales less the cost of goods sold. The gross profit (gross margin) percentage is equal to gross profit (gross margin) divided by net sales.8. Turnover ratios are used to evaluate how efficiently assets are used. A higher number indicates a faster turnover and more efficiency.9. The accounts receivable turnover is determined by dividing net credit sales by average accounts receivable and the inventory turnover is determined by dividing cost of goods sold by average inventory.10. The current ratio, the quick ratio, and the debt-to-equity ratio are all debt related ratios that indicate the financing structure of the business and its ability to pays its debts. 11. The current ratio is equal to current assets divided by current liabilities.。

《管理会计(双语)》教学大纲

《管理会计(双语)》课程教学大纲课程编码:12120203k206课程性质:专业必修课学分:3课时:48开课学期:第五学期适用专业:会计学一、课程简介《管理会计(双语》是会计学专业(本科)的一门必修课程。

是以现代企业所处的社会经济环境为背景,明确阐明以企业为主体,密切联系现代会计的预测、决策、规划、控制、考核评价等职能,系统地介绍了现代管理会计的基本理论、基本方法和实用操作技术。

课程分为三部分,第一部分主要交代了管理会计的基本原理和传统管理会计的基本方法;第二部分主要分别讨论管理会计各项职能在实践中的应用程序与具体操作方法。

第三部分集中介绍管理会计发展的新领域。

管理会计是一门理论性较强、计算内容较多的课程。

通过该门课程的学习,使学生领会管理会计的精髓,掌握管理会计的基本理论和基本方法,学会各种分析方法的应用技能和技巧,不断提高学生分析问题和解决问题的能力。

二、教学目标课程总体目标:通过本课程教学,掌握管理会计的基本理论和基本分析方法,结合相应的实践教学,培养学生能独立开展各项管理会计工作的能力。

具体入下:1.了解管理会计的产生与发展,明确管理会计的特点、职能、内容和任务;2.掌握成本习性与变动成本法、本量利分析等管理会计基础分析方法,并了解方法的一般原理;3.掌握短期经营决策分析、长期投资决策分析、全面预算、标准成本控制、责任会计等内容的基本理论与方法。

三、教学内容(一)Chapter 1 Managerial Accounting Concepts and PrinciplesThe main content: Chapter 1 introduces students to managerial accounting and the manufacturing process. Students will learn how managerial accounting is used in the management decision process. They will also be exposed to the terminology used to describe costs related to manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe managerial accounting and the role of managerial accounting in a business.2. Define and illustrate the following costs: 1. direct and indirect costs, 2. direct materials,direct labor, and factory overhead costs, 3. product and period costs.3. Describe and illustrate the following statements for a manufacturing business: 1.balance sheet, 2. statement of cost of goods manufactured, 3. income statement.4. Describe the uses of managerial accounting information.Some key points: direct and indirect costs, direct materials, direct labor, factory overhead costs, product and period costs; cost of goods manufactured.Teaching methods: use of multimedia tools. We ad opt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(二)Chapter 2Job Order CostingThe main content:Chapter 2 introduces students to managerial job order cost systems. Students will be exposed to the terminology used to describe costs related to manufacturing. The first of two basic manufacturing accounting systems, job order, is described in this chapter. Students learn how costs flow through a manufacturing system and the basis for determining product costs under job order costing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe cost accounting systems used by manufacturing businesses.2. Describe and illustrate a job order cost accounting system.3. Describe the use of job order cost information for decision making.4. Describe the flow of costs for a service business that uses a job order cost accountingsystem.Some key points: Job Order Cost System; Overapplied Factory Overhead; Underapplied Factory Overhead; predetermined overhead rate;Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is suppl emented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(三)Chapter 3Process Cost SystemsThe main content:Chapter 3 completes the coverage of manufacturing accounting by introducing process costing. The text demonstrates process costing under the FIFO method.The average cost method is presented in th e chapter’s appendix. Chapter 3 also discusses the impact of just-in-time systems on manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe process cost systems.2. Prepare a cost of production report.3. Journalize entries for transactions using a process cost system.4. Describe and illustrate the use of cost of production reports for decision making.5. Compare just-in-time processing with traditional manufacturing processing.Some key points: Process Cost System; First-in, First-out (FIFO) Method; Cost of Production Report; Just-in-Time (JIT) Processing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(四)Chapter 4 Cost Behavior and Cost-Volume-Profit AnalysisThe main content: In Chapter 4, students learn how to conduct cost-volume-profit analysis. In preparation for this activity, the chapter discusses variable, fixed, and mixed costs.Learning Objectives:After studying the chapter, your students should be able to:1. Classify costs as variable costs, fixed costs, or mixed costs.2. Compute the contribution margin, the contribution margin ratio, and the unitcontribution margin.3. Determine the break-even point and sales necessary to achieve a target profit.4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-evenpoint and sales necessary to achieve a target profit.5. Compute the break-even point for a company selling more than one product, theoperating leverage, and the margin of safety.Some key points:variable costs; fixed costs; mixed costs; High-Low Method; Contribution Margin; Cost-Volume-Profit Analysis; Contribution Margin Ratio; Unit Contribution Margin.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(五)Chapter 5 BudgetingThe main content: Chapter 5 emphasizes accounting activities that help managers plan, direct, and control the operations of a business. Budgeting is used to establish business goals in the planning function. Budgets help guide managers’ operational decisions. Budgets are also used to control operations as actual results are compared to the budgeted results.Learning Objectives:After studying the chapter, your students should be able to:1. Describe budgeting, its objectives, and its impact on human behavior.2. Describe the basic elements of the budget process, the two major types of budgeting,and the use of computers in budgeting.3. Describe the master budget for a manufacturing company.4. Prepare the basic income statement budgets for a manufacturing company.5. Prepare balance sheet budgets for a manufacturing company.Some key points: Goal Conflict;Budgetary Slack;Continuous Budgeting;Static Budget;Flexible Budget;Zero-Based Budgeting;Capital Expenditures Budget.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(六)Chapter 6 Performance Evaluation Using Variances from Standard Costs The main content: Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to produce its product. Deviations from these standards are reported as variances.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the types of standards and how they are established.2. Describe and illustrate how standards are used in budgeting.3. Compute and interpret direct materials and direct labor variances.4. Compute and interpret factory overhead controllable and volume variances.5. Journalize the entries for recording standards in the accounts and prepare an incomestatement that includes variances from standard.6. Describe and provide examples of nonfinancial performance measures.Some key points: Direct Labor Rate Variance ;Direct Materials Price Variance;Direct Labor Time Variance;Direct Materials Quantity Variance;Budgeted Variable Factory Overhead;Factory Overhead Cost Variance Report;Controllable Variance;Volume Variance.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(七)Chapter 7 Performance Evaluation for Decentralized Operations The main content: Chapter 7 applies responsibility accounting to cost, profit, and investment centers. The chapter demonstrates the responsibility accounting reports that are used to evaluate department or division performance. This provides an excellent opportunity to remind your students that managers are judged, at least in part, using accounting data.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the advantages and disadvantages of decentralized operations.2. Prepare a responsibility accounting report for a cost center.3. Prepare responsibility accounting reports for a profit center.4. Compute and interpret the rate of return on investment, the residual income, and thebalanced scorecard for an investment center.5. Describe and illustrate how the market price, negotiated price, and cost priceapproaches to transfer pricing may be used by decentralized segments of a business.Some key points:Responsibility Accounting;Balanced Scorecard;Profit Margin;DuPont Formula;Rate of Return on Investment (ROI);Investment Center ;Residual Income;Investment TurnoverTeaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(八)Chapter 8 Differential Analysis, Product Pricing, and Activity-Based Costing The main content: This chapter covers (1) differential analysis, (2) methods of determining the selling price of a product using a cost-plus markup approach, (3) the effects of production bottlenecks, and (4) activity-based costing. The cost-plus approach of product cost is described in Objective 2; total cost and variable cost methods are presented in thechapter appendix. All topics in this chapter are able to stand alone. Therefore, the instructor is free to cover only one or two of the topics if class time is a limited resource as the term draws to a close.Learning Objectives:After studying the chapter, your students should be able to:1. Prepare differential analysis reports for a variety of managerial decisions.2. Determine the selling price of a product, using the product cost concept.3. Compute the relative profitability of products in bottleneck production processes.4. Allocate product costs using activity-based costing.Some key points:Product Cost Concept ; Target Costing; Production Bottleneck; Theory of Constraints (TOC); Activity-Based Costing (ABC).Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(九)Chapter 9 Capital Investment AnalysisThe main content: Capital investment analysis is a topic that usually receives detailed coverage in introductory finance courses and/or intermediate accounting. The purpose of this chapter is to give students a brief introduction to the basics of capital investment analysis using the following methods: average rate of return, cash payback, net present value, and internal rate of return.Learning Objectives:After studying the chapter, your students should be able to:1. Explain the nature and importance of capital investment analysis.2. Evaluate capital investment proposals using the average rate of return and cashpayback methods.3. Evaluate capital investment proposals using the net present value and internal rate ofreturn methods.4. List and describe factors that complicate capital investment analysis.5. Diagram the capital rationing process.Some key points: Capital Investment Analysis;Time Value of Money Concept;Average Rate of Return;Cash Payback Period;Internal Rate of Return (IRR) Method;Capital Rationing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.四、整体课时分配五、实验教学1. 实验项目与课时分配3.实验报告The basic requirements of the experiment report, including: name of the experiment, purpose of the experiment, case data, case analysis, conclusions and enlightenment.六、课程考核与成绩评定1.考核方式:考查;笔试;闭卷。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。