会计英语之长期负债

会计英语科目介绍

会计英语科目介绍1. Introduction在学习会计的过程中,学习和掌握会计英语是非常重要的。

会计英语科目是会计领域的专业术语,有助于我们理解和运用相关会计概念。

本文将介绍一些常见的会计英语科目及其英文表达,帮助读者更好地理解和掌握会计英语。

2. Financial Accounting(财务会计)财务会计是指对一个组织的财务状况和经营成果进行记录、分析和报告的过程。

以下是一些与财务会计相关的会计英语科目:2.1 Assets(资产)•Cash(现金)•Accounts receivable(应收账款)•Inventory(存货)•Property, Plant, and Equipment(固定资产)2.2 Liabilities(负债)•Accounts payable(应付账款)•Notes payable(应付票据)•Long-term debt(长期负债)2.3 Equity(所有者权益)•Common stock(普通股)•Retned earnings(留存盈余)2.4 Revenue(收入)•Sales revenue(销售收入)•Service revenue(服务收入)2.5 Expenses(费用)•Cost of goods sold(销售成本)•Rent expense(租金支出)3. Managerial Accounting(管理会计)管理会计是指用于内部决策、规划和控制的会计信息。

以下是一些与管理会计相关的会计英语科目:3.1 Cost(成本)•Direct costs(直接成本)•Indirect costs(间接成本)•Fixed costs(固定成本)•Variable costs(变动成本)3.2 Budgeting(预算)•Operating budget(经营预算)•Capital budget(资本预算)3.3 Decision Making(决策)•Cost-volume-profit analysis(成本-销售-利润分析)•Break-even point(盈亏平衡点)3.4 Performance Evaluation(绩效评估)•Return on investment(投资回报率)•Balanced scorecard(平衡记分卡)4. Auditing(审计)审计是指对财务报表的真实性、完整性和准确性进行独立检查和评估的过程。

长期负债的意思-长期负债是什么意思

长期负债的意思|长期负债是什么意思基本解释长期负债(long-term liability of long-term debt)长期负债是会计分录的内容,是指期限超过1年的债务,1年内到期的长期负债在资产负债表中列入短期负债。

长期负债与流动负债相比,具有数额较大、偿还期限较长的特点。

因此,举借长期负债往往附有一定的条件,如需要企业指定某项资产作为还款的担保品,要求企业指定担保人。

设置偿债基金等,以保护债权人经济利益。

详细解释长期负债的偿还特点长期负债的偿还有以下几个特点:第一,保证长期负债得以偿还的基本前提是企业短期偿债能力较强,不至于破产清算。

所以,短期偿债能力是长期偿债能力的基础;第二,长期负债因为数额较大,其本金的偿还必须有一种积累的过程。

从长期来看,所有真实的报告收益应最终反映为企业的现金净流入,所以企业的长期偿债能力与企业的获利能力是密切相关的;第三,企业的长期负债数额大小关系到企业资本结构的合理性,所以对长期债务不仅要从偿债的角度考虑。

还要从保持资本结构合理性的角度来考虑。

保持良好的资本结构又能增强企业的偿债能力。

由过去的经济活动引起的,能以货币计量的,偿还期在1年或者超过1年的一个营业周期以上的经济义务。

常见的长期负债有长期借款、公司债券、住房基金和长期应付款等。

长期负债的分类长期负债可按不同的标志进行分类。

(1)根据筹集方式,可分为长期借款、公司债券、住房基金和长期应付款等;(2)按不同的偿还方式,可分为定期偿还的长期负债和分期偿还的长期负债;(3)按债务是否有低押长期负债,没有抵押品的称为信用借款。

长期负债的计价长期负债的计价,由于货币时间价值影响较大,其价值应是根据合同或契约在未来必须支付的本金和所有利息之和按适当的贴现率的折现值之和。

由于长期负债有多各类型,其计价方法也有所不同,如在公司债券情况下,议定的利息支付、到期日的偿付值及所有分期还本金额都应该折算成现值。

这里的贴现率在理论上有两种选择:一是现时证券市场上具有类似风险条件投资的收益率;另一个是债券发行日的市场收益率。

会计实用英语术语

会计实用英语术语概述会计是一门重要的商业领域,涉及到复杂的财务交易和报告。

在全球化的商业环境中,掌握会计实用英语术语是非常关键的。

本文将介绍一些常见的会计实用英语术语,帮助读者更好地理解和运用会计术语。

1. 资产和负债类术语1.1 资产 (Assets)资产是企业拥有的经济资源,能够为企业带来未来经济利益。

常见的资产类术语包括: - Current Assets:流动资产,如现金、应收账款等。

- Non-current Assets:非流动资产,如土地、房屋等固定资产。

- Intangible Assets:无形资产,如专利、商标等。

1.2 负债 (Liabilities)负债是企业为满足未来利益而欠他人的债务或义务。

常见的负债类术语包括: - Current Liabilities:流动负债,如应付账款、短期贷款等。

- Long-term Liabilities:长期负债,如债券、长期贷款等。

2. 收入和费用类术语2.1 收入 (Revenue)收入是企业在经营活动中获得的来自外部的经济利益。

常见的收入类术语包括: - Sales Revenue:销售收入。

- Service Revenue:服务收入。

2.2 费用 (Expense)费用是企业用于经营活动的成本支出。

常见的费用类术语包括: - Cost of Goods Sold:销售成本。

- Operating Expenses:营业费用。

3. 会计报表类术语3.1 资产负债表 (Balance Sheet)资产负债表是企业在特定日期的财务状况的总结报表。

常见的资产负债表类术语包括: - Assets = Liabilities + Equity:资产等于负债加所有者权益。

- Current Ratio:流动比率,用于衡量企业的偿债能力。

3.2 损益表 (Income Statement)损益表是企业在特定期间的经营活动结果的总结报表。

企业财务管理--长期负债(英文版)

Trustee

United Bank of Florida

Trustee is appointed to represent bondholders

Security

None

Bonds are unsecured debenture

Rating

Moody's A1, S&P A+ Bond credit quality rated upper medium grade by Moody's and S&P's rating

Coupon dates

6/30, 12/31

Coupons are paid semiannually

Offering price 100

Offer price is 100% of face value

Yield to maturity 10%

Based on stated offer price

20.2 The Public Issue of Bonds

❖ The general procedure is similar to the issuance of stock, chapter.

❖ Indentures and covenants are not relevant to stock issuance.

Protective Covenants

❖ Agreements to protect bondholders ❖ Negative covenant: Thou shalt not:

pay dividends beyond specified amount sell more senior debt & amount of new debt is

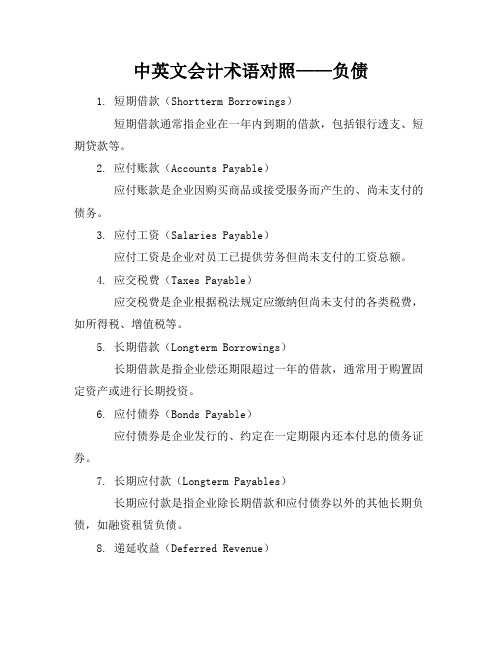

中英文会计术语对照——负债

中英文会计术语对照——负债1. 短期借款(Shortterm Borrowings)短期借款通常指企业在一年内到期的借款,包括银行透支、短期贷款等。

2. 应付账款(Accounts Payable)应付账款是企业因购买商品或接受服务而产生的、尚未支付的债务。

3. 应付工资(Salaries Payable)应付工资是企业对员工已提供劳务但尚未支付的工资总额。

4. 应交税费(Taxes Payable)应交税费是企业根据税法规定应缴纳但尚未支付的各类税费,如所得税、增值税等。

5. 长期借款(Longterm Borrowings)长期借款是指企业偿还期限超过一年的借款,通常用于购置固定资产或进行长期投资。

6. 应付债券(Bonds Payable)应付债券是企业发行的、约定在一定期限内还本付息的债务证券。

7. 长期应付款(Longterm Payables)长期应付款是指企业除长期借款和应付债券以外的其他长期负债,如融资租赁负债。

8. 递延收益(Deferred Revenue)递延收益是企业已收到的客户预付款或收到但尚未实现收入的款项,将在未来期间确认为收入。

9. 预计负债(Provision)预计负债是企业基于现有情况预计未来可能发生的支出,如产品质量保证、未决诉讼等。

10. 应付利息(Interest Payable)应付利息是企业尚未支付的借款利息或债券利息。

了解这些中英文会计负债术语对照,有助于在国际商务交流中准确传达财务信息,确保会计信息的透明度和可比性。

中英文会计术语对照——负债Continued11. 一年内到期的非流动负债(Noncurrent Liabilities Due within One Year)这是指原本属于长期负债,但根据合同规定,将在一年内到期的部分。

12. 应付职工薪酬(Employee Benefits Payable)包括除了工资之外的其他职工福利,如奖金、津贴、社会保险费等。

第十章 长期负债培训资料

9 长期负债

(二)科目设置

总账科目 应付债券

明细科目 面值

利息调整 应计利息

(三)溢折价的摊销方法

实际利率法

是以债券发行时的实际利率(市场利率)来计算各 期溢价或折价摊销额的方法。

中 级会计学 Intermediate Accounting

9 长期负债

(四)债券平价发行的核算

应付债券—债券面值

银行存款

间的购建或者生产活动才能达到预定可使用或者可 销售状态的固定资产、投资性房地产和存货等资产。 举例: 房地产开发企业开发的用于出售的房地产开发产品 机械制造企业制造的用于对外出售的大型机械设备 建造合同

三、长期借款

• (一)借款费用的处理 • 资本化期间:开始资本化

停止资本化

购建或生产符合资本化条件的资产达 到预资定产支可出使已用经或发可生销售状态时

在建工程、财务费用

4.支付利息

2. 各期计提利息

债券发行费用的处理

如果发行费用>发行期间冻结资金产生利息收入 ①如果是为购建固定资产而筹措的借款:

• 计入固定资产成本 ②如果不是为购建固定资产而筹措的借款:

• 计入当期的财务费用 如果发行费用<发行期间冻结资金的利息收入

视为债券的溢价处理。

• (四)会计科目 • “应付债券”

(二)长期负债特点 期限长 金额大 还款方式多样

(三)举债筹资的特点

优点: • 维护企业原有的股权结构及股票价格 • 为股东提供剩余利益 • 税收上的好处 不足:

有可能减少股东权益 有可能影响企业的财务灵活性 具有较大的财务风险

中 级会计学 Intermediate Accounting

9 2年1月2日向中国银行借款100万元, 用于企业的固定资产建造,期限2年,年利率6%,每年计 息一次,利息按单利法计算,到期一次还本付息。该项固 定资产建造工程于2012年12月31日完工并交付使用,并办 妥了决算手续。项目实际发生支出145万元(假定均以银行 存款支付)。

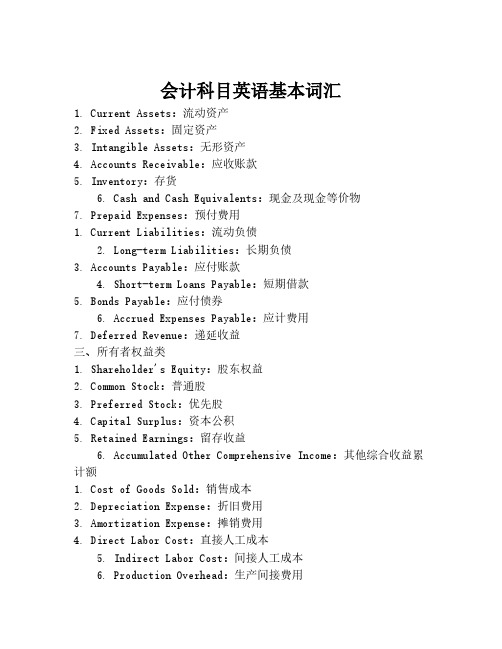

会计科目英语基本词汇

会计科目英语基本词汇1. Current Assets:流动资产2. Fixed Assets:固定资产3. Intangible Assets:无形资产4. Accounts Receivable:应收账款5. Inventory:存货6. Cash and Cash Equivalents:现金及现金等价物7. Prepaid Expenses:预付费用1. Current Liabilities:流动负债2. Long-term Liabilities:长期负债3. Accounts Payable:应付账款4. Short-term Loans Payable:短期借款5. Bonds Payable:应付债券6. Accrued Expenses Payable:应计费用7. Deferred Revenue:递延收益三、所有者权益类1. Shareholder's Equity:股东权益2. Common Stock:普通股3. Preferred Stock:优先股4. Capital Surplus:资本公积5. Retained Earnings:留存收益6. Accumulated Other Comprehensive Income:其他综合收益累计额1. Cost of Goods Sold:销售成本2. Depreciation Expense:折旧费用3. Amortization Expense:摊销费用4. Direct Labor Cost:直接人工成本5. Indirect Labor Cost:间接人工成本6. Production Overhead:生产间接费用1. Sales Revenue:销售收入2. Service Revenue:服务收入3. Interest Income:利息收入4. Dividend Income:股利收入5. Rental Income:租金收入6. Gain on Sale of Assets:资产出售收益1. Operating Expenses:营业费用2. Administrative Expenses:管理费用3. Selling Expenses:销售费用4. Financial Expenses:财务费用5. Research and Development Expenses:研发费用6. Income Tax Expense:所得税费用以上是关于会计科目的英语基本词汇,希望能对您的学习和工作有所帮助。

会计的英语名词解释

会计的英语名词解释在商业和财务领域中,会计是一个至关重要的职业。

会计负责记录和报告一个组织的财务信息,为决策者提供有关财务状况和业绩的准确数据。

在这个领域,有很多专业术语和名词。

本文将解释一些常见的会计英语名词。

1. Assets(资产)资产是指一个组织拥有的任何有经济价值的物品或资源。

资产可以是现金、股票、债券、不动产、机器设备等。

在会计报表中,资产被分为流动资产(比如现金和应收账款)和固定资产(比如房地产和设备)。

2. Liabilities(负债)负债是指一个组织所欠的债务或义务。

负债可以是贷款、应付账款、未结工资等。

负债分为流动负债(比如短期贷款和应付账款)和长期负债(长期贷款和债券)两种。

3. Equity(所有者权益)所有者权益是指一个组织的净资产,即资产减去负债后的余额。

所有者权益代表了组织所有者对其资本的权益。

它包括股东的股本和利润留存。

4. Revenue(收入)收入是指一个组织在特定会计期间内从经营活动中获得的货币流入。

收入可以包括销售收入、服务收入、利息收入等。

收入是一个组织盈利能力的一个重要指标。

5. Expenses(费用)费用是指一个组织在特定会计期间内为了生产和销售商品或提供服务而发生的成本。

费用包括人员薪酬、租金、采购成本、广告费用等。

费用是一个组织盈利能力的一个重要指标。

6. Depreciation(折旧)折旧是指资产在使用过程中由于年限或使用量的变化而产生的值减少。

折旧是费用,用于表示长期资产的价值损耗。

例如,一辆车的价值随着时间的推移会逐渐减少,折旧费用就被用来表示这种价值损耗。

7. Balance Sheet(资产负债表)资产负债表是一份会计报表,展示了一个组织在特定时间点的资产、负债和所有者权益的状况。

资产负债表可以帮助决策者了解组织的财务状况和偿债能力。

8. Income Statement(损益表)损益表是一份会计报表,展示了一个组织在特定会计期间内的收入、费用和净收益。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Accounting method

பைடு நூலகம்

debit

Text in here

credit

Current liabilities and long-term liabilities (caption of account) have the same accounting method.

[Image Info] www.wizdata.co.kr

- Note to customers : This image has been licensed to be used within this PowerPoint template only. You may not extract the image for any other use.

Relevant financial indicators

Contents

Team Introduction Long-term liabilities Bond issuance long-term notes payable Case Analysis

Long term liabilities’ definition and connotation

Definition and Connotation:Long-term

Bond issuance

Issuing mode of Bond

According to the similarities and differences between the actualissue price and coupon bond price, the issuance of bonds can beissued at par (平价), premium (溢价)and discount.(折价) 5 At par,it means the bond price equal to par value Issued at a premium, it means that the bond price is higher than the par value Issued at a discount , it means that the bond price is lower than the par value

(total liabilities and accounts receivable) / total assets 100%

(total longterm debt / assets)* 100%

(current assets / liabilities inventory)

Cash / current liabilities

computational formula

Ratio of fixed assets to long-term liabilities = Fixed assets / liabilities * 100%

This ratio can indicate how much the company fixed assets are available for long-term borrowing collateral as well as the long-term creditors’ rights security degree. As an ordinary company, fixed assets, especially as collateral, should be maintained in a certain ratio with long-term debt, as a debt security. Generally, this ratio is at least more than 100%, the greater the more can guarantee the long-term interests of creditors.

Bond issuance

Bond issuance conditions

Bond issuance conditions refer to the relevant factors of bond issuers must consider the bond financing, including the issuance, par value(面值), time limit,(期限) repayment method(偿还方式), interest rate(利率), payment of interest, issue price(发行价格), issue expenses(发行费用) and so on. Bond issuance 5 conditions determine the profitability(收益性), liquidity (流动性) and security(安全性) of bonds issuer, directly affect the financing cos(筹资成本)t and the amount of investment profit(投资收益). For investors, the most importantissue is the bond's coupon rate(票面利率), the maturity date(偿还期限) and issue price(发行价格) because they determine the bond investment value, so it is called the three basic conditions of bond issuance

Click to edit title style

Characteristics of long-term liabilities

Thirdly Secondly Firstly

maintaining a good capital structure can enhance the solvency of enterprises The long-term solvency of the enterprise and enterprise's profit ability is closely related to each other

Long-term Debt Ratio

Analysis of the main points

1

Compared with the current liabilities, long-term liabilities are relatively stable。

2

Compared with the owner's equity, long-term liabilities have fixed terms of repayment, fixed interest payments and capital source.And its stability cannot compare with the owner's equity.

The short-term debt paying ability is the foundation of long-term solvency

Types of long-term liabilities

1 long-term loan 2

bonds payable

3 long-term payables

Date Name

Long-term Debt Ratio

The quick ratio

Cash flow and debt ratio

Asset liability ratio (%)

The liquidity ratio

Net accounts receivable after the debt ratio

Total debt / total assets

100%

Assets / liabilities

Important ratio analysis

5

Long-term Debt Ratio

Definition :Long term debt ratio, as is also called "the capital ratio", is an indicator of corporate debt in general. It is the ratio of long-term 5 debt to total assets. Total assets equal liabilities and shareholders’ equity.

Bond issuance

The accounting of bond issuance

Example1

Assume that a company on January 1st 2012 issue a three year bond 100 pieces, each with a face value of 1000 yuan,10% of the nominal interest rate, every June 30th and December 31st all interest bearing time, of a debt due. If The issue of corporate bonds at par. 5 The issuance of bonds shall be recorded by the following entry:

Long-term Debt Ratio

● Formula as follows

Long term liabilities ratio = (total long-term debt / assets)* 100% Explanation:If the index reveals small, the degree of debt capitalization can be low, as well as the pressure from long-term debt paying; On the contrary, it reveals that high5capitalization company debt and long-term debt paying pressure. The indicator is mainly used to reflect the proportion of long-term debt with interest in the long-term working capital. So, the ratio should not be too high, the general should be below 20%.