ACCAF7基础讲义2015新大纲

Financial Reporting(F7)考试科目介绍及知识结构

Financial Reporting(F7)考试科目介绍及知识结构

本文由高顿ACCA整理发布,转载请注明出处

Financial Reporting(F7)

F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

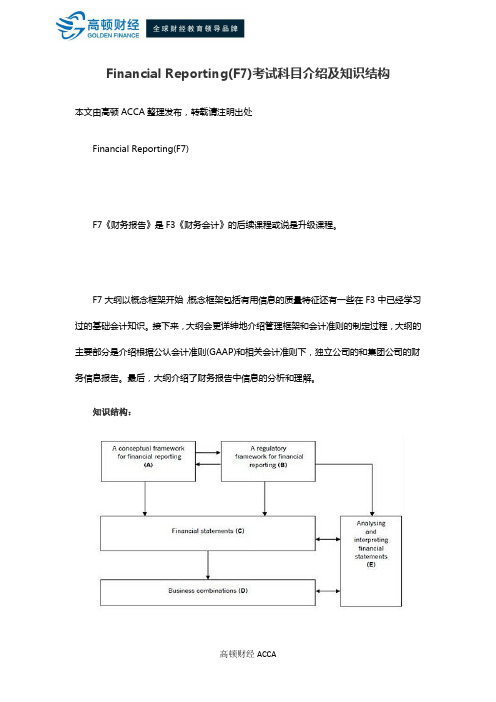

F7大纲以概念框架开始,概念框架包括有用信息的质量特征还有一些在F3中已经学习过的基础会计知识。

接下来,大纲会更详绅地介绍管理框架和会计准则的制定过程,大纲的主要部分是介绍根据公认会计准则(GAAP)和相关会计准则下,独立公司的和集团公司的财务信息报告。

最后,大纲介绍了财务报告中信息的分析和理解。

知识结构:

更多ACCA资讯请关注高顿ACCA官网:。

ACCA-F7-知识点总结

ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular,provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognizedwhen it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it is not a contingent liability – instead,a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the relatedeconomic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolittle’s premises are now empty and surplus to requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.cca f7真题对于acca f7的考试的重要性我相信各位acca考生都心知肚明了,首先我们先看一下acca f7科目的考试内容ACCA F7科目介绍:F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

ACCA-F7-知识点总结

ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular,provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognizedwhen it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it is not a contingent liability – instead,a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the relatedeconomic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolitt le’s premises are now empty and surplus to requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.cca f7真题对于acca f7的考试的重要性我相信各位acca考生都心知肚明了,首先我们先看一下acca f7科目的考试内容ACCA F7科目介绍:F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

acca f7课程大纲

acca f7课程大纲【最新版】目录1.ACCA F7 课程简介2.ACCA F7 课程大纲的主要内容3.ACCA F7 课程大纲的学习建议正文1.ACCA F7 课程简介ACCA(Association of Chartered Certified Accountants,特许公认会计师公会)是全球最具影响力的财会职业会员组织,而 F7 课程是其专业资格考试中的一门重要课程,名为“财务报告”。

该课程旨在帮助学员掌握企业财务报告的基本原则、会计处理方法以及相关法规,从而提高学员在财务报告领域的专业能力。

2.ACCA F7 课程大纲的主要内容ACCA F7 课程大纲分为三个部分,分别是:(1)财务报告框架:这部分主要介绍企业财务报告的基本原则、会计处理方法和相关法规。

学员需要了解国际财务报告准则(IFRS)及其在财务报告中的应用。

(2)资产、负债和所有者权益:这部分主要涉及企业的资产、负债和所有者权益的会计处理,包括固定资产、无形资产、存货、应收账款、流动负债、长期负债以及所有者权益等内容。

(3)收入、费用和利润:这部分主要涉及企业的收入、费用和利润的会计处理,包括营业收入、营业成本、销售费用、管理费用、财务费用以及利润分配等内容。

3.ACCA F7 课程大纲的学习建议(1)掌握基本概念:在学习 ACCA F7 课程大纲的过程中,要重视基本概念的掌握,如财务报告框架、会计处理方法等。

(2)注重实践操作:通过大量的练习题和案例分析,将理论知识运用到实际问题中,提高自己在财务报告领域的实际操作能力。

(3)关注最新动态:财务报告领域的法规和准则不断更新,需要关注最新的国际财务报告准则(IFRS),以便在考试中取得好成绩。

总之,ACCA F7 课程大纲涉及的内容较为广泛,需要学员投入足够的时间和精力进行学习和实践。

ACCA考前复习指南:F7重要知识点、考点总结.doc

ACCA考前复习指南:F7重要知识点.考点总结改革之后的F7考试,考查范围更加全面。

同学们在备考的时候,需要对每个准则基本内容进行准备。

考官一般围绕recognition , measurement和presentation等方面考查。

而选择题部分,考前可以结合三套真题的选择题和练习册的选择题梳理知识点。

试卷分析SectionA SectionB考试题型选择题20题大题:15分x2大题:30分xl考察范围整个考纲Ratio analysisSectionA备考要点■仔细读题■理解准则基础■排除法,举反例■计算题排除干扰自己算SectionB备考要点■计算ratio ,分类别(profitability/liquidity/gearing/i n vest or)■关注题目角色,以谁的角度写report■又寸比ratio :纟吉合题目要求,VS past year/competitors/industry benchmark■特殊关注点:从无到有,变化迅速,人无我有,人有我优■思考:financing sources, overtrading cashflow, risk going concernsConsolidation FS 重要知识点FV of considerationShare exchangeDeferred cashLoan noteContingent considerationFV Adjustment of net asset Depreciatio nFurther value in crease after acquisitionGoodwillImpairment of GoodwillMid?year acquisitiontime apportionIntra-group tradingSale &COSURP considering who is seller (S or P)Intra-group balancereceivables & payablesCIT & GITIntra-group loanInvestment & liabilityFinance cost & Investment incomeNCIFull methods(FV methods) VS proportionate methodsAssociateIntra-trading A&P: URP * P%Impairment of AssociateSingle entity重要知识点IAS16 PPEInitial Cost measurementDepreciationRevaluati on? watch out DT from revaluationDisposalIFRS9 Financial instrumentFinance asset-FVTPL/FVTOCI/Amortizatio n-Watch out Issue cost?Debt instrument & Equity instrumentFinance liability-Loan note■Convertible loan noteIFRS15 Revenue5 steps to recognize revenueConstruction contractService-Deferred revenueAgency sale-sales & repurchase-sales & return-sales & leasebackFactor receivablesIAS 2 Inventory adjustmentopening inventory+ purchase -closing inventory= cost of saleIAS 17 leaseFinance lease-NCL/CL & finance cost-Asset: CV & depreciationoperating lease?annual lease payment(time apportion)TaxCurrent taxDeferred tax-watch out DT from revaluationIAS 37Provision & contingent liabilityIAS 33 EPSEPS 计算:full market issue bonus issue & right issueCashflowInvestment, operating f financing局部计算选择题高频考点梳理Framework选择题文字题为主Qualitative characteristics 理解应用Recognition结合田可准则考察会计处理是否正确Measurement结合任何准则考察会计处理是否正确Historical cost, replacement cost, current cost Conceptual frameworkIAS 16 PPEInitial measurement costCapital expenditure VS revenue expenditure Depreciatio nRevaluationIAS 36 ImpairmentIndicators-carrying value > recoverable amount-external or internal indicatorCalculati on?Lower of carrying value-FV -cost to sell, Value in useCGU?order to impairment-1st specific damaged Asset■2nd Goodwill-3rd other asset (pro rata allocation)IAS 38 Intangible assetRecog nition-Research & development (capitalized criteria) Amortizati on-Finite life■Infinitive life : impairment reviewIFRS 5 NCA - Held for sale & discontinued operations Recognition Criteria 分类为IFRS5 的条件Measureme nt-Lower of:l.FV-cost to sell2.CV■No depreciation being held for saleIAS 23 Borrowing costConditions to be met for capitalizationInterest expenseIAS 20 Government GrantRevenue VS capital grantDeferred income / deducted from value of assetIAS 40 investment propertyFV to p/lIAS 2 InventoryValued at lower of 1: NRV=selling price - cost to sell2:Costopening inventory + purchase -closing inventory二cost of saleIAS 41 AgricultureScopeMeasurement: FVIFRS 15 (IAS 18/IAS11) revenue文字题-Revenue确认时点及金额■结合sales & repurchase z sales &lease back zFactor receivables/agency sales/sales & return 等特殊事项处理。

ACCA考前复习指南:F7重要知识点、考点总结.doc

ACCA考前复习指南:F7重要知识点.考点总结改革之后的F7考试,考查范围更加全面。

同学们在备考的时候,需要对每个准则基本内容进行准备。

考官一般围绕recognition , measurement和presentation等方面考查。

而选择题部分,考前可以结合三套真题的选择题和练习册的选择题梳理知识点。

试卷分析SectionA备考要点■仔细读题■理解准则基础■排除法,举反例■计算题排除干扰自己算SectionB备考要点■计算ratio ,分类别(profitability/liquidity/gearing/i n vest or)■关注题目角色,以谁的角度写report■又寸比ratio :纟吉合题目要求,VS past year/competitors/industry benchmark■特殊关注点:从无到有,变化迅速,人无我有,人有我优■ 思考:financing sources, overtrading cashflow, risk going concernsConsolidation FS 重要知识点FV of considerationShare exchangeDeferred cashLoan noteContingent considerationFV Adjustment of net asset Depreciatio nFurther value in crease after acquisitionGoodwillImpairment of GoodwillMid・year acquisitiontime apportionIntra-group tradingSale &COSURP considering who is seller (S or P)Intra-group balancereceivables & payablesCIT & GITIntra-group loanInvestment & liabilityFinance cost & Investment incomeNCIFull methods(FV methods) VS proportionate methodsAssociateIntra-trading A&P: URP * P%Impairment of AssociateSingle entity重要知识点IAS16 PPEInitial Cost measurementDepreciationRevaluati on・ watch out DT from revaluationDisposalIFRS9 Financial instrumentFinance asset-FVTPL/FVTOCI/Amortizatio n-Watch out Issue cost・Debt instrument & Equity instrument Finance liability-Loan note■Convertible loan noteIFRS15 Revenue5 steps to recognize revenueConstruction contractService-Deferred revenueAgency sale-sales & repurchase-sales & return-sales & leasebackFactor receivablesIAS 2 Inventory adjustmentopening inventory+ purchase -closing inventory= cost of saleIAS 17 leaseFinance lease-NCL/CL & finance cost-Asset: CV & depreciationoperating lease・annual lease payment(time apportion)TaxCurrent taxDeferred tax-watch out DT from revaluationIAS 37Provision & contingent liabilityIAS 33 EPSEPS 计算:full market issue bonus issue & right issueCashflowInvestment, operating f financing局部计算选择题高频考点梳理Framework选择题文字题为主Qualitative characteristics 理解应用Recognition结合田可准则考察会计处理是否正确Measurement结合任何准则考察会计处理是否正确Historical cost, replacement cost, current cost Conceptual frameworkIAS 16 PPEInitial measurement costCapital expenditure VS revenue expenditure Depreciatio nRevaluationIAS 36 ImpairmentIndicators-carrying value > recoverable amount-external or internal indicatorCalculati on・Lower of carrying value-FV -cost to sell, Value in useCGU・order to impairment-1st specific damaged Asset■2nd Goodwill-3rd other asset (pro rata allocation)IAS 38 Intangible assetRecog nition-Research & development (capitalized criteria) Amortizati on-Finite life■Infinitive life : impairment reviewIFRS 5 NCA - Held for sale & discontinued operations Recognition Criteria 分类为IFRS5 的条件Measureme nt-Lower of:l.FV-cost to sell2.CV■No depreciation being held for saleIAS 23 Borrowing costConditions to be met for capitalizationInterest expenseIAS 20 Government GrantRevenue VS capital grantDeferred income / deducted from value of assetIAS 40 investment propertyFV to p/lIAS 2 InventoryValued at lower of 1: NRV=selling price - cost to sell2:Costopening inventory + purchase -closing inventory二cost of saleIAS 41 AgricultureScopeMeasurement: FVIFRS 15 (IAS 18/IAS11) revenue文字题-Revenue确认时点及金额■结合sales & repurchase z sales &lease back zFactor receivables/agency sales/sales & return 等特殊事项处理。

2015年12月ACCA考试P1讲义

2015年12月ACCA考试P1讲义12月ACCA考试就要到了,为了方便大家更好地复习12月ACCAP1考试,小编在百度文库定期传一些考试资料,如有需要请关注财萃财经的百度文库。

Governance:Directors(a)ChairmanRunning the board and setting its agendaEnsuring the board receives accurate and timely informationEnsuring effective communication with shareholdersEnsuring sufficient time is allowed for discussion of controversial issuesTaking the lead in board developmentFacilitating board appraisalEncouraging active engagement by all the members of the boardReporting in and signing off accounts(b) CEOBusiness strategy and managementInvestment and financingRisk managementEstablishing the company’s managementBoard committeesLiaison with stakeholders(c) Division of responsibilitiesCEO run the company, Chairman run the board and take the lead in liaising withshareholders Chairman carries the authority of the board, CEO has the authority that isdelegated by the board. Unfettered powers is concentrated into on pair of handsAvoiding conflict of interestBoard can’t make the CEO accountable for management if it is led by CEOBoard is more able to express its concerns effectively by providing a point ofreporting for the NEDsChairman is responsible for obtaining the information that other directorsrequire to exercise proper oversight and monitor the organizationeffectivelyCompliance with governance best practice and hence reassures shareholders(d) Roles of NEDsStrategy. Contribute to, and challenge the direction of, StrategyScrutiny. Scrutiny the performance of executive management in meeting goals andobjectives and monitor the reporting of performance.Risk. Financial information is accurate and financial controls and systems ofrisk managementare robust.People. Determining appropriate levels of remuneration for executives, and arekey figures in the appointment and removal of senior managers and in successionplanningContribution of NEDs:Better balanced board(power, skills and experiences)Representing shareholder interests(put shareholders’viewpoint in board discussion,)Monitoring function(monitors risks, controls and operations effectively, theperformance of executive directors)(e) Advantages of NEDsExternal experience and knowledge which executive directors do not possess.Provide a wider perspective than executive directorsA comfort factor for third parties such as investors or creditorsCertain roles (father confessor: being a confidant for the chairmanand other directors; oil-can: intervening to make the board run moreeffectively; high-sheriff: if necessary taking steps to remove thechairman or CEO)Full board members who are excepted to have the level of knowledge that fullboard membership implies.(f) Problems of NEDsLack independence (no business, financial or other connection;Cross-directorships; should not take part in share option schemes and theirservice should not be pensionable; Appointments should not be for aspecified term and reappointment should not be automatic; Procedures shouldexist to ensure NEDs take independent advice)Prejudice and against widening the recruitment of NEDsHigh-calibre NEDs may gravitate towards the best run companiesHave difficulty imposing their views upon the board.Not enough emphasis is given to the role of NEDs in preventing troubleLimited timeDamage company performance by weakening board unity and stiflingentrepreneurship(g) Remuneration packageBasic salary(experience, market rate)Performance related bonuses(transaction bonuses; loyalty bonuses)SharesShare options (align management and shareholder interests, particularlyheld for a long time)Benefits in kind (transport/ health provisions / life assurance /holidays / expenses / loans) Pensions(h) Remuneration policyPay scalesProportion of different types of rewardPeriodBe related to measureable performanceBalance between short and long-term performance elementsTransparencyResponsibilities of the boardFormal schedule of matters specifically reserved to it for decisionat board meetingsMonitoring the CEOOverseeing strategyMonitoring risks, control systems and governanceMonitoring the human capital aspects of the company, eg succession, morale,trainingMonitoring potential conflicts of interestEnsuring that there is effective communication of its strategic plans.Nomination Committee(a)Consist mainly of NEDs, to consider:The balance between executive and independent NEDsThe skills, knowledge and experience possessed by the current boardThe need for continuity and succession planningThe desirable size of the boardThe need to attract board members from a diversity or backgrounds(b)InductionBuild an understanding of the nature of the company, its business and itsmarkets;Build a link with the company’s peopleBuild an understanding of the company’s main relationship including meetingswith auditors(c) Continuing professional developmentExtend their knowledge and skills continuously;Concentrate on the role of board, obligations and entitlements of existing directorsand the behaviors needed for effective board performance.Audit committee(a)FunctionImprove the quality of financial reportingReduce the opportunity for fraudEnable the NEDs continue an independent judgement and play a positive roleHelp the finance director (raise issues of concern; get difficult things done)Strengthen the position of the external auditorThe External auditor can asserthis independence when dispute withmanagementStrengthen the position of the internal auditorIncrease public confidence(b) Review of financial statements andsystemsConsidering performance indicators and information systems that allowmonitoring of the most significant business and financial risks.(c) Liaison with external auditorsBeing responsible for the appointment or removal of the external auditorsAny other threats to external auditor independence (non-audit service; conflictof interest)Discussing the scope of the external auditActing as a forum for liaison between the external auditors, the IAs and thefinance directors Helping the external auditors to obtain the informationMaking themselves available to the external auditors for consultantDealing with any serious reservations.(d)Review of internal auditStandards including objectivity, technical knowledge and professional standardsScope including how much emphasis is given to different types of reviewResources (enough hours, personal technical and skills)Reporting arrangementsWork plan (review of controls and coverage of high risk areas)Liaison with external auditorsResultsRelate to external auditor (increase the independence of external auditor; actas liaison person to facilitate the communication between the executivedirectors and external auditors; Act as coordinate the work between externalauditor and internal auditor;To monitor the independence and quality of workof external auditor)Related to internal audit function (To approve the appointment ortermination???? of appointment of the head of internal audit; To review the workof the internal audit function)(e)Review of internal controlMonitor the adequacy of internal control systems in mitigating???? risks(control environment, management’s attitude)Cover legal compliance and ethicsAddress the risk of fraud (report fraud, frand to be investigated)Reviewing the company’s statement on internal controlsConsider the recommendation of the auditors in the management letter andmanagement’s responseActive supervisory role (review major transactions)(f)Review of risk managementConfirming a formal policy in place for risk management, risk management isupdated to reflect current positions and strategy.(g) Independence of internal auditcommittee:Only be effective if NEDs are independence.Crucial to discuss the management’s competence and judgement with the externalauditors, if not, they may feel loyalty towards managementInvestors’confidenceReporting of the internal audit committee need the NEDs’independence,otherwise influence the integrity of the auditors.Internal auditors/external auditors comparison of role in the context ofcorporate governance(a)Assess the need for internal auditScale, diversity and complexity of the company’s operationsNumber of employeesCost-benefit considerationsChanges in organizational structureChanges in key risksProblems with internal control systemsIncreased number of unexplained or unacceptable events(b)Role of internal audit functionIndependent checking, examination and evaluation the internal control systemestablished by executive director.Internal control over financial reportingFS whether show true and fairInternal control over operationOperational information(management information)Review of “3E”Review of compliance with laws and regulationsReview of safeguarding of the organization’s assetsReview of implementation of corporate goals and objectivesReview of significant risks to the organisation, monitoring risk managementpolicy and risk management strategies.(c) Advantages of appointing internalauditor from outside the company:External appointment would bring detachment and independence (reduce or avoidsthe independence and familiarity threats)An external appointment would help with independence and objectivity. Own nopersonal loyalties nor ‘favours’from previous positions. Have no personalgrievances nor conflicts with other people. (Increase the confidence ofinvestors)Some benefit would be expected from the “new broom effect’in that theappointment would see the company through fresh eyes .(bring a fresh pair ofeyes to the task) Come in with new ideas and expertise gained from other situationsThe possibility exists for the transfer of best practice in from outside.(bestpractice and current developments can be introduced)(d) Review of the risk managementIdentification. Risks comes and go with the changing nature of businessactivity, and with the continual change in any organization’s environment.Assessment. The probability of the risk being realized; the impact or hazard.Review. Analyses the controls that the organization has.Report. A report on the review is produced and submitted to the principal.(e)Social and environmental audit: WhyThere is a growing belief that environment issues represent a source of risk interms of unforeseen liabilities, reputational damage, or similar.The ethical performance of a business, such as its social and environmentalbehaviour, is a factor in some people’s decision to engage with thebusiness in its resource and product markets.An increasing number of investors are using social and environmentalperformance as a key criterion for their investment decisions.(f)Environmental audit: whatIs a systematic, documented, periodic and objective evaluation of how well anentity, itsmanagement and equipment are performing, with the aim of helping tosafeguard the environment by facilitating(??) management control of environmentpractice and assessing compliance with entity policies and externalregulations.。

《财务报告(F7)》-课程教学大纲

《财务报告(F7)》课程教学大纲一、课程基本信息课程代码:16134904课程名称:财务报告F7英文名称: Financial Reporting (F7)课程类别:专业课学时:65学分: 4适用对象:ACCA学生考核方式:考试先修课程:会计学、财务管理学、管理学、F1-F6等二、课程简介本门课程采用原版教材,按学校要求进行全英教学,其出发点主要在于:原版教材广泛的题材、翔实的内容、迥然不同的风格,一改传统专业英语的枯燥、乏味,能够大大提高学生学习英语的兴趣;规范的语言、生动的文字、丰富多样的练习不仅能帮助学生巩固原有的语言知识,而且还在学生学习掌握专业术语、专业表达方法的同时传授专业领域的知识,从而提高学生用英语获取专业知识和用英语从事交流的能力。

F7 takes your financial reporting knowledge and skills up to the next level. New topics are consolidated financial statements, long-term contracts, biological assets, financial instruments and leases. There is also coverage of creative accounting and the limitations of financial statements and ratios。

三、课程性质与教学目的《财务报告(F7)》是ACCA考试的主要课程之一,也是ACCA专业学生的必修专业课程,是会计专业的核心课程。

该课程主要介绍了财务报告概念框架、会计具体事项处理、合并报表及个别报告、财务分析等部分的内容。

本课程所涉及内容主要是介绍国际财务会计准则的具体运用。

国际会计准则要求报表信息能够客观公正反企业的经济事务,为投资者及利益相关者提供公允的财务信息,有利于报表使用者做出正确判断。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

F7FINANCIAL REPORTING--PART B ACCOUNTING STANDARDS Chapter 4 Revenue recognition and substance of transactionsDefinition p53Revenue: Income arising in the course of an entity’s ordinary activities.Contract: An agreement between two or more parties that creates enforceable rights and obligations.Definition p53Performance obligation: A promise in a contract with a customer to transfer to the customer either:(a) a good or service (or a bundle of goods or services) that is distinct; or(b) a series of distinct goods or services that are substantially the same and that have the same pattern of transfer to the customer.Agency?Definition p53In an agency relationship, the gross inflows of economic benefits include amounts collected on behalf of the principal and which do not result in increases in equity for the entity. The amounts collected on behalf of the principal are not revenue. Instead, revenue is the amount of commission.Recognition p54: Five-stepapproachStep 1: Identify the contract(s) with a customer—a contract is an agreement between two or more parties that creates enforceable rights and obligations.Recognition p54: Five-stepapproachStep 2: Identify the performance obligations in the contract—a contract includes promises to transfer goods or services to a customer. If those goods or services are distinct, the promises are performance obligations and are accounted for separately.Recognition p54: Five-stepapproachA good or service is distinct if either of the following criteria is met:(a) the entity regularly sells the good or service separately’ or(b) the customer can benefit from the good or service either on its own or together with resources that are readily available to the customer.Recognition p54: Five-stepapproachStep 3: Determine the transaction price—the transaction price is the amount of consideration in a contract to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer.Recognition p54: Five-stepapproachThe transaction price can be a fixed amount of customer consideration, but it may sometimes include variable consideration or consideration in a form other than cash such as discounts, rebates, refunds, credits, incentives, bonuses, penalties. Under the proposal, these variable amounts would be estimated and included in the transaction price using either the ‘expected value’ or the ‘most likely amount’ approach.Recognition p54: Five-stepapproachStep 4: Allocate the transaction price to the performance obligations in the contract—an entity typically allocates the transaction price to each performance obligation on the basis of the relative stand-alone selling prices of each distinct good or service promised in the contract. If a stand-alone selling price is not observable, an entity estimates it.Recognition p54: Five-stepapproachStep 5: A company would recognise revenue when (or as) it satisfies a performance obligation by transferring a promised good or service to a customer (which is when the customer obtains control of that good or service).Recognition p54: Five-stepapproachTo determine the point in time when a customer obtains control of a promised asset and an entity satisfies a performance obligation, the entity would consider indicators of the transfer of control that include, but are not limited to, the following:(a) the entity has a present right to payment for the asset;(b) the customer has legal title to the asset;Recognition p54: Five-stepapproach(c) the entity has transferred physical possession of the asset;(d) the customer has the significant risks and rewards of ownership ofthe asset; and(e) the customer has accepted the asset.Recognition p54: Five-stepapproachA performance obligation may be satisfied at a point in time (typically for promises to transfer goods to a customer) or over time (typically for promises to transfer services to a customer). For performance obligations satisfied over time, a company would select an appropriate measure of progress to determine how much revenue should be recognised as the performance obligation is satisfied.IAS 18 REVENUEMeasurement P55•When (or as) a performance obligation is satisfied, an entity shall recognise as revenue the amount of the transaction price.Ex 1,2 P231OFF BALANCE SHEETcreativeaccounting p52Profit smoothing , where profits from good years are held back and released in bad years to make the results look consistent year on yearReducing gearing , disguise debt on the balance sheet good returnlow riskIAS 1 requires to report substance (substance over form)Form: A sells assets to BA still controls the asset A doesn't control theassetSubstance : not a real sale Substance : a real saleA/C treatment: no revenue recognised A/Ctreatment: recognise revenuereport substanceConsignment inventory P56manufacturerdealer (agent)customerdeliver inventoriessale goodsConsignment inventories Should be inventory recognised in dealer ’s book?Should be revenue recognised at delivery?Who recog the revenue?control!!!!!Consignment inventory P56 IndicatorsThe product is controlledby the manufacturer until a specified event occurs YNYThe manufacturer is able to require the return of the product or transfer the product to a third party (such as another dealer)NEx 2 P232Consignment inventory P56IndicatorsThe dealer does not havean unconditional obligationto pay for the productY NManufacturer can’t recognise revenue until customer purchases goods from dealer and dealer can’t recognise inv. Both manufacturer and dealer can recognise revenue when goods is delivered and dealer can recognise inv.Ex 2 P232Sales and repurchase P57 seller buyer salesrepurchase IndicatorsEx 3 P232Repurchasemanufacturer ’s obligation/right to repurchase the asset manufacturer ’s obligation to repurchase the asset at thecustomer ’s requestthe buyer is limited in its ability todirect the use of, and obtainsubstantially all of the remainingbenefits from, the assetwhether the buyer has a significant economic incentive to exercise that rightSales and repurchase P57 seller buyer salesrepurchase IndicatorsEx 3 P232Repurchasethe buyer does not obtain control of the assetY Nsubstance:a financing arrangementsubstance: sale of a product with a right of returnnot a real saleSales and repurchase P57 seller buyersalesrepurchase IndicatorsEx 3 P232Repurchasesubstance:a financing arrangementRepurchase price≥original selling priceYNsubstance:a lease not a real sale'Bill and hold' sales P59A bill-and-hold arrangement is a contract under which an entity bills a customer for a product but the entity retains physical possession of the product until it is transferred to the customer at a point in time in the future.An entity shall determine when it has satisfied its performance obligation to transfer a product by evaluating when a customer obtains control of that product.'Bill and hold' sales P59 IndicatorsThe reason for the bill-and-hold arrangement issubstantive (for example, the customer has requested the arrangement)NNThe product is identified separately as belonging to the customerYY'Bill and hold' sales P59 IndicatorsThe product is currently ready for physical transfer to the customer N YThe manufacturer can have the ability to use the product or to direct it to another customer.NYRecognise the revenue when customer obtains control later, usually at delivery. Recognise the revenue when the bill is received.。