财务管理-AnalysisandValuation(财务报表分析,台湾中

财务管理英语知识

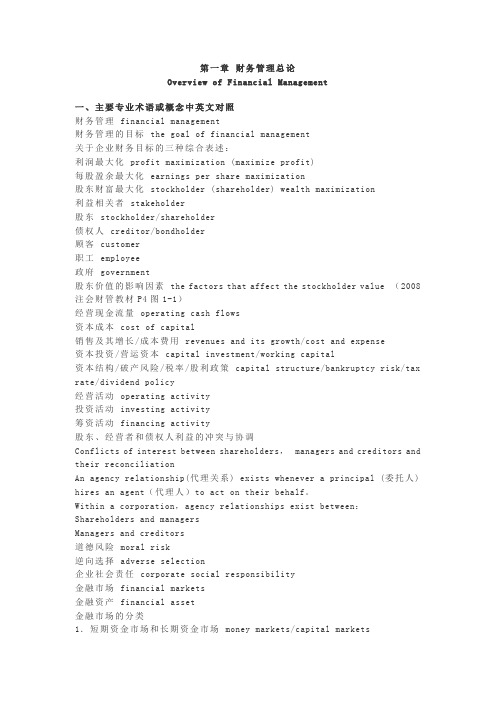

第一章财务管理总论Overview of Financial Man agement一、主要专业术语或概念中英文对照财务管理financial management财务管理的目标the goal of financial management关于企业财务目标的三种综合表述:利润最大化profit maximization (maximize profit)每股盈余最大化earnings per share maximization股东财富最大化stockholder (shareholder) wealth maximization利益相关者stakeholder股东stockholder/shareholder债权人creditor/bondholder顾客customer职工employee政府government股东价值的影响因素the factors that affect the stockholder value (2008注会财管教材P4图1-1)经营现金流量operating cash flows资本成本cost of capital销售及其增长/成本费用revenues and its growth/cost and expense资本投资/营运资本capital investment/working capital资本结构/破产风险/税率/股利政策capital structure/bankruptcy risk/tax rate/dividend policy经营活动operating activity投资活动investing activity筹资活动financing activity股东、经营者和债权人利益的冲突与协调Conflicts of interest between shareholders,managers and creditors and their reconciliationAn agency relationship(代理关系) exists whenever a principal (委托人) hires an agent(代理人)to act on their behalf。

关于财务管理的英文单词

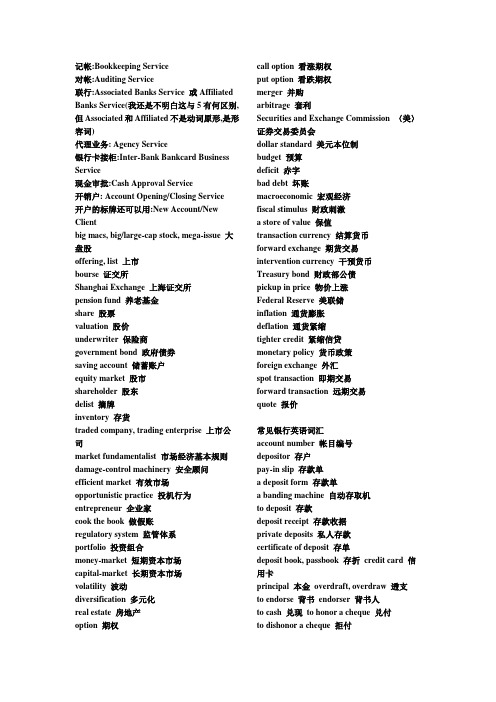

记帐:Bookkeeping Service对帐:Auditing Service联行:Associated Banks Service 或Affiliated Banks Service(我还是不明白这与5有何区别,但Associated和Affiliated不是动词原形,是形容词)代理业务: Agency Service银行卡接柜:Inter-Bank Bankcard Business Service现金审批:Cash Approval Service开销户: Account Opening/Closing Service开户的标牌还可以用:New Account/New Clientbig macs, big/large-cap stock, mega-issue 大盘股offering, list 上市bourse 证交所Shanghai Exchange 上海证交所pension fund 养老基金share 股票valuation 股价underwriter 保险商government bond 政府债券saving account 储蓄账户equity market 股市shareholder 股东delist 摘牌inventory 存货traded company, trading enterprise 上市公司market fundamentalist 市场经济基本规则damage-control machinery 安全顾问efficient market 有效市场opportunistic practice 投机行为entrepreneur 企业家cook the book 做假账regulatory system 监管体系portfolio 投资组合money-market 短期资本市场capital-market 长期资本市场volatility 波动diversification 多元化real estate 房地产option 期权call option 看涨期权put option 看跌期权merger 并购arbitrage 套利Securities and Exchange Commission 〈美〉证券交易委员会dollar standard 美元本位制budget 预算deficit 赤字bad debt 坏账macroeconomic 宏观经济fiscal stimulus 财政刺激a store of value 保值transaction currency 结算货币forward exchange 期货交易intervention currency 干预货币Treasury bond 财政部公债pickup in price 物价上涨Federal Reserve 美联储inflation 通货膨胀deflation 通货紧缩tighter credit 紧缩信贷monetary policy 货币政策foreign exchange 外汇spot transaction 即期交易forward transaction 远期交易quote 报价常见银行英语词汇account number 帐目编号depositor 存户pay-in slip 存款单a deposit form 存款单a banding machine 自动存取机to deposit 存款deposit receipt 存款收据private deposits 私人存款certificate of deposit 存单deposit book, passbook 存折credit card 信用卡principal 本金overdraft, overdraw 透支to endorse 背书endorser 背书人to cash 兑现to honor a cheque 兑付to dishonor a cheque 拒付to suspend payment 止付cheque,check 支票cheque book 支票本crossed cheque 横线支票blank cheque 空白支票rubber cheque 空头支票cheque stub, counterfoil 票根cash cheque 现金支票traveler's cheque 旅行支票cheque for transfer 转帐支票outstanding cheque 未付支票canceled cheque 已付支票forged cheque 伪支票Bandar's note 庄票,银票banker 银行家president 行长savings bank 储蓄银行Chase Bank 大通银行National City Bank of New York 花旗银行Hongkong Shanghai Banking Corporation 汇丰银行Chartered Bank of India, Australia and China 麦加利银行Banque de I'IndoChine 东方汇理银行central bank, national bank, banker's bank 中央银行bank of issue, bank of circulation 发行币银行commercial bank 商业银行,储蓄信贷银行member bank, credit bank 储蓄信贷银行discount bank 贴现银行exchange bank 汇兑银行requesting bank 委托开证银行issuing bank, opening bank 开证银行advising bank, notifying bank 通知银行negotiation bank 议付银行confirming bank 保兑银行paying bank 付款银行associate banker of collection 代收银行consigned banker of collection 委托银行clearing bank 清算银行local bank 本地银行domestic bank 国内银行overseas bank 国外银行unincorporated bank 钱庄branch bank 银行分行trustee savings bank 信托储蓄银行trust company 信托公司financial trust 金融信托公司unit trust 信托投资公司trust institution 银行的信托部credit department 银行的信用部commercial credit company(discount company) 商业信贷公司(贴现公司)neighborhood savings bank, bank of deposit 街道储蓄所credit union 合作银行credit bureau 商业兴信所self-service bank 无人银行land bank 土地银行construction bank 建设银行industrial and commercial bank 工商银行bank of communications 交通银行mutual savings bank 互助储蓄银行post office savings bank 邮局储蓄银行mortgage bank, building society 抵押银行industrial bank 实业银行home loan bank 家宅贷款银行reserve bank 准备银行chartered bank 特许银行corresponding bank 往来银行merchant bank, accepting bank 承兑银行investment bank 投资银行import and export bank (EXIMBANK) 进出口银行joint venture bank 合资银行money shop, native bank 钱庄credit cooperatives 信用社clearing house 票据交换所public accounting 公共会计business accounting 商业会计cost accounting 成本会计depreciation accounting 折旧会计computerized accounting 电脑化会计general ledger 总帐subsidiary ledger 分户帐cash book 现金出纳帐cash account 现金帐journal, day-book 日记帐,流水帐bad debts 坏帐investment 投资surplus 结余idle capital 游资economic cycle 经济周期economic boom 经济繁荣economic recession 经济衰退economic depression 经济萧条economic crisis 经济危机economic recovery 经济复苏inflation 通货膨胀deflation 通货收缩devaluation 货币贬值revaluation 货币增值international balance of payment 国际收支favourable balance 顺差adverse balance 逆差hard currency 硬通货soft currency 软通货international monetary system 国际货币制度the purchasing power of money 货币购买力money in circulation 货币流通量note issue 纸币发行量national budget 国家预算national gross product 国民生产总值public bond 公债stock, share 股票debenture 债券treasury bill 国库券debt chain 债务链direct exchange 直接(对角)套汇indirect exchange 间接(三角)套汇cross rate, arbitrage rate 套汇汇率foreign currency (exchange) reserve 外汇储备foreign exchange fluctuation 外汇波动foreign exchange crisis 外汇危机discount 贴现discount rate, bank rate 贴现率gold reserve 黄金储备money (financial) market 金融市场stock exchange 股票交易所broker 经纪人commission 佣金bookkeeping 簿记bookkeeper 簿记员an application form 申请单bank statement 对帐单letter of credit 信用证strong room, vault 保险库equitable tax system 等价税则specimen signature 签字式样banking hours, business hours 营业时间(Consumer Price Index) 消费者物价指数business 企业商业业务financial risk 财务风险sole proprietorship 私人业主制企业partnership 合伙制企业limited partner 有限责任合伙人general partner 一般合伙人separation of ownership and control 所有权与经营权分离claim 要求主张要求权management buyout 管理层收购tender offer 要约收购financial standards 财务准则initial public offering 首次公开发行股票private corporation 私募公司未上市公司closely held corporation 控股公司board of directors 董事会executove director 执行董事non- executove director 非执行董事chairperson 主席controller 主计长treasurer 司库revenue 收入profit 利润earnings per share 每股盈余return 回报market share 市场份额social good 社会福利financial distress 财务困境stakeholder theory 利益相关者理论value (wealth) maximization 价值(财富)最大化common stockholder 普通股股东preferred stockholder 优先股股东debt holder 债权人well-being 福利diversity 多样化going concern 持续的agency problem 代理问题free-riding problem 搭便车问题information asymmetry 信息不对称retail investor 散户投资者institutional investor 机构投资者agency relationship 代理关系net present value 净现值creative accounting 创造性会计stock option 股票期权agency cost 代理成本bonding cost 契约成本monitoring costs 监督成本takeover 接管corporate annual reports 公司年报balance sheet 资产负债表income statement 利润表statement of cash flows 现金流量表statement of retained earnings 留存收益表fair market value 公允市场价值marketable securities 油价证券check 支票money order 拨款但、汇款单withdrawal 提款accounts receivable 应收账款credit sale 赊销inventory 存货property,plant,and equipment 土地、厂房与设备depreciation 折旧accumulated depreciation 累计折旧liability 负债current liability 流动负债long-term liability 长期负债accounts payout 应付账款note payout 应付票据accrued espense 应计费用deferred tax 递延税款preferred stock 优先股common stock 普通股book value 账面价值capital surplus 资本盈余accumulated retained earnings 累计留存收益hybrid 混合金融工具treasury stock 库藏股historic cost 历史成本current market value 现行市场价值real estate 房地产outstanding 发行在外的a profit and loss statement 损益表net income 净利润operating income 经营收益earnings per share 每股收益simple capital structure 简单资本结构dilutive 冲减每股收益的basic earnings per share 基本每股收益complex capital structures 复杂的每股收益diluted earnings per share 稀释的每股收益convertible securities 可转换证券warrant 认股权证accrual accounting 应计制会计amortization 摊销accelerated methods 加速折旧法straight-line depreciation 直线折旧法statement of changes in shareholders’equity 股东权益变动表source of cash 现金来源use of cash 现金运用operating cash flows 经营现金流cash flow from operations 经营活动现金流direct method 直接法indirect method 间接法bottom-up approach 倒推法investing cash flows 投资现金流cash flow from investing 投资活动现金流joint venture 合资企业affiliate 分支机构financing cash flows 筹资现金流cash flows from financing 筹资活动现金流time value of money 货币时间价值simple interest 单利debt instrument 债务工具annuity 年金future value 终至present value 现值compound interest 复利compounding 复利计算pricipal 本金mortgage 抵押credit card 信用卡terminal value 终值discounting 折现计算discount rate 折现率opportunity cost 机会成本required rate of return 要求的报酬率cost of capital 资本成本ordinary annuity普通年金annuity due 先付年金financial ratio 财务比率deferred annuity 递延年金restrictive covenants 限制性条款perpetuity 永续年金bond indenture 债券契约face value 面值financial analyst 财务分析师coupon rate 息票利率liquidity ratio 流动性比率nominal interest rate 名义利率current ratio 流动比率effective interest rate 有效利率window dressing 账面粉饰going-concern value 持续经营价值marketable securities 短期证券liquidation value 清算价值quick ratio 速动比率book value 账面价值cash ratio 现金比率marker value 市场价值debt management ratios 债务管理比率intrinsic value 内在价值debt ratio 债务比率mispricing 给……错定价格debt-to-equity ratio 债务与权益比率valuation approach 估价方法equity multiplier 权益乘discounted cash flow valuation 折现现金流量模型long-term ratio 长期比率undervaluation 低估debt-to-total-capital 债务与全部资本比率overvaluation 高估leverage ratios 杠杆比率option-pricing model 期权定价模型interest coverage ratio 利息保障比率contingent claim valuation 或有要求权估价earnings before interest and taxes 息税前利润promissory note 本票cash flow coverage ratio 现金流量保障比率contractual provision 契约条款asset management ratios 资产管理比率par value 票面价值accounts receivable turnover ratio 应收账款周转率maturity value 到期价值inventory turnover ratio 存货周转率coupon 息票利息inventory processing period 存货周转期coupon payment 息票利息支付accounts payable turnover ratio 应付账款周转率coupon interest rate 息票利率cash conversion cycle 现金周转期maturity 到期日asset turnover ratio 资产周转率term to maturity 到期时间profitability ratio 盈利比率call provision赎回条款gross profit margin 毛利润call price 赎回价格operating profit margin 经营利润sinking fund provision 偿债基金条款net profit margin 净利润conversion right 转换权return on asset 资产收益率put provision 卖出条款return on total equity ratio 全部权益报酬率indenture 债务契约return on common equity 普通权益报酬率covenant 条款market-to-book value ratio 市场价值与账面价值比率trustee 托管人market value ratios 市场价值比率protective covenant 保护性条款dividend yield 股利收益率negative covenant 消极条款dividend payout 股利支付率positive covenant 积极条款financial statement财务报表secured deht担保借款profitability 盈利能力unsecured deht信用借款viability 生存能力creditworthiness 信誉solvency 偿付能力collateral 抵押品collateral trust bonds 抵押信托契约debenture 信用债券bond rating 债券评级current yield 现行收益yield to maturity 到期收益率default risk 违约风险interest rate risk 利息率风险authorized shares 授权股outstanding shares 发行股treasury share 库藏股repurchase 回购right to proxy 代理权right to vote 投票权independent auditor 独立审计师straight or majority voting 多数投票制cumulative voting 积累投票制liquidation 清算right to transfer ownership 所有权转移权preemptive right 优先认股权dividend discount model 股利折现模型capital asset pricing model 资本资产定价模型constant growth model 固定增长率模型growth perpetuity 增长年金mortgage bonds 抵押债券。

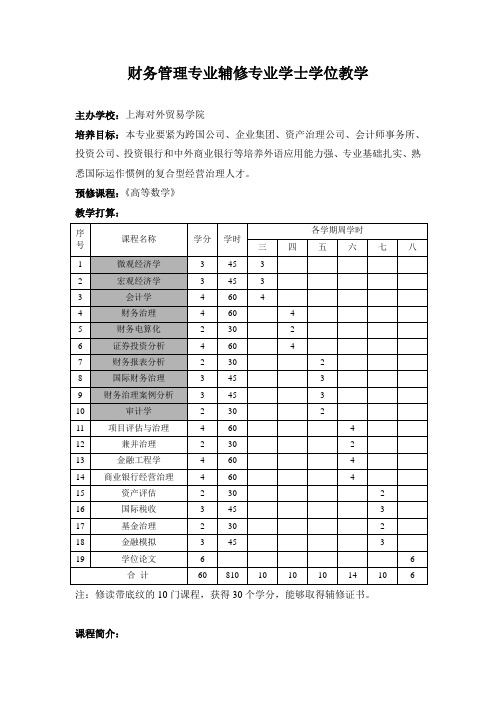

财务管理专业辅修专业学士学位教学

财务管理专业辅修专业学士学位教学主办学校:上海对外贸易学院培养目标:本专业要紧为跨国公司、企业集团、资产治理公司、会计师事务所、投资公司、投资银行和中外商业银行等培养外语应用能力强、专业基础扎实、熟悉国际运作惯例的复合型经营治理人才。

预修课程:《高等数学》教学打算:注:修读带底纹的10门课程,获得30个学分,能够取得辅修证书。

课程简介:课程名称:微观经济学课程简介:本课程介绍西方经济学的差不多概念、差不多理论和差不多方法。

微观经济学以单个经济行为者的经济行为为研究对象,分析在市场机制作用下的资源配置作用。

要紧内容:均衡价格决定理论、消费者行为理论、生产理论、厂商均衡理论、生产要素价格决定和收入分配理论、微观经济决策等。

课程名称:宏观经济学课程简介:本课程介绍西方经济学的差不多概念、差不多理论和差不多方法。

宏观经济学是以整个国民经济为研究对象,分析资源利用问题。

要紧内容有:国际收入核算理论,简单国民收入决定理论,产业市场和货币市场的均衡,总需求和总供给模型,通货膨胀理论,经济周期与经济增长理论,宏观经济政策,开放条件下的宏观经济模型。

课程名称:会计学课程简介:本课程要紧讲述会计总论,包括会计差不多前提和一样原则、会计要素与会计科目、复式记账与账户、会计凭证与账簿、会计核算程序等;会计要素专论,包括资产、负债、资本、收入与费用、利润等运算与分配;会计报表,包括会计报表的意义和种类、会计报表的编制与分析等。

课程名称:财务治理课程简介;财务治理的环境,汇率的确定及均衡关系;汇率的推测;外汇风险的测定;外汇风险的治理;跨国公司短期资金筹集分析;国际现金治理;应收账款和库存治理;跨国财务系统治理;国际税收治理;跨国公司投资策略分析;跨国资本规划;政治风险治理;对外投资成本;跨国融资策略;融资场所。

课程名称:财务电算化课程简介:随着财务软件的普及,财务类人员能否熟练把握其使用变得越来越重要。

这门课程以教师教授与学生上机实践相结合,要紧介绍了财务软件中账务处理模块、报表生成模块、应收账款治理模块、应对账款治理模块、存货治理模块、财务分析模块、资金治理模块等的使用。

财务报表分析-英文

Introduction and Basic Concepts

Business Partnership Vision Strategy Budget Forecast

Others Treasury M&A Risk Management Insurance Auditing Compliance Hedging ….

Introduction and Basic Concepts

Minimize Working Capital Maintain Strong Cash Flow

Pay Debts As They Are Due Increase Liquidity

Maintain Strong Financial Position

Introduction and Basic Concepts

导言及基本概念 Introduction and Basic Concepts Introduction Finance Organization Finance Activity Other topics

This training will allow you to understand: Finance Function Concept of Financial KPIs (Revenue, DM, DL, VOH, FOH, SG&A, OI, OCF, EBITDA, DOH, DSO, DPO, Incremental, etc.) BS, P&L and Cash Flow Statements Concepts of Financial Statement Evaluation and Investment Appraisal

财务报表分析中英文对照外文翻译文献编辑

财务报表分析中英文对照外文翻译文献编辑Introduction:Financial statement analysis is an essential tool used by businesses and investors to evaluate the financial performance and position of a company. It involves the examination of financial statements such as the balance sheet, income statement, and cash flow statement to assess the company's profitability, liquidity, solvency, and efficiency. In this document, we will provide a detailed analysis and translation of foreign literature related to financial statement analysis.1. Importance of Financial Statement Analysis:Financial statement analysis provides valuable insights into a company's financial health and helps stakeholders make informed decisions. It enables investors to assess the profitability and growth potential of a company before making investment decisions. Additionally, it helps creditors evaluate the creditworthiness and repayment capacity of a company before extending credit. Furthermore, financial statement analysis assists management in identifying areas of improvement and making strategic decisions to enhance the company's performance.2. Key Elements of Financial Statement Analysis:a) Balance Sheet Analysis:The balance sheet provides a snapshot of a company's financial position at a specific point in time. It presents the company's assets, liabilities, and shareholders' equity. By analyzing the balance sheet, stakeholders can assess the company's liquidity, solvency, and financial stability.b) Income Statement Analysis:The income statement, also known as the profit and loss statement, presents the company's revenues, expenses, and net income over a specific period. It helps stakeholders evaluate the company's profitability, revenue growth, and cost management.c) Cash Flow Statement Analysis:The cash flow statement details the inflows and outflows of cash during a specific period. It provides insights into the company's operating, investing, and financing activities. By analyzing the cash flow statement, stakeholders can assess the company's ability to generate cash, meet its financial obligations, and fund its growth.3. Financial Ratios for Analysis:Financial ratios are essential tools used in financial statement analysis to assess a company's performance and compare it with industry benchmarks. Some commonly used financial ratios include:a) Liquidity Ratios:- Current Ratio: Measures a company's ability to meet short-term obligations.- Quick Ratio: Measures a company's ability to meet short-term obligations without relying on inventory.b) Solvency Ratios:- Debt-to-Equity Ratio: Measures the proportion of debt to equity in a company's capital structure.- Interest Coverage Ratio: Measures a company's ability to meet interest payments on its debt.c) Profitability Ratios:- Gross Profit Margin: Measures the profitability of a company's core operations.- Net Profit Margin: Measures the profitability of a company after all expenses, including taxes.d) Efficiency Ratios:- Inventory Turnover Ratio: Measures how quickly a company sells its inventory.- Accounts Receivable Turnover Ratio: Measures how quickly a company collects cash from its customers.4. Translation of Foreign Literature:In this section, we will provide a translation of key points from foreign literature related to financial statement analysis. The literature emphasizes the importance of accurate financial reporting, the use of financial ratios for analysis, and the interpretation of financial statements to make informed decisions.Conclusion:Financial statement analysis is a crucial process for evaluating a company's financial performance and position. It provides valuable insights into a company's profitability, liquidity, solvency, and efficiency. By analyzing financial statements and using financial ratios, stakeholders can make informed decisions regarding investments, credit extension, and strategic planning. Accurate translation and understanding of foreign literature related to financial statement analysis can further enhance the effectiveness of this process.。

财务管理财务分析中英文对照外文翻译文献

独资企业的资产也可以卖给其他公司,只要它还存在。经营者的寿命终止,那么独资企业的寿命终止,虽然资产经营可以通过经营者的继承人。

合伙企业

合伙企业是在两个或更多的人签订协议来经营业务,合伙是相似于个人独资企业,除了所有者替代经营者,这里是不止一个。事实上,有超过一个经营者,介绍了一些问题:谁说在日常经营业务吗?谁是承担经济责任(也就是说最终的责任,)为企业债务?如何分配企业收入? 如何产生纳税收入? 这些问题和合伙协议一起被解决,有些是通过法律进行解决。合伙协议描述损益在合伙人中如何都是分担,它详细企业管理责任。

图例。数学概念利用表格和插图在视觉上被仔细谨慎动态的描述。例如我们指出银行的资产负债增长率通过复利的方式,在数学上表示为次数和柱状图。

实用性。尽可能的,我们要通过实务例子提出的概念和数学公式。例如,我们首先提出财务分析要通过假设一个公司的简化财务报表。最后,你会学到基础的使用假设的公司数据,我们通过沃尔玛超市的数据来证明分析工具,真实的案例帮助我们更好的理解和记住主要的概念和工具。我们对本书中100个真实的公司的案例求积,你不会希望错过它们。考虑到本书案例和研究问题和难题,你将看到无数的真实公司数据。

通过对本书的学习,你将了解我们是如何理解财务的。我们所说的财务决策作为公司所做决策的一部分,不是一个被分离出来的功能。财务决策的做出协调了企业会计部、市场部和生产部。

无论企业的形式和规模如何,财务原理和财务工具均适用。就像对小规模的私营企业而言存在如何筹资的问题,大企业面临所有权和经营权分离时出现的代理问题。不管公司的规模和形式是如何的,公司财务管理的基本原理是一样的。例如,无论是独资企业做出的决策还是大企业做出的决策,今天一美元的价值都高于未来一美元的价值。

mba财务管理参考题目方向

mba财务管理参考题目方向英文回答:1. Financial Statement Analysis.Vertical and horizontal analysis.Common-size financial statements.Trend analysis.DuPont analysis.Ratio analysis.2. Working Capital Management.Cash conversion cycle.Inventory management.Accounts receivable management. Accounts payable management.3. Capital Budgeting.Net present value (NPV)。

Internal rate of return (IRR)。

Payback period.Profitability index.4. Risk Management.Financial risk.Operational risk.Market risk.5. Investment Analysis.Bond valuation.Stock valuation.Portfolio management.6. Financial Planning and Forecasting. Financial planning process.Forecasting techniques.Sensitivity analysis.7. Management Accounting.Cost accounting.Budgeting.Performance measurement.Transfer pricing.8. Corporate Finance.Capital structure.Dividend policy.Mergers and acquisitions.9. Financial Ethics.Fiduciary duty.Conflicts of interest.insider trading.10. International Financial Management.Foreign exchange risk.Currency hedging.International investment.中文回答:1. 财务报表分析。

财务报表分析课程简介

“财务报表分析”课程简介

课程名称:财务报表分析

英文名称:FinancialStatementsAnalysis

课程代码:182035

开设专业:财务管理

课程类型:专业基础课

先行课程:宏观经济学(181007)、财务会计(182029)、财务管理(182030)

内容简介:《财务报表分析》是一门是为培养学生基本理论知识和应用能力而设置的一门专业课。

本课程主要阐述了财务报表分析的基本原理、基本知识和基本方法。

本课程的任务是通过教学,使学生能够系统掌握财务报表分析的基本知识和基本方法,具有较强的财务报表分析能力,

为未来在实际工作中分析会计信息、使用会计信息打下坚实的基础。

教材:

张新民、钱爱民《财务报表分析》第三版,中国人民出版社

参考教材:

1、崔也光主编《财务务报表分析》,天津:南开大学出版社出版,2003年

2、张先治、陈友邦编著《财务分析》(第一版),大连:东北财经大学出版社2004年。

3.金中泉《财务务报表分析》(第一版),北京:中国财政经济出版社出版,2001年。

4.曹冈主编《财务务报表分析》(第一版),北京:经济科学出版社出版,2002年。

声明:此资源由本人收集整理于网络只用于交流学习。

如有侵权请联系删除处理。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Specific Recasting Procedures • Discretionary expenses are segregated • Distinct components are segregated (such as equity in income of

unconsolidated subsidiaries) and often reported net of tax • When components of continuing income are separately

➢ Deductions—tax credits, capital gains rates, tax-free income, lower foreign tax rates

Components can be rearranged, subdivided, and tax effected Total recasted components must reconcile to reported net income

Earnings Persistence

Recasting and Adjusting

Equity Analysis and Valuation

McGraw-Hill/Irwin

12

CHAPTER

© 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Earnings Persistence

Recasting and Adjusting

Earnings Persistence

Recasting and Adjusting

General Recasting Procedures

Income statements of several years (typically at least five) are recast

Recast earnings components to yield meaningful classifications and a relevant format for analysis

reclassified, their pre-tax amounts along with their tax effects must be removed • Income tax disclosures enable one to separate factors that either reduce or increase taxes such as:

❖ Recasting of income statement ❖ Adjusting of income statement

Earnings Persistence

Recasting and Adjusting

Information for Recasting and Adjusting

➢ Income statement, including its subdivisions: Income from continuing operations Income from discontinued operations Extraordinary gains and losses Cumulative effect of changes in accounting principles

• Earnings persistence is a key to effective equity analysis and valuation

• Analyzing earnings persistentive

• Attributes of earnings persistence include:

innovations, work stoppages, and raw material constraints

Earnings Persistence

Recasting and Adjusting

Objectives of Recasting

1. Recast earnings and earnings components so that stable, normal and continuing elements comprising earnings are distinguished and separately analyzed from random, erratic, unusual and nonrecurring elements

2. Recast elements included in current earnings that should more properly be included in the operating results of one or more prior periods

Recasting and adjusting earnings also aids in determining earning power

Stability Predictability Variability Trend Earnings management Accounting methods

Earnings Persistence

Recasting and Adjusting

Two common methods to help assess earnings persistence: