兹维博迪金融学第二版课件Chapter01

兹维博迪 投资学 中文课件

标准普尔指数

标准普尔500指数

涵盖500家公司的指数

市值加权指数

投资者可以购买指数投资组合:

购买与各种指数相对应的共同基金

购买交易所交易基金 (ETFs)

2-25

其他指数

美国的指数 纽约证交所综合指数 纳斯达克综合指数 威尔希尔5000指数

国外的指数 日本日经指数 英国富时指数 德国综合指数 中国香港恒生指数 加拿大多伦多股市指数

2-20

图 2.6 抵押担保证券余额

2-21

权益证券

普通股:

代表所有权 剩余所有权 有限责任 永续性 固定收益 优先于普通服 税务处理

2-22

优先股:

美国存托凭证

股票市场指数

道琼斯工业平均指数

包括30家大型绩优公司 自1896年被计算出来 价格加权平均数

货币市场基金使得个人投资者可以购买各种货币市场 证券。

2-3

图2.1 货币市场的主要组成

2-4

货币市场证券

短期国库券: 美国政府发行的短期债务。

买方报价与买方报价 银行贴现法

大额存单: 银行定期存单 商业票据: 公司发行的短期无担保债务票据。

Байду номын сангаас

2-5

货币市场证券

银行承兑汇票: 银行客户向银行发出在未来某一日期支付 一笔款项的指令。 欧洲美元: 在美国以外的银行以美元计价的存款。 回购协议与逆回购: 由政府证券支持的短期借款。 联邦基金: 银行之间超短期借款。

2-6

货币市场工具的收益率

除了短期国库券,货币市场证券并不是没有违约风险。 银行大额存单一直以来持续支付高于短期国库券的风险溢 价,且该溢价在经济危机期间更大。 在2008年信用危机中, 在一些基金遭遇严重损失后,联邦 政府为货币市场基金提供了保险。

兹维博迪金融学第二版课件

兹维博迪金融学第二版

20

1.5 企业的组织形式

• 独资企业

• 一个人或家庭所有的企业 • 企业的资产和负债是所有者个人的资产和负债 • 无限责任 • 低管理成本

兹维博迪金融学第二版

21

• 合伙企业

• 至少有两个人分享所有权的企业。合伙协议通常 规定如何共同作出决策和利润(损失)如何共享 (共担)。

兹维博迪金融学第二版

8

• 人们利用金融系统来实施其金融决策。金融系统定义为用来订立 金融合约、交换资产与风险的一组市场和其他机构。

兹维博迪金融学第二版

9

• 金融理论包括:

• 一组概念,帮助一个人组织关于怎样跨时配置资 源的思考。

• 一组数量模型,帮助评估备选项、决策和实施决 策。

• 这些概念和模型适用于所有层次和规模的决策

预防损失 • 不动产管理

兹维博迪金融学第二版

41

税务管理

• 税务政策、程序的建立和管理 • 与税收征稽机构的关系 • 税务报告的准备 • 税务计划

兹维博迪金融学第二版

Hale Waihona Puke 42投资者关系• 建立和维护与投资群体的关系 • 建立和维护与公司股东的关系 • 向分析师咨询—公共财务信息

兹维博迪金融学第二版

43

离

• 1.7 管理的目标 • 1.8 市场性管束:收购 • 1.9 财务专家在公司中的

角色

兹维博迪金融学第二版

6

导言

• 我为退休储蓄。我应该用哪一种投资形式? 银行存单、共同基金还是直接买股票?

• 我想有一辆新车。我应该用存款购买还是租用? • 我正在考虑创业。它能带给我足够的回报吗? • 公司正寻求进军电信业。你应该给CFO提供怎样的建

【免费下载】金融市场与金融机构基础Fabozzi Chapter01

Foundations of Financial Markets and Institutions, 4e (Fabozzi/Modigliani/Jones) Chapter 1 IntroductionMultiple Choice Questions1 Financial Assets1) An asset is a possession that has value in an exchange and can be classified as ________.A) financial or intangible.B) financial or variable.C) tangible or intangible.D) fixed or variable.Answer: CDiff: 2Topic: 1.1 Financial AssetsObjective: 1.5: the various ways to classify financial markets2) The financial asset is referred to as a ________ if the claim is a fixed dollar.A) debt instrument.B) common equity instrument.C) derivative instrument.D) preferred equity instrument.Answer: ADiff: 2Topic: 1.1 Financial AssetsObjective: 1.4: the distinction between debt instruments and equity instruments3) A basic economic principle is that the price of any financial asset ________ the present value of its expected cash flow, even if the cash flow is not known with certainty.A) is greater thanB) is equal toC) is less thanD) is equal to or greater thanAnswer: BDiff: 2Topic: 1.1 Financial AssetsObjective: 1.1: what a financial asset is and the principal economic functions of financial assets4) A(n) ________ such as plant or equipment purchased by a business entity shares at least one characteristic with a financial asset: Both are expected to generate future cash flow for their owner.A) tangible assetB) intangible assetC) balance sheet assetD) cash assetAnswer: ADiff: 1Topic: 1.1 Financial AssetsObjective: 1.2: the distinction between financial assets and tangible assets5) Financial assets have two principal economic functions. Which of the below is ONE of these?A) A principal economic function is to transfer funds from those who have surplus funds to borrow to those who need funds to invest in intangible assets.B) A principal economic function is to transfer funds in such a way as to redistribute the avoidable risk associated with the cash flow generated by intangible assets among those seeking and those providing the funds.C) A principal economic function is to transfer funds in such a way as to redistribute the unavoidable risk associated with the cash flow generated by tangible assets among those seeking and those providing the funds.D) A principal economic function is to transfer funds from those who have surplus funds to invest to those who need funds to invest in intangible assets.Answer: CComment: Financial assets have two principal economic functions.(1) The first is to transfer funds from those who have surplus funds to invest to those who need funds to invest in tangible assets.(2) The second economic function is to transfer funds in such a way as to redistribute the unavoidable risk associated with the cash flow generated by tangible assets among those seeking and those providing the funds.Diff: 3Topic: 1.1 Financial AssetsObjective: 1.1: what a financial asset is and the principal economic functions of financial assets6) A principal economic function to transfer funds from those who have ________ to invest to those who need funds to invest in ________.A) deficit funds; tangible assets.B) surplus funds; intangible assets.C) deficit funds; intangible assets.D) surplus funds; tangible assets.Answer: DComment: Financial assets have two principal economic functions.(1) The first is to transfer funds from those who have surplus f unds to invest to those who need funds to invest in tangible assets.(2) The second economic function is to transfer funds in such a way as to redistribute the unavoidable risk associated with the cash flow generated by tangible assets among those seeking and those providing the funds.Diff: 2Topic: 1.1 Financial AssetsObjective: 1.1: what a financial asset is and the principal economic functions of financial assets 2 Financial Markets1) Financial markets provide three economic functions. Which of the below is NOT one of these?A) The interactions of buyers and sellers in a financial market determine the price of the traded asset.B) Financial markets provide a mechanism for an investor to sell a financial asset.C) Financial markets increases the cost of transacting.D) The interactions of buyers and sellers in a financial market determine the required return on a financial asset.Answer: CComment: Financial markets provide three economic functions.First, the interactions of buyers and sellers in a financial market determine the price of the traded asset. Or, equivalently, they determine the required return on a financial asset. As the nducement for firms to acquire funds depends on the required return that investors demand, it is this feature of financial markets that signals how the funds in the economy should be allocated among financial assets. This is called the price discovery process.Second, financial markets provide a mechanism for an investor to sell a financial asset. Because of this feature, it is said that a financial market offers liquidity, an attractive feature when circumstances either force or motivate an investor to sell. If there were not liquidity, the owner would be forced to hold a debt instrument until it matures and an equity instrument until the company is either voluntarily or involuntarily liquidated.While all financial markets provide some form of liquidity, the degree of liquidity is one of the factors that characterize different markets.The third economic function of a financial market is that it reduces the cost of transacting. There are two costs associated with transacting: search costs and information costs.Diff: 3Topic: 1.2 Financial MarketsObjective: 1.3: what a financial market is and the principal economic functions it performs2) The shifting of the financial markets from dominance by retail investors to institutional investors is referred to as the ________ of financial markets.A) globalizationB) institutionalizationC) securitizationD) diversificationAnswer: BDiff: 2Topic: 1.2 Financial MarketsObjective: 1.5: the various ways to classify financial markets3) Financial markets can be categorized as those dealing with newly issued financial claims that are called the ________, and those for exchanging financial claims previously issued that are called the ________.A) secondary market; primary market.B) financial market; secondary market.C) OTC market; NYSE/AMEX market.D) primary market; secondary market.Answer: DDiff: 2Topic: 1.2 Financial MarketsObjective: 1.6: the differences between the primary and secondary markets4) Business entities include nonfinancial and financial enterprises. ________ manufacture products such as cars and computers and/or provide nonfinancial services such as transportation and utilities.A) Financial enterprisesB) Nonfinancial enterprisesC) Both financial and nonfinancial enterprisesD) None of theseAnswer: BDiff: 1Topic: 1.2 Financial MarketsObjective: 1.7: the participants in financial markets3 Globalization of Financial Markets1) Which of the below is NOT a factor that has led to the integration of financial markets?A) A factor is liberalization of markets and the activities of market participants in key financial centers of the world.B) A factor is deregulation of markets and the activities of market participants in key financial centers of the world.C) A factor is technological advances for monitoring world markets, executing orders, and analyzing financial opportunities.D) A factor is decreased institutionalization of financial markets.Answer: DComment: The factors that have led to the integration of financial markets are (1) deregulation or liberalization of markets and the activities of market participants in key financial centers of the world; (2) technological advances for monitoring world markets, executing orders, and analyzing financial opportunities; and (3) increased institutionalization of financial markets. Diff: 3Topic: 1.3 Globalization of Financial MarketsObjective: 1.8: reasons for the globalization of financial markets2) A factor leading to the integration of financial markets is ________.A) decreased institutionalization of financial markets.B) increased monitoring of markets.C) technological advances for monitoring domestic markets, executing orders, and analyzing financial opportunities.D) technological advances for monitoring world markets, executing orders, and disregarding financial opportunities.Answer: DComment: The factors that have led to the integration of financial markets are (1) deregulation or liberalization of markets and the activities of market participants in key financial centers of the world; (2) technological advances for monitoring world markets, executing orders, and analyzing financial opportunities; and (3) increased institutionalization of financial markets. Diff: 2Topic: 1.3 Globalization of Financial MarketsObjective: 1.8: reasons for the globalization of financial markets3) From the perspective of a given country, financial markets can be classified as either internal or external. The internal market is composed of two parts: the domestic market and the foreign market. The domestic market is ________.A) where the securities of issuers not domiciled in the country are sold and traded.B) where issuers domiciled in a country issue securities and where those securities are subsequently traded.C) where securities are offered simultaneously to investors in a number of countries.D) where issuers domiciled in a country issue securities and where those securities are NOT subsequently traded.Answer: BDiff: 2Topic: 1.3 Globalization of Financial MarketsObjective: 1.10: the distinction between a domestic market, a foreign market, and the Euromarket4) A reason for a corporation using ________ is a desire by issuers to diversify their source of funding so as to reduce reliance on domestic investors.A) EuromarketsB) domestic equity marketsC) domestic government marketsD) None of theseAnswer: ADiff: 1Topic: 1.3 Globalization of Financial MarketsObjective: 1.11: the reasons why entities use foreign markets and Euromarkets4 Derivative Markets1) The two basic types of derivative instruments are ________ and ________.A) insurance contracts; options contractsB) futures/forward contracts; indenturesC) futures/forward contracts; legal contractsD) futures/forward contracts; options contractsAnswer: DDiff: 2Topic: 1.4 Derivative MarketsObjective: 1.12: what a derivative instrument is and the two basic types of derivative instruments2) Derivative instruments derive their value from ________.A) market conditions at time of delivery.B) market conditions at time of issue.C) the underlying instruments to which they relate.D) variations in the future claims conveyed from spot markets.Answer: CDiff: 2Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments3) Derivative contracts provide ________.A) issuers and investors an expensive but efficient way of controlling some major risks.B) issuers and investors an inexpensive way of controlling some major risks.C) issuers and investors an inexpensive but inefficient way of controlling all major risks.D) issuers and investors an expensive way of controlling some minor risks.Answer: BDiff: 1Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments4) Derivative markets may have at least three advantages over the corresponding cash (spot) market for the same financial asset. Which of the below is ONE of these advantages?A) Transactions typically can be accomplished faster in the derivatives market.B) It will always cost more to execute a transaction in the derivatives market in order to adjust the risk exposure of an investor's portfolio to new economic information than it would cost to make that adjustment in the cash market.C) All derivative markets can absorb a greater dollar transaction without an adverse effect on the price of the derivative instrument; that is, the derivative market may be more liquid than the cash market.D) Some derivative markets can absorb a greater dollar transaction but with an adverse effect on the price of the derivative instrument; that is, the derivative market may be more liquid than the cash market.Answer: AComment: Derivative markets may have at least three advantages over the corresponding cash (spot) market for the same financial asset.First, depending on the derivative instrument, it may cost less to execute a transaction in the derivatives market in order to adjust the risk exposure of an investor’’s portfolio to new economic information than it would cost to make that adjustment in the cash market. Second, transactions typically can be accomplished faster in the derivatives market.Third, some derivative markets can absorb a greater dollar transaction without an adverse effect on the price of the derivative instrument; that is, the derivative market may be more liquid than the cash market.Diff: 3Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments5 The Role of the Government in Financial Markets1) Which of the following statements is FALSE?A) Because of the prominent role played by financial markets in economies, governments have long deemed it necessary to regulate certain aspects of these markets.B) In their regulatory capacities, governments have had little influence on the development and evolution of financial markets and institutions.C) It is important to realize that governments, markets, and institutions tend to behave interactively and to affect one another's actions in certain ways.D) A sense of how the government can affect a market and its participants is important to an understanding of the numerous markets and securities.Answer: BComment: In their regulatory capacities, governments have greatly influenced the development and evolution of financial markets and institutions.Diff: 2Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.15 the different ways that governments regulate markets, including disclosure regulation, financial activity regulation, financial institution regulation, regulation of foreign firm participation, and regulation of the monetary system2) Which of the below statements is TRUE?A) Because of differences in culture and history, different countries regulate financial markets and financial institutions in varying ways, emphasizing some forms of regulation more than others.B) The standard explanation or justification for governmental regulation of a market is that the market, left to itself, will produce its particular goods or services in an efficient manner and at the lowest possible cost.C) Governments in most developed economies have created elaborate systems of regulation for financial markets, in part because the markets themselves are simple and in part because financial markets are unimportant to the general economies in which they operate.D) Financial activity regulation are free of rules about traders of securities and trading on financial markets.Answer: AComment: The standard explanation or justification for governmental regulation of a market is that the market, left to itself, will not produce its particular goods or services in an efficient manner and at the lowest possible cost.Governments in most developed economies have created elaborate systems of regulation for financial markets, in part because the markets themselves are complex and in part because financial markets are so important to the general economies in which they operate.Financial activity regulation consists of rules about traders of securities and trading on financial markets.Diff: 3Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.14: the typical justification for governmental regulation of markets3) The regulatory structure in the United States is largely the result of ________.A) the first IPO bubble in the 20th century.B) the boom in the stock market experienced in the 1990s.C) bull markets that have occurred at various times.D) financial crises that have occurred at various times.Answer: DDiff: 1Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.16 the U.S. Department of the Treasury's proposed plan for regulatory reform4) The proposal by the U.S. Department of the Treasury, popularly referred to as the "Blueprint for Regulatory Reform" or simply Blueprint, would replace the prevailing complex array of regulators with a regulatory system based on functions. More specifically, there would be three regulators. Which of the below is NOT one of these?A) market stability regulatorB) prudential regulatorC) uninhibited regulatorD) business conduct regulatorAnswer: CDiff: 2Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.15 the different ways that governments regulate markets, including disclosure regulation, financial activity regulation, financial institution regulation, regulation of foreign firm participation, and regulation of the monetary system6 Financial Innovation1) ________ increase the liquidity of markets and the availability of funds by attracting new investors and offering new opportunities for borrowers.A) Market-broadening instrumentsB) Market-management instrumentsC) Risk-management instrumentsD) Arbitraging-broadening instrumentsAnswer: AComment: The Economic Council of Canada classifies financial innovations into the following three broad categories:(1) market-broadening instruments, which increase the liquidity of markets and the availability of funds by attracting new investors and offering new opportunities for borrowers (2) risk-management instruments, which reallocate financial risks to those who are less averse to them, or who offsetting exposure and thus are presumably better able to should them(3) arbitraging instruments and processes, which enable investors and borrowers to take advantage of differences in costs and returns between markets, and which reflect differences in the perception of risks, as well as in information, taxation, and regulationsDiff: 2Topic: 1.6 Financial InnovationObjective: 1.17 the primary reasons for financial innovation2) The Economic Council of Canada classifies financial innovations into three broad categories. Which of the below is NOT one of these?A) market-broadening instrumentsB) risk-management instrumentsC) risk-broadening instrumentsD) arbitraging instruments and processesAnswer: CComment: The Economic Council of Canada classifies financial innovations into the following three broad categories:(1) market-broadening instruments, which increase the liquidity of markets and the availability of funds by attracting new investors and offering new opportunities for borrowers (2) risk-management instruments, which reallocate financial risks to those who are less averse to them, or who offsetting exposure and thus are presumably better able to should them(3) arbitraging instruments and processes, which enable investors and borrowers to take advantage of differences in costs and returns between markets, and which reflect differences in the perception of risks, as well as in information, taxation, and regulationsDiff: 2Topic: 1.6 Financial InnovationObjective: 1.17 the primary reasons for financial innovation3) There are two extreme views of financial innovation. Which of the below is ONE of these?A) Some hold that the essence of innovation is the introduction of financial assets that are less efficient for redistributing risks among market participants.B) There are some who believe that the minor impetus for innovation has been the endeavor to circumvent regulations and find loopholes in tax rules.C) Some hold that the essence of innovation is the introduction of financial instruments that are more efficient for redistributing risks among market participants.D) None of theseAnswer: CComment: There are two extreme views of financial innovation.There are some who believe that the major impetus for innovation has been the endeavor to circumvent (or arbitrage) regulations and find loopholes in tax rules.At the other extreme, some hold that the essence of innovation is the introduction of financial instruments that are more efficient for redistributing risks among market participants.Diff: 2Topic: 1.6 Financial InnovationObjective: 1.17 the primary reasons for financial innovation4) An ultimate and important cause of financial innovation does not involve ________.A) incentives to follow existing regulation and and tax laws.B) increased volatility of interest rates, inflation, equity prices, and exchange rates.C) changing global patterns of financial wealth.D) financial intermediary competition.Answer: AComment: It would appear that many of the innovations that have passed the test of time and have not disappeared have been innovations that provided more efficient mechanisms for redistributing risk. Other innovations may just represent a more efficient way of doing things. Indeed, if we consider the ultimate causes of financial innovation,the following emerge as the most important:1. Increased volatility of interest rates, inflation, equity prices, and exchange rates.2. Advances in computer and telecommunication technologies.3. Greater sophistication and educational training among professional market participants.4. Financial intermediary competition.5. Incentives to get around existing regulation and and tax laws.6. Changing global patterns of financial wealth.Diff: 2Topic: 1.6 Financial InnovationObjective: 1.17 the primary reasons for financial innovationTrue/False Questions1 Financial Assets1) An equity instrument (also called a residual claim) obligates the issuer of the financial asset to pay the holder an amount based on earnings, if any, after holders of debt instruments have been paid.Answer: TRUEDiff: 1Topic: 1.1 Financial AssetsObjective: 1.4: the distinction between debt instruments and equity instruments2) A intangible asset is one whose value depends on particular physical properties such as buildings, land, or machinery. Tangible assets, by contrast, represent legal claims to some future benefit.Answer: FALSEComment: A tangible asset is one whose value depends on particular physical properties such as buildings, land, or machinery. Intangible assets, by contrast, represent legal claims to some future benefit.Diff: 1Topic: 1.1 Financial AssetsObjective: 1.2: the distinction between financial assets and tangible assets3) Financial assets have two principal economic functions. One function is to transfer funds from those who have surplus funds to invest to those who need funds to invest in tangible assets. Answer: TRUEDiff: 1Topic: 1.1 Financial AssetsObjective: 1.1: what a financial asset is and the principal economic functions of financial assets 2 Financial Markets1) The three economic functions of financial markets are: to improve the price discovery process; to lessen liquidity; and, to reduce the cost of transacting.Answer: FALSEComment: The three economic functions of financial markets are: to improve the price discovery process; to enhance liquidity; and to reduce the cost of transacting.Diff: 2Topic: 1.2 Financial MarketsObjective: 1.3: what a financial market is and the principal economic functions it performs2) The market participants include households, business entities, national governments, national government agencies, state and local governments, supranationals, and regulators.Answer: TRUEDiff: 1Topic: 1.2 Financial MarketsObjective: 1.3: what a financial market is and the principal economic functions it performs3) One economic function of a financial market is to reduce the cost of transacting. There are two costs associated with transacting: search costs and information costs.Answer: TRUEDiff: 1Topic: 1.2 Financial MarketsObjective: 1.3: what a financial market is and the principal economic functions it performs3 Globalization of Financial Markets1) Globalization means the integration of financial markets throughout the world into an international financial market.Answer: TRUEDiff: 1Topic: 1.3 Globalization of Financial MarketsObjective: 1.8: reasons for the globalization of financial markets2) The domestic market in any country is the market where the securities of issuers not domiciled in thecountry are sold and traded.Answer: FALSEComment: The foreign market in any country is the market where the securities of issuers not domiciled in the country are sold and traded.Diff: 1Topic: 1.3 Globalization of Financial MarketsObjective: 1.10: the distinction between a domestic market, a foreign market, and the Euromarket3) Global competition has forced governments to exercise control various aspects of their financial markets so that their financial enterprises can compete effectively around the world. Answer: FALSEComment: Global competition has forced governments to deregulate (or liberalize) various aspects of their financial markets so that their financial enterprises can compete effectively around the world.Diff: 1Topic: 1.3 Globalization of Financial MarketsObjective: 1.8: reasons for the globalization of financial markets4 Derivative Markets1) Derivative instruments play a critical role in global financial markets.Answer: TRUEDiff: 1Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments2) IBM pension fund owns a portfolio consisting of the common stock of a large number of companies. Suppose the pension fund knows that two months from now it must sell stock in its portfolio to pay beneficiaries $20 million. The risk that IBM pension fund faces is that two months from now when the stocks are sold, the price of most or all stocks may be higher than they are today.Answer: FALSEComment: IBM pension fund owns a portfolio consisting of the common stock of a large number of companies. Suppose the pension fund knows that two months from now it must sell stock in its portfolio to pay beneficiaries $20 million. The risk that IBM pension fund faces is that two months from now when the stocks are sold, the price of most or all stocks may be lower than they are today.Diff: 2Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments3) When the option grants the owner of the option the right to buy a financial asset from the other party, the option is called a put option.Answer: FALSEComment: When the option grants the owner of the option the right to buy a financial asset from the other party, the option is called a call option.Diff: 2Topic: 1.4 Derivative MarketsObjective: 1.13: the role of derivative instruments5 The Role of the Government in Financial Markets1) The market stability regulator would take on the traditional role of the Federal Reserve by giving it the responsibility and authority to ensure overall financial market stability.Answer: TRUEDiff: 1Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.15 the different ways that governments regulate markets, including disclosure regulation, financial activity regulation, financial institution regulation, regulation of foreign firm participation, and regulation of the monetary system2) Blueprint regulation is the form of regulation that requires issuers of securities to make publica large amount of financial information to actual and potential investors.Answer: FALSEComment: Disclosure regulation is the form of regulation that requires issuers of securities to make public a large amount of financial information to actual and potential investors.Diff: 1Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.16 the U.S. Department of the Treasury's proposed plan for regulatory reform3) Financial activity regulation is the form of regulation that requires issuers of securities to make public a large amount of financial information to actual and potential investors. Answer: FALSEComment: Disclosure regulation is the form of regulation that requires issuers of securities to make public a large amount of financial information to actual and potential investors.NOTE. Financial activity regulation consists of rules about traders of securities and trading on financial markets.Diff: 1Topic: 1.5 The Role of the Government in Financial MarketsObjective: 1.14: the typical justification for governmental regulation of markets。

兹维博迪金融学第二版课件

系统性风险

探索系统性风险的概念,包 括金融危机、政治不稳定和 经济周期波动等因素。

非系统性风险

分析非系统性风险对个别公 司或行业的影响,包括管理 风险、行业竞争和市场需求 波动等。

股票与债券

股票

深入了解股票市场的运作原理, 包括股票的购买、卖出和股息分 红等关键概念。

债券

多元化投资组合

研究债券市场的特点和运作方式, 包括债券利息、到期日和信用评 级等重要信息。

市场环境

1

宏观经济因素

了解宏观经济因素对金融市场的影响,包括经济增长、通货膨胀率和利率等。

2

政治与法律环境

探讨政治和法律环境对金融市场的重要性,包括政策变化、法规制度和国际贸易协议等。

3

社会氛围

分析社会氛围对金融市场的影响,包括人们对投资的态度、价值观和消费习惯等。

市场风险

市场波动

了解市场波动对投资者的风 险和机会,学会管理风险并 制定有效的投资策略。

探索如何建立一个多元化的投资 组合,有效分散风险并实现长期 收益。

经济增长与衰退

1

经济增长

了解经济增长的关键因素,包括生产率提高、投资增加和创新技术的引入等。

2

经济衰退

分析经济衰退的原因和影响,学会应对经济衰退的策略和措施。

3

经济周期

探讨经济周期的特征和不同阶段的投资机会,以及如何利用周期性变化来做出明智的投资决 策。

兹维博迪金融学第二版课 件

欢迎来到兹维博迪金融学第二版课件,本课程将带您深入了解金融市场、市 场环境、市场风险等关键概念。让我们一起开始这个充满挑战与机遇的学习 旅程吧!

课程介绍

在本节中,我们将探讨课程的内容、学习目标以及学习方法。通过本课程, 您将获得对金融学的深入理解,为未来的职业发展奠定坚实的基础。

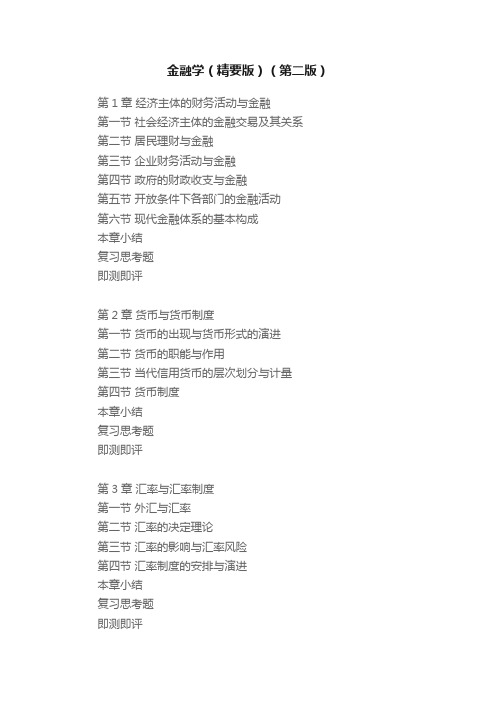

金融学(精要版)(第二版)

金融学(精要版)(第二版)第1章经济主体的财务活动与金融第一节社会经济主体的金融交易及其关系第二节居民理财与金融第三节企业财务活动与金融第四节政府的财政收支与金融第五节开放条件下各部门的金融活动第六节现代金融体系的基本构成本章小结复习思考题即测即评第2章货币与货币制度第一节货币的出现与货币形式的演进第二节货币的职能与作用第三节当代信用货币的层次划分与计量第四节货币制度本章小结复习思考题即测即评第3章汇率与汇率制度第一节外汇与汇率第二节汇率的决定理论第三节汇率的影响与汇率风险第四节汇率制度的安排与演进本章小结复习思考题即测即评第4章信用与信用体系第一节信用概述第二节信用形式第三节信用体系本章小结复习思考题即测即评第5章货币的时间价值与利率第一节货币的时间价值与利息第二节利率分类及其与收益率的关系第三节利率的决定及其影响因素第四节利率的作用及其发挥本章小结复习思考题即测即评第6章金融资产与价格第一节金融工具与金融资产第二节金融资产的价格第三节金融资产定价第四节金融资产价格与利率、汇率的关系本章小结复习思考题即测即评……第7章投融资活动与金融市场第8章货币市场第9章资本市场第10章衍生工具市场第11章金融机构体系第12章存款性公司第13章其他金融性公司第14章中央银行第15章货币需求第16章货币供给第17章货币均衡第18章货币政策第19章金融监管第20章金融发展参考文献。

Bodie2e_Chapter01 Financial Economics 英文版PPT 金融学(第二版)

Financial Decisions of Firms

• Strategic plans specify the business the firm is in

Defining Finance

• Financial theory consists of:

– the set of concepts that help to organize one’s thinking about how to allocate resources over time

– the set of quantitative models used to help evaluate alternatives, make decisions, and implement them

• These concepts and models apply at all levels and scales of decision making

– Preferred stock holders usually gain some control if preferred dividends are not paid

– Bondholder covenants restrict decisions that could adversely affect bond values

– they vary widely in size from part-time businesses run from a spare room, to giant corporations (e.g. Mitsubishi or General Motors) with hundreds of thousands of employees, and an even larger ownership

《金融学》考研博迪第2版重点讲义

《金融学》考研博迪第2版重点讲义博迪《金融学》(第2版)笔记(修订版)第1章金融学1.1复习笔记【知识框架】【考点难点归纳】考点一:对金融学进行界定1金融金融是货币流通、信用活动及与之相关的经济行为的总称。

简言之,就是货币资金的融通。

一般是指以银行、证券市场等为中心的货币流通和信用调节活动,包括货币的发行和流通、存款的吸收和提取、贷款的发放和收回、国内外汇兑往来、有价证券的发行和流通、保险、信托、抵押、典当以及各种金融衍生工具交易等。

按金融中介机构是否充当资金转移的媒介,金融可以分为直接金融(direct finance)和间接金融(indirect finance)。

2金融学金融学是一项针对人们怎样跨期配置稀缺资源的研究。

金融决策区别于其他资源配置决策的两项特征是:①金融决策的成本和收益是跨期分摊的;②无论是决策者还是其他人,通常都无法预先确知金融决策的成本和收益。

金融学是主要研究货币领域的理论及货币资源的配置与选择、货币与经济的关系及货币对经济的影响、现代银行体系的理论和经营活动的经济学科,是当代经济学的一个相对独立而又极为重要的分支。

金融学所涵盖的内容极为丰富,诸如货币原理、货币信用与利息原理、金融市场与银行体系、储蓄与投资、保险、信托、证券交易、货币理论、货币政策、汇率及国际金融等。

3金融体系金融体系是金融市场与金融机构的集合,这些集合被用于金融合同的订立以及资产和风险的交换。

金融体系是由连接资金盈余者和资金短缺者的一系列金融中介机构和金融市场共同构成的一个有机体,包括股票、债券和其他金融工具的市场、金融中介(如银行和保险公司)、金融服务公司(如金融咨询公司)以及监控管理所有这些单位的管理机构等。

研究金融体系如何发展演变是金融学科的重要方面。

4金融理论金融理论由一系列概念和数量化模型组成。

概念帮助人们思考如何在时间上配置资源;数量化模型用于估价替代方案、制定决策和执行决策。

各个层次的决策都采用同样的基本概念和数量化模型。

金融学课件-博迪版

– 如公司不动产价值可能会发生很大变化,但是不会 反映在公司会计报表中

•权责发生制。

36

GPC Income Statement for Year Ending 2xx1

Sales revenues Cost of goods sold *Gross margin Gen sell, & admin exp *Operating income Interest expense *Taxable income Income tax *Net income Allocation to divs *Chg retained earn 200.0 (110.0) 90.0 (30.0) 60.0 (21.0) 39.0 (15.6) 23.4 (10.0) 13.4

37

•教材P62

现金流量表

• 提供一定时期内(一年)现金流流入和流 出企业的信息

– 关注企业的现流状态

• 一个赢利性的企业可能会出现现金短缺

– 与资产负债表、利润表不同,现金流量表独立 于会计方法

•收付实现制。

38

GPC Cash Flow Statement, for the Year ending Dec 31, 2xx0

9%£ /£

16241 ¥ 15450 ¥

149 ¥ /£

£ 109

18

汇率举例

时间

日本

15000 ¥ (borrowed) 3% ¥ /¥(direct) 3% ¥ /£ /£ /¥

英国

150 ¥ /£

£ 100 Invested

9%£ /£

15450 ¥ 15450 ¥ Repaid

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.6 所有权和管理权分离

• 企业所有者将委托管理层管理企业,如果 代理问题(如道德风险)有成本有效解。

– 职业经理有专业技能

– 企业有效规模聚集了大量“小”所有者,不可 能让他们都参与管理

11 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.2 为什么学习金融学?

• 管理个人资源

• 经商 • 追求有趣、高回报的职业机会 • 作为一个公民做出有见识的公共选择

• 智力上的挑战

12 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

金融学

李小龙

lxl@

浙江财经大学金融学院

2016年3月

教学计划

一、金融和金融体系 二、时间与资源配置 三、价值评估模型 四、风险管理与资产组合理论

教材 兹维·博迪、罗伯特·C·默顿、戴维 ·L·克利顿.金融学(第二版).中国人 民大学出版社.2010.

公共邮箱

finance_bmc@

• 营运资本

– 所有企业(包括那些盈利很好的企业),如果不对 营运资本管理足够重视,就可能承受严重损失。现 金的流入流出在时间上并非完全匹配。为了为现金 流赤字融资,为现金流盈余找到好的投资项目,管 理者必须关心向客户收款和及时支付账单。

20 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

– 企业的所有者可能同时还是其他多家企业的所 有者

24 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

– 节省信息搜集成本 – “学习曲线”/“持续经营”效应:若管理者必须 是所有者,则一旦企业转让,新的所有者必须学 习该企业的管理知识和技术,学习成本非常高。 而老的管理者积累起的管理知识和技术却可能无 用武之地。资源双重浪费。所有权与管理权分离 解决了这一问题,可保证所有权频繁转让,管理 层却相当稳定,企业持续经营不被打扰。

– 另一个可能的原则是“利润最大化”,但有两个问题很难解 决:一,企业要考虑多期利润,该最大化哪一期的利润?二 ,企业未来利润存在不确定性,如何比较两个项目的利润? 而股东财富最大化原则就没有这些问题(企业股票价格是确 27 定的)。

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

– 资本结构是企业市场价值归入每一类已发行证券的数 量。它决定企业未来现金流的归属和风险水平【如股 票融资对企业没有撤资风险,债务融资有】 – 资本结构的分析单位是作为整体的企业,而不是一个 投资项目。

18 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.1 定义金融学

• 金融学是对人们怎样跨时配置稀缺资源的 研究。金融决策区别于其他资源配置决策 的两个特征:

– 成本和收益的跨时配置 – 未来现金流实际的时序和规模经常只能以一定 概率知道,而不能完全确知

• 理解金融学帮助你评估这些不确定的现金 流

8 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 在一个竞争的市场上,减少管理弊端的一 个机制是公司收购。例如:

– 客户、供应商、竞争对手或者擅长恶意收购的 企业能较容易地获知公司管理弊端方面的专门 知识 – 恶意收购者控股公司并设置新管理层

– 股价上升,恶意收购者卖出企业获取利润

29 Copy, Inc. Publishing as Prentice Hall

首席财务官

• CFO负责公司所有财务功能

• 合伙企业至少要有一名承担无限责任的合伙人 ,称为普通合伙人。 • 可以有只承担有限责任的合伙人,称为有限合 伙人。有限合伙人一般不参与企业经营管理。

– 所有权变更意味着解除旧合伙关系并形成新合 伙关系。

22 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.3 家庭的金融决策

• 消费和储蓄决策 • 投资决策 • 融资决策 • 风险管理决策

13 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

重要术语

• 资产(Assets)

• 个人投资和资产配置(Personal investing & Asset allocation)

银行存单、共同基金还是直接买股票?

• 我想有一辆新车。我应该用存款购买还是租用? • 我正在考虑创业。它能带给我足够的回报吗? • 公司正寻求进军电信业。你应该给CFO提供怎样的建 议? • 一个拉美国家申请为其大项目贷款。你所在的组织应 该贷给它吗?

7 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.4 厂商的金融决策

• 企业

– 以生产物品和服务为基本功能的实体。 – 企业的规模变化很大,从临时的小生意到有数 十万雇员和更多所有者的巨型公司(如三菱或 通用汽车)。

15 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 管理原则:现有股东财富最大化

– 股东财富最大化原则实现“一致同意”,不用了解股东偏好 ,不用股东参与管理,大大节省决策成本。

– 股东财富最大化原则只依赖于生产技术、市场利率、市场风 险升水和证券价格。该原则引导管理者做出的投资决策与每 一位所有者自己的决策相同【即使一个所有者不喜欢某个最 大化股东财富的风险项目,他还是会实施它,因为实施后卖 掉股份得到的利益比不实施更大】。

17 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 融资过程

– 一旦企业已决定准备实施的新项目,这些项目就必须 用未分配利润、普通股、优先股、债券、可转换证券 、银行贷款、雇员股票期权、租赁合约、退休金债务 等等来融资。

25 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

26 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.7 管理的目标

1.8 市场性管束:收购

– 一家公司的所有权通常

• 是相当分散的和间接的(共同基金) • 缺乏内部的交流渠道 • 很难知悉管理上的弊病 • 不愿为变革买单,不愿组织变革 • 不能抵抗来自一个团结的、自我持续的董事会 的控制 • 不满意时只会抛售股票,这增加了股价向下的 压力

28 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

1.9 财务专家在公司中的角色

公司组织结构图

30 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

首席执行官

• CEO一般是总裁

– 向董事会报告

31 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 1.3 家庭的金融决策

• 1.4 厂商的金融决策 • 1.5 组织企业的形式 • 1.6 所有权和管理权的 分离

6 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

导言

• 我为退休储蓄。我应该用哪一种投资形式?

• 负债(Liability, Debt) • 净值=资产-负债(Net Worth = Assets – Liabilities) • 外生和内生因素(Exogenous and endogenous elements)

14 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

– 一组数量模型,帮助评估备选项、决策和实施 决策。

• 这些概念和模型适用于所有层次和规模的决策

10 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 金融学的基本信条是,经济组织(如厂商 和政府)的存在便利了人们消费偏好的满 足。

• 战略规划确定了厂商进入的行业

– 战略规划可能随时间发生剧烈变化 – 厂商所属行业可以用其产品、技术或顾客来定 义

16 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

• 资本预算过程

– 准备一个计划,以获取实施战略规划的厂房、 机器、实验室、展厅、仓库和人力资本。 – 基本分析单位是投资项目。资本预算过程中, 投资项目被识别、排优先序和实施。