2014年ACCA考试(p3商务分析)考前总结30

2014年ACCA考试(p3商务分析)考前总结1

2014年ACCA考试(p3商务分析)考前总结1本文由高顿ACCA整理发布,转载请注明出处COMMUNICATING CORE VALUES AND MISSIONThis article focuses on the syllabus area relating to an organisation’s core values and mission to the public, shareholders and employees. This is an objective which can easily get overlooked in the rush to master environmental analyses, strategic choice and outsourcing decisionsLearning objective 6(g) of the Paper P3, Business Analysis syllabus relates to how an organisation communicates its core values and mission to the public, shareholders and employees. This is an objective that can easily get overlooked in the rush to master environmental analyses, strategic choice and outsourcing decisions. However, it is important in practice and it is a challenge that many organisations take very seriously. This article will:· briefly describe what the terms ‘mission’, ‘mission statement’ and ‘core values’ mean · suggest why their communication to stakeholders is important· describe a commonly used model of communication· briefly describe communication methods that are available· describe and give examples of how organisations might undertake the communication process.TERMINOLOGYAn organisation’s mission is its basic purpose: What is it for? Why does it e xist? What is its ‘raison d’être’?A mission statement formalises the organisation’s mission by writing it down. Johnson, Scholes and Whittington define a mission statement as ‘a statement of the overriding direction and purpose of an organisation’. Some companies refer to ‘vision statements’ instead of mission statements; some writers and textbooks wring their hands attempting to distinguish between the terms ‘vision’ and ‘mission’. However, the distinction does not achieve much and the Paper P3 exam will treat the terms as meaning the same.Many other writers attempt to expand the definition of a mission statement by adding detail to it. In summary, mission statements are usually assumed to address: · what business is the company in?· whom does the organisation serve?· what benefits are to be delivered?· what are the organisation’s values and ethics?The final line above introduces the concept of values or core values. Johnson, Scholes and Whittington define core values as ‘principles that guide an organisation’s actions’.Remember, there is no standard format or list of contents for mission statements, and organisations are completely free to write their own. However, for most purposes, it is worth distinguishing between a mission stateme nt and a slogan. Nike’s ‘Just do it’ is a powerful advertising slogan, but under most definitions does not qualify as a mission statement. Here are several examples of mission statements and core values:TESCO (A UK SUPERMARKET CHAIN):Our vision To be the most highly valued by:The customers we serve Our core purpose is to create value for customers to earn their lifetime loyalty. This objective sits right at the heart of our business as one part of our Values –‘No one tries harder for customers’.The communities in which we operate For Tesco to be considered a force for good, we must be a good neighbour and a responsible member of society.Our loyal and committed staff We know that if we look after our staff, they will look after our customers. Work can be a large part of our lives so our people deserve an employer who cares. That’s why one of our values is ‘Treat people how we like to be treated’. We are committed to providing opportunities for our people to get on and turn their jobs into careers, and across all of our markets we offer a wide range of competitive benefits.Our shareholders As the owners of the business, it’s crucial that our shareholders value Tesco highly. Shareholders want a good return on their investment and that’s what we will continue to deliver for them. … We offer sustainable, profitable growth from a combination of a strong core UK business and exposure to rapidly growing emerging markets.更多ACCA资讯请关注高顿ACCA官网:。

ACCA P3知识要点汇总(上)

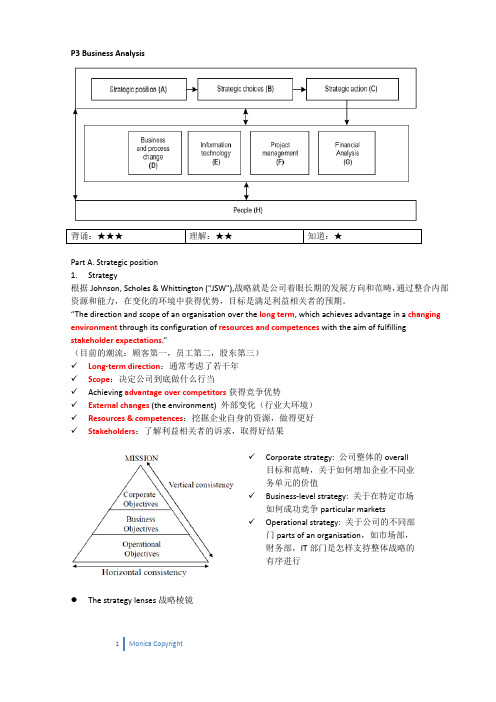

P3 Business Analysis背诵:★★★ 理解:★★ 知道:★Part A. Strategic position1.Strategy根据Johnson, Scholes & Whittington ("JSW"),战略就是公司着眼长期的发展方向和范畴,通过整合内部资源和能力,在变化的环境中获得优势,目标是满足利益相关者的预期。

“The direction and scope of an organisation over the long term, which achieves advantage in a changing environment through its configuration of resources and competences with the aim of fulfilling stakeholder expectations.”(目前的潮流:顾客第一,员工第二,股东第三)✓Long‐term direction:通常考虑了若干年✓Scope:决定公司到底做什么行当✓Achieving advantage over competitors获得竞争优势✓External changes (the environment) 外部变化(行业大环境)✓Resources & competences:挖掘企业自身的资源,做得更好✓Stakeholders:了解利益相关者的诉求,取得好结果✓Corporate strategy: 公司整体的overall 目标和范畴,关于如何增加企业不同业务单元的价值✓Business‐level strategy: 关于在特定市场如何成功竞争particular markets✓Operational strategy: 关于公司的不同部门parts of an organisation,如市场部,财务部,IT部门是怎样支持整体战略的有序进行●The strategy lenses战略棱镜✓Design: 战略的设计应该是理性的rational,自上而下的top‐down process,中级管理层根据战略设定来分析信息,确认一个清晰的行动方案。

ACCAP3学习总结_学习总结_

ACCAP3学习总结范文一在网校ACCA学习期间,给我印象最深的是Emma老师那标准的英式口语,Apple Liu老师对于考官文章的独到见解,还有Ellen Luo 老师利用各种案例对每一个知识点的详细解读。

历经了2年的学习时间,我从F1考到了P3,在这期间有过迷茫,有过怀疑,但庆幸的是,我坚持了下来。

在决定考ACCA之前,我整体计划了自己几年内的考试进度。

目标定在“两年半”考完所有14门!在此我跟大家分享自己对于P3(商业分析)考试的学习心得:1、浏览教材。

注意P阶段的教材都无需细细研读,因为我们不是要去研究这些理论,而是要学会如何运用这些理论见解到实际案例当中。

教材作为一个基础学习只是得工具,有对各项理论的讲解,是我们需要知晓的。

教材中的知识点很多很分散,很容易混淆,不容易记住。

例如教材上strategic planning和strategic marketing两部分涉及内容太多。

只需看一遍教材,把知识点进行整理和规整。

然后把更多的精力花在做习题上,通过习题来复习概念。

2、历年试题。

历年试题是用于熟悉题型和运用知识的。

P3考试出题非常灵活,很多是对概念的灵活应用。

刚开始看题会感觉非常晦涩,甚至连答案都看不懂,因为它不像其他课程有具体的答案,只是给了一个思考的过程,一个判断该用什么理论、模型来解题的过程,用于引导我们的思维。

所以所有的试题都需要反复研读,要学会发散性思维。

3、仔细研读考官文章。

有许多考生遗忘了考官文章的重要性,只是一味地利用教材和历年试题进行学习。

但要注意到了P阶段,教材只能作为一个基础的学习知识的工具,用于理解相关理论的重要来源。

历年试题只是用于熟悉题型。

考官文章详细解读了各种理论框架的适用环境和优劣势,并且详细解读了如何利用现有的知识和经验去解读不同的案例。

里面有很多发散性的问题提问和解答,可以用于扩充知识。

并且多看考官文章可以培养人的发散性思维,从而满足考试的需求。

4、15 mins Reading time 的利用。

2014年ACCA考试(p3商务分析)考前总结26

2014年ACCA考试(p3商务分析)考前总结26本文由高顿ACCA整理发布,转载请注明出处THE CREATIVE ORGANISATION AND KNOWLEDGE MANAGEMENTThe organisational cultural change required to facilitate the focus, development and application of organisational knowledge should include the development of an environment where innovation and creativity operate together.While these two are somewhat intangible, a recent illustration of culture development is the way creativity is part of the culture at Google: ‘Is creativity fun or should it be fun w orks and work is more productive when it is fun … as a result, companies that integrate fun, creativity, and work are best able to attract and retain peak performers in an economy that promotes and rewards the rapid and constant changing of jobs.’Companies are driving towards creativity and innovation. Trends suggest that the knowledge economy is rapidly being transformed into the creativity economy. As more high-level knowledge work is outsourced to less developed countries, companies in the US, Europe, and Japan are at the next level of generating economic value from creativity, imagination, and innovation.Organisations are facing the need to change quickly and dramatically in order to survive, recognising ‘the need for greater product and service in novation to keep pace with technological and societal advances and compete with the growing power of companies in China and other developing countries, rather than focusing on ways to improve efficiency and cut costs. Today’s companies are rewiring for creativity.’The characteristics of creative organisations correspond to those of individuals. Creative organisations are loosely structured. People find themselves in a situation of ambiguity, where assignments are vague, jobs and roles overlap, tasks can be poorly defined, and much work is done through teams.Variety is important, and managers strive to involve employees in a varied range of projects, so that people are not stuck in the rhythm of routine jobs, and they drive out the fear of making mistakes that can inhibit creative thinking.Creative organisations have an internal culture of playfulness, freedom, challenge, and grassroots participation. They harness all potential sources of new ideas as sources for knowledge management. These strategies allow the freedom to discuss ideas, and as projects are seen as long term, resources are allocated without immediate payoff.This creative approach, as with any other policy around new product development, has to be incorporated into the overall company/business strategy. It must also be aligned with a knowledge management strategy, which a company should have in order to gain thevalue evolving within the idea generating process, as well as the knowledge that emerges. This allows creativity to lead to innovation and, in addition, to product or service development and delivery.In terms of the value to be gained, the strategy also needs to include the process of valuation, and the valuation methods and perspectives used to evaluate need to be considered.As accountants, you will need to understand that knowledge – its management, optimisation and valuation – requires focus if it is to be the basis of market success or failure. It is already an area that is being measured in terms of its contribution to the existence of an organisation, and it is therefore a critical success factor, if not already an unrecognised core competence. Talent and knowledge are an organisation’s capabilities and abilities. Talent as capability and knowledge as ability, requires management.更多ACCA资讯请关注高顿ACCA官网:。

ACCAP3知识点总结

ACCAP3知识点总结ACCAP3是ACCA(特许公认会计师)课程的第三阶段,在ACCA考试的过程中是非常重要的一个阶段。

在这个阶段,学员需要掌握更加深入复杂的会计知识,具备扎实的专业能力和解决问题的能力。

以下是ACCAP3的知识点总结:1.管理会计管理会计是指为企业内部管理决策服务的会计。

在ACCAP3课程中,学员需要掌握管理会计的基本概念和技巧,包括成本-收益分析、成本分类、成本控制、绩效评估等方面的知识。

此外,学员还需要了解现代管理会计技术的应用,如活动基础成本管理、质量成本管理、目标成本管理等。

2.管理决策管理决策是管理会计的核心内容之一,涉及企业内部各个方面的决策。

在ACCAP3课程中,学员需要掌握管理决策的基本原理和方法,包括差异分析、边际成本、机会成本等概念。

此外,学员还需掌握现代管理决策模型的应用,如线性规划、灵敏度分析、风险分析等。

3.财务管理财务管理是企业财务决策的核心内容,包括资金管理、投资管理、风险管理等方面。

在ACCAP3课程中,学员需要掌握财务管理的基本原理和技巧,包括财务报表分析、资本预算、财务风险管理等。

此外,学员还需了解国际财务管理的相关规范和标准,如国际金融报告准则(IFRS)。

4.企业战略企业战略是企业长期发展的规划和决策,包括市场定位、竞争战略、资源配置等方面。

在ACCAP3课程中,学员需要掌握企业战略的基本概念和方法,包括SWOT分析、价值链分析、波特五力分析等。

此外,学员还需了解战略规划的实施过程和方法,如平衡计分卡、战略地图等。

5.风险管理6.企业伦理企业伦理是企业社会责任的核心内容,包括企业与员工、客户、股东、社会等各方面的道德义务。

在ACCAP3课程中,学员需要掌握企业伦理的基本原则和规范,包括公平、诚信、责任等。

此外,学员还需了解企业伦理的实施要求和方法,如道德决策模型、伦理审计等。

ACCA P3 考点总结极简版

P3 走近60分 ( Final review of knowledge & Skill Part)1.Strategy can be defined as:‘the direction and scope of an organisation over the long-term, which achieves advantage in a changing environment through its configuration of resources and competences with the aim of fulfilling stakeholder expectations’.CAI’s selection 12. Major TypesStrategic planning involves formal analysis of each of the stages of strategic position before a final strategic choice is made. Strategic planning is useful because:•It forces managers to consider each stage of the strategic process•It forces managers to justify their actions•It forces managers to consider the effect of a strategy on all aspects of the business•It allows managers to be proactive rather than reactive.Emergent strategies involve no long-term strategic plan – in effect, making up the strategy as the organisation goes along. An emergent strategy is useful because:•It allows managers to quickly exploit changing circumstances•It is quicker and cheaper than strategic planning.CAI’s selection 23.Position,Choice,and actionUnder the rational planning model, there are a number of stages. Each of these will be discussed in more detail later in the notes.Stage 1 – Strategic Position1 Identify key stakeholders and their expectations.2 Develop long-term objectives to satisfy these stakeholder expectations.3 Calculate financial and nonfinancial ratios to show position of organisation.4 Identify core resources and competences within the organisation.5 Identify key factors changing the environment outside the organisation.6 Use SWOT analysis (also known as a corporate appraisal) to summarise the strategic position.Stage 2 – Strategic Choices1 Consider possible exit from existing industries.2 Consider diversification into new industries.3 Consider developing new competitive advantages.4 Consider entry into new markets.5 Consider development of new products.Stage 3 – Strategy into Action1. Evaluate above options and choose strategy to be followed.2. Implement any necessary changes in the organisation.3.This might involve changing processes, people etc.CAI’s selection 34.Model Johnson and Scholes – three lensesThis model argues that strategy can be set in different ways:•Strategy as experience.Here the strategy is basically repeating what has been done in the past.•Strategy as ideas.Here the strategy aims to encourage innovation. Culture will be very important here.•Strategy as design.Here the strategy is driven from the top in order to meet the objectives of the organisation. The process is very similar to that given earlier in this chapter.5.MODEL – Mendelow stakeholder mappingThere will always be a conflict of interest between what different groups want. For example giving employees better pay levels reduces the profit available for shareholders. Stakeholders can be divided into:•High Interest with High Power = Key players•Low Interest with High Power = Keep satisfied•High Interest with Low Power = Keep informed•Low Interest with Low Power = Minimal effort.Stakeholders matter because objectives should be geared towards the needs of those with high power. Stakeholders matter because any strategy followed will need to be acceptable to the key players and keep satisfied.CAI’s selection 46.Corporate governanceJohnson and Scholes suggest that corporate governance is about answering two questions:1. Who is the organisation there to serve (i.e. who are the key stakeholders?)?2. How should the priorities of the organisation be decided (i.e. should strategy e planned or should the organisation be opportunistic?)?Johnson and Scholes define the main ethical position for a company as: The extent to which an organisation will exceed its minimum obligations toshareholders.The four main ethical positions are:1. Short-term shareholder interest.2. Longer-term shareholder interest.3. Multiple stakeholder obligations.4. Shaper of society.7.Core values are the principles that guide the behaviour of an organisation.A mission statement explains to the external world and to those managers making strategic decisions inside the organisation, the basic principles theorganisation should be following.A mission statement will commonly contain the following:•Purpose of the organisation.•Overall strategy of the organisation.•The core values of the organisation.Supporters of mission statements claim they help:•Resolve stakeholder conflict.•To guide managers when setting strategy.•Communicate the values of the organisation to employees.•Help with marketing the organisation.CAI’s selection 58.MODEL – Charles Handy types of cultureOrganisational culture consists of the beliefs, attitudes, practices and customs to which people are exposed during their interaction with the organisation.•Power – Heavily centralised with few decision-makers. Allows quick responses to changes in the environment.•Role – Lots of formalised procedures. Can be very useful in an environment that is stable.•Task – Emphasis on getting the job done rather than following rules. Works well in complex, unstable environments.•Person – Purpose is purely to look after the individuals (found where self-employed people are the norm).This may impact on whether a strategy chosen by the Directors is likely to be accepted by the employees.9.MODEL – Miles and Snow – Strategic cultures•Defenders – like strategic options that have worked in the past / low risks / secure markets.•Prospectors – like options that could deliver results even if they entail high risk.•Analysers – will move into new areas but only after someone else has proved they work.•Reactors – do not plan ahead.•The above may impact on the type of decisions made by the organisation.10.MODEL – Johnson and Scholes the cultural web•Rituals and routines – Which procedures are emphasised?•Symbols – Are status symbols used within the organisation as rewards?•Control systems – What is most closely monitored?•Organisational structures – How tall / flat is the organisation?•Power structures – How much centralisation is there?•Stories – Does news within the organisation focus on successes or failures?•The paradigm – What assumptions are taken for granted?CAI’s selection 611.Model – Johnson and Scholes Key drivers of change•Market globalisation•Cost globalisation•Global competition.In addition to the above, if you have a UK company, use:•Economic – conditions as they are at the time of the exam.•Environmental – the move towards more environmentally friendly products (this includes things like materials and packaging).•Legal – minimum wage for unskilled labour.12. MODEL – PESTEL•Political – includes government policies on education and infrastructure.•Economic – includes the state of the economy, interest rates and tax levels.•Social – includes attitudes, demographics and household structure.•Technological – includes new technologies making current products obsolete.•Environmental – includes the move towards environmentally cleaner products.•Legal – includes changes in law making it e.g. harder / more expensive to operate.CAI’s selection 713.Scenario planning•These methods look at what might happen (scenarios) and then decide what the organisation should do if they occur.14.Time Series AnalysisTime Series Analysis is used when sales tend to be seasonal. The time series is made up of two parts:•The long-term trend (calculated using moving averages).•The seasonal variation (calculated as the average of actual figures against the trend).Regression Analysis is used when sales tend to be steady throughout the year.15.MODEL – Porter’s national diamondCompanies based in certain countries seem to be more competitive than companies from other countries. Porter’s diamond looks at why.Porter comes up with 4 reasons for this:•Factor conditions•Firm strategy, structure and rivalry•Demand conditions•Related and supporting industries.CAI’s selection 816.Industries LifecycleIndustries grow and then shrink over time. It is important for a company to consider which industries it is involved in so that it can deliver profits to shareholders over the long-term. The stages the industry goes through are:Introduction•The industry is only just being established.•The industry may be seen as a niche.•At this point there may be only a few competitors (or maybe only one).•Customers may not be entirely sure why they need the product.Growth•An increasing number of customers start to buy the product and reasonable profits can be made.•The industry becomes more attractive and new competitors attempt to join.Maturity•The industry typically goes through a period of consolidation.•Weaker companies might leave.Decline•Customers are buying different products and so total sales are falling.•The industry may again become a niche.•As part of its corporate strategy, a company should regularly review the industries it is in to decide whether to:•Exit from existing industries.•Enter into new ones.CAI’s selection 917.Porter’s 5 forcesPorter’s 5 forces model looks at why some industries might be more profitable than others. In general the more of the forces that are favourable within an industry the more profits will be earned. Unfortunately as the industry becomes more attractive then more rivals will want to enter it.The 5 forces are:•Competitors (new)•Competitors (existing)•Customers•Suppliers•Substitutes.18.MODEL – The marketing mix•Product – What the customer receives•Price – the Cost to the customer•Place – the convenience to the customer•Promotion – how does the company Communicates with the customer19.CSF & KPICritical success factors are those elements that an organisation must perform properly in order to succeed. These often link with competences.•Threshol d competence•Core competen ces.CAI’s selection 10A common way of thinking about KPI’s is to group them into various categories. One common approach is to use:•Econo my – the amount spent on inputs (materials, labour, marketing etc).•Effectiveness – whether customers are satisfied with the products / services provided (customer satisfaction, repeat customers etc).•Efficiency – how good the organisation is at turning inputs into outputs (wastage, idle time etc).20.MODEL – the nine M’s modelThis model gives nine possible areas an organisation might be strong in•Machinery•Money•Materials•Men and Women•Makeup (culture)•Markets (products)•Management information•Management•Methods (processes).In the exam, look at the numbers that the Examiner gives you (particularly ones that do not fit into Financial Accounting areas). These often indicate weaknesses. Examples could include:•Sales per employee•Age of machinery•Time taken to process orders.CAI’s selection 1121.Cost controlOne common threshold competence in the exam is cost control.This is important to public sector organisations as they may have a fixed income.This is important to companies as they are trying to make a profit. If costs increase then either they have to accept lower profits or attempt to pass this on to customers through higher prices. The likelihood of costs rising will be affected by the power of the organisation’s suppliers.The possibility of raising sales prices will be affected by the power of customers. Costs could be reduced through:•Economies of scale•Low supply costs•Sensible design•Experience.CAI’s selection 1222.Sustainable competitive advantageSustainable competitive advantage is about the reasons a customer buys from one firm rather than another.The key word here is “sustainable”, a resource may give an organisation an advantage in the short-term but this will not be sustainable if it is easy for competitors to acquire as well.Similarly a competence that can easily be copied by others will only give a short-term advantage.Sustainable competitive advantage will need to focus on resources and capabilities which are:•Rare (this could include patents or a skill).•Robust (things that are difficult to imitate). Examples include:o Complex procedureso Uncertainty to outsiders.•Difficult for a customer to substitute with somethi• A final thing to remember is that the customer must be willing to pay for this unique resource or core competence.CAI’s selection 1323.MODEL – Porter’s value chainPorter divides a business into nine different areas. The five primary activities are:•Inbound logistics•Operations•Outbound logistics•Marketing and sales•Service.The four secondary activities are:•Firm infrastructure•Human Resource Management•Technology Development•Procurement.Porter argues that each cost in the business is one of two types.•Value-adding – the extra cost is outweighed by the extra the customer is willing to pay•Non value-adding – the extra cost is not valued by the customer.CAI’s selection 1424.Knowledge managementThe knowledge that an organisation has is a resource that may be difficult for other organisations to acquire and so can be a source of competitive advantage.For this to happen the organisation must record the knowledge of its employees and make it available to others.Knowledge management is the collective and shared experience accumulated through systems, routines and activities of sharing across the organisation.25.MODEL – Nonaka and Takeuchi on tacit and explicit knowledgeTacit knowledge is knowledge that staff possess. They are often unaware of how important this knowledge is. Explicit knowledge is knowledge that has been recorded by the organisation.Nonaka and Takeuchi say knowledge can be transferred by:•Socialisation•Externalisation•Internalisation•Combination.CAI’s selection 1526.SWOTOnce the organisation has analysed the external and internal environments it should be able to identify:•Strengths•Weaknesses•Opportunities•Threats.It is important to remember that strengths and weaknesses are in the eye of the customer not the company.It is important to remember in the exam that opportunities and strengths need to match up. If there is an opportunity for which the organisation does not have a matching strength – then the organisation will not be able to exploit the opportunity.Strategic capability can be improved by:•Extending competences•Ceasing nonessential activities•Extending best practices•Adding or improving activities•Remedying weaknesses.CAI’s selection 1627.Benchmarking•Historical comparisons are made between actual and past figure to see if the organisation is improving / deteriorating.•Strategic– comparisons are made between actual and budget (note that the budget should be set at a level so that meeting the budget should mean the critical success factor is achieved).•Industry – comparisons are made between actual and performance of others to see if we are performing better or worse than our rivals (this will identify strengths and weaknesses).28.Balanced scorecardAll processes must be as efficient and effective as possible in order to support the strategy. This means the organisation will need some method of measuring performance. One common method is to use the balanced scorecard. Processes can be measured to see if they are helping the following perspectives:•Financial•Customers•Internal business•Innovation and learning.CAI’s selection 1729.MODEL – Ansoff’s growth vector matrixIgor Ansoff came up with a simple method of identifying strategic options. The areas for a business to consider are:•Should they carry on selling their existing products?•Should they carry on selling to their existing market (this means the types of customer they already target)?Ansoff comes up with four possibilities:•Market penetration – existing products and existing markets•Market development – existing products and a new market•Product development – new products and an existing market•Diversification – new products to a new market.30.Methods?We will look at all of these in turn in this sectioWhichever of these is chosen there is an additional decision to be made. Should the organisation:•Grow organically – should the organisation launch a new product / go into a new market themselves?•Grow by acquisition – should the organisation buy another company that sells a new product / operates in a different market?A company can attempt to enter a foreign market in a number of ways. The main ones for a manufacturer are:Direct exporting – selling directly to overseas customers.•Advantages – the company gets to know the needs of the final customer•Disadvantages – it may be costly to build up customer awareness.Indirect exporting – selling to intermediaries such as retailers who then sell to final consumer.CAI’s selection 18•Advantages – the company gets access to the local company’s knowledge•Disadvantages – the company will not see all of the profits.Overseas production– the company manufactures and sells the products in the target country.•Advantages – distribution costs will be reduced•Disadvantages – may require a large capital investment.Contract manufacture (licensing) – the product is made abroad by another company.•Advantages – lower risk since no need to build manufacturing plant•Disadvantages – may lose control over areas such as quality.Joint ventures – the company goes into partnership with a local company.•Advantages – lower risk since local knowledge gained and costs shared•Disadvantages – lower returns since profits shared.CAI’s selection 1931.MODEL – Porter’s generic strategiesA further possibility would be to change HOW the company competes (the business strategy). This means changing the reason why customers should buy theproduct. Porter comes up with three possibilities:•Cost leadership•Product differentiation•Focussing on a particular type of customer.32.MODEL – The BCG matrixIn the exam you may have to calculate the market share of a product. If the information is available it would also be useful to calculate profit margins for each product.•Cash cows are in the mature or decline stage of the life cycle:o The threat of new competitors is low and the high market share makes the threats from substitutes and existing competitors low as well.o This product should be earning reasonable profits.o The product cannot grow any further (since the market is already mature).•Stars also have a high market share:o The market is growing (introduction or growth stage of the lifecycle) so new competitors will be attracted into the marketo Prices may need to be kept low to maintain market shareo Marketing costs might also need to be high to keep sales upo Profits may not be high.•Question marks have a lot of potential due to the high growth. Decision is whether to:o Spend money to build up market shareCAI’s selection 20o Spend money to hold market shareo Leave market.•Dogs have low market share and low growth. They should be closed unless needed by one of the other products.33.Related diversificationRelated diversification (also known as concentric diversification) means moving into areas that are similar to those the business already operates in.The idea is use the current strengths of the company to exploit new opportunities. In the exam look for examples of:•Horizontal integration – e.g. a shirt manufacturer that starts manufacturing shoes•Backwards integration – e.g. a shirt manufacture that starts manufacturing cloth•Forwards integration – e.g. a shirt manufacturer that starts retailing clothes.CAI’s selection 2134.Model Johnson and Scholes strategic rationale•P ortfolio Managers•Synergy managers•Parental developers35.Ashridge ModelThe four groups are:•High Feel / High BenefitHeartland businesses which gain most benefit from the attention of the parent (concentrate on these).•High Feel / Low BenefitBallast businesses which would be just as viable if they were independent businesses (so leave these ones alone to run themselves).•Low Feel / High BenefitValue Trap businesses which do not have much overlap with the skills of the parent (these may have been acquired as a method of unrelateddiversification). Unless the parent can develop these skills the business may not be of much benefit.•Low / Feel / Low BenefitAlien businesses which should be sold off.From this follows the idea that the amount of cost being spent by the parent should reflect the value it adds to the divisions.CAI’s selection 2236.Model – Johnson and Scholes SFA testJohnson and Scholes suggest that for any option to be considered seriously it must pass three tests. The option must be:•Suitable•Feasible•Acceptable.A strategic option is suitable if:•It builds on strengths/ reduces weaknesses / exploits opportunities / avoids threats.•Gives a new competitive advantage / maintains an existing one.•Suits the organisation’s culture .•It fits with the current strategies already being aA strategic option is feasible if:•The organisation has enough finance to pursue it.•The organisation has the rights skills / knowledge / experience to pursue it.•The company will be able to deal with any responses from competitors.•The company has enough time to follow the strategy.A strategic option is acceptable if:•The additional reward if the strategy is successful is greater than the risk if it is unsuccessful.•The additional risk is acceptable to shareholders / banks etc.•It helps the company to meet its financial objectives (ROCE etc) – shareholders.•Any interest payments will be maintained – banks.•It does not break any regulations – government.•It does not adversely affect connected stakeholders – customers / suppliers.CAI’s selection 2337.Financial RatiosThe following are common causes for ADVERSE variances;•Materials price Powerful supplier Change of supplier•Materials usage Poor quality material•Labour rate Powerful supplier•Labour usage Poor quality labour•Overhead efficiency Poor levels of maintenance•Sales price Powerful customersMany substitutes•Sales volume Sales lost to new entrantsMany competitorsCAI’s selection 2438.Decision treeA decision tree is another quantitative method for looking at uncertainty.A decision tree is a diagrammatic approach to solving problems involving probabilities and decision making.MethodStep1: Draw the tree from left to right showing appropriate decisions andUsefor a decision point,and an outcome point.Label tree and cash inflows/outflows and probabilities associated with outcomes.Step2: Evaluate the tree from right to left.•Calculate an expected value at each outcome point.•Select the option to maximise expected payoff at each decision point.Step3: Recommend a course of action to management.CAI’s selection 2539.Model Harmon’s process-strategy matrixThere are four approaches to change depending on:•Is the pro cess strategically important? (does it tie up with SWOT); and•Is the proces s complex?This leads to•High importance / complex Improve processes focusing on staff•High importance / simple Use an automated ERP solution•Low importance / complex Outsource•Low import ance / simple Automate.40.OutsourcingIt will often be more efficient to outsource these since the outsourcing company can obtain economies of scale.Problems with outsourcing processes include:•Fragmentat ion of complex processes (outsourcers can only do part of the process).•Concerns with relying on others for key business processes.•Concerns about quality.•Unwillingness to be locked into long-term contracts.41.Evaluating Business ProcessesProcess improvement methods•Lean proce sses – eliminate nonvalue adding activities or time between activities.CAI’s selection 26•Human perfor mance analysis – redesign incentives, improve training.Process redesign methods•Automa te activities.•Integrate processes – to reduce gaps and disconnects.•Process Measu rement schemes – develop or redesign the way performance ids measured.42.Model – Skidmore and Eva – stages in selecting software package•The company may decide to have a software package written especially (known as a bespoke package). There are five stages the company goes through:•Obtain tenders•First pass selection•Second pass selection•Implementation•Managing long-term relationship.CAI’s selection 2743.6C- the benefits of E-businessThe above definition does NOT mean that goods / services have to be sold to customers over the internet – this is referred to as ecommerce. Benefits of adopting e-business include:•Cost reduction•Capability•Communication•Control•Customer service•Competitive.44.Model – McFarlan’s gridMcFarlan’s grid looks at how important IT is to the organisation, in particular, how it can help with the organisation’s strategy.•The impact of current IT systems on gaining an advantage.•The potential impact of future IT systems on gaining an advantage.1. Current Low / Future low SupportIT is useful but no advantage is being achieved (e.g. payroll).2. Current High / Future low FactoryIT is crucial to the current operations but it is unlikely that it can be developed further to give an advantage in the future( e.g. a JIT system).CAI’s selection 283. Current Low / Future High TurnaroundIT can be used to develop new advantages over the long-term (e.g. Amazon’s Kindle e-reader and store).4. Current High / Future High StrategicIT will be fundamental to the ongoing success of the business.45.Model 6i’s for emarketing1 Interactivity – Customers can be asked for contact details.2 Integration – Adverts on the web can be clicked to go straight to purchasing.3 Intelligence – websites can record how many visitors they have and what they do on the website.4 Industry structure – Websites can change distribution channels (by cutting out intermediaries and selling direct).5 Independence of location.6 Individualisation – if a customer regularly visits a website it can be tailored to that individual.46.Model – Adcock’s guide to CRMCRM is the establishment, development, maintenance and optimisation of long-term mutually valuable relationships between consumers and organisations.CRM has many benefits including:•Improved retention•Improved cross-sellingCAI’s selection 29Improved profitability.In order to build relationships with customers, businesses need to:•Build a customer database•Develop customer oriented service systems•Have more direct contacts with customers.As part of this process, businesses should think about their long-term relationship with customers and what that is likely to be worth over the customer’s lifetime. CAI’s selection 30。

2014年ACCA考试(p3商务分析)考前总结6

高顿财经ACCA 2014年ACCA 考试(p3商务分析)考前总结6本文由高顿ACCA 整理发布,转载请注明出处 ELEVISION/VIDEO – THE COOPERATIVE GROUPTelevision advertising is often used to promote values and mission. A 60-second advert will never contain a vast quantity of detailed information but a well-shot short film can be very effective indeed at getting across an organisation’s ethos, particularly to external stakeholders.The Cooperative Group is a diverse UK organisation that includes supermarkets, a bank, insurance, travel, legal services and funeral care. It is a mutual organisation, owned by its customers and has been very successful in differentiating itself by promoting a very ethical approach to business. The ad is quite long, but shows the care and expense that the organisation went to try to communicate its values.TELEVISION/VIDEO – ETIHADThis video example is too long for a television advert but was used for staff recruitment and training.Listen to the words relating to mission and values that the film packs in: challenging the status quo, change, a belief that nothing is impossible, continual striving, embrace optimism and creativity, vision is to be a driving force of change in the industry, see things differently, hospitality, multinational crew, vision of a more elegant flight experience, innovative design, attempt to meet diverse needs, investment in customers, continual growth, challenge and creativity.更多ACCA 资讯请关注高顿ACCA 官网:。

ACCA P3 经验总结

这是我在备战P3时,针对P3的历年真题,逐题,逐字逐句,根据考点,结合BPP练习册的答题点,考官给的答题点,总结出的。

老实说,我P3考了两次,第一次是跟着高顿的lily老师上课,做题,后来发现只做题,不总结是徒劳的。

所以第二次考的时候,我因为对模型的理论已经了解了,就只刷题。

这是我自己根据ACCA的notes 上的每章考点,再结合历年真题,翻译,总结套路,然后背诵。

共250页

以下是一些截图

只需要背会了这些套路就可以过啦

需要的可以联系QQ :290988738

备注:P3历年真题总结讲义

售价:20元

相信我肯定会对你有用的

(相对于P3的考试费来说,真的是太便宜了好吗,真的是百分之一的价格都不到啊我就是靠这个过的,花了足足3个月的时间来准备这次考试)

只需要背会了这些套路就可以过啦

需要的可以联系QQ :290988738

备注:P3历年真题总结讲义

售价:20元

相信我肯定会对你有用的

(相对于P3的考试费来说,真的是太便宜了好吗,真的是百分之一的价格都不到啊我就是靠这个过的,花了足足3个月的时间来准备这次考试)。

2014年ACCA考试(p3商务分析)考前总结2

2014年ACCA考试(p3商务分析)考前总结2本文由高顿ACCA整理发布,转载请注明出处INTEL (A MANUFACTURER OF COMPUTER CHIPS):Our missionThis decade we will create and extend computing technology to connect and enrich the lives of every person on earth.Our values Customer orientation Results orientation Great place to work Quality Discipline Risk taking.ACCAACCA's mission is to:· provide opportunity and access to people of ability around the world and support our members throughout their careers in accounting, business and finance· achieve and promote the highest professional, ethical and governance standards · advance the public interest· be a global leader in the profession.ACCA's core values are:· Opportunity: we provide opportunity, free from artificial barriers, to people around the world – whether students, members or employees and we support them in their careers.· Diversity: we respect and value difference, embracing diversity in our people and in our output.· Innovation: we create new and unexpected possibilities, providing innovative solutions for the future.· Accountability: we accept individual and corporate responsibility for our actions, working together to deliver a quality service and to promote the best interests of our stakeholders.· Integrity: we act ethically and work in the public interest, treating people fairly and honestly; we encourage the same from others.WHY COMMUNICATION OF MISSION AND CORE VALUES TO STAKEHOLDERS IS IMPORTANT· Investors need to know how the organisation intends to make profits or fulfil some other ambition.· Directors and other employees need to know the organisation’s purpose, and how it intends to add value and to compete.· Customers may wish to know what the organisation promises.· All stakeholders should want to know how the organisation intends to conduct its operations; the principles that guide its actions; its moral and ethical ‘compass’.For example, it is clear from Tesco’s mission statement that it places the highest emphasis on its long-term relationship with customers. This should guide management and staff as they make day-to-day strategic, tactical and operational decisions. To a large extent the other three parts of their vision statement flow from the first: customers, their families and friends will be part of the community, so it is important to deal fairly with that; staff are the company’s interface with its customers; if customers are well looked after and are loyal, good financial results should follow.If Tesco had not placed such emphasis on its customer relationships it is likely that the goods it stocks, sales promotions, customer facilities, prices and quality would all subtly change. Tesco is saying to all that it lives or dies by the strength of its customer relations.Of course, a strong and focussed mission does not guarantee success and in January 2012 Tesco suffered a 16% fall in share price after it announced its results. In response to this, the chief executive said that the company needed to reconnect with its customers and that Tesco needed to sharpen up its act in the quality and availability of its goods and the service it offered customers. The company planned to invest cash to put more people into the right stores, in the right areas, and to train them to be even better so they can look after the product and customers.Intel places its sphere of business in the technology sector and has an international outlook. Nothing surprising there, but interesting detail is added in its core values. Perhaps t he juxtaposition of discipline’ and ‘risk’ is most noteworthy. Stakeholders are made aware that a high tech company will only survive by taking risks (not all research and development will pay off), but this must be counter-balanced by a disciplined approach to market research, forecasting, expenditure and deadlines.ACCA states very plainly that at its heart is the provision of opportunities to all nationalities and a diverse population. This will influence management, employees, students and members. Without the strong international reference, presumably ACCA would be much more likely to concentrate on a narrow, local market. Additionally, there is great emphasis on ethics and accountability.Communicating objectives to stakeholders is likely to require different messages to each stakeholder group (for example, customers do not need to know about detailed cost objectives given to employees). However, mission and core values are long-term public commitments and promises, and it is vital that they are consistent otherwise they are quickly undermined. There is no point preaching to customers that the company aims tohave a low carbon footprint while at the same time telling employees not to bother with recycling. Inconsistencies and half-heartedness will quickly be exposed and are likely to cause the organisation reputational damage – at the very least.更多ACCA资讯请关注高顿ACCA官网:。

ACCA考试技巧:P3 Business Analysis

ACCA考试技巧:P3 Business Analysis本文由高顿ACCA整理发布,转载请注明出处KaplanSection AEnvironmentalanalysis, people with financial analysis.Section BProjectmanagement.Strategicaction.Informationtechnology – pricing strategy.BPPGeneraladviceIfwe look back at the 2014 P3 exams we can see that the examiner has againrequired students to have a very good grasp of the syllabus, both breadth anddepth, combined with an ability to apply that knowledge to the specificcircumstances of the scenario.Inaddition it is clear that the examiner likes to keep students on their toes byincluding substantial “random” elements within questions that are from areasthat could be either be considered to be from the fringes of the syllabus orare based largely on knowledge carried forward from earlier papers. Forinstance in the June 2014 paper there was a 10 mark question on benefitsowners, maps and realisation and in December 2014 risk management and linearregression were included.Itis therefore extremely dangerous for any student to focus on certain elementsof the syllabus at the expense of others. To stand the best chance of passingP3 students need to have a good understanding of the entire syllabus. This willenable them to choose the questions where they believe they will find it easierto pick up marks (for instance becauseit is easier to understand therequirements, or easier to structure an answer, or easier to pick up knowledgemarks) rather than having to choose questions because of the syllabus area.Inaddition if students were to look at the exams in the past couple of years theywill see that all of the key areas of the syllabus have been examined over thepast four or five sittings which again shows the danger of question spotting orignoring areas.Importantareas to cover for the June 2015 exam include:Itcould be argued that the following areas, despite being key syllabus areas thathave been regularly examined, have not been examined significantly in the pastcouple of papers, and therefore may be a little more likely to surface (howeverremember that this is a very dangerous game to play if it distracts studentsfrom other syllabus areas):– Strategy Lensesand approaches to strategy– Mission, Cultureand Ethics– Critical successfactors and KPIs– Role of thecorporate parent including BCG matrix/Ashridge– People,leadership, job design and staff developmentItis certainly worth a reminder that a number of new elements were brought intothe syllabus in 2014. It could be argued that the examiner may take theopportunity to test these specifically because they are relatively new andtherefore students should ensure that they are familiar with:– IntegratedReporting– Changemanagement frameworks (POPIT and the business change lifecycle) and– OrganisationalConfiguration – new definitions: Boundary-less organisations, –Outsourcing vs.Offshoring, Hollow and Modular structuresFinallyit is worth pointing out first that the December 2014 paper saw a significantnumerical element (two out of four questions, including Q1) requiringinterpretation, calculation or both, and second, that the exam continues tofeature visual aspects such a process diagrams, organisational charts and datatables, thus practising interpretation of these from past questions isrecommended as we would fully expect both to continue in June this year.LSBFStrategicanalysis (external in particular).Calculationand interpretation of basic financial ratios.Usingthe SFA model to evaluate strategic options.Improvingbusiness processes using IT (and the IT controls required).Makingstaff more efficient and effective.TheBusiness Change lifecycle (including the POPIT approach).更多ACCA资讯请关注高顿ACCA官网:。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

高顿财经ACCA 2014年ACCA 考试(p3商务分析)考前总结

30

本文由高顿ACCA 整理发布,转载请注明出处 FIGURE 2: STAGES OF THE PROJECT LIFECYCLE

All projects will start from an initial idea, perhaps embedded in the strategic plan. A project will then progress to the initiation stage when a project manager will be

appointed. The project manager will choose a project team and they will carry out a feasibility study. The feasibility study is necessary to establish the following: · Commercial feasibility – will the likely benefits exceed the cost?

· Technical feasibility – do we think this project has a good chance of working? · Operational feasibility – will it help the organisation reach its objectives?

· Social feasibility – will our employees, customers and other stakeholders tolerate it?

A feasibility report should be produced and this will have to be studied by senior managers, because if the project goes ahead substantial expenditure might be required. Note that the feasibility report does not merely have to present management with simple ‘yes’ or ‘no’ options, but can set out a range of options, each with particular benefits, costs and time frames. Where there is some doubt as to the potential benefits that will arise from the project, it is particularly valuable to offer a range of choices which allow the organisation to first try out a modest project and later allow the project to be extended. This approach is a useful way to reduce risk. If you are not sure about something, start in a small way and extend later if worthwhile

更多ACCA 资讯请关注高顿ACCA 官网:。