上财CGA AU2 Module 1 2013

上海财大金融金融学院培养方案

23 国际金融理论与实务

2

√

金融学院

250247

24 行为金融学

2

√

金融学院

250248

25 金融模拟与实务

2

√

金融学院

/eams/allMajorPlanSearch!info.action?planId=33456

备注

证券投资选 修模块 证券投资选 修模块 证券投资选 修模块 证券投资选 修模块 银行管理选 修模块 银行管理选 修模块 银行管理选 修模块 银行管理选 修模块 公司金融选 修模块 公司金融选 修模块 公司金融选 修模块 国际金融选 修模块 国际金融选 修模块 国际金融选 修模块 国际金融选 修模块 公共选修模 块 公共选修模 块

硕士研究生 普通研究生 金融学院 金融硕士专业 金融分析师 培养计划 (2012-9)

分类 课程代码

课程名称

按学期学分分配

学分

1

2

3

4

开课院系

学位 250252

1 社会主义经济理论

公共 第一外语模块课

课

学分小计

2√

22

2

22

经济学院

250491

学位 250492 基础 课 250493

2 金融计量学 3 会计学 4 经济分析

1/2

2014年12月10日

250249 250250 250251 250496 250497 250498 任意选修课

实践 250353 教学 环节

250351

备注

26 保险学

/eams/allMajorPlanSearch!info.action?planId=33456

250236

上海财经大学科研管理系统用户手册-上海财经大学经济学院

附件一上海财经大学科研管理系统用户手册适用对象:学生目录第一章引言 (3)第二章操作指南 (4)1.1系统登陆 (4)1.2密码维护 (4)第三章业务管理 (6)3.1校级项目 (6)3.1.1项目申报与立项 (6)3.1.2项目变更 (9)3.1.3项目结项 (10)第一章引言随着计算机技术的发展和高校办公自动化的建设,使科研管理工作更加规范化、科学化,建设一个科研管理信息系统已显得非常重要。

通过科研管理系统建设,可以实现科研工作的网络化管理,形成一个动态的科研数据中心和科研管理沟通平台,全面、实时、准确提供学校的有关科研信息,服务于高校学生和科研人员,辅助领导进行科研管理决策。

高校科研管理信息系统包括科研项目管理、科研成果管理、学术会议管理、科研获奖管理等。

编写目的本文档面向学生,用于指导项目管理功能模块的操作、使用。

第二章操作指南1.1 系统登陆访问学校“公共数据平台”,进入“我的科研”标签,点击“科研管理信息系统”入口后即可访问系统;在浏览器(推荐IE)地址栏中输入“”,出现系统的登录界面,如下图所示,在管理平台入口输入用户名和密码及对应的验证码,点击“登录”即可进入科研管理系统,用户名为学号,初始密码为学号后六位,登录后请及时修改密码。

系统界面登录示意图1.2密码维护密码设置登录到系统首页界面我们可以看到页面顶部【密码维护】,点击【密码维护】进入密码修改页面,修改后的密码为用户登录系统默认密码。

如《密码维护示意图》所示:密码维护示意图第三章业务管理3.1校级项目包括项目的申报、立项、变更、中检、结项等流程管理。

3.1.1项目申报与立项管理流程如下图:项目申报学生通过【项目申报】功能进入申报信息列表,选择预申报的项目,点击【进入申报】链接进入项目申报材料信息列表。

如《申报信息列表页示意图》所示:申报信息列表示意图进入到项目申报材料列表页。

如《项目申报材料列表页》所示:项目申报材料列表示意图点击【新增】进入项目申报页面。

上海财大ACCA F1讲义1

• (c) Organisations save time. • (d) Organisations accumulate and share knowledge. • (e) Organisations enable synerge.

• 2.2 Private vs public sector

– Private sector

• Organisations not owned or run by central or local government, or government agencies.

– Public sector

?13howorganisationsdifferownershippublicvsprivate?ownedbythegovernmentpublicsectororganisations?ownedbyprivateownersorshareholdersprivatesectororganisationscontrol?controlledbytheownersthemselves?controlledbypeopleworkingontheirbehalf?indirectlycontrolledbygovernmentsponsoredregulatorsactivityprofitornonprofitorientationlegalstatus?limitedcompanies?partnershipssizesourcesoffinance?borrowingfrombanks?governmentfunding?issuingsharestechnology?varyingdegreesoftechnologyuse?14whattheorganisationdoesorganisationsdomanydifferenttypesofwork2typesofbusinessorganisation?21profitvsnonprofitorientationprofitorientation?maximiseprofittoownersnonprofitorientation?provisionofgoodsservicestopublicbeneficiaries?22privatevspublicsectorprivatesector?organisationsnotownedorrunbycentralorlocalgovernmentorgovernmentagencies

ca_exm_au2_2007-12

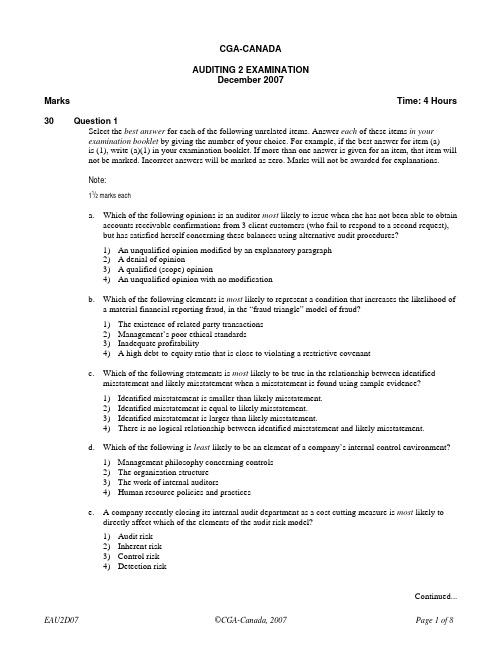

CGA-CANADAAUDITING 2 EXAMINATIONDecember 2007Marks Time: 4 Hours 130 QuestionSelect the best answer for each of the following unrelated items. Answer each of these items in yourexamination booklet by giving the number of your choice. For example, if the best answer for item (a)is (1), write (a)(1) in your examination booklet. If more than one answer is given for an item, that item willnot be marked. Incorrect answers will be marked as zero. Marks will not be awarded for explanations.Note:11/2 marks eacha. Which of the following opinions is an auditor most likely to issue when she has not been able to obtainaccounts receivable confirmations from 3 client customers (who fail to respond to a second request),but has satisfied herself concerning these balances using alternative audit procedures?1) An unqualified opinion modified by an explanatory paragraph2) A denial of opinion3) A qualified (scope) opinion4) An unqualified opinion with no modificationb. Which of the following elements is most likely to represent a condition that increases the likelihood ofa material financial reporting fraud, in the “fraud triangle” model of fraud?1) The existence of related party transactions2) Management’s poor ethical standardsprofitability3) Inadequate4) A high debt-to-equity ratio that is close to violating a restrictive covenantc. Which of the following statements is most likely to be true in the relationship between identifiedmisstatement and likely misstatement when a misstatement is found using sample evidence?1) Identified misstatement is smaller than likely misstatement.2) Identified misstatement is equal to likely misstatement.3) Identified misstatement is larger than likely misstatement.4) There is no logical relationship between identified misstatement and likely misstatement.d. Which of the following is least likely to be an element of a company’s internal control environment?1) Management philosophy concerning controlsorganizationstructure2) The3) The work of internal auditors4) Human resource policies and practicese. A company recently closing its internal audit department as a cost cutting measure is most likely todirectly affect which of the elements of the audit risk model?risk1) Auditrisk2) Inherentrisk3) Controlrisk4) Detectionf. How, if at all, should financial statements be changed when a material subsequent event that providesinformation about new conditions that did not exist at the balance sheet date occurs after the end of a company’s fiscal year?1) The subsequent event should be disclosed.2) The subsequent event should be disclosed and the related financial statement amounts should beadjusted retroactively as of the balance sheet date.3) There is no need for disclosure but the related financial statement amounts should be adjustedretroactively as of the balance sheet date.4) The subsequent event should be ignored.g. Which of the following is an example of a processing control in a computerized IT environment?signatures1) Electronic2) Automated tracking of transaction sequence numberstechnology3) Opticalscanning4) Independent verification of data conversionh. Which of the following sets of values for elements of the risk model is most likely to characterize asmall business audit?1) Low audit risk and low inherent risk2) High detection risk and high control risk3) High control risk and low detection risk4) High inherent risk and high detection riski. Which of the following actions by a junior auditor would be most appropriate when the junior auditoris spending considerably more time performing an audit procedure than is allowed for by the time budget for the engagement?1) Perform the procedure and discuss the matter with the client’s staff2) Perform the procedure and discuss the matter with the audit senior3) Perform the procedure and discuss the matter with the audit partner4) Perform the procedure but do not report the excess hoursj. Which of the following is likely to be of greatest concern when a CGA firm performs an audit of a small business client’s financial statements?1) Availability of staff2) Competence of the CGA firm3) Timing of the engagement4) Independence of the CGA firmk. A secondary auditor, upon whom the primary auditor places reliance, issues a qualified (scope) opinion on the financial statements of a material consolidated subsidiary of a Canadian consolidated entity. The qualified opinion is issued because the secondary encountered a client-imposed scope restriction when auditing the subsidiary. Which of the following opinions is most likely to be issued by the primary auditor?opinion1) Unqualified2) Denialopinionof3) Shared opinion, with each auditor taking responsibility for their portion of the audit4) Adverse opinion because the scope restriction was client imposedl. Under which of the following circumstances is non-sampling error least likely to increase?1) An audit procedure is performed by an audit junior with limited experience.2) The sample size is relatively small.3) A substantive audit procedure is performed at an interim date rather than at fiscal year end.4) An audit procedure is performed by client personnel at the auditor’s request.m. A public sector auditor is most likely to comment on the efficiency of an entity’s operations when performing which of the following services?1) A financial statement auditauditcompliance2) A3) A value-for-money audit4) An audit of internal controlsn. Canadian not-for-profit organizations are required to prepare financial statements on which of the following accounting bases?basis1) Cashbasis2) Accrualbasisaccrual3) Modifiedcostbasis4) Historicalo. Which of the following statements concerning the strategic systems-based audit approach is true?1) Since the Enron fraud, strategic systems-based audits are not in compliance with generallyaccepted auditing standards.2) Strategic systems-based audits represent a “top down” approach to auditing based on intensivestudy of the client’s business.3) Strategic systems-based audits require extensive expertise in and use of sophisticatedcomputer-assisted audit techniques.4) Strategic systems-based audits can be expected to result in large savings in time and audit costs,and hence reduced audit fees.p. Which of the following financial statement assertions are most likely to be of concern in the audit of a company that is planning an initial public offering of securities?1) Existence of assets and completeness of liabilities2) Completeness of assets and existence of liabilities3) Completeness of assets only4) Existence of liabilities onlyq. Attribute sampling techniques are most closely linked to which element of the audit risk model?risk1) Auditrisk2) Inherentrisk3) Controlrisk4) Detectionr. Which of the following forms of analysis is least likely to be used in the planning stages of an audit engagement?1) Scanning financial statements2) Statistical time series analysisanalysis3) Formalratio4) Detailed industry analysiss. A CGA performs specific but limited audit procedures that are agreed upon between the CGA and the client and then reports the factual findings from those procedures. In this case, what level of assurancewould the CGA normally provide?assurance1) No2) Limited or low-level assuranceassurance3) Moderate4) Audit or high-level assurancet. Which of the following tasks is least likely to be performed by an audit partner?1) Performing certain analytical procedures2) Assessing the quality of the client’s internal control environment3) Performing substantive tests of key balance sheet accounts4) Reviewing the working papers215 QuestionThe following are 5 independent situations involving possible violations of the CGA-Canada Code ofEthical Principles and Rules of Conduct (CEPROC) and/or standards for the performance of audits,reviews, other forms of assurance engagements, and/or related services.RequiredFor each situation, state whether or not the CGA has violated CEPROC and/or other standards. Explainyour reasoning.3 a. Joy, CGA, audits the financial statements of Natural Foods Ltd., which operates 2 large retail stores.The company is owned and managed by 2 brothers who are pioneers in the growth and developmentof the natural foods industry. In addition to the audit, Joy prepares the corporate tax return and thepersonal tax returns of the owners. She has also advised them in developing a computerized perpetualinventory and order processing system that is linked up with the IT systems of their major suppliers.The brothers have great confidence in Joy’s work and often recommend her to their businessassociates. As a result, Joy charges a very low fee of $15,000 for her annual audits of Natural Foods’financial statements.3 b. Stan, CGA, a partner in the firm of Ostrow and Jacobs, CGAs, is planning the audit of the financialstatements of his long-time client, Ledger and Quill Ltd., a wholesaler of office supplies. Because thecompany’s operations are simple and very stable, Stan skips the analysis of the unaudited financialstatements this year to save time. In addition, he instructs the audit senior to use a planning materialitylevel of $50,000, which is about 10% of the company’s unaudited net income. Finally, Stan tells thesenior not to study and evaluate the client’s internal controls, since these have not changed in manyyears, but rather to assess the risk of material misstatement for most assertions as low, unless thesenior encounters specific problems during the audit that would lead to a higher risk assessment.3 c. Chiu, CGA, is auditing the financial statements of Fantastic Jewellers Ltd. This is Chiu’s first audit ofthe company’s financial statements. To verify the client’s ending inventories of unset gemstones, Chiurelies upon a report given to him by the client, prepared by a certified gemologist employed by thecompany. The report is a detailed list of all the items on hand, including a description of each stone,the date of purchase and the cost, along with an estimate of each stone’s market value. Chiu checksthe clerical accuracy of the list and physically inspects 25 of 250 gemstones on the list using hisprofessional judgment, and traces their cost to paid invoices. He encounters no exceptions andconcludes that the inventory of gemstones is fairly stated.3 d. George, CGA, is performing a review of the financial statements of a medium-sized manufacturingcompany for which he has not previously performed any assurance services. His review proceduresconsist of a discussion with management concerning the nature and operations of the business and itsindustry, along with a ratio analysis of the financial statements prepared by the client. In that analysis,George compares the client’s key ratios of the balance sheet and income statement for the current yearto those of the previous year, where the previous year’s ratios are also derived from client-preparedfinancial statements with which no professional accountant was associated. George notes a fewsignificant differences between ratios for the 2 years. Management provides explanations for thedifferences that George considers to be reasonable. George then issues a normal review engagementreport, without modification or reservation.3 e. Sharon, CGA, is compiling financial statements for her client, a retail clothing store, based on recordsand other information prepared by the owner. Among other things, the owner provides Sharon with alist of clothing on hand at the balance sheet date along with the cost of those items. While Sharon doesnot attempt to verify the merchandise on the list, it appears to her that the number of listed items ismuch more than the store normally carries. She asks the owner about this possible discrepancy and theowner says that she needs to send the financial statements to the bank as a condition of her banks loanand “wants things to look good.” While Sharon is somewhat concerned by this comment, she preparesthe financial statements on plain white paper and gives them to the owner, along with her invoice for$1,000. She also tells the owner not to mention to the bank that she (Sharon) was involved with thefinancial statements in any manner. The owner agrees to this arrangement, and promptly paysSharon’s invoice.14 Question3The following are 7 independent statements concerning certain auditing issues.RequiredFor each statement indicate whether you agree or disagree. Explain your reasoning.2 a. The potential conflict of interest between shareholders and management, the remoteness ofinformation sources from financial statement users, and the possibility of employee fraud are allsources of information risk that would be reduced by an audit of financial statements in accordancewith generally accepted auditing standards.2 b. The smoothing of earnings through the recording by management of abnormally large or smallaccruals is allowed by generally accepted accounting principles and would not be considered amaterial misstatement by an auditor.2 c. When using the audit risk model, control risk can be set equal to 1, but should never be set equal tozero. This is true since complete assurance from controls is never possible because the design ofcontrol systems is subject to cost/benefit considerations and there are inherent limitations to everycontrol system.2 d. General internal controls in a computerized environment include controls over network operations,access security, and various types of preventative controls (such as edit checks) that are designed toprevent data entry or processing errors.2 e. When identified misstatements from a sampling-based substantive audit test exceed materiality, theauditor must issue a qualified (GAAP) or adverse opinion unless the client corrects the identifiedmisstatements, in which case the auditor can issue an unqualified opinion.2 f. The possibility of dual-dating of an auditor’s report arises under certain circumstances when there isan accidental discovery of material facts that existed at the balance sheet date, but the discovery is notmade until after an audit report has been issued.2g. In a discovery sampling plan, which is a form of attribute sampling, the risk of unwarranted reliance on internal controls is normally set at a low value, the expected error rate is set at a high value, and thetolerable error rate is set at or near zero.Liu, CGA, is examining the loans receivable of E-Z Credit Union, a local financial institution, as part of her annual audit of the organization’s financial statements. The credit union is a major lender in thecommunity, and about one-half of its outstanding loans are to local businesses, while the remainder are mostly mortgage loans and secured lines of credit issued to personal borrowers. Based on Liu’s auditexaminations in prior years as well as her assessment of inherent risk and her study and evaluation ofinternal controls this year, Liu believes that the credit union is well managed and that the risk of material misstatements with respect to the existence, completeness, and valuation of the loans receivable ismoderate to low.Based on the financial statements prepared by the controller, the credit union has total assets of$150,000,000 at the balance sheet date and revenues of $10,000,000 for the year. The loans receivable at the balance sheet date total $90,000,000 owed by 500 borrowers. The loans receivable records aremaintained using a computerized system, and Liu has obtained a copy of the loans receivable master file from the client at the balance sheet date. Liu also has a generalized audit software system available for use in the audit.To test loans receivable, Liu decides to use a 2-stage sampling plan, where she will first sort the loansreceivable file by the total dollar amount outstanding at the balance sheet date. She will then send positive confirmation requests to the 10 largest borrower accounts. The remaining 490 loans will be tested using a dollar-unit sampling (DUS) plan. Liu decides to use 1% of the client’s recorded total assets, or $1,500,000, as her materiality threshold. However, she is unsure about the appropriate values to use for the estimated error amount (EE) and acceptable risk of incorrect acceptance (ARIA). Based on her professionaljudgment, she assesses EE at 0 (since she believes that few, if any, errors are likely to be found) and ARIA at 20%. Having determined the required sample size, Liu will select a DUS sample, send positiveconfirmations to the borrowers in the sample, and then evaluate her sampling results as well as the results of her tests of the largest loan balances.Required3 a. Without regard to the details of the case, briefly explain the nature of generalized audit software(GAS) and its potential uses in an audit engagement. Also indicate a major advantage of using GAS inan audit.6 b. Evaluate Liu’s plan for auditing the credit union’s loans receivable, and explain whether the plan islikely to yield sufficient appropriate evidence with respect to the existence, completeness, andvaluation of the client’s loans receivable.3 c. Since Liu is unsure about the appropriate parameter values to use in her DUS plan, explain whatimpact (if any) each of the following changes would have on the DUS sample size:•Increasing EE from $0 to $100,000•Increasing ARIA from 20% to 25%•Increasing materiality from 1% of assets to 2% of assets3 d. Suppose Liu performs her tests as described above and finds no errors in her audit of the 490 accountsusing DUS, but receives one confirmation from her audit of the 10 largest accounts concerning a loanbalance of $1,500,000 that states: “I am unable to comply with your confirmation request, as I havefiled for personal bankruptcy. All enquires about this loan should be made through my lawyers,Lord & King.” Briefly explain what Liu should do.You are a partner in the firm of Arnold Schorn & Co., Certified General Accountants. You are responsible for conducting the final, independent review of audits completed by the firm, as part of your firm’s newly instituted quality control program. Prior to this year, the firm did not utilize the services of an independent review partner, but engagement partners were expected to consult with their colleagues on critical issues encountered in performing audits of financial statements. Arnold Schorn & Co. performs mostly accounting and tax work, but also has a few small business clients for which it performs audits of financial statements.You are currently reviewing the audit working papers and a draft of the audited financial statements of Olmen Jamar Construction Ltd. for the fiscal year ended June 30, 2007, along with the suggested auditor’s report (an unqualified opinion) prepared by the engagement partner. The company fabricates and installs metal ductwork used in ventilation and heating systems in homes and office buildings.The company is controlled by a small group of related shareholders, some of whom are active in the business. The company has been an audit client of your firm for 5 years. The audit fieldwork, which took about 4 weeks, was performed by a senior auditor assisted by two junior auditors, and the working papers were reviewed by the engagement partner. The audited financial statements show total assets at year end of $40,000,000, contract revenues of $15,000,000, and income before taxes of $2,000,000.Based on your independent review of the working papers (including various memoranda and review notes prepared by the staff and engagement partner) and the proposed financial statements and audit opinion, you have noted the following issues that arose during the audit, along with the manner in which they were resolved:1. While testing the executive payroll records of the company, one of the junior auditors noticed that thecompany’s controller, Frank Hughes, who is not a shareholder, received a salary plus bonus payments of $400,000 this year. This was more than was paid to any other executive of the company, including the chief executive officer (CEO). The junior mentioned the issue to the audit senior, who asked Frank Hughes why he was being paid so well. Frank hesitated, and then explained that part of his duties was to pay bribes — but only when absolutely necessary — to municipal building inspectors, to make sure that the inspectors accepted the company’s work and certified the completion of a job.Frank went on to say: “This one of the sad facts of life in this city and in this business. I convert some of my salary to cash and make these payments. But we report my total salary properly to Canada Revenue Agency — so there should be no problem.” The senior made a note of this explanation in the payroll working papers with a note saying “this is not an audit issue since salaries and taxes arerecorded properly.” The engagement partner wrote: “I agree” and initialled the working paper.2. The company normally recognizes all revenues on a completed contract basis. However, this year thecompany was involved in a large job installing a ventilation system in a downtown office building and the work was about 50% completed at June 30, 2007. The total contract amount is $4,000,000 and the company decided to recognize $2,000,000 of revenues on this contract in the fiscal year ended June 30, 2007. The costs incurred on the contract as of June 30, 2007 totalled $1,700,000. The engagement partner agreed with the accounting treatment and wrote a memorandum for the working papers that explained the transaction and concluded: “This is likely to be a one-time event, so financial statement disclosure is not necessary.”3. Because of the nature of the construction business, payroll expenses are a major cost. The juniorauditors studied the company’s payroll processing systems, completed an internal controlquestionnaire for payrolls, and verified the details of 30 payroll transactions during March 2007. Noexceptions were found in this test. The only weakness noted was that the company often hires “casuallabourers” to work on certain jobs and pays these labourers in cash. The supervisor on every job hascontrol over a petty cash fund (usually $5,000) designated for that purpose and is authorized bymanagement to make such payments. The supervisor submits a list of labourers and amounts paid as“casual labour” to the head office at the end of each week and receives reimbursement. When a job iscompleted, the supervisor returns any excess cash to the company and the fund is closed out on thebooks. According to the company’s records, about 5% of payroll expenses of $8,000,000 werehandled in this manner during the fiscal year. Based on studies of the client’s system, the audit staffconcluded that control risk over payroll transactions was low, except in the area of casual labour,where they assessed the risk as maximum. In addition, the senior wrote a note on the payroll workingpaper saying: “While controls over payments to casual labourers are poor, there is no effect on thefinancial statements. However, we should discuss this control weakness in our management letter.”4. The company’s assets at June 30, 2007 include a $2,000,000 loan receivable from one of thecontrolling shareholders who is facing personal financial difficulties. This loan was made in May 2007and was authorized by the company’s board of directors. The loan is due and payable in May 2008and bears interest at the prevailing prime rate. The loan is shown on the June 30, 2007 balance sheet as“loans receivable from shareholders” and is classified as a current asset, as is the accrued interest onthe loan, which was unpaid at the date of completion of the fieldwork. The financial statementscontain no other disclosure related to the loan.5. The engagement partner is a close friend and brother-in-law of the client’s CEO. They live in the samecommunity, belong to the same country club, and frequently dine together to discuss politics,business, and other issues. The CEO often consults with the engagement partner on operating mattersand ways to improve profitability of the company. Because of this close relationship, several years agothe engagement partner wrote a memorandum for the permanent files fully describing the situationand assuring his partners that the audit is always conducted with professional skepticism and to thehighest ethical and professional standards.6. When planning the audit, the engagement partner used an audit risk level of 10%. He explained thisdecision in the working papers saying: “This is a small business that has always been profitable. Weknow the management staff and they are of the highest integrity. Also, the firm is largely financedwith equity capital and has little debt. Accordingly, our business risk related to this engagement isvery low.”After thinking about these various issues, you decide to write a memo to the engagement partner, with acopy to the managing partner of the firm, expressing your views on these matters and what needs to bedone before you are prepared to “sign off” on the engagement.Required20Write the memo that you will send to the engagement partner (with a copy to the firm’s managing partner).Note:Limit your memo to about 1,000 words.6 6 marks are allocated for clarity, logic, impact, and persuasiveness.END OF EXAMINATION 100AUDITING 2 [AU2]EXAMINATIONBefore starting to write the examination, make sure that it is complete and that there are no printing defects. This examination consists of 8 pages. There are 5 questions for a total of 100 marks.READ THE QUESTIONS CAREFULLY AND ANSWER WHAT IS ASKED.To assist you in answering the examination questions, CGA-Canada includes the following glossary of terms.GlossaryFrom David Palmer, Study Guide: Developing Effective Study Methods (Vancouver: CGA-Canada, 1996). Copyright David Palmer.Compare Examine qualities or characteristics thatresemble each other. Emphasize similarities,although differences may be mentioned. Contrast Comparebyobservingdifferences. Stressthe dissimilarities of qualities orcharacteristics. (Also Distinguish between) Criticize Express your own judgment concerning thetopic or viewpoint in question. Discuss bothpros and cons.Define Clearly state the meaning of the word orterm. Relate the meaning specifically to theway it is used in the subject area underdiscussion. Perhaps also show how the itemdefined differs from items in other classes. Describe Tellthewhole story in narrative form. Diagram Give a drawing, chart, plan or graphicanswer. Usually you should label a diagram.In some cases, add a brief explanation ordescription.Discuss This calls for the most complete and detailed answer. Examine and analyze carefully andpresent both pros and cons. To discussbriefly requires you to state in a fewsentences the critical factors.Evaluate This requires making an informed judgment.Your judgment must be shown to be basedon knowledge and information about thesubject. (Just stating your own ideas is notsufficient.) Cite authorities. Cite advantagesand limitations.Explain In explanatory answers you must clarify the cause(s), or reasons(s). State the “how” and“why” of the subject. Give reasons fordifferences of opinions or of results. Illustrate Make clear by giving an example, e.g., afigure, diagram or concrete example. Indicate Provide a short explanation.Interpret Translate, give examples of, solve, orcomment on a subject, usually making ajudgment on it.Justify Prove or give reasons for decisions orconclusions.List Present an itemized series or tabulation.Be concise. Point form is oftenacceptable. (Also Enumerate or Identify) Outline This is an organized description. Give ageneral overview, stating main andsupporting ideas. Use headings andsub-headings, usually in point form. Omitminor details.Prove Establish that something is true by citingevidence or giving clear logical reasons. Relate Show how things are connected with eachother or how one causes another,correlates with another, or is like another. Review Examine a subject critically, analyzingand commenting on the importantstatements to be made about it.State Present the main points in brief, clearsequence, usually omitting details,illustrations, or examples.Summarize Give the main points or facts in condensedform, like the summary of a chapter,omitting details and illustrations.Trace In narrative form, describe progress,development, or historical events fromsome point of origin.。

2013年ACCA新大纲各科目全解析-P4

新旧考纲的主要变化:

� 增加的新内容 G3 Developments in Islamic finance Demonstrate an understanding of the role of, and 了解 Islamic financing 在公司发展融资 developments in, Islamic financing as a growing source 来源时的角色和其重要性。解释它的使用 of finance for organisations; explaining the rationale for 的原理和定义它的优缺点。 its use, and identifying its benefits and deficiencies � 删去的内容

考官介绍:

高顿 ACCA 研究中心:中国 上海 虹口区中山北一路 369 号 课程咨询:上海虹口 021-6199 9158 上海徐汇 021-6167 9188 远程课程:021-6052 0476

中国领先 ACCA 培训中心,官方认可黄金级机构 http://Acca.

因为 P4 的考官 Shishir Malde 是 2010 年 6 月新上任,目前任职于英国诺丁汉特伦特大学。主要研究 领域为:财务管理, 战略投资, 融资管理等。

中国领先 ACCA 培训中心,官方认可黄金级机构 http://Acca.

2013 年 ACCA 新大纲考试科目全介绍 Advanced Financial Management (P4)

相关资源下载:

P4 2013 syllabus and study guide P4 Pilot Paper Questions and Answers P4 Sample question relevant for exams from December 2010 P4 2010 Jun Exam Question P4 2010 Jun Exam Answer P4 2010 Dec Exam Question P4 2010 Dec Exam Answer P4 2011 Jun Exam Question P4 2011 Jun Exam Answer P4 2011 Dec Exam Question P4 2011 Dec Exam Answer

CGA教学计划65分及格

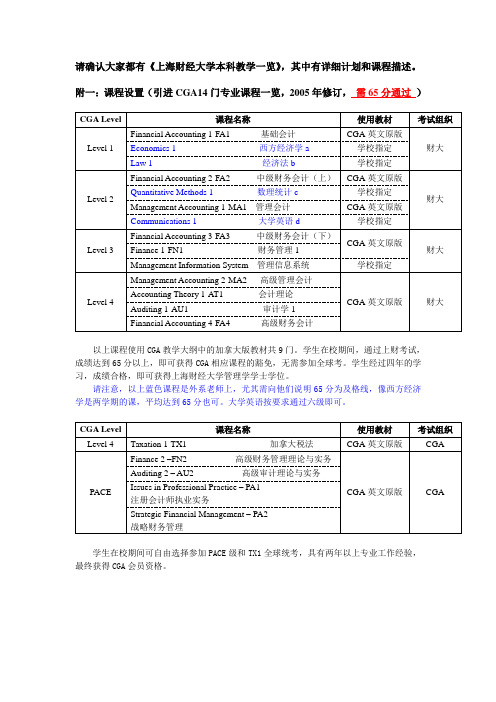

请确认大家都有《上海财经大学本科教学一览》,其中有详细计划和课程描述。

附一:课程设置(引进CGA14门专业课程一览,2005年修订,需65分通过)

Financial Accounting 1-FA1

Financial Accounting 2-FA2

Quantitative Methods 1

Management Accounting 1-MA1

Financial Accounting 3-FA3

Management Accounting 2-MA2

Accounting Theory 1-AT1

Auditing 1-AU1

以上课程使用CGA教学大纲中的加拿大版教材共9门。

学生在校期间,通过上财考试,成绩达到65分以上,即可获得CGA相应课程的豁免,无需参加全球考。

学生经过四年的学习,成绩合格,即可获得上海财经大学管理学学士学位。

请注意,以上蓝色课程是外系老师上,尤其需向他们说明65分为及格线,像西方经济学是两学期的课,平均达到65分也可。

大学英语按要求通过六级即可。

Finance 2

Auditing 2

注册会计师执业实务

学生在校期间可自由选择参加PACE级和TX1全球统考,具有两年以上专业工作经验,最终获得CGA会员资格。

教学管理信息系统操作手册(学生用户)

上海金仕达多媒体有限公司上海财经大学教学管理信息系统操作手册2013/6/19上海财经大学教学管理信息系统操作手册,此文档适用于:学生用户目录1如何查看我的个人信息? (2)2如何查询培养计划? (2)3如何检查我的个人培养计划完成进度? (3)4选课操作说明 (3)5如何查看课程安排信息? (6)6如何查看成绩? (6)7评教相关问题说明 (7)8考试报名 (8)9论文 (11)10毕业与学位 (23)1如何查看我的个人信息?功能入口:学籍信息>> 个人信息功能说明:系统内可查询个人相关信息,如班级、注册、学籍、奖惩等。

通过点击切换以上页签查询不同类型的个人信息。

功能入口:学籍信息>> 班级信息2如何查询培养计划?功能入口:培养计划>> 我的计划功能说明:查询我的培养计划如果有多个专业计划,右上角还可以选择对应的专业计划;3如何检查我的个人培养计划完成进度?功能入口:培养计划>> 完成进度功能说明:培养计划完成进度,显示个人学业完成情况与培养计划比较的结果。

说明:对于红色字部分,请同学在选课时特别注意,避免学分不够情况。

功能入口:课程>> 选课功能说明:页面下部为课程列表,在此区域分为“可选课程”和“已选课程”两个页签;对于“可选课程”页签,点击操作列的【选课】按钮选取当前的课程;对于“已选课程”页签,点击操作列的【退课】按钮删除已选择的课程(如下图)选课功能界面(已选课表):选课时间表,以课表形式展示出已经选课的课程,当鼠标单击名称,显示该门课程的详细信息,在选课开放期间,可以通过该列表中“退课”按钮实现退课操作(如下图)选课时间表,当鼠标单击选课时间表空白处,如果该时段已有课程安排,则显示该时间的课程详细信息,可以通过该列表中“选课”按钮实现课程选择(如下图)对于已开放重修的选课轮次,系统将在选课界面下部显示“已修课程”页签,如有未及格课程成绩,可在此处进行重修选课(如下图)说明:当选课轮次开放重修,下图中会多出“已修课程”页签;对于重修课,在可选课程里面会出现该课程,操作列会显示“重修”字样:同样的在课表上点击空白处点击后,可选的课程也会出现“重修”字样:5如何查看课程安排信息?功能入口:课程>> 我的课表功能说明:显示选课结果情况;请同学注意星期下方包含绝对日期和节次下方的具体时间;课程详细信息(如下图):6如何查看成绩?功能入口:课程>> 我的成绩功能说明:查看自己的成绩课程成绩有不同的状态,课程成绩状态为“已发布”方可显示出来;点击右上方【所有学期成绩】查询本人所有学期的成绩情况;课程成绩状态说明:成绩状态含义说明未提交表示教师尚未录入成绩;课程成绩无法查看;未发布表示教师已完成成绩录入,教务处尚未发布成绩;课程成绩无法查看;已发布表示教师已民完成成绩录入,教务处已完成成绩发布;课程成绩可以查看;7评教相关问题说明功能入口:评教>> 评估课程功能说明:评教包含两种形式:一、问卷评教;二、文字评教;其中“问卷评教”有开始截止日期限制、“文字评教”可持续提交;点击【进行评教】对当学期课程逐门进行评教;点击【文字评教】对当学期课程进行文字评教,此处是否评教不与选课关联,也没有开放时间限制;8考试报名1)本科生二专业报名功能入口:考试报名>> 双专业报名功能说明:本功能仅针对本科生;第二专业报名有开放时间限制;当学校开放第二专业报名并在系统设定过以后,方可进入第二专业报名功能;可报名专业:报名信息:点击【提交】完成报名:提交后,页面显示如下图:如果取消报名可以点击【取消报名】;如果被录取,报名信息栏会出现,红框内的录取信息。

成本与管理会计基础(ACCAF2)智慧树知到答案2024年上海财经大学浙江学院

成本与管理会计基础(ACCAF2)上海财经大学浙江学院智慧树知到答案2024年绪论单元测试1.本课程目标是通过学习,掌握成本与管理会计的相关知识,同时能应用相关知识和技能,解决企业运营过程中出现的一些问题,为企业计划、管理、控制活动提供所需要的信息。

A:对 B:错答案:A2.本课程在ACCA的课程体系中属于基础阶段。

A:错 B:对答案:B3.只有企业需要管理会计,非盈利性机构只需要财务会计。

A:错 B:对答案:A4.成本会计就是管理会计,两者没有区别。

A:错 B:对答案:A5.管理会计是会计的重要分支,从它的功能来说,主要是会计记录和核算。

A:对 B:错答案:B第一章测试1.Which of the following statements is false? ()A:The format of management accounts is entirely at management discretion.B:Management accounts detail the performance of an organisation over adefined period and the state of affairs at the end of that period.C:Limited liability companies must prepare financial accounts.D:There is no legal requirement to prepare management accounts.答案:B2.Diane carries out routine processing of invoices in the purchasingdepartment of L Co. Joanne is Diane's supervisor. Lesley is trying to decidehow many staff will be needed if some proposed new technology isimplemented. Tracey is considering the new work that L Co will be able tooffer and the new markets it could enter, once the new technology is wellestablished. Which member of L Co carries out tactical activities? ( )A:JoanneB:LesleyC:TraceyD:Diane答案:B3.Which of the following statements is false? ( )A:Financial accounting information can be used for internal reportingpurposes.B:Cost accounting can only be used to provide inventory valuations forinternal reporting.C:Management accounting provides information relevant to decision making, planning, control and evaluation of performances.D:Routine information can be used to make decisions regarding both the long term and the short term.答案:B4.Which of the following is not part of the planning stage in the decision-making process? ( )A:Obtaining data about actual resultsB:Identifying goals or objectivesC:Identifying ways which might contribute to the achievement of specifiedobjectivesD:Deciding on the optimal way in which an objective might be achieved答案:A5.Which of the following is an example of discrete data from a primary source?( )A:A website showing the average height for children aged sevenB:An eyewitness account of the number of customersC:A report in a newspaper giving retail sales for the monthD:A colleague's measurement of the distance from the office to the headoffice答案:B第二章测试1. A company which makes rechargeable batteries selects some of the batteriesfor examination. The procedure used chooses two random numbers, say nand m. Starting at the nth battery, every battery at an interval of m is thenchosen for examination. This type of sampling is known as: ( )A:StratifiedB:SystematicC:MultistageD:Random答案:B2. A company's weekly costs ($C) were plotted against production level (P) forthe last 50 weeks and a regression line calculated to be C = 1,000 + 250P.Which statement about the breakdown of weekly costs is true? ( )A:Fixed costs are $250. Variable costs per unit are $1,000.B:Fixed costs are $250. Variable costs per unit are $4.C:Fixed costs are $1,000. Variable costs per unit are $5.D:Fixed costs are $1,000. Variable costs per unit are $250答案:D3.The value of the correlation coefficient between x and y is 0.9. Which of thefollowing is correct? ( )A:x is 90% of y.B:There is a very strong relationship between x and y.C:If the values of x and y were plotted on a graph, the line relating themwould have a slope of 0.9.D:There is a weak relationship between x and y.答案:B4.The correlation coefficient between A and B is 0.4 and the correlationcoefficient between C and D is –0.7. Which of the following statements is correct? ( )A:There is a stronger relationship between A and B than between C and D.B:There is a stronger relationship between C and D than between A and B.C:The relationship between A and B and between C and D is the same.D:There is insufficient information to determine which relationship isstronger.答案:B5.Which of the following statements about stratification is/are true? ( )I The sample selected will be representative of the population.II The structure of the sample will reflect that of the population if the same proportion of individuals is chosen from each stratum.III It requires prior knowledge of each item in the population.A:I and III onlyB:II and III onlyC:I, II and IIID:III only答案:C第三章测试1.The costs of materials for product B are made up as follows.Material P: $1,000Material Q: $600Material R: $1,025Material S: $375If the material proportions were displayed on a pie chart, how many degrees would material Q represent? ( )A:72 degreesB:120 degreesC:144 degreesD:204 degrees答案:A2.You have just calculated for the last two six-monthly periods, the runningcosts of a factory, broken down into five categories. You are using a computer package which can produce radar charts, pie charts, time series graphs andscatter diagrams, among others. The graphics to best illustrate the relativesizes of the cost categories in this situation will be: ( )A:Line graphsB:Scatter diagramsC:Radar chartsD:Pie charts答案:D3.The following data relates to an item of raw material.Unit cost of raw material $20Usage per week 250 unitsCost of ordering material, per order $400Annual cost of holding inventory, as a % of cost 10%Number of weeks in a year 48What is the economic order quantity, to the nearest unit? ( )A:1,549 unitsB:2,191 unitsC:316 unitsD:693 units答案:B4.If the first in, first out method of pricing had been used, the value of the issueon 9 September would have been: ( )A:$350B:$420C:$355D:$395答案:C5.FIFO prices materials issues at the prices of the newest items in inventory,and values closing inventory at the value of the most oldest items ininventory.A:对 B:错答案:B第四章测试1. A manufacturing company always carries finished goods inventory equal to20% of the next month's budgeted sales. Sales for the current month are2,000 units and are budgeted to be 20% higher next month. How many units will be produced in the current month? ( )A:1,920 (400 + 2,000 – 480)B:2,400 (2,000 + 400)C:2,000 (no adjustment)D:2,080答案:D2.What does the statement 'sales is the principal budget factor' mean? ( )A:The level of sales will determine the level of profit at the end of the period.B:Sales is the largest item in the budget.C:The company's activities are limited by the level of sales it can achieve.D:The level of sales will determine the level of cash at the end of the period.答案:C3.Which of the following is unlikely to be contained with a budget manual? ( )A:Selling overhead budgetB:Objectives of the budgetary processC:Organisational structuresD:Administrative details of budget preparation答案:A4.Which of the following is not a functional budget? ( )A:Cash budgetB:Selling cost budgetC:Distribution cost budgetD:Production budget答案:A5.Which of the following may be considered to be objectives of budgeting? ( )(i) Co-ordination(ii) Communication(iii) Expansion(iv) Resource allocationA:(i), (ii) and (iv) onlyB:All of themC:(i) and (iii) onlyD:(ii) and (iii) only答案:A第五章测试1.JC Co operates a bottling plant. The liquid content of a filled bottle of productT is 2 litres. During the filling process there is a 30% loss of liquid input dueto spillage and evaporation. The standard price of the liquid is $1.20 per litre.The standard cost of the liquid per bottle of product T, to the nearest cent, is: ( )A:$2.86B:$3.12C:$2.40D:$3.43答案:D2.What is an attainable standard? ( )A:A standard which includes some allowance for losses, waste andinefficiencies. It represents the level of performance which is attainableunder efficient operatingconditions.B:A standard which is kept unchanged, to show the trend in costs.C:A standard which includes no allowance for losses, waste and inefficiencies.It represents the level of performance which is attainable under perfectoperating conditions.D:A standard which is based on currently attainable operating conditions.答案:A3.The B Co uses a standard absorption costing system and produces oneproduct, the Blob. The following information is available for September.Standard cost per Blob $31Budgeted sales (units) 7,100Actual sales (units) 6,600Sales price variance $1,250 (A)Sales volume variance $4,500 (A)Calculate the sales revenue for September . ( )A:$262,750B:$256,750C:$265,250D:$252,250答案:A4.Extracts from H Co’s records for June are as follows.What is the total direct labour cost variance?A:$1,536 (A)B:$1,920 (A)C:$1,536 (F)D:$1,920 (F)答案:B5. A standard marginal costing system:(i) Calculates fixed overhead variances using the budgeted absorption rateper unit(ii) Calculates sales volume variances using the standard contribution per unit(iii) Values finished goods stock at the standard variable cost of production Which of the above statements is/are correct?( )A:(i) and (ii) onlyB:(i), (ii) and (iii)C:(i) and (iii) only D:(ii) and (iii) only答案:D第六章测试1.The following information relates to P Limited at 31 December 20X0.$Inventories 1,550Short-term payables 2,100Receivables 1,300Cash at bank 1,250Which of the following is the quick ratio for P Limited to two decimal places?( )A:0.74B:1.95C:1.21D:0.62答案:C2.Which of the following is a non-financial performance measure? ( )A:Share priceB:Delivery timeC:Cash flowD:Revenue答案:B3.The following information relates to P Limited at 31 December 20X4.$Revenue 3,000Gross profit 990Net profit 450Non-current assets 1,920Calculate the net profit percentage. ( )A:66%B:33%C:85%D:15%答案:D4.The following information relates to P Limited at 31 December 20X7.$Revenue 3,000Gross profit 990Net profit 450Inventory 125Trade receivables 260Cash 1,920Calculate the accounts receivable payment period. (All sales are oncredit.) ( )A:49 daysB:211 daysC:32 daysD:95 days答案:C5.Which of the following is a feature of the residual income performancemeasure? ( )A:It measures divisional performance based on multiple values.B:It generally decreases as assets get older.C:It helps you to select a proposal that will maximise wealth in absolute terms.D:It is a relative measure.答案:C。

上海财经大学本科生2014-2015学年第一学期选课手册

李毅 李毅 李毅 李毅 李毅 曾晓洋 吴芳 曾晓洋 江晓东 吴纯杰 徐珂 苏均和 马俊玲 黄涛 高瑜 董敏凯 陈瑜 刘建业 陈敬 王苑苑 陈惠芳 成月祥 文红为 顾雪兰 张燕 吕季东 顾德平 郑玲 蔡颖敏 高瑜 戴勇 安舒扬 陈瑜

管理学 管理学 管理学 管理学 管理学 国际法学 国际法学 国际结算 国际贸易 国际贸易 国际贸易 国际贸易 国际贸易专题讲座 国际企业经营管理模拟 国际企业经营管理模拟 国际投资学 国际投资学 国际投资学 合同法学 合同法学 合同法学 宏观经济学 宏观经济学 宏观经济学 宏观经济学 宏观经济学 会计学II 会计学II 会计学II 会计学II 货币银行学 货币银行学 货币银行学 货币银行学 绩效管理 计算机编程 计算机编程 计算机编程 计算机编程 计算机编程 计算机编程 计算机编程 计算机编程 计算机编程 计算机应用 计算机应用 计算机应用 计算机应用 计算机应用 计算机应用 金融法学 金融法学 经济法概论 经济法概论 经济法概论 经济法概论

100491 100491 101271 101271 101271 101725 101725 108687 100831 100831 100831 100831 100464 101121 101121 104465 104465 104465 100482 100482 100482 100096 100096 100096 100096 100096 102882 102882 102882 102882 102502 102502 102502 102502 100477 101564 101564 101564 101564 101564 101564 101564 101564 101564 103710 103710 103710 103710 103710 103710 100181 100181 100481 100481 100481 100481

上海财经大学管理信息系统课程-试卷样张

上海财经大学管理信息系统课程-试卷样张上海财经大学管理信息系统课程-试卷样张管理信息系统试卷样张一、True or False (20Points,1 Point Each)1.CRM system can help businesses to devise more effective marketing campaignsbased on more precise knowledge of customer needs and wants.( )2.When the cash register in a supermarket prints a receipt, the printer they are using isa input device. ( )3.Minicomputers are smaller than desktop computers.. ( )4.When companies use IT system to support the Top-line activities, the IT system canhelp decrease costs. ( )5.CIS provides PERIODIC report, MIS provides SUMMARIZED reports. ( )6.If a salesperson attempts to order merchandise for a customer not in the customerdatabase, the database will typically generate an error message. This messageindicates that an integrity constraint has been violated. ( )7.According to the decision theory of Simon, the decision making process includesthree phases: design, choice and implementation. ( )8.Expert systems are excellent for diagnostic and prescriptive problems. ( )9.Online transaction processing (OLTP) involves gathering input information,processing that information, and updating existing information to reflect thegathered and processed information. ( )/doc/1c13769353.html, is a directory search engine. ( )11.If the sales reps in a company are responsible for developing a new salesinformation system, they are using the OUTSOURING development method. ( ) 12.B2B Ecommerce often uses financial cybermediary such as PayPal to pay theirsuppliers. ( )/doc/1c13769353.html,panies should not let the end users develop infrastructure-related IT system.( )14.For a knowledge worker, the smallest logical unit of information in a database iscalled a file. ( )15.Operational management levels require more regular internal reports that emphasizedetailed data. ( )16.The B2B e-commerce revenue is relatively small compared to the B2C e-commercesegment. ( )17.A Web server provides information and services to Web surfers. ( )/doc/1c13769353.html,rmation can be described as facts or observations about physical phenomena or business transactions. ( )19.Direct material purchases usually occur in horizontal e-marketplace. ( )20.Because our university provides Internet access service for students, our universityis an Internet service provider. ( )二、Single Choice (10Points, 1 Point Each)1. What is a tool you use to send information to and receive it from another person orlocation?A) Input device B) Output deviceC) Storage device D) Telecommunications device2. The form of conversion process in which both the old and the new system areoperated until there is agreement to switch completely to the new system is called_______A)pilot conversion. B) plunge or direct conversionC) parallel conversion. D) phased conversion.3. Wireless mouse is a ________.A) Input device B) Output deviceC) Storage device D) Telecommunications device4. Which of the following tools is used to help an organization build and use businessintelligence?A) Data warehouse B) Data mining toolsC) Database management systems D) All of the above5. Which type of software provides additional functionality to an operating system?A)System B) ApplicationB)Operating system D) Utility6. The direct computer-to-computer transfer of transaction information contained instandard business documents, such as invoices and purchase orders, in a standardformat is ________.A)Electronic transaction interchange. B) Electronic information interchange.C) Electronic data interchange. D) Electronic funds transfer.7. A company like Wal-Mart that has both stores and a web site for purchasing and isreferred to as?A) Click-and-order B) Click-and-mortarC) Brick-and-order D) Brick-and-click8. What does Porter's five forces model determine? _______A) The relative attractiveness of an industryB) The competitive advantage of a competitorC) The distribution chain of a competitorD) The relative attractiveness of another business9. The power companies use artificial intelligence software to find electricity usagepatterns so that they can analyze rate structures and forecast demand. So which type of artificial intelligence software do they use? ______A) Expert systems B) Neural NetworksC) Genetic Algorithms D) Intelligent Agents10. Land’s End Co. lets its order-entry employees enter the customers’ orders into the mainframe database from home. According to our textbook, this is__________.A) ordering products and services by EDI B) moving money through EFTC) telecommuting D) reaching the exact customers三、Multiple Choice (30 points,2 Points Each)1.The BPR (Business Processing Reengineering) are ______A)Radical redesign of business processesB)Fundamental rethinking of business processesC)Achieve dramatic improvementD)Eliminating jobsE)Continuous and incremental improvement2.The sales information gathered in a retail store pass up to the headquarter can beclassified as ______A)Upward flow of informationB)Downward flow of informationC)Horizontally flow of informationD)Internal informationE)external informationF)Objective informationG)Subjective information3.Data mining tools include the following tools, ______A)query and reporting toolsB)intelligent agentsC)multidimensional analysis toolsD)database management systemE)statistical tools4. When ______, the substitute power is high in the industry.A) there are many price competitive substitute products existing in the marketB) there are many suppliers existing in the marketC) the switching cost in low in the marketD) there many competitors who provide the same products5. The core ERP functions found in the successful ERP systems include .A) Accounting management & Financial managementB) Manufacturing management & Production managementC) Transportation managementD) Sales and Distribution managementE) Human resources managementF) Integrated collaboration environments management6. According to our textbook, Microsoft Office software is .A) convenience productB) specialty productC) commoditylike productD) digital product7.Which of the storage media use optical technology to store information?______A) Hard diskB) Floppy diskC) CDD) DVDE) Flash memory DevicesF) Flash memory cards8. The strategic and competitive opportunities with SCM include______.A) ensuring the right quantity of parts for production or products for sale arrive atthe right time.B) ensuring production lines function smoothly because high quality parts areavailable when neededC) Keeping the cost of transporting materials as low as possible consistent withsafe and reliable deliveryD) providing superior after-sale service and support9. Distinction between MISs and DSSs are ______ .A) DSS perfor m “what -if” analysesB) DSS use different modeling tools to analyze informationC) MIS perform OLTP analysisD) DSS perform OLTP analysisE) MIS perform OLAP analysisF) DSS perform OLAP analysis ……………………………………………………………装订线…………………………………………………10.When do scope creep and feature creep most likely occur ?A). Unclear or missing requirementsB). Failure to manage project scopeC). Changing technologyD). developers add extra features that were not part of the initial requirements11.The decision whether to expand your business into west of China is ______.A).Structured decisionB).Nonstructured decisionC).Recurring decisionD).Nonrecurring decision12.Which are techniques B2C e-commerce companies use to attract customers?A).Registering with search enginesB).Viral marketingC).Online adsD).Virtual marketing13.Which of the following describes an RFP?A) A formal documentB) Describes detailed logical system requirementsC) Describes detailed time and cost constrainsD) Invites outsourcing organizations to submit bids for system development14.Which statement about database management system tools is true ________.A)data definition subsystem of a DBMS helps you create and maintain the datadictionary and define the structure of the files in a databaseB)DBMS engine allows you to see, change, sort and query the content of adatabase.C)Data manipulation subsystem helps you add, change and delete information in adatabase and query it for valuable informationD)Application generation subsystem contains facilities to help you developtransaction intensive applications.15.Which type of outsourcing can save cost for businesses?A) purchasing software packagesB)onshore outsourcingC)nearshore outsourcingD)offshore outsourcing四、Term Explanation (8Points, 2 Points Each)1.Data Warehouse 2. SCM3. DSS4. The Long Tail五、Short Answers (12 Points)1.Can you explain how Value Chain method helps businesses find their IT strategies?2.What are the seven phases in SDLC method, and what are the main activities ineach phase?六、Case (20Points, 10 Points Each)1 At allied Engineering, Inc., a consultant was asked to design an office automation system that would improve the productivity of managers and secretarial staff. After a week of interviewing managers throughout recognized, Specialists would operate PC-based word processing and database applications, while the other secretaries in the firm would be responsible for handling administrative tasks, such as making travel arrangements, handling the phone, and arranging meetings.At first, the management of the firm felt that the recommendations would work well. The equipment supporting office automation was brought in. The consultant argued that the work processing and database software were so easy that no training was necessary.After about a month, the consultant returned to find that the system was hardly being used. The secretaries were performing the tasks they were accustomed to doing. The equipment was idle. Changes in procedures and work allocation had not been put into place. The overall productivity of the office had not been impacted by the new office automation system.Please answer the following questions:(1)Why did this situation occur?(2) What should the consultant have done differently in order to bring about change in the office?2. Answer the questions after reading the following materialUnifying Communications in AlaskaGeneral Communications Inc. of Anchorage, Alaska, used toprovide half of all the long-distance calls in Alaska. In 1996, the company sensed a future in which all communications services could be provided by a single company. Most customers would choose to have single carrier provide all their communications services.General planed for combining services for telephone, cable television, mobile communications, and satellite communications together, providing customers with all in one communication package. The task of redesigning General’s billing service so that each type of communications service would appear on one comprehensive bill was the most important thing for them. Combining this information would be complicated because all of General’s billing information was already contained in a 20-year-old。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

The Conceptual Issues

1

Key Points of Module 1

Information risk (信息风险) Expectation gap (期望差距) Independence (独立性) Audit risk model (审计风险模型) Audit evidence (审计证据)

7

Complexity and quantity of data

• 绿大地(002200): 公司的主营业务为绿化苗木种植及销售,绿 化工程设计及施工。具体的经营范围为:植 物种苗工厂化生产、观赏植物盆景、植物科 研、培训、示范推广、技术咨询服务、绿化 园艺工程设计及施工、园林机械、工艺美术 品、花木制品、塑料制品、陶瓷制品的生产 及本公司产品的销售. • How to measure the value of biological assets?

ANSWER: 3

10

Theoretical Foundation of Auditing

Shareholders (股东)

Board of Directors (董事会)

Audit Committee

Auditor

CEO

Financial Statements

CFO

COO

CTO

CMO

11

AU2: True or False

ቤተ መጻሕፍቲ ባይዱ14

Expectation Gap (期望差距)

• The standards gap represents the difference between the public expectation of audits and what is currently required of auditors by professional standards. • The performance gap represents the difference between what the present prefessional standards require and the public perception of actual auditor performance.

Answer: T

12

AU2

• The demand for auditing primarily arises because of information asymmetry between which of the following parties? • 1) Shareholders and creditors • 2) Managers and employees • 3) Shareholders and employees • 4) Managers and shareholders

6

Biases and motives of the provider

绿大地(002200): IPO in 2007: 2007年上市, 募集资金3.29亿 元. – To raise more money. Largest Shareholder: 何学葵个人持有公司 股份43,357,985股,所占比例为28.63%,为 第一大股东. 折合市值为11.7亿(2009年12 月31日). – To maximize personal wealth

9

AU2

• Which of the following is the best example of information risk? • 1) Risk that a company will go bankrupt after an unqualified opinion is issued • 2) Risk that a company’s share price will fall after audited earnings are announced • 3) Risk that a company’s financial statements are materially misstated after an unqualified opinion is issued • 4) Risk that a company’s employees will steal a material amount of inventory from the employer during the fiscal year

8

Theoretical Foundation of Auditing

Incentives to manipulate accounting numbers: • To meet benchmark (e.g., budget) • For personal compensation • To raise money from bank or stock market • To pay less tax • When CEO changes

Answer: 4

18

The Audit Institutional Environment

• From Jan, 1978 to 2010, there are around 800 firms engaging in accounting frauds or financial misrepresentations on US stock market, such as: • Enron • Worldcom • Dell • Etc. – Investors lost confidence in auditors and their work. – Collapse of Arthur Anderson

3

Theoretical Foundation of Auditing

• Information risk (信息风险): the risk that the financial statements are false or misleading. – Remoteness of information – Complexity and quantity of data – Inadvertent error or employee fraud – User reliance – Motivation, bias and conflicts of interest

5

Biases and motives of the provider

• 绿大地(002200): Chairman and CEO (绿大地董事长兼总经理 何学葵女士): 曾获“中国科协西部开发 突出贡献奖”、“云南省有突出贡献优秀 专业技术人才”、“昆明市劳动模范”、 “昆明十大杰出青年”称号。

Expectation Reasonable

15

Expectation Gap

• An audit is designed to provide reasonable assurance that the financial statements as a whole are free from material misstatements. • Auditor should exercise professional skepticism (应有的关注或者职业谨慎) and being alert to evidence that calls into question the reliability of management representations. • The primary responsibility for preventing and detecting fraud and errors rests with management and those charged with governance of the entity.

Answer: 4

13

Expectation Gap (期望差距) • Expectation gap: the difference between users’ expectation of what accountants or auditors should do and what users perception of the services actually provided by accountants or auditors. • Auditor’s opinion: reasonable assurance (合理保证), not guarantee.

Public Expectation Standards Gap Expectation Unreasonable Present Standards Performance Gap Actual Shortfall Shortfall Perceived but Not Real Public Perception

2

Theoretical Foundation of Auditing

Shareholders

Information Asymmetry

Auditing Financial Statements

Corporation

Managers

Separation of ownership and management: Agency problem

• The potential conflict of interest between shareholders and management, the remoteness of information sources from financial statement users, and the possibility of employee fraud are all sources of information risk that would be reduced by an audit of financial statements in accordance with generally accepted auditing standards.