西方财务会计

西方财务会计理论问题探索( 三)

西方财务会计理论问题探索(三)第一,企业公司)报告不是企业盈利信息的惟一来源,企业经理通过会计选择来加工盈利信息不可能取得经济利润;第二,如果盈利信息是己经实现的现金流量的替代量,那么,根据CAPM,未预计到的盈利就可能与未预期的现金流量(UnexpectedCashFlow)异常的与报酬氧AbnormalRateofReturn)相关。

BallandBromwn1968年开始对未预期盈利的变化和异常报酬率的关系进行经验检验和实证会计研究。

其根据是从上述第二个假定和CAPM推演出来的。

他们利用了科学的方法收集并检验了两个重要的变量:异常报酬率和未预期的盈利。

两人根据严格的标准挑选了261家中纽约证券交易所上市的公司所公布的盈利作为‘样本”(Sample),并把盈利和股票价格的关系的分析限定在1957~1965等9个会计年度(不考虑1957年以前己作为盈利变化的回归中预计参数)。

将上述变量包括每股盈利)通过图表进行分析,得出如下结论:1)85%~90%股票价格的变化之间和未预期的盈利是相联系的,但发生在年度收益表公布之前,于是可以假设,盈利(季度报告或来自其他方面)确实能够向会计信息使用者传递信息,但是年度财务报表提供的信息不够及时。

(2)盈利的变化同异常的报酬率的变化是相关的,盈利仍然是影响股票价格的有用信息。

初步研究成果实证研究方法在下列意义上,是一种科学的理论。

因为它能对会计中的若干现实事实作出有根据的解释和合理的预测,实证会计理论主要提出并初步检验了下列几项假设(假想):1、会计信息(主要指盈利信息)与股票价格的关系假设。

这一假设认为,财务报告上的收益(盈利)信息,不是股票价格受到影响的惟一因素,由于该信息己在证券市场的价格变动中得到反映,管理当局不可能通过会计程序的选择左右盈利,去干扰股票价格。

但是,盈利信息并不是对股票价格毫无影响。

如果盈利信息包含了市场未预测到的未预期盈利这一新的信息就会影响股价的变动(Ball&Brown:会计收益数据的经验评估(《(JournalofAccountingResearcKAutumn1968》,P159-178)d该假设建立在有效市场假设(EMH)和资本资产计量模式(CAPM)的基础上,并假定资本市场为次强式市场。

浅析中西方财务会计的差异

浅析中西方财务会计的差异一、浅析中西方财务会计的差异——简述二、会计制度的差异——西方强调市场价值,中方强调历史成本三、会计标准的差异——国际会计准则与中国会计准则的对比四、财务报表呈现的差异——西方更加注重信息透明度五、会计职业道德差异——西方强调独立性,中方强调忠诚敬业中西方财务会计的差异:财务会计是一个重要的财务管理领域,适用于从事财务工作的各行各业各企业的管理人员。

而财务会计的原则、标准、方法、技巧都不是固定不变的,更不是一国之内可以完全一致的。

本文主要从以下五个方面进行分析。

一、会计制度的差异会计制度是国家对财务报告制度的底线要求标准,也是各国财务会计的基础规则。

西方国家的会计制度更加重视市场价值,而中国则更加注重历史成本。

在西方国家,由于市场的高度发达和信息透明度的提高,公司股权、负债、资产等的市场价值日益凸显。

因此,西方国家的财务会计更注重准确反映公司的市场价值和风险,能够反映资金变化的现值效应。

而中国的财务会计更注重历史成本,因为中国的市场主体相对较少,整个市场环境较为稳定,企业的资产和权益之间没有过大的波动,因此历史成本更能够真实反映资产变化情况。

两种制度的差异主要表现在公司的财务报表中,当经济越发达的时候,市场价值会更加凸显,财务会计制度也会越来越注重市场价值。

二、会计标准的差异会计标准即口径、计量、披露等方面的规范,也是财务会计的基础标准,各国的会计标准存在不同。

国际会计准则(this refers to International Financial Reporting Standards(IFRS))与中国会计准则的差异体现在以下方面:股权投资、债务重组、信用损失、按成本或公允价值进行计量等,而且中国会计准则在主席,审计、计算调整方面也有不同的规定。

国际会计准则需要披露的信息要比中国的会计准则更加详细和全面,国际会计准则主要以披露市场价格的口径作为核算标准,更注重市场欺诈行为的预防,增加信息透明度,而中国会计准则更加注重各个交易环节数据的记录。

西方财务会计第六章答案

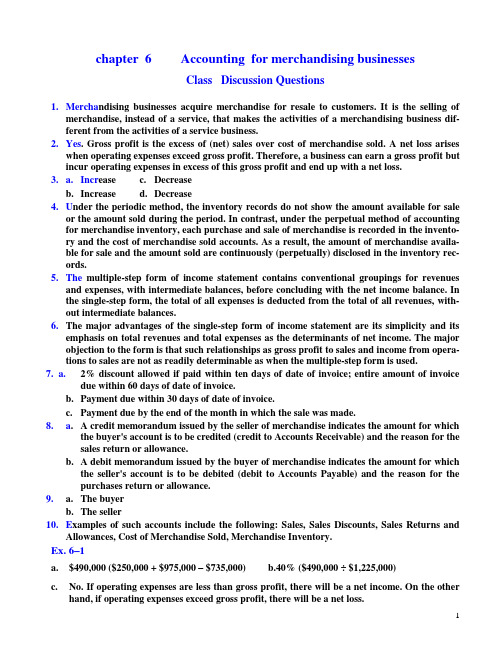

chapter 6 Accounting for merchandising businessesClass Discussion Questions1. Mercha ndising businesses acquire merchandise for resale to customers. It is the selling ofmerchandise, instead of a service, that makes the activities of a merchandising business dif-ferent from the activities of a service business.2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss ariseswhen operating expenses exceed gross profit. Therefore, a business can earn a gross profit but incur operating expenses in excess of this gross profit and end up with a net loss.3. a. Incr ease c. Decreaseb. Increase d. Decrease4. U nder the periodic method, the inventory records do not show the amount available for saleor the amount sold during the period. In contrast, under the perpetual method of accounting for merchandise inventory, each purchase and sale of merchandise is recorded in the invento-ry and the cost of merchandise sold accounts. As a result, the amount of merchandise availa-ble for sale and the amount sold are continuously (perpetually) disclosed in the inventory records.5. The multiple-step form of income statement contains conventional groupings for revenuesand expenses, with intermediate balances, before concluding with the net income balance. In the single-step form, the total of all expenses is deducted from the total of all revenues, with-out intermediate balances.6. The major advantages of the single-step form of income statement are its simplicity and itsemphasis on total revenues and total expenses as the determinants of net income. The major objection to the form is that such relationships as gross profit to sales and income from opera-tions to sales are not as readily determinable as when the multiple-step form is used.7. a. 2% discount allowed if paid within ten days of date of invoice; entire amount of invoicedue within 60 days of date of invoice.b. Payment due within 30 days of date of invoice.c. Payment due by the end of the month in which the sale was made.8. a. A credit memorandum issued by the seller of merchandise indicates the amount for whichthe buyer's account is to be credited (credit to Accounts Receivable) and the reason for the sales return or allowance.b. A debit memorandum issued by the buyer of merchandise indicates the amount for whichthe seller's account is to be debited (debit to Accounts Payable) and the reason for the purchases return or allowance.9. a. The buyerb. The seller10. E xamples of such accounts include the following: Sales, Sales Discounts, Sales Returns andAllowances, Cost of Merchandise Sold, Merchandise Inventory.Ex. 6–1a. $490,000 ($250,000 + $975,000 – $735,000)b.40% ($490,000 ÷ $1,225,000)c. No. If operating expenses are less than gross profit, there will be a net income. On the otherhand, if operating expenses exceed gross profit, there will be a net loss.Ex. 6–2 : $15,710 million ( $20,946 million – $5,236 million )Ex. 6–3a. Purchases discounts, purchases returns and allowancesb. Transportation in;c. Merchandise available for saled. Merchandise inventory (ending)Ex. 6–41. The schedule should begin with the January 1, not the December 31, merchandise inventory.2. Purchases returns and allowances and purchases discounts should be deducted from (notadded to) purchases.3. The result of subtracting purchases returns and allowances and purchases discounts frompur chases should be labeled ―net purchases.‖4. Transportation in should be added to net purchases to yield cost of merchandise purchased.5. The merchandise inventory at December 31 should be deducted from merchandise availablefor sale to yield cost of merchandise sold.A correct cost of merchandise sold section is as follows:Cost of merchandise sold:Merchandise inventory, January 1, 2006 ........ $132,000 Purchases ........................................................... $600,000Less: Purchases returns and allowances$14,000Purchases discounts .............................. 6,000 20,000 Net purchases ..................................................... $580,000Add transportation in ....................................... 7,500Cost of merchandise purchased ................. 587,500 Merchandise available for sale ......................... $719,500 Less merchandise inventory,December 31, 2006....................................... 120,000 Cost of merchandise sold .................................. $599,500 Ex. 6–5Net sales: $3,010,000 ( $3,570,000 – $320,000 – $240,000 )Gross profit: $868,000 ( $3,010,000 – $2,142,000 )Ex. 6–6THE MERIDEN COMPANYIncome StatementFor the Year Ended June 30, 2006Revenues:Net sales ................................................................................. $5,400,000Rent revenue ......................................................................... 30,000Total revenues................................................................... $5,430,000 Expenses:Cost of merchandise sold ..................................................... $3,240,000Selling expenses .................................................................... 480,000Administrative expenses ...................................................... 300,000Interest expense .................................................................... 47,500Total expenses ................................................................... 4,067,500Net income ..................................................................................... $1,362,500Ex. 6–71. Sales returns and allowances and sales discounts should be deducted from (not added to)sales.2. Sales returns and allowances and sales discounts should be deducted from sales to yield "netsales" (not gross sales).3. Deducting the cost of merchandise sold from net sales yields gross profit.4. Deducting the total operating expenses from gross profit would yield income from operations(or operating income).5. Interest revenue should be reported under the caption ―Other income‖ and should be addedto Income from operations to arrive at Net income.6. The final amount on the income statement should be labeled Net income, not Gross profit.A correct income statement would be as follows:THE PLAUTUS COMPANYIncome StatementFor the Year Ended October 31, 2006Revenue from sales:Sales .................................................................... $4,200,000Less: Sales returns and allowances ............... $81,200Sales discounts ....................................... 20,300 101,500Net sales ........................................................ $4,098,500 Cost of merchandise sold ........................................ 2,093,000 Gross profit .............................................................. $2,005,500 Operating expenses:Selling expenses ................................................. $ 203,000Transportation out ............................................ 7,500Administrative expenses ................................... 122,000Total operating expenses ............................ 332,500 Income from operations .......................................... $1,673,000 Other income:Interest revenue ................................................. 66,500Net income ................................................................ $1,739,500 Ex. 6–8a. $25,000 c. $477,000 e. $40,000 g. $757,500b. $210,000 d. $192,000 f. $520,000 h. $690,000Ex. 6–9a. Cash ......................................................................................... 6,900Sales ................................................................................... 6,900 Cost of Merchandise Sold ...................................................... 4,830Merchandise Inventory .................................................... 4,830b. Accounts Receivable ............................................................... 7,500Sales ................................................................................... 7,500 Cost of Merchandise Sold ...................................................... 5,625Merchandise Inventory .................................................... 5,625c. Cash ......................................................................................... 10,200Sales ................................................................................... 10,200 Cost of Merchandise Sold ...................................................... 6,630Merchandise Inventory .................................................... 6,630d. Accounts Receivable—American Express ........................... 7,200Sales ................................................................................... 7,200 Cost of Merchandise Sold ...................................................... 5,040Merchandise Inventory .................................................... 5,040e. Credit Card Expense (675)Cash (675)f. Cash ......................................................................................... 6,875Credit Card Expense (325)Accounts Receivable—American Express ..................... 7,200Ex. 6–10It was acceptable to debit Sales for the $235,750. However, using Sales Returns and Allow-ances assists management in monitoring the amount of returns so that quick action can be taken if returns become excessive.Accounts Receivable should also have been credited for $235,750. In addition, Cost of Mer-chandise Sold should only have been credited for the cost of the merchandise sold, not the selling price. Merchandise Inventory should also have been debited for the cost of the merchandise re-turned. The entries to correctly record the returns would have been as follows: Sales (or Sales Returns and Allowances) ............................. 235,750Accounts Receivable ......................................................... 235,750 Merchandise Inventory .......................................................... 141,450Cost of Merchandise Sold ................................................ 141,450Ex. 6–11a. $7,350 [$7,500 – $150 ($7,500 × 2%)]b. Sales Returns and Allowances .............................................. 7,500Sales Discounts (150)Cash ................................................................................... 7,350Merchandise Inventory .......................................................... 4,500Cost of Merchandise Sold ................................................ 4,500Ex. 6–12(1) Sold merchandise on account, $12,000.(2) Recorded the cost of the merchandise sold and reduced the merchandise inventory account,$7,800.(3) Accepted a return of merchandise and granted an allowance, $2,500.(4) Updated the merchandise inventory account for the cost of the merchandise returned,$1,625.(5) Received the balance due within the discount period, $9,405. [Sale of $12,000, less return of$2,500, less discount of $95 (1% × $9,500).]Ex. 6–13a. $18,000b. $18,375c. $540 (3% × $18,000)d. $17,835Ex. 6–14a. $7,546 [Purchase of $8,500, less return of $800, less discount of $154 ($7,700 × 2%)]b. Merchandise InventoryEx. 6–15Offer A is lower than offer B. Details are as follows:A BList price ............................................................................... $40,000 $40,300Less discount ......................................................................... 800 403$39,200 $39,897 Transportation (625)$39,825 $39,897Ex. 6–16(1) Purchased merchandise on account at a net cost of $8,000.(2) Paid transportation costs, $175.(3) An allowance or return of merchandise was granted by the creditor, $1,000.(4) Paid the balance due within the discount period: debited Accounts Payable, $7,000, and cre-dited Merchandise Inventory for the amount of the discount, $140, and Cash, $6,860.Ex. 6–17a. Merchandise Inventory .......................................................... 7,500Accounts Payable ............................................................. 7,500b. Accounts Payable ................................................................... 1,200Merchandise Inventory .................................................... 1,200c. Accounts Payable ................................................................... 6,300Cash ................................................................................... 6,174Merchandise Inventory (126)a. Merchandise Inventory .......................................................... 12,000Accounts Payable—Loew Co. ......................................... 12,000b. Accounts Payable—Loew Co. ............................................... 12,000Cash ................................................................................... 11,760Merchandise Inventory (240)c. Accounts Payable*—Loew Co. ............................................. 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. (940)*Note: The debit of $2,940 to Accounts Payable in entry (c) is the amount of cash refund due from Loew Co. It is computed as the amount that was paid for the returned merchandise, $3,000, less the purchase discount of $60 ($3,000 × 2%). The credit to Accounts Payable of $2,000 in en-try (d) reduces the debit balance in the account to $940, which is the amount of the cash refund in entry (e). The alternative entries below yield the same final results.c. Accounts Receivable—Loew Co. .......................................... 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. ............................................... 2,000Accounts Receivable—Loew Co. .................................... 2,940Ex. 6–19a. $10,500b. $4,160 [($4,500 – $500) ⨯ 0.99] + $200c. $4,900d. $3,960e. $834 [($1,500 – $700) ⨯ 0.98] + $50Ex. 6–20a. At the time of sale c. $4,280b. $4,000 d. Sales Tax PayableEx. 6–21a. Accounts Receivable ............................................................... 9,720Sales ................................................................................... 9,000Sales Tax Payable (720)Cost of Merchandise Sold ...................................................... 6,300Merchandise Inventory .................................................... 6,300b. Sales Tax Payable ................................................................... 9,175Cash ................................................................................... 9,175a. Accounts Receivable—Beta Co. ........................................... 11,500Sales ................................................................................... 11,500 Cost of Merchandise Sold ...................................................... 6,900Merchandise Inventory .................................................... 6,900b. Sales Returns and Allowances (900)Accounts Receivable—Beta Co. (900)Merchandise Inventory (540)Cost of Merchandise Sold (540)c. Cash ......................................................................................... 10,388Sales Discounts (212)Accounts Receivable—Beta Co. ...................................... 10,600Ex. 6–23a. Merchandise Inventory .......................................................... 11,500Accounts Payable—Superior Co. ................................... 11,500b. Accounts Payable—Superior Co. (900)Merchandise Inventory (900)c. Accounts Payable—Superior Co. ......................................... 10,600Cash ................................................................................... 10,388Merchandise Inventory (212)Ex. 6–24a. debit c. credit e. debitb. debit d. debit f. debitEx. 6–25(b) Cost of Merchandise Sold (d) Sales (e)Sales Discounts(f) Sales Returns and Allowances (g) Salaries Expense (j) Supplies ExpenseEx. 6–26a. 2003: 2.07 [$58,247,000,000 ÷ ($30,011,000,000 + $26,394,000,000)/2]2002: 2.24 [$53,553,000,000 ÷ ($26,394,000,000 + $21,385,000,000)/2]b.These analyses indicate a decrease in the effectiveness in the use of the assets to generateprofits. This decrease is probably due to the slowdown in the U.S. economy during 2002–2003. However, a comparison with similar companies or industry averages would be helpful in making a more definitive statement on the effectiveness of the use of the assets.Ex. 6–27a. 4.13 [$12,334,353,000 ÷ ($2,937,578,000 + $3,041,670,000)/2]b. Although Winn-Dixie and Zales are both retail stores, Zales sells jewelry at a much slowervelocity than Winn-Dixie sells groceries. Thus, Winn-Dixie is able to generate $4.13 of sales for every dollar of assets. Zales, however, is only able to generate $1.53 in sales per dollar of assets. This makes sense when one considers the sales rate for jewelry and the relative cost of holding jewelry inventory, relative to groceries. Fortunately, Zales is able to counter its slow sales velocity, relative to groceries, with higher gross profits, relative to groceries. Appendix 1—Ex. 6–28a. and c.SALES JOURNALCost of MerchandiseSold Dr.Invoice Post.Accts. Rec. Dr. MerchandiseDate No. Account Debited Ref.Sales Cr. Inventory Cr.2006Aug. 3 80 Adrienne Richt ................... ✓12,000 4,0008 81 K. Smith .............................. ✓10,000 5,50019 82 L. Lao .................................. ✓9,000 4,00026 83 Cheryl Pugh ........................ ✓14,000 6,50045,000 20,000b. andc.PURCHASES JOURNALAccounts Merchandise OtherPost Payable Inventory Accounts Post.Date Account Credited Ref.Cr. Dr. Dr. Ref. Amount2006Aug. 10 Draco Rug Importers ................. ✓8,000 8,00012 Draco Rug Importers ................. ✓3,500 3,50021 Draco Rug Importers ................. ✓19,500 19,50031,000 31,000d.Merchandise inventory, August 1 ............................................... $ 19,000Plus: August purchases ................................................................ 31,000Less: Cost of merchandise sold ................................................... (20,000)Merchandise inventory, August 31 ............................................. $ 30,000ORQuantity Rug Style Cost2 10 by 6 Chinese* $ 7,5001 8 by 10 Persian 5,5001 8 by 10 Indian 4,0002 10 by 12 Persian 13,000$ 30,000*($4,000 + $3,500)。

西方会计学知识点归纳

西方会计学知识点归纳在全球范围内,会计被认为是商业领域中最为重要的职业之一。

西方会计学是指以美国为代表的西方国家在财务会计领域的研究和实践。

随着全球经济的发展和国际贸易的增加,西方会计学的知识点也变得越来越重要。

本文将归纳西方会计学的一些重要知识点。

一、财务报表财务报表是一家公司或组织的财务状况、盈利能力和现金流量的重要信息来源。

根据西方会计学的观点,财务报表通常包括资产负债表、损益表和现金流量表。

资产负债表展示了公司在特定日期的资产、负债和所有者权益,损益表反映了公司在一段时间内的盈利能力,而现金流量表则显示了公司在一段时间内的现金收入和支出情况。

二、会计原则和准则在西方会计学中,会计原则和准则被视为规范会计实践的重要指导。

比较常见的会计原则包括权责发生制、实质重于形式原则和成本原则。

权责发生制要求会计应该在经济交易发生的同时确认和记录相关的收入和支出。

实质重于形式原则强调会计报表应该反映经济实质而不是法律形式。

成本原则要求会计以历史成本为基础计量资产和负债。

三、财务分析财务分析是评估公司财务状况以及预测未来经营绩效的过程。

西方会计学中的财务分析通常包括水平分析、垂直分析和比率分析。

水平分析用于比较相同公司在不同时间点的财务数据,以了解其变化情况。

垂直分析则将财务数据以百分比形式展示,以便更好地分析资产和负债的结构。

比率分析则通过比较不同财务指标之间的比率,来评估公司的盈利能力、偿债能力和运营能力等方面。

四、预算与控制预算和控制是西方会计学中的重要概念,用于确保公司达到其预期目标并保持财务稳定。

预算是指对公司在一定时间范围内的收入和支出进行规划和控制。

通过编制预算,公司可以更好地管理和分配资源,以实现经营目标。

而控制则是通过比较实际结果与预算来评估业绩,并采取相应措施进行调整和改进。

五、内部控制内部控制是指公司为了保护财务资产、确保财务报告的准确性和促进经营活动的有效性而采取的一系列措施和程序。

西方财务会计_Chapter647页PPT.pptx

Page 69

Debit 21,875

Credit 21,875

Accounts Receivable Method Example

Single Composite Rate Crecore, Inc. determined that the balance in the

Allowance for Doubtful Accounts should be 2.5% of Accounts Receivable. At year-end

Allowance Method

When we estimate the amount of our uncollectible receivables, we make the following adjusting entry:

GENERAL JOURNAL

Post.

Date

Description

year, whether a debit or a credit, is again adjusted to

bring the account to the proper balance when a new estimate is made.

Collecting written-off accounts

Allowance Method

As accounts become uncollectible, the following entry is made:

GENERAL JOURNAL

Post.

Date

Description

Ref.

Allowance for Doubtful Accounts

Accounts Receivable

西方财务会计 第五章

第五章 现金及其他流动性金融资产

第一节 现金

• 一、现金的内容及其管理

• 现金 • 充分、有效地安排使用现金,使其保持合理的数量 • 现金的管理 • 充分、有效地安排使用现金,使其保持合理的数量。 • 二、现金的内部控制 • 为保护资产安全、保证会计记录的可靠性、提高经营效率以及促进对 法律法规的遵守而设计和执行的政策及程序

续

三、坏账损失的估计方法 1、销售收入百分比 以一定百分乘赊销额估计坏账费用 2、应收账款法 着眼于资产负债表,分析资产负债表中应收账款可收回金 额,通过会计调整确认坏账费用 • 运用坏账准备账户 • • • • •

续

• 估计坏账准备余额两种方法: • 1、应收账款余额百分比法 • 以一定百分乘以应收账款余额计算出不能收回的应收账款 金额,即“坏账准备”账户的期末余额 • 比较计算出的不能收回的应收账款金额与“坏账准备”账 户调整前余额 • 确定坏账费用 • 2、应收账款账龄分析法 • 通过分析应收账款账龄估计无法收回的应收账款金额 • 不同账龄的坏账比例不同 • 两种估计方法程序完全一样

续

• 四、银行对账单

• 银行对账:开户银行向开户企业每月寄送列明开户企 业银行账户的变化情况的银行账单

• 1、未达账项

• (1)企业已入账而银行未记录的收入

• (2)企业已入账而银行未记录的支出 • (3)银行已入账而企业未记录的收入

• (4)银行已入账而企业未记录的支出

续

• 2、银行存款余额调节表 • 根据对账单,将企业现金账户余额和银行账户余额调整到 正确余额的调节表 • 3、现金账户余额调整 • 根据调节表,调整企业现金账户 • 五、现金列报

西方财务会计

第一章 企业活动简介、财务报表 与会计程序概述

第一节 企业活动概观

企业一般来说有四种主要活动 (1)建立企业目标和策略 (2)融资活动 (3)投资活动 (4)经营活动

一、建立企业目标和策略

企业目标:企业要实现的任务或最终追求的结 果。 企业策略:实现目标的途径。 设立目标和策略时必须考虑的外部因素: 1、竞争对手 2、行业障碍 3、行业对产品的需求发展趋势 4、行业所受的行政法规约束

公司一般会通过股东年报来向股东报告企业的 经营成果。具体包括: 1、资产负债表 2、利润表 3、现金流量表 4、财务报表附注 5、独立会计师出具的负债和所有者权益的概念 资产负债表的分析

二、利润表

净利润、收入和费用的概念 利润表和资产负债表的关系 利润表分析

二、融资活动

从所有者及债权人处获得资金

三、投资活动

投资活动的主要内容: 1、土地、建筑物和设备 2、专利、许可证和其他契约权利 3、普通股或其他公司债券 4、存货 5、应收账款 6、现金

四、经营活动

1、采购 2、生产 3、营销 4、管理

第二节 主要财务报表

三、现金流量表

现金流的三大来源 现金流量表的分析

第三节 年报中的其他事项

一、财务报表和附注 二、审计报告 审计报告分三个阶段: 1、审计意见所概括的内容 2、确认审计师遵循了公认的会计准则和工作 程序 3、出具审计意见

第四节 财务报告事项

财务报告过程涉及的参与者 财务报告中的伦理问题

西方财务会计双语单词

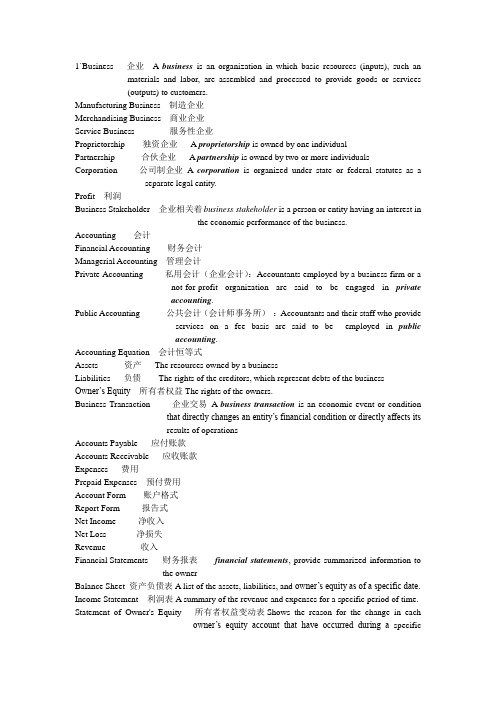

1`Business 企业 A business is an organization in which basic resources (inputs), such an materials and labor, are assembled and processed to provide goods or services(outputs) to customers.Manufacturing Business 制造企业Merchandising Business 商业企业Service Business 服务性企业Proprietorship 独资企业 A proprietorship is owned by one individualPartnership 合伙企业 A partnership is owned by two or more individuals Corporation 公司制企业A corporation is organized under state or federal statutes as a separate legal entity.Profit 利润Business Stakeholder 企业相关着business stakeholder is a person or entity having an interest inthe economic performance of the business.Accounting 会计Financial Accounting 财务会计Managerial Accounting 管理会计Private Accounting 私用会计(企业会计):Accountants employed by a business firm or anot-for-profit organization are said to be engaged in privateaccounting.Public Accounting 公共会计(会计师事务所):Accountants and their staff who provideservices on a fee basis are said to be employed in publicaccounting.Accounting Equation 会计恒等式Assets 资产The resources owned by a businessLiabilities 负债The rights of the creditors, which represent debts of the business Owner’s Equity所有者权益The rights of the owners.Business Transaction 企业交易A business transaction is an economic event or conditionthat directly changes an entity’s financial condition or directly affects itsresults of operationsAccounts Payable 应付账款Accounts Receivable 应收账款Expenses 费用Prepaid Expenses 预付费用Account Form 账户格式Report Form 报告式Net Income 净收入Net Loss 净损失Revenue 收入Financial Statements 财务报表financial statements, provide summarized information tothe ownerBalance Sheet 资产负债表A list of the assets, liabilities, and owner’s equity as of a specific date. Income Statement 利润表A summary of the revenue and expenses for a specific period of time. Statement of Owner's Equity 所有者权益变动表Shows the reason for the change in eachowner’s equity account that have occurred during a specificperiod of time.Generally Accepted Accounting Principles (GAAP) 公认会计原则Statement of Cash Flows 现金流量表A summary of the cash receipts and disbursements for a specific period of time.Certified Public Accountant (CPA) 注册会计师2`Account 账户An account is a separate record to show the increase and decrease of each financial statement item.Ledger 分类账A group of accounts for a business entity is called a ledgerChart of Accounts 科目表A list of the accounts in the ledger is called a chart of account Revenues 收入类账户Expenses 资产消耗Drawing 提款账户Balance of the Account 账户余额Debits 借方金额Credits 贷方金额T Account T 型帐 An account can be drawn to resemble the letter T, it is called a T account. Double-Entry Accounting 复式记账会计Journal Entry 日记账分录Journal 日记账Journalizing 日记簿记账2Posting 过账Two-Column Journal 二栏式日记账Unearned Revenue 预收收入The liability created by receiving the cash in advance of providing the service is called unearned revenve.Trial Balance 试算平衡3`Cash Basis 现今制(收付实现制)period in which cash is received or paidAccrual Basis 应计制(权责发生制)period in which they are earnedAdjusting Process 调整程序Accruals 应计项目Deferrals 递延项Deferred Expenses 递延费用(预付费用)have been initially recorded as assets but areexpected to become expensesAccrued Expenses 应计费用(accrued liabilities)Deferred Revenues 递延收入(预收收入)have ben initially recorded as liability bu areexpected to become revenuesAccrued Revenues 应计收入(accrued assets)Prepaid Expenses 预付费用Adjusting Entries 调整账户Unearned Expenses 预收费用?Adjusted Trial Balance 调整试算平衡Accumulated Depreciation累计折旧Depreciation 折旧Book Value of the Asset 资产账面价值Depreciation Expense 折旧费用Contra Accounts 备抵账户accumulated depreciation accountsFixed Assets 固定资产(plant assets)4`Accounting Cycle 会计循环Work Sheet 工作底稿Current Assets 流动资产Cash and other assets that are expected to be converted into cash,sold, or used up usually in less than a year are current assets.Current Liabilities 流动负债Long-Term Liabilities 长期负债Post-Closing Trial Balance 结账后试算表Closing Entries 结账分录Real Account 实账户Temporary Accounts (Nominal Accounts ) 虚账户(类似过渡账户)Income Summary 损益表(反应某一特定时期收入费用状况的报表)5`Accounting System 会计系统General Ledger 总分类账Accounts Payable Subsidiary Ledger 应付账款明细账Accounts Receivable Subsidiary Ledger 应收账款明细账Purchases Journal 赊购日记账The purchases journal is designed for recording allpurchases on account.Cash Payments Journal 现金支出日记账Revenue Journal 赊销日记账Cash Receipts Journal 现金收入日记账All transactions that involve the receipt of cash arerecorded in the cash receipts journalSpecial Journals 特种日记账Controlling Account 控制账户General Journal 普通日记账6` Multiple-Step Income Statement 多步式损益表Single-Step Income Statement 单步式损益表Sales 销售额Sales Discounts 销售折扣Sales Returns & Allowances 销售退回及折让Purchase 购买额Purchase Discount 购货折扣Purchase Returns & Allowances 购货退回或折让Periodic Method 实地盘存制Perpetual Method 永续盘存制Merchandise Inventory 商品存货Cost of Merchandise Sold 商品销售成本Gross Profit 毛利润Administrative Expenses管理费用Selling Expenses 销售费用Income from Operations 营业收入Other Expense 其他费用Other Income 其他收益Invoice 发票Credit Memorandum 贷项通知单Debit Memorandum 借项通知单FOB Destination 目的地交货FOB Shipping Point 船上交货Trade Discounts 商业折扣7` Cash 现金Bank Reconciliation 银行存款余额调节表Check 支票Remittance advice 汇款通知Transactions register 交易登记册(交易账簿)Deposit ticket 存款票据Signature card 签名卡Drawee 付款人Drawer 发票人Payee 收款人8` Accounts Receivable 应收账款Notes Receivable 应收票据Allowance Method 备抵法Uncollectible Accounts Expense 坏账损失Direct Write-Off Method 直接冲销法Aging the Receivables 应收账款账龄分析法Net Realizable Value 可变现价值Maturity Value 到期价值Promissory Note 本票9`Inventory 存货Periodic Inventory System 实地盘存制Perpetual Inventory System 永续盘存制Average Cost Method 加权平均法First-in, First-out (FIFO) Method 先进先出法Last-in, First-out (LIFO) Method 后进先出法Lower-of-Cost-or-Market (LCM) Method 成本与市价孰低法Gross Profit Method 毛利率法Retail Inventory Method 零售价法10`Fixed assets 固定资产损失Depreciation 折旧Residual Value 剩余价值Book Value 账面价值Accelerated Depreciation Method 加速折旧法Straight-Line Method 直线法Declining-Balance Method 余额递减法Units-of-Production Method 工作量法Trade-in Allowance 交换折价Depletion 折耗Amortization 摊销Intangible Assets 无形资产Copyright 版权Patents 专利Goodwill 商誉Trademark 商标Boot 补价(附得利益)11`Discount 折价Discount Rate 贴现率Proceeds 应收票据贴现率Gross Pay 毛工资Net Pay 净薪资Payroll 薪酬Defined Contribution Plan 确定投入计划Defined Benefit Plan 确定收益计划12`Stock 股份Stockholders 股东Stockholders’Equity 股东权益Retained Earnings 留存收益Paid-in Capital 实收资本Common Stock 普通股Preferred Stock 优先股Par 平价Cumulative Preferred Stock 累积优先股Nonparticipating Preferred StockStated Value 设定价值Outstanding Stock发行在外股票Premium 溢价Treasury Stock 库藏股票Stock Split 股票分割Cash Dividend 现金股利Stock Dividend 股票股利。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2、财务报表的要素和会计恒等式

一、财务会计的定义

1、财务会计与管理会计是现代会计的两大分支 在现代会计中已向企业外部的各种利害关系人提供财务信息为主要目标 的分支,就是财务会计。正是在这个意义上,财务会计被视为对外会计。 在现代会计中,有发展和形成了一个向企业内部各级管理当局提供进行 经营决策和业绩考核所需信息为主要目标的分支,这就是管理会计。也 正是在这个意义上,管理会计被视为内部会计。管理会计已大大的突破 了传统的会计程序和方法。

课程的主要内容:财务会计中的基本概念;复式记账原理与 会计循环;商品购销业务;现金收支业务;商业账款和 商业票据;存货;长期资产;应纳税捐;应付公司债与 债券投资;公司的股东权益;合伙的业主权益;财务状 况变动表和现金流量表;财务报表的分析;财务会计中 的特定领域。

第一章 财务会计中的基本概念 要求:理解规范财务会计的公认会计准则和

制作人:焦平英

联系方式: zileiningxiang@

➢课程介绍 ➢教学内容 ➢相关资料 ➢考试指导

教学内容

第一章 财务会计中的基本概念 第二章 复式记账原理与会计循环 第三章 商品购销业务 第四章 现金收支业务 第五章 商业帐款与商业票据 第六章 存货 第七章 长期资产 第八章 应纳税捐 第九章 应付公司债与债券投资 第十章 公司的股东权益 第十一章 合伙的业主权益 第十二章 财务状况变动表和现金流量表 第十三章 财务报表的分析 第十四章 财务会计的特定领域

1、企业财务报表的五项基本要素:

(1)资产;(2)负债;(3)业主权益;(4)收入;(5)费用。 请分别掌握它们的含义。 资产是指作为以往事项的结果而由企业拥有或控制的、可望为企业创造

未来经济利益的资源。 负债是指由于以往事项而发生的、企业现有的义务,这种义务的清偿或

履行将导致含有经济利益的企业资源的流出。 业主权益是指在企业的资产中扣除企业全部负债以后的余剩权益,也即

业主对企业的净资产享有的权益。 收益是指会计期间内经济利益的增加。其形式表现为因资产流入、资产

增值或是负债减少而导致业主权益的增加,但不包括与业主出资有关 的事项。 费用是指会计期间内经济及利益的减少。其形式表现为因资产流出、资 产低耗或是负债发生而导致业主权益的减少,但不包括与业主派得有 关的类似事项。

课程介绍

《西方财务会计》是现代远程教育财务会计专业的一门选修 课程。通过教学,要求学生更好地理解和掌握西文财务 会计理论知识以及会计核算方法、内容和技术的具体运 用,结合我国企业的特点,从实际情况出发,联系实际, 借鉴国际经济,按照国际惯例,达到改进和提高我国的 会计工作和财务管理水平。

主要介绍美国企业财务会计的基本理论和基本方法。

2、 财务会计的定义:财务会计是在企业传统会计基础上形成的、受公认 会计准则 规范的、以提供企业外部利害关系人所需的通用财务报告为主要目标的 会计系统。

二、会计基本假设与会计基本原则

1、会计基本假设: 作为财务会计结构基础的四项基本原则假设是: (1)经济主体假设 (2)持续经营(企业)假设 (3)货币计量(单位)假设 (4)会计分期假设

而财务状况变动表、现金流量表则在第十二章加以论述。

第二章 复式记账原理与会计循环

要求:通过会计循环,熟练地掌握帐务处理 和报表编制的基本程序与技术。

重点:1、帐项调整;2、报表编制; 3、结账。

会计计量、确认、反应是会计基本方法的三个方面,这在第一章论 述会计基本原则时已经说明,当前在财务会计中,一般的说,会计 计量是以历史成本原则为基础,会计确认是以权责发生制为基础, 本章将继而说明;会计反映以复式记帐程序为基础,在这一章加以 说明。 在这一章,以服务企业为例,说明会计循环及帐册组织的最基本形式。 一、 复式记账原理 1、复式记账原理与借贷规则。 2、账户的设计。

二、分录与过账 会计循环是由一次完成的帐务处理和报表编制程序构成的。可大致分为

五个步骤:(1)作分录,(2)过账,(3)调整某些帐项, (4)编制财务报表,(5)结账。

理解分录与过账的实例:日记账与分类账。

三、帐项调整、编制报表与结账 (一)帐项调整 1、帐项调整的意义:

通过会计日常记录反映在帐户中的经济业务,有些不只影响到一个 会计期间的净收益确定。为了在权责发生制的基础上反映企业在各 个期间的经营成果,就必须把报告期内已赚得收入同为赚得当期收 入而发生的全部费用相配比。因而,常常需要在每个会计期末调整 一些有关帐户的余额,即进行帐项调整程序。 2、内容: (1)预收收入:按收益的会计期间摊配已入帐的资本支出。 (2)预付费用:按赚取的会计期间摊配已入帐的的预收收益。 (3)应计收入:计提这一会计期间已发生但尚未入帐的费用。 (4)应计费用:计提这一会计期间已赚取但尚未入帐的收入。 (二)编制财务报表:在实际工作中工作底表的应用; (三)结帐: 通常要使用“收益汇总”帐户来结转收益和费用帐户的余额,结转以 后,收益汇总帐户的余额即等于本期净收益额。而后,再把收益汇

总帐户和业主提款帐户的余额结转业主资本帐户。

第三章 商品购销业务

要求:熟练地掌握商品购、销业务的帐务处理。

重点: 1、商品购、销业务的帐务处理全过程; 2、商业企业收益表的基本结构。

2、资产负债表的会计恒等式 资产=负债+业主权益 收益表的关系式:收益—费用=净收益

因为业主权益的变动时有以下两个所引起的: (1)投资与派得;(2)企业的净收益, 所以,对会计恒等式中业主权益这一要素也可以表达成:

业主权益=业主出资+净收益-业主派得

四、财务报表的基本形式

资产负债表、收益表、业主权益表三个报表实际上都是上述三个关系 式的展开。

2、会计基本原则: 作为记录企业经济业务的指南的会计基本原则是: (1)历史成本原则(2)收入实现原则(3)配比原则 (4)一致性原则 (5)充分揭示原则(6)客观性原则 (7)重大性原则 (8)稳健性原则。

一般说,第(4)至(8)条,是涉及会计基本要素与会计恒等式