chapter-12习题课解读

Chapter 12 课后答案

新编语言学教程Chapter 12答案Applied Linguistics1. Define the following terms briefly.(1)applied linguistics: the study of language and linguistics in relation to practicalissues, e.g. speech therapy, language teaching, testing, and translation.More often than not nowadays, it is used in the narrow sense, and refers tolanguage teaching in particular.(2)grammar-translation method: a method of foreign or second languageteaching which makes use of translation and grammar study as the mainteaching and learning activities.(3) audiolingual method: the teaching of a second language through imitation,repetition, and reinforcement. It emphasizes the teaching of speaking andlistening before reading and writing and the use of mother tongue in theclassroom is not allowed.(4)communicative language teaching: an approach to foreign or second languageteaching which emphasizes that the goal of language learning is toachieve communicative competence.(5)testing: the use of tests, or the study of the theory and practice of their use,development, evaluation, etc.(6)achievement test: a test which measures how much of a language someone haslearned with reference to a particular course of study or program of instruction.(7)validity: (in testing) the degree to which a test measures what it is supposedto measure, or can be used successfully for the purposes for which it is intended.A number of different statistical procedures can be applied to a testto estimate its validity. Such procedures generally seek to determine what thetest measures, and how well it does so.(8)reliability: (in testing) a measure of the degree to which a test gives consistentresults; a test is said to be reliable if it gives the same results when it isgiven on different occasions or when it is taken by different people.(9)proficiency test: a test which measures how much of a language someone haslearned without considering the syllabus, duration and manner of learning.(10) subjective test: a test which is scored according to the personal judgment ofthe marker, such as essay writing or translation.(11) objective test: a test that can be marked without the use of the examiner’spersonal judgment.(12) language aptitude test: a test which measures a person’s aptitude for secondor foreign language learning and it can be used to identify those learners who are most likely to succeed.(13) diagnostic test: a test which is designed to show what skills or knowledge alearner knows and doesn’t know. For example, a diagnostic pronunciationtest may be used to measure the learner’s pronunciation of English sounds.It would show which sounds a student is and is not able to pronounce. Diagnostictests may be used to find out how much a learner knows or to measure how successful an instruction program has been.(14) backwash effect: Tests strongly affect what actually occurs in the classroomand the effect of tests on classroom L2 teaching and learning is known as thebackwash effect.2. The advantages of grammar-translation method:(1)As the grammars described in this method contain very detailed descriptionsof the correct construction of phrases and sentences of a language, accuracyis stressed and improved.(2)Students’ ability to read and write is encouraged and improved since themethod focuses on the written work.(3)This method is less demanding than some other approaches for a teacherwhose oral proficiency may not be adequate.(4)This method is popular with people who would like to study English independently,especially the adult learners who want to learn grammar rules anduse them to approach new materials by themselves.The disadvantages of grammar-translation method:(1)It emphasizes language at the sentence level regardless of context, so the organizationof language above the sentence level is not so carefully studied.(2)As the focus is on written work, oral fluency and spontaneity is not so welldeveloped and common everyday language is not taught enough.(3)The basic techniques in this method are rote learning of the rules and vocabulary,and grammar rules are taught deductively as general statements tobe applied in particular exercises in translation, so the learners may find itboring to learn.(4)With the emphasis on grammar, students typically know a lot about the languagebut are unable to actually use it. As a result, their use of the new languageoften tends to be literal or unnatural.3.Changes required would include:(1)Change in teacher’s role. The teacher can no longer be the source of knowledgeand trut h about the language. The teacher’s role has more to do withinitiating activities.(2)Change in learner’s role. The learner can no longer be passive. The learnermust actively participate in the activities.(3)Change of materials. These should, as far as possible, preserve the features ofauthentic instances of language use.(4)Change of techniques. These should emphasize the tasks (not drills) to beperformed and identify the skills being practiced.(5)Change in attitude. If the above are to be achieved then we are involved inchanging our attitudes towards teaching and learning in general.4.Achievement tests are based on a particular language syllabus, or part of a syllabus,or chapters in a textbook that learners are known to have studied and theyaim to know how well learners know what they have been taught. For example,the Chinese MET test, which is based on the Middle School English Syllabus andtaken by students leaving Senior Middle School, and Mid-Term tests, designed forUniversity English Majors based on just a few chapters from a textbook.5.The validity of a test relates to what the test claims to measure and how well itdoes so. If we know that a test is valid, then we know what we can confidently sayabout a person who passes or fails it. The two most important aspects of validityare content validity and construct validity. If a test has content validity it meansthat the test questions cover a fair sample of the language structures and skillsthat the test claims to be measuring. If a test has construct validity, it shows that itmeasures only what it claims to measure and nothing else.6.A test is said to be reliable if it gives the same results when it is given on differentoccasions or when it is taken by different people. There are two aspects to reliability:test reliability and scorer reliability. Test reliability refers to how consistent scoresare on a test. If, for example, there are two versions of a particular test and the sameperson takes them on consecutive days and his scores are almost the same on eachversion, then such a test has test reliability. A test has scorer reliability if there is ahigh level of agreement between different people marking the same test paper.。

-新课标高三英语Unit12知识点讲解与练习.ppt[原创]

![-新课标高三英语Unit12知识点讲解与练习.ppt[原创]](https://img.taocdn.com/s3/m/741f9a5aaf1ffc4ffe47ac5c.png)

4. absent adj. 缺席的,不在场的. n. absence 缺席 be absent from 心不在焉的 absent-minded

当我和他说话时,他茫然地看着我, 没有回答. When I spoke to him, he looked at me in an absent way but did not answer. 反义词: present 出席,到场 be present at n. presence

I. New words 1. 张老师对我们在学习方面要求很严格. Miss Zhang is strict with us in our study. 2. 起初, 她太年轻做不了这份工作. To begin with, she was too young for the job. 3. 晚会以一首民歌开始了. The evening party began with a folk song. The teacher asked the students to read poems, ____ C Tom. A. to start with B. to begin with C. starting with D. start with

II. Reading Passages 1. Expressions about education 1). 被准予入学 be admitted into / to school 2). 受教育 receive education go to school 3). 去上学 4). 上学/听课 attend school / class 5). 旷课 be absent from school 6). 辍学 drop out of school 7). 毕业 leave school / graduate from school 8). 义务教育 compulsory education

公司理财课后习题及答案chapter12estimatingthecostofcapital

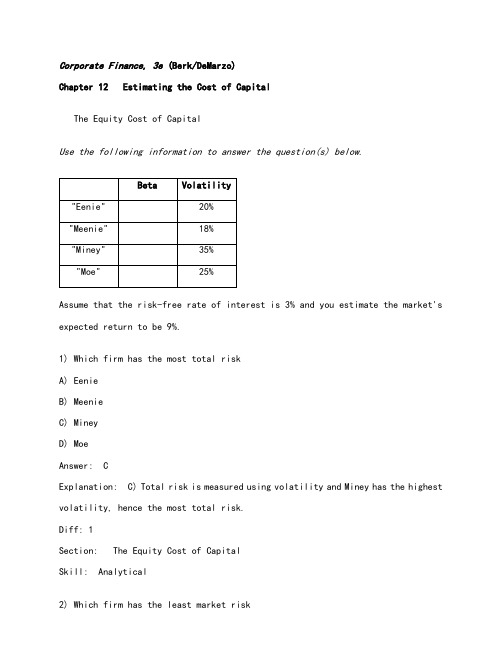

Corporate Finance, 3e (Berk/DeMarzo)Chapter 12 Estimating the Cost of CapitalThe Equity Cost of CapitalUse the following information to answer the question(s) below.Assume that the risk-free rate of interest is 3% and you estimate the market's expected return to be 9%.1) Which firm has the most total riskA) EenieB) MeenieC) MineyD) MoeAnswer: CExplanation: C) Total risk is measured using volatility and Miney has the highest volatility, hence the most total risk.Diff: 1Section: The Equity Cost of CapitalSkill: Analytical2) Which firm has the least market riskA) EenieB) MeenieC) MineyD) MoeAnswer: AExplanation: A) Market risk is measured using beta and Eenie has the lowest beta, hence the lowest market risk.Diff: 1Section: The Equity Cost of CapitalSkill: Analytical3) Which firm has the highest cost of equity capitalA) EenieB) MeenieC) MineyD) MoeAnswer: DExplanation: D) Cost of capital is measured using the CAPM and is a linear function of beta. Therefore the firm with the highest beta (Moe) has the highest cost of equity capital.Diff: 1Section: The Equity Cost of CapitalSkill: Analytical4) The equity cost of capital for "Miney" is closest to:A) %B) %C) %D) %Answer: CExplanation: C) r Miney = 3% + (9% - 3%) = %Diff: 1Section: The Equity Cost of CapitalSkill: Analytical5) The equity cost of capital for "Meenie" is closest to:A) %B) %C) %D) %Answer: BExplanation: B) r Meenie = 3% + (9% - 3%) = %Diff: 1Section: The Equity Cost of CapitalSkill: Analytical6) The risk premium for "Meenie" is closest to:A) %B) %C) %D) %Answer: AExplanation: A) risk premium Meenie = (9% - 3%) = % Diff: 2Section: The Equity Cost of CapitalSkill: AnalyticalThe Market PortfolioUse the following information to answer the question(s) below.Suppose all possible investment opportunities in the world are limited to the four stocks list in the table below:1) The weight on Taggart Transcontinental stock in the market portfolio is closest to:A) 15%B) 20%C) 25%D) 30%Answer: BExplanation: B)Section: The Market Portfolio Skill: Analytical2) The weight on Wyatt Oil stock in the market portfolio is closest to:A) 15%B) 20%C) 25%D) 30%Answer: AExplanation: A)Section: The Market PortfolioSkill: Analytical3) Suppose that you are holding a market portfolio and you have invested $9,000 in Rearden Metal. The amount that you have invested in Nielson Motors is closest to:A) $6,000B) $7,715C) $9,000D) $10,500Answer: DExplanation: D)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$Rearden Metal$45$Wyatt Oil$10$Nielson Motors$26$Total$Amount Nielson = × Amount Rearden = × $9,000 = $10,500 Diff: 2Section: The Market PortfolioSkill: Analytical4) Suppose that you are holding a market portfolio and you have invested $9,000 in Rearden Metal. The amount that you have invested in Taggart Transcontinental is closest to:A) $4,500B) $6,000C) $7,715D) $9,000Answer: BExplanation: B)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$Rearden Metal$45$Wyatt Oil$10$Nielson Motors$26$Total$Amount Nielson = × Amount Rearden = × $9,000 = $6,000Diff: 2Section: The Market PortfolioSkill: Analytical5) Suppose that you have invested $30,000 invested in the market portfolio. Then the amount that you have invested in Wyatt Oil is closest to:A) $4,500B) $6,000C) $7,715D) $9,000Answer: AExplanation: A)Amount WO = Weight WO × Amount Market= .15 × $30,000 = $4,500Diff: 2Section: The Market PortfolioSkill: Analytical6) Suppose that you have invested $30,000 in the market portfolio. Then the number of shares of Rearden Metal that you hold is closest to:A) 450 sharesB) 700 sharesC) 1,400 sharesD) 2,300 sharesAnswer: BExplanation: B)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$ Rearden Metal$45$ Wyatt Oil$10$ Nielson Motors$26$Total$ Shares RM = = = sharesDiff: 2Section: The Market PortfolioSkill: Analytical7) Suppose that you have invested $30,000 in the market portfolio. Then the number of shares of Wyatt Oil that you hold is closest to:A) 150 sharesB) 300 sharesC) 350 sharesD) 450 sharesAnswer: AExplanation: A)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$ Rearden Metal$45$ Wyatt Oil$10$ Nielson Motors$26$Total$ Shares WO = = = sharesDiff: 2Section: The Market PortfolioSkill: Analyticalin Taggart Transcontinental. The number of shares of Wyatt Oil that you hold is closest to:A) 90 sharesB) 460 sharesC) 615 sharesD) 770 sharesAnswer: BExplanation: B)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$ Rearden Metal$45$ Wyatt Oil$10$ Nielson Motors$26$Total$= = sharesDiff: 2Section: The Market PortfolioSkill: Analyticalin Taggart Transcontinental. The number of shares of Rearden Metal that you hold is closest to:A) 780 sharesB) 925 sharesC) 1,730 sharesD) 2,075 sharesAnswer: BExplanation: B)Calculations B × C D/1950Stock Price perShareNumber of SharesOutstanding(Millions)MarketCap WeightTaggart Transcontinental$25$Rearden Metal$45$Wyatt Oil$10$Nielson Motors$26$Total$= = 2, sharesDiff: 2Section: The Market PortfolioSkill: Analytical10) Suppose that you have invested $100,000 invested in the market portfolio and that the stock price of Taggart Transcontinental suddenly drops to $ per share.Which of the following trades would you need to make in order to maintain your investment in the market portfolio:1. Buy approximately 1,140 shares of Taggart Transcontinental2. Sell approximately 256 shares of Rearden Metal3. Sell approximately 57 shares of Wyatt Oil4. Sell approximately 148 shares of Nielson MotorsA) 1 onlyB) 2 onlyC) 2, 3, and 4 onlyD) 1, 2, 3, and 4E) None of the aboveAnswer: EExplanation: E) There is no need to rebalance your portfolio. As an investor, you still hold the market portfolio and therefore there are no trades needed. Diff: 3Section: The Market PortfolioSkill: AnalyticalUse the following information to answer the question(s) below.Suppose that Merck (MRK) stock is trading for $ per share with billion shares outstanding while Boeing (BA) has million shares outstanding and a market capitalization of $ billion. Assume that you hold the market portfolio.11) Boeing's stock price is closest to:A) $B) $C) $D) $Answer: CExplanation: C) Price BA = = = $Diff: 1Section: The Market PortfolioSkill: Analytical12) Merck's market capitalization is closest to:A) $ billionB) $ billionC) $ billionD) $ billionAnswer: BExplanation: B) Market Cap = Price × shares outstanding = $ × 2,110 = $77,437 millionDiff: 1Section: The Market PortfolioSkill: Analytical13) If you hold 1,000 shares of Merck, then the number of shares of Boeing that you hold is closest to:A) 240 sharesB) 330 sharesC) 510 sharesD) 780 sharesAnswer: BExplanation: B) Shares BA== = sharesDiff: 3Section: The Market PortfolioSkill: Analytical14) Which of the following statements is FALSEA) All investors should demand the same efficient portfolio of securities in the same proportions.B) The Capital Asset Pricing Model (CAPM) allows corporate executives to identify the efficient portfolio (of risky assets) by using knowledge of the expected return of each security.C) If investors hold the efficient portfolio, then the cost of capital for any investment project is equal to its required return calculated using its beta with the efficient portfolio.D) The CAPM identifies the market portfolio as the efficient portfolio. Answer: BDiff: 1Section: The Market PortfolioSkill: Conceptual15) Which of the following statements is FALSEA) If investors have homogeneous expectations, then each investor will identify the same portfolio as having the highest Sharpe ratio in the economy.B) Homogeneous expectations are when all investors have the same estimates concerning future investments and returns.C) There are many investors in the world, and each must have identical estimates of the volatilities, correlations, and expected returns of the available securities.D) The combined portfolio of risky securities of all investors must equal the efficient portfolio.Answer: CDiff: 1Section: The Market PortfolioSkill: Conceptual16) Which of the following statements is FALSEA) If some security were not part of the efficient portfolio, then every investor would want to own it, and demand for this security would increase causing its expected return to fall until it is no longer an attractive investment.B) The efficient portfolio, the portfolio that all investors should hold, must be the same portfolio as the market portfolio of all risky securities.C) Because every security is owned by someone, the sum of all investors' portfolios must equal the portfolio of all risky securities available in the market.D) If all investors demand the efficient portfolio, and since the supply of securities is the market portfolio, then two portfolios must coincide. Answer: ADiff: 2Section: The Market PortfolioSkill: Conceptual17) Which of the following statements is FALSEA) The market portfolio contains more of the smallest stocks and less of the larger stocks.B) For the market portfolio, the investment in each security is proportional to its market capitalization.C) Because the market portfolio is defined as the total supply of securities, the proportions should correspond exactly to the proportion of the total market that each security represents.D) Market capitalization is the total market value of the outstanding shares of a firm.Answer: ADiff: 1Section: The Market PortfolioSkill: Conceptual18) Which of the following statements is FALSEA) A value-weighted portfolio is an equal-ownership portfolio: We hold an equal fraction of the total number of shares outstanding of each security in the portfolio.B) When buying a value-weighted portfolio, we end up purchasing the same percentage of shares of each firm.C) To maintain a value-weighted portfolio, we do not need to trade securities and rebalance the portfolio unless the number of shares outstanding of some security changes.D) In a value weighted portfolio the fraction of money invested in any security corresponds to its share of the total number of shares outstanding of all securitiesin the portfolio.Answer: DDiff: 1Section: The Market PortfolioSkill: Conceptual19) Which of the following statements is FALSEA) The most familiar stock index in the United States is the Dow Jones Industrial Average (DJIA).B) A portfolio in which each security is held in proportion to its market capitalization is called a price-weighted portfolio.C) The Dow Jones Industrial Average (DJIA) consists of a portfolio of 30 large industrial stocks.D) The Dow Jones Industrial Average (DJIA) is a price-weighted portfolio. Answer: BExplanation: B) A portfolio in which each security is held in proportion to its market capitalization is called a value-weighted portfolio.Diff: 2Section: The Market PortfolioSkill: Conceptual20) Which of the following statements is FALSEA) Because very little trading is required to maintain it, an equal-weighted portfolio is called a passive portfolio.B) If the number of shares in a value weighted portfolio does not change, but only the prices change, the portfolio will remain value weighted.C) The CAPM says that individual investors should hold the market portfolio, a value-weighted portfolio of all risky securities in the market.D) A price weighted portfolio holds an equal number of shares of each stock, independent of their size.Answer: AExplanation: A) Because very little trading is required to maintain it, a value-weighted portfolio is called a passive portfolio.Diff: 3Section: The Market PortfolioSkill: Conceptual21) Which of the following statements is FALSEA) A market index reports the value of a particular portfolio of securities.B) The S&P 500 is the standard portfolio used to represent "the market" when using the CAPM in practice.C) Even though the S&P 500 includes only 500 of the more than 7,000 individual . Stocks in existence, it represents more than 70% of the . stock market in terms of market capitalization.D) The S&P 500 is an equal-weighted portfolio of 500 of the largest . stocks. Answer: DExplanation: D) The S&P 500 is a value-weighted portfolio of 500 of the largest .stocks.Diff: 2Section: The Market PortfolioSkill: Conceptual22) Which of the following statements is FALSEA) The S&P 500 and the Wilshire 5000 indexes are both well-diversified indexes that roughly correspond to the market of . stocks.B) Practitioners commonly use the S&P 500 as the market portfolio in the CAPM with the belief that this index is the market portfolio.C) Standard & Poor's Depository Receipts (SPDR, nicknamed "spider") trade on the American Stock Exchange and represent ownership in the S&P 500.D) The S&P 500 was the first widely publicized value weighted index and it has become a benchmark for professional investors.Answer: BDiff: 2Section: The Market PortfolioSkill: Conceptual23) In practice which market index is most widely used as a proxy for the market portfolio in the CAPMA) Dow Jones Industrial AverageB) Wilshire 5000C) S&P 500D) . Treasury BillAnswer: CDiff: 1Section: The Market PortfolioSkill: Conceptual24) In practice which market index would best be used as a proxy for the market portfolio in the CAPMA) S&P 500B) Dow Jones Industrial AverageC) . Treasury BillD) Wilshire 5000Answer: DDiff: 1Section: The Market PortfolioSkill: ConceptualUse the table for the question(s) below.Consider the following stock price and shares outstanding data:25) The market capitalization for Wal-Mart is closest to:A) $415 BillionB) $276 BillionC) $479 BillionD) $200 BillionAnswer: DExplanation: D)Diff: 1Section: The Market Portfolio Skill: Analytical26) The total market capitalization for all four stocks is closest to:A) $479 BillionB) $415 BillionC) $2,100 BillionD) $200 BillionAnswer: BExplanation: B)Section: The Market PortfolioSkill: Analytical27) If you are interested in creating a value-weighted portfolio of these four stocks, then the percentage amount that you would invest in Lowes is closest to:A) 25%B) 11%C) %D) 12%Answer: BExplanation: B)Section: The Market Portfolio Skill: Analyticalvalue-weighted portfolio of these four stocks. The number of shares of Wal-Mart that you would hold in your portfolio is closest to: A) 710 B) 1390 C) 1000 D) 870 Answer: C Explanation: C)Stock Name Price per Share SharesOutstanding (Billions)MarketCapitalization (Billions)Percent of Total Number ofSharesLowes $ $ % 368 Wal-Mart $ $ % 1,002 Intel $ $ % 1,387 Boeing $ $ %190Total$Number of shares =Diff: 2Section: The Market Portfolio Skill: Analyticalvalue-weighted portfolio of these four stocks. The percentage of the shares outstanding of Boeing that you would hold in your portfolio is closest to: A) .000018% B) .000020% C) .000024% D) .000031% Answer: C Explanation: C)Stock Name Price per Share SharesOutstanding (Billions)MarketCapitalization (Billions)Percent of Total Number ofSharesLowes $ $ % 368 Wal-Mart $ $ % 1,002 Intel $ $ % 1,387 Boeing $ $ %190Total$Number of shares =percentage shares outstanding = 190/0 = .000024% Diff: 2Section: The Market Portfolio Skill: Analytical30) Assume that you have $250,000 to invest and you are interested in creating a value-weighted portfolio of these four stocks. How many shares of each of the fourstocks will you hold What percentage of the shares outstanding of each stock will you holdAnswer:Stock Name Price perShareSharesOutstanding(Billions)MarketCapitalization(Billions)Percentof TotalNumber ofSharesLowes$ $ %368Wal-Mart$ $ %1,002Intel$ $ %1,387Boeing$ $ %190Total$% of Shares%Number of shares =In a value weighted portfolio, the percentage of shares of every stock will be the same.Diff: 3Section: The Market PortfolioSkill: AnalyticalBeta EstimationUse the following information to answer the question(s) below.Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyatt OilExcessReturn Beta2007%%%%% 2008%%%.40%% 2009%%%%%1) Wyatt Oil's average historical return is closest to:A) %B) %C) %D) %Answer: AExplanation: A) r average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyatt OilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%Section: Beta EstimationSkill: Analytical2) The Market's average historical return is closest to:A) %B) %C) %D) %Answer: BExplanation: B) r average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%Section: Beta EstimationSkill: Analytical3) Wyatt Oil's average historical excess return is closest to:A) %B) %C) %D) %Answer: CExplanation: C) excess return average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%Section: Beta EstimationSkill: Analytical4) The Market's average historical excess return is closest to:A) %B) %C) %D) %Answer: DExplanation: D) excess return average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%Section: Beta EstimationSkill: Analytical5) Wyatt Oil's excess return for 2009 is closest to:A) %B) %C) %D) %Answer: AExplanation: A) excess return e = (r WO - r rf)2009Section: Beta Estimation Skill: Analytical6) The Market's excess return for 2008 is closest to:A) %B) %C) %D) %Answer: AExplanation: A) excess return e = (r WO - r rf)2009Section: Beta EstimationSkill: Analytical7) Using the average historical excess returns for both Wyatt Oil and the Market portfolio, your estimate of Wyatt Oil's Beta is closest to:A)B)C)D)Answer: BExplanation: B) excess return average = excess return average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%βWO= = = .8375Diff: 3Section: Beta EstimationSkill: Analytical8) Using the average historical excess returns for both Wyatt Oil and the Market portfolio estimate of Wyatt Oil's Beta. When using this beta, the alpha for Wyatt oil in 2007 is closest to:A) %B) %C) %D) +%Answer: CExplanation: C) excess return average =excess return average =Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%βWO = = = .8375α = actual return - expected return for CAPM = % - [3% + .8375(6% - 3%)] = %Diff: 3Section: Beta EstimationSkill: Analytical9) Using just the return data for 2009, your estimate of Wyatt Oil's Beta is closest to:A)B)C)D)Answer: BExplanation: B)Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%%2008%%%%%2009%%%%% Average%%%%%βWO = = = .8651Diff: 2Section: Beta EstimationSkill: Analytical10) Using just the return data for 2008, your estimate of Wyatt Oil's Beta is closest to:A)B)C)D)Answer: A Explanation: A)Year Risk-freeReturnMarketReturnWyatt OilReturnMarketExcessReturnWyattOilExcessReturn2007%%%%% 2008%%%%% 2009%%%%% Average%%%%%βWO = - = .8525Diff: 2Section: Beta EstimationSkill: Analytical11) Which of the following statements is FALSEA) Beta is the expected percent change in the excess return of the security for a 1% change in the excess return of the market portfolio.B) Beta represents the amount by which risks that affect the overall market are amplified for a given stock or investment.C) It is common practice to estimate beta based on the historical correlation and volatilities.D) Beta measures the diversifiable risk of a security, as opposed to its market risk, and is the appropriate measure of the risk of a security for an investor holding the market portfolio.Answer: DExplanation: D) Beta measures the nondiversifiable risk of a security.Diff: 1Section: Beta EstimationSkill: Conceptual12) Which of the following statements is FALSEA) One difficulty when trying to estimate beta for a security is that beta depends on the correlation and volatilities of the security's and market's returns in the future.B) It is common practice to estimate beta based on the expectations of future correlations and volatilities.C) One difficulty when trying to estimate beta for a security is that beta depends on investors expectations of the correlation and volatilities of the security's and market's returns.D) Securities that tend to move less than the market have betas below 1.Answer: BExplanation: B) Beta is measured using past information.Diff: 1Section: Beta EstimationSkill: Conceptual13) Which of the following statements is FALSEA) Securities that tend to move more than the market have betas higher than 0.B) Securities whose returns tend to move in tandem with the market on average have a beta of 1.C) Beta corresponds to the slope of the best fitting line in the plot of the securities excess returns versus the market excess return.D) The statistical technique that identifies the bets-fitting line through a set of points is called linear regression.Answer: ADiff: 2Section: Beta EstimationSkill: ConceptualUse the equation for the question(s) below.Consider the following linear regression model:(R i - r f) = a i + b i(R Mkt - r f) + e i14) The b i in the regressionA) measures the sensitivity of the security to market risk.B) measures the historical performance of the security relative to the expected return predicted by the SML.C) measures the deviation from the best fitting line and is zero on average.D) measures the diversifiable risk in returns.Answer: ADiff: 2Section: Beta EstimationSkill: Conceptual15) The a i in the regressionA) measures the sensitivity of the security to market risk.B) measures the deviation from the best fitting line and is zero on average.C) measures the diversifiable risk in returns.D) measures the historical performance of the security relative to the expected return predicted by the SML.Answer: DDiff: 2Section: Beta EstimationSkill: Conceptual16) The e i in the regressionA) measures the market risk in returns.B) measures the deviation from the best fitting line and is zero on average.C) measures the sensitivity of the security to market risk.D) measures the historical performance of the security relative to the expected return predicted by the SML.Answer: BDiff: 2Section: Beta EstimationSkill: ConceptualThe Debt Cost of CapitalUse the following information to answer the question(s) below.Consider the following information regarding corporate bonds:1) Wyatt Oil has a bond issue outstanding with seven years to maturity, a yield to maturity of %, and a BBB rating. The corresponding risk-free rate is 3% and the market risk premium is 5%. Assuming a normal economy, the expected return on Wyatt Oil's debt is closest to:A) %B) %C) %D) %Answer: BExplanation: B) r d = r rf + β(r m - r rf) = 3% + (5%) = %Diff: 1Section: The Debt Cost of CapitalSkill: Analytical2) Wyatt Oil has a bond issue outstanding with seven years to maturity, a yield to maturity of %, and a BBB rating. The bondholders' expected loss rate in the event of default is 70%. Assuming a normal economy the expected return on Wyatt Oil'sdebt is closest to:A) %B) %C) %D) %Answer: DExplanation: D) r d = ytm - prob(default) × loss rate = 7% - %(70%) = % Diff: 2Section: The Debt Cost of CapitalSkill: Analytical3) Wyatt Oil has a bond issue outstanding with seven years to maturity, a yield to maturity of %, and a BBB rating. The bondholders' expected loss rate in the event of default is 70%. Assuming the economy is in recession, then the expected return on Wyatt Oil's debt is closest to:A) %B) %C) %D) %Answer: BExplanation: B) r d = ytm - prob(default) × loss rate = 7% - %(70%) = %Diff: 2Section: The Debt Cost of CapitalSkill: Analytical4) Rearden Metal has a bond issue outstanding with ten years to maturity, a yield to maturity of %, and a B rating. The corresponding risk-free rate is 3% and the market risk premium is 6%. Assuming a normal economy, the expected return on Rearden Metal's debt is closest to:A) %B) %C) %D) %Answer: CExplanation: C) r d = r rf + β(r m - r rf) = 3% + (6%) = %Diff: 1Section: The Debt Cost of Capital。

(大纲版)2012高三生物一轮复习同步辅导课后练习第12课时光合作用(2021年整理)

(大纲版)2012高三生物一轮复习同步辅导课后练习第12课时光合作用(word 版可编辑修改)编辑整理:尊敬的读者朋友们:这里是精品文档编辑中心,本文档内容是由我和我的同事精心编辑整理后发布的,发布之前我们对文中内容进行仔细校对,但是难免会有疏漏的地方,但是任然希望((大纲版)2012高三生物一轮复习同步辅导课后练习第12课时光合作用(word版可编辑修改))的内容能够给您的工作和学习带来便利。

同时也真诚的希望收到您的建议和反馈,这将是我们进步的源泉,前进的动力。

本文可编辑可修改,如果觉得对您有帮助请收藏以便随时查阅,最后祝您生活愉快业绩进步,以下为(大纲版)2012高三生物一轮复习同步辅导课后练习第12课时光合作用(word版可编辑修改)的全部内容。

课时作业(十二)一、选择题(共13小题,每小题5分,共65分)1.(2010·成都)在下列有关光合作用的叙述中,不正确的是()A.水的分解发生在叶绿体片层结构的薄膜上B.光反应和暗反应中都有许多酶参与C.温度降到0℃,仍有植物能进行光合作用D.NADP+在暗反应中起还原作用,并将能量转移到糖类分子中答案D解析叶绿体片层结构薄膜上分布着光反应所需要的各种光合色素和酶,是光反应的场所;整个光合作用过程包括光反应和暗反应都需要多种酶参与催化;由于长期自然选择,使生物具有多样性和各种适应性特征,某些植物在温度降到0℃时,仍能进行光合作用;NADPH在暗反应中起还原作用,共将能量转移到糖类分子中。

2.(2010·合肥)下列作用中哪些属于光合作用的光反应( )A.2、4、5 B.2、3、6C.1、3、6 D.4、5、6答案B解析在光合作用光反应阶段中,在光的照射下,具有吸收和传递光能作用的色素,将吸收的光能传递给少数处于特殊状态的叶绿素a,使这些叶绿素a被激发而失去电子。

脱离叶绿素a的电子,经过一系列的传递,最后传递给一种带正电荷的有机物——NADP+,再结合一个H +后使之转变为NADPH。

初中英语_Unit 12 练习课教学课件设计

二、根据汉语意思完成句子。 (5×5分=25分) 26.我们昨天去海滩了。 We _w__e_n_t __t_o__ _th_e____b_ea_c_h_e_s_ yesterday. 27.你上周六干什么了? __W__h_a_t_ _di_d __ you __d_o _ last Saturday? 28.他们上周末去湖边野营了。 They ___w_e_n_t _c_a_m__p_in_g_ __b_y___ __t_h_e__ __l_a_k_e_ last weekend. 29.我们星期天下午去动物园了。 We went to the zoo __o_n___ _S_u_n_d_a_y___ __a_f_te_r_n_o_o_n. 30.这个周末咱们去公园划船吧! Let's ___g_o___ b_o_a_t_in_g____ in the park this weekend. 三、用所给词的适当形式填空。(5×5分=25分) 6.Li Hui's family __m__o_v_e_d (move) to Shanghai ten years ago. 7.She got a ___s_u_r_p_ri_s_e_ (surprised) when she saw the snake. 8.Mom ____w_o_k_e__ (wake) me up at six this morning. 9.Betty was so ____sc_a_r_e_d__ (scare) that she couldn't move. 10.This was a very _____u_se_f_u_l (use) lesson for her.

牛津深圳九年级英语chapter12教案与练习

九年级第十二课短语归纳weather forecast department have a haircutdress tidily in a department store begin the hunt local Career Advice Centre as well asnext step search the Internetapply for a job a letter of applicationas a result be invited to an interviewbe pleased note the thingsat all costs possible interview questiongive an example (of) make a good first impressionwork experience preferred be well preparedthe post of secretary receive no replysearch…for…be calm and confidentcomplete the conversation in reply topart-time/full-time sales assistant get good marksmain interests work as a cashierbe close to be hard-workingat any time after-school activitiesprotect the environment give a reasen foroffer good prospects study abroadfeel happy for on dutybelow standard ought tohave a bad effect on one’s offer of help/advicesimilar to student adviserwork independently ask for advicecontinue one’s study stay onthe job advertisement in turnbased on walk confidently into the interview roomweather forecast department 气象预报局have a haircut 理发dress tidily 打扮整齐in a department store 在百货公司begin the hunt 开始收寻local Career Advice Centre 当地求职咨询中心as well as 也,和next step 下一步search the Internet 网上查询apply for a job 申请工作a letter of application 求职信as a result 结果be invited to an interview 被邀请参加面试be pleased 高兴note the things 记下东西at all costs 不惜任何代价,无论如何possible interview question 可能的面试问题give an example (of) 举一个….例子make a good first impression留下良好的第一印象work experience preferred有工作经验者优先be well prepared 准备充分the post of secretary 秘书的职位receive no reply 没收到答复search…for…搜查be calm and confident 冷静自信complete the conversation 完成对话in reply to 作为对…..的答复part-time/full-time sales assistantget good marks 取得好分数兼职的,全职的销售助理main interests 主要的兴趣work as a cashier 从事收银员工作be close to 离……很近be hard-working 工作努力at any time 在任何时候after-school activities 课外活动protect the environment 保护环境give a reasen for 给出……的理由offer good prospects 提供好的发展前景study abroad在国外学习feel happy for 为….感到高兴on duty 值班below standard 不合格ought to 应该have a bad effect on 对……有不好的影响make request 提出要求one’s offer of help/advice 某人提出的帮助、建议similar to 与……相似student adviser 学生的指导老师work independently 独立工作ask for advice 征求建议continue one’s study 继续学习stay on 记下待在the job advertisement 招聘广告in turn 依次,轮流based on 依据,以……为基础walk confidently into the interview room自信地走进面试室状语从句1 时间状语从句:在一个句子中作时间状语的句子。

深圳牛津英语九年级chapter12基础知识复习讲与练.docx

9ABC12基础知识复习讲与练一.例题解析仮U 1 • ___________________________________ We should give love to the children lost their parents in the earthquake.A.who B・ whom C・ Ihose D. which【解析】答案:A本题考查定语从句。

Children为先行词,其后为定语从句;先行词指人, 排除C和D ;关系代词在定语从句中作主语,排除B.例2. …When ________ again? …When he _______ , Fll let you know.A. he comes, will come B・ will he come, will comeC. he comes, comesD. will he come, comes【解析】答案:D本题考查简单句和状语从句。

问句为简单句,动作尚未发生,用一般将来时;答语为复合句,when引导的为时间状语从句,用一般现在时代替一般将来时。

例3. Milk quickly turns sour _________________ i t^s in a fridge.A. untilB. sinceC. asD. unless【解析】答案:D本题考查状语从句连词用法。

分析全句,从句表示条件,意为“如果不放进冰箱……”,unless表示条件,意为“如果不”。

仮|] 4. We must go to work on time every day _______ Sunday・A. besideB. besidesC. exceptingD. except【解析】答案:D 本题主要考查besides和except的区别用法。

Besides意为“除......... 之外包括本身”。

Except意为“除之外不包括本身”。

而本题中Sunday没包括在上班屮。

教学PPT Chapter 12

However, the unjustified hostility that Chinese investors face in some countries, especially those debtladen rich nations, show the international community is not yet ready to accept China's new role as a global investor.

按照国际金融公司的权威定义只要一个国家或地区的人均国民生产总值gnp没有达到世界银行划定的高收入国家水平一般的标准是人均9000多美元那么这个国家或地区的股市就是新兴市场

Business English Reading Courseware Book One

Chapter 12

Abstracts from Articles on Investment

• 26. devolution n. (责任,权利等的)转移; 授权代理; (中央对地方)权利下放 • 27. reiterate v. 重申;反复讲 • 28. outsource n. 外包

单元注释

1. Foreign direct investment (FDI)

境外直接投资,是现代的资本国际化的主要 形式之一。按照国际货币基金组织的定义 FDI是指:在投资人以外的国家所经营的 企业拥有持续利益的一种投资,其目的在 于对该企业的经营管理具有发言权。跨国 公司是主要形式。

While China's ODI rose to $56.5 billion in 2009, Chinese companies had invested only about $900 million of that amount in the world's largest economy. That would not look so abnormal had investment-led growth not been badly needed to help lift the US economy out of its worst recession since the 1930s.

九年级英语人教版全一册_Unit12_名师教材解读

Unit12 名师教材解读1.0T extbook Analysis教材解读1.1本单元以“难以预料的事情(Unexpected Events)”为话题,谈论过去发生的事件。

Section A在内容上侧重讲述发生过的意想不到的事情,涉及了解到过去完成时描述过去某一时间或动作之前已经发生或完成了的动作,以及运用一般过去时态描述过去某个时间里发生的动作或存在的状态。

在语法方面,要求学生掌握“had + 过去分词形式”的结构来表示过去完成时态,构建对于由by the time + 从句作为时间状语后的过去完成时态的语言表达。

在情感态度方面,教师借助本部分内容的学习,帮助学生能够用适当的时态叙述过去发生的事情,特别是意想不到的事情。

Section B在话题上,从学生的生活琐事、意外事故过渡到生活当中的出其不意的玩笑,特别是愚人节发生的让人难以预料的事情。

在语言上,进一步丰富与学习相关的话题词汇。

在技能上,将听说能力综合,突出阅读训练,由读促写。

在教学策略上,要引导学生关注过去完成时态的结构,并且能判断和正确使用过去完成时态描述过去发生的事情。

在情感上,多鼓励学生敢于和坦然面对描述和表达自己的或有趣或窘迫或有意义的人生经历,同时引导和告诉学生在遇到地震或者火灾的时候如何进行自救和逃生。

1.2S ection A 1a 活动1a是Lead-in部分。

旨在通过Free talk导入新的语言现象,谈论出其不意的事情。

教师可以鼓励学生积极思考提出更多的同类型短语。

这样可以有效为1c的口语小对话做好铺垫。

1.3S ection A 1b-1c 活动1b-1c是Listening and speaking部分。

引导学生观察1b 的三个句子,找出未学过的过去完成时语法结构“had + 过去分词形式”,然后两人一组讨论什么时候要用过去完成时态和相关的句型结构。

教师可以抽问学生过去完成时态的名称和基本结构,帮助学生建立对过去完成时态的初步的印象。

《金融学(第二版)》讲义大纲及课后习题答案详解十二章

《⾦融学(第⼆版)》讲义⼤纲及课后习题答案详解⼗⼆章CHAPTER 12CHOOSING AN INVESTMENT PORTFOLIOObjectivesTo understand the process of personal investing in theory and in practice.To build a quantitative model of the tradeoff between risk and reward.Outline12.1 The Process of Personal Portfolio Selection12.2 The Trade-off between Expected Return and Risk12.3 Efficient Diversification with Many Risky AssetsSummaryThere is no single portfolio selection strategy that is best for all people.Stage in the life cycle is an imp ortant determinant of the optimal composition of a person’s optimal portfolio of assets and liabilities.Time horizons are important in portfolio selection. We distinguish among three time horizons: the planning horizon, the decision horizon, and the trading horizon.In making portfolio selection decisions, people can in general achieve a higher expected rate of return only by exposing themselves to greater risk.One can sometimes reduce risk without lowering expected return by diversifying more completely either withina given asset class or across asset classes.The power of diversification to reduce the riskiness of an investor’s portfolio depends on the correlations among the assets that make up the portfolio. In practice, the vast majority of assets are positively correlated with each other because they are all affected by common economic factors. Consequently, one’s ability to reduce risk through diversification among risky assets without lowering expected return is limited.Although in principle people have thousands of assets to choose from, in practice they make their choices from a menu of a few final products offered by financial intermediaries such as bank accounts, stock and bond mutual funds, and real estate. In designing and producing the menu of assets to offer to their customers theseintermediaries make use of the latest advances in financial technology.Solutions to Problems at End of Chapter1. Suppose that your 58-year-old father works for the Ruffy Stuffed Toy Company and has contributed regularly to his company-matched savings plan for the past 15 years. Ruffy contributes $0.50 for every $1.00 your father puts into the savings plan, up to the first 6% of his salary. Participants in the savings plan can allocate their contributions among four different investment choices: a fixed-income bond fund, a “blend” option that invests in large companies, small companies, and the fixed-income bond fund, a growth-income mutual fund whose investments do not include other toy companies, and a fund whose sole investment is stock in the Ruffy Stuffed Toy Company. Over Thanksgiving vacation, Dad realizes that you have been majoring in finance and decides to reap some early returns on that tuition money he’s been investing in your education. He shows you the most recent quarterly statement for his savings plan, and you see that 98% of its current value is in the fourth investment option, that of the Ruffy Company stock..a.Assume that your Dad is a typical risk-averse person who is considering retirement in five years. Whenyou ask him why he has made the allocation in this way, he responds that the company stock has continually performed quite well, except for a few declines that were caused by problems in a division that the company has long since sold off. Inaddition, he says, many of his friends at work have done the same. What advice would you give your dad about adjustments to his plan allocations? Why?b.If you consider the fact that your dad works for Ruffy in addition to his 98% allocation to the Ruffy stockfund, does this make his situation more risky, less risky, or does it make no difference? Why? SOLUTION:a.Dad has exposed himself to risk by concentrating almost all of his plan money in the Ruffy Stock fund. This is analogous to taking 100% of the money a family has put aside for investment and investing it in a single stock.First, Dad needs to be shown that just because the company stock has continually performed quite well is no guarantee that it will do so indefinitely. The company may have sold off the divisions which produced price declines in the past, but future problems are unpredictable, and so is the movement of the stock price. “Past performance is no guarantee of future results” is the lesson.Second, Dad needs to hear about diversification. He needs to be counseled that he can reduce his risk by allocating his money among several of the options available to him. Indeed, he can reduce his risk considerably merely by moving all of his money into the “blend” fund because it is diversifi ed by design: it has a fixed-income component, a large companies component, and a small companies component. Diversification isachieved not only via the three differing objectives of these components, but also via the numerous stocks that comprise each of the three components.Finally, Dad’s age and his retirement plans need to be considered. People nearing retirement age typically begin to shift the value of their portfolios into safer investments. “Safer” normally connotes less variability, so that the risk of a large decline in the value of a portfolio is reduced. This decline could come at any time, and it would be very unfortunate if it were to happen the day before Dad retires. In this example, the safest option would be the fixed-income bond fund because of its diversified composition and interest-bearing design, but there is still risk exposure to inflation and the level of interest rates. Note that the tax-deferred nature of the savings plan encourages allocation to something that produces interest or dividends. As it stands now, Dad is very exposed to a large decline in the value of his savings plan because it is dependent on the value of one stock.Individual equities over time have proven to produce the most variable of returns, so Dad should definitely move some, probably at least half, of his money out of the Ruffy stock fund. In fact, a good recommendation given his retirement horizon of five years would be to re-align the portfolio so that it has 50% in the fixed- income fund and the remaining 50% split between the Ruffy stock fund (since Dad insists) and the “blend” fund.Or, maybe 40% fixed-income, 25% Ruffy, 15% growth-income fund, and 20% “blend” fund. This latterallocation has the advantage of introducing another income-producing component that can be shielded by the tax-deferred status of the plan.b.The fact that Dad is employed by the Ruffy Company makes his situation more risky. Let’s say that the companyhits a period of slowed business activities. If the stock price declines, so will th e value of Dad’s savings plan. If the company encounters enough trouble, it may consider layoffs. Dad’s job may be in jeopardy. At the same time that his savings plan may be declining in value, Dad may also need to look for a job or go onunemployment. Thus, Dad is exposed on two fronts to the same risk. He has invested both his human capital and his wealth almost exclusively in one company.2. Refer to Table 12.1.a.Perform the calculations to verify that the expected returns of each of the portfolios (F, G, H, J, S) in thetable (column 4) are correct.b.Do the same for the standard deviations in column 5 of the table.c.Assume that you have $1million to invest. Allocate the money as indicated in the table for each of the fiveportfolios and calculate the expected dollar return of each of the portfolios.d.Which of the portfolios would someone who is extremely risk tolerant be most likely to select? SOLUTION:d.An extremely risk tolerant person would select portfolio S, which has the largest standard deviation but also thelargest expected return.3. A mutual fund company offers a safe money market fund whose current rate is4.50% (.045). The same company also offers an equity fund with an aggressive growth objective which historically has exhibited an expected return of 20% (.20) and a standard deviation of .25.a.Derive the equation for the risk-reward trade-off line.b.How much extra expected return would be available to an investor for each unit of extra risk that shebears?c.What allocation should be placed in the money market fund if an investor desires an expected return of15% (.15)?SOLUTION:a.E[r] = .045 + .62b.0.62c.32.3% [.15 = w*(.045) + (1-w)*(.020) ]4. If the risk-reward trade-off line for a riskless asset and a risky asset results in a negative slope, what does that imply about the risky asset vis-a-vis the riskless asset?SOLUTION:A trade-off line wit h a negative slope indicates that the investor is “rewarded” with less expected return for taking on additional risk via allocation to the risky asset.5. Suppose that you have the opportunity to buy stock in AT&T and Microsoft.a.stocks is 0? .5? 1? -1? What do you notice about the change in the allocations between AT&T andMicrosoft as their correlation moves from -1 to 0? to .5? to +1? Why might this be?b.What is the variance of each of the minimum-variance portfolios in part a?c.What is the optimal combination of these two securities in a portfolio for each value of the correlation,assuming the existence of a money market fund that currently pays 4.5% (.045)? Do you notice any relation between these weights and the weights for the minimum variance portfolios?d.What is the variance of each of the optimal portfolios?e.What is the expected return of each of the optimal portfolios?f.Derive the risk-reward trade-off line for the optimal portfolio when the correlation is .5. How much extraexpected return can you anticipate if you take on an extra unit of risk?SOLUTION:a.Minimum risk portfolios if correlation is:-1: 62.5% AT&T, 37.5% Microsoft0: 73.5% AT&T, 26.5% Microsoft.5: 92.1% AT&T, 7.9% Microsoft1: 250% AT&T, short sell 150% MicrosoftAs the correlation moves from -1 to +1, the allocation to AT&T increases. When two stocks have negativec orrelation, standard deviation can be reduced dramatically by mixing them in a portfolio. It is to the investors’benefit to weight more heavily the stock with the higher expected return since this will produce a high portfolio expected return while the standard deviation of the portfolio is decreased. This is why the highest allocation to Microsoft is observed for a correlation of -1, and the allocation to Microsoft decreases as the correlationbecomes positive and moves to +1. With correlation of +1, the returns of the two stocks will move closely together, so you want to weight most heavily the stock with the lower individual standard deviation.b. Variances of each of the minimum variance portfolios:62.5% AT&T, 37.5% Microsoft Var = 073.5% AT&T, 26.5% Microsoft Var = .016592.1% AT&T, 7.9% Microsoft Var = .0222250% AT&T, short 150% Microsoft Var = 0c. Optimal portfolios if correlation is:-1: 62.5% AT&T, 37.5% Microsoft0: 48.1% AT&T, 51.9% Microsoft.5: 11.4% AT&T, 88.6% Microsoft1: 250% AT&T, short 150% Microsoftd. Variances of the optimal portfolios:62.5% AT&T, 37.5% Microsoft Var = 048.1% AT&T, 51.9% Microsoft Var = .022011.4% AT&T, 88.6% Microsoft Var = .0531250% AT&T, short 150% Microsoft Var = 0e. Expected returns of the optimal portfolios:62.5% AT&T, 37.5% Microsoft E[r] = 14.13%48.1% AT&T, 51.9% Microsoft E[r] = 15.71%11.4% AT&T, 88.6% Microsoft E[r] = 19.75%250% AT&T, short 150% Microsoft E[r] = -6.5%f.Risk-reward trade-off line for optimal portfolio with correlation = .5:E[r] = .045 + .66/doc/31dbf23b580216fc700afd59.html ing the optimal portfolio of AT&T and Microsoft stock when the correlation of their price movements is 0.5, along with the results in part f of question 12-5, determine:a.the expected return and standard deviation of a portfolio which invests 100% in a money market fundreturning a current rate of 4.5%. Where is this point on the risk-reward trade-off line?b.the expected return and standard deviation of a portfolio which invests 90% in the money market fundand 10% in the portfolio of AT&T and Microsoft stock.c.the expected return and standard deviation of a portfolio which invests 25% in the money market fundand 75% in the portfolio of AT&T and Microsoft stock.d.the expected return and standard deviation of a portfolio which invests 0% in the money market fundand 100% in the portfolio of AT&T and Microsoft stock. What point is this?SOLUTION:a.E[r] = 4.5%, standard deviation = 0. This point is the intercept of the y (expected return) axis by the risk-rewardtrade-off line.b.E[r] = 6.03%, standard deviation = .0231c.E[r] = 15.9%, standard deviation = .173d.E[r] = 19.75%, standard deviation = .2306. This point is the tangency between the risk-reward line from 12-5part f and the risky asset risk-reward curve (frontier) for AT&T and Microsoft.7. Again using the optimal portfolio of AT&T and Microsoft stock when the correlation of their price movements is 0.5, take $ 10,000 and determine the allocations among the riskless asset, AT&T stock, and Microsoft stock for:a. a portfolio which invests 75% in a money market fund and 25% in the portfolio of AT&T and Microsoftstock. What is this portfolio’s expected return?b. a portfolio which invests 25% in a money market fund and 75% in the portfolio of AT&T and Microsoftstock. What is this portfolio’s expect ed return?c. a portfolio which invests nothing in a money market fund and 100% in the portfolio of AT&T andMicrosoft stock. What is this portfolio’s expected return?SOLUTION:a.$7,500 in the money-market fund, $285 in AT&T (11.4% of $2500), $2215 in Microsoft. E[r] = 8.31%, $831.b.$2,500 in the money-market fund, $855 in AT&T (11.4% of $7500), $6645 in Microsoft. E[r] = 15.94%, $1,594.c.$1140 in AT&T, $8860 in Microsoft. E[r] = 19.75%, $1,975.8. What strategy is implied by moving further out to the right on a risk-reward trade-off line beyond the tangency point between the line and the risky asset risk-reward curve? What type of an investor would be most likely to embark on this strategy? Why?SOLUTION:This strategy calls for borrowing additional funds and investing them in the optimal portfolio of AT&T and Microsoft stock. A risk-tolerant, aggressive investor would embark on this strategy. This person would be assuming the risk of the stock portfolio with no risk-free component; the money at risk is not onl y from this person’s own wealth but also represents a sum that isowed to some creditor (such as a margin account extended by the investor’s broker).9. Determine the correlation between price movements of stock A and B using the forecasts of their rate of return and the assessments of the possible states of the world in the following table. The standard deviations for stock A and stock B are0.065 and 0.1392, respectively. Before doing the calculation, form an expectation of whether that correlation will be closer to1 or -1 by merely inspecting the numbers.SOLUTION:Expectation: correlation will be closer to +1.E[r A] = .05*(-.02) + .15*(-.01) + .60*(.15) + .20*(.15) = .1175, or, 11.75%E[r B] = .05*(-.20) + .15*(-.10) + .60*(.15) + .20*(.30) = .1250, or, 12.50%Covariance = .05*(-.02-.1175)*(-.20-.125) + .15*(-.01-.1175)*(-.10-.125) +.60*(.15-.1175)*(.15-.125) + .20*(.15-.1175)*(.30-.125) =.008163Correlation = .008163/(.065)*(.1392) = .90210.Analyze the “expert’s” answers to the following questions:a.Question:I have approx. 1/3 of my investments in stocks, and the rest in a money market. What do you suggestas a somewhat “safer” place to invest another 1/3? I like to keep 1/3 accessible for emergencies.Expert’s answer:Well, you could try 1 or 2 year Treasury bonds. You’d get a little bit more yie ld with no risk.b.Question:Where would you invest if you were to start today?Expert’s answer:That depends on your age and short-term goals. If you are very young – say under 40 –and don’tneed the money you’re investing for a home or college tuition or such, you would put it in a stockfund. Even if the market tanks, you have time to recoup. And, so far, nothing has beaten stocks overa period of 10 years or more. But if you are going to need money fairly soon, for a home or for yourretirement, you need to play it safer.SOLUTION:a.You are not getting a little bit more yield with no risk. The real value of the bond payoff is subject to inflationrisk. In addition, if you ever need to sell the Treasury bonds before expiration, you are subject to the fluctuation of selling price caused by interest risk.b.The expert is right in pointing out that your investment decision depends on your age and short-term goals. In addition, the investment decision also depends on other characteristics of the investor, such as the special character of the labor income (whether it is highly correlated with the stock market or not), and risk tolerance.Also, the fact that over any period of 10 years or more the stock beats everything else cannot be used to predict the future.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

-8

-4

I单

0

1

I

单缝衍射 轮廓线

0

4

a sin k

2

(a b)sin k

8

12-1 在双缝干涉实验中,两缝的间距为 0.6mm,照亮狭缝S 的光杠杆汞弧灯加上绿 色滤光片,在2.5m远处的屏幕上出现干涉条 纹,测得相邻两明条纹中心的距离为2.27 mm。试计算入射光的波长。

=5.19×10-4 (mm) =590 (nm)

结束 返回

12-10 一柱面平凹透镜A,曲率半径为R放

在平玻璃片B上,如图所示。现用波长为 的单色

平行光自上方垂直往下照射,观察A和B间空气薄

膜的反射光的干涉条纹,如空气膜的最大厚度d

=2 ,

(1)分析干涉条纹的特点(形状、分布、级次高

低),作图表示明条纹;

(3)若将玻璃片B向下平移,条纹将向外移动

结束 返回

12-13 迈克耳孙干涉仪可用来测量单 色光的波长,当M2移动距离d=0.3220mm 时,测得某单色光的干涉条纹移过N=1204 条,试求该单色光的波长。

结束 返回

解:

2d =N

N

= 2d

=

0.32×2×10-3 1024

=534.8

(nm)

=6.25×10-4 (mm)

=625 (nm)

结束 返回

12-16 在复色光照射下的单缝衍射图样 中,其中某一波长的第3级明纹位置恰与波

长 =600nm的单色光的第2级明纹位置重

合,求这光波的波长。

结束 返回

解:

(2k+1)

2

= (2k0+1)20

7 2

=

50 2

=428.6(nm)

结束 返回

12-17 用波长1=400nm和2 =700 nm的混合光垂直照射单缝,在衍射图样中, 1 的第 k1级明纹中心位置恰与2的第k2级 暗纹中心位置重合。求k1和k2 。试问 1 的 暗纹中心位置能否与 k2 的暗纹中心位置重 合?

结束 返回

解:(1)由题意

(2k1+1)

1

结束 返回

解:

j =1.22

d

=Δfx

Δx

=1.22

d

f

=1.22

×

632.8×10-9×3.84×108 2×10-3

=1.48×105 (m)

d =2Δx =2.96×105 (m)

激光束经扩束后 d´=2m

2Δx ´= 2×1.22 × 632.82×10-9×3.84×108

=2.96 (m)

sinj

=

k (a+b)

=

Nk d

=

600×5.893×10-5 2.0

k

=50.1768k

在 -900 < j < 900 间,

对应的光强极大的角位置列表如下:

k 0 ±1

±2

±3

±4

±5

sinj 0 ±0.1786 ±0.3536 ±0.5304 ±0.7072 ±0.8840

j 00 ±10011’ ±20042’ ±3202’ ± 450 ± 6208’

一、杨氏双缝实验

k

( k 0, 1, 2, )

r2

r1

(2k

1)

2

( k 0,

1,

2, )

x

D d

kD

d

( 2k 1)

D

2d

( k 0,

1,

2, )

亮纹 暗纹

二、等厚干涉条纹

2d

n

2 2

n12sin

2i

第二级明纹的宽度为

Δx

´=

Δx 2

=2.73 (mm)

结束 返回

12-15 一单色平行光束垂直照射在宽 为 1.0mm 的单缝上,在缝后放一焦距为 20m的会其透镜,已知位于透镜焦面处的 屏幕上的中央明条纹宽度为2.5mm。求入 射光波长。

结束 返回

解:

=

aΔx 2D

=

1.0×2.5 2×2.0×103

(2)求明条纹距中心线的距离;

(3)共能看到多少条明条纹;

(4)若将玻璃片B向下

A

d

平移,条纹如何移动?

若玻璃片移动了 /4,

B

问这时还能看到几条明条纹?

结束 返回

解:对于边缘处e =0由于有半波损失为暗纹

暗纹条件:

2e

+

2

=

(2k+1) 2

k=0,1,2,...

暗纹最高级数

k=

2e

=

2× 2

结束 返回

解:

j

=1.22

d

j

=Δlx

=

1.22

d

l

=1.d2Δ2x

=

5×10-3×1.2 1.22×550×10-9

=8.94×103 (m)

结束 返回

12-19 已知天空中两极星相对于一望远 镜的角距离为 4.84×10-6 rad,由它们发出 的光波波长 =550nm,望远镜物镜的口径 至少要多大,才能分辨出这两颗星?

结束 返回

解:由杨氏双缝干涉条件

Δx

=

D d

=

dΔx D

=

0.60×2.27 2500

=5.45×10-4 (mm) =5450 (Å)

结束 返回

12-2 在双缝干涉实验装置中,屏幕到 双缝的距高D 远大于双缝之间的距离d,对 于钠黄光( = 589.3nm),产生的干涉条纹, 相邻两明纹的角距离(即相邻两明纹对双缝处 的张角)为0.200 。

=

2k-1 R 2

r2 k+5

2(k+5)-1 =2

R

=

2k2+9R

r2 k+5

r

2 k

=5

R

=

r r 2

2

k+5 k

5R

= (rk+5

r k )(rk+5+ r k) 5R

= (dk+5

d k)(dk+5 + 4 ×5R

dk

)

(4.60+3.00)(4.60-3.00)

=

4×5×1030

第十二章 光学

§12-1 光源 单色光 相干光 §12-2 双缝干涉 §12-3 光程与光程差 §12-4 薄膜干涉

§12-6 光的衍射现象 惠更斯–菲涅耳原理 §12-7 单缝的夫琅禾费衍射 §12-8 圆孔的夫琅禾费衍射 光学仪器的分辨本领 §12-9 光栅衍射

§12-11 自然光和偏振光 §12-12 起偏和检偏 马吕斯定律 §12-13 反射和折射时光的偏振

2

=

k22

(2k1

1)400 2

k2 700

4k1 2 7k2

k1 3 k2 2

(2) a sin =k11 a sin =k22 k11 =k22

k1 k2

=

2 1

=

700 400

=

7 4

即1的第7级暗纹与2的第4级暗纹相重结合束 返回

12-18 在迎面驶来的汽车上,两盏前灯 相距1.2m。试问汽车离人多远的地方,眼 睛才可能分辨这两盏前灯?假设夜间人眼瞳 孔直径为5.0mm,而入射光波长 =550.0nm。

结束 返回

解:

j

=1.22

d

=Δfx

=1.22×

5.55×10-5 0.5×10-3

=13.9

(cm)

结束 返回

19-20 已 知 地 球 到 月球的距离是 3.84×108m ,设 来自月球的光的波长为 600nm,若在地球上用物镜直径为 l m的 一天文望远镜观察时,刚好将月球正面一 环形山上的两点分辨开,则该两点的距离 为多少?

=684.2×10-4 (nm)

(2) 放入水中后

2

=

n

sinj

=

sinj0

n

=

sin0.20

1.33

j =0.150

结束 返回

12-3 用很薄的云母片(n=1.58)覆盖在 双缝实验中的一条缝上,这时屏幕上的零级 明条纹移到原来的第七级明条纹的位置上, 如果入射光波长为 =550 nm。 试问此云 母片的厚度为多少?

结束 返回

12-22 一光栅,宽为2.0cm,共有

6000条缝。如用钠光(589.3nm)垂直入射,

中央明纹的位置? 共有几级?如钠光与光

栅的法线方向成300角入射。中央明纹的位

置? 共有几级?

(a b)sin k

L

P

o

f

a b 2 mm 1 105 m

600

3

sin 1 k 5

=

4×1.33×380 2×3-1

=404 (nm)紫

k=4 远紫外

所以水膜呈现紫红色 返回

12-9 使用单色光来观察牛顿环,测得 某一明环的直径为3.00mm,在它外面第五 个明环的直径为4.60mm,所用平凸透镜的 曲率半径为1.03m,求此单色光的波长。

结束 返回

解:第k级明环半径

r

2 k

结束 返回

解:

j

=1.22

d

=Δfx

Δx

=1.22

d

f

=1.22×

600×10-9 1

×3.84×108

=281 (m)