ACCA_F7_2007年06月试题

【国际注册会计师ACCA】F7 2008-2014历年真题-f7int_2011_dec_a

Fundamentals Level – Skills Module, Paper F7 (INT)Financial Reporting (International)December 2011 Answers 1Consolidated statement of financial position of Paladin as at 30 September 2011$’000$’000 AssetsNon-current assets:Property, plant and equipment (40,000 + 31,000 + 4,000 –1,000)74,000Intangible assets (w (i))–goodwill15,000–other intangibles (7,500 + 3,000 –500)10,000Investment in associate (w (ii))7,700––––––––106,700 Current assetsInventory (11,200 + 8,400 –600 URP (w (iii)))19,000T rade receivables (7,400 + 5,300 –1,300 intra-group (w (iii)))11,400Bank3,40033,800–––––––––––––––T otal assets140,500––––––––Equity and liabilitiesEquity attributable to owners of the parentEquity shares of $1 each 50,000Retained earnings (w (iv))35,200––––––––85,200 Non-controlling interest (w (vi))7,900––––––––T otal equity93,100Non-current liabilitiesDeferred tax (15,000 + 8,000)23,000Current liabilitiesBank overdraft2,500Deferred consideration 5,400T rade payables (11,600 + 6,200 –1,300 intra-group (w (iii))) 16,50024,400–––––––––––––––T otal equity and liabilities140,500––––––––Workings (figures in brackets are in $’000)(i)Goodwill in Saracen$’000$’000 Controlling interest (see below)Immediate cash32,000Deferred consideration (5,400 x 100/108)5,000Non-controlling interest (10,000 x 20% (see below) x $3·50)7,000–––––––44,000 Equity shares10,000Pre-acquisition reserves:At 1 October 2010 12,000Fair value adjustments– plant4,000–intangible3,000(29,000)––––––––––––––Goodwill arising on acquisition15,000–––––––The cost of the majority shareholding in Saracen was $32 million. Paladin acquired eight million shares and Saracen has10 million $1 shares, this gives a controlling interest of 80% and a non-controlling interest of 20%.The customer relationship asset is recognised as an intangible asset in the consolidated financial statements under IFRS 3 Business combinations.(ii)Carrying amount of Augusta at 30 September 2011$’000 Cash consideration10,000Share of post-acquisition profits (1,200 x 8/12 x 25%)200Impairment loss (2,500)––––––7,700––––––(iii)Unrealised profit (URP) in inventory/intra-group current accountsThe URP in Saracen’s inventory (supplied by Paladin) of $2·6 million is $600,000 (2,600 x 30/130). The current account balances of Paladin and Saracen should be eliminated from trade receivables and payables at the agreed amount of $1·3 million.(iv)Consolidated retained earnings:$’000 Paladin’s retained earnings (25,700 + 9,200)34,900Saracen’s post-acquisition profits (4,500 (w (v)) x 80%) 3,600Augusta’s post-acquisition profits (w (ii))200Augusta’s impairment loss(2,500)URP in inventory (w (iii))(600)Finance cost of deferred consideration (5,000 x 8%)(400)–––––––35,200–––––––(v)Post-acquisition adjusted profit of Saracen is:$’000 Profit as reported6,000Additional depreciation of plant (4,000/4 years)(1,000)Additional amortisation of customer relationship asset (3,000/6 years)(500)––––––4,500––––––(vi)Non-controlling interest$’000 Fair value on acquisition (w (i))7,000Post-acquisition profits (4,500 (w (v)) x 20%)900––––––7,900––––––2(a)Keystone – Statement of comprehensive income for the year ended 30 September 2011$’000$’000 Revenue (380,000 – 2,400 (w (i)))377,600Cost of sales (w (ii))(258,100)––––––––Gross profit119,500Distribution costs (14,200)Administrative expenses (46,400 – 24,000 dividend (50,000 x 5 x 2·40 x 4%))(22,400)Investment income800Loss on fair value of investments (18,000 – 17,400)(600)Finance costs (350)––––––––Profit before tax82,750Income tax expense (24,300 + 1,800 (w (v)))(26,100)––––––––Profit for the year56,650Other comprehensive incomeRevaluation of leased property8,000T ransfer to deferred tax (w (v))(2,400)5,600––––––––––––––T otal comprehensive income for the year 62,250––––––––(b)Keystone – Statement of financial position as at 30 September 2011$’000$’000 AssetsNon-current assetsProperty, plant and equipment (w (iv))78,000Financial asset: equity investments17,400––––––––95,400 Current assetsInventory (w (iii))56,600T rade receivables (33,550 – 2,400 (w (i))) 31,15087,750–––––––––––––––T otal assets183,150––––––––Equity and liabilitiesEquityEquity shares of 20 cents each50,000Revaluation reserve (w (iv))5,600Retained earnings (33,600 + 56,650 – 24,000 dividend paid) 66,25071,850–––––––––––––––121,850 Non-current liabilitiesDeferred tax (w (v))6,900Current liabilitiesT rade payables27,800Bank overdraft2,300Current tax payable24,30054,400–––––––––––––––T otal equity and liabilities183,150––––––––Workings (figures in brackets in $’000)(i)Where there is uncertainty over goods sold on a sale or return basis they should not be recognised as revenue until theyhave been formally accepted by the buyer. Thus $2·4 million should be removed from revenue and receivables. The goods should be added to the inventory at 30 September 2011 at their cost of $1·8 million (2·4 million x 75%).(ii)Cost of sales$’000 opening inventory46,700materials (64,000 – 3,000)61,000production labour (124,000 – 4,000)120,000factory overheads (80,000 – (4,000 x 75%))77,000Amortisation of leased property (w (iv))3,000Depreciation of plant (1,000 + 6,000 (w (iv)))7,000Closing inventory (w (iii))(56,600)––––––––258,100––––––––The cost of the self-constructed plant is $10 million (3,000 + 4,000 + 3,000 for materials, labour and overheads respectively that have also been deducted from the above items in cost of sales). It is not permissible to add a profit margin to self-constructed assets.(iii)Inventory at 30 September 2011:$’000 per count54,800goods on sale or return (w (i))1,800–––––––56,600–––––––(iv)Non-current assets:The leased property has been amortised at $2·5 million per annum (50,000/20 years). The accumulated amortisation of $10 million therefore represents four years, thus its remaining life at the date of revaluation is 16 years.$’000 carrying amount at date of revaluation (50,000 – 10,000)40,000revalued amount48,000–––––––gross gain on revaluation 8,000transfer to deferred tax (at 30%)(2,400)–––––––net gain to revaluation reserve5,600–––––––The revalued amount of $48 million will be amortised over its remaining life of 16 years at $3 million per annum.The self-constructed plant will be depreciated for six months by $1 million (10,000 x 20% x 6/12) and have a carryingamount at 30 September 2011 of $9 million. The plant in the trial balance will be depreciated by $6 million ((44,500– 14,500) x 20%) for the year and have a carrying amount at 30 September 2011 of $24 million.In summary:$’000 Leased property (48,000 – 3,000)45,000Plant (9,000 + 24,000)33,000–––––––Property, plant and equipment78,000–––––––(v)Deferred taxProvision required at 30 September 2011 ((15,000 + 8,000) x 30%)6,900Provision at 1 October 2010 (2,700)–––––––Increase required4,200Transferred from revaluation reserve (w (iv))(2,400)–––––––Balance: charge to income statement1,800–––––––3(a)Mocha – Statement of cash flows for the year ended 30 September 2011:(Note: figures in brackets are in $’000)Cash flows from operating activities:$’000$’000Profit before tax3,900Adjustments fordepreciation of non-current assets 2,500profit on the disposal of property, plant and equipment (8,100 – 4,000)(4,100)investment income(1,100)interest expense500increase in inventory (10,200 – 7,200)(3,000)decrease in receivables (3,700 – 3,500)200decrease in payables (4,600 – 3,200)(1,400)decrease in warranty provision (4,000 – 1,600)(2,400)–––––––Cash generated from operations (4,900)Interest paid(500)Income tax paid (w (i))(800)–––––––Net cash deficit from operating activities(6,200)Cash flows from investing activities:Purchase of property, plant and equipment(8,300)Disposal of property, plant and equipment8,100Disposal of investment3,400Dividends received200–––––––Net cash from investing activities3,400Cash flows from financing activities:Shares issued (w (ii))2,400Payment of finance lease obligations (w (iii))(3,900)–––––––Net cash from financing activities(1,500)–––––––Net decrease in cash and cash equivalents (4,300)Cash and cash equivalents at beginning of the year1,400–––––––Cash and cash equivalents at end of the year(2,900)–––––––Workings(i)Income tax paid:$’000Provision b/f–current(1,200)–deferred(900)Income statement tax charge (1,000)Provision c/f–current1,000–deferred1,300––––––Difference – cash paid(800)––––––(ii)Share issues$’000Increase in share capital (14,000 – 8,000)6,000Bonus issue–share premium(2,000)–revaluation reserve (3,600 – 2,000)(1,600)––––––Shares issued for cash at par2,400––––––(iii)Finance leaseBalance b/f–current(2,100)–non-current(6,900)New leases in year(6,700)Balance c/f–current4,800–non-current7,000––––––Principal repaid(3,900)––––––Tutorial note:Reconciliation of investments/investment income$’000InvestmentsBalance b/f7,000Carrying amount sold(3,000)Balance c/f(4,500)––––––Difference: increase in fair value500––––––Carrying amount sold3,000Proceeds(3,400)––––––Profit on sale in income statement400––––––Tutorial note:as the retained earnings at 30 September 2010 (10,100) plus the profit for the period (2,900) equalthe retained earnings at 30 September 2011 (13,000) there was no equity dividend paid.(b)(i)Mocha has reported an operating profit of $3·3 million (12,000 – 8,700) for the year ended 30 September 2011, whichis likely to give a favourable impression to shareholders. However, its cash generated from operations is a deficit of$4·9 million. The reconciling items of these two figures appear in the statement of cash flows and it can be seen thatoperating profit has been boosted by the profit on the sale of a property and a large decrease in the product warrantyprovision. Some commentators argue that a profit on the sale of non-current assets is not really an ‘operating’ profit andit is misleading to be classed as such. Also, many items included in operating profit are subjective (for example theproduct warranty provision), and as such can be subject to manipulation. Cash flows are unaffected by such subjectiveestimates and from this perspective they are considered less susceptible to manipulation and therefore more reliable.(ii)From the statement of financial position it can be seen that net investment in property, plant and equipment (after depreciation) has increased by $8·5 million (32,600 –24,100). This may give the impression that the company isinvesting heavily in property, plant and equipment, and in one sense it is. However, the statement of cash flows showsthat net cash investment in property, plant and equipment is only $200,000 (purchases of 8,300 less disposals of8,100). Most of the difference is due to a (non-cash) acquisition of plant under finance leases (meaning furtherborrowing) and disposal proceeds of plant and equipment in excess of its carrying amounts. The cash flow informationgives a somewhat different (and possibly more realistic) view of the company’s investment in property, plant andequipment during the year.4(a)IAS 37 Provisions, contingent liabilities and contingent assets defines provisions as liabilities of uncertain timing or amount that should be recognised where there is a present obligation (as a result of past events), it is probable (assumed to be more than a 50% chance) that there will be an outflow of economic benefits (to settle the obligation) and the amounts can be estimated reliably. The obligation may be legal or constructive.A contingent liability has more uncertainty in that it is a possible obligation (assumed to be less than a 50% chance) whoseexistence will be confirmed only by one or more future uncertain events that are not wholly within the control of the entity.An existing obligation where the amount cannot be reliably measured is also treated as a contingent liability.The Standard seeks to improve consistency in the reporting of provisions. In the past some entities created ‘general’ (rather than specific) provisions for liabilities that did not really exist (known as ‘big bath’ provisions); equally many entities did not recognise provisions where there was a present obligation. T he latter often related to deferred liabilities such as future environmental costs. T he effect of such inconsistencies was that comparability was weakened and profit was frequently manipulated.(b)(i)Although the information in the question says the environmental provision is not a legal obligation, it implies that it is aconstructive obligation (Borough has created an expectation that it will pay the environmental costs) and therefore thesecosts should be provided for. The obligation for the fixed element of the cost arose as soon as the extraction commenced,whereas the variable element accrues in line with the extraction of oil. The present value of the environmental cost isshown as a non-current liability (credit) with the debit added to the cost of the licence and (effectively) charged to incomeas part of the annual amortisation charge.The relevant extracts from Borough’s statement of financial position as at 30 September 2011 are:$’000Non-current assetLicence for oil extraction (50,000 + 20,000)70,000Amortisation (10 years)(7,000)–––––––Carrying amount63,000–––––––Non-current liabilityEnvironmental provision ((20,000 + (150,000 x 0·02 cents)) x 1·08 finance cost)24,840–––––––(ii)From Borough’s perspective, as a separate entity, the guarantee for Hamlet’s loan is a contingent liability of $10 million.As Hamlet is a separate entity, Borough has no liability for the secured amount of $15 million, not even for the potentialshortfall for the security of $3 million. The $10 million contingent liability would normally be described and disclosedin the notes to Borough’s entity financial statements.In Borough’s consolidated financial statements, the full liability of $25 million would be included in the statement offinancial position as part of the group’s consolidated non-current liabilities – there would be no contingent liabilitydisclosed.The concerns over the potential survival of Hamlet due to the effects of the recession may change the disclosure inBorough’s entity financial statements. If Borough deems it probable that Hamlet is not a going concern the $10 millionloan, which was previously a contingent liability, would become an actual liability and should be provided for onBorough’s entity statement of financial position and disclosed as a current (not a non-current) liability.5(a)(i)The interest rate (5%) for the convertible loan notes is lower because of the potential value of the conversion option.The cost of equivalent loan notes without the option is 8%, the difference is mainly due to the market expectation of thehigher worth of Bertrand’s equity shares (compared to the cash alternative) when the loan notes are due for redemption.From the entity’s viewpoint, the conversion option means lower payments of interest (to help cash flow), but it willeventually cause a dilution of earnings.(ii)If the directors’ treatment were acceptable, the use of the conversion option (compared to issuing non-convertible loans) would improve profit and earnings per share because of lower interest rates (and hence interest charges) and thecompany’s gearing would be lower as the loan notes would not be shown as debt. However, this proposed treatment isnot acceptable. A convertible loan note is a complex (hybrid) financial instrument and IFRS requires that the proceedsof the issue should be allocated between equity (the value of the option) and debt and the finance charge should bebased on that of an equivalent non-convertible loan (8% in this case).(b)Extracts from the financial statements of BertrandIncome statement for the year ended 30 September 2011$’000 Finance costs (9,190 x 8%)735rounded Statement of financial position as at 30 September 2011EquityEquity option810Non-current liabilities8% convertible loan notes ((9,190 x 1·08) – 500)9,425rounded WorkingYear ended Cash flow Discount rate Discounted cash flows30 September $’000at 8%$’00020115000·9346520125000·86430201310,5000·798,295–––––––value of debt component9,190value of equity option component (= balance)810–––––––total proceeds 10,000–––––––Fundamentals Level – Skills Module, Paper F7 (INT)Financial Reporting (International)December 2011 Marking SchemeThis marking scheme is given as a guide in the context of the suggested answers. Scope is given to markers to award marks for alternative approaches to a question, including relevant comment, and where well-reasoned conclusions are provided. This is particularly the case for written answers where there may be more than one acceptable solution.Marks1property, plant and equipment2½goodwill5other intangibles2½investment in associate2inventory1receivables1bank½equity shares½retained earnings 5non-controlling interest 2deferred tax½bank overdraft½deferred consideration1trade payables1Total for question252(a)Income statementrevenue1cost of sales7distribution costs½administrative expenses 1½investment income1loss on fair value of investment1finance costs½income tax expense1½other comprehensive income 115(b)Statement of financial positionproperty, plant and equipment2equity investments½inventory ½trade receivables1equity shares ½revaluation reserve1½retained earnings1½deferred tax1trade payables½bank overdraft½current tax payable½10Total for question25Marks 3(a)profit before tax½depreciation1profit on disposal of property (deducted) 1investment income adjustment (deducted)½interest expense adjustment (added back)½working capital items1½decrease in warranty provisions1½interest paid (cash flow)1income tax paid2purchase of property, plant and equipment 1disposal of property, plant and equipment 1disposal of investment1investment income (dividends received)1share issue2½payment of finance lease obligations2cash b/f½cash c/f½19(b)(i)and (ii)3 marks each 6Total for question254(a)definition of provisions2 definition of contingent liabilities2how the Standard improves comparability26(b)(i)it is a constructive obligation1explanation of treatment1non-current asset (including amortisation) 1½environmental provision (including unwinding of discount)1½(ii)entity financial statements contingent liability of $10 million1 no obligation for secured $15 million 1consolidated statements show full $25 million as a liability1if not a going concern, guarantee would be shown as an actual (current)liability in entity financial statements 19Total for question155(a)(i) 1 mark per valid point 2 (ii) 1 mark per valid point3(b)finance cost2value of equity option1value of debt at 30 September 201125Total for question10。

acca f7课程大纲

acca f7课程大纲【最新版】目录1.ACCA F7 课程简介2.ACCA F7 课程大纲的主要内容3.ACCA F7 课程大纲的学习建议正文1.ACCA F7 课程简介ACCA(Association of Chartered Certified Accountants,特许公认会计师公会)是全球最具影响力的财会职业会员组织,而 F7 课程是其专业资格考试中的一门重要课程,名为“财务报告”。

该课程旨在帮助学员掌握企业财务报告的基本原则、会计处理方法以及相关法规,从而提高学员在财务报告领域的专业能力。

2.ACCA F7 课程大纲的主要内容ACCA F7 课程大纲分为三个部分,分别是:(1)财务报告框架:这部分主要介绍企业财务报告的基本原则、会计处理方法和相关法规。

学员需要了解国际财务报告准则(IFRS)及其在财务报告中的应用。

(2)资产、负债和所有者权益:这部分主要涉及企业的资产、负债和所有者权益的会计处理,包括固定资产、无形资产、存货、应收账款、流动负债、长期负债以及所有者权益等内容。

(3)收入、费用和利润:这部分主要涉及企业的收入、费用和利润的会计处理,包括营业收入、营业成本、销售费用、管理费用、财务费用以及利润分配等内容。

3.ACCA F7 课程大纲的学习建议(1)掌握基本概念:在学习 ACCA F7 课程大纲的过程中,要重视基本概念的掌握,如财务报告框架、会计处理方法等。

(2)注重实践操作:通过大量的练习题和案例分析,将理论知识运用到实际问题中,提高自己在财务报告领域的实际操作能力。

(3)关注最新动态:财务报告领域的法规和准则不断更新,需要关注最新的国际财务报告准则(IFRS),以便在考试中取得好成绩。

总之,ACCA F7 课程大纲涉及的内容较为广泛,需要学员投入足够的时间和精力进行学习和实践。

acca9月F7考试题及答案

acca9月F7考试题及答案ACCA 9月 F7考试题及答案1. 题目一:财务报表分析问题:请解释财务报表分析的目的,并给出两个常用的财务比率。

答案:财务报表分析的目的是评估企业的财务状况、业绩和盈利能力,以便做出明智的投资和信贷决策。

两个常用的财务比率包括:- 流动比率:衡量企业短期偿债能力,计算公式为流动资产除以流动负债。

- 资产负债率:衡量企业财务杠杆水平,计算公式为总负债除以总资产。

2. 题目二:资本成本问题:说明如何计算加权平均资本成本(WACC)。

答案:加权平均资本成本(WACC)的计算公式为:\[WACC = \frac{E}{V} \times Re + \frac{D}{V} \times Rd\times (1 - Tc)\]其中:- \( E \) 代表企业市场价值的股权- \( V \) 代表企业资本的市场价值总和(\( E + D \))- \( Re \) 代表股权要求的回报率- \( D \) 代表企业市场价值的债务- \( Rd \) 代表债务的税后成本- \( Tc \) 代表公司税率3. 题目三:财务风险管理问题:描述两种财务风险管理策略。

答案:财务风险管理策略包括:- 对冲:通过使用衍生金融工具(如期货、期权)来减少价格波动对企业财务状况的影响。

- 多元化:通过投资不同行业和地区的资产来分散风险,减少单一资产或市场对企业整体财务状况的负面影响。

4. 题目四:现金流量表问题:解释现金流量表中的经营活动、投资活动和融资活动。

答案:现金流量表分为三个部分:- 经营活动:涉及企业日常运营产生的现金流入和流出,如销售收入和运营支出。

- 投资活动:涉及企业购买或出售资产、投资等产生的现金流,如购买固定资产或出售投资。

- 融资活动:涉及企业筹资活动产生的现金流,如发行债券、支付股息或偿还债务。

5. 题目五:财务规划和预算问题:描述财务规划和预算过程的步骤。

答案:财务规划和预算过程包括以下步骤:- 目标设定:确定企业的财务目标和战略。

ACCA-F7-知识点总结教学教材

A C C A-F7-知识点总结ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence, little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies, and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular, provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations, not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made, then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognized when it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb, probable means more than 50% likely. If an obligation is probable, it is not a contingent liability – instead, a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the related economic benefits is virtually certain should recognition take place. At that point, the asset is no longer a contingent asset.Disclosure: contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past, provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory, but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade, assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolittle’s pre mises are now empty and surplus to requirements.However, just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord, as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business, closure of business locations, changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common, and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses, locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example, assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.cca f7真题对于acca f7的考试的重要性我相信各位acca考生都心知肚明了,首先我们先看一下acca f7科目的考试内容ACCA F7科目介绍:F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

ACCA考试F7知识点辅导

ACCA考试F7知识点辅导本文由高顿ACCA整理发布,转载请注明出处I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular,provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37,a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognized when it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it is not a contingent liability – instead,a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the related economic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolittle’s premises are now empty and surplus to requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.更多ACCA资讯请关注高顿ACCA官网:。

ACCA考试F6mock答案

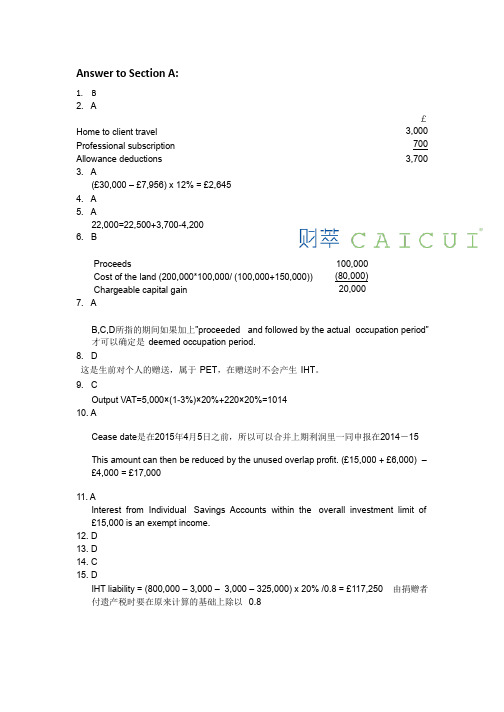

Answer to Section A:1. B2. A£ 3,000 700 Home to client travel Professional subscription Allowance deductions 3,7003. A(£30,000 – £7,956) x 12% = £2,645 4. A5. A22,000=22,500+3,700-4,2006. BProceeds100,000 (80,000) 20,000Cost of the land (200,000*100,000/ (100,000+150,000)) Chargeable capital gain 7. AB,C,D 所指的期间如果加上”proceeded and followed by the actual occupation period” 才可以确定是 deemed occupation period.8. D这是生前对个人的赠送,属于 PET ,在赠送时不会产生 IHT 。

9. COutput VAT=5,000×(1-3%)×20%+220×20%=1014 10. ACease date 是在2015年4月5日之前,所以可以合并上期利润里一同申报在2014-15 This amount can then be reduced by the unused overlap profit. (£15,000 + £6,000) – £4,000 = £17,00011. AInterest from Individual Savings Accounts within the overall investment limit of £15,000 is an exempt income. 12. D 13. D 14. C 15. DIHT liability = (800,000 – 3,000 – 3,000 – 325,000) x 20% /0.8 = £117,250 付遗产税时要在原来计算的基础上除以 0.8由捐赠者Answer to Section B1. Flick Pick (TX 06/12 Q1)Answer: all figures are in one pound, unless indicated otherwise (a)Other income (Total income)Trading profit (W2)(W3)(W4) Employment income (W1) Property income (W5) Total (net) income8,220 34,388 5,940 48,548 -10,000 38,548Less: Personal allowance (W6) Taxable incomeWorking 1 Employment income Salary 25,665 Benefit:-accommodation benefit (W1.1) -furniture benefit 9,400*0.2 Total6,843 1,880 34,388 Working 1.1 accommodation benefit basic rate: annual value4,600 2,243 6,843additional charge: (144,000-75,000)*3.25% taxable benefit:Working 2 tax -adjusted trading profitYear ended 30 April 2015=29,700- 300 (W2.1) =29,400 Working 2.1 capital allowanceprivate -used carsBusiness use %Capital allowanceTWDV B/D addition 0 18,750 18,750 -500 Balance WDA (8%*4/12) Total60%300 30018,250Working 3 Partnership profit allocationFlickArtTotalTotal29,400 (W2)-2,000less: salary to art Remaining 6,000*4/12=2,00016,44027,400 profit sharing10,960-27,400ratio(4:6) Total10,960 18,440 Working 4 sole trader basis tax year Basis periodProfit2014/15from 1/1/2015-6/4/201510,960 (W3)*3/4=8,220Working 5 property income Rental 660*12 7,920 council tax -1,320 -660 W&T allowance Total(7,920-1,320)*10%5,940Working 6 Personal allowances Adjusted net income= 49,065Born on or after 6 April 1948, so the standard PA of 10,000 should be used(b)3D Ltd will be responsible for paying class 1 NIC (both primary and secondary contributions) in respect of Flick’s salary.3D Ltd will be responsible for paying class 1A NIC in respect of Flick’s taxable benefits. Flick will be responsible for paying class 2 NIC in respect of her trading income. Flick will be responsible for paying class 4 NIC in respect of her trading income Tutorials:1.第一个税务年度所对应的 basis period 应该为公司成立日至第一个税务年度日(06/04/20XX) 2. For accommodation benefit, since the property was acquired more than 6 years before being provided to Flick, the market value at the date it was provided to her is used as the cost of providing the benefit, instead of the original cost.3. Cost of replacing furniture 和 wear & tear allowance 只能选其一抵减,本题中 flick 选择 使用 wear & tear allowance.4.对于求 trading income 的综合题,必须按照规定步骤按顺序计算:1.先求 tax -adjusted trading profit. 2. Partnership profit allocation 3. Basis period assessment.2. Neung Ltd (a ) Associates● ● Second Ltd and Fourth Ltd are not associated companies as Neung Ltd has ashareholding of less than 50% in Second Ltd, and Fourth Ltd is dormant. Third Ltd and Fifth Ltd is associated companies as Neung Ltd has ashareholding of over 50% in each case, and both are trading companies.(b ) Neung Ltd – Corporation tax computation for the year ended 31 March 2015£Trading profit(W1) 358,766(25,200 + 12,600) 37,800396,566Interest income Taxable total profitFranked investment income Augmented profits(37,800/90%) 42,000438,566Corporation tax at marginal rate £396,566 at 21% 83,279(139) Marginal relief1/400 * (500,000 – 438,566) x396,566/438,566 Corporation tax liability83,140(W1) Trading profit£622,536 11,830 Operating profit Depreciation Amortisation7,000 Less: Deduction for lease premium (w2) Capital allowances (w3) Trading profit(4,340) (278,260) 358,766(W2) Deduction for lease premium£140,000 (53,200 86,800 4,340Premium paidLess: £140,000*2%*(20-1)) Assessment on landlordAllowable deduction per year(£86,800/20)(W3) Capital allowancesMain poolSpecial rate poolAllowanceTWDV b/f4,80012,700Additional (no AIA ) Motor car (1) Motor car (2) Additional ( with AIA)15,40028,600 Ventilation system Less: AIA 270,000 (270,000) 28,100 270,000Balance 33,400 (6,012) WDA (18%) WDA (8%) 6,012 2,248 (2,248) 25,852TWDV C/F Total allowance27,388278,260 (W4) Corporation tax rateNeung Ltd has two associated companies; therefore there are three associated companies in total. £ 500,000 100,000Upper limit (£1,500,000/3) Lower limit (£ 300,000/3)3. TomOrdinary shares in Kapook plc(W1)Ordinary shares in Jooba Ltd (no gain no loss transfer between spouses) Antique table (W2)13,600- 3,500- UK Government securities (exempt) Chargeable gains 17,100 (6,100) 11,000 (11,000)Less: losses b/f (W3) Net chargeable gainsLess: annual exempt amount Taxable gainsTom therefore has a nil liability to capital gains tax in 2014/15 and capital losses carried forward of £ (15,900 – 6,100) = £9,800.(w1) The shares in Kapook plc are valued at the lower of: (a) 3.70 + ¼ × (3.90 – 3.70) = 3.75; (b) (3.60 + 3.80)/2 = 3.70The disposal is first matched against the purchase on 24 July 2014 (this is within the following 30 days) and then against the shares in the share pool. The cost of the shares disposed of is, therefore, £23,400 (5,800 + 17,600).No. of sharesCost£ £ Purchase 19 February 2004 Purchase 6 June 20098,000 6,00016,200 14,600 30,800 (17,600) 13,20014,000 (8,000) 6,000 Disposal 20 July 2014 £30,800 × 8,000/14,000 Balance c/f£ Deemed proceeds (10,000 × £3.70) Less: cost 37,000 (23,400) 13,600Chargeable gains(w2) The antique table is a non -wasting chattel. £ proceeds 8,700 (5,200) 3,500Less: cost Chargeable gainsThe maximum gain is 5/3 × £(8,700 − 6,000) = £4,500. The chargeable gain is the lower of £3,500 and £4,500, so it is £3,500.(w3)The set off of the brought forward capital losses is restricted to £6,100 (17,100 – 11,000) so that chargeable gains are reduced to the amount of the annual exempt amount.4. IHT£CLT (20/06/2007) 280,000 Less annual exemption - - 2007/08 2006/07 (3,000) (3,000) 274,000IHT liability274,000 x 0% = 0£PET (05/10/2013)255,000 Less annual exemption - - 2013/14 2012/13(3,000) (3,000) 249,000The PET is initially exemption from IHT liability.Death date: 12/03/2015CLT (20/06/2007) was made more than 7 years ago, so there is no additional IHT liability incurred.£PET (05/10/2013)249,0000 422,500 (W1) – 274,000 = 148,500 x 0% 249,000 – 148,500 = 100,500 x 40% IHT liability40,200 40,200Value of death estate£850,000 460,000 275,000 PropertyBuilding society depositsProceeds of life assurance policy Less Funeral cost(18,000) 1,567,000422,500 – 249,000 = 173,500 x 0%1,567,000 – 173,500 = 1,393,500 x 40%557,400557,400IHT liability(W1)Nil rate band for Nicola in tax year 2014/15 is 325,000 + 325,000 x (1 – 70%) = £422,500. 5.(a) (1) Wind can use both schemes because its expected taxable turnover for the next 12month does not exceed £1,350,000 exclusive of VAT; in addition, for both of the schemes the company is up to date with its VAT returns.(2) With the cash accounting scheme, output VAT will be accounted for one monthlater than at present since the scheme will result in the tax point becoming the date that payment is received from customers and the recovery of input VAT will not be affected as these are paid in cash.(3) With the annual accounting scheme, the reduced administration in only having tofile one VAT return each year should have save overtime costs.此处的考点为special scheme,注意三种不同的scheme的使用条件以及各自的优缺点,在回答优缺点时注意结合题目所给具体条件答题(b) (1) from suppliers situated outside EUWind Ltd will have to pay VAT of £8,000 (40,000×20%) to HM Revenue and Customs at the time of importation, and this will be reclaimed as input VAT on the VAT return for the period during which the equipment is imported.(2) From supplier situated within EUVAT will have to be accounted for according to the date of acquisition. This will be the Earlier of date that a VAT invoice is issued or the 15th day of the month following the Month in which the equipment transported to UK.The VAT charged of £8,000 will be declared on Wind Ltd’ VAT return as output VAT, But will then be reclaimed as input VAT on the same VAT return.6.(a) Sophie Shape – Schedule of tax paymentsDue date Tax year Payment £31 July 20152014–15Second payment on account 3,240 6,480 (5,240 + 1,240) x 50%31 January 20162014–15Balancing payment 5,98012,460 (6,100 + 1,480 + 4,880) – 6,480 (3,240 x 2)31 January 20162015–16First payment on account 3,790 7,580 (6,100 + 1,480) x 50%(b) (1) If Sophie’s payments on account for 2014–15 were reduced to nil, then she would be charged intereston the payments due of £3,240 from the relevant due date to the date of payment.(2) A penalty based on the amount of underpaid tax will be charged as the claim to reduce the payments on account to nil would appear to be made fraudulently or negligently.(c) (1) Unless the return is issued late, the latest date when Sophie can file a paperself-assessment tax return for 2014–15 is 31 October 2015.(d) (1) If HM Revenue and Customs (HMRC) intend to carry out a compliance check into Sophie’s 2014-15 tax return they will have to notify her within 12 months of the date when they receive the return.(2) HMRC has the right to carry out a compliance check as regards the completeness and accuracy of any return, and such a check may be made on a completely random basis.(3) However, compliance checks are generally carried out because of a suspicion that income has been undeclared or because deductions have been incorrectly claimed. For example, where accounting ratios are out of line with industry norms.X。

2007会计综合试题和答案

对外经济贸易大学2007年硕士研究生入学考试初试试题考试科目:831会计综合第一部分:英文试题(共70分)1.Give a brief explanation for the following terms(9 points)(1)Useful life;(2)Revenue expenditure;(3)Interest·bearing liability;(4)Conservatism principle;(5)Working capital;(6)Direct write-off method.2.True and false(7 points)For each of the following statements,write the T or the F to indicate whether the statement is True or False.(1)The only business events thin are entered in accounting records are those that can be expressed in monetary terms.(2)The ledger is sometimes called the book of original entry because it is the accounting record where transactions are,first recorded.(3)When the direct write-off method is used to recognize un-collectible accounts expense,an Allowance for Doubtful Accounts is not required.(4)Assets wear out more quickly when they are depreciated by all accelerated method.(5)If capital stock is issued by a corporation at a price higher than par value, the excess amount represents income in the period in which the shares of stocks are issued.(6)When a corporation presents both‘basic’and‘diluted’earnings per share,the basic earnings per share will be the smaller of the two figures.(7)Issuing bonds at a discount increases the actual cost of borrowing above the contact rate of interest printed on the bonds.3.Translate the following statements into Chinese。

ACCA f7 2014 06 官方试卷

P a p e r F 7 ( I N T )ALL FIVE questions are compulsory and MUST be attempted1On 1 October 2013, Penketh acquired 90 million of Sphere’s 150 million $1 equity shares. The acquisition was achieved through a share exchange of one share in Penketh for every three shares in Sphere. At that date the stock market prices of Penketh’s and Sphere’s shares were $4 and $2·50 per share respectively. Additionally, Penketh will pay $1·54 cash on 30 September 2014 for each share acquired. Penketh’s finance cost is 10% per annum.The retained earnings of Sphere brought forward at 1 April 2013 were $120 million.The summarised statements of profit or loss and other comprehensive income for the companies for the year ended31 March 2014 are:Penketh Sphere$’000 $’000 Revenue620,000310,000Cost of sales(400,000)(150,000)––––––––––––––––Gross profit220,000160,000Distribution costs(40,000)(20,000)Administrative expenses(36,000)(25,000)Investment income (note (iii))5,0001,600Finance costs (2,000)(5,600)––––––––––––––––Profit before tax147,000111,000Income tax expense(45,000)(31,000)––––––––––––––––Profit for the year102,00080,000Other comprehensive incomeGain/(loss) on revaluation of land (notes (i) and (ii))(2,200)3,000––––––––––––––––T otal comprehensive income for the year99,80083,000––––––––––––––––The following information is relevant:(i) A fair value exercise conducted on 1 October 2013 concluded that the carrying amounts of Sphere’s net assetswere equal to their fair values with the following exceptions:–the fair value of Sphere’s land was $2 million in excess of its carrying amount–an item of plant had a fair value of $6 million in excess of its carrying amount. The plant had a remaining life of two years at the date of acquisition. Plant depreciation is charged to cost of sales.–Penketh placed a value of $5 million on Sphere’s good trading relationships with its customers. Penketh expected, on average, a customer relationship to last for a further five years. Amortisation of intangible assetsis charged to administrative expenses.(ii)Penketh’s group policy is to revalue land to market value at the end of each accounting period. Prior to its acquisition, Sphere’s land had been valued at historical cost, but it has adopted the group policy since its acquisition. In addition to the fair value increase in Sphere’s land of $2 million (see note (i)), it had increased bya further $1 million since the acquisition.(iii)On 1 October 2013, Penketh also acquired 30% of Ventor’s equity shares. Ventor’s profit after tax for the year ended 31 March 2014 was $10 million and during March 2014 Ventor paid a dividend of $6 million. Penketh uses equity accounting in its consolidated financial statements for its investment in Ventor.Sphere did not pay any dividends in the year ended 31 March 2014.(iv)After the acquisition Penketh sold goods to Sphere for $20 million. Sphere had one fifth of these goods still in inventory at 31 March 2014. In March 2014 Penketh sold goods to Ventor for $15 million, all of which were still in inventory at 31 March 2014. All sales to Sphere and Ventor had a mark-up on cost of 25%.(v)Penketh’s policy is to value the non-controlling interest at the date of acquisition at its fair value. For this purpose, the share price of Sphere at that date (1 October 2013) is representative of the fair value of the shares held by the non-controlling interest.(vi)All items in the above statements of profit or loss and other comprehensive income are deemed to accrue evenly over the year unless otherwise indicated.Required:(a)Calculate the consolidated goodwill as at 1 October 2013.(b)Prepare the consolidated statement of profit or loss and other comprehensive income of Penketh for the yearended 31 March 2014.The following mark allocation is provided as guidance for this question:(a) 6 marks(b)19 marks(25 marks)2The following trial balance relates to Xtol at 31 March 2014:$’000$’000 Revenue (note (i))490,000Cost of sales 290,600Distribution costs 33,500Administrative expenses 36,800Loan note interest and dividends paid (notes (iv) and (v))13,380Bank interest90020-year leased property at cost (note (ii)) 100,000Plant and equipment at cost (note (ii))155,500Accumulated amortisation/depreciation at 1 April 2013:leased property25,000plant and equipment43,500 Inventory at 31 March 2014 61,000T rade receivables 63,000T rade payables32,200Bank5,500Equity shares of 25 cents each (note (iii))56,000Share premium25,000Retained earnings at 1 April 201326,0805% convertible loan note (note (iv))50,000Current tax (note (vi))3,200Deferred tax (note (vi))4,600––––––––––––––––757,880757,880––––––––––––––––The following notes are relevant:(i)Revenue includes an amount of $20 million for cash sales made through Xtol’s retail outlets during the year onbehalf of Francais. Xtol, acting as agent, is entitled to a commission of 10% of the selling price of these goods.By 31 March 2014, Xtol had remitted to Francais $15 million (of the $20 million sales) and recorded this amount in cost of sales.(ii)Plant and equipment is depreciated at 12½% per annum on the reducing balance basis.All amortisation/depreciation of non-current assets is charged to cost of sales.(iii)On 1 August 2013, Xtol made a fully subscribed rights issue of equity share capital based on two new shares at60 cents each for every five shares held. The market price of Xtol’s shares before the issue was $1·02 each. Theissue has been fully recorded in the trial balance figures.(iv)On 1 April 2013, Xtol issued a 5% $50 million convertible loan note at par. Interest is payable annually in arrears on 31 March each year. The loan note is redeemable at par or convertible into equity shares at the option of the loan note holders on 31 March 2016. The interest on an equivalent loan note without the conversion rights would be 8% per annum.The present values of $1 receivable at the end of each year, based on discount rates of 5% and 8%, are:5%8%End of year10·950·9320·910·8630·860·79(v)An equity dividend of 4 cents per share was paid on 30 May 2013 and, after the rights issue, a further dividend of 2 cents per share was paid on 30 November 2013.(vi)The balance on current tax represents the under/over provision of the tax liability for the year ended 31 March 2013. A provision of $28 million is required for current tax for the year ended 31 March 2014 and at this date the deferred tax liability was assessed at $8·3 million.Required:(a)Prepare the statement of profit or loss for Xtol for the year ended 31 March 2014.(b)Prepare the statement of changes in equity for Xtol for the year ended 31 March 2014.(c)Prepare the statement of financial position for Xtol as at 31 March 2014.(d)Calculate the basic earnings per share (EPS) for Xtol for the year ended 31 March 2014.Note: Answers and workings (for parts (a) to (c)) should be presented to the nearest $1,000; notes to the financial statements are not required.The following mark allocation is provided as guidance for this question:(a)8 marks(b) 6 marks(c)8 marks(d) 3 marks(25 marks)3Shown below are the financial statements of Woodbank for its most recent two years:Statements of profit or loss for the year ended 31 March:20142013$’000$’000 Revenue 150,000110,000Cost of sales(117,000)(85,800)––––––––––––––––Gross profit33,00024,200Distribution costs(6,000)(5,000)Administrative expenses(9,000)(9,200)Finance costs –loan note interest(1,750)(500)––––––––––––––––Profit before tax16,2509,500Income tax expense (5,750)(3,000)––––––––––––––––Profit for the year 10,5006,500––––––––––––––––Statements of financial position as at 31 March:20142013$’000$’000 AssetsNon-current assetsProperty, plant and equipment 118,00085,000Goodwill30,000nil––––––––––––––––148,00085,000––––––––––––––––Current assetsInventory 15,50012,000T rade receivables11,0008,000Bank5005,000––––––––––––––––27,00025,000––––––––––––––––T otal assets175,000110,000––––––––––––––––Equity and liabilitiesEquityEquity shares of $1 each 80,00080,000Retained earnings 15,00010,000––––––––––––––––95,00090,000––––––––––––––––Non-current liabilities10% loan notes55,0005,000––––––––––––––––Current liabilitiesT rade payables21,00013,000Current tax payable4,0002,000––––––––––––––––25,00015,000––––––––––––––––T otal equity and liabilities175,000110,000––––––––––––––––The following information is available:(i)On 1 January 2014, Woodbank purchased the trading assets and operations of Shaw for $50 million and, onthe same date, issued additional 10% loan notes to finance the purchase. Shaw was an unincorporated entity and its results (for three months from 1 January 2014 to 31 March 2014) and net assets (including goodwill not subject to any impairment) are included in Woodbank’s financial statements for the year ended 31 March 2014 .There were no other purchases or sales of non-current assets during the year ended 31 March 2014.(ii)Extracts of the results (for three months) of the previously separate business of Shaw, which are included in Woodbank’s statement of profit or loss for the year ended 31 March 2014, are:$’000 Revenue 30,000Cost of sales(21,000)–––––––Gross profit9,000Distribution costs(2,000)Administrative expenses(2,000)(iii)The following six ratios have been correctly calculated for Woodbank for the year ended 31 March 2013: Return on capital employed (ROCE) 10·5%(profit before interest and tax/year-end total assets less current liabilities)Net asset (equal to capital employed) turnover 1·16 timesGross profit margin22·0%Profit before interest and tax margin9·1%Current ratio 1·7:1Gearing (debt/(debt + equity))5·3%Required:(a)Calculate for the year ended 31 March 2014:(i)equivalent ratios (all six) to the above for Woodbank based on its reported figures; and(ii)equivalent ratios to the first FOUR only for Woodbank excluding the effects of the purchase of Shaw.Note: Assume the capital employed for Shaw is equal to its purchase price of $50 million.(10 marks) (b)Assess the comparative financial performance and position of Woodbank for the year ended 31 March 2014.Your answer should refer to the effects of the purchase of Shaw.(15 marks)(25 marks)4(a) A director of Enca, a public listed company, has expressed concerns about the accounting treatment of some of the company’s items of property, plant and equipment which have increased in value. His main concern is that the statement of financial position does not show the true value of assets which have increased in value and that this ‘undervaluation’ is compounded by having to charge depreciation on these assets, which also reduces reported profit. He argues that this does not make economic sense.Required:Respond to the director’s concerns by summarising the principal requirements of IAS 16 Property, Plant and Equipment in relation to the revaluation of property, plant and equipment, including its subsequent treatment.(5 marks)(b)The following details relate to two items of property, plant and equipment (A and B) owned by Delta which aredepreciated on a straight-line basis with no estimated residual value:Item A Item BEstimated useful life at acquisition8 years 6 years$’000$’000Cost on 1 April 2010240,000120,000Accumulated depreciation (two years)(60,000)(40,000)––––––––––––––––Carrying amount at 31 March 2012180,00080,000––––––––––––––––Revaluation on 1 April 2012:Revalued amount160,000112,000Revised estimated remaining useful life 5 years 5 years Subsequent expenditure capitalised on 1 April 2013nil14,400At 31 March 2014 item A was still in use, but item B was sold (on that date) for $70 million.Note:Delta makes an annual transfer from its revaluation surplus to retained earnings in respect of excess depreciation.Required:Prepare extracts from:(i)Delta’s statements of profit or loss for the years ended 31 March 2013 and 2014 in respect of charges(expenses) related to property, plant and equipment;(ii)Delta’s statements of financial position as at 31 March 2013 and 2014 for the carrying amount of property, plant and equipment and the revaluation surplus.The following mark allocation is provided as guidance for this requirement:(i) 5 marks(ii) 5 marks(10 marks)(15 marks)5The following issues have arisen during the preparation of Skeptic’s draft financial statements for the year ended31 March 2014:(i)From 1 April 2013, the directors have decided to reclassify research and amortised development costs asadministrative expenses rather than its previous classification as cost of sales. They believe that the previous treatment unfairly distorted the company’s gross profit margin.(ii)Skeptic has two potential liabilities to assess. The first is an outstanding court case concerning a customer claiming damages for losses due to faulty components supplied by Skeptic. The second is the provision required for product warranty claims against 200,000 units of retail goods supplied with a one-year warranty.The estimated outcomes of the two liabilities are:Court case Product warranty claims10% chance of no damages awarded70% of sales will have no claim65% chance of damages of $4 million 20% of sales will require a $25 repair25% chance of damages of $6 million 10% of sales will require a $120 repair (iii)On 1 April 2013, Skeptic received a government grant of $8 million towards the purchase of new plant with a gross cost of $64 million. The plant has an estimated life of 10 years and is depreciated on a straight-line basis.One of the terms of the grant is that the sale of the plant before 31 March 2017 would trigger a repayment ona sliding scale as follows:Sale in the year ended:Amount of repayment31 March 2014100%31 March 201575%31 March 201650%31 March 201725%Accordingly, the directors propose to credit to the statement of profit or loss $2 million ($8 million x 25%) being the amount of the grant they believe has been earned in the year to 31 March 2014. Skeptic accounts for government grants as a separate item of deferred credit in its statement of financial position. Skeptic has no intention of selling the plant before the end of its economic life.Required:Advise, and quantify where possible, how the above items (i) to (iii) should be treated in Skeptic’s financial statements for the year ended 31 March 2014.The following mark allocation is provided as guidance for this question:(i) 3 marks(ii) 4 marks(iii) 3 marks(10 marks)End of Question Paper。

accaf7知识点总结

accaf7知识点总结ACCA F7(财务报告与分析)考试是ACCA专业资格考试中的一门核心科目,主要涵盖财务报表的制作与分析,财务报表的解读与应用,以及财务报告的合并与调整等内容。

下面将从几个方面对ACCA F7的知识点进行总结。

一、财务报表制作与分析财务报表制作与分析是ACCA F7考试的重点内容,主要包括资产负债表、利润表和现金流量表的制作和分析。

在制作财务报表方面,考生需要掌握会计政策选择、会计估计和会计差错的处理方法,以及对企业合并、重组和业务分割的会计处理等。

在分析财务报表方面,考生需要学会利用比率分析、趋势分析和竞争对手分析等方法,对财务报表进行评估和解读。

二、财务报表的解读与应用财务报表的解读与应用是ACCA F7考试的另一个重要内容,主要包括财务报表的解读、财务报表的分析和财务报表的应用。

在财务报表的解读方面,考生需要学会分析财务报表中的各项指标和数据,了解企业的经营状况和财务状况。

在财务报表的分析方面,考生需要学会利用财务指标和分析方法,对财务报表进行评估和解读。

在财务报表的应用方面,考生需要学会利用财务报表的信息,进行业务决策和财务管理。

三、财务报告的合并与调整财务报告的合并与调整是ACCA F7考试的另一个考点,主要包括子公司合并财务报表的制作和分析,以及关联交易和企业重组的会计处理。

在子公司合并财务报表的制作和分析方面,考生需要学会制作合并财务报表,了解合并财务报表中的关键指标和数据。

在关联交易和企业重组的会计处理方面,考生需要学会处理关联交易和企业重组的会计问题,了解其对财务报表的影响。

ACCA F7考试主要涵盖财务报表制作与分析、财务报表的解读与应用,以及财务报告的合并与调整等内容。

考生需要掌握财务报表的制作和分析方法,学会解读和应用财务报表的信息,了解财务报告的合并和调整的会计处理方法。

只有全面掌握这些知识点,才能在ACCA F7考试中取得好成绩。

希望以上内容对大家有所帮助。

2007年度注册会计师全国统一考试财务成本管理试题及参考答案

销其 所 欠 甲公 司 的相 应 债 务 。

() 5 甲公 司 共 欠 本 公 司职 工 工 资 和 应 当 划入 职 工 个 人 账 户 的 基 本 养 老 保 险 、基 本 医疗 保 险 费用 3 . 79万元 ,其 中 , 在 20 0 6年 8月 2 7日新 的 《 业 破 产 法 》 布 之 前 , 欠 本 公 司 企 公 所 职 工 工 资 和应 当划 入 职 工 个 人 账 户 的 基 本 养 老 保 险 、基 本 医

要求 :

一

、

单 项 选 择 题

1 下 列 预 算 中 , 于 财 务 预 算 的 是 ( ) . 属 。 A. 售 预 算 销 预 算 B 生产 预 算 c. 品成 本 预 算 . 产 D. 本 支 出 资

【 案 】D 答

【 解析】财务预 算是 关于资金 筹措和使用的预算 . 包括 短

疗 保 险费 用 为 2 0万元 。 甲公 司 的 全 部 财产 在清 偿 破 产 费 用 和 共 益 债 务 后 , 剩 余 价 值 15 0万元 的 厂 房 及 土 地 使 用 权 , 仅 0 但 该厂房及土地使用 权已于 20 0 6年 6月 被 甲 公 司 抵 押 给 B 银 行 , 于 担 保 一 笔 20 0万 元 的 借 款 。 用 0

( )0 6 6月 . 公 司 向 A 银 行 借 款 10万 元 , 款 期 2 20 年 丙 2 借

限为 1 。 年 甲公 司 以 所 属部 分设 备 为丙 公 司提 供 抵 押 担 保 , 并

定, 理人依照《 管 企业 破 产 法》 定 解 除合 同的 , 方 当事人 以 规 对

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。