Contents

contents

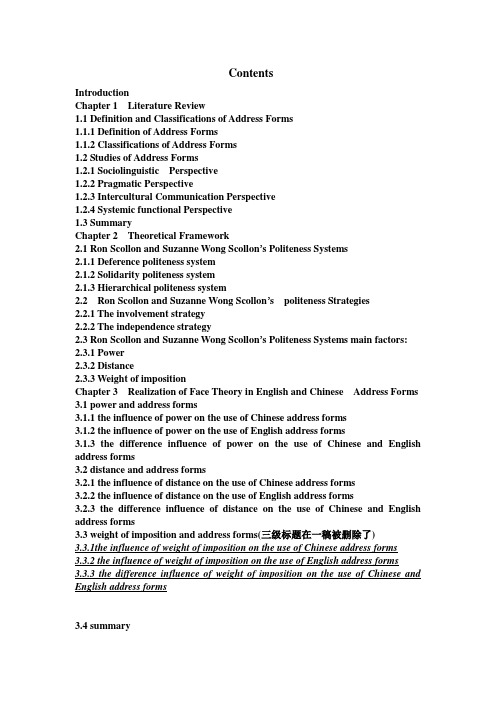

ContentsIntroductionChapter 1 Literature Review1.1 Definition and Classifications of Address Forms1.1.1 Definition of Address Forms1.1.2 Classifications of Address Forms1.2 Studies of Address Forms1.2.1 Sociolinguistic Perspective1.2.2 Pragmatic Perspective1.2.3 Intercultural Communication Perspective1.2.4 Systemic functional Perspective1.3 SummaryChapter 2 Theoretical Framework2.1 Ron Scollon and Suzanne Wong Scollon’s Politeness Systems2.1.1 Deference politeness system2.1.2 Solidarity politeness system2.1.3 Hierarchical politeness system2.2 Ron Scollon and Suzanne Wong Scollon’s politeness Strategies2.2.1 The involvement strategy2.2.2 The independence strategy2.3 Ron Scollon and Suzanne Wong Scollon’s Politeness Systems main factors: 2.3.1 Power2.3.2 Distance2.3.3 Weight of impositionChapter 3 Realization of Face Theory in English and Chinese Address Forms 3.1 power and address forms3.1.1 the influence of power on the use of Chinese address forms3.1.2 the influence of power on the use of English address forms3.1.3 the difference influence of power on the use of Chinese and English address forms3.2 distance and address forms3.2.1 the influence of distance on the use of Chinese address forms3.2.2 the influence of distance on the use of English address forms3.2.3 the difference influence of distance on the use of Chinese and English address forms3.3 weight of imposition and address forms(三级标题在一稿被删除了)3.3.1the influence of weight of imposition on the use of Chinese address forms3.3.2 the influence of weight of imposition on the use of English address forms3.3.3 the difference influence of weight of imposition on the use of Chinese and English address forms3.4 summaryChapter 4 Causes of the Differences in the Influence of Face theory on the use of English and Chinese Address Forms4.1 Effects of different historical and cultural traditions4.1.1 Cultural Roots and Cultural Orientation4.1.2 Patriarchal Clan System and Traditional Ethic4.1.3 Parallel Structure and Hierarchical Structure4.2 Effects of different cultural values4.2.1 Collectivism and Individualism4.2.2 Power and SolidarityChapter 5 Avoiding face conflict strategies in address forms5.1the cultivation of intercultural communicative awareness5.2 avoiding intercultural communication failure in address forms Conclusion。

CONTENTS

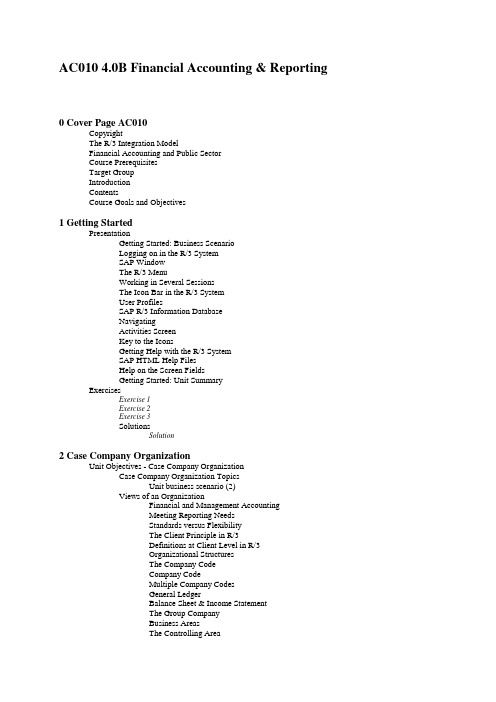

AC010 4.0B Financial Accounting & Reporting 0 Cover Page AC010CopyrightThe R/3 Integration ModelFinancial Accounting and Public SectorCourse PrerequisitesTarget GroupIntroductionContentsCourse Goals and Objectives1 Getting StartedPresentationGetting Started: Business ScenarioLogging on in the R/3 SystemSAP WindowThe R/3 MenuWorking in Several SessionsThe Icon Bar in the R/3 SystemUser ProfilesSAP R/3 Information DatabaseNavigatingActivities ScreenKey to the IconsGetting Help with the R/3 SystemSAP HTML Help FilesHelp on the Screen FieldsGetting Started: Unit SummaryExercisesExercise 1Exercise 2Exercise 3SolutionsSolution2 Case Company OrganizationUnit Objectives - Case Company OrganizationCase Company Organization TopicsUnit business scenario (2)Views of an OrganizationFinancial and Management AccountingMeeting Reporting NeedsStandards versus FlexibilityThe Client Principle in R/3Definitions at Client Level in R/3Organizational StructuresThe Company CodeCompany CodeMultiple Company CodesGeneral LedgerBalance Sheet & Income StatementThe Group CompanyBusiness AreasThe Controlling AreaThe Operating ConcernProfitability SegmentsTwo Additional StructuresCredit CheckingFunctional AreaOrganizational Structures: Summary2-1 Topic: Organizational StructuresOrganizational StructuresExercise 2-1-12-1-2 Organizational Structures in R/3IDES InternationalThe Company Codes of IDESThe Group CompanyOrganizational Element: Business AreasThe Business Areas of IDESControlling AreaOrganizational Element: Controlling AreaThe Operating Concern of IDESIDES: SummaryExercise 2-1-22-2 Topic: Accounting Sub-ModulesAccounting Sub-Modules2-2-1 R/3 Financial Accounting ApplicationsFI: Financial Accounting (1 of 3)FI: Financial Accounting (2 of 3)FI: Financial Accounting (3 of 3)Organizational Structures in Asset AccountingTR: TreasuryOrganizational Structures in TreasuryCO: ControllingEC: Enterprise ControllingIM: Capital Investment ManagementBusiness Transaction EventsBusiness Transaction Events DetailExercise 2-2-1Unit Review - Case Company OrganizationWhat Organizational Structure? (1)Answer: What organizational structure? (1)What Organizational Structure? (2)Answer: What Organizational Structure? (2)What Organizational Structure? (3)Answer: What organizational structure? (3)What Organizational Structure Provides?Answer: What Organizational Structure Provides?Business Area: True or FalseAnswer: Business Area - True or FalseWhat Component for Reporting?Answer: What Component for Reporting?Name Three Organizational Structures?Answer: Name 3 organizational structures?Questions: True or False?Answers: True or False?Case Company Organization: Unit SummarySolution 2-1Solution 2-23 Master DataUnit Objectives - Master DataMaster Data TopicsUnit business scenario (3)Accounting along the Value ChainAccounting Data Within R/3Chart of AccountsAdditional ChartsGeneral Ledger Account GroupsG/L Master Record - Chart of Accts SegmentG/L Master Record - Company Code SegmentCreating a G/L AccountThe Reconciliation Account and SubledgersThe Reconciliation Account in Financial AccountingCustomer Master Record LayoutMaintaining the Cust Master Record CentrallyCustomer Master Data - Account GroupVendor Master RecordMaintaining the Vendor Master Record CentrallyVendor Master Data - Account GroupOpen Item Management3-1 Topic: A/P, A/R & G/L Master RecordsA/P, A/R & G/L Master Records3-1-1 Chart of Accounts in DetailOperating Chart of Accounts DetailCountry/Alternative Chart of Accounts (1)Country/Alternative Chart of Accounts (2)Corporate/Group Chart of Accounts DetailExercise 3-1-13-1-2 Account Groups in DetailG/L Account Groups in Detail (1 of 2)G/L Account Groups in Detail (2 of 2)Customer and Vendor Account Groups (1 of 2)Customer and Vendor Account Groups (2 of 2)Exercise 3-1-23-1-3 The G/L Account Master RecordThe G/L Account Master Record: InformationControl DataG/L Account Master Record - 2 SegmentsG/L Collection of AccountsExercise 3-1-33-1-4 Reconciliation AccountsAdditional Reconciliation Account DetailsExercise 3-1-4Online Help 3-1-5Exercise 3-1-5Exercise 3-1-6More About Master DataReview Creating a Customer AccountBank Master DataHouse Bank Master DataAdd Bank Data to Customer AccountThe Asset Master RecordThe Asset ClassMaster Data used in ControllingCost Elements within R/3Primary Cost ElementsSecondary Cost ElementsThe Cost CenterInternal OrdersThe Profitability SegmentThe Profit CenterThe Grouping of CO Data3-2 Topic: Bank, Asset & Controlling Master RecordsBank, Assets & Controlling Master Records3-2-1 Bank Master Data Details (1)Bank Master Data Details (2)Exercise 3-2-13-2-2 Asset AccountingThe Asset Sub-LedgerAsset Master Data in DetailMore on the Asset ClassExercise 3-2-23-2-3 More About Controlling Master RecordsInternal OrdersInternal Order SettlementProfit Center / Cost CenterProfit Center as Investment CenterCost Center GroupsHierarchiesHierarchies for Internal OrdersExercise 3-2-33-3 Topic: Reporting on Master RecordsReporting on Master Records3-3-1 Organization of ReportsReport VariantsExercise 3-3-2Exercise 3-3-3Exercise 3-3-4Exercise 3-3-5Review Questions - Master Data / COAReview Questions - Master Data / Account GroupsReview Questions - Master Data / Reconciliation A.Review Questions - Master Data / Cost ElementReview Questions - Master Data / ControllingReview Questions - Master Data / AssetsReview Questions - Master Data / BanksMaster Data: Unit SummarySolution 3-1Solution 3-2Solution 3-34 Daily ProcessingUnit Objectives - Daily ProcessingDaily Processing TopicsUnit business scenario (4)Integrated Business ProcessesThe SAP Document PrincipleThe Accounting DocumentDocument TypeDocument TypesDocument Number RangePosting KeysValid Posting PeriodsCreating an A/P InvoiceThe Audit Trail4-1 Topic: Posting MethodsPosting MethodsExercise 4-1-14-1-2 Let’s Post a DocumentPosting a Document - 4 DatesPosting a Document - CurrenciesPosting a Document - Document TypesImportant Standard Document TypesPosting a Document - Posting KeysPosting a Document - AccountPosting a Document - Account Assignment FieldsPosting a Document - PostExercise 4-1-2Exercise 4-1-34-1-4 Changing & Reversing DocumentsReversing DocumentsChanging DocumentsDisplaying Changed DocumentsExercise 4-1-4Posting TipsPosting Using Previously Posted DocumentsG/L Fast EntryThe Account Assignment ModelAdditional AssignmentsMultiple Models Within One DocumentParameter ID’sPark that DocumentParking a DocumentPosting a Parked DocumentParking a document4-2 Topic: Posting TipsPosting TipsExercise 4-2-1Exercise 4-2-2Exercise 4-2-3Review of Techniques used in PostingReference Docs/Sample Docs DiscussionAccount Assignment Model DiscussionG/L Fast Entry Setup DiscussionHold/Set Data, PID DiscussionSpecialized Posting Concepts4-3 Topic: Specialized PostingsSpecialized Posting Concepts4-3-1 Terms of PaymentTerms of Payment - DatesTerms of Payment DefaultTerms For Retainage of PaymentsExercise 4-3-1Online Help 4-3-2Exercise 4-3-24-3-3 Foreign Currency ProcessingExchange Rate TablesExchange Rate TypesForeign Currency Functionality - The EuroExercise 4-3-3Online Help 4-3-4Exercise 4-3-44-3-5 Master Data ChecksValidationsValidation MessageSubstitutionExercise 4-3-54-3-6 Special G/L TransactionsMore about Special G/L EntriesExamples of Special G/L Transactions4-4 Topic: Daily Posting Account AnalysisDaily Posting Account AnalysisExercise 4-4-14-4-2 Document Detail Line AnalysisLine Item Detail AnalysisDocument Header Detail AnalysisSort by Allocation FieldAllocation FieldLine LayoutOnline Help 4-4-2Exercise 4-4-24-4-3 Work ListsWork Lists: continuedExercise 4-4-34-5 Topic: Reporting on Daily Activities (optional)Reporting on Daily Activities (optional)4-5-1 Reports, Reports, ReportsFinancial ReportingReporting Objectives (a)Reporting Objectives (b)Reporting Objectives (c)Reporting Objectives (d)Reporting Objectives (e)Reporting Objectives (f)Basis of ComparisonTypes of ReportsMore Types of ReportsSummaryExercise 4-5-1Exercise 4-5-2Exercise 4-5-3Exercise 4-5-4Exercise 4-5-5Exercise 4-5-6Unit Summary - Daily Processing NeedsUnit Summary - Daily Processing TerminologyUnit Summary - Daily Processing PostingDaily Processing: Unit SummarySolution 4-1Solution 4-2Solution 4-3Solution 4-4Solution 4-55 IntegrationUnit Objectives - IntegrationIntegration TopicsUnit business scenario (5)Management of Resources/ProcessesDocument Flow Within R/3SD Document Flow in the R/3 SystemOrganization in SD - Distribution ChannelsBusiness Process in COM CycleSales Order ProcessingDeliveryBillingCreating InvoicesInterface to AccountingCreating a Sales OrderMaterials Management OverviewThe Procurement ProcessPurchase Order CreationGoods Receipt ProcessingGoods Receipt for Stock MaterialInvoice Verification and PaymentCreating a PO, Receipt & Invoice5-1 Topic: Originating DocumentsOriginating Documents5-1-1 Organizational Structures in LogisticsOrganizational Structures in Sales and DistributionComplete SD FunctionalitySales and DistributionFunctionsDocuments, Documents, DocumentsUpdate A/R & Subsequent SystemsExercise 5-1-15-1-2 Organizational Structures in Materials ManagementExternal Procurement ProcessingEffects of a Goods Receipt PostingInvoice VerificationTypes of Invoice VerificationDocuments, Documents, More DocumentsExercise 5-1-25-2 Topic: Accounting DocumentsAccounting Documents5-2-1 Accounting Document TrackingCost Center Report - An ExampleCost Center Report SelectionReport Analysis - Drill Down (1)Report Analysis - Drill Down (2)Report Analysis - Drill Down (3)Exercise 5-2-15-3 Topic: Additional Reporting (optional)Additional Reporting (optional)5-3-1 Customer Defined Special LedgersSpecial Ledgers for ReportingThe Structure of FI-SLThe Coding Block ExtensionP&L: Period AccountingP&L: Cost-of-Sales AccountingP&L Statement According to the Funct. AreasExercise 5-3-15-3-2 Report Painter / Report WriterThe Report Painter ToolBasic Report StructureAdditional Painter FunctionalityExercise 5-3-25-3-3 Cash Management ReportsCash Position and Liquidity ForecastExercise 5-3-3Integration Topics for DiscussionUnit Summary - IntegrationSolution 5-1Solution 5-2Solution 5-36 Periodic ProcessingUnit Objectives - Periodic ProcessingPeriodic Processing TopicsUnit business scenario (6)Periodic Financial ActivitiesAids for Periodic EntriesAutomatic Payment ProcessingPayment Selection Program FlowAutomatic ReceiptsDunningOverview of the Dunning RunCorrespondenceOverview of CorrespondenceInterest CalculationFinancial Calendar6-1 Topic: The Financial CalendarThe Financial Calendar6-1-1 The Financial CalendarFinancial Calendar DetailExercise 6-1-16-2 Topic: Automatic Payments and ReceiptsAutomatic Payments and Receipts6-2-1 Automatic Payment Processing DetailsPayment MethodsExercise 6-2-16-2-2 Electronic Bank StatementsLockbox Processing (USA)Exercise 6-2-26-2-3 Clearing Open ItemsClearing Document DetailsClearing an AccountOnline Help 6-2-3Exercise 6-2-36-3 Topic: Correspondence and DunningCorrespondence & Dunning6-3-1 SAPscript in the R/3 SystemSAPscript within Financial AccountingExercise 6-3-1Exercise 6-3-26-4 Periodic EntriesPeriodic Entries6-4-1 Recurring EntriesExercise 6-4-16-4-2 Accrual Journal Entries within R/3Accrual Journal Entry ReversalsAccrual Journal Entry HintsExercise 6-4-2Exercise 6-4-3More Periodic Financial ActivitiesPosting PeriodsPeriod ClosingPre-Closing ActivitiesManagerial ClosingFinancial ClosingEnd of Period ReportingYear-end ClosingCompany Consolidation Levels6-5 Topic: ClosingClosing6-5-1 Posting Period ControlPosting Period VariantPosting Period Control ExampleExercise 6-5-16-5-2 FI - CO ReconciliationBalance Sheet ReadjustmentForeign Currency ValuationUS GAAP AccountingGR/IR ReclassExercise 6-5-26-6 Topic: Balance Sheet ReportingBalance Sheet Reporting6-6-1 Balance Sheet and P&L, RFBILA00Balance Sheet Selection CriteriaFinancial Statement VersionsDirectory of Financial Statement VersionsExercise 6-6-16-6-2 G/L Information SystemReports for Financial Statement VersionKey Figure ReportsExercise 6-6-26-6-3 Balance Carry Forward/ Opening Balance SheetProfit & Loss CalculationPosting Period Details - Fiscal YearExercise 6-6-3Discussion on Automatic ProcessingReporting Question for DiscussionUnit Summary - Periodic ProcessingSolution 6-1Solution 6-2Solution 6-3Solution 6-4Solution 6-5Solution 6-67 Project Implementation Tools & Wrap-upUnit Objectives - Project Implementation Tools & Wrap-upProject Implementation Tools & Wrap-up TopicsUnit business scenario (7)Project Implementation ToolsR/3 ConfigurationThe AcceleratedSAP RoadmapWhat is different about AcceleratedSAP?The Business Navigator - a tool7-1 Topic: Project Implementation ToolsR/3 Project Implementation ToolsExercise 7-1 Project ToolsTopic: Self AssessmentExercise 7-2 Self AssessmentTopic: Case StudyExercise 7-3 Case StudyCourse Wrap-upSummaryReview of Course Goals and ObjectivesCurriculum Progression4.0- Curr Paths for FI, AA, SL, FI- Cons & PublicGlossary and Menu PathsGlossaryMenu PathsSolution 7-1Solution 7-2。

contents

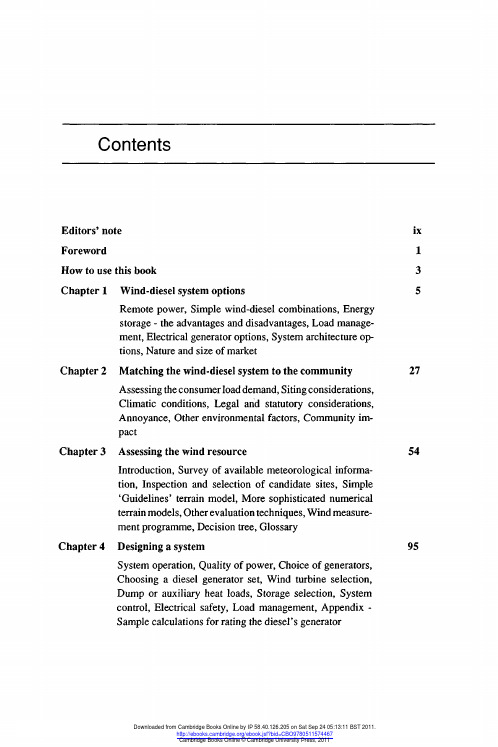

Editors' note Foreword How to use this book Chapter 1 Wind-diesel system options Remote power, Simple wind-diesel combinations, Energy storage - the advantages and disadvantages, Load management, Electrical generator options, System architecture options, Nature and size of msel system to the community Assessing the consumer load demand, Siting considerations, Climatic conditions, Legal and statutory considerations, Annoyance, Other environmental factors, Community impact Chapter 3 Assessing the wind resource Introduction, Survey of available meteorological information, Inspection and selection of candidate sites, Simple 'Guidelines' terrain model, More sophisticated numerical terrain models, Other evaluation techniques, Wind measurement programme, Decision tree, Glossary Chapter 4 Designing a system System operation, Quality of power, Choice of generators, Choosing a diesel generator set, Wind turbine selection, Dump or auxiliary heat loads, Storage selection, System control, Electrical safety, Load management, Appendix Sample calculations for rating the diesel's generator

contents

Research papersS.P . Caro, M.M. Lambrechts, J. Balthazart and P . Perret (Belgium, France)Non-photoperiodic factors and timing of breeding in blue tits: Impact of environmental and social influences in semi-natural conditions 1C.M. Bloom, J. Venard, M. Harden and S. Seetharaman (USA)Non-contingent positive and negative reinforcement schedules of supersitious behaviors8R.M. Colwill (USA)Effect of the passage of time on the contribution of initial response–outcome associations to instrumental performance 14O.Yu. Vekovischeva, E.V . Verbitskaya, T. Aitta-aho, K. Sandnabba and E.R. Korpi (Finland, Russia)Multimetric statistical analysis of behavior in mice selected for high and low levels of isolation-induced male aggression23O. Pineño (Spain)An examination of the effectiveness of inflation and deflation treatments in detecting within-compound learning of a taste aversion 33A. C ˇokl, M. Zorovic ´and J.G. Millar (Slovenia, USA)Vibrational communication along plants by the stink bugs Nezara viridula and Murgantia histrionica 40C.M. Thorpe, D. Hallett and D.M. Wilkie (Canada, UK)The role of spatial and temporal information in learning interval time–place tasks55C. Arzel, M. Guillemain, D.B. Gurd, J. Elmberg, H. Fritz, A. Arnaud, C. Pin and F . Bosca (France, Sweden, Canada)Experimental functional response and inter-individual variation in foraging rate of teal (Anas crecca )66T.W. Belke (Canada)Rats do not respond differently in the presence of stimuli signaling wheel-running reinforcers of different durations 72Short reportL.K.M. Wright and M.G. Paule (USA)Response sequence difficulty in an incremental repeated acquisition (learning) procedure81S. HirataA note on the responses of chimpanzees (Pan troglodytes ) to live self-images on television monitors 85Special IssueProceedings of the Meeting of the Society for the Quantitative Analyses of Behavior (SQAB 2006)May 26–27, 2006, Atlanta, GA, USA Guest Editors Randolph C. Grace Alliston K. ReidPrefaceR.C. Grace and A.K. Reid (New Zealand, USA)SQAB 2006: “It’s the Non-Arbitrary Metrics, Stupid!”91Research reportsJ.J. McDowell and M.L. Caron (USA)Undermatching is an emergent property of selection by consequences 97E. Fantino, S. Gaitan, A. Kennelly and S. Stolarz-Fantino (USA)How reinforcer type affects choice in economic games 107A.H. Doughty, S.P . da Silva and K.A. Lattal (USA)Differential resurgence and response elimination115G.R. Foxall (UK)Explaining consumer choice: Coming to terms with intentionality 129C.P . Shimp (USA)Quantitative behavior analysis and human values146Contents of volume 75Behavioural Processes 75 (2007) e5–e6doi:10.1016/S0376-6357(07)00168-4e6Contents of volume 75olume 75 doi:10.1016/S0376-6357(07)00166-0olume 75 doi:10.1016/S0376-6357(07)00167-2olume 75 doi:10.1016/S0376-6357(07)00168-4Additional material available online.。

Contents

Contents1.Introduction ----------------------------------------------------- 32.International Trade Terms---------------------------------------- 42.1 Three sets of rules----------------------------------------- 42.2 Defines 6 terms:-------------------------------------------- 42.3 International Rules for the Interpretation of Trade Terms 2000(Incoterms 2000)------------------------------------------------ 5 3.terms into four categories-------------------------------------- 63.1 Intercoms 2000---------------------------------------------- 63.2 Brief of Incoterms------------------------------------------ 83.2.1The “E” term (EXW)------------------------------------ 83.2.2 The “F” terms (FCA, FAS, FOB)------------------------ 83.2.3 The “C” terms (CFR, CIF, CPT, CIP)----------------- 93.2.4 The “D” terms (DAF, DES, DEQ, DDU, DDP)----------- 114.Three of the most popular in international trade of trade terms144.1 FOB-------------------------------------------------------- 144.2 CIF-------------------------------------------------------- 154.3 CFR-------------------------------------------------------- 165.Three Common Used Trade Terms---------------------------------- 185.1 FCA-------------------------------------------------------- 185.2 CPT-------------------------------------------------------- 195.3 CIP-------------------------------------------------------- 19 Conclusion -------------------------------------------------------- 21 References -------------------------------------------------------- 22AbstractIn the foreign trade in English,some commonly used the "price" of the phrase.Foreign trade also occurs because a country often does not have enough of a particular item to meet its needs.In today’s economic world, neither individuals nor nations are self-sufficient. Nations have utilized different economic resources while people have developed different skills. This is the foundation of world trade and economic activity.Trade terms stand for specific obligations of the buyer and the seller. Every commercial transaction is based upon a sales contract, and the trade terms used in the contract have the important function of naming the exact point at which the ownership of the merchandise is transferred from the seller to the buyer.The seller or the buyer shall handle a series of complicated formalities, which include carrying out customs formalities for the goods, obtaining the import or export license, chartering a ship or booking shipping space, making insurance, asking for inspection, etc. and pay all kinds of charges and expenses, such as freight, loading and unloading expenses, insurance premium, warehouse charges, duties and taxes, and other miscellaneous expenses.The buyer should note that under the CIP term, the seller is required to obtain insurance only on minimum cover. Should the buyer wish to have the protection of greater cover, he would need either to agree as such expressly with the seller or to make his own extra insurance arrangements.Keywords: foreign trade , individuals ,ownership,insurance1.IntroductionIn international trade,price term lies at the core of the terms and conditions of a contract and often results in some of the key problems for which an exporter and an importer have to strive .what`s more, sending goods from one country to another ,as part of a commercial transaction ,can be a risky business. If they are lost or damaged,or if delivery does not take place for some other reasons,the climate of confidence between the parties may gegenerate to the point where a lawsuit is brought.Thus,the pricing problem an exporter and an importer deal with is far more complicated than that in domestic trade.Besides the cost covered in the calculation of export price,the price quotation in export trade should also indicate which party is to bear the expenses of freightage,insurance and other relevant charges,and which party is to bearthe risks in case of the goods being damaged.In order to complete their deals successful,the sellers and the buyers in international contracts had better,at the very beginning of the deal,make clear to each other their respective obligations and find the full expression of those in the price terms2.International Trade Terms2.1 Three sets of rulesWarsaw-Oxford Rules 1932Revised American Foreign Trade Definitions 1941International Rules for the Interpretation of Trade Terms 2000 Warsaw-Oxford Rules 1932Initially in 1928---“Warsaw Rules, 1928”22 provisions governing the rights and obligations of the parties to a sale of goods on CIF (Cost, Insurance and Freight) contract terms. Revised in 1932---the “Warsaw-Oxford Rules 1932”provisions again mainly about CIFRevised American Foreign Trade Definitions 19412.2 Defines 6 terms:Ex Point of OriginFOB (free on board)FAS (free along side)6 variants of FOBFOB (named inland carrier at named inland point of departure)FOB (named inland carrier at named inland point of departure) Freight Prepaid to (named point of exportation)FOB (named inland carrier at named inland point of departure) Freight Allowed to (named point of exportation)FOB (named inland carrier at named inland point of exportation)FOB Vessel (named port of shipment) ≈ Incoterms’ FOBFOB (named inland point in country of importation)2.3 International Rules for the Interpretation of Trade Terms 2000 (Incoterms 2000)1936--- first created by International Chamber of Commerce (ICC)The purposes of incoterms:To give the businessmen a set of international rules for the interpretation of the most commonly used trade termsTo clarify the obligations of the buyer and the sellerTo simplify the contract negotiationsTo save time and costRevised in 1953、1967、1976、1980、1990、2000Basics of Incoterms 20003. terms into four categories"E"-term—the seller only makes the goods available to the buyer at the seller's own premises."F"-terms — the seller is called upon to deliver the goods to a carrier appointed by the buyer."C"-terms —the seller has to contract for carriage, but without assuming the risk of loss or damage to the goods or additional costs due to events occurring after shipment or dispatch."D"-terms — the seller has to bear all costs and risks needed to bring the goods to the place of destination.3.1 Intercoms 2000 Group Analysis:3.2 Brief of Incoterms3.2.1 The “E” term (EXW)Seller’s obligation min.Placing the goods at the disposal of the buyer at the agreed place –usually his own premisesIn practice, also including assisting the buyer in loading the goods on the buyer’s collecting vehicle without charging a loading feeFor the buyer to get lower price, but too demanding for him, therefore only applied to buyers having offshore branchesEXW:Delivery: at seller’s premisesTransfer of risks: goods at the disposal of the buyerPackaging and loading:Usu. seller no obligation for export packaging and loading;Export customs clearance:Usu. buyer’s responsibility, sometimes buyer do it for buyer, but bear no risks3.2.2 The “F” terms (FCA, FAS, FOB)Shipment contract:Seller delivers the goods for carriage as instructed by the buyer;buyer pays freight and signs carriage contract with carrier and notify sellerFAS & FOB only for sea or inland waterway transportation mode Seller’s obligation, cost and risk transfers to buyer after delivery of the goods;Seller – exporting license and export customs clearance Buyer – importing license and import customs clearanceFCA Free Carrier (…. Named place)Transfer of risks:goods at the disposal of the (1st) carrierDelivery point:If at seller’s site, seller responsible for loading If anywhere else, seller responsible for delivering the goods to the point required, but not responsible for unloading or reloadingFAS Free Alongside Ship (…named port of shipment)Delivery point: at port of shipmentTransfer of risk:goods put alongside the vesselIf vessel unable to enter the port due to force majeure, the seller is responsible for arranging and paying for the lighters to send the goods alongside the vessel offshore. (seller pays for lighter charges)FOB Free on Board (… named port of shipment)Delivery point: at port of shipmentTransfer of risks: goods pass over the ship’s railCost and obligation: the seller is paying for the necessary handling of goods until they are loaded onboard the vessel.Strictly speaking, transfer of risks ≠ transfer of obligation and cost 3.2.3 The “C” terms (CFR, CIF, CPT, CIP)Shipment contractsSeller contract for carriage on usual terms at his own expense.CFR & CIF only for sea or inland waterway transportation modeUnder CIF and CIP, seller also takes out insurance and insurance cost. The “C” terms (CFR, CIF, CPT, CIP)Two “critical” points :Port (place) of shipment – to which the buyer takes over the risksPort (place) of destination – to which the seller is bound to arrange and bear the costs of a contract of carriage.Exception of containertransport: the container ship has no rail, delivery is fulfilled when the goods are handed over to the container carrier.CFR Cost and Freight (… named port of destination)Shares every feature with FOB except for ocean freight chargeFreight at seller’s cost:Seller pay the normal transport cost for the carriage of the vessel by a usual route and in a customary manner to the agreed placeBuyer take the risk of loss or damage to the goods and additional costs resulting from events occurring after the delivery of the goods Obligation: seller’s responsibilityfor booking shipping space and getter goods ready for shipment in due time to notify to buyer about the delivery of goods (Shipping advice) so as to facilitate buyer to fulfill insurance procedures notification is more important under CFR than under FOB and CIFCIF Cost, Insurance and Freight (… named port of destination)One step forward from CFR;Insurance born by seller;Insurance for the buyer The seller pays for the insurance, but he does not take the risk of the cargo.Seller responsible for “min. coverage”If required by buyer and at buyer’s expense, additional coverage such as war, strike can be addedSeller has no responsibility to guarantee the arrival of the goods at the destination.CPT Carriage Paid to (… named place of destination)CPT is similar to CFRDifferences: Mode of transport CPT – any modeCFR – Sea or Inland WaterwayDelivery point :CPT – inland place or port of shipmentCFR – port of shipmentTransfer of risks:CPT – goods delivered to carrierCFR – goods pass over ship’s railCIP Carriage and Insurance Paid to (… named place of destination) CIP is similar to CIFDifferences:Mode of transport CIP –any mode CIF –sea or inland waterwayDelivery point :CIP – Inland place or port of shipmentCIF – port of shipmentTransfer of risks:CIP – goods at the disposal of carrierCIF – goods passing ship’s railFreight and insurance:CIP – whole journey freight and insuranceCIF – voyage freight and insurance3.2.4 The “D” terms (DAF, DES, DEQ, DDU, DDP)Arrival contracts – seller bear all risks and costs in bringing the goods to the agreed place or point of destination at the border or within the country of import.Seller’s responsibility max.DES & DEQ only for sea or inland waterway transportation modeSeller responsible for both export and import customs clearance under DDP DAF Delivered at Frontier (… named place)Only suitable for trade between neighboring countries who have inlandborders.Delivery point: inland place at frontier cleared stipulated in the contractTransfer of risks: goods at the disposal of the buyer at frontier DES Delivered ex Ship (… named port of destination)DES similar to CIF:Differences:Place of deliveryDES – port of destination, CIF – port of shipmentTransfer of risks:DES – goods at the disposal of buyer on board the vessel at the port of destinationCIF – goods pass over ship’s rail at the port of shipmentObligation and cost:DES – seller responsible for freight, insurance and any other costs until the goods arrive at the named port of destination CIF – seller only responsible for normal freight and min. insurance DEQ Delivered ex Quay (… named port of destination)One step forward from DESDifference: Under DEQ, sellers must also unload the goods and place on the wharf (quay), so Transfer of risks: DEQ – goods at the disposal of buyer on the quay at the port destinationDES – goods at the disposal of buyer on board the vessel at the port destinationObligation and cost:DEQ – seller responsible for unloading charges from the vessel to the quayDES – no unloading is involvedDDU Delivered duty Unpaid (… named place of destination)Similar to CIP Differences:Place of deliveryDDU – inland place in the importing countryCIP – inland place in the exporting countryTransfer of risks:DDU – goods at the disposal of buyerCIP – goods at the disposal of the carrierObligation and cost:DDU – seller responsible for all costs and risks before the completion of deliveryCIP – seller only responsible for normal freight and min. insurance DDP Delivered Duty Paid (… named place of destination)DDP – seller’s obligation max.: seller provides a “door-to-door”delivery and bears the entire risk of loss until the goods are placed in the buyer’s premises.Unlike DDU, sellers must also responsible for import customs clearance and other payments of domestic duties in the importing country Applied unless the seller has the resources and capability to handle all the procedures.4. Three of the most popular in international trade of trade terms4.1 FOBFree On Board (… named port of shipment) This term means that the seller delivers when the goods pass the ship’s rail at the named port of shipment. And the buyer has to bear all costs and risks of loss of or damage to the goods from that point. The FOB term requires the seller to clear the goods for export. This term can be used only for sea or inland waterway transport. If the parties do not intend to deliver the goods across the ship’s rail, the FCA term should be used.FOB is a widely used term in international trade. Under this term, the seller must obtain at his own risk and expense any export license or other official authorization and carry out, where applicable, all customs formalities for the import of the goods and, where necessary, for their transit through any country. The risk of loss of or damage to the goods is transferred from the seller to the buyer when these goods pass over the ship’s rail at the named port of shipment. The buyer bears all costs and risks of loss or damage to the goods from the time it has passed the ship’s rail and pays the price as specified in the sales contract. However, as the loading of the goods is a continuous process, it is hard to use ship’s rail as a point to divide responsibilities and costs. To avoid any dispute, there are several derived terms:FOB Liner TermsIt means that the ship will be responsible for loading and the seller does not have to pay loading expenses.FOB Under TackleThis term only requires the seller to send and place the goods on the wharfwithin the reach of the ship’s tackle. Loading expenses incurred thereafter will be borne by the buyer.FOB StowedUnder this term, the seller loads the goods into the ship’s hold and pays the loading expenses including stowing expenses.FOB TrimmedThe seller pays all the loading expenses including trimming expenses (which actually also includes stowing expenses).For example, we offer to sell mushroom in brine 10.00 MT, USD 1,000.00 MT FOB Shanghai, shipment during April.4.2 CIFCost, Insurance and Freight (… named port of destination)This term means that the seller delivers when the goods pass the ship’s rail at the port of shipment. The seller must pay the costs and freight necessary to bring the goods to the named port of destination but the risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time of delivery, is transferred from the seller to the buyer. Under CIF, in addition to CFR obligations, the seller is obliged to arrange marine insurance against the risk of loss of or damage to the goods in transit. That is to say, the seller contracts with the insurer and pays the insurance premium.However, the buyer should note that under the CIF term the seller is required to obtain insurance only on minimum cover. Should the buyer wish to have the protection of greater cover, he would need either to agree as such expressly with the seller or to make his own extra insurance arrangements.The CIF term requires the seller to clear the goods for export.This term is a popular cargo delivery arrangement and can only be used for sea and inland waterway transportation. To stipulate clearly the responsibility and cost of unloading as CFR, CIF also has some derived terms: CIF Liner terms, CIF Landed and CIF Ex-Ship’s Hold.For example, we offer to sell … 10,000 MT US$ 100.00 per MT CIF Pusan, prompt shipment.4.3 CFRCost and Freight (… named port of destination)This term means that the seller delivers when the goods pass the ship’s rail at the port of shipment. The seller must pay the costs and freight necessary to bring the goods to the named port of destination but risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time of delivery, is transferred from the seller to the buyer. The seller must bear all risks of loss of or damage to the goods until such time as they have passed the ship’s rail at the port of shipment, while the buyer must accept delivery of the goods when they have been delivered and receive them from the carrier at the named port of destination. The CFT term requires the seller to clear the goods for export.This term can be used only for sea and inland waterway transport. If the parties do not intend to deliver the goods across the ship’s rail, the CPT term should be used.It is the seller that charters the ships, books shipping space and pays for the cargo loading. When the goods are loaded on board the vessel, the seller should send shipping notice to the buyer.Cargo insurance is to be effected by the buyer. The buyer receives the goods at the port of destination and funds all unloading expenses at destination port unless such costs have been included in the freight or collected by the ship-owner at the time freight was paid.To specify clearly the responsibility and cost of unloading, some derived terms can also be used.CFR Liner TermsThe ship is responsible for the discharge of goods. The unloading charges are included in freight that is paid by the seller.CFR LandedThe goods must be unloaded onto the dock. The seller is responsible for discharge of the goods and pays the cost, including lighterage and wharfage charges.CFR Ex-Ship’s HoldThe seller fulfills his obligations when he has made the goods available to the buyer for unloading. The buyer pays the cost for discharging the goods from the ship’s hold.For example, we offer to sell tongue depressors 4,000 cartons US$13,000 per carton CFR Kobe, shipment during May.5. Three Common Used Trade Terms5.1 FCAFree Carrier (… named place)This term means that the seller delivers the goods,clears for export, to the carrier nominated by the buyer at the named place. It should be noted that the chosen place of delivery has an impact on the obligations of loading and unloading the goods at that place. If delivery occurs at the seller’s premises, the seller is responsible for loading. If delivery occurs at any other place, the seller is not responsible for loading.This term may be used irrespective of the mode of transport, including multi-modal transport. “Carrier” means any person who, in a contract of carriage, undertakes to perform or to procure the performance of transport by rail, road, air, sea, inland waterway or by a combination of such modes.If the buyer nominates a person other than a carrier to receive the goods, the seller is deemed to have fulfilled his obligation to deliver the goods when they are delivered to that person. The risk of loss of or damage to the goods is transferred from the seller to the buyer at the time the nominated carrier accepts them at the prescribed place.The seller must provide any requisite export license and customary packing, and supply the buyer with the customary transport documents (bill of lading, etc.) as proof of delivery of the goods to the carrier. The buyer must bear all the cost and risk of the goods from the time they have been delivered to the carrier.For example, we offer to sell ladies’ nylon umbrellas 10,000 dozens US$15 per dozen Free Carrier’s warehouse at 32 Sichuan Road, Shanghai, China, delivery during August.5.2 CPTCarriage Paid to (… named place of destination)This term means that the seller delivers the goods to the carrier nominated by him but the seller must in addition pay the cost of carriage necessary to bring the goods to the named destination. This means that the buyer bears all risks and any other costs occurring after the goods have been so delivered. “Carrier” means any person who, in a contract of carriage, undertakes to perform or to procure the performance of transport, by rail, road, air, sea, inland waterway or by a combination of such modes. If subsequent carriers are used for the carriage to the agreed destination, the risk passes when the goods have been delivered to the first carrier.The CPT term requires the seller to clear the goods for export.CPT is almost the same as CFR except that CFR is only applied to sea and inland water transportation while CPT may be used for any mode of transport including multi-modal transport.For example, we offer to sell groundnuts 5,000 MT US $300 per MT CPT Salt Lake City, delivery during October.5.3 CIPCarriage and Insurance Paid to (… named place of destination)This term means that the seller delivers the goods to the carrier nominated by him but the seller must in addition pay the cost of carriage necessary to bring the goods to the named destination. This means that the buyer bears all risks and any additional costs occurring after the goods have been so delivered. However, under CIP term the seller also has to procure insurance against the buyer’s risk of or damage to the goods during the carriage. Consequently, the seller contracts for insurance and pays the insurance premium.The buyer should note that under the CIP term, the seller is required to obtain insurance only on minimum cover. Should the buyer wish to have the protection of greater cover, he would need either to agree as such expressly with the seller or to make his own extra insurance arrangements. “Carrier” means any person who, in a contract of carriage undertakes to perform or to procure the performance of transport, by rail, road, air, sea, inland waterway or by a combination of such modes.If subsequent carriers are used for the carriage to the agreed destination, the risk passes when the goods have been delivered to the first carrier. The CIP term requires the seller to clear the goods for export.This term may be used irrespective of the mode of transport including multimodal transport.Briefly, this term is almost identical to CPT except that under CIP, the seller has to fund the cargo insurance. The seller’s liability ceases when the cargo has been accepted by the carrier or the first carrier under multimodal transport operation. Its only difference from CIP is that CIF is applied to all modes of transport.For example, we offer to sell ice-cream sticks 5,000 cartons US$2.80 per carton CIP Qingdao city, delivery during September.ConclusionIt becomes apparent that every business is confronted with a pricing problem. Businessmen are particularly interested in seeing the goods of their firms sold in sufficient volume and at profitable prices. Price occupies a position of first-rank importance and present some of the key problems with which they are forced to contend. The same is true with the foreign trade business. To some extent, however, the pricing problems an exporter tackles are more complicated than that in domestic trade. In addition to the cost of the goods included in the calculation of the export price, the price quotations in foreign trade are invariably accompanied by an indication as to which party is to pay the expenses of freightage, insurance, loading, unloading and other incidental charges, and to bear the risks in case of the goods being damaged. It is essential that a foreign trade merchant should know how an export quotation is constructed.References[1].Alexander Eckstein, Communist China's Economic Growth and Foreign Trade,McGrawHillAlexander Eckstein,1966-01.[2].Nicholas R. Lardy,Foreign Trade and Economic Reform in China, 1978-1990,Cambridge University Press,Cambridge University PressNicholas R Lardy,1992.[3]william f. Spalding,the finance of foreign trade , london sir isaac pitman & sons,ltd,1936-01.[4].Steiner, G. (1998). After Babel. (3rd ed.). New York: Oxford University Press[5].Tan Zaixi. (1999). 新编奈达论翻译. [Nida’s theory on translation]. Beijing:[6].Wang Xuxiao. (1994). 美学与市场营销. [Aesthetics and marketing]. Shengyang: Chunfeng Press.[7].Xu Yuanchong. (2000, March). 新世纪的新译论. [New translation theories of the new centry]. Chinese Translators Journal, p. 2. [8].王乃彦李富森等编著,Oral English for foreign trade,出版社:对外经济贸易大学出版社,出版日期:2000-4-1.[9].中国国际贸易学会商务培训认证考试办公室编,Foreign Trade Logistic English ,出版社中国商务出版社, 出版时间:2007年10月.[10]. 廖瑛...[等]编著作者廖瑛编著禹金林编著覃蔚编著李春江编著,English for International Business Negotiations,出版者北京:对外经贸大学出版社 ,2004索书号H31/5665 ISBN7-81078-379-3分类号H31 H31 .[11].刘法公 ,《国际贸易实务英语》浙江大学出版社 2002年.[12].李小牧陈伟,《国际支付方式》,清华大学出版社,2006年.[13].郝美彦主编,《外贸英语》出版社:东北财经大学出版社出版日期:2008-1-1.。

Contents

But when you knocked at the door …

Oh my Goddess..

Mary felt surprised. Why?

In China, it’s OK to visit friends without calling ahead of time. While in the U.S., it’s impolite to do so.

For detail

Structure of the Text

随 笔 词汇学习 课文阅读

导入

预习

小结

写作

Back

Part I Part II Part III

Main Idea of Part I

[Para. 1&2 ] To Americans, time lost can not be The author presents the general idea of the replaced. So time is always a precious resource passage —— Americans value time greatly —— they are committed to saving by all means. by coming straight to the point.

How to greet in English?

Blessings: Treasures fill the home

金玉满堂

Business flourishes

Peace all year round May all your wishes come true Everything goes well The country flourishes and people live in peace

单复数意义不同的英语单词名词

advice 忠告 advices 消息 ash 灰烬 ashes 骨灰 blue 兰色 blues 烦闷,忧郁 colour 颜色 colours 旗帜 content 容量,内容 contents 目录 damage 损害 damages 赔偿金 effect 效果 effects 动产,家产 fetter 脚镣 fetters 囚禁,束缚 foot 脚 foots 渣滓 fund 资金 funds 现金 ground 土地 grounds 根据,理由 heaven 天国 heavens 天空 iron 铁 irons 镣铐 line 行 lines 诗歌 manner 方式 manners 礼貌 moral 教训 morals 品行 pain 痛苦 pains 辛苦,努力 physic 药品 physics 物理 quarter 四分之一 quarters 住宅 sand 沙 sands 沙滩 scale 风度 scales 天平 spectacle 景象 spectacles 眼镜 step 步骤,脚步 steps 台阶 troop 群,队 troops 军队 wit 有才能的人 wits 智力 air 空气 airs 风度、神气 beef 牛肉 beeves 食用牛,菜牛 brain 脑髓 brians 脑力 compass 罗盘 compasses 圆规 custom 习惯,风俗 customs 海关,关税 drawer 抽屉 drawers 衬裤 copper 铜 coppers 铜线 experience 经验 experiences 经历 force 力 forces 军队,兵力 green 绿色 greens 蔬菜 gut 肠子 guts 内脏,内容,勇气 honour 荣誉 honours 优等成绩 letter 信,字母 letter

Contents

ContentsDiscipline & Self-discipline04 Intelligent Human-Machine Synergy in Collaborative Teaching of Intelligent Era: Path Design Basedon Avatar, Digital Twin, and RobotHUANG Ronghuai, LIU Dejian, Ahmed Tlili, ZHANG Guoliang, CHEN Ying & WANG Huanhuan

15 Research Policy Planning and Innovation Path of Generative AI Education: Key Points andReflections of UNESCO's Guidance for Generative AI in Education and ResearchLAN Guoshuai, DU Shuilian, SONG Fan, XIAO Qi, DING Linlin & QI Chunyan

27 Reflections on Open University Evaluation: Taking the Platform University Construction as an EntryPointJIA Wei

34 Future-generation Assessment Design: OECD Innovation Assessment to Measure and SupportComplex CapacityLI Gang, ZHAO Jiaqi & ZHENG Zelin

42 A New Inquiry Learning: Conversational Learning with ChatGPTDAI Ling, ZHAO Xiaowei & ZHU Zhiting

CONTENTS目录

CONTENTS 目录【特别报道】引领竞跑 全线齐发东风轻型车:百城巡展尽显风流来自商务处、经销商和客户的声音“东风汽车”行业首推整车消费信贷【风范时讯】“东风汽车”一季度产销大捷“双品牌”谋划郑州日产 LCV新天地新一代东风轻型车成广交会“明星”东风沼气服务车在安徽受欢迎“东风金莲花”成为博鳌亚洲论坛指定接待用车 埃及 MCV 公司总裁访问东风旅行车公司43 辆“东风莲花”落户湖北京山河南环保执法车辆发车仪式在郑州举行郑州日产 2008“夏季服务月”活动诚意进行 【招商信息】“东风零服”:创造中国汽车后市场新商机】【外眼看“东风汽车”《“东风汽车”拉开“315”事业计划序幕》等 【行业动态】《柴油不存在实质性的货源短缺》等三则【客户驿站】东风轻卡:80 万公里风采依旧大哥情怀塞上致富双宝告诉你一个赚钱的秘诀王先生的皮卡情结【创富讲堂】养成良好驾驶习惯跑熟悉的路线【包律师说法】汽车保险案例(八)【营销寓言】天使与魔鬼赵襄王学御【东风兄弟俱乐部】东风兄弟俱乐部进行分部运作指导东风兄弟俱乐部 IC 卡联网系统正式启用 倾听和微笑【健哥走天下】西递探幽【郝师傅教修车】发动机不能转动发动机有沉重而强烈的震动声【车趣四格】【特别报道】引领竞跑 全线齐发策划/《风范》编辑部 本刊记者 傅祥友 闫 霞 丰 凡/文从 2005 年 12 月底开始, 国家就已经在北京率先推行执行国家第三阶段排放标准的汽车 产品。

接下来,几个主要城市也开始推行。

例如,2006 年 9 月,广州拉开珠三角执行国Ⅲ 的序幕;2007 年 7 月1 日,深圳开始执行国Ⅲ排放标准,2008 年7 月 1 日后,全国都要执 行国家第三阶段排放标准。

在这种形势下,行业几个主要品牌陆续也推出了满足国Ⅲ法规的产品。

但由于这些产品 仅着眼于满足法规,所谓的国Ⅲ产品整体的性能和品质并未得到提升,这样,用户在承受高 价格压力的同时并未得到相应的高品质产品,致使市场需求受到抑制。

通常以复数形式出现的词

通常以复数形式出现的词一、表示由两部分构成的东西:scissors 剪刀 pants 裤子 shorts 短裤 jeans 牛仔裤 briefs 三角裤 compasses 圆规 scales 天平 pliers 钳子 tongs 火钳 spectacles (glasses) 眼镜 ear-phones 耳机 braces 背带 cords 灯芯绒裤 binoculars 双眼望远镜 knickers 灯笼裤 tights 紧身衣 overalls 工装裤 trunks 男用运动裤 pyjamas 睡衣裤 underpants 内裤 slacks 便装裤 specs 眼镜 nail-clippers 指甲刀二、以-ing结尾的词:belongings 所有物 surroundings 环境 tidings 消息 doings 行为 savings 储蓄 findings 调查结果 shavings 刨花 earnings 挣的钱 sweepings 扫拢的垃圾 clippings 铰下的东西 winnings 赢的钱 writings 作品三、其他:contents 目录 arms 武器 statistics 统计资料 fireworks 烟火 remains 残余 oil-colours 油画 outskirts 城郊 assets 资产 living-quarters 住宅区 riches 财富 ashes 灰烬 valuables 珍贵物品 amends 补债 annals 编年史 archives 档案室 arrears 欠款 bowels 肠 dregs 渣滓 guts 胆量 particulars 细节 armed forces 武装部队 dominoes 多米诺骨牌 effects (家庭)财物 greens 青菜 tropics 热带 dues 应交的费 brains 头脑 goods 货物四、只用于复数形式的合成名词:armed forces 武装部队 current affairs 时事,新闻 grass roots 基层 inverted commas 引号 natural resources 自然资源 social services 社会服务 swimming trunks 泳裤 yellow pages (电话簿)黄页 civil rights 公民权利 French fries 炸土豆条 human rights 人权 luxury goods 奢侈品 race relations 种族关系 social studies 社会研究。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

BibliographymanagerNickApostolakis

AdissertationsubmittedinpartfulfillmentoftherequirementoftheDegreeofMScinInformationTechnologyatTheUniversityofGlasgow.

September2005Contents1.Introduction52.Otherbibliographymanagementsystems72.1.EndNote...............................72.1.1.Features...........................72.1.2.Comparisonwiththebibliographymanager........82.2.JabRef................................92.2.1.Features............................92.2.2.Comparisonwiththebibliographymanager........102.3.Jorge.................................112.3.1.Features............................112.3.2.Comparisonwithbibliographymanager..........112.4.RefDB.................................12

3.Analysis133.1.SoftwareSystemRequirements...................133.1.1.Usecasedescriptions....................143.2.Initialtechnologyresearch.....................153.2.1.Thefirstcandidatetechnology................163.2.2.Thesecondcandidatetechnology..............163.2.3.Thedatarepository......................173.2.4.TheIDE............................173.3.SoftwareSystemDesign.......................173.3.1.Thedatabasebackend....................193.3.2.TheRdbmspackage.....................193.3.3.TheBibtexpackage......................19

2Contents3.3.4.TheBusinessLogicpackage.................203.3.5.TheUserInterfacepackage.................203.3.6.Classesperpackage.....................21

4.DesignandImplementation264.1.Databaseimplementation......................264.1.1.Tabledescriptions......................264.1.2.Constraintdescriptions...................274.2.Applicationdesignandimplementation..............294.2.1.Searchandsave.......................294.2.2.ParseLaTEXfile........................304.2.3.LoadBiBTEXfile.......................30

5.TestingandEvaluation325.1.Testing................................325.1.1.Databasetesting.......................325.1.2.Unitandcomponenttesting.................335.2.Evaluation..............................33

6.Conclusion35A.Diagrams37A.1.Developmentprocess........................38A.2.Analysisdiagrams..........................39A.2.1.Requirementdiagram....................39A.2.2.PackageDiagram.......................40A.2.3.ERdiagram..........................41A.2.4.Classesperpackage.....................42A.3.Design/Implementationdiagrams.................43A.3.1.Classdiagram.........................43A.3.2.Searchdatabasesequencediagrams............44A.3.3.ParseLaTEXfilesequencediagrams.............47A.3.4.LoadBiBTEXfilesequencediagram.............49

B.SQLdata51B.1.Databaseschema..........................51

3ContentsB.2.Droptablescommands.......................51B.3.Insertinentry_typestable......................52B.4.Insertinfieldstable.........................52B.5.Insertinnecessity_of_fieldstable..................53B.6.Insertinis_consisted_oftable...................54

C.Evaluation55C.1.EvaluationResults..........................55C.2.EvaluationForm...........................62

D.InstallationInstructions63E.Applicationmanual66E.1.Introduction.............................66E.1.1.Whatisthegoalofthebibliographymanager.......66E.1.2.Whoneedsthebibliographymanager............66E.2.Searchtab..............................67E.2.1.UserInterfacedescription..................67E.2.2.Functionalitydescription...................68E.3.ExportListtab............................69E.3.1.UserInterfacedescription..................69E.3.2.Functionalitydescription...................70E.4.Importtab..............................72E.4.1.Userinterfacedescription..................73E.4.2.Functionalitydescription...................74E.5.TheInserttab............................75E.5.1.Userinterfacedescription..................76E.5.2.Functionalitydescription...................76E.6.Themenuoptions..........................78E.6.1.TheFileoption........................78E.6.2.TheToolsOption.......................79

Bibliography83

41.IntroductionItisacommonproblemamongtheacademiccommunitytohuntdownbiblio-graphicreferencesduringthecreationoftheirpublicationsandpreservetheminawaythattheywillbeusefulfortheircurrentandfuturepublications.Itisveryimportanttocreatecollectionsofbibliographicrecordsthatwillbereusedforthefutureneedsoftheresearcher.AlthoughtheBiBTEXbibliographicrecordsarethemselvesreusableitisdif-ficultforonetonavigatethroughabigcollectionofrecordsandevenmoredifficulttoidentifyduplicateentriesorwhenforexampletwodifferententriesbythesameauthorindifferentfileshavethesamebibliographickey,thuscompromisingtheconsistencyofthecollection.Asonecouldeasilyguessduringthepastyearsanumberofsoftwarepack-ageshavebeendevelopedthatwouldsolvesomeoftheaboveproblems.Thesepackagesusemanydifferentapproachestotheproblemandanequallydi-versenumberoftechnologiestoachievetheirsolutions.Manyoftheseprojectshavetheformofwebapplicationsinclient/serverarchitectureform,othersaretraditionalapplicationsstillinclientserverformandsomeofthemarestan-daloneapplications.Someofthemmoveintheopenandfreesoftwarerealmandothersusethetraditionalproprietarylicensemethod.InthisreportIwilldescribeanumberofsuchsystemsandthesolutionIhavecreatedduringasmydissertationproject.Shortlythechaptersofthisdocumentare: