Auditing Engagement Planning

介绍公司高层管理人员介绍英文模板范文

介绍公司高层管理人员介绍英文模板范文As a document creator, it is important to have a clear understanding of the key members of the company's senior management team. This information is crucial for internal communication, external stakeholders, and the overall success of the organization. In this document, we will introduce the key members of the company's senior management team, highlighting their roles, responsibilities, and contributions to the company.1. Chief Executive Officer (CEO)。

The CEO is responsible for the overall strategic direction and leadership of the company. They work closely with the board of directors to develop and implement long-term goals, strategies, and plans. The CEO is also the public face of the company, representing it in various capacities, including with investors, the media, and other stakeholders. In addition, the CEO oversees the performance of the executive team and ensures that the company's operations are in line with its mission and values.2. Chief Financial Officer (CFO)。

实用审计英语

Introduction to auditing(审计概述)【key words and phrases】1. Audit - the objective of an audit of financial statements is to enable the CPA to express an opinion whether the financial statements are prepared, in all material respects, in accordance with an identified financial reporting framework. 审计2. CPA - Certified Public Accountant or independent CPA, the CPA is the person with final responsibility for the audit. 注册会计师3. Attestation - CPAs are engaged to issue a written communication that expresses a conclusion about the reliability of a written assertion that is the responsibility of another party. 鉴证4. Assurance - CPAs evaluate or measure a subject matter through the application of independent professional judgment to enhance the credibility of information about subject matter and thereby to improve the likelihood that the information will meet the needs of an intended use. 可信性保证5. Audit of financial statements - the CPA's performance of the necessary audit procedures to obtain sufficient appropriate audit evidence on the entity's financial statements in accordance with the requirements of the Independent Auditing Standards, and the expression of an audit opinion on the financial statements, following the CPA's acceptance of the engagement in accordance with relevant laws an regulations. 会计报表审计6. Financial statements - the annual financial statements which need to be audited by the CPA. They include the balance sheet, the profit and loss account (or the income statement), the statement of changes in financial position(or the cash flow statement), notes to the financial statements and relevant appendices. 会计报表7. Agreed-upon procedures - an CPA is engaged to vary out those procedures of an audit nature to which the CPA and the entity and any appropriate third parties have agreed and to report on factual findings. 执行商定程序8. Compilation - in a compilation engagement, the accountant is engaged to use accounting expertise as opposed to auditing expertise to collect, classify and summarize financial information. 编制9. High levels of assurance - any assurance engagement intended to provide a high, but not absolute, level of assurance. The professional accountant has obtained sufficient appropriate evidence to conclude that the subject matter conforms in all maturate respects with identified suitable criteria. 高保证水平10. Moderate levels of assurance - the professional accountant has obtained sufficient appropriate evidence to be satisfied that the subject matter is plausible in the circumstances. 中等保证水平11. Credibility 可信性、可信程度12. Reliability 可靠性、可靠程度13. Relevance 相关、相关性Introduction to CPAs(注册会计师)【key words and phrases】1. continuing professional education(CPE)-the study and research undertaken by CPAs with a view to maintaining and improving their professional competence and the standard of their professional work, and obtaining and applying relevant new knowledge, skills, laws and regulation. 职业后续教育2. A uniform CPA examination- a uniform CPA examination administered once a year by the Chinese Institute of Certified Public Accountants for state boards of accountancy to enable them to issue CPA licenses. 统一的注册会计师考试3. Professional skepticism -an attitude that includes a questioning mind and a critical assessment of audit evidence. 职业谨慎4. Objectivity - a combination of impartiality, intellectual honesty and a freedom from conflicts of interest. 客观,客观性5. Professional competence - any CPA performing independent audit work should possess professional knowledge and experience, receive appropriate professional training and possess adequate analytical capability and judgment. 专业胜任能力6. Senior/CPA-in-charge - the senior/CPA-in-charge is an individual qualified to assume responsibility for planning and conducting an audit and drafting the audit report, subject to review and approval by the manager and partner. 项目经理Audit engagement letters(审计业务约定书)【key words and phrases】1. audit engagement letter - a written agreement or contract(usually acknowledged and accepted by the client as indicated by the client's signature)that documents and confirms the CPA's acceptance of the engagement, the objective and scope of the audit, the extent of the CPA's responsibilities to the client, and the form of any reports. 业务约定书2. recurring audit - an audit performed by a continuing CPA who also performed the prior year audit. 常年审计,连续审计3. the client - the entity or individual who engages the accounting firm and signs the audit engagement letter with the accounting firm. 委托人4. the nominated CPA 被提名审计师5. change CPA 更换审计师6. the existing CPA 现任审计师7. the successor CPA - the auditors who have accepted an engagement or who have been invited to make a proposal for an engagement to replace the CPA firm that formerly served as auditors. 后任审计师8. the preceding CPA(The predecessor CPA) - the CPA firm that formerly served as CPA but has resigned from the engagement or has been notified that its services have been terminated. 前任审计师9. audit appointment 审计委托10. the agreed term 约定条款11. accept an audit engagement 接受业务委托12. the objective of the engagement 委托目的13. the scope of the audit - the review procedures deemed necessary in the circumstances to achieve the objective of the audit. 审计范围14. issue the audit report 出具审计报告15. other CPA - the CPA of another accounting firm who is responsible for performing an audit on the accounting information of one or more components of the entity 其他注册会计师16. expert - a person or firm possessing special skill or knowledge in a field other than accounting or auditing, such as an actuary. 专家17. withdraw 撤消18. an initial audit 初次审计19. the board of directors 董事会20. a change in engagement 变更约定书21. shareholder 股东22. component - the entity's division, branch, subsidiary of associated company etc. Whose accounting information is included in the financial statements as a whole, audited by the principal CPA. 组成部分Knowledge of the entity's business【key words and phrases】1. knowledge of then entity's business - a general understanding of the economic environment and the industry within which the entity operates, and a more detailed understanding of the entity's internal condition. 了解被审计单位情况2. performing an audit of financial statements 实施财务报表审计3. assess inherent and control risks 评估固有风险和控制风险4. determine the nature, timing and extent of the audit procedures 确定审计程序的性质、时间和范围5. a general knowledge of...,a preliminary knowledge of 初步了解...的情况6. a more particular knowledge of ... 进一步了解...的情况7. prior to accepting an engagement 承接业务委托前8. following acceptance of the engagement 承接业务委托后9. update and reevaluate information gathered previously 更新并重新评价以前收集的信息10. the prior year's working papers 以前年度工作底稿11. director 董事12. senior operating personnel 高级管理人员13. internal audit personnel, internal audit's —— corporation employees who design and execute audit programs to test the effectiveness and efficiency of all aspects of internal control. The primary objective of internal audit is to evaluate improve the effectiveness and efficiency of the various operating units of an organization rather than to express an opinion as to the fairness of financial statements. 内部审计人员,内部审计师14. internal audit reports 内部审计报告15. minutes of meeting 会议纪要16. material sent to shareholders or filed with regulatory authorities 寄送给股东或报送监管部门备案的资料17. interim financial reports 中期财务报告18. management policy manual 管理政策手册19. chart of accounts 会计科目表20. exercise professional judgement 作出专业判断21. business risks (of the client) ——the risk assumed by investors or creditors that is associated with the company's survival and profitability. 经营风险22. management response thereto 管理当局的对策23. appropriateness ——the measure of the quality of audit evidence and its relevance to a particular assertion and its reliability. 适当性24. accounting estimate 会计估计25. management representations ——representations provided by management to the CPA that are related to the financial statements, either unsolicited or in response to specific inquiries. 管理当局声明26. related party ——parties are considered to be related if one party has the ability to control the other party or exercise significant influence over the other party in making financial and operating decisions. 关联方27. related party transaction ——a transfer of resources or obligations between related parties, regardless of whether a price is changed. 关联交易28. going concern assumption —— under the going concern assumption, an entity is ordinarily viewed as continuing in business for the foreseeable future with neither the intention nor the necessity of liquidation, ceasing trading or seeking protection from creditors pursuant to laws or regulations. 持续经营假设Audit planning【key words and phrases】1. audit plan ——a work plan, prepared by the CPA before performing detailed audit procedures, for completing an audit engagement of annual financial statements and achieving the expected audit objectives. 审计计划2. the overall audit plan —— the overall audit plan gives guidance on the expected scope of the audit and the way to perform the audit tests. It is a comprehensive plan of what the CPA's work basically involves throughout the whole process, from the acceptance of an audit engagement to the issuance of an audit report. 总体审计计划3. the detailed audit paln ——the detailed plan is prepared based on the overall audit plan. it sets out a detailed descriptionof the approach, nature, timing and extent of the audit procedures required in implementing the overall audit plan. 具体审计计划4. efficient audit (Audit in an effective manner) ——an effective audit that is performed at the lowest possible cost. 提高审计效率5. the size of the entity 被审计单位的规模6. the complexity of the audit 审计的复杂程度7. the specific methodology and technology 具体方法和技术8. financial performance 财务业绩9. material misstatement 重大虚假陈述10. significant audit areas 重点审计领域11. accounting estimate 会计估计12. coordination 协调13. review 复核14. statutory responsibility 法定责任15. time budget ——an estimate of the time required to perform each step in the audit 时间预算Error and Fraud【key words and phrases】1. error ——error refers to an unintentional misstatements or omissions in financial statements. 错误2. fraud ——fraud refers to intentional act which results in a misrepresentation of financial statement. 舞弊3. modified or additional procedures 修改或追加审计程序4. plan and perform audit procedure 计划和实施审计程序5. adequate accounting and internal control system 适当的会计和内部控制系统6. reduce but not eliminate 减少但不能消除7. manipulation 篡改8. falsification 伪造9. alteration of records or documents 更改记录和凭证10. misapproporation of assets 侵占资产11. transaction without substance 虚假交易12. misapplication of accounting policies 滥用(误用)会计政策13. the underlying records 原始凭证14. oversight or misinterpretation 疏忽或误解15. unusual pressures 异常压力16. accounting policy alternative 会计政策变更17. unusual transactions 异常交易18. incomplete files 不完整的档案19. out of balance control accounts 账户余额不平衡20. lack of proper authorization 缺乏适当的授权21. computer information systems environment 计算机信息系统环境22. inherent limitations of audit test 审计测试的固有限制23. discuss with management 与管理当局讨论24. the remedial action 纠正措施25. seek legal advice 寻求法律咨询Noncompliance with laws and regulations【key words and phrases】1. laws and regulations —— state laws, administrative regulations, departmental rulesand local laws and regulations other than the Accounting Standards for Business Enterprises and other relevant financial and accounting laws and regulations promulgated by the State. 法律与规章2. noncompliance ——noncompliance refers to acts of omission or commissionby the entity being audited, either intentional or unintentional, which are contrary to the prevailing laws or regulations. Such acts, include transtractions entered into by, or in the name of, the entity or on its behalf by its management or employees. 违反,不遵守3. withdrawal from the engagement 报销审计约定4. board of directors 董事会5. senior management 高级管理层6. detect noncompliance laws and regulations 发现违反法律和规章的行为7. deliberate failure to record transactions 故意漏记交易8. senior management override of control 高级管理层逾越控制9. intentional misrepresentations being made to the CPA 故意对注册会计师作出错误的陈述10. written representation 管理当局声明11. the suspected noncompliance 涉嫌存在违法行为12. audit committee ——a committee of a corporation's board of that engages independent auditors, reviews audit findings monitors activities of the internal staff, and intervenes in any disputes between management and the independent auditors. Preferably, members of the audit committee are directors, that is, members of the board of directors who do not also serve as corporate officers. 审计委员会13. supervisory board 监事会14. regulatory and enforcement authorities 监管和执法部门Audit materiality【key words and phrases】1. materiality ——the seriousness of misstatements or omissions in the entity's financial statements. The degree of the seriousness may affect the judgement or decisions made by users of financial statements in certain specific circumstances. 重要性2. exceed the materiality level 超过重要性水平3. approach the materiality level 接近重要性水平4. an acceptably low level 可接受水平5. the overall financial statement level and in related account balances and transaction levels 会计报表层面和相关账户、交易层面6. misstatement or omissions 错报或漏报7. the detected but uncorrected misstatements or omissions 已发现但尚未调整的错报或漏报8. the detected and the projected misstatements or omissions 已发现的和推断的错报或漏报9. aggregate 总计、合计10. subsequent events —— both events occurring between the balance sheet date andthe date of the audit report and events occurring between the date of the audit report and the date the financial statements are issued, which have an impact on the financial statements. 期后事项11. contingencies 或有事项12. extend the scope of the substantive test 扩大实质性测试范围13. adjust the financial statements 调整会计报表14. perform additional audit procedures 实施追加的审计程序15. carry out extended or additional tests of control 实施扩大或追加的控制测试16. modify the nature, timing and extent of planned substantive procedures. 修改计划的实质性测试程序的性质、时间和范围Audit risk【key words and phrases】1. audit risk ——the risk that the CPA gives an inappropriate audit opinion when the fianncial statements are materially misstated. Audit risk has three components: inherent risk, control risk and detection risk 审计风险2. inherent risk —— the susceptibility of an account balance or class of transactions to misstatement that could be material, individually or when aggregated with misstatements in other balances or classes, assuming that there were no related internal controls. 固有风险3. control risk ——the risk that a misstatement, that could occur in an account balance or class of transactions and that could be material individually or when aggregated with misstatements in other balances or classes, will not be prevented or detected and corrected on a timely basis by the accounting and internal control systems. 控制风险4. detection risk —— the risk that an CPA's substantive procedures will not detect a misstatement that exists in an account balance or class of transactions that could be material, individually or when aggregated with misstatements in other balances or classes. 检查风险5. an acceptably low level 可接受的低水平6. inappropriate audit opinion 不适当的审计意见7. material misstatement 重大的错报8. analytical procedures risk 分析性测试风险9. substantive tests of the detail risk 实质性测试风险10. tolerable misstatement 可容忍误差11. the combined level of inherent and control risks 固有风险和控制风险的综合水平12. the acceptable level of detection risk 可接受的检查风险13. planned assessed level of control risk ——the level of control risk auditor uses in developing a preliminary audit strategy which includes an appropriate combination of tests of controls and substantive tests. 控制风险的评估水平14. small business ——a business that has a low level of turnover or of total assets, few employees and limited segregation of duties. 小规模企业Internal control【key words and phrases】1. accounting system ——the series of tasks and records of an entity by which transactions are processed as a means of maintaining financial records. Such systems identify, assemble, analyze, calculate, classify, record, summarize and report transactions and other events.2. internal control system ——all the policies and procedures (internal controls) adopted by the management of an entity to assist in achieving management's objective of ensuring, as far as practicable, the orderly and efficient conduct of its business, including adherence to management policies, the safeguarding of assets, the prevention and detection of fraud and error, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information.3. control environment —— the overall attitude, awareness and actions of directors and management regarding the internal control system and its importance in the entity.4. control procedures ——those policies and procedures in addition to control environment which management has established to achieve the entity's specific objectives.5. compliance test6. test of control ——tests directed toward the design or operation of a control to assess its effectiveness in preventing or detecting material misstatements of financial statement assertions.7. walk-through test ——a test of the accuracy and completeness of the CPAs' working paper description of internal control. A walk-through is performed by tracing several transactions through each step of the related transaction cycle, noting whether the sequence of procedures actually performed corresponds to that described in the audit working papers.8. management letter —— a report to management containing the written recommendations made by the CPA with respect to material internal control weaknesses identified during the audit, which may result in material misstatements or omissions in the entity's financial statements9. material weakness in internal control —— a reportable condition in which the risk that material errors or irregularities might occur and not be detected.10. risk assessment —— the identification, analysis, and management of risk relevant to the preparation of financial statements that are fairly presented.11. control activities —— the policies and procedures that help ensure that necessary actions are taken to address the risks involve in the achievement of the entity's objectives.12. information —— the information system relevant to financial reporting objectives, which includes the accounting system, consists of methods and records established to record, process, summarize, and report an entity's transactions and to maintain accountability for the related assets and liabilities.13. communication ——communication involves providing an understanding of individual roles and responsibilities pertaining to internal control over financialreporting.14. monitoring ——monitoring is a process that assesses the quality of internal control over time.15. procedures manual16. job descriptions17. flow chart —— a graphic representation of the major steps and logic of a system or a series of procedures.18. written narrative ——memoranda that describe the flow of transaction cycles, identifying the employees performing various tasks, documents prepared, records maintained, and the division of duties. Written narratives are more flexible than questionnaires, but by themselves are practical only for describing relatively small, simply systems.19. questionnaire —— questionnaires are usually designed to describe internal control in audit working papers so that "no" answers prominently identify weaknesses in internal control.20. reperformance of internal control21. computer-assisted audit techniques22. communication with management —— a CPA's enquiring or informing the entity's management of matters relevant to the audit of financial statements or discussing such matters with the entity's management.Audit evidence【key words and phrases】1. audit evidence ——the information obtained by the CPA in arriving at the conclusions on which the audit opinions is based. 审计证据21. enquiry —— enquiry consists of the CPA questioning the relevant staff in written form of orally. 询问22. confirmation ——confirmation consists of the CPA's written correspondence with third parties to corroborate information contained in the entity's accounting records. 函证23. computation ——computation consists of the CPA checking the arithmetical accuracy of the data in the entity’s source documents and accounting records, or of the CPA performing independent calculations. 计算24. analytical procedures ——analytical procedures consist of the CPA analyzing material ratios or trends, including the investigation of unusual fluctuations and their differences from the expected amounts and relevant information. 分析性程序25. vouch ——to verify the accuracy and authenticity of entries in the accounting records by examining the original source documents supporting the entries. 核对26. aged trial balance —— a listing of individual customers’accounts classified by the number of days subsequent to billing, that is, age, serves as a preliminary step in estimating the collectibles of accounts receivable. 账龄分析表27. trace —— the direction of testing is from selecting an accounting transaction( a source document) to the journal or ledger. 追查Audit sampling【key words and phrases】1.audit sampling —— the CPA’s performance of tests on certain number of sampleitems selected from the population when the CPA performs the audit procedures.The CPA then projects the characteristics of the population based on the results of the tests. 审计抽样2.error ——either control deviations, when performing tests of control, ormisstatements, when performing substantive procedures. Similarly, total error is used to mean either the rate of deviation or total misstatement. 误差3.anomalous error ——an error that arises from an isolated event that has notrecurred other than on specifically identifiable occasions and is therefore not representative of errors in the population. 偶发性误差4.expected error —— the error that the CPA expects to present in the population.预期误差5.population —— the entire set of data from which a sample is selected and aboutwhich the CPA wishes to draw conclusions. For example, all of the items in an account balance or a class of transactions constitute a population. A population may be divided into strata, or sub-populations, with each stratum being examined separately. The term population is used to include the term stratum. 总体6.sampling risk —— arises from the possibility that the CPA’s conclusion, based ona sample may be different from the conclusion reached if the entire populationwere subjected to the same audit procedures. 抽样风险7.non-sampling risk ——arises from factors that cause the CPA to reach anerroneous conclusion for any reason not related to the size of the sample. For example, most audit evidence is persuasive rather than conclusive, the CPA might use inappropriate procedures, or the CPA might misinterpret evidence and fail to recognize an error. 非抽样风险8.sampling unit ——the individual items constituting a population, for examplechecks listed on deposit slips, credit entries on bank statements, sales invoices or debtor s’ balances, or a monetary unit. 抽样单位9.statistical sampling ——any approach to sampling that has the followingcharacteristics: (1)random selection of a sample; and (2)use of probability theory to evaluate sample results, including measurement of sampling risk. 统计抽样A sampling approach that does not have characteristics (1) and (2) isconsidered non-statistical sampling. (非统计抽样)10.stratification —— the process of dividing a population into subpopulations, eachof which is a group of sampling units which have similar characteristics (often monetary) 分层11.tolerable error —— the maximum error in population that the CPA is willing toaccept. 可容忍误差12.the risk of under reliance ——because of the sample result, the CPA does notadequately rely on the internal controls which could actually be relied upon. 信赖不足风险13.the risk of over reliance —— because of the sample result, the reliance the CPAplaces on the internal controls exceeds the reliance exceeds the reliance that should actually be placed on them. 信赖过度风险14.the risk of incorrect rejection ——although the sample result supports theconclusion that an account balance is materially misstated, in fact it is not materially misstated. 误拒风险15.the risk of incorrect acceptance ——although the sample result supports theconclusion that an account balance is not materially misstated, in fact it is materially misstated. 误受风险16.the rate of deviation 偏离程度17.sample size 样本量18.required confidence level 可信赖水平19.the number of sampling units in the population 总体中样本单位的数量20.methods used 所选用的方法21.effective audit —— an audit that achieves the planned degree of effectiveness indetecting any material misstatement in the client’s financial statements. 审计效果22.efficient audit —— an effective audit that is performed at the lowest possible cost.审计效率Audit working papers【key words and phrases】1.audit working papers (documentation) ——the audit working records andmaterials prepared, or obtained, by CPA in connection with the performance of the audit. 审计工作底稿2.working trial balance ——the working trial balance links the amounts in thefinancial statements to the audit working papers. It contains columns for working paper references, the prior year’s balance, the unadjusted current-year balances, and columns for adjusting and reclassification entries. 试算平衡表3.adjusting and reclassification entries ——adjusting entries are made to correcterrors in the client’s records. Reclassification entries are made to provide proper presentation of information on the financial statements. Adjusting entries are posted in both the client’s records and the working trial balance. Reclassification entries are not posted to the client’s records. 调整和重分类分录4.audit mark —— CPAs use audit marks as a way of documenting work performed.Audit mark is typically explained or defined at the bottom of the working paper, although many firms use a standard set of audit marks. 审计标识5.indexing and cross-referencing ——this process of indexing andcross-referencing provides a trail from the financial statements to the individual working papers that a reviewer can easily follow. 索引和交叉索引6.permanent audit files —— those audit files which contain information that is notfrequently changed and is referred to cover a long period of time. They also contain information of continuing relevance to, or with a direct impact on, succeeding audits. 永久性档案7.current audit files ——those audit files, the contents of which vary frequently.They are primarily used for the audit of the current period and for reference in thenext subsequent period. 当期档案prehensive working papers —— audit working papers prepared by the CPAduring the audit planning and reporting states. They are used for planning, controlling and concluding the audit engagement as a whole and for documenting the audit opinion. 综合类工作底稿9.audit-oriented working papers ——audit working papers prepared by the CPAregarding his performance of specific audit procedures during the audit implementation stage. 业务性工作底稿10.reference working papers —— the audit working papers used merely for referencewhich are prepared by the CPA in the course of the audit. 备查类工作底稿11.the use of standardized working papers 使用标准的工作底稿12.checklists 核对用清单Audit reporting【key words and phrases】1.audit report —— the written document which expresses the CPA’s audit opinionon the entity’s annual financial statements, following the performance of the necessary audit procedures in accordance with the requirements of the Independent Auditing Standards. 审计报告2.the truthfulness of the audit report ——the requirement that the audit reportshould objectively reflect the CPA’s scope and basis of the audit, the audit procedures performed and the audit opinion that should be expressed. 审计报告的真实性3.the legitimacy of the audit report ——the requirement that the preparation andissuance of the audit report should be in accordance with the requirements of both the Law of PRC on CPA and the Independent Auditing Standards. 审计报告的合法性4.entity —— an enterprise, or an institution managed on a commercial basis, whichis responsible for the preparation and submission of financial statements and audited by the CPA. 被审计单位,客户5.addressee of the audit report ——the client of the audit engagement. The fullname of the addressee should be stated in the audit report. 审计报告的收件人6.unqualified opinion ——an unqualified opinion should be expressed when theCPA concludes that。

审计词汇英汉对照

审计词汇英汉对照Aability to continue as a going concern持续经营能力acceptability 可接受性,可接受程度acceptable level of detection risk检查风险的可接受水平acceptance of engagement接受委托accepting the engagement for the first time 首次接受委托access to asset对资产的接触[·ækses]according to 根据,依据,依照account balance 账户余额account for 对……进行会计处理,核算;解释accounting 会计,会计学accounting advisory serve 会计咨询服务[əd·vaizəri] accounting firm 会计师事务所accounting information 会计信息,会计资料accounting period 会计期间accounting policies会计政策accounting professional bodies 会计职业组织,会计职业团体accounting records 会计记录accounting responsibility会计责任accounting service 会计服务accounting standards 会计准则Accounting Standards for Business Enterprises企业会计准则accounting system 会计系统accounting treatment 会计处理accuracy准确性,精确性additional audit procedures 追加审计程序addressee 收件人,收信人Administration of State-owned Assets (the~)国有资产管理局administrative laws and regulations行政法规adverse impact 不利影响,负面影响[·ædvə:s]adverse opinion反对意见(否定意见)advisory group 咨询组,顾问组agency fee代理费,代理费用aggregate 总计,合计为……alternation of document and record变造文件和记录alternative audit procedures 替代审计程序,备选审计程序amend 修改,修订amortisation 摊销analytical capacity 分析能力analytical procedures 分析性程序annual financial statements年度会计报表,年度财务报表appendix附录,附表applicable 适用的applicable laws and regulations适用的法规application systems应用系统apply consistently 一贯地执行,一贯地实施appropriate适当的,合适的;appropriate authorization适当的授权appropriateness of audit evidence 审计证据的适当性approval批准,核准[ə·pru:vəl]assessed level of control risk 对控制风险的评估,控制风险的评估水平asset资产,财产asset restructuring 资产重组assignment of duties 职责的划分assistant 助理,助理人员associated company 联属公司,联营公司association 联合,结合;协会,社团assumption假设,假定at a given date在某一特定时日attestation 鉴证,公证attestation service鉴证服务audit adjustment审计调整audit areas 审计领域audit conclusion 审计结论audit effectiveness 审计效果audit efficiency 审计效率audit engagement letter 审计业务约定书audit evidence 审计证据audit fee审计费audit files审计档案audit findings审计中发现的事项audit implementation stage审计实施阶段audit mark审计标识audit materiality 审计重要性audit method 审计方法audit objective审计目标,审计目的audit of financial statements 会计报表审计,财务报表审计audit opinion审计意见audit period被审计期间,被审计年度audit plan 审计计划audit planning 编制审计计划,制定审计计划,审计计划audit planning stage审计计划阶段audit procedure审计程序audit programme 审计程序表,具体审计计划audit report审计报告audit report with a disclaimer of opinion拒绝表示意见审计报告audit report with a qualified opinion 有保留意见的审计报告audit report with an adverse opinion 否定意见的审计报告audit report with dual dates双重日期审计报告audit reporting stage 审计报告阶段audit responsibility 审计责任audit results审计结果audit risk审计风险audit sampling审计抽样audit sampling techniques 审计抽样方法,审计抽样技术audit strategies审计策略audit summary审计总结,审计小结audit team 审计小组audit test审计测试audit trail 审计轨迹audit work审计工作audit working paper审计工作底稿audited financial statement 审计会计报表,已审计财务报表Auditing Guidelines (the~)审计规X指南auditing standards 审计准则audit-oriented working paper (审计)业务类工作底稿authorisation 授权authorisation of transaction 交易的授权availability 可获得性Bbalance余额;差额;平衡balance sheet 资产负债表bank 银行bank account 银行账户,银行户头bank statement 银行对账单barter transaction易货交易,以物换物交易basis of audit 审计依据basis of preparation (会计报表的)编制基础book of account账目,账簿borrowing 借款,贷款,借债branch分支,分支机构,分店brought forward (账户余额等的)承上年,承上期,承上页budget预算building 建筑物;大楼business conditions 业务情况,经营情况business licence (企业等的)营业执照business relation 业务关系。

审计英语课件第4章

accounting standards; and

(b) Whether the financial statements are presented fairly,

in all material respects, the financial position, operating

results and cash flows of the entity.

精选ppt

11

3.1.3 Auditor’s Responsibilities

➢ An auditor has a responsibility to plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, which caused by error or fraud. Due to the nature of the audit evidence and the characteristics of fraud, the auditor is able to obtain reasonable, but not absolute, assurance that material misstatements are detected. The auditor has no responsibility to plan and perform the audit to obtain reasonable assurance those misstatements, which caused by errors or fraud, that are not material to the financial statements are detected.

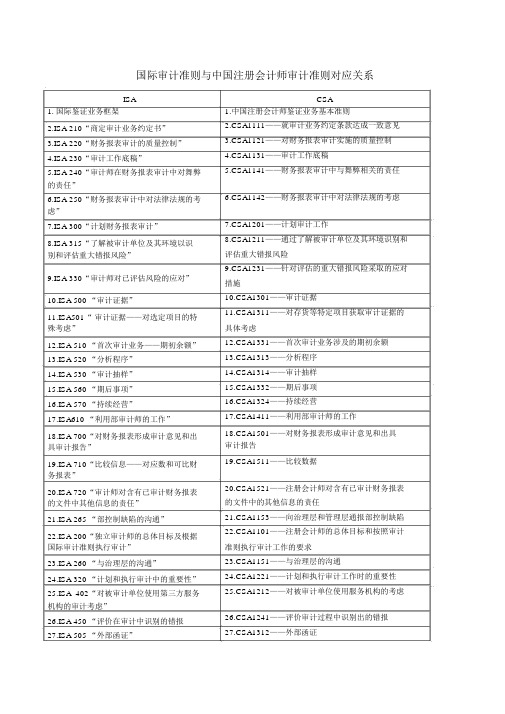

国际审计准则与中国注册会计师审计准则对应关系

国际审计准则与中国注册会计师审计准则对应关系ISA1.国际鉴证业务框架2.ISA 210“商定审计业务约定书”3.ISA 220“财务报表审计的质量控制”4.ISA 230“审计工作底稿”5.ISA 240“审计师在财务报表审计中对舞弊的责任”6.ISA 250“财务报表审计中对法律法规的考虑”7.ISA 300“计划财务报表审计”8.ISA 315“了解被审计单位及其环境以识别和评估重大错报风险”9.ISA 330“审计师对已评估风险的应对”10.ISA 500 “审计证据”11.ISA501“审计证据——对选定项目的特殊考虑”12.ISA 510 “首次审计业务——期初余额”13.ISA 520 “分析程序”14.ISA 530 “审计抽样”15.ISA 560 “期后事项”16.ISA 570 “持续经营”17.ISA610 “利用部审计师的工作”18.ISA 700“对财务报表形成审计意见和出具审计报告”19.ISA 710“比较信息——对应数和可比财务报表”20.ISA 720“审计师对含有已审计财务报表的文件中其他信息的责任”21.ISA 265 “部控制缺陷的沟通”22.ISA 200“独立审计师的总体目标及根据国际审计准则执行审计”23.ISA 260 “与治理层的沟通”24.ISA 320 “计划和执行审计中的重要性”25.ISA 402“对被审计单位使用第三方服务机构的审计考虑”26.ISA 450 “评价在审计中识别的错报27.ISA 505 “外部函证”CSA1.中国注册会计师鉴证业务基本准则2.CSA1111——就审计业务约定条款达成一致意见3.CSA1121——对财务报表审计实施的质量控制4.CSA1131——审计工作底稿5.CSA1141——财务报表审计中与舞弊相关的责任6.CSA1142——财务报表审计中对法律法规的考虑7.CSA1201——计划审计工作8.CSA1211——通过了解被审计单位及其环境识别和评估重大错报风险9.CSA1231——针对评估的重大错报风险采取的应对措施10.CSA1301——审计证据11.CSA1311——对存货等特定项目获取审计证据的具体考虑12.CSA1331——首次审计业务涉及的期初余额13.CSA1313——分析程序14.CSA1314——审计抽样15.CSA1332——期后事项16.CSA1324——持续经营17.CSA1411——利用部审计师的工作18.CSA1501——对财务报表形成审计意见和出具审计报告19.CSA1511——比较数据20.CSA1521——注册会计师对含有已审计财务报表的文件中的其他信息的责任21.CSA1153——向治理层和管理层通报部控制缺陷22.CSA1101——注册会计师的总体目标和按照审计准则执行审计工作的要求23.CSA1151——与治理层的沟通24.CSA1221——计划和执行审计工作时的重要性25.CSA1212——对被审计单位使用服务机构的考虑26.CSA1241——评价审计过程中识别出的错报27.CSA1312——外部函证28.ISA540“审计会计估计和相关披露,包括公允价值会计估计”29.ISA 550 “关联方”30.ISA 580 “书面声明书”31.ISA600 “对集团财务报表审计的特殊考虑,包括组成部分审计师的工作”32.ISA 620 “利用审计师的专家的工作”33.ISA 705 “对独立审计报告意见的修改”34.ISA 706“独立审计报告中的强调事项段和其他事项段”35.ISA 800“对按照特殊目的框架编制的财务报表审计的特殊考虑”36.ISA 805“对单个财务报表和财务报表的特定要素、账户或项目审计的特殊考虑” 37.ISA 810 “对简要财务报表出具报告”38.IAPS1000 银行间函证程序39.IAPS1004 银行监管机构与银行外部审计师的关系40.IAPS1006 银行财务报表审计41.IAPS1010 财务报表审计中对环境的考虑42.IAPS1012 衍生金融工具审计43.IAPS1013 电子商务对财务报表审计的影响44.ISRE2400 财务报表审阅45.ISRE2410 由被审计单位独立审计师执行的中期财务信息审阅46.ISAE3000 历史财务信息审计或审阅以外的鉴证业务47.ISAE3400预测性财务信息的审核48.ISAE3402 对第三方服务机构的控制提供鉴证报告49.ISRS4400 对财务信息执行商定程序28.CSA1321——审计会计估计(包括公允价值会计估计)和相关披露29.CSA1323——关联方30.CSA1341——书面声明31.CSA1401——对集团财务报表审计的特殊考虑32.CSA1421——利用专家的工作33.CSA1502——在审计报告中发表非无保留意见34.CSA1503——在审计报告中增加强调事项段和其他事项段35.CSA1601——对按照特殊目的框架编制的财务报表审计的特殊考虑36.CSA1603——对单一财务报表和财务报表的特定要素、账户或项目审计时的特殊考虑37.CSA1604——对简要财务报表出具报告的业务38.CSA1152——前后任注册会计师的沟通39.CSA1602——验资40.中国注册会计师审计准则第1612 号——银行间函证程序41.中国注册会计师审计准则第1613 号——与银行监管机构的关系42.中国注册会计师审计准则第1611 号——商业银行财务报表审计43.中国注册会计师审计准则第1631 号——财务报表审计中对环境事项的考虑44.中国注册会计师审计准则第1632 号——衍生金融工具的审计45.中国注册会计师审计准则第1633 号——电子商务对财务报表审计的影响46.中国注册会计师审阅准则第2101 号——财务报表审阅无47.中国注册会计师其他鉴证业务准则第3101 号——历史财务信息审计或审阅以外的鉴证业务48.中国注册会计师其他鉴证业务准则第3111 号——预测性财务信息的审核无49. 中国注册会计师相关服务准则第4101 号50.ISRS4410 代编财务信息——对财务信息执行商定程序50.中国注册会计师相关服务准则第 4111 号——代编财务信息51.ISQC 1“会计师事务所执行财务报表审计51. 质量控制准则第5101 号——会计师事务所对执和审阅、其他鉴证业务和相关服务的质量控行财务报表审计和审阅、其他鉴证和相关服务业务实制”施的质量控制国际鉴证业务准则:具体包括 1 项国际鉴证业务框架、36 项审计准则、6 个审计实务公告、 2 项审阅准则、 3 项其他鉴证业务准则、 2 项相关服务准则和 1 项会计师事务所质量控制准则。

审计专业词汇中英对照

audit evidence 审计证据audit program 审计方案audit procedures 审计程序competence 适当性sufficiency 充分性combined effect 联合效应persuasiveness 说服力relevance 相关性effectiveness 有效性objectivity 客观性timeliness 及时性physical evidence 实物证据confirmation evidence 函证证据documentation evidence 书面证据analytical procedures 分析程序获得的数据inquires of the client 询问客户获得的证据reperformance evidence 重新执行获得的证据observation evidence 观察获得的证据auditing standards 审计准则sample size 样本规模accounts receivable 应收账款notes receivable 应收票据liabilities 负债advances from customers 客户预付款mortgages payable 应付抵押账款bonds payable 应付债券owners’ equity 所有者权益creditor 债权人lender 借款人mortgagor 抵押人bondholder 债券持有人shares outstanding 发行在外股份contingent liabilities 或有负债examine 检查scan 浏览read 阅读recomputed 重新计算foot 加总trace 追查compare 比较count 盘点observe 观察inquire 询问vouch 核对audit documentation 审计档案audit files 审计文件audit working papers 审计工作底稿interest receivable 应收利息permanent files 永久文件working trial balance 试算平衡草稿adjusting and reclassification entries 调整分录及重分类分录supporting schedules 支持性档案cash count sheet 现金盘点表bank reconciliation 银行存款余额调节表trial balance/list 试算平衡表(列表)reconciliation of amounts 金额调节表acceptable audit risk 可接受审计风险inherent risk 固有风险business risk 经营风险analytical procedures 分析程序materiality 重要性水平control risk 控制风险fraud risks 舞弊风险directors 董事会the audit committee 审计委员会corporate charter and bylaws 公司章程与规章meeting minutes 会议记录material misstatements 重大错报enterprise risk management 企业风险管理short-term debate-paying ability 短期偿债能力current ratio 流动比率liquidity activity ratio 流动性比率inventory turnover 存货周转率long-term obligation 长期义务debt to equity 债务权益比profitability ratio 盈利能力比率profit margin 利润率planning phase 计划阶段going concern 持续经营能detailed test 细节测试testing phase 测试阶段completion 完成阶段gross margin 毛利率cash ratio 现金比率quick ratio 速动比率accounts receivable turnover 应收账款周转率debt to equity 债务权益比times interest earned 利息赚取倍数planning extent of planning 计划测试的范围evaluating results 评价结果bases 基数qualitative factors 定性的因素planned detection risk 计划的检查风险engagement risk 业务风险related parties 关联方the overall audit 审计整体tolerable misstatement 可容忍错报detection risk 检查风险management’s responsibility 管理层的责任inherent limitations 固有局限existence 存在性completeness 完整性accuracy 准确性classification 分类timing 及时性posting 过账summarization 汇总risk assessment 风险评估control activities 控制活动information and communication 信息与沟通monitoring 监控initiate 发起process 处理assess control risk 评估控制风险test control 控制测试substantive tests 实质性测试potential material misstatements 潜在的重大错报narrative 文字表述flowchart 流程图internal control questionnaire 内部控制调查表compensating controls 替代性测试management letters 管理层建议书reperform 重新执行walking-through 穿行测试sampling 抽样general control 一般控制application control 应用控制input controls 输入控制processing controls 处理控制pilot testing 引导测试parallel testing 并行测试batch input controls 批输入控制financial total 数值总额控制hash total 无用数据总和控制record count 记录数目控制validation test 有效性检验sequence test 顺序校验arithmetic accuracy test 算数准确性校验data reasonableness test 数据合理性校验completeness test 完整性校验。

英文版审计委托书格式

英文版审计委托书格式以下是审计委托书的英文格式:[Your Name][Your Title][Your Address][City, State, ZIP Code][Email Address][Phone Number][Date][Client Name][Client Title][Client Address][City, State, ZIP Code]Subject: Engagement Letter for Audit ServicesDear [Client Name],We are pleased to confirm our agreement to perform an audit of the financial statements of [Client Name] for the fiscal year ended [End Date], in accordance with generally accepted auditing standards (GAAS).Our audit will be conducted to express an opinion on the fairness of the financial statements as of [End Date] and for the entire fiscal year. The scope of our audit will include examining the supporting documents, making inquiries, and performing other audit procedures as deemed necessary to obtain a reasonable assuranceabout the financial statements.The responsibilities of [Client Name] will include providing us with access to all necessary financial records, books, and supporting documentation. You will also provide us with all relevant information, including any changes to accounting principles or policies, transactions, or events that occurred during the fiscal year under audit.Our responsibilities as auditors will include planning and conducting the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. We will perform our audit in accordance with GAAS and provide you with a report containing our findings, including any identified material weaknesses or significant deficiencies in internal controls, if applicable.Our fees for this engagement will be based on the estimated level of effort required to complete the audit. We will provide you with a detailed fee estimate once we have completed our initial planning and scoping procedures.This engagement letter will remain effective for future fiscal years unless terminated by either party upon 30 days' written notice.If you agree with the terms outlined in this letter, please sign and return a copy of this letter to us. Should you require any further clarification or have any questions, please do not hesitate to contact me.We look forward to working with you and providing a successful audit for [Client Name].Sincerely,[Your Name][Your Title][Your Company Name]。

Auditing(审计)

Section 1Supply the missing information in the following in the following statement.1.Auditing is a process based on logic and reasoning.2.In the audit of financial statements prepared by a company, the established criteria aregenerally accepted principles.3.In the audit ,the auditor gives an opinion as to whether the assertions arereported in accordance with the established criteria.4.Auditing involves the results of the audit to the interested users.5.auditing, auditing,and auditing all serve differentobjectives.6.The of internal auditing is to assist members of the organization in the effectivedischarge of their responsibilities.7.External auditing involves reporting on financial statements prepared by management forusers or parties.8.External Audits are performed by independent firms.9.is the backbone of the external auditing.10.Stockholders desire audits to determine management’s of their assets.Section 21. Supply the missing information in the following in the following statement.(1)If there was a previous audit ,inquires must be made of the auditor.(2)An engagement letter is the audit that describes the responsibilities of theauditor and the client.(3) A review of the client’s system of internal control is a step in very auditengagement.(4) A compliance test measures the of a particular control procedure.(5)Auditors should make an intensive investigation in areas for which internal controlis .(6)When serious deficiencies in internal control are discovered ,the auditors should issue aletter to the client.(7)Tests designed to substantiate the fairness of a special financial statement item are termedtests.(8)If the auditors are to issue anything other than an opinion of standard form ,considerable care must go into the precise wording of the audit report.2. Which information should be included in an engagement letter? of the client and its year-end dateb.financial statement to be examined and other reports to be preparedc.the audit fee and the manner of paymentd.the type of opinion expected to be issued as a result of the audit worke.the auditor’s responsibility for the detection on errors and irregularitiesf.obligations of the client’s staff to prepare schedules and statements and assist in other aspectsof the audit work.g.identification of any limitations imposed by the client or the timing of the engagement thatmay affect the auditor’s ability to gather sufficient competent evidential matter in support of the financial statementsSection 31. Supply the missing information in the following statements.(1)The standard report consists of a scope paragraph and an paragraph.(2)There are four types of audit reports. They are the unqualified opinion report, the qualifiedopinion report, the opinion report and the of opinion report.(3)When a disclaimer of opinion is issued, the auditor’s report must disclose all of thereasons for the disclaimer.2. Choose the best answer.An auditor may issue report when he or she has reached the following conclusion: 1) The financial statements present fairly overall financial position, results of operations, and changes in financial position in conformity with GAAP or other comprehensive basis of accounting. 2) GAAP or the other comprehensive basis of accounting applied on a basis consistent with that of the proceeding period. 3) The financial statements have adequate information disclosure.A.an unqualified opinionB. a qualified opinionC.an adverse opinionD. a disclaimer of opinion3. Choose the best answer.An auditor may issue report when he or she has reached the conclusion that the financial statements present fairly overall in conformity with GAAP or other comprehensive basis of accounting, but there is an exception regarding a material item:1) The scope of the auditor’s examination was restricted by the circumstances of the engagement, condition of the client’s records, or other reasons.2) There is material uncertainty regarding the statements.3) Disclosure is lacking.4) An accounting principle or the method of its application is not in conformity with GAAP.5) Accounting principles followed in the current period are not consistent with those in the proceeding period.A.an unqualified opinionB. a qualified opinionC.an adverse opinionD. a disclaimer of opinion4. Choose the best answer.When the restriction on the auditor’s ability to gather to gather evidence is so pervasive that the auditor can’t support an overall opinion on the financial statement, is issued.A.an unqualified opinionB. a qualified opinionC.an adverse opinionD. a disclaimer of opinion5. Choose the best answer.is issued for scope restriction relating to a material item which is not so pervasive as to impair the ability to issue an overall opinion on the financial statements.A.An unqualified opinionB. A qualified opinionC.An adverse opinionD. A disclaimer of opinion6. Choose the best answer.Which of the following reasons can make an auditor issue a disclaimer of opinion?A.The auditor is unable to apply procedures deemed necessary in an audit engagement and theeffect is so pervasive that a qualified opinion is not appropriate.B.An uncertainty regarding the financial statements is so pervasive that a qualified opinion isnot appropriate.C.The auditor has not audited the financial statements.D.The financial statements have adequate information disclosure.。

会计师事务所审计报告备案管理暂行办法

会计师事务所审计报告备案管理暂行办法The Interim Measures for the Management of Filing of Audit Reports by Certified Public Accountants' FirmsThe Interim Measures for the Management of Filing of Audit Reports by Certified Public Accountants’ Firms, also known as the Measures, were introduced in order to strengthen regulation and supervision over audit reports filed by certified public accountants' firms. The Measures outline the requirements and procedures for filing audit reports with regulatory authorities.这项名为《会计师事务所审计报告备案管理暂行办法》的规定旨在加强对会计师事务所申报审计报告的监管。

该办法概述了向监管机构备案审计报告的要求和程序。

According to these Measures, all certified public accountants' firms are required to file their audit reports with the competent regulatory authority within a specified period after completion of the audit engagement. The regulatory authority will review and verify theauthenticity and accuracy of the filed audit reports.根据这些规定,所有会计师事务所都必须在完成审计工作后的一定期限内向主管监管机构备案审计报告。

AICPA常见问题

AICPA常见问题报考美国CPA的学历要求目前美国50多个州都要求达到本科及以上学历。

但是个别州在学历上的要求相对降低,比如特拉华州和伊利诺伊州的最低学历为专科,佛蒙特州在最低学历要求上没有特别的限制。

所以考生在选州时需要根据自己的学历进行选择。

如果是中国认可的大学所颁发的自考本科或是成人教育所获得的本科文凭,也可以申请多数要求本科学历的州,但是有一些州是不承认自学或是远程获得的学历。

报考美国CPA时的学历认证一般需要约2-6周,要求将申请表、美金汇票、密封成绩单学历寄给FACS (Foreign Academic Credentials Service)或其他申请州可以接受的教育评估机构。

报考前是否需要有实习?美国CPA考试不像许多其它国家的CPA应考要求,美国CPA的外国应考者不必于考试时就具会计相关工作经验,也无实习要求;任何相关工作经验都可在你通过考试后再取得即可。

学历评估需要多长时间?考试申请审核需要多久?一般在1个半月到两个月左右。

缅因州学历认证时间较短,在一个到一个半月左右。

考试申请审核时间一般在1个到一个半月左右。

但是缅因州和关岛审核时间也较短,最快可在7-20天收到NTS。

学历材料可以自己寄吗?还是必须是学校寄出?只要是学校敲章的密封件,可以自己寄出考试举行时间?美国CPA考试为机考(CBT),一年按照四个季度分为四个Test window开放考试,除了每年的3、6、9、12月不能考以外其他每个月都能考试。

其中要注意的是考试时间不能是美国国家假日,同时每一周周日是不开放考试的。

考试申请步骤?报考分为六大步骤:第一、决定你要报考和申请的州/管辖区;第二、检阅标准CPA公告;第三、申请学历及成绩认证;第四、申请考试;第五、填写并提出申请表格,完成付费;第六、安排考试时间。

学历评估需要多长时间?考试申请审核需要多久?一般在1个半月到两个月左右。

缅因州学历认证时间较短,在一个到一个半月左右。