AP-353.1 Inbound Invoice Postings (CARATS)

SAP中过账码和记账码

SAP中过账码和记账码是指同一个事物。

在实际业务中,记账码就是只有“借”和“贷”,而SAP中Posting Code肩负着更多的任务:1)界定科目类型,2)借贷方向,3)凭证输入时画面上的字段的输入状态。

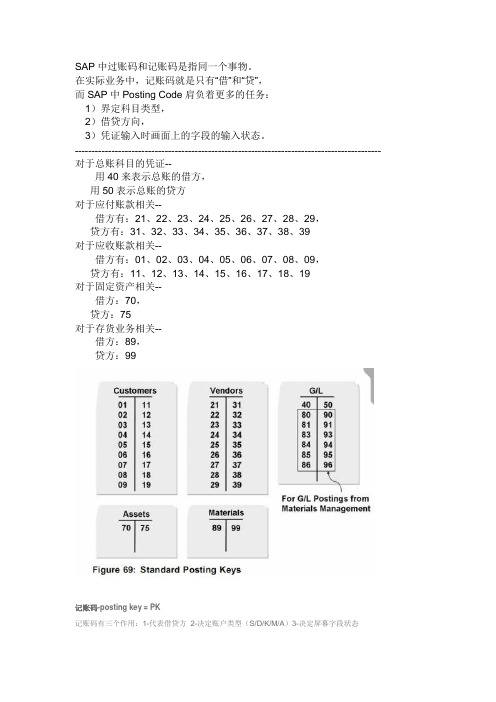

-------------------------------------------------------------------------------------------- 对于总账科目的凭证--用40来表示总账的借方,用50表示总账的贷方对于应付账款相关--借方有:21、22、23、24、25、26、27、28、29,贷方有:31、32、33、34、35、36、37、38、39对于应收账款相关--借方有:01、02、03、04、05、06、07、08、09,贷方有:11、12、13、14、15、16、17、18、19对于固定资产相关--借方:70,贷方:75对于存货业务相关--借方:89,贷方:99记账码-posting key = PK记账码有三个作用:1-代表借贷方2-决定账户类型(S/D/K/M/A)3-决定屏幕字段状态记帐码/Posting Key在手工的会计核算过程中,我们通过用记帐符号“debit”与“credit”来描述资产、负债的增、减。

但在SAP中,却变得有些复杂了。

客户D对于与应收帐款有关的,其应收帐款的debitcredit所用的记帐码:λ用01、02、03、04、05、06、07、08、09表示debit,λ用11、12、13、14、15、16、17、18、19表示credit,如输入一笔与客户发票有关的分录:01:客户有关的号码50:其他业务收入。

供应商K对于与供应商发票有关的凭证输入,主要与应付帐款有关的debitcredit就比较复杂了,如λ debit用21、22、23、24、25、26、27、28、29,λ credit用31、32、33、34、35、36、37、38、39,如供应商发票输入分录为:40:50100101(营业费用-电费)31:10100037(表示通过主数据创建的供应商编号)。

ABAP-SAP增强应用实例

ABAP-SAP增强应用实例SAP增强应用实例SAP增强大家都很熟悉,在此不再详细讲解,下面只是通过一个实例来展示一下增强的应用。

系统增强实例为建立工单前进行校验,如没有进行标准成本发布则提示错误信息E。

T-code:CMOD通过增强程序我们可以控制相关应用,如果你不知道到底功能是用到的哪个增强,那么请看我附录上的列表。

我们以ppco0006举例如下:如图2.data:begin of l_matnr,matnr like mbew-matnr,VPRSV like mbew-VPRSV,vjvpr like mbew-vjvpr,pprdl like mbew-pprdl,lplpr like mbew-lplpr,end of l_matnr.select single matnr vprsv vjvpr pprdl lplpr from mbew into l_matnrwhere matnr = CAUFVD_IMP-MATNR* and pprdl <> ''* and lplpr <> ''and bwkey = CAUFVD_IMP-WERKS.* and vjvpr = 'S'.if l_matnr-vprsv = 'V'./移动平均价exit.elseif sy-subrc <> 0 or ( l_matnr-pprdl is initial and l_matnr-lplpr is initial ).message e888(sabapdocu) with '物料' CAUFVD_IMP-MATNR'没有做成本估算, 不能创建生产订单,请通知SAP方丈,yeah~~~!'.exit.endif.endif.OK,快去看看你增强后的效果吧~~~~~¥%&%&*(*(SAP所有模块用户出口:用户出口名称短文本描述0VRF0001 客户指定路线确定AAIC0001 IM 总结: 在选择后处理数据AAIC0002 IM 总结: 在选择后处理指定的输入项AAIP0001 IM 追溯: 实际价值对预算类别的分配AAIP0002 IM 追溯: 定义用户定义的指标AAIP0003 IM 追溯: 定义用户定义的特性AAIR0001 IM-IS: 适用请求报表中的用户值字段AAIR0002 IM-FA: 拨款申请的用户字段AAIR0003 IM: 创建拨款申请中的PM 定单时工作场所的分配AAIR0004 IM 追溯: 定义用户定义的特性AAIS0003 投资计量对资产的实际结算AAIS0004 全部计划值或预算值的结算AAPM0001 资产会计和工厂维护的集成ACBAPI01 会计核算: 对BAPI 界面的客户增强功能ACCID001 会计核算的IDoc 过程ACCID002 支出会计的IDoc 处理ACCOBL01 代码块中PAI 和PBO 的客户出口AD010001 更改对象清单及其层次AD010002 定界选择和/或过滤已定数据AD010003 创建自定义动态项目特性AD010005 创建自定义资源AD010006 菜单退出:更改动态项目值AD010007 更改DI 处理信息AFAR0001 External determination of ref. valuefor dep. calculationAFAR0002 External determination of depreciationAFAR0003 外部转换方式AFAR0004 报废比例值的确定AINT0001 当记帐资产时进行扩展的检查AINT0002 出入流水中冲销帐户的替代...AINT0003 定义投资支持再付款的百分比/金额AINT0004 更改某范围已过帐金额AINT0005 虚拟扩展语法检查. 不使用。

国际结算英文术语

国际结算(International settlement)贸易(Trade Settlement)非贸易(Non-Trade Settlement)EDI(Electronic Data Intercharge)电子数据交换,控制文件(Control Documents)有权签字人的印鉴(Specimen Signatures)密押(Test Key)费率表(Terms and Condition)货物单据化,履约证书化,( cargo documentation ,guarantee certification)权利单据(document of title)流通转让性(Negotiability)让与(Assignment)转让(Transfer)流通转让(Negotiation)汇票的定义是:A bill of exchange is an unconditional order in writing, addressed by one person to another,signed by the person giving it,requiring the person to whom it is addressed to pay on demand or at a fixed or determinable future time a sum certain in money to the order or specified person or to bearer。

“汇票” (bill of exchange,exchange或draft)无条件支付命令(unconditional order to pay)出票条款(drawn clause)利息条款(with interest)分期付款(by stated instalment)支付等值其它货币(pay the other currency according to an indicated rate of exchange)付款人(payer)受票人(drawee)付款期限(time of payment)或(tenor)即期(at sight, on demand, on presentation)付款.远期(at a determinable future time ,time/ usance / term bill)付款。

Confirmation 报工

->日期在将来(每次报工时都会过账日期,看到底什么时候过账的,这个日期到底允不允许在后天,在未来?比如31号的提前报工,SPRO->生产->商店底价控制->工序->确认->定义确认参数->PP01(标准的)其中 CO11->人员/附加数据>最后确认下的,除预定”打钩表示最后确认时,假如需求103,其中3个是损耗不管你是否报工;打钩表示预留的不需要了,因为已经完全报工,预留会被清掉。

这里的清除预定跟后台CO01-> 建立并下达订单CO11->报工,输入工序,假如先输入工序0020, 会出现警告信息或者错误信息CO 15:针对订单做确认,而不是像CO11针对工序做确认。

CO12:集中确认。

(批量做确认)confirmation的类型:Milestone confirmation 重大确认1.CO01 ->工序(选中需要设置重大确认的工序)-> 点击控制码 -> 重大确认 ->下达存盘2.CO11->选中上一步你做重大确认的工序->3.CO03 ->工序图标->看状态,可以看到你只对一个工序做了重大确认,但是其他的工序也会自动做成重大确认CO03 ->菜单栏的工序(P)->显示确认,可以看到时间,这里的时间是标准时间计算的。

Progress confirmation 进度确认1.CO01 ->下达存盘2.CO1F:进度确认->第一次报工2个,第二次再去报工1个,产量不能直接输入1,要输入3才能过,因为是累加的形式数量累加,但是时间不是累加的,所以“增量作业”栏目下的“机器”‘工时“的时间还是之前的数字。

反冲 Backflusha.MM01->MRP2, 1 一直反冲 2 工作中心反冲b.CR01->基本数据:反冲a选2 + b 配合起来才是反冲。

CO01建立生产订单时候,看组件物料,可以看到你a选2+b的那颗物料是反冲的。

会计分录英文版

资产类 Assets流动资产 Current assets货币资金 Cash and cash equivalents库存现金 Cash on hand银行存款 Cash in bank其他货币资金 Other cash and cash equivalents外埠存款 Other city Cash in bank银行本票 Cashier's cheque银行汇票 Bank draft信用卡 Credit card信用证保证金 L/C Guarantee deposits存出投资款 Refundable deposits交易性金融资产 Financial assets held for trading短期投资 Short-term investments股票 Short-term investments - stock债券 Short-term investments - corporate bonds基金 Short-term investments - corporate funds其他 Short-term investments - other短期投资跌价准备 Short-term investments falling price reserves应收款 Account receivable应收票据 Note receivable银行承兑汇票 Bank acceptance商业承兑汇票 Trade acceptance 、应收股利 Dividend receivable应收利息 Interest receivable应收账款 Account receivable其他应收款 Other notes receivable坏账准备 Bad debt reserves资产减值损失 Asset impairment loss预付账款 Advance payment应收补贴款 Cover deficit by state subsidies of receivable库存资产 Inventories物资采购 Supplies purchasing原材料 Raw materials包装物 Wrappage低值易耗品 Low-value consumption goods材料成本差异 Materials cost variance自制半成品 Semi-Finished goods在途物资Materials in transport库存商品 Finished goods 商品进销差价 Differences between purchasing and selling price委托加工物资 Work in process - outsourced委托代销商品 Trust to and sell the goods on a commission basis受托代销商品 Commissioned and sell the goods on a commission basis存货跌价准备 Inventory falling price reserves分期收款发出商品 Collect money and send out the goods by stages待摊费用 Deferred and prepaid expenses长期投资 Long-term investment长期股权投资 Long-term investment on stocks股票投资 Investment on stocks其他股权投资 Other investment on stocks长期债权投资 Long-term investment on bonds债券投资 Investment on bonds其他债权投资 Other investment on bonds长期投资减值准备 Long-term investments depreciation reserves股权投资减值准备 Stock rights investment depreciation reserves债权投资减值准备 Bcreditor's rights investment depreciation reserves委托贷款 Entrust loans本金 Principal利息 Interest减值准备 Depreciation reserves固定资产 Fixed assets房屋 Building建筑物 Structure机器设备 Machinery equipment运输设备 Transportation facilities工具器具 Instruments and implement累计折旧 Accumulated depreciation固定资产减值准备 Fixed assets depreciation reserves 房屋、建筑物减值准备 Building/structure depreciation reserves机器设备减值准备 Machinery equipment depreciation reserves工程物资 Project goods and material专用材料 Special-purpose material专用设备 Special-purpose equipment预付大型设备款 Prepayments for equipment为生产准备的工具及器具 Preparative instruments and implement for fabricate在建工程 Construction-in-process安装工程 Erection works在安装设备 Erecting equipment-in-process技术改造工程 Technical innovation project大修理工程 General overhaul project在建工程减值准备 Construction-in-process depreciation reserves固定资产清理 Liquidation of fixed assets无形资产 Intangible assets专利权 Patents非专利技术 Non-Patents商标权 Trademarks, Trade names著作权 Copyrights土地使用权 Tenure商誉 Goodwill无形资产减值准备 Intangible Assets depreciation reserves专利权减值准备 Patent rights depreciation reserves商标权减值准备 trademark rights depreciation reserves 未确认融资费用 Unacknowledged financial charges待处理财产损溢 Wait deal assets loss or income长期待摊费用 Long-term deferred and prepaid expenses待处理财产损溢 Wait deal assets loss or income待处理流动资产损溢 Wait deal intangible assets loss or income待处理固定资产损溢 Wait deal fixed assets loss or income二、负债类 Liability短期负债 Current liability短期借款 Short-term borrowing应付票据 Notes payable银行承兑汇票 Bank acceptance商业承兑汇票 Trade acceptance应付账款 Account payable预收账款 Deposit received代销商品款 Proxy sale goods revenue应付工资 Accrued wages 应付福利费 Accrued welfarism应付股利 Dividends payable应交税金 Tax payable应交增值税 value added tax payable进项税额 Withholdings on VAT已交税金 Paying tax转出未交增值税 Unpaid VAT changeover减免税款 Tax deduction销项税额 Substituted money on VAT出口退税 Tax reimbursement for export进项税额转出 Changeover withnoldings on VAT出口抵减内销产品应纳税额 Export deduct domestic sales goods tax转出多交增值税 Overpaid VAT changeover未交增值税 Unpaid VAT应交营业税 Business tax payable应交消费税 Consumption tax payable应交资源税 Resources tax payable应交所得税 Income tax payable应交土地增值税 Increment tax on land value payable 应交城市维护建设税 Tax for maintaining and building cities payable应交房产税 Housing property tax payable应交土地使用税 Tenure tax payable应交车船使用税 Vehicle and vessel usage license plate tax(VVULPT) payable应交个人所得税 Personal income tax payable其他应交款 Other fund in conformity with paying其他应付款 Other payables预提费用 Drawing expense in advance其他负债 Other liabilities待转资产价值 Pending changerover assets value预计负债 Anticipation liabilities长期负债 Long-term Liabilities长期借款 Long-term loans一年内到期的长期借款 Long-term loans due within one year一年后到期的长期借款 Long-term loans due over one year应付债券 Bonds payable债券面值 Face value, Par value债券溢价 Premium on bonds债券折价 Discount on bonds应收利息 Interest receivable应计利息 Accrued interest长期应付款 Long-term account payable应付融资租赁款 Accrued financial lease outlay一年内到期的长期应付 Long-term account payable due within one year一年后到期的长期应付 Long-term account payable over one year专项应付款 Special payable一年内到期的专项应付 Long-term special payable due within one year一年后到期的专项应付 Long-term special payable over one year递延税款 Deferral taxes三、所有者权益类 OWNERS'' EQUITY资本 Capita实收资本(或股本) Paid-up capital(or stock)实收资本 Paicl-up capital实收股本 Paid-up stock已归还投资 Investment Returned公积资本公积 Capital reserve资本(或股本)溢价 Cpital(or Stock) premium接受捐赠非现金资产准备 Receive non-cash donate reserve股权投资准备 Stock right investment reserves拨款转入 Allocate sums changeover in外币资本折算差额 Foreign currency capital其他资本公积 Other capital reserve盈余公积 Surplus reserves法定盈余公积 Legal surplus任意盈余公积 Free surplus reserves法定公益金 Legal public welfare fund储备基金 Reserve fund企业发展基金 Enterprise expension fund利润归还投资 Profits capitalizad on return of investment 润 Profits本年利润 Current year profits利润分配 Profit distribution其他转入 Other chengeover in提取法定盈余公积 Withdrawal legal surplus 提取法定公益金 Withdrawal legal public welfare funds 提取储备基金 Withdrawal reserve fund提取企业发展基金 Withdrawal reserve for business expansion提取职工奖励及福利基金 Withdrawal staff and workers'' bonus and welfare fund利润归还投资 Profits capitalizad on return of investment 应付优先股股利 Preferred Stock dividends payable提取任意盈余公积 Withdrawal other common accumulation fund应付普通股股利 Common Stock dividends payable转作资本(或股本)的普通股股利 Common Stock dividends change to assets(or stock)未分配利润 Undistributed profit四、成本类 Cost生产成本 Cost of manufacture基本生产成本 Base cost of manufacture辅助生产成本 Auxiliary cost of manufacture制造费用 Manufacturing overhead材料费 Materials管理人员工资 Executive Salaries奖金 Wages退职金 Retirement allowance补贴 Bonus外保劳务费 Outsourcing fee福利费 Employee benefits/welfare会议费 Coferemce加班餐费 Special duties市内交通费 Business traveling通讯费 Correspondence电话费 Correspondence水电取暖费 Water and Steam税费 Taxes and dues租赁费 Rent管理费 Maintenance车辆维护费 Vehicles maintenance油料费 Vehicles maintenance培训费 Education and training接待费 Entertainment图书、印刷费 Books and printing运费 Transpotation保险费 Insurance premium支付手续费 Commission杂费 Sundry charges折旧费 Depreciation expense机物料消耗 Article of consumption劳动保护费 Labor protection fees季节性停工损失 Loss on seasonality cessation劳务成本 Service costs五、损益类 Profit and loss收入 Income业务收入 OPERATING INCOME主营业务收入 Prime operating revenue产品销售收入 Sales revenue服务收入 Service revenue其他业务收入 Other operating revenue材料销售 Sales materials代购代售包装物出租 Wrappage lease出让资产使用权收入 Remise right of assets revenue返还所得税 Reimbursement of income tax其他收入 Other revenue公允价值变动损益 Profit and loss arising from fair value changes持有至到期投资 Held-to-maturity investment投资收益 Investment income摊余成本 Amortized cost短期投资收益 Current investment income长期投资收益 Long-term investment income计提的委托贷款减值准备 Withdrawal of entrust loans reserves补贴收入 Subsidize revenue国家扶持补贴收入 Subsidize revenue from country其他补贴收入 Other subsidize revenue营业外收入 NON-OPERATING INCOME非货币性交易收益 Non-cash deal income现金溢余 Cash overage处置固定资产净收益 Net income on disposal of fixed assets出售无形资产收益 Income on sales of intangible assets 固定资产盘盈 Fixed assets inventory profit 罚款净收入 Net amercement income支出 Outlay业务支出 Revenue charges主营业务成本 Operating costs产品销售成本 Cost of goods sold服务成本 Cost of service主营业务税金及附加 Tax and associate charge营业税 Sales tax消费税 Consumption tax城市维护建设税 Tax for maintaining and building cities 资源税 Resources tax土地增值税 Increment tax on land value其他业务支出 Other business expense销售其他材料成本 Other cost of material sale其他劳务成本 Other cost of service其他业务税金及附加费 Other tax and associate charge 费用 Expenses营业费用 Operating expenses代销手续费 Consignment commission charge运杂费 Transpotation保险费 Insurance premium展览费 Exhibition fees广告费 Advertising fees管理费用 Administrative expenses职工工资 Staff Salaries修理费 Repair charge低值易耗摊销 Article of consumption办公费 Office allowance差旅费 Travelling expense工会经费 Labour union expenditure研究与开发费 Research and development expense福利费 Employee benefits/welfare职工教育经费 Personnel education待业保险费 Unemployment insurance劳动保险费 Labour insurance医疗保险费 Medical insurance会议费 Coferemce聘请中介机构费 Intermediary organs咨询费 Consult fees诉讼费 Legal cost业务招待费 Business entertainment技术转让费 Technology transfer fees矿产资源补偿费 Mineral resources compensation fees排污费 Pollution discharge fees房产税 Housing property tax车船使用税 Vehicle and vessel usage license plate tax(VVULPT)土地使用税 Tenure tax印花税 Stamp tax财务费用 Finance charge利息支出 Interest exchange汇兑损失 Foreign exchange loss各项手续费 Charge for trouble各项专门借款费用 Special-borrowing cost营业外支出 Nonbusiness expenditure捐赠支出 Donation outlay减值准备金 Depreciation reserves非常损失 Extraordinary loss处理固定资产净损失 Net loss on disposal of fixed assets出售无形资产损失 Loss on sales of intangible assets固定资产盘亏 Fixed assets inventory loss债务重组损失 Loss on arrangement罚款支出 Amercement outlay所得税 Income tax以前年度损益调整 Prior year income adjust ment应交税费-应交所得税 Tax payable - income tax payable应交税费-应交增值税(进项税额) Tax payable - VAT(input VAT)应交税费-应交增值税(销项税额)Tax payable - VAT(output VAT)应交税费-应交增值税(出口退税)Tax payable - VAT(refund of export duty)应交税费-应交增值税(进项税额转出)Tax payable - VAT(transfer-out of input VAT)应交税费-应交增值税(已交税金)Tax payable - VAT(taxes paid)应交税费-应交增值税(转出未交增值税)Tax payable - VAT(transfer-out of unpaid VAT)应交税费-应交增值税(转出多交增值税)Tax payable - VAT(transfer-out of overpaid VAT)应交税费-应交增值税(减免税款)Tax payable - VAT(VAT deductions and exemptions)应交税费-应交增值税(出口抵减内销产品应纳税额) Tax payable -VAT(export duty deductible from taxes payable on domestic sales)应交税费-应交营业税 Tax payable - business tax payable 应交税费-应交消费税 Tax payable - excise tax payable。

ACCAF3官网题库—样题卷3

1. Jason has received payment for a debt that had been written off as irrecoverable. What debit and credit should be used to record the correct journal entry for this transaction?.Cash Receivables controlaccountIrrecoverable debtsDebitCredit2. Which of the following organisations provides guidance to the International Accounting Standards Board on the implications of proposed standards for users and preparers of financial statements?The International Financial Reporting Standards Interpretations CommitteeThe International Financial Reporting Standards FoundationThe International Financial Reporting Standards Advisory CouncilThe International Federation of Accountants3. Which of the following statements about directors are true?(1) The directors of a company are responsible for the preparation of the financial statements of that company(2) The directors and external auditors of a company have joint responsibility for the governance of that company(3) The directors of a company must act honestly in what they consider to be the best interests of their fellow directors(4) The directors of a company should seek to create wealth for the shareholders of the company as their main aim1 and 4 only1, 2 and 41 and 32, 3 and 44. Which of the following statements regarding the qualitative characteristics of financial information is FALSE?Information is verifiable if different, knowledgeable and independentobservers could reach consensus that a particular depiction is a faithfulrepresentationInformation will only be useful if it is relevant and faithfully representedUnderstandability means that points that are too complex for non-expert users should be excludedIf information is timely then its usefulness is enhanced5. On 3 December, a credit customer returned goods of $3,500 to Gerry. Gerry returned goods of $4,100 to his credit supplier on 2 December.What is Gerry's correct journal entry to record these two returns?Dr Payables $3,500 Cr Returns outwards $3,500Dr Returns inwards $4,100 Cr Receivables $4,100Dr Payables $4,100 Cr Returns outwards $4,100Dr Returns inwards $3,500 Cr Receivables $3,500Dr Returns outwards $3,500 Cr Payables $3,500Dr Receivables $4,100 Cr Returns inwards $4,100Dr Returns outwards $4,100 Cr Payables $4,100Dr Receivables $3,500 Cr Returns inwards $3,5006. Katie sold goods with a list price of $18,500 to Marta on 22 May 20X0. Katie allowsa trade discount of 15% and a further discount of 5% if payment is made within seven days.How much should Katie record in the sales ledger control account in respect of this sale?$2,775$15,725$14,800$3,7007. If Marta pays within seven days, the further discount of 5% will be recorded in Katie's accounts as a discount allowed, which is an expense in the statement of profit or loss.Which of the following statements about petty cash is/are true?(1) If a business makes all of its sales on credit, it has no need to maintain a petty cash book(2) If petty cash transactions are very small, they do not need to be recorded(3) Petty cash records should be compared to the bank statement to confirm that payments made from petty cash are recorded1, 2 and 33 only1 and2 onlyNone of the statements are true8. On 31 May 20X0, Charmaine counted her closing inventory for the year ended 31 May 20X0. Its valuation at cost amounted to $459,204. Several days later, she realised that she had included inventory of $5,130 which was in the despatch area and was to be returned to the supplier as it was faulty. Additionally, certain inventory items with a cost of $6,700 were obsolete and only had a net realisable value of $6,150.What should the adjustments be to profit and closing inventory in the financial statements for the year ended 31 May 20X0?.Increase by $5,680 Reduce by $5,680ProfitClosing inventory9. Which TWO of the following statements about IAS 2 Inventories are correct?The costs of purchase of inventory should include any import duties paid, less any trade discounts receivedAverage cost and last in first out are both acceptable methods of arriving atthe cost of inventoryInventory should be valued at the lower of cost and net realisable valueVariable production overheads should not be included in the cost ofinventory10. What should the balance on the revaluation surplus be immediately after the revaluation?$11. ABK Co bought a property on 31 December 20X3 for $340,000. At the date of purchase, ABK estimated the useful life of the property to be 32 years.On 31 December 20X5, the property was revalued to $410,000. There was no change in its useful life.On 30 June 20X7, ABC Co sold the property for $485,000.ABK Co depreciates property on a straight line basis, with a proportional charge in the years of purchase and disposal.What is the profit on disposal of the property that should be recorded in ABK Co's financial statements at 31 December 20X7?12. Daisy Co owns a non-current asset which cost $75,000 on 1 June 20X6. It had a useful life of 10 years and an expected residual value of $5,000. Non-current assets are depreciated using the straight line method.On 1 June 20X8, Daisy Co estimated that the remaining life of the asset was now only five years with an expected residual value of $3,000.What should the depreciation charge be for the financial year ending 31 May 20X9?13. What amount should be capitalised as development expenditure in the year ended 30 November 20X7?$277,400 $362,050 $265,500 $014. Anders is analysing his accounts for the year ended 31 May 20X0. He has not yet made adjustments for the following:(1) Electricity expenses for the three months to 31 May 20X0 are estimated to be $250(2) Insurance of $528 for the 12 months to 31 December 20X0 was paid on 1 January 20X0What is the net impact on profit when the appropriate adjustments are made?Decrease of $558Decrease of $58Increase of $30Increase of $5815.Which of the following statements is true?Redeemable preference shares are disclosed as a liability in the statement of financial positionIssued shares are included in the statement of financial position at theirmarket valuePreference shares give the holders a right to vote at company meetingsHolders of ordinary shares will always receive an annual dividend16. The share capital and reserves of Bondai on 1 January 20X8 were as follows:$Share capital ($1 shares) 52,000Share premium 21,000Retained earnings 25,65998,659On 1 April 20X8, Bondai issued 1,500 shares in a bonus issue utilising the share premium account.On 1 May 20X8, Bondai issued 5,000 $1 shares for $1.50 per share.What is the balance of share capital and share premium after both share transactions have taken place?.$22,000 $23,500 $57,000 $58,500Share premiumShare capital17. Mary has the following ledger balances in her general ledger:$Capital 6,260Cash at bank 890Discounts allowed 1,500Discounts received 2,300Expenses 15,910Non-current assets (carrying amount) 31,845Opening inventory 4,820Purchases 71,470Payables 6,930Receivables 15,870Sales 126,970What is the balance required in a suspense account to make Mary's trial balance agree?$155 Dr$155 Cr$1,445 Cr18. Which of the following would cause the totals of the debit column and the credit column of a trial balance not to agree?(1) A sale of $600 was recorded only as a credit in the sales account(2) A purchase invoice was recorded as a debit of $965 in the purchases account and a credit of $956 in payables(3) A payment of $440 was omitted from the ledger accounts entirely1, 2 and 31 and 3 only1 and2 only2 and3 only19. Emily's payables ledger control account shows a balance of $24,903 which does not agree with the payables ledger. She has found three errors:(1) A purchase invoice has been entered into the purchase day book as $594 rather than $495(2) The purchase day book has been undercast by $200(3) Discounts received of $150 from credit suppliers have not been entered in the control accountWhat is the corrected payables ledger control account balance?$24,654$24,854$24,95220. The following are Hubble's transactions for the month of May:$Opening payables 64,199Opening receivables 84,122Purchases 122,914Purchase returns 6,192Sales 154,610Sales returns 8,112Cash paid to suppliers 100,032Cash received from customers 132,011Contra between purchase ledger and sales ledger 2,912All sales and purchases are made on credit.What should the balance on the purchase ledger control account be at the end of May?21. The following information relates to a business's bank balance at 30 November 20X7:$Balance in cash book 25,050 DrCheques not yet presented at bank 8,612Deposits not yet cleared at bank 11,665Cheques paid to suppliers on 29 November not yet recorded in the cash2,157 bookCheque received on 27 November recorded twice in the cash book 620Cheque received on 1 December 20X7 1,019What is the correct bank balance to be included in the financial statements at 30 November 20X7?22. Which of the following errors would lead to the creation of a suspense account?An error of omission An error of principle A compensating error A transposition error23. Which of the following statements describes a suspense account?An account used to record period end adjustments such as accruals and prepaymentsA ledger account which records non-standard accounting entries A temporary account used when the business is not sure where an accounting entry should be postedAn account used to record the balances extracted from the ledger accounts at the period end24. Below is an extract of ADC Co's trial balance, after adjustments.Dr ($)Cr ($) Cash at bank 2,500Receivables3,750Allowances for receivables550Irrecoverable debts200What entries would be made in ADC Co's statement of financial position in relation to these items?Current assets $3,400Current liabilities $2,500Current assets $3,750Current liabilities $3,050Current assets $3,200Current liabilities $2,500Current assets $3,750Current liabilities $2,85025. Albert Co is preparing accounts for the year ended 31 May 20X0. The tax charge has been estimated as $112,500 for the year. In the previous financial year, the tax expense was estimated to be $99,400 and the company actually paid $102,600 when the tax expense was agreed with the tax authorities.What should the tax expense be in the statement of profit or loss for the year ended 31 May 20X0?$26. Which of the following statements about disclosure notes is/are correct?(1) IAS 37 Provisions, Contingent Liabilities and Contingent Assets requires remotecontingent liabilities to be disclosed if they are material(2) IAS 2 Inventories requires the disclosure of the amount of inventories carried atnet realisable value(3) IAS 16 Property, Property, Plant and Equipment requires disclosure of whetheran independent valuer was involved in the valuation of revalued assets1 and 22 and 31 and 32 only27. Dresden Co makes all sales on credit. At 30 November 20X9, the total receivables balance amounted to $136,400.The following information has come to light a few days after the 30 November 20X9 year end.(1) Fred Willis, who owed Dresden Co $44,300 at the year end, has been declaredbankrupt. The liquidators have stated that the maximum Dresden Co will receive is $18,000 of the debt owed (2)Flora Bailey, who owed Dresden Co $22,500 at the year end, has left the country and has no intention of ever settling her debtFollowing the principles in IAS 10, Events after the Reporting Period, what should Dresden Co include in the statement of financial position for receivables at 30 November 20X9? $28. On 1 January 20X9, Shelter Co had 100,000 $1 ordinary shares. On 1 April 20X9, Shelter Co issued 50,000 $1 ordinary shares for $1.25 per share and on 1 October 20X9, made a bonus issue of $20,000 $1 ordinary shares.On 1 January 20X9, Shelter Co had $65,000 outstanding in bank loans which had increased to $92,000 by the end of the financial year.On 1 January 20X9, Shelter Co had non-current asset investments of $40,000. Shelter Co purchased a further $10,000 of investments during the year and received $3,000 of interest income on investments.In the statement of cash flows for the year ended 31 December 20X9, what is the net cash flow from financing activities?$35,500 inflow$82,500 inflow$89,500 inflow$109,500 inflow29. Carmela purchased goods for resale in March of $86,000. All sales are at a gross margin of 20%. Carmela had opening inventory of $22,000 and closing inventory of $16,000.What should Carmela's revenue be for March?30. Colin has not kept accounting records for his first year of trading. He has purchased $65,000 of goods during the year and has $5,000 of goods left in inventory at the end of the year. All sales are made at a mark-up on cost of 40%.What is Colin's gross profit for his first year of trading?31. Which of the following statements is true?The interpretation of an entity's financial statements using ratios is onlyuseful for potential investorsRatios based on historical data can predict the future performance of anentityThe analysis of financial statements using ratios provides useful information when compared with previous performance or industry averagesAn entity's management will not assess an entity's performance usingfinancial ratios32. The draft accounts of a limited company include the following assets and liabilities at the end of an accounting period.Current assets $ $ $ Inventory 201,000Less: Allowance for obsolescence (16,900)184,100Trade receivables 150,500Less: Allowance for irrecoverable debts (11,200)139,300Total current assets 323,400 Current liabilitiesBank overdraft 18,500Trade payables 174,200Accruals 9,300Total current liabilities 202,000 Which of the following is the company's Quick (Acid Test) Ratio?1.60: 10.75: 10.69: 1None of these33. The auditor of Four Co, a manufacturing company, has noted an increase in total sales value but a decrease in the company's gross profit percentage for 20X9, as compared to the previous year.Which of the following is consistent with, and adequately explains, the decrease?Sales commission payable to the company's sales force increased in relation to sales values as compared to 20X8Sales volumes have decreased as compared to 20X8During 20X9, due to a scarcity of supply the company had to pay higher prices when purchasing componentsDuring 20X9, a major component supplier withdrew the settlement discounts previously granted34. Florida Co had an on-going litigation claim which had been brought against the company for damage to a public road allegedly caused by one of its lorries. At 1 October 20X2, Florida Co had disclosed a contingent liability of $120,000.Due to new developments in the court case, the latest correspondence with the solicitors at 30 September 20X3 suggests it is now probable that Florida Co will lose and have to pay damages of $150,000.What is the impact of the above provision on the total statement of profit or loss expense for the year ended 30 September 20X3?$150,000Nil$30,000$120,00036. BackgroundClaus, a limited liability company, acquired 75% of Rolph's voting share capital on 1 October 20X1 for $1.50 per share.Rolph's share capital comprised 1 million $1 ordinary shares.Task 1 4 marks Complete the following sentencesClaus has acquired abe accounted for in the consolidated financial statements as at 31 March 20X2 asThe cost of the investment in Rolph will appear inAny investment income Claus receives from Rolph will be recorded inTask 28 marksClaus purchased 75% of the voting capital of Rolph on 1 October 20X1. The additional information relates to the year ended 31 March 20X2.The following information is relevant:(1) On 1 October 20X1 Rolph's retained earnings were $475,000.(2) At the date of acquisition, the fair value of Rolph's property, plant and equipment was equal to its carrying amount with the exception of Rolph's land which had a fair value of $200,000 in excess of its carrying amount. The fair value has not been reflected in Rolph's individual financial statements.(3)Included in Claus' receivables is a balance of $11,000 due from Rolph. This agrees with the corresponding figure shown in Rolph's balances.Complete the following extracts from the consolidated statement of financial position as at 31 March 20X2:Tasks 3 and 4 3 marks The following year, trading between Claus and Rolph continues. There is no change to Claus' shareholding in Rolph.Claus makes sales of $240,000 to Rolph during the year, at a mark up of 60%.30% of the items have been sold to a third party by the year end.Task 3 2 marks What is the journal entry in the consolidated statement of financial position to record the elimination of the unrealised profit?.Debit Credit No debit or creditInventoryGroup retained earningsNon-controlling interestGoodwill: Net assets at acquisitionTask 4 1 mark What is the amount of the unrealised profit in inventory at the year end?37. BackgroundExtracts from the trial balance of Desmond, a limited liability company, for the year ended 30 September 20X8 are shown below:The intangible assets were purchased on 1 April 20X8 and have a useful life of five years from that date. Amortisation is calculated on a monthly basis.Task 1 3 marks What is the carrying amount of intangible assets at 30 September 20X8?How will this balance be classified in the statement of financial position?Task 2 4 marks On 30 September 20X8, Desmond disposed of an item of plant for $12,000. The plant originally cost $24,000 and had accumulated depreciation of $9,000 at 1 October20X7.Plant is depreciated at 25% per annum using the reducing balance method. A full year's depreciation is charged in the year of acquisition and no depreciation is charged in the year of disposal.What is the profit or loss on disposal of the plant?What is the correct calculation for the depreciation expense on the remaining plant for the year ended 30 September 20X8 (all figures are in $’000)?Correct Answer $’000 Proceeds12 Carrying amount (24 – 9) 15 Loss3The carrying amount of the asset exceeds the sale proceeds by $3,000 therefore Desmond has made a loss.As Desmond uses the reducing balance method depreciation on the remaining plant is based on net book value (cost – accumulated depreciation). The balances provided for both cost and accumulated depreciation at 1 October 20X7 must be adjusted to reflect the disposal.Tasks 3 and 45 marksThe buildings were revalued on 1 October 20X7 to $620,000.Task 32 marksWhat is the journal entry to record the revaluation of buildings? .Debit Credit No debit or creditBuildings - accumulated depreciationRevaluation surplusBuildings - costDepreciation expenseTask 4 3 marks The buildings are depreciated at 5% per annum on cost or valuation. Desmond’s policy is to make an annual transfer of the excess depreciation from the revaluation surplus to retained earnings.What is the depreciation expense to be charged in the statement of profit or loss for the year ended 30 September 20X8?$What amount should be transferred for excess depreciation from the revaluation surplus to retained earnings for the year ended 30 September 20X8?Task 53 marksThe trade receivables balance has been reviewed at the year end and the following adjustments are required:(1) An irrecoverable debt of $6,000 is to be written off.(2) The allowance for receivables needs to be adjusted to 2% of the remaining receivables.Complete the following statements:The irrecoverable debt willThe impact of the movement in the allowance for receivables for the year ended30 September 20X8 will。

常用商务方面英文单词缩写

1 C&F(cost&freight)成本加运费价2 T/T(telegraphic transfer)电汇3 D/P(document against payment)付款交单4 D/A (document against acceptance)承兑交单5 C.O (certificate of origin)一般原产地证6 G..(generalized system of preferences)普惠制7 CTN/CTNS(carton/cartons)纸箱8 PCE/PCS(piece/pieces)只、个、支等9 DL/DLS(dollar/dollars)美元10 DOZ/DZ(dozen)一打11 PKG(package)一包,一捆,一扎,一件等12 WT(weight)重量13 G.W.(gross weight)毛重14 .(net weight)净重15 C/D (customs declaration)报关单16 EA(each)每个,各17 W (with)具有18 w/o(without)没有19 FAC(facsimile)传真20 IMP(import)进口21 EXP(export)出口22 MAX (maximum)最大的、最大限度的23 MIN (minimum)最小的,最低限度24 M 或MED (medium)中等,中级的25 M/V(merchant vessel)商船26 (steamship)船运27 MT或M/T(metric ton)公吨28 DOC (document)文件、单据29 INT(international)国际的30 P/L (packing list)装箱单、明细表31 INV (invoice)发票32 PCT (percent)百分比33 REF (reference)参考、查价34 EMS (express mail special)特快传递35 STL.(style)式样、款式、类型36 T或LTX或TX(telex)电传37 RMB(renminbi)人民币38 S/M (shipping marks)装船标记39 PR或PRC(price) 价格40 PUR (purchase)购买、购货41 S/C(sales contract)销售确认书42 L/C (letter of credit)信用证43 B/L (bill of lading)提单44 FOB (free on board)离岸价45 CIF (cost,insurance&freight)成本、保险加运费价补充:CR=credit贷方,债主DR=debt借贷方(注意:国外常说的debt card,就是银行卡,credit card就是信誉卡。

《国际结算》作业题参考答案一名词解释

《国际结算》作业题参考答案⼀名词解释《国际结算》作业题参考答案⼀、名词解释:1、国际结算:即International Settlement,是指国际间由于经济、政治等各⽅⾯交往⽽引起的、以货币所表现的债券债务结算。

2、代理⾏:即Correspondent Banks,是指两家银⾏通过签订协议,建⽴委托代理关系,互相委办诸如国际结算、出⼝信贷、银团贷款等业务或提供服务。

这样的两家银⾏互称代理⾏。

3、控制⽂件:即control Documents,两家建⽴代理⾏关系在银⾏在互相委办业务或提供服务时所相互交换的⽤以明确关系和⽅便业务的⽂件,包括密押、印鉴、和费率表等。

4、CHIPS:即美国纽约票据交换所银⾏同业⽀付系统,有纽约清算协会于1971年成⽴,专门⽤于全球美元清算,是⼀个实时的、银⾏对银⾏交易的终局性付款系统。

⽬前全球⼤约95%的美元⽀付都是通过这⼀系统处理完成的。

5、SWIFT:即环球银⾏间⾦融电讯协会,成⽴于1973年,总部设在⽐利时的布鲁塞尔,其创建之⽬的在于创造⼀个全球共享的使⽤统⼀语⾔的数据处理和通讯⽹络体系,⼀边于所有的国际⾦融交易。

现有设在荷兰、⾹港、英国和美国的四个基地,主要向全球7000多家会员提供资⾦划拨、国际贸易⽀付、国债、证券、外汇交易等服务。

6、CHAPS:即英国伦敦票据交换所银⾏同业⽀付系统,成⽴于1984年,是银⾏间即⽇电⼦⽀付系统,与英格兰银⾏合作提供收付和清算服务,它同时是世界上最⼤的全国性清算系统之⼀,1999年1⽉起在运⾏原有英镑清算系统的同时开始运⾏欧元清算系统。

7、TARGET:即欧元⾃动拨付与清算系统,位于德国法兰克福欧洲中央银⾏总部,与1999年1⽉4⾥开始运⾏。

由15个欧盟成员国的全国实时清算系统和欧洲中央银⾏的⽀付系统组成,以提供公共平台便利各成员国之间的跨境⽀付。

8、存放国外同业:即NOSTRO,代理⾏之间建⽴的账户关系之⼀,属资产类科⽬,即借⽅记录资产的增加、负债的减少,贷⽅记录资产的减少、负债的增加。

大额支付系统报文格式汇总

大额支付系统MESG报文格式汇总版本号:V2.3中国人民银行科技司二○○六年七月目录1 概述 (4)1.1 说明 (4)1.2 数据格式描述 (4)1.3 属性符号 (5)1.4 x-字符集 (6)1.5 英文简称命名规范 (6)2 报文结构 (7)2.1 报文块的说明 (7)2.1.1 系统信息块(sysInfoB) (7)2.1.2 报头块(basHeadB) (7)2.1.3 批量支付业务头块(batAppHeadB) (7)2.1.3 业务头块(appHeadB) (8)2.1.4 正文块(textB) (8)2.1.5 基本数据块 (8)2.1.6 报尾块(trailerB) (8)2.2 报文块之间的关系 (9)2.3 报文块结构规则 (10)3 报文块格式描述 (12)3.1 系统信息块 (12)3.2 报头块 (12)3.3 批量支付业务头块 (13)3.4 业务头块 (14)3.5 正文块 (15)3.6 报尾块 (15)4 报文分类 (17)4.1 报文功能分类 (17)4.2 报文结构分类 (23)4.2.1系统信息 (23)4.2.2实时支付指令 (23)4.2.3批量支付业务指令 (24)4.2.4无编押应用报文 (24)5处理码说明 (25)附录A TAG与域名 (27)A1各种TAG值类型的格式说明 (27)A2 TAG与域名一览表 (28)附录B 处理码一览表 (56)B1涉及处理码的报文列表 (56)B2处理码一览表 (57)B3涉及处理码的报文列表 (66)CMT253 大额或即时转账清算结果返回报文 (66)CMT910 通用回应报文 (68)CMT420 登录返回报文 (72)CMT422 退出登录返回报文 (72)CMT683 排队情况查询返回报文 (73)CMT682 余额查询模块返回报文 (73)CMT686 预期头寸查询模块返回报文 (74)CMT687 账户信息查询模块返回报文 (74)CMT684 同城轧差净额查询模块返回报文 (75)CMT685 小额轧差清算情况查询模块返回报文 (75)CMT448 单边及错账冲正业务查询回应报文 (75)CMT660 小额拒绝报文 (75)CMT404 人工质押融资回复报文 (76)B4新增处理码列表(2002-06-02) (76)附录C 支付系统报文正文 (78)报文编号:CMT100 报文名称:汇兑支付报文 (78)报文编号:CMT101 报文名称:委托收款(划回)支付报文 (80)报文编号:CMT102 报文名称:托收承付(划回)支付报文 (81)报文编号:CMT103 报文名称:国库资金汇划(贷记)支付报文 (82)报文编号:CMT104 报文名称:定期贷记支付报文 (84)报文编号:CMT105 报文名称:银行间同业拆借支付报文 (85)报文编号:CMT108 报文名称:退汇支付报文 (86)报文编号:CMT109 报文名称:电子联行专用汇兑报文 (87)报文编号:CMT110 报文名称:银行汇票支付报文 (88)报文编号:CMT112 报文名称:旅行支票支付报文 (89)报文编号:CMT113 报文名称:国库资金汇划(借记)支付报文 (90)报文编号:CMT114 报文名称:定期借记支付报文 (91)报文编号:CMT119 报文名称:通用借记支付报文 (92)报文编号:CMT221 报文名称:同城轧差净额清算报文 (93)报文编号:CMT222 报文名称:小额轧差净额清算报文 (94)报文编号:CMT223 报文名称:大额或即时转账清算报文 (95)报文编号:CMT253 报文名称:大额或即时转账清算结果返回报文 (95)报文编号:CMT301 报文名称:查询报文 (96)报文编号:CMT302 报文名称:查复报文 (98)报文编号:CMT303 报文名称:自由格式报文 (99)1 概述1.1 说明报文是支付系统与银行系统交换业务、控制数据的基本单位。

(完整word版)ACCA会计科目中英对照

一级科目二级科目三级科目四级科目代码名称代码名称代码名称代码名称英译1 资产 assets11~ 12 流动资产 current assets111 现金及约当现金 cash and cash equivalents1111 库存现金 cash on hand1112 零用金/周转金 petty cash/revolving funds1113 银行存款 cash in banks1116 在途现金 cash in transit1117 约当现金 cash equivalents1118 其它现金及约当现金 other cash and cash equivalents112 短期投资 short—term investments1121 短期投资—股票 short-term investments - stock1122 短期投资 -短期票券 short-term investments - short—term notes and bills1123 短期投资 -政府债券 short—term investments - government bonds1124 短期投资 -受益凭证 short-term investments — beneficiary certificates1125 短期投资—公司债 short—term investments - corporate bonds1128 短期投资—其它 short-term investments - other1129 备抵短期投资跌价损失 allowance for reduction of short-term investment to market 113 应收票据 notes receivable1131 应收票据 notes receivable1132 应收票据贴现 discounted notes receivable1137 应收票据 -关系人 notes receivable — related parties1138 其它应收票据 other notes receivable1139 备抵呆帐-应收票据 allowance for uncollec— tible accounts- notes receivable114 应收帐款 accounts receivable1141 应收帐款 accounts receivable1142 应收分期帐款 installment accounts receivable1147 应收帐款 -关系人 accounts receivable - related parties1149 备抵呆帐-应收帐款 allowance for uncollec- tible accounts - accounts receivable 118 其它应收款 other receivables1181 应收出售远汇款 forward exchange contract receivable1182 应收远汇款 -外币 forward exchange contract receivable - foreign currencies1183 买卖远汇折价 discount on forward ex—change contract1184 应收收益 earned revenue receivable1185 应收退税款 income tax refund receivable1187 其它应收款 - 关系人 other receivables — related parties1188 其它应收款 - 其它 other receivables - other1189 备抵呆帐—其它应收款 allowance for uncollec- tible accounts — other receivables 121~122 存货 inventories1211 商品存货 merchandise inventory1212 寄销商品 consigned goods1213 在途商品 goods in transit1219 备抵存货跌价损失 allowance for reduction of inventory to market1221 制成品 finished goods1222 寄销制成品 consigned finished goods1223 副产品 by—products1224 在制品 work in process1225 委外加工 work in process - outsourced1226 原料 raw materials1227 物料 supplies1228 在途原物料 materials and supplies in transit1229 备抵存货跌价损失 allowance for reduction of inventory to market125 预付费用 prepaid expenses1251 预付薪资 prepaid payroll1252 预付租金 prepaid rents1253 预付保险费 prepaid insurance1254 用品盘存 office supplies1255 预付所得税 prepaid income tax1258 其它预付费用 other prepaid expenses126 预付款项 prepayments1261 预付货款 prepayment for purchases1268 其它预付款项 other prepayments128~129 其它流动资产 other current assets1281 进项税额 VAT paid ( or input tax)1282 留抵税额 excess VAT paid (or overpaid VAT)1283 暂付款 temporary payments1284 代付款 payment on behalf of others1285 员工借支 advances to employees1286 存出保证金 refundable deposits1287 受限制存款 certificate of deposit—restricted1291 递延所得税资产 deferred income tax assets1292 递延兑换损失 deferred foreign exchange losses1293 业主(股东)往来 owners'(stockholders') current account1294 同业往来 current account with others1298 其它流动资产—其它 other current assets - other13 基金及长期投资 funds and long—term investments131 基金 funds1311 偿债基金 redemption fund (or sinking fund)1312 改良及扩充基金 fund for improvement and expansion1313 意外损失准备基金 contingency fund1314 退休基金 pension fund1318 其它基金 other funds132 长期投资 long-term investments1321 长期股权投资 long-term equity investments1322 长期债券投资 long—term bond investments1323 长期不动产投资 long—term real estate in-vestments1324 人寿保险现金解约价值 cash surrender value of life insurance1328 其它长期投资 other long-term investments1329 备抵长期投资跌价损失 allowance for excess of cost over market value of long-term investments 14~ 15 固定资产 property , plant, and equipment141 土地 land1411 土地 land1418 土地—重估增值 land — revaluation increments142 土地改良物 land improvements1421 土地改良物 land improvements1428 土地改良物 -重估增值 land improvements — revaluation increments1429 累积折旧—土地改良物 accumulated depreciation - land improvements143 房屋及建物 buildings1431 房屋及建物 buildings1438 房屋及建物—重估增值 buildings -revaluation increments1439 累积折旧 -房屋及建物 accumulated depreciation - buildings144~146 机(器)具及设备 machinery and equipment1441 机(器)具 machinery1448 机(器)具 -重估增值 machinery — revaluation increments1449 累积折旧—机(器)具 accumulated depreciation — machinery151 租赁资产 leased assets1511 租赁资产 leased assets1519 累积折旧—租赁资产 accumulated depreciation - leased assets152 租赁权益改良 leasehold improvements1521 租赁权益改良 leasehold improvements1529 累积折旧- 租赁权益改良 accumulated depreciation — leasehold improvements156 未完工程及预付购置设备款 construction in progress and prepayments for equipment1561 未完工程 construction in progress1562 预付购置设备款 prepayment for equipment158 杂项固定资产 miscellaneous property, plant, and equipment1581 杂项固定资产 miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant,and equipment - revaluation increments1589 累积折旧—杂项固定资产 accumulated depreciation - miscellaneous property, plant, and equipment16 递耗资产 depletable assets161 递耗资产 depletable assets1611 天然资源 natural resources1618 天然资源—重估增值 natural resources -revaluation increments1619 累积折耗—天然资源 accumulated depletion — natural resources17 无形资产 intangible assets171 商标权 trademarks1711 商标权 trademarks172 专利权 patents1721 专利权 patents173 特许权 franchise1731 特许权 franchise174 著作权 copyright1741 著作权 copyright175 计算机软件 computer software1751 计算机软件 computer software cost176 商誉 goodwill1761 商誉 goodwill177 开办费 organization costs1771 开办费 organization costs178 其它无形资产 other intangibles1781 递延退休金成本 deferred pension costs1782 租赁权益改良 leasehold improvements1788 其它无形资产-其它 other intangible assets — other18 其它资产 other assets181 递延资产 deferred assets1811 债券发行成本 deferred bond issuance costs1812 长期预付租金 long—term prepaid rent1813 长期预付保险费 long-term prepaid insurance1814 递延所得税资产 deferred income tax assets1815 预付退休金 prepaid pension cost1818 其它递延资产 other deferred assets182 闲置资产 idle assets1821 闲置资产 idle assets184 长期应收票据及款项与催收帐款 long—term notes , accounts and overdue receivables1841 长期应收票据 long-term notes receivable1842 长期应收帐款 long—term accounts receivable1843 催收帐款 overdue receivables1847 长期应收票据及款项与催收帐款-关系人 long—term notes, accounts and overdue receivables- related parties1848 其它长期应收款项 other long—term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款 allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产 assets leased to others1851 出租资产 assets leased to others1858 出租资产—重估增值 assets leased to others - incremental value from revaluation1859 累积折旧—出租资产 accumulated depreciation - assets leased to others186 存出保证金 refundable deposit1861 存出保证金 refundable deposits188 杂项资产 miscellaneous assets1881 受限制存款 certificate of deposit — restricted1888 杂项资产 -其它 miscellaneous assets - other2 负债 liabilities21~ 22 流动负债 current liabilities211 短期借款 short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款 bank loan2114 短期借款—业主 short-term borrowings — owners2115 短期借款 -员工 short-term borrowings - employees2117 短期借款 -关系人 short—term borrowings- related parties2118 短期借款 -其它 short-term borrowings — other212 应付短期票券 short—term notes and bills payable2121 应付商业本票 commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券 other short-term notes and bills payable2129 应付短期票券折价 discount on short—term notes and bills payable213 应付票据 notes payable2131 应付票据 notes payable2137 应付票据—关系人 notes payable - related parties2138 其它应付票据 other notes payable214 应付帐款 accounts pay able2141 应付帐款 accounts payable2147 应付帐款—关系人 accounts payable - related parties216 应付所得税 income taxes payable2161 应付所得税 income tax payable217 应付费用 accrued expenses2171 应付薪工 accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐 -其它 accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款 other payables2181 应付购入远汇款 forward exchange contract payable2182 应付远汇款 -外币 forward exchange contract payable - foreign currencies2183 买卖远汇溢价 premium on forward exchange contract2184 应付土地房屋款 payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款 -关系人 other payables — related parties2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳 compensation payable to directors and supervisors2198 其它应付款—其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债 long-term liabilities —current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款 long-term loans payable — current portion2273 一年或一营业周期内到期长期应付票据及款项 long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人 long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债 other long-term lia— bilities — current portion 228~229 其它流动负债 other current liabilities2281 销项税额 VAT received(or output tax)2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债 estimated warranty liabilities2291 递延所得税负债 deferred income tax liabilities2292 递延兑换利益 deferred foreign exchange gain2293 业主(股东)往来 owners' current account2294 同业往来 current account with others2298 其它流动负债-其它 other current liabilities — others23 长期负债 long—term liabilities231 应付公司债 corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价 premium(discount) on corporate bonds payable232 长期借款 long-term loans payable2321 长期银行借款 long-term loans payable — bank2324 长期借款 -业主 long—term loans payable — owners2325 长期借款 -员工 long-term loans payable - employees2327 长期借款 -关系人 long—term loans payable — related parties2328 长期借款—其它 long—term loans payable — other233 长期应付票据及款项 long—term notes and accounts payable2331 长期应付票据 long—term notes payable2332 长期应付帐款 long-term accounts pay-able2333 长期应付租赁负债 long—term capital lease liabilities2337 长期应付票据及款项—关系人 Long—term notes and accounts payable — related parties 2338 其它长期应付款项 other long—term payables234 估计应付土地增值税 accrued liabilities for land value increment tax2341 估计应付土地增值税 estimated accrued land value incremental tax pay-able235 应计退休金负债 accrued pension liabilities2351 应计退休金负债 accrued pension liabilities238 其它长期负债 other long—term liabilities2388 其它长期负债—其它 other long-term liabilities — other28 其它负债 other liabilities281 递延负债 deferred liabilities2811 递延收入 deferred revenue2814 递延所得税负债 deferred income tax liabilities2818 其它递延负债 other deferred liabilities286 存入保证金 deposits received2861 存入保证金 guarantee deposit received288 杂项负债 miscellaneous liabilities2888 杂项负债 -其它 miscellaneous liabilities - other3 业主权益 owners' equity31 资本 capital311 资本(或股本) capital3111 普通股股本 capital - common stock3112 特别股股本 capital — preferred stock3113 预收股本 capital collected in advance3114 待分配股票股利 stock dividends to be distributed3115 资本 capital32 资本公积 additional paid—in capital321 股票溢价 paid-in capital in excess of par3211 普通股股票溢价 paid—in capital in excess of par- common stock3212 特别股股票溢价 paid—in capital in excess of par- preferred stock323 资产重估增值准备 capital surplus from assets revaluation3231 资产重估增值准备 capital surplus from assets revaluation324 处分资产溢价公积 capital surplus from gain on disposal of assets3241 处分资产溢价公积 capital surplus from gain on disposal of assets325 合并公积 capital surplus from business combination3251 合并公积 capital surplus from business combination326 受赠公积 donated surplus3261 受赠公积 donated surplus328 其它资本公积 other additional paid-in capital3281 权益法长期股权投资资本公积 additional paid—in capital from investee under equity method3282 资本公积- 库藏股票交易 additional paid-in capital — treasury stock trans—actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积 legal reserve3311 法定盈余公积 legal reserve332 特别盈余公积 special reserve3321 意外损失准备 contingency reserve3322 改良扩充准备 improvement and expansion reserve3323 偿债准备 special reserve for redemption of liabilities3328 其它特别盈余公积 other special reserve335 未分配盈余(或累积亏损) retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏 accumulated profit or loss3352 前期损益调整 prior period adjustments3353 本期损益 net income or loss for current period34 权益调整 equity adjustments341 长期股权投资未实现跌价损失 unrealized loss on market value decline of long-term equity investments3411 长期股权投资未实现跌价损失 unrealized loss on market value decline of long-term equity investments342 累积换算调整数 cumulative translation adjustment3421 累积换算调整数 cumulative translation adjustments343 未认列为退休金成本之净损失 net loss not recognized as pension cost3431 未认列为退休金成本之净损失 net loss not recognized as pension costs35 库藏股 treasury stock351 库藏股 treasury stock3511 库藏股 treasury stock36 少数股权 minority interest361 少数股权 minority interest3611 少数股权 minority interest4 营业收入 operating revenue41 销货收入 sales revenue411 销货收入 sales revenue4111 销货收入 sales revenue4112 分期付款销货收入 installment sales revenue417 销货退回 sales return4171 销货退回 sales return419 销货折让 sales allowances4191 销货折让 sales discounts and allowances46 劳务收入 service revenue461 劳务收入 service revenue4611 劳务收入 service revenue47 业务收入 agency revenue471 业务收入 agency revenue4711 业务收入 agency revenue48 其它营业收入 other operating revenue488 其它营业收入-其它 other operating revenue4888 其它营业收入-其它 other operating revenue - other5 营业成本 operating costs51 销货成本 cost of goods sold511 销货成本 cost of goods sold5111 销货成本 cost of goods sold5112 分期付款销货成本 installment cost of goods sold512 进货 purchases5121 进货 purchases5122 进货费用 purchase expenses5123 进货退出 purchase returns5124 进货折让 charges on purchased merchandise513 进料 materials purchased5131 进料 material purchased5132 进料费用 charges on purchased material5133 进料退出 material purchase returns5134 进料折让 material purchase allowances514 直接人工 direct labor5141 直接人工 direct labor515~518 制造费用 manufacturing overhead5151 间接人工 indirect labor5152 租金支出 rent expense, rent5153 文具用品 office supplies (expense)5154 旅费 travelling expense, travel5155 运费 shipping expenses, freight5156 邮电费 postage (expenses)5157 修缮费 repair(s) and maintenance (expense )5158 包装费 packing expenses5161 水电瓦斯费 utilities (expense)5162 保险费 insurance (expense)5163 加工费 manufacturing overhead - outsourced5166 税捐 taxes5168 折旧 depreciation expense5169 各项耗竭及摊提 various amortization5172 伙食费 meal (expenses)5173 职工福利 employee benefits/welfare5176 训练费 training (expense)5177 间接材料 indirect materials5188 其它制造费用 other manufacturing expenses56 劳务成本制 ervice costs561 劳务成本 service costs5611 劳务成本 service costs57 业务成本 gency costs571 业务成本 agency costs5711 业务成本 agency costs58 其它营业成本 other operating costs588 其它营业成本-其它 other operating costs—other5888 其它营业成本-其它 other operating costs — other 6 营业费用 operating expenses61 推销费用 selling expenses615~618 推销费用 selling expenses6151 薪资支出 payroll expense6152 租金支出 rent expense, rent6153 文具用品 office supplies (expense)6154 旅费 travelling expense, travel6155 运费 shipping expenses, freight6156 邮电费 postage (expenses)6157 修缮费 repair(s) and maintenance (expense)6159 广告费 advertisement expense, advertisement6161 水电瓦斯费 utilities (expense)6162 保险费 insurance (expense)6164 交际费 entertainment (expense)6165 捐赠 donation (expense)6166 税捐 taxes6167 呆帐损失 loss on uncollectible accounts6168 折旧 depreciation expense6169 各项耗竭及摊提 various amortization6172 伙食费 meal (expenses)6173 职工福利 employee benefits/welfare6175 佣金支出 commission (expense)6176 训练费 training (expense)6188 其它推销费用 other selling expenses62 管理及总务费用 general & administrative expenses625~628 管理及总务费用 general & administrative expenses6251 薪资支出 payroll expense6252 租金支出 rent expense, rent6253 文具用品 office supplies6254 旅费 travelling expense, travel6255 运费 shipping expenses,freight6256 邮电费 postage (expenses)6257 修缮费 repair(s) and maintenance (expense)6259 广告费 advertisement expense, advertisement6261 水电瓦斯费 utilities (expense)6262 保险费 insurance (expense)6264 交际费 entertainment (expense)6265 捐赠 donation (expense)6266 税捐 taxes6267 呆帐损失 loss on uncollectible accounts6268 折旧 depreciation expense6269 各项耗竭及摊提 various amortization6271 外销损失 loss on export sales6272 伙食费 meal (expenses)6273 职工福利 employee benefits/welfare6274 研究发展费用 research and development expense6275 佣金支出 commission (expense)6276 训练费 training (expense)6278 劳务费 professional service fees6288 其它管理及总务费用 other general and administrative expenses63 研究发展费用 research and development expenses635~638 研究发展费用 research and development expenses6351 薪资支出 payroll expense6352 租金支出 rent expense, rent6353 文具用品 office supplies6354 旅费 travelling expense, travel6355 运费 shipping expenses, freight6356 邮电费 postage (expenses)6357 修缮费 repair(s) and maintenance (expense)6361 水电瓦斯费 utilities (expense)6362 保险费 insurance (expense)6364 交际费 entertainment (expense)6366 税捐 taxes6368 折旧 depreciation expense6369 各项耗竭及摊提 various amortization6372 伙食费 meal (expenses)6373 职工福利 employee benefits/welfare6376 训练费 training (expense)6378 其它研究发展费用 other research and development expenses7 营业外收入及费用 non—operating revenue and expenses, other income(expense)71~74 营业外收入 non—operating revenue711 利息收入 interest revenue7111 利息收入 interest revenue/income712 投资收益 investment income7121 权益法认列之投资收益 investment income recognized under equity method7122 股利收入 dividends income7123 短期投资市价回升利益 gain on market price recovery of short-term investment713 兑换利益 foreign exchange gain7131 兑换利益 foreign exchange gain714 处分投资收益 gain on disposal of investments7141 处分投资收益 gain on disposal of investments715 处分资产溢价收入 gain on disposal of assets7151 处分资产溢价收入 gain on disposal of assets748 其它营业外收入 other non—operating revenue7481 捐赠收入 donation income7482 租金收入 rent revenue/income7483 佣金收入 commission revenue/income7484 出售下脚及废料收入 revenue from sale of scraps7485 存货盘盈 gain on physical inventory7486 存货跌价回升利益 gain from price recovery of inventory7487 坏帐转回利益 gain on reversal of bad debts7488 其它营业外收入—其它 other non—operating revenue- other items75~ 78 营业外费用 non—operating expenses751 利息费用 interest expense7511 利息费用 interest expense752 投资损失 investment loss7521 权益法认列之投资损失 investment loss recog— nized under equity method7523 短期投资未实现跌价损失 unrealized loss on reduction of short—term investments to market(完整word版)ACCA会计科目中英对照753 兑换损失 foreign exchange loss7531 兑换损失 foreign exchange loss754 处分投资损失 loss on disposal of investments7541 处分投资损失 loss on disposal of investments755 处分资产损失 loss on disposal of assets7551 处分资产损失 loss on disposal of assets788 其它营业外费用 other non-operating expenses7881 停工损失 loss on work stoppages7882 灾害损失 casualty loss7885 存货盘损 loss on physical inventory7886 存货跌价及呆滞损失 loss for market price decline and obsolete and slow-moving inventories 7888 其它营业外费用-其它 other non—operating expenses— other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit)811 所得税费用(或利益) income tax expense (or benefit)8111 所得税费用(或利益) income tax expense ( or benefit)9 非经常营业损益 nonrecurring gain or loss91 停业部门损益 gain(loss) from discontinued operations911 停业部门损益—停业前营业损益 income(loss) from operations of discontinued segments 9111 停业部门损益—停业前营业损益 income(loss) from operations of discontinued segment 912 停业部门损益—处分损益 gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益 gain(loss) from disposal of discontinued segment92 非常损益 extraordinary gain or loss921 非常损益 extraordinary gain or loss9211 非常损益 extraordinary gain or loss93 会计原则变动累积影响数 cumulative effect of changes in accounting principles931 会计原则变动累积影响数 cumulative effect of changes in accounting principles9311 会计原则变动累积影响数 cumulative effect of changes in accounting principles94 少数股权净利 minority interest income941 少数股权净利 minority interest income9411 少数股权净利 minority interest income。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

ImaginePA Test Scenario (AP-353.1)

4/10/2013 1

CONFIDENTIAL

Test Scenario: AP-353.1 – Invoice Postings (CARATS)

SCENARIO

DESCRIPTION

Testing of PennDOT specific invoice postings via inbound interfaces

AUTHOR Bret Challenger

PREDECESSOR N/A

SUCCESSOR N/A

EXPECTED

RESULTS

All invoice transactions posted or parked in accordance with the interface data mapping strategy

for PennDOT.

TEST START DT

TEST END DT

STATUS

SETUP DATA

Data Object Value/Code Description Comments and Notes

Vendor #-600001 One time vendor/non 1099

Earmark Fund

G/L Account 6399999

DFS

DFS Description Tester OK, error, problem?

TEC_Interface-F_004739

ImaginePA Test Scenario (AP-353.1)

4/10/2013 2

CONFIDENTIAL

TRANSACTIONAL STEPS

No. BUSINESS PROCESS STEPS / BPP FILENAME TRANS. CODE INPUT DATA / SPECIAL INFORMATION OUTPUT DATA / EXPECTED RESULTS ACTUAL RESULTS TESTER OK or

ERROR &

PROB #

1 Receive interface file from PennDOT AL11 View interface file from legacy system

2 Create IDOCs for posting File Run by MQSI Team IDOCs created for each invoice

3 View IDOCs created and posting/error status WE02 IDOC contains legacy data. SAP document number created

4 Invoice posted and blocked in SAP R/3 FB03 ZI document created

5 Comptroller review blocked invoice and if satisfied with payment, remove block FB02 Block type A removed

6 Review vendor posting ZFBL1N Review open invoice

7 Review ZF-Budget-Review Report