财务会计试译

财会资料的中英翻译

财会资料的中英翻译Accountingconvention会计惯例Accountingforacquisitions购并的会计处理Accountingfordebtors应收账款核算Accountingfordepreciation折旧核算Accountingforforeigncurrencies外汇核算Accountingforgoodwill商誉核算Accountingforstocks存货核算Accountingpolicies会计政策Accountingstandards会计准则Accrualsconcept权责发生原则Achievingcreditcontrol实现信用控制Acidtestratio酸性测试比率Actualcashflow实际现金流量Adjustingcompanyprofits企业利润调整Advancepaymentguarantee提前偿还保金Adversetrading不利交易Advertisingbudget广告预算Advisingbank通告银行Ageanalysis账龄分析Ageddebtorsanalysis逾期账款分析Ageddebtors‘exceptionreport逾期应收款的特殊报告Ageddebtors‘exceptionreport逾期账款特别报告Ageddebtors‘report逾期应收款报告Ageddebtors‘report逾期账款报告All—moniesclause全额支付条款Amortization摊销Analyticalquestionnaire调查表分析Analyticalskills分析技巧Analyzingfinancialrisk财务风险分析Analyzingfinancialstatements财务报表分析Analyzingliquidity流动性分析Analyzingprofitability盈利能力分析Analyzingworkingcapital营运资本分析Annualexpenditure年度支出Anticipatingfutureincome预估未来收入Areasoffinancialratios财务比率分析的对象Articlesofincorporation合并条款AscoresA值Asiancrisis亚洲(金融)危机Assessingcompanies企业评估Assessingcountryrisk国家风险评估Assessingcreditrisks信用风险评估Assessingstrategicpower战略地位评估Assessmentofbanks银行的评估Assetconversionlending资产转换贷款Assetprotectionlending资产担保贷款Assetsale资产出售Assets资产Assetturnover资产周转率AssociationofBritishFactorsandDiscounters英国代理人与贴现商协会Auditor'sreport审计报告Aval物权担保Baddebtlevel坏账等级Baddebtrisk坏账风险Baddebtsperformance坏账发生情况Baddebt坏账Badloans坏账Balancesheetstructure资产负债表结构Balancesheet资产负债表Bankcredit银行信贷Bankfailures银行破产Bankloans.Availability银行贷款的可获得性Bankruptcycode破产法Bankruptcypetition破产申请书Bankruptcy破产Bankstatusreports银行状况报告BasleAgreement《巴塞尔协议》Basleagreement塞尔协议Behavorialscoring行为评分Billofexchange汇票Billoflading提单BISagreement国际清算银行协定BIS国际清算银行Bluechip蓝筹股Bonds债券Bookreceivables账面应收账款Borrowingmoney借人资金Borrowingproposition借款申请Breakthroughproducts创新产品Budgets预算Buildingcompanyprofiles勾画企业轮廓Bureaux(信用咨询)公司Businessdevelopmentloan商业开发贷款Businessfailure破产Businessplan经营计划Businessrisk经营风险Buyercredits买方信贷Buyerpower购买方力量Buyerrisks买方风险CAMPARI优质贷款原则Canonsoflending贷款原则Capex资本支出Capitaladequacyrules资本充足性原则Capitaladequacy资本充足性Capitalcommitments资本承付款项Capitalexpenditure资本支出Capitalfunding资本融资Capitalinvestment资本投资Capitalizationofinterest利息资本化Capitalizingdevelopmentcosts研发费用资本化Capitalizingdevelopmentexpenditures研发费用资本化。

财务会计中英文对

财务会计中英文对37accountability unit 责任单位38Accountancy 《会计》杂志39accountancy 会计40accountant 会计员,会计师41accountant general 会计主任,总会计42accounting in charge 主管会计师43accountant,s legal liability 会计师的法律责任44accountant,s report 会计师报告45accountant,s responsibility 会计师职责46account form 账户式,账式47accounting①会计②会计学48accounting assumption 会计假定,会计假设49accounting basis 会计基准,会计基本方法50accounting changes 会计变更51accounting concept 会计概念52accounting control 会计控制53accounting convention 会计常规,会计惯例54accounting corporation 会计公司55accounting cycle 会计循环56accounting data 会计数据57accounting doctrine 会计信条58accounting document 会计凭证59accounting elements 会计要素60accounting entity 会计主体,会计个体61accounting entry 会计分录62accounting equation 会计等式63accounting event 会计事项64accounting exposure 会计暴露,会计暴露风险65accounting firm 会计事务所考试大论坛66Accounting Hall of Fame 会计名人堂67accounting harmonization 会计协调化68accounting identity 会计恒等式69accounting income 会计收益70accounting information 会计信息71accounting information system 会计信息系统72accounting internationalization 会计国际化73accounting journals 会计杂志74accounting legislation 会计法规75accounting manual 会计手册76accounting objective 会计目标77accounting period 会计期78accounting policies 会计政策79accounting postulate 会计假设80accounting practice 会计实务81accounting principle 会计原则82Accounting Principle Board 会计原则委员会83accounting procedures 会计程序84accounting profession 会计职业,会计专业85accounting rate of return 会计收益率86accounting records 会计记录,会计簿籍87Accounting Review 《会计评论》88accounting rules 会计规则89Accounting Series Release 《会计公告文件》90accounting service 会计服务91accounting software 会计软件92accounting standard 会计标准,会计准则93accounting standardization 会计标准化94Accounting Standards Board 会计准则委员会(英)95Accounting Standards Committee 会计准则委员会(英)96accounting system①会计制度②会计系统97accounting technique 会计技术98accounting theory 会计理论99accounting transaction 会计业务,会计账务100Accounting Trend and Techniques 《会计趋势和会计技术》101accounting unit 会计单位102accounting valuation 会计计价103accounting year 会计年度104accounts 会计账簿,会计报表105account sales 承销清单,承销报告单106accounts payable 应付账款107accounts receivable 应收账款108accounts receivable aging schedule 应收账款账龄分析表109accounts receivable assigned 已转让应收账款110accounts receivable collection period应收账款收款期111accounts receivable discounted 已贴现应收账款112accounts receivable financing 应收账款筹资,应收账款融资113accounts receivable management 应收账款管理114accounts receivable turnover 应收账款周转率,应收账款周转次数115accretion 增殖116accrual basis accounting 应计制会计,权责发生制会计117accrued asset 应计资产118accrued expense 应计费用119accrued liability 应计负债120accrued revenue 应计收入121accumulated depreciation 累计折旧122accumulated dividend 累计股利123accumulated earnings tax 累积盈余税,累积收益税124accumulation 累积,累计125acid test ratio 酸性试验比率126acquired company 被盘购公司,被兼并公司127acquisition 购置,盘购128acquisition accounting 盘购会计129acquisition cost 购置成本130acquisition decision 购置决策131acquisition excess 盘购超支132acquisition surplus 盘购盈余133across-the-board 全面调整134ACT 预交公司税135act 法案,法规136action 起诉,诉讼137active account 活动账户138active assets 活动资产139activity 业务活动,作业140activity account 作业账户141activity accounting 作业会计142activity ratio 业务活动比率143activity variance 业务活动量差异144act of bankruptcy 破产法145act of company 公司法146act of God 天灾,不可抗力147actual capital 实际资本148actual value 实际价值149actual wage 实际工资150added value 增值151added value statement 增值表152added value tax 增值税153addition 增置,扩建154additional depreciation 附加折旧,补提折旧155additional paid-in capital 附加实缴资本156additional tax 附加税157adequate disclosure 充分披露158adjunct account 附加账户159adjustable-rate bond 可调整利率债券160adjusted gross income 调整后收益总额,调整后所得总额161adjusted trial balance 调整后试算表162adjusting entry 调整分录163adjustment 调整164adjustment account 调整账户165adjustment bond 调整债券166administrative accounting 行政管理会计167administrative budget 行政管理预算168administrative expense行政管理费用169ADR 资产折旧年限幅度170ad valorem tax 从价税171advance 预付款,垫付款172advance corporation tax 预交公司税173advances from customers 预收客户款174advance to suppliers 预付货款175adventure 投机经营,短期经营176adverse opinion 反面意见,否定意见177adverse variance 不利差异,逆差178advisory services咨询服务179affiliated company 联营公司180affiliation 联营181after closing trial balance 结账后试算表182after cost 售后成本183after date 出票后兑付184after sight 见票后兑付185after-tax 税后186AGA 政府会计师联合会187age 寿命,账龄,资产使用年限188age allowance年龄减免189age analysis 账龄分析190agency 代理,代理关系191agency commission 代理佣金192agency fund 代管基金193agenda 议事日程,备忘录194agent 代理商,代理人195aggregate balance sheet 合并资产负债表196aggregate income statement 合并损益表197AGI 调整后收益总额,调整后所得总额198aging of accounts receivable应收账款账龄分析199aging schedule 账龄表200agio 贴水,折价201agiotage 汇兑业务,兑换业务202AGM 年度股东大会203agreement 协议204agreement of partnership 合伙协议205AICPA 美国注册公共会计师协会206AIS 会计信息系统207all capital earnings rate 资本总额收益率208all-inclusive income concept 总括收益概念209allocation 分摊,分配210allocation criteria分配标准211allotment①分配,拨付②分配数,拨付数212allowance①备抵②折让③津贴213allowance for bad debts 呆账备抵214allowance for depreciation 折旧备抵账户215allowance method 备抵法216all-purpose financial statement 通用财务报表,通用会计报表217alpha risk 阿尔法风险,第一种审计风险218altered check 涂改支票219alternative accounting methods 可选择性会计方法220alternative proposals 替代方案,备选方案221amalgamation 企业合并222American Accounting Association 美国会计学会223American depository receipts 美国银行证券存单,美国银行证券托存收据224American Institute of Certified Public Accountants 美国注册会计师协会,美国注册公共会计师协会225American option 美式期权226American Stock Exchange 美国股票交易所227amortization①摊销②摊还228amortized cost 摊余成本229amount 金额,合计230amount differ 金额不符231amount due 到期金额232amount of 1 dollar 1元的本利和233analysis 分析234analyst分析师235analytical review 分析性检查236annual audit 年度审计237annual closing 年度结账238annual general meeting 年度股东大会239annualize 按年折算240annualized net present value 折算年度净现值241annual report 年度报告242annuity 年金243annuity due期初年金244annuity in advance预付年金245annuity in arrears迟付年金246annuity method of depreciation 年金折旧法247antedate 填早日期248anticipation 预计,预列249anti-dilution clause 防止稀释条款250anti-pollution investment 消除污染投资251anti-profiteering tax 反暴利税252anti-tax avoidance 反避税253anti-trust legislation 反拖拉斯立法254A/P 应付账款255APB 会计原则委员会256APB Opinion 《会计原则委员会意见书》257Application申请,申请书258applied overhead 已分配间接费用259appraisal 估价260appraisal capital 评估资本261appraisal surplus 估价盈余262appraiser 估价员,估价师263appreciation 增值264appropriated retained earnings 已拨定留存收益,已指定用途留存收益265appropriation 拨款,指拨经费266appropriation account ①拨款账户②留存收益分配账户267appropriation budget拨款预算268approval 核定,审批269approved account 核定账户270approved bond 核定债券271A/R 应收账款272arbitrage 套利,套汇273arbitrage transaction 套利业务,套汇业务274arbitration 仲裁,公断275arithmetical error 算术误差276arm,s-length price 正常价格,公正价格277arm,s-length transaction 一臂之隔交易,正常交易278ARR 会计收益率279arrears①拖欠,欠款②迟付280arrestment 财产扣押281Authur Anderson & Co. 约瑟?安德森会计师事务所,安达信会计师事务所282article 文件条文,合同条款283articles of incorporation公司章程284articles of partnership 合伙契约285articulate 环接286articulated concept 环接观念287artificial intelligence 人工智能288ASB 审计准则委员会289ASE美国股票交易所290Asian Development Bank 亚洲开发银行291Asian dollar 亚洲美元292asking price 索价,卖方报价293assessed value 估定价值294assessment①估定,查定②特别税捐,特别摊派税捐295asset 资产296asset cover 资产担保,资产保证297asset depreciation range 资产折旧年限幅度298asset-liability view 资产—负债观念299asset quality 资产质量300asset retirement 资产退役,资产报废。

财务会计英文对照.doc

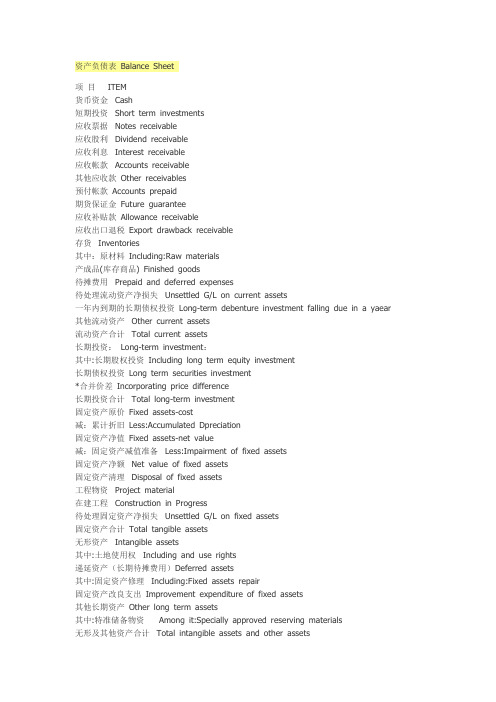

资产负债表Balance Sheet项目ITEM货币资金Cash短期投资Short term investments应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款Other receivables预付帐款Accounts prepaid期货保证金Future guarantee应收补贴款Allowance receivable应收出口退税Export drawback receivable存货Inventories其中:原材料Including:Raw materials产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets流动资产合计Total current assets长期投资:Long-term investment:其中:长期股权投资Including long term equity investment长期债权投资Long term securities investment*合并价差Incorporating price difference长期投资合计Total long-term investment固定资产原价Fixed assets-cost减:累计折旧Less:Accumulated Dpreciation固定资产净值Fixed assets-net value减:固定资产减值准备Less:Impairment of fixed assets固定资产净额Net value of fixed assets固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理Including:Fixed assets repair固定资产改良支出Improvement expenditure of fixed assets其他长期资产Other long term assets其中:特准储备物资Among it:Specially approved reserving materials无形及其他资产合计Total intangible assets and other assets递延税款借项Deferred assets debits资产总计Total Assets资产负债表(续表) Balance Sheet项目ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款Other payable to government其他应付款Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year 其他流动负债Other current liabilities流动负债合计Total current liabilities长期借款Long-term loans payable应付债券Bonds payable长期应付款long-term accounts payable专项应付款Special accounts payable其他长期负债Other long-term liabilities其中:特准储备资金Including:Special reserve fund长期负债合计Total long term liabilities递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"s capital 集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve公益金public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列)Unaffirmed investment loss未分配利润Retained earnings外币报表折算差额Converted difference in Foreign Currency Statements所有者权益合计Total shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表INCOME STATEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales减:销售折扣与折让Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales减:销售费用Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额Total profit减:所得税Less:Income tax净利润Net profit现金流量表Cash Flows StatementPrepared by:Period: Unit:Items1.Cash Flows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)Value added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activities2.Cash Flows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible 23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activities3.Cash Flows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activities4.Effect of Foreign Exchange Rate Changes on Cash Increase in Cash and Cash EquivalentsSupplemental Information1.Investing and Financing Activities that do not Involve in Cash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investories2.Reconciliation of Net Profit to Cash Flows from Operating Activities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activities Increase in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents现金流量表的现金流量声明拟制人:时间:单位:项目1.cash流量从经营活动:01 )所收到的现金从销售货物或提供劳务02 )收到的租金增值税销售额收到退款的价值03 )增值税缴纳04 )退回的其他税收和征费以外的增值税07 )其他现金收到有关经营活动08 )分,总现金流入量09 )用现金支付的商品和服务10 )用现金支付经营租赁11 )用现金支付,并代表员工12 )增值税购货支付13 )所得税的缴纳14 )支付的税款以外的增值税和所得税17 )其他现金支付有关的经营活动18 )分,总的现金流出19 )净经营活动的现金流量2.cash流向与投资活动:20 )所收到的现金收回投资21 )所收到的现金从分配股利,利润22 )所收到的现金从国债利息收入现金净额收到的处置固定资产,无形资产23 )资产和其他长期资产26 )其他收到的现金与投资活动27 )小计的现金流入量用现金支付购建固定资产,无形资产28 )和其他长期资产29 )用现金支付,以获取股权投资30 )用现金支付收购债权投资33 )其他现金支付的有关投资活动34 )分,总的现金流出35 )的净现金流量,投资活动产生3.cash流量筹资活动:36 )的收益,从发行股票37 )的收益,由发行债券38 )的收益,由借款41 )其他收益有关的融资活动42 ),小计的现金流入量43 )的现金偿还债务所支付的44 )现金支付的费用,对任何融资活动45 )支付现金,分配股利或利润46 )以现金支付的利息费用47 )以现金支付,融资租赁48 )以现金支付,减少注册资本51 )其他现金收支有关的融资活动52 )分,总的现金流出53 )的净现金流量从融资活动4.effect的外汇汇率变动对现金增加现金和现金等价物补充资料1.investing活动和筹资活动,不参与现金收款和付款56 )偿还债务的转让固定资产57 )偿还债务的转移投资58 )投资在形成固定资产59 )偿还债务的转移库存量2.reconciliation净利润现金流量从经营活动62 )净利润63 )补充规定的坏帐或不良债务注销64 )固定资产折旧65 )无形资产摊销损失处置固定资产,无形资产66 )和其他长期资产(或减:收益)67 )损失固定资产报废68 )财务费用69 )引起的损失由投资管理(或减:收益)70 )defered税收抵免(或减:借记卡)71 )减少存货(或减:增加)72 )减少经营性应收(或减:增加)73 )增加的经营应付账款(或减:减少)74 )净支付的增值税(或减:收益净额75 )净经营活动的现金流量增加现金和现金等价物76 )的现金,在此期限结束77 )减:现金期开始78 )加:现金等价物在此期限结束79 )减:现金等价物期开始80 ),净增加现金和现金等价物。

财务会计用英语怎么说

财务会计用英语怎么说财务会计是现代企业的一项重要的基础性工作,通过一系列会计程序,提供决策有用的信息,并积极参与经营管理决策,提高企业经济效益,服务于市场经济的健康有序发展。

那么你知道财务会计用英语怎么说吗?下面店铺为大家带来财务会计的英语说法,供大家参考学习。

财务会计的英语说法:financial accounting财务会计相关英语表达:工业企业财务会计 Accounting in Industrial Enterprises中级财务会计 Intermediate Financial Accounting财务会计理论 Financial Accounting Theory高级财务会计学 Advanced Financial Accounting财务会计的英语例句:1. Financial Accounting and Management Accounting.财务会计和管理会计.2. Provides U . S corporate finance accountant and the tax affairs processes.提供美国公司财务会计及税务处理.3. The article analyses the component parts of financial accounting report in detail.对企业的财务会计报告的组成部分进行了一一的详细分析.4. Social responsibility of accounting for financial accounting development an important extension.社会责任会计是财务会计发展的一个重要延伸.5. You only specify particular functions when you customize in Financial Accounting.你在用户化财务会计的时候,也就具体化“公司”了.6. The most prominent among them is the FinancialAccounting Standards Board.在他们中间最卓越的是财务会计准则委员会(FASB).7. Financial AccountingManagerial Accounting are two major specialized fields in Accounting.财务会计和管理会计是会计的两个主要的专门领域.8. College degree, major in accounting or finance, preferred with accredited qualification.8大专以上毕业, 财务会计类专业.有会计从业资格证或会计职称者优先.9. In June 2005, FASB issued Statement no. 154, Accounting Changes and Error Corrections.2005年, 美国财务会计准则委员会发布了第154号财务会计准则公告“会计变更和错误更正”.10. Bachelors Degree in Finance, Accounting or related business degree.要求本科学历,财务, 会计或相关商学专业.11. Bachelor degree or above, majored in finance , accounting or related subjects.国家正规院校本科以上学力, 财务会计相关专业.12. Minimum 3 years finance, accounting or other relevant experience with multi - national companies.至少3年跨国公司财务, 会计相关经验.13. Financial accounting data are expected to be objective and verifiable.做财务会计报告是强制性;那就是说,它必须得做.14. Financial Accounting and Managerial Accounting are two major specialized fields in Accounting.财务会计和管理会计是会计的两个重要的专门范畴.15. SFAS Rules - Knowledge of applicable Financial Accounting and Standards Board ( FASB ) accounting rules.SFAS规则——熟悉可应用的财务会计和基准委员会 ( FASB ) 会计规则.。

财务会计英语练习及答案ch

财务会计英语练习及答案ch个人收集整理勿做商业用途CHAPTER 16 STATEMENT OF CASH FLOWS个人收集整理勿做商业用途Chapter 16—Statement of Cash FlowsTRUE/FALSE1. The statement of cash flows is not one of the basic financial statements.ANS: F DIF: 1 OBJ: 012. Cash, as the term is used for the statement of cash flows, could indicate either cash or cashequivalents.ANS: T DIF: 1 OBJ: 013. The statement of cash flows is an optional financial statement.ANS: F DIF: 1 OBJ: 014. The statement of cash flows shows the effects on cash ofa company's operating, investing,and financing activities.ANS: T DIF: 1 OBJ: 015. The statement of cash flows reports a firm's major sources of cash receipts and major uses ofcash payments for a period.ANS: T DIF: 1 OBJ: 016. Cash flows from operating activities, as part of the statement of cash flows, include cashtransactions that enter into the determination of net income.ANS: T DIF: 1 OBJ: 017. To arrive at cash flows from operations, it is necessary toconvert the income statement froman accrual basis to the cash basis of accounting.ANS: T DIF: 2 OBJ: 018. Cash flows from investing activities, as part of the statement of cash flows, include receiptsfrom the sale of land.ANS: T DIF: 2 OBJ: 019. Cash flows from financing activities, as part of the statement of cash flows, include paymentsfor dividends.ANS: T DIF: 2 OBJ: 0110. Cash flows from investing activities, as part of the statement of cash flows, include paymentsfor the purchase of treasury stock.ANS: F DIF: 2 OBJ: 0111. Cash flows from investing activities, as part of the statement of cash flows, include receiptsfrom the issuance of bonds payable.ANS: F DIF: 2 OBJ: 0112. There are two alternatives to reporting cash flows from operating activities in the statement ofcash flows: (1) the direct method and (2) the indirect method.ANS: T DIF: 1 OBJ: 0113. The direct method of preparing the operating activities section of the statement of cash flowsreports major classes of gross cash receipts and gross cash payments.ANS: T DIF: 1 OBJ: 0114. Under the direct method of reporting cash flows from operations, the major source of cash iscash received from customers.ANS: T DIF: 1 OBJ: 0115. The main disadvantage of the direct method of reporting cash flows from operating activitiesis that the necessary data are often costly to accumulate.ANS: T DIF: 2 OBJ: 0116. A major disadvantage of the indirect method of reporting cash flows from operating activitiesis that the difference between the net amount of cash flows from operating activities and net income is not emphasized.ANS: F DIF: 2 OBJ: 01个人收集整理勿做商业用途17. Cash outflows from financing activities include the payment of cash dividends, theacquisition of treasury stock, and the repayment of amounts borrowed.ANS: T DIF: 2 OBJ: 0118. Cash flows from investing activities, as part of the statement of cash flows, include paymentsfor the acquisition of fixed assets.ANS: T DIF: 2 OBJ: 0119. The acquisition of land in exchange for common stock is an example of noncash investing andfinancing activity.ANS: T DIF: 2 OBJ: 0120. If a business issued bonds payable in exchange for land, the transaction would be reported in aseparate schedule on the statement of cash flows.ANS: T DIF: 2 OBJ: 0121. A cash flow per share amount should be reported on thestatement of cash flows.ANS: F DIF: 1 OBJ: 0122. Although there is no order in which the noncash balance sheet accounts must be analyzed indetermining data for preparing the statement of cash flows by the indirect method, time can be saved and greater accuracy can be achieved by selecting the accounts in the reverse order in which they appear on the balance sheet.ANS: T DIF: 1 OBJ: 0223. The 2002 edition of Accounting Trends and Techniques reported that 90% of the companiessurveyed used the indirect method to report changes in cash flows from operations.ANS: F DIF: 2 OBJ: 0224. Rarely would the cash flows from operating activities, as reported on the statement of cashflows, be the same as the net income reported on the income statement.ANS: T DIF: 2 OBJ: 0225. If land costing $75,000 was sold for $135,000, the amount reported in the investing activitiessection of the statement of cash flows would be $75,000.ANS: F DIF: 2 OBJ: 0226. If land costing $150,000 was sold for $205,000, the $55,000 gain on the sale would be addedto net income in converting the net income reported on the income statement to cash flows from operating activities for the statement of cash flows prepared by the indirect method.ANS: F DIF: 2 OBJ: 0227. In preparing the cash flows from operating activitiessection of the statement of cash flows bythe indirect method, the net decrease in inventories from the beginning to the end of the period is added to net income for the period.ANS: T DIF: 2 OBJ: 0228. In determining the cash flows from operating activities for the statement of cash flows by theindirect method, the depreciation expense for the period is added to the net income for the period.ANS: T DIF: 2 OBJ: 0229. In preparing the cash flows from operating activities section of the statement of cash flows bythe indirect method, the amortization of bond discount for the period is deducted from the net income for the period.ANS: F DIF: 2 OBJ: 02个人收集整理勿做商业用途30. If cash dividends of $145,000 were declared during the year and the decrease in dividendspayable from the beginning to the end of the year was $7,000, the statement of cash flows would report $152,000 in the financing activities section.ANS: T DIF: 2 OBJ: 0231. The declaration and issuance of a stock dividend would be reported on the statement of cashflows.ANS: F DIF: 2 OBJ: 0232. If 900 shares of $40 par common stock are sold for $48,000, the $48,000 would be reported inthe cash flows from financing activities section of the statement of cash flows.ANS: T DIF: 2 OBJ: 0233. If $500,000 of bonds payable are sold at 101, $500,000 would be reported in the cash flowsfrom financing activities section of the statement of cash flows.ANS: F DIF: 2 OBJ: 0234. Net income was $ 52,000 for the year. The accumulated depreciation balance increased by$17,000 over the year. There were no sales of fixed assets or changes in noncash current assets or liabilities. The cash flow from operations is $35,000ANS: F DIF: 2 OBJ: 0235. Net income for the year was $29,000. Accounts receivable increased $2,500, and accountspayable increased $5,100. The cash flow from operations is $31,600.ANS: T DIF: 2 OBJ: 0236. A building with a cost of $153,000 and accumulated depreciation of $42,000 was sold for an$11,000 gain. The cash generated from this investing activity was $121,000.ANS: F DIF: 2 OBJ: 0237. The indirect method reports cash received from customers in the cash flows from operatingactivities section of the statement of cash flows.ANS: F DIF: 2 OBJ: 0238. Cash paid to acquire treasury stock should be shown on the statement of cash flows frominvesting activities.ANS: F DIF: 2 OBJ: 0239. Repayments of bonds would be shown as a cash outflow in the investing section of thestatement of cash flows.ANS: F DIF: 2 OBJ: 0240. Acquiring equipment by issuing a six-month note should be shown on the statement of cashflows under the investing activities section.ANS: F DIF: 2 OBJ: 0241. In reporting cash flows from investing activities on the statement of cash flows, the cashinflows are usually reported first, followed by the cash outflows.ANS: T DIF: 1 OBJ: 0242.Cash inflows and outflows are not netted in any activity section of the statement of cash flows but are separately disclosed to give the reader full information.ANS: T DIF: 1 OBJ: 0243. The manner of reporting cash flows from investing and financing activities will be differentunder the direct method as compared to the indirect method.ANS: F DIF: 1 OBJ: 0344. Sales reported on the income statement were $375,000. The accounts receivable balancedeclined $6,500 over the year. The amount of cash received from customers was $368,500.个人收集整理勿做商业用途ANS: F DIF: 2 OBJ: 0345. To determine cash payments for merchandise for the cash flow statement using the directmethod, a decrease in accounts payable is added to the cost of merchandise sold.ANS: T DIF: 2 OBJ: 0346. To determine cash payments for operating expenses for the cash flow statement using thedirect method, a decrease in prepaid expenses is added to operating expenses other thandepreciation.ANS: F DIF: 2 OBJ: 0347. To determine cash payments for operating expenses for the cash flow statement using thedirect method, a decrease in accrued expenses is added to operating expenses other thandepreciation.ANS: T DIF: 2 OBJ: 0348. To determine cash payments for income tax for the cash flow statement using the directmethod, an increase in income taxes payable is added to the income tax expense.ANS: F DIF: 2 OBJ: 0349. Free cash flow is cash flow from operations, less cash used to purchase fixed assets tomaintain productive capacity and cash used for dividends.ANS: T DIF: 1 OBJ: 0450. Free cash flow is the measure of operating cash flow available for corporate purposes afterproviding sufficient fixed asset additions to maintain current productive capacity anddividends.ANS: T DIF: 1 OBJ: 04MULTIPLE CHOICE1. Which of the following is not one of the four basic financial statements?a. balance sheetb. statement of cash flowsc. statement of changes in financial positiond. income statementANS: C DIF: 1 OBJ: 012. Which of the following concepts of cash is not appropriate to use in preparing the statementof cash flows?a. cashb. cash and money market fundsc. cash and cash equivalentsd. cash and U.S. treasury bondsANS: D DIF: 2 OBJ: 013. The statement of cash flows reportsa. cash flows from operating activitiesb. total assetsc. total changes in stockholders' equityd. changes in retained earningsANS: A DIF: 1 OBJ: 014. On the statement of cash flows, the cash flows from operating activities section would includea. receipts from the issuance of capital stockb. receipts from the sale of investmentsc. payments for the acquisition of investments个人收集整理勿做商业用途d. cash receipts from sales activitiesANS: D DIF: 2 OBJ: 015. Preferred stock issued in exchange for land would be reported in the statement of cash flowsina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: C DIF: 2 OBJ: 016. Cash paid to purchase long-term investments would be reported in the statement of cash flowsina. the cash flows from operating activities sectionb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. a separate scheduleANS: C DIF: 2 OBJ: 017. A statement of cash flows would not disclose the effects of which of the followingtransactions?a. stock dividends declaredb. bonds payable exchanged for capital stockc. purchase of treasury stockd. capital stock issued to acquire fixed assetsANS: A DIF: 2 OBJ: 018. Which of the following does not represent an outflow of cash and therefore would not bereported on the statement of cash flows as a use of cash?a. purchase of noncurrent assetsb. purchase of treasury stockc. discarding an asset that had been fully depreciatedd. payment of cash dividendsANS: C DIF: 2 OBJ: 019. Which of the following represents an inflow of cash and therefore would be reported on thestatement of cash flows?a. appropriation of retained earningsb. acquisition of treasury stockc. declaration of stock dividendsd. issuance of long-term debtANS: D DIF: 2 OBJ: 0110. A ten-year bond was issued at par for $150,000 cash. This transaction should be shown on astatement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activitiesd. operating activitiesANS: B DIF: 1 OBJ: 0111. Cash paid for preferred stock dividends should be shown on the statement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activities个人收集整理勿做商业用途d. operating activitiesANS: B DIF: 2 OBJ: 0112. The last item on the statement of cash flows prior to the schedule of noncash investing andfinancing activities reportsa. the increase or decrease in cashb. cash at the end of the yearc. net cash flow from investing activitiesd. net cash flow from financing activitiesANS: B DIF: 2 OBJ: 0113. Which of the following is a noncash investing and financing activity?a. payment of a cash dividendb. payment of a six-month note payablec. purchase of merchandise inventory on accountd. issuance of common stock to acquire landANS: D DIF: 2 OBJ: 0114. Which of the following should be shown on a statement of cash flows under the financingactivity section?a. the purchase of a long-term investment in the common stock of another companyb. the payment of cash to retire a long-term notec. the proceeds from the sale of a buildingd. the issuance of a long-term note to acquire landANS: B DIF: 2 OBJ: 0115. A company purchases equipment for $29,000 cash. This transaction should be shown on thestatement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activitiesd. operating activitiesANS: A DIF: 2 OBJ: 0116. Cash flow per share isa. required to be reported on the balance sheetb. required to be reported on the income statementc. required to be reported on the statement of cash flowsd. not required to be reported on any statementANS: D DIF: 1 OBJ: 0117. On the statement of cash flows prepared by the indirect method, the cash flows from operatingactivities section would includea. receipts from the sale of investmentsb. amortization of premium on bonds payablec. payments for cash dividendsd. receipts from the issuance of capital stockANS: B DIF: 2 OBJ: 0118. The statement of cash flows may be used by management toa. assess the liquidity of the businessb. assess the major policy decisions involving investments and financingc. determine dividend policyd. do all of the aboveANS: D DIF: 1 OBJ: 01个人收集整理勿做商业用途19. Depreciation on factory equipment would be reported in the statement of cash flows preparedby the indirect method ina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: D DIF: 2 OBJ: 0220. Which of the following should be added to net income incalculating net cash flow fromoperating activities using the indirect method?a. an increase in inventoryb. a decrease in accounts payablec. preferred dividends declared and paidd. a decrease in accounts receivableANS: D DIF: 2 OBJ: 0221. Which of the following should be deducted from net income in calculating net cash flow fromoperating activities using the indirect method?a. depreciation expenseb. amortization of premium on bonds payablec. a loss on the sale of equipmentd. dividends declared and paidANS: B DIF: 2 OBJ: 0222. Which of the following below increases cash?a. depreciation expenseb. acquisition of treasury stockc. borrowing money by issuing a six-month noted. the declaration of a cash dividendANS: C DIF: 2 OBJ: 0223. Which one of the following below would not be classified as an operating activity?a. interest expenseb. income taxesc. payment of dividendsd. selling expensesANS: C DIF: 2 OBJ: 0224. Which one of the following below should be added to net income in calculating net cash flowfrom operating activities using the indirect method?a. a gain on the sale of landb. a decrease in accounts payablec. an increase in accrued liabilitiesd. dividends paid on common stockANS: C DIF: 2 OBJ: 0225. On the statement of cash flows prepared by the indirect method, a $50,000 gain on the sale ofinvestments would bea. deducted from net income in converting the net income reported on the incomestatement to cash flows from operating activitiesb. added to net income in converting the net income reported on the income statementto cash flows from operating activitiesc. added to dividends declared in converting the dividends declared to the cash flowsfrom financing activities related to dividends个人收集整理勿做商业用途d. deducted from dividends declared in converting the dividends declared to the cashflows from financing activities related to dividendsANS: A DIF: 2 OBJ: 0226. Accounts receivable arising from trade transactions amounted to $45,000 and $52,000 at thebeginning and end of the year, respectively. Net income reported on the income statement for the year was $105,000. Exclusive of the effect of other adjustments, the cash flows from operating activities to be reported on the statement of cash flows prepared by the indirect method isb. $112,000c. $98,000d. $140,000ANS: C DIF: 2 OBJ: 0227. The net income reported on the income statement for the current year was $275,000.Depreciation recorded on fixed assets and amortization of patents for the year were $40,000 and $9,000, respectively. Balances of current asset and current liability accounts at the end and at the beginning of the year are as follows:End Beginning Cash $ 50,000 $ 60,000 Accounts receivable 112,000 108,000 Inventories 105,000 93,000 Prepaid expenses 4,500 6,500 Accounts payable (merchandise creditors) 75,000 89,000 What is the amount of cash flows from operating activities reported on the statement of cash flows prepared by the indirect method?a. $198,000b. $324,000c. $352,000d. $296,000ANS: D DIF: 3 OBJ: 0228. The following information is available from the current period financial statements:Net income .................................... $140,000Depreciation expense ..................... 28,000Increase in accounts receivable ....... 16,000Decrease in accounts payable ......... 21,000The net cash flow from operating activities using the indirect method isb. $163,000c. $107,000d. $205,000ANS: A DIF: 3 OBJ: 0229. On the statement of cash flows, the cash flows from investing activities section would includea. receipts from the issuance of capital stockb. payments for dividendsc. payments for retirement of bonds payabled. receipts from the sale of investmentsANS: D DIF: 2 OBJ: 02个人收集整理勿做商业用途30. A building with a book value of $ 45,000 is sold for $50,000 cash. Using the indirect method,this transaction should be shown on the statement of cash flows as follows:a. an increase of $45,000 from investing activitiesb. an increase of $50,000 from investing activities and a deduction from net income of$5,000c. an increase of $50,000 from investing activitiesd. an increase of $45,000 from investing activities and an addition to net income of$5,000ANS: B DIF: 2 OBJ: 0231. Cash paid for equipment would be reported in the statement of cash flows ina. the cash flows from operating activities sectionb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. a separate scheduleANS: C DIF: 2 OBJ: 0232. If a gain of $9,000 is incurred in selling (for cash) office equipment having a book value of$55,000, the total amount reported in the cash flows from investing activities section of the statement of cash flows isa. $46,000b. $9,000c. $55,000d. $64,000ANS: D DIF: 2 OBJ: 0233. Which of the following types of transactions would be reported as a cash flow from investingactivity on the statement of cash flows?a. issuance of bonds payableb. issuance of capital stockc. purchase of treasury stockd. purchase of noncurrent assetsANS: D DIF: 2 OBJ: 0234. Land costing $47,000 was sold for $78,000 cash. The gain on the sale was reported on theincome statement as other income. On the statement of cash flows, what amount should be reported as an investing activity from the sale of land?a. $78,000b. $47,000c. $109,000d. $31,000ANS: A DIF: 2 OBJ: 0235. Equipment with an original cost of $50,000 and accumulated depreciation of $20,000 wassold at a loss of $7,000. As a result of this transaction, cash woulda. increase by $23,000b. decrease by $7,000c. increase by $43,000d. decrease by $30,000ANS: A DIF: 2 OBJ: 0236. On the statement of cash flows, the cash flows from financing activities section would includea. receipts from the sale of investmentsb. payments for the acquisition of investmentsc. receipts from a note receivabled. receipts from the issuance of capital stockANS: D DIF: 2 OBJ: 0237. On the statement of cash flows, the cash flows from financing activities section would includeall of the following excepta. receipts from the sale of bonds payableb. payments for dividendsc. payments for purchase of treasury stockd. payments of interest on bonds payableANS: D DIF: 2 OBJ: 0238. Cash dividends paid on capital stock would be reported in the statement of cash flows ina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: A DIF: 2 OBJ: 0239. Cash dividends of $80,000 were declared during the year. Cash dividends payable were$10,000 and $15,000 at the beginning and end of the year, respectively. The amount of cash for the payment of dividends during the year isa. $85,000b. $80,000c. $95,000d. $75,000ANS: D DIF: 2 OBJ: 0240. On the statement of cash flows, a $20,000 gain on the sale of fixed assets would bea. added to net income in converting the net income reported on the income statementto cash flows from operating activitiesb. deducted from net income in converting the net income reported on the incomestatement to cash flows from operating activitiesc. added to dividends declared in converting the dividends declared to the cash flowsfrom financing activities related to dividendsd. deducted from dividends declared in converting the dividends declared to the cashflows from financing activities related to dividendsANS: B DIF: 2 OBJ: 0241. A business issues 20-year bonds payable in exchange for preferred stock. This transactionwould be reported on the statement of cash flows ina. a separate scheduleb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. the cash flows from operating activities sectionANS: A DIF: 2 OBJ: 0242. Land costing $68,000 was sold for $50,000 cash. The loss on the sale was reported on theincome statement as other expense. On the statement of cash flows, what amount should be reported as an investing activity from the sale of land?a. $50,000b. $78,000c. $118,000d. $68,000ANS: A DIF: 2 OBJ: 0243. The current period statement of cash flows includes the flowing:Cash balance at the beginning of the period................... $410,000Cash provided by operating activities ............................ 185,000 Cash used in investing activities .................................... 43,000Cash used in financing activities .................................... 97,000 The cash balance at the end of the period isa. $45,000b. $735,000c. $455,000d. $85,000ANS: C DIF: 2 OBJ: 0244. On the statement of cash flows, the cash flows from operating activities section would includea. receipts from the issuance of capital stockb. payment for interest on short-term notes payablec. payments for the acquisition of investmentsd. payments for cash dividendsANS: B DIF: 2 OBJ: 0345. The cost of merchandise sold during the year was $50,000. Merchandise inventories were$12,500 and $10,500 at the beginning and end of the year, respectively. Accounts payable were $6,000 and $5,000 at the beginning and end of the year, respectively. Using the direct method of reporting cash flows from operating activities, cash payments for merchandise totala. $49,000b. $47,000c. $51,000d. $53,000ANS: A DIF: 2 OBJ: 0346. Sales for the year were $600,000. Accounts receivable were $100,000 and $80,000 at thebeginning and end of the year. Cash received from customers to be reported on the cash flow statement using the direct method isa. $700,000b. $600,000c. $580,000d. $620,000ANS: D DIF: 2 OBJ: 0347. Operating expenses other than depreciation for the year were $400,000. Prepaid expensesincreased by $17,000 and accrued expenses decreased by $30,000 during the year. Cash payments for operating expensesto be reported on the cash flow statement using the direct method would bea. $353,000b. $413,000c. $447,000d. $383,000ANS: C DIF: 2 OBJ: 0348. The following selected account balances appeared on the financial statements of the FranklinCompany:Accounts Receivable, Jan. 1 ........... $13,000Accounts Receivable, Dec. 31 ........ 9,000Accounts Payable, Jan 1 ................ 4,000Accounts payable Dec. 31 .............. 7,000Merchandise Inventory, Jan 1 ......... 10,000Merchandise Inventory, Dec 31 ...... 15,000Sales ............................................. 56,000Cost of Goods Sold ........................ 31,000The Franklin Company uses the direct method to calculate net cash flow from operatingactivities. Cash collections from customers area. $56,000b. $52,000c. $60,000d. $45,000ANS: C DIF: 3 OBJ: 0349. The following selected account balances appeared on the financial statements of the FranklinCompany:Accounts Receivable, Jan. 1 ......... $13,000Accounts Receivable, Dec. 31 ...... 9,000Accounts Payable, Jan 1 .............. 4,000Accounts payable Dec. 31 ............ 7,000Merchandise Inventory, Jan 1 ....... 10,000Merchandise Inventory, Dec 31 .... 15,000Sales ........................................... 56,000Cost of Goods Sold ....................... 31,000The Franklin Company uses the direct method to calculate net cash flow from operatingactivities. Cash paid to suppliers isa. $39,000b. $33,000c. $29,000d. $23,000ANS: B DIF: 3 OBJ: 0350. Income tax was $400,000 for the year. Income tax payable was $30,000 and $40,000 at thebeginning and end of the year. Cash payments for income tax reported on the cash flow statement using the direct method isa. $400,000b. $390,000c. $430,000d. $440,000ANS: B DIF: 2 OBJ: 0351. Free cash flow isa. all cash in the bankb. cash from operationsc. cash from financing, less cash used to purchase fixed assets to maintain productive。

财务会计中英文对照(doc 8页)(完美版)

1AAA 美国会计学会2Abacus《算盘》杂志3abacus 算盘考试大论坛4Abandonment废弃,报废;委付5abandonment value 废弃价值6abatement①减免②冲销7ability to service debt 偿债能力8abnormal cost 异常成本9abnormal spoilage 异常损耗10above par 超过票面价值11above the line线上项目12absolute amount 绝对数,绝对金额13absolute endorsement 绝对背书14absolute insolvency 绝对无力偿付15absolute priority 绝对优先求偿权16absolute value 绝对值17absorb 摊配,转并18absorption account 摊配账户,转并账户19absorption costing 摊配成本计算法20abstract 摘要表考试大论坛21abuse 滥用职权22abuse of tax shelter 滥用避税项目23ACCA特许公认会计师公会24accelerated cost recovery system 加速成本收回制度25accelerated depreciation method 加速折旧法,快速折旧法26acceleration clause 加速偿付条款,提前偿付条款27acceptance①承兑②已承兑票据③验收28acceptance bill 承兑票据29acceptance register 承兑票据登记簿30acceptance sampling验收抽样31access time 存取时间32accommodation 融通33accommodation bill 融通票据34accommodation endorsement 融通背书35account①账户,会计科目②账簿,报表③账目,账项④记账36accountability 经营责任,会计责任37accountability unit 责任单位38Accountancy 《会计》杂志39accountancy 会计40accountant 会计员,会计师41accountant general 会计主任,总会计42accounting in charge 主管会计师43accountant,s legal liability 会计师的法律责任44accountant,s report 会计师报告45accountant,s responsibility 会计师职责46account form 账户式,账式47accounting①会计②会计学48accounting assumption 会计假定,会计假设49accounting basis 会计基准,会计基本方法50accounting changes 会计变更51accounting concept 会计概念52accounting control 会计控制53accounting convention 会计常规,会计惯例54accounting corporation 会计公司55accounting cycle 会计循环56accounting data 会计数据57accounting doctrine 会计信条58accounting document 会计凭证59accounting elements 会计要素60accounting entity 会计主体,会计个体61accounting entry 会计分录62accounting equation 会计等式63accounting event 会计事项64accounting exposure 会计暴露,会计暴露风险65accounting firm 会计事务所考试大论坛66Accounting Hall of Fame 会计名人堂67accounting harmonization 会计协调化68accounting identity 会计恒等式69accounting income 会计收益70accounting information 会计信息71accounting information system 会计信息系统72accounting internationalization 会计国际化73accounting journals 会计杂志74accounting legislation 会计法规75accounting manual 会计手册76accounting objective 会计目标77accounting period 会计期78accounting policies 会计政策79accounting postulate 会计假设80accounting practice 会计实务81accounting principle 会计原则82Accounting Principle Board 会计原则委员会83accounting procedures 会计程序84accounting profession 会计职业,会计专业85accounting rate of return 会计收益率86accounting records 会计记录,会计簿籍87Accounting Review 《会计评论》88accounting rules 会计规则89Accounting Series Release 《会计公告文件》90accounting service 会计服务91accounting software 会计软件92accounting standard 会计标准,会计准则93accounting standardization 会计标准化94Accounting Standards Board 会计准则委员会(英)95Accounting Standards Committee 会计准则委员会(英)96accounting system①会计制度②会计系统97accounting technique 会计技术98accounting theory 会计理论99accounting transaction 会计业务,会计账务100Accounting Trend and Techniques 《会计趋势和会计技术》101accounting unit 会计单位102accounting valuation 会计计价103accounting year 会计年度104accounts 会计账簿,会计报表105account sales 承销清单,承销报告单106accounts payable 应付账款107accounts receivable 应收账款108accounts receivable aging schedule 应收账款账龄分析表109accounts receivable assigned 已转让应收账款110accounts receivable collection period应收账款收款期111accounts receivable discounted 已贴现应收账款112accounts receivable financing 应收账款筹资,应收账款融资113accounts receivable management 应收账款管理114accounts receivable turnover 应收账款周转率,应收账款周转次数115accretion 增殖116accrual basis accounting 应计制会计,权责发生制会计117accrued asset 应计资产118accrued expense 应计费用119accrued liability 应计负债120accrued revenue 应计收入121accumulated depreciation 累计折旧122accumulated dividend 累计股利123accumulated earnings tax 累积盈余税,累积收益税124accumulation 累积,累计125acid test ratio 酸性试验比率126acquired company 被盘购公司,被兼并公司127acquisition 购置,盘购128acquisition accounting 盘购会计129acquisition cost 购置成本130acquisition decision 购置决策131acquisition excess 盘购超支132acquisition surplus 盘购盈余133across-the-board 全面调整134ACT 预交公司税135act 法案,法规136action 起诉,诉讼137active account 活动账户138active assets 活动资产139activity 业务活动,作业140activity account 作业账户141activity accounting 作业会计142activity ratio 业务活动比率143activity variance 业务活动量差异144act of bankruptcy 破产法145act of company 公司法146act of God 天灾,不可抗力147actual capital 实际资本148actual value 实际价值149actual wage 实际工资150added value 增值151added value statement 增值表152added value tax 增值税153addition 增置,扩建154additional depreciation 附加折旧,补提折旧155additional paid-in capital 附加实缴资本156additional tax 附加税157adequate disclosure 充分披露158adjunct account 附加账户159adjustable-rate bond 可调整利率债券160adjusted gross income 调整后收益总额,调整后所得总额161adjusted trial balance 调整后试算表162adjusting entry 调整分录163adjustment 调整164adjustment account 调整账户165adjustment bond 调整债券166administrative accounting 行政管理会计167administrative budget 行政管理预算168administrative expense行政管理费用169ADR 资产折旧年限幅度170ad valorem tax 从价税171advance 预付款,垫付款172advance corporation tax 预交公司税173advances from customers 预收客户款174advance to suppliers 预付货款175adventure 投机经营,短期经营176adverse opinion 反面意见,否定意见177adverse variance 不利差异,逆差178advisory services咨询服务179affiliated company 联营公司180affiliation 联营181after closing trial balance 结账后试算表182after cost 售后成本183after date 出票后兑付184after sight 见票后兑付185after-tax 税后186AGA 政府会计师联合会187age 寿命,账龄,资产使用年限188age allowance年龄减免189age analysis 账龄分析190agency 代理,代理关系191agency commission 代理佣金192agency fund 代管基金193agenda 议事日程,备忘录194agent 代理商,代理人195aggregate balance sheet 合并资产负债表196aggregate income statement 合并损益表197AGI 调整后收益总额,调整后所得总额198aging of accounts receivable应收账款账龄分析199aging schedule 账龄表200agio 贴水,折价201agiotage 汇兑业务,兑换业务202AGM 年度股东大会203agreement 协议204agreement of partnership 合伙协议205AICPA 美国注册公共会计师协会206AIS 会计信息系统207all capital earnings rate 资本总额收益率208all-inclusive income concept 总括收益概念209allocation 分摊,分配210allocation criteria分配标准211allotment①分配,拨付②分配数,拨付数212allowance①备抵②折让③津贴213allowance for bad debts 呆账备抵214allowance for depreciation 折旧备抵账户215allowance method 备抵法216all-purpose financial statement 通用财务报表,通用会计报表217alpha risk 阿尔法风险,第一种审计风险218altered check 涂改支票219alternative accounting methods 可选择性会计方法220alternative proposals 替代方案,备选方案221amalgamation 企业合并222American Accounting Association 美国会计学会223American depository receipts 美国银行证券存单,美国银行证券托存收据224American Institute of Certified Public Accountants 美国注册会计师协会,美国注册公共会计师协会225American option 美式期权226American Stock Exchange 美国股票交易所227amortization①摊销②摊还228amortized cost 摊余成本229amount 金额,合计230amount differ 金额不符231amount due 到期金额232amount of 1 dollar 1元的本利和233analysis 分析234analyst分析师235analytical review 分析性检查236annual audit 年度审计237annual closing 年度结账238annual general meeting 年度股东大会239annualize 按年折算240annualized net present value 折算年度净现值241annual report 年度报告242annuity 年金243annuity due期初年金244annuity in advance预付年金245annuity in arrears迟付年金246annuity method of depreciation 年金折旧法247antedate 填早日期248anticipation 预计,预列249anti-dilution clause 防止稀释条款250anti-pollution investment 消除污染投资251anti-profiteering tax 反暴利税252anti-tax avoidance 反避税253anti-trust legislation 反拖拉斯立法254A/P 应付账款255APB 会计原则委员会256APB Opinion 《会计原则委员会意见书》257Application申请,申请书258applied overhead 已分配间接费用259appraisal 估价260appraisal capital 评估资本261appraisal surplus 估价盈余262appraiser 估价员,估价师263appreciation 增值264appropriated retained earnings 已拨定留存收益,已指定用途留存收益265appropriation 拨款,指拨经费266appropriation account ①拨款账户②留存收益分配账户267appropriation budget拨款预算268approval 核定,审批269approved account 核定账户270approved bond 核定债券271A/R 应收账款272arbitrage 套利,套汇273arbitrage transaction 套利业务,套汇业务274arbitration 仲裁,公断275arithmetical error 算术误差276arm,s-length price 正常价格,公正价格277arm,s-length transaction 一臂之隔交易,正常交易278ARR 会计收益率279arrears①拖欠,欠款②迟付280arrestment 财产扣押281Authur Anderson & Co. 约瑟?安德森会计师事务所,安达信会计师事务所282article 文件条文,合同条款283articles of incorporation公司章程284articles of partnership 合伙契约285articulate 环接286articulated concept 环接观念287artificial intelligence 人工智能288ASB 审计准则委员会289ASE美国股票交易所290Asian Development Bank 亚洲开发银行291Asian dollar 亚洲美元292asking price 索价,卖方报价293assessed value 估定价值294assessment①估定,查定②特别税捐,特别摊派税捐295asset 资产296asset cover 资产担保,资产保证297asset depreciation range 资产折旧年限幅度298asset-liability view 资产—负债观念299asset quality 资产质量300asset retirement 资产退役,资产报废。

财务会计及科目管理知识分析中英文对照(DOC 37页)

财务会计及科目管理知识分析中英文对照(DOC 37页)1123 短期投资-政府债券short-term inv estments - government bonds1124 短期投资-受益凭证short-term inv estments - beneficiary certificates1125 短期投资-公司债short-term inves tments - corporate bonds1128 短期投资-其它short-term investme nts - other1129 备抵短期投资跌价损失allowance fo r reduction of short-term investment to market113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现discounted notes rec eivable1137 应收票据-关系人notes receivable - related parties1138 其它应收票据other notes receivab le1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivabl e114 应收帐款accounts receivable1141 应收帐款accounts receivable 1142 应收分期帐款installment accounts receivable1147 应收帐款-关系人accounts receiva ble - related parties1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts recei vable118 其它应收款other receivables1181 应收出售远汇款forward exchange contract receivable1182 应收远汇款-外币forward exchang e contract receivable - foreign currencie s1183 买卖远汇折价discount on forward ex-change contract1184 应收收益earned revenue receivabl e1185 应收退税款income tax refund rece ivable1187 其它应收款- 关系人other receivables - related parties1188 其它应收款- 其它other receivable s - other1189 备抵呆帐- 其它应收款allowance f or uncollec- tible accounts - other receiv ables121~122 存货inventories1211 商品存货merchandise inventory 1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失allowance for r eduction of inventory to market1221 制成品finished goods1222 寄销制成品consigned finished goo ds1223 副产品by-products1224 在制品work in process1225 委外加工work in process - outsou rced1226 原料raw materials1227 物料supplies1228 在途原物料materials and suppliesin transit1229 备抵存货跌价损失allowance for re duction of inventory to market125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费prepaid insurance 1254 用品盘存office supplies1255 预付所得税prepaid income tax 1258 其它预付费用other prepaid expens es126 预付款项prepayments1261 预付货款prepayment for purchase s1268 其它预付款项other prepayments 128~129 其它流动资产other current asse ts1281 进项税额VAT paid ( or input ta x)1282 留抵税额excess VAT paid (or ove rpaid VAT)1283 暂付款temporary payments1284 代付款payment on behalf of other s1285 员工借支advances to employees 1286 存出保证金refundable deposits 1287 受限制存款certificate of deposit-res tricted1291 递延所得税资产deferred income ta x assets1292 递延兑换损失deferred foreign exc hange losses1293 业主(股东)往来owners'(stockholder s') current account1294 同业往来current account with othe rs1298 其它流动资产-其它other current a ssets - other13 基金及长期投资funds and long-term investments131 基金funds1311 偿债基金redemption fund (or sink ing fund)1312 改良及扩充基金fund for improvement and expansion1313 意外损失准备基金contingency fun d1314 退休基金pension fund1318 其它基金other funds132 长期投资long-term investments 1321 长期股权投资long-term equity inve stments1322 长期债券投资long-term bond inves tments1323 长期不动产投资long-term real esta te in-vestments1324 人寿保险现金解约价值cash surren der value of life insurance1328 其它长期投资other long-term inve stments1329 备抵长期投资跌价损失allowance fo r excess of cost over market value of lo ng-term investments14~ 15 固定资产property , plant, and e quipment141 土地land1411 土地land1418 土地-重估增值land - revaluation i ncrements142 土地改良物land improvements 1421 土地改良物land improvements 1428 土地改良物-重估增值land improv ements - revaluation increments1429 累积折旧-土地改良物accumulated depreciation - land improvements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值buildings -re valuation increments1439 累积折旧-房屋及建物accumulated depreciation - buildings144~146 机(器)具及设备machinery and e quipment1441 机(器)具machinery1448 机(器)具-重估增值machinery - re valuation increments1449 累积折旧-机(器)具accumulated de preciation - machinery151 租赁资产leased assets1511 租赁资产leased assets1519 累积折旧-租赁资产accumulated d epreciation - leased assets152 租赁权益改良leasehold improvement s1521 租赁权益改良leasehold improveme nts1529 累积折旧- 租赁权益改良accumulat ed depreciation - leasehold improvement s156 未完工程及预付购置设备款constructi on in progress and prepayments for equi pment1561 未完工程construction in progress 1562 预付购置设备款prepayment for eq uipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous propert y, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - reva luation increments1589 累积折旧- 杂项固定资产accumulate d depreciation - miscellaneous property, plant, and equipment16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resourc es -revaluation increments1619 累积折耗-天然资源accumulated d epletion - natural resources17 无形资产intangible assets171 商标权trademarks1711 商标权trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权franchise174 著作权copyright1741 著作权copyright175 计算机软件computer software1751 计算机软件computer software c ost176 商誉goodwill1761 商誉goodwill177 开办费organization costs1771 开办费organization costs178 其它无形资产other intangibles 1781 递延退休金成本deferred pensio n costs1782 租赁权益改良leasehold improveme nts1788 其它无形资产-其它other intangible assets - other18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond iss uance costs1812 长期预付租金long-term prepaid re nt1813 长期预付保险费long-term prepaid i nsurance1814 递延所得税资产deferred income tax assets1815 预付退休金prepaid pension cost 1818 其它递延资产other deferred asset s182 闲置资产idle assets1821 闲置资产idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receiv ables1841 长期应收票据long-term notes re ceivable1842 长期应收帐款long-term accounts re ceivable1843 催收帐款overdue receivables 1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and over due receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accou nts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others 1851 出租资产assets leased to other s1858 出租资产-重估增值assets leased t o others - incremental value from revalu ation1859 累积折旧-出租资产accumulated d epreciation - assets leased to others186 存出保证金refundable deposit 1861 存出保证金refundable deposit s188 杂项资产miscellaneous assets 1881 受限制存款certificate of deposit - restricted1888 杂项资产-其它miscellaneous asset s - other2 负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(d ebt)2111 银行透支bank overdraft2112 银行借款bank loan2114 短期借款-业主short-term borrowi ngs - owners2115 短期借款-员工short-term borrowi ngs - employees2117 短期借款-关系人short-term borr owings- related parties2118 短期借款-其它short-term borrowi ngs - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票bank acceptance 2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价discount on sho rt-term notes and bills payable213 应付票据notes payable2131 应付票据notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据other notes payabl e214 应付帐款accounts pay able2141 应付帐款accounts payable 2147 应付帐款-关系人accounts payable - related parties216 应付所得税income taxes payable 2161 应付所得税income tax payabl e217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金accrued rent payable 2173 应付利息accrued interest payabl e2174 应付营业税accrued VAT payable 2175 应付税捐-其它accrued taxes paya ble- other2178 其它应付费用other accrued expens es payable218~219 其它应付款other payables 2181 应付购入远汇款forward exchange contract payable2182 应付远汇款-外币forward exchang e contract payable - foreign currencies 2183 买卖远汇溢价premium on forward exchange contract2184 应付土地房屋款payables on land and building purchased2185 应付设备款Payables on equipmen t2187 其它应付款-关系人other payables - related parties2191 应付股利dividend payable2192 应付红利bonus payable2193 应付董监事酬劳compensation paya ble to directors and supervisors2198 其它应付款-其它other payables -other226 预收款项advance receipts2261 预收货款sales revenue received in advance2262 预收收入revenue received in adva nce2268 其它预收款other advance receipt s227 一年或一营业周期内到期长期负债lo ng-term liabilities -current portion 2271 一年或一营业周期内到期公司债corporate bonds payable - current portio n2272 一年或一营业周期内到期长期借款l ong-term loans payable - current portio n2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one ope rating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and ac counts payables to related parties - curr ent portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债other current liabilities2281 销项税额VAT received(or outp ut tax)2283 暂收款temporary receipts2284 代收款receipts under custody 2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债deferred income ta x liabilities2292 递延兑换利益deferred foreign exc hange gain2293 业主(股东)往来owners' current ac count2294 同业往来current account with oth ers2298 其它流动负债-其它other current li abilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds paya ble2311 应付公司债corporate bonds pay able2319 应付公司债溢(折)价premium(disco unt) on corporate bonds payable232 长期借款long-term loans payable 2321 长期银行借款long-term loans p ayable - bank2324 长期借款-业主long-term loans pay able - owners2325 长期借款-员工long-term loans pay able - employees2327 长期借款-关系人long-term loans p ayable - related parties2328 长期借款-其它long-term loans pay able - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes p ayable2332 长期应付帐款long-term accounts p ay-able2333 长期应付租赁负债long-term capita l lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - relate d parties2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabiliti es for land value increment tax2341 估计应付土地增值税estimated a ccrued land value incremental tax pay-a ble235 应计退休金负债accrued pension liab ilities2351 应计退休金负债accrued pension liabilities238 其它长期负债other long-term liabilit ies2388 其它长期负债-其它other long-ter m liabilities - other28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入deferred revenue 2814 递延所得税负债deferred income t ax liabilities2818 其它递延负债other deferred liabilit ies286 存入保证金deposits received2861 存入保证金guarantee deposit re ceived288 杂项负债miscellaneous liabilities 2888 杂项负债-其它miscellaneous lia bilities - other3 业主权益owners' equity31 资本capital311 资本(或股本)capital3111 普通股股本capital - common st ock3112 特别股股本capital - preferred stoc k3113 预收股本capital collected in advan ce3114 待分配股票股利stock dividends to be distributed3115 资本capital32 资本公积additional paid-in capital321 股票溢价paid-in capital in excess of par3211 普通股股票溢价paid-in capital i n excess of par- common stock3212 特别股股票溢价paid-in capital in excess of par- preferred stock323 资产重估增值准备capital surplus fr om assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积capital surplus fr om gain on disposal of assets3241 处分资产溢价公积capital surplu s from gain on disposal of assets325 合并公积capital surplus from busin ess combination3251 合并公积capital surplus from b usiness combination326 受赠公积donated surplus3261 受赠公积donated surplus328 其它资本公积other additional paid-in capital3281 权益法长期股权投资资本公积additional paid-in capital from investee un der equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-ac tions33 保留盈余(或累积亏损) retained earnin gs (accumulated deficit)331 法定盈余公积legal reserve3311 法定盈余公积legal reserve 332 特别盈余公积special reserve 3321 意外损失准备contingency reser ve3322 改良扩充准备improvement and exp ansion reserve3323 偿债准备special reserve for rede mption of liabilities3328 其它特别盈余公积other special res erve335 未分配盈余(或累积亏损) retained ea rnings-unappropriated (or accumulated d eficit)3351 累积盈亏accumulated profit orloss3352 前期损益调整prior period adjustm ents3353 本期损益net income or loss for c urrent period34 权益调整equity adjustments341 长期股权投资未实现跌价损失unr ealized loss on market value decline of l ong-term equity investments3411 长期股权投资未实现跌价损失u nrealized loss on market value decline of long-term equity investments342 累积换算调整数cumulative translati on adjustment3421 累积换算调整数cumulative tran slation adjustments343 未认列为退休金成本之净损失net lo ss not recognized as pension cost 3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股treasury stock351 库藏股treasury stock3511 库藏股treasury stock36 少数股权minority interest361 少数股权minority interest3611 少数股权minority interest4 营业收入operating revenue41 销货收入sales revenue411 销货收入sales revenue4111 销货收入sales revenue4112 分期付款销货收入installment sales revenue417 销货退回sales return4171 销货退回sales return419 销货折让sales allowances4191 销货折让sales discounts and al lowances46 劳务收入service revenue461 劳务收入service revenue4611 劳务收入service revenue47 业务收入agency revenue471 业务收入agency revenue4711 业务收入agency revenue48 其它营业收入other operating revenue488 其它营业收入-其它other operatin g revenue4888 其它营业收入-其它other operati ng revenue - other5 营业成本operating costs51 销货成本cost of goods sold511 销货成本cost of goods sold5111 销货成本cost of goods sold 5112 分期付款销货成本installment cost of goods sold512 进货purchases5121 进货purchases5122 进货费用purchase expenses5123 进货退出purchase returns5124 进货折让charges on purchased me rchandise513 进料materials purchased5131 进料material purchased5132 进料费用charges on purchased ma terial5133 进料退出material purchase return s5134 进料折让material purchase allowa nces514 直接人工direct labor5141 直接人工direct labor515~518 制造费用manufacturing overhe ad5151 间接人工indirect labor5152 租金支出rent expense, rent 5153 文具用品office supplies (expense) 5154 旅费travelling expense, travel 5155 运费shipping expenses, freight 5156 邮电费postage (expenses)5157 修缮费repair(s) and maintenance (expense )5158 包装费packing expenses5161 水电瓦斯费utilities (expense) 5162 保险费insurance (expense)5163 加工费manufacturing overhead - outsourced5166 税捐taxes5168 折旧depreciation expense5169 各项耗竭及摊提various amortizati on5172 伙食费meal (expenses)5173 职工福利employee benefits/welfar e5176 训练费training (expense)5177 间接材料indirect materials5188 其它制造费用other manufacturing expenses56 劳务成本制ervice costs561 劳务成本service costs5611 劳务成本service costs57 业务成本gency costs571 业务成本agency costs5711 业务成本agency costs58 其它营业成本other operating costs588 其它营业成本-其它other operatin g costs-other5888 其它营业成本-其它other operati ng costs - other6 营业费用operating expenses61 推销费用selling expenses615~618 推销费用selling expenses6151 薪资支出payroll expense 6152 租金支出rent expense, rent 6153 文具用品office supplies (expense) 6154 旅费travelling expense, travel 6155 运费shipping expenses, freight 6156 邮电费postage (expenses)6157 修缮费repair(s) and maintenance (expense)6159 广告费advertisement expense, adv ertisement6161 水电瓦斯费utilities (expense) 6162 保险费insurance (expense)6164 交际费entertainment (expense) 6165 捐赠donation (expense)6166 税捐taxes6167 呆帐损失loss on uncollectible acco unts6168 折旧depreciation expense6169 各项耗竭及摊提various amortizati on6172 伙食费meal (expenses)6173 职工福利employee benefits/welfar e6175 佣金支出commission (expense) 6176 训练费training (expense)6188 其它推销费用other selling expense s62 管理及总务费用general & administra tive expenses625~628 管理及总务费用general & a dministrative expenses6251 薪资支出payroll expense6252 租金支出rent expense, rent6253 文具用品office supplies6254 旅费travelling expense, travel 6255 运费shipping expenses,freight 6256 邮电费postage (expenses)6257 修缮费repair(s) and maintenance (expense)6259 广告费advertisement expense, adv ertisement6261 水电瓦斯费utilities (expense)6262 保险费insurance (expense)6264 交际费entertainment (expense) 6265 捐赠donation (expense)6266 税捐taxes6267 呆帐损失loss on uncollectible acco unts6268 折旧depreciation expense a6269 各项耗竭及摊提various amortizati on6271 外销损失loss on export sales 6272 伙食费meal (expenses)6273 职工福利employee benefits/welfar e6274 研究发展费用research and develop ment expense6275 佣金支出commission (expense) 6276 训练费training (expense)6278 劳务费professional service fees 6288 其它管理及总务费用other general and administrative expenses63 研究发展费用research and developme nt expenses635~638 研究发展费用research and development expenses6351 薪资支出payroll expense6352 租金支出rent expense, rent6353 文具用品office supplies6354 旅费travelling expense, travel 6355 运费shipping expenses, freight 6356 邮电费postage (expenses)6357 修缮费repair(s) and maintenance (expense)6361 水电瓦斯费utilities (expense) 6362 保险费insurance (expense)6364 交际费entertainment (expense) 6366 税捐taxes6368 折旧depreciation expense6369 各项耗竭及摊提various amortizatio n6372 伙食费meal (expenses)6373 职工福利employee benefits/welfar e6376 训练费training (expense)6378 其它研究发展费用other research and development expenses7 营业外收入及费用non-operating reven ue and expenses, other income(expense) 71~74 营业外收入non-operating reven ue711 利息收入interest revenue7111 利息收入interest revenue/incom e712 投资收益investment income 7121 权益法认列之投资收益investme nt income recognized under equity meth od7122 股利收入dividends income7123 短期投资市价回升利益gain on ma rket price recovery of short-term invest ment713 兑换利益foreign exchange gain 7131 兑换利益foreign exchange gain 714 处分投资收益gain on disposal of in vestments7141 处分投资收益gain on disposalof investments715 处分资产溢价收入gain on disposal of assets7151 处分资产溢价收入gain on dispo sal of assets748 其它营业外收入other non-operating revenue7481 捐赠收入donation income 7482 租金收入rent revenue/income 7483 佣金收入commission revenue/inco me7484 出售下脚及废料收入revenue from sale of scraps7485 存货盘盈gain on physical inventor y7486 存货跌价回升利益gain from price recovery of inventory7487 坏帐转回利益gain on reversal of bad debts7488 其它营业外收入-其它other non-ope rating revenue- other items75~ 78 营业外费用non-operating expenses751 利息费用interest expense7511 利息费用interest expense752 投资损失investment loss7521 权益法认列之投资损失investme nt loss recog- nized under equity metho d7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investm ents to market753 兑换损失foreign exchange loss 7531 兑换损失foreign exchange loss 754 处分投资损失loss on disposal of in vestments7541 处分投资损失loss on disposal o f investments755 处分资产损失loss on disposal of as sets7551 处分资产损失loss on disposal o f assets788 其它营业外费用other non-operating expenses7881 停工损失loss on work stoppage s7882 灾害损失casualty loss7885 存货盘损loss on physical inventor y7886 存货跌价及呆滞损失loss for marke t price decline and obsolete and slow-mo ving inventories7888 其它营业外费用-其它other non-ope rating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax exp ense (or benefit)811 所得税费用(或利益) income tax e xpense (or benefit)8111 所得税费用(或利益)income ta x expense ( or benefit)9 非经常营业损益nonrecurring gain or l oss91 停业部门损益gain(loss) from disco ntinued operations911 停业部门损益-停业前营业损益in come(loss) from operations of discontinue d segments9111 停业部门损益-停业前营业损益in come(loss) from operations of discontinue d segment912 停业部门损益-处分损益gain(loss) fr om disposal of discontinued segments 9121 停业部门损益-处分损益gain(loss) from disposal of discontinued segment 92 非常损益extraordinary gain or loss921 非常损益extraordinary gain or l oss9211 非常损益extraordinary gain or l oss93 会计原则变动累积影响数cumulative e ffect of changes in accounting principles 931 会计原则变动累积影响数cumulati ve effect of changes in accounting princi ples9311 会计原则变动累积影响数cumul ative effect of changes in accounting principles94 少数股权净利minority interest incom e941 少数股权净利minority interest in come9411 少数股权净利minority interest i ncom。

(财务会计)英语会计科目最全版

1500

FurnitureandFixtures

器具设备和装置

1510

Equipment

设备

1520

Vehicles

车辆

1530

OtherDepreciableProperty

其他可折旧资产

1540

LeaseholdImprovements

租赁物改良

1550

Buildings

建筑物

Buildingunderconstruction

在建工程

1560

BuildingImprovements

建筑物改良(支出)

1690

Land

土地

1700

AccumulatedDepreciation,FurnitureandFixtures

累计折旧—器具设备和装置

1710

AccumulatedDepreciation,Equipment

累计摊销费—开办费

1920

NotesReceivable,Non-current

应收票据—长期票据

1990

OtherNon-currentAssets

其他长期资产

LiabilityAccounts

CurrentLiabilities

2000

AccountsPayable

应付账款

2300

AccruedExpenses

投资—存款单

1100

AccountsReceivable

应收账款

1140

OtherReceivables

其他应收款

1150

AllowanceforDoubtfulAccounts

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1. 请将下列3篇内容全部翻译成英语,格式为英中段段对照;

2. 试译后,请将试译文发送到公司邮箱job@ 中。

第1篇

Borrowing costs are recognised in the statement of total return using the effective interest method, except to the extent that they are capitalised as being directly attributable to the acquisition, construction or production of an asset which necessarily takes a substantial period of time to be prepared for its intended use or sale.

第2篇

3.9 Provision

A provision is recognised if, as a result of a past event, the Group has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability. The unwinding of the discount is recognised as finance cost.

第3篇

* Investment in equity instruments carried at cost

Fair value information has not been disclosed for the Company's investments in equity instruments that are carried at cost because fair value cannot be measured reliably. These equity instruments represent ordinary shares in companies operating business parks in China, Taiwan and Vietnam. These investments are not quoted on any market and do not have any comparable industry peer that is listed. In addition, the variability in the range of reasonable fair value estimates of these investments derived from valuation techniques is significant.。