Chapter 6 Solutions

医学英语Chapter 6_Obesity Causes and Prevention

《当代医学·英语综合教程 II—关注健康》

catastrophic a. 悲惨的,灾难的

wage v.

开展,进行

adaptive a. 适应的,适合的

prescriptive a. 规定的,惯例的

gastric a. 胃的

bypass n. 旁路

morbid a. 病态的

obese a.

过度肥胖的

Obesity and Social Ties

《当代医学·英语综合教程 II—关注健康》

Chapter 6

When one person gains weight, their close friends often follow. Researchers have just (1)_o_f_f_e_re_d__ evidence in a study that says obesity appears to (2) _s_p_re_a_d__ through social ties. But the findings might also offer hope.

lipid n.

类脂(化合)物

execute v.

实施,执行

havoc n.

大破坏,浩劫

undernourished a. 营养不足的

《当代医学·英语综合教程 II—关注健康》

Chapter 6

strategically ad. exertion n. sedentary a. winch n. casket n.

《当代医学·英语综合教程 II—关注健康》

Chapter 6

obese. A sister or brother of a person who became obese had a 40 percent increased chance of becoming obese. The (10) _ri_s_k___ for a wife or husband was a little less than that.

数据库系统基础教程第六章答案

Solutions Chapter 6Attributes must be separated by commas. Thus here B is an alias of A.6.1.2a)SELECT address AS Studio_AddressFROM StudioWHERE NAME = 'MGM';b)SELECT birthdate AS Star_BirthdateFROM MovieStarWHERE name = 'Sandra Bullock';c)SELECT starNameFROM StarsInWHERE movieYear = 1980OR movieTitle LIKE '%Love%';However, above query will also return words that have the substring Love e.g. Lover. Below query will only return movies that have title containing the word Love.SELECT starNameFROM StarsInWHERE movieYear = 1980OR movieTitle LIKE 'Love %'OR movieTitle LIKE '% Love %'OR movieTitle LIKE '% Love'OR movieTitle = 'Love';d)SELECT name AS Exec_NameFROM MovieExecWHERE netWorth >= 10000000;e)SELECT name AS Star_NameFROM movieStarWHERE gender = 'M'OR address LIKE '% Malibu %';a)SELECT model,speed,hdFROM PCWHERE price < 1000 ;MODEL SPEED HD----- ---------- ------1002 2.10 2501003 1.42 801004 2.80 2501005 3.20 2501007 2.20 2001008 2.20 2501009 2.00 2501010 2.80 3001011 1.86 1601012 2.80 1601013 3.06 8011 record(s) selected.b)SELECT model ,speed AS gigahertz,hd AS gigabytesFROM PCWHERE price < 1000 ;MODEL GIGAHERTZ GIGABYTES ----- ---------- ---------1002 2.10 2501003 1.42 801004 2.80 2501005 3.20 2501007 2.20 2001008 2.20 2501009 2.00 2501010 2.80 3001011 1.86 1601012 2.80 1601013 3.06 8011 record(s) selected.c)SELECT makerFROM ProductWHERE TYPE = 'printer' ; MAKER-----DDEEEHH7 record(s) selected.d)SELECT model,ram ,screenFROM LaptopWHERE price > 1500 ; MODEL RAM SCREEN ----- ------ -------2001 2048 20.12005 1024 17.02006 2048 15.42010 2048 15.44 record(s) selected.e)SELECT *FROM PrinterWHERE color ;MODEL CASE TYPE PRICE----- ----- -------- ------3001 TRUE ink-jet 993003 TRUE laser 9993004 TRUE ink-jet 1203006 TRUE ink-jet 1003007 TRUE laser 2005 record(s) selected.Note: Implementation of Boolean type is optional in SQL standard (feature IDT031). PostgreSQL has implementation similar to above example. Other DBMS provide equivalent support. E.g. In DB2 the column type can be declare as SMALLINT with CONSTRAINT that the value can be 0 or 1. The result can be returned as Boolean type CHAR using CASE.CREATE TABLE Printer(model CHAR(4) UNIQUE NOT NULL,color SMALLINT ,type VARCHAR(8) ,price SMALLINT ,CONSTRAINT Printer_ISCOLOR CHECK(color IN(0,1)));SELECT model,CASE colorWHEN 1THEN 'TRUE'WHEN 0THEN 'FALSE'ELSE 'ERROR'END CASE ,type,priceFROM PrinterWHERE color = 1;f)SELECT model,hdFROM PCWHERE speed = 3.2AND price < 2000;MODEL HD----- ------1005 2501006 3202 record(s) selected.6.1.4a)SELECT class,countryFROM ClassesWHERE numGuns >= 10 ; CLASS COUNTRY------------------ ------------ Tennessee USA1 record(s) selected.b)SELECT name AS shipName FROM ShipsWHERE launched < 1918 ; SHIPNAME------------------HarunaHieiKirishimaKongoRamilliesRenownRepulseResolutionRevengeRoyal OakRoyal Sovereign11 record(s) selected.c)SELECT ship AS shipName, battleFROM OutcomesWHERE result = 'sunk' ; SHIPNAME BATTLE------------------ ------------------ Arizona Pearl Harbor Bismark Denmark Strait Fuso Surigao Strait Hood Denmark Strait Kirishima Guadalcanal Scharnhorst North Cape Yamashiro Surigao Strait 7 record(s) selected.d)SELECT name AS shipNameFROM ShipsWHERE name = class ;SHIPNAME------------------IowaKongoNorth CarolinaRenownRevengeYamato6 record(s) selected.e)SELECT name AS shipNameFROM ShipsWHERE name LIKE 'R%';SHIPNAME------------------RamilliesRenownRepulseResolutionRevengeRoyal OakRoyal Sovereign7 record(s) selected.Note: As mentioned in exercise 2.4.3, there are some dangling pointers and to retrieve all ships a UNION of Ships and Outcomes is required.Below query returns 8 rows including ship named Rodney.SELECT name AS shipNameFROM ShipsWHERE name LIKE 'R%'UNIONSELECT ship AS shipNameFROM OutcomesWHERE ship LIKE 'R%';f) Only using a filter like '% % %' will incorrectly match name such as ' a b ' since % can match any sequence of 0 or more characters.SELECT name AS shipNameFROM ShipsWHERE name LIKE '_% _% _%' ;SHIPNAME------------------0 record(s) selected.Note: As in (e), UNION with results from Outcomes.SELECT name AS shipNameFROM ShipsWHERE name LIKE '_% _% _%'UNIONSELECT ship AS shipNameFROM OutcomesWHERE ship LIKE '_% _% _%' ;SHIPNAME------------------Duke of YorkKing George VPrince of Wales3 record(s) selected.6.1.5a)The resulting expression is false when neither of (a=10) or (b=20) is TRUE.a = 10b = 20 a = 10 OR b = 20NULL TRUE TRUETRUE NULL TRUEFALSE TRUE TRUETRUE FALSE TRUETRUE TRUE TRUEb)The resulting expression is only TRUE when both (a=10) and (b=20) are TRUE.a = 10b = 20 a = 10 AND b = 20TRUE TRUE TRUEThe expression is always TRUE unless a is NULL.a < 10 a >= 10 a = 10 ANDb = 20TRUE FALSE TRUEFALSE TRUE TRUEd)The expression is TRUE when a=b except when the values are NULL.a b a = bNOT NULL NOT NULL TRUE when a=b; else FALSEe)Like in (d), the expression is TRUE when a<=b except when the values are NULL.a b a <= bNOT NULL NOT NULL TRUE when a<=b; else FALSE6.1.6SELECT *FROM MoviesWHERE LENGTH IS NOT NULL;6.2.1a)SELECT AS starNameFROM MovieStar M,StarsIn SWHERE = S.starNameAND S.movieTitle = 'Titanic'AND M.gender = 'M';b)SELECT S.starNameFROM Movies M ,StarsIn S,Studios TWHERE ='MGM'AND M.year = 1995AND M.title = S.movieTitleAND M.studioName = ;SELECT AS presidentName FROM MovieExec X,Studio TWHERE X.cert# = T.presC#AND = 'MGM';d)SELECT M1.titleFROM Movies M1,Movies M2WHERE M1.length > M2.lengthAND M2.title ='Gone With the Wind' ;e)SELECT AS execNameFROM MovieExec X1,MovieExec X2WHERE Worth > WorthAND = 'Merv Griffin' ;6.2.2a)SELECT R.maker AS manufacturer,L.speed AS gigahertzFROM Product R,Laptop LWHERE L.hd >= 30AND R.model = L.model ; MANUFACTURER GIGAHERTZ------------ ----------A 2.00A 2.16A 2.00B 1.83E 2.00E 1.73E 1.80F 1.60F 1.60G 2.0010 record(s) selected.SELECT R.model,P.priceFROM Product R,PC PWHERE R.maker = 'B'AND R.model = P.model UNIONSELECT R.model,L.priceFROM Product R,Laptop LWHERE R.maker = 'B'AND R.model = L.model UNIONSELECT R.model,T.priceFROM Product R,Printer TWHERE R.maker = 'B'AND R.model = T.model ; MODEL PRICE----- ------1004 6491005 6301006 10492007 14294 record(s) selected.c)SELECT R.makerFROM Product R,Laptop LWHERE R.model = L.model EXCEPTSELECT R.makerFROM Product R,PC PWHERE R.model = P.model ; MAKER-----FG2 record(s) selected.SELECT DISTINCT P1.hd FROM PC P1,PC P2WHERE P1.hd =P2.hdAND P1.model > P2.model ; Alternate Answer:SELECT DISTINCT P.hdFROM PC PGROUP BY P.hdHAVING COUNT(P.model) >= 2 ;e)SELECT P1.model,P2.modelFROM PC P1,PC P2WHERE P1.speed = P2.speed AND P1.ram = P2.ramAND P1.model < P2.model ; MODEL MODEL----- -----1004 10121 record(s) selected.f)SELECT M.makerFROM(SELECT maker,R.modelFROM PC P,Product RWHERE SPEED >= 3.0AND P.model=R.modelUNIONSELECT maker,R.modelFROM Laptop L,Product RWHERE speed >= 3.0AND L.model=R.model) MGROUP BY M.makerHAVING COUNT(M.model) >= 2 ; MAKER-----B1 record(s) selected.6.2.3a)SELECT FROM Ships S,Classes CWHERE S.class = C.classAND C.displacement > 35000;NAME------------------IowaMissouriMusashiNew JerseyNorth CarolinaWashingtonWisconsinYamato8 record(s) selected.b)SELECT ,C.displacement,C.numGunsFROM Ships S ,Outcomes O,Classes CWHERE = O.shipAND S.class = C.classAND O.battle = 'Guadalcanal' ;NAME DISPLACEMENT NUMGUNS------------------ ------------ -------Kirishima 32000 8Washington 37000 92 record(s) selected.Note:South Dakota was also engaged in battle of Guadalcanal but not chosen since it is not in Ships table(Hence, no information regarding it's Class isavailable).SELECT name shipName FROM ShipsUNIONSELECT ship shipName FROM Outcomes ; SHIPNAME------------------ArizonaBismarkCaliforniaDuke of YorkFusoHarunaHieiHoodIowaKing George VKirishimaKongoMissouriMusashiNew JerseyNorth CarolinaPrince of Wales RamilliesRenownRepulseResolutionRevengeRodneyRoyal OakRoyal Sovereign ScharnhorstSouth DakotaTenneseeTennesseeWashingtonWest VirginiaWisconsinYamashiroYamato34 record(s) selected.SELECT C1.countryFROM Classes C1,Classes C2WHERE C1.country = C2.country AND C1.type = 'bb'AND C2.type = 'bc' ; COUNTRY------------Gt. BritainJapan2 record(s) selected.e)SELECT O1.shipFROM Outcomes O1,Battles B1WHERE O1.battle = AND O1.result = 'damaged'AND EXISTS(SELECT B2.dateFROM Outcomes O2,Battles B2WHERE O2.battle= AND O1.ship = O2.shipAND B1.date < B2.date) ;SHIP------------------0 record(s) selected.f)SELECT O.battleFROM Outcomes O,Ships S ,Classes CWHERE O.ship = AND S.class = C.class GROUP BY C.country,O.battleHAVING COUNT(O.ship) > 3; SELECT O.battleFROM Ships S ,Classes C,Outcomes OWHERE C.Class = S.classAND O.ship = GROUP BY C.country,O.battleHAVING COUNT(O.ship) >= 3;6.2.4Since tuple variables are not guaranteed to be unique, every relation Ri should be renamed using an alias. Every tuple variable should be qualified with the alias. Tuple variables for repeating relations will also be distinctlyidentified this way.Thus the query will be likeSELECT A1.COLL1,A1.COLL2,A2.COLL1,…FROM R1 A1,R2 A2,…,Rn AnWH ERE A1.COLL1=A2.COLC2,…6.2.5Again, create a tuple variable for every Ri, i=1,2,...,nThat is, the FROM clause isFROM R1 A1, R2 A2,...,Rn An.Now, build the WHERE clause from C by replacing every reference to some attribute COL1 of Ri by Ai.COL1. In addition apply Natural Join i.e. add condition to check equality of common attribute names between Ri and Ri+1 for all i from 0 to n-1. Also, build the SELECT clause from list of attributes L by replacing every attribute COLj of Ri by Ai.COLj.6.3.1a)SELECT DISTINCT makerFROM ProductWHERE model IN(SELECT modelFROM PCWHERE speed >= 3.0);SELECT DISTINCT R.makerFROM Product RWHERE EXISTS(SELECT P.modelFROM PC PWHERE P.speed >= 3.0AND P.model =R.model);SELECT P1.modelFROM Printer P1WHERE P1.price >= ALL(SELECT P2.priceFROM Printer P2) ;SELECT P1.modelFROM Printer P1WHERE P1.price IN(SELECT MAX(P2.price)FROM Printer P2) ;c)SELECT L.modelFROM Laptop LWHERE L.speed < ANY(SELECT P.speedFROM PC P) ;SELECT L.modelFROM Laptop LWHERE EXISTS(SELECT P.speedFROM PC PWHERE P.speed >= L.speed ) ;SELECT modelFROM(SELECT model,priceFROM PCUNIONSELECT model,priceFROM LaptopUNIONSELECT model,priceFROM Printer) M1WHERE M1.price >= ALL (SELECT priceFROM PCUNIONSELECT priceFROM LaptopUNIONSELECT priceFROM Printer) ;(d) – contd --SELECT modelFROM(SELECT model,priceFROM PCUNIONSELECT model,priceFROM LaptopUNIONSELECT model,priceFROM Printer) M1WHERE M1.price IN(SELECT MAX(price)FROM(SELECT priceFROM PCUNIONSELECT priceFROM LaptopUNIONSELECT priceFROM Printer) M2) ;e)SELECT R.makerFROM Product R,Printer TWHERE R.model =T.model AND T.price <= ALL(SELECT MIN(price)FROM Printer);SELECT R.makerFROM Product R,Printer T1WHERE R.model =T1.model AND T1.price IN(SELECT MIN(T2.price) FROM Printer T2);f)SELECT R1.makerFROM Product R1,PC P1WHERE R1.model=P1.modelAND P1.ram IN(SELECT MIN(ram)FROM PC)AND P1.speed >= ALL(SELECT P1.speedFROM Product R1,PC P1WHERE R1.model=P1.model AND P1.ram IN(SELECT MIN(ram)FROM PC));SELECT R1.makerFROM Product R1,PC P1WHERE R1.model=P1.modelAND P1.ram =(SELECT MIN(ram)FROM PC)AND P1.speed IN(SELECT MAX(P1.speed)FROM Product R1,PC P1WHERE R1.model=P1.model AND P1.ram IN(SELECT MIN(ram)FROM PC));6.3.2a)SELECT C.countryFROM Classes CWHERE numGuns IN(SELECT MAX(numGuns)FROM Classes);SELECT C.countryFROM Classes CWHERE numGuns >= ALL(SELECT numGunsFROM Classes);b)SELECT DISTINCT C.class FROM Classes C,Ships SWHERE C.class = S.classAND EXISTS(SELECT shipFROM Outcomes OWHERE O.result='sunk' AND O.ship = ) ;SELECT DISTINCT C.class FROM Classes C,Ships SWHERE C.class = S.classAND IN(SELECT shipFROM Outcomes OWHERE O.result='sunk' ) ;c)SELECT FROM Ships SWHERE S.class IN(SELECT classFROM Classes CWHERE bore=16) ;SELECT FROM Ships SWHERE EXISTS(SELECT classFROM Classes CWHERE bore =16AND C.class = S.class );SELECT O.battleFROM Outcomes OWHERE O.ship IN(SELECT nameFROM Ships SWHERE S.Class ='Kongo' );SELECT O.battleFROM Outcomes OWHERE EXISTS(SELECT nameFROM Ships SWHERE S.Class ='Kongo' AND = O.ship );SELECT FROM Ships S,Classes CWHERE S.Class = C.ClassAND numGuns >= ALL(SELECT numGunsFROM Ships S2,Classes C2WHERE S2.Class = C2.Class AND C2.bore = C.bore) ;SELECT FROM Ships S,Classes CWHERE S.Class = C.ClassAND numGuns IN(SELECT MAX(numGuns)FROM Ships S2,Classes C2WHERE S2.Class = C2.Class AND C2.bore = C.bore) ;Better answer;SELECT FROM Ships S,Classes CWHERE S.Class = C.ClassAND numGuns >= ALL(SELECT numGunsFROM Classes C2WHERE C2.bore = C.bore) ;SELECT FROM Ships S,Classes CWHERE S.Class = C.ClassAND numGuns IN(SELECT MAX(numGuns)FROM Classes C2WHERE C2.bore = C.bore) ;6.3.3SELECT titleFROM MoviesGROUP BY titleHAVING COUNT(title) > 1 ;6.3.4SELECT FROM Ships S,Classes CWHERE S.Class = C.Class ;Assumption: In R1 join R2, the rows of R2 are unique on the joining columns. SELECT COLL12,COLL13,COLL14FROM R1WHERE COLL12 IN(SELECT COL22FROM R2)AND COLL13 IN(SELECT COL33FROM R3)AND COLL14 IN(SELECT COL44FROM R4) ...6.3.5(a)SELECT ,S.addressFROM MovieStar S,MovieExec EWHERE S.gender ='F'AND Worth > 10000000AND = AND S.address = E.address ;Note: As mentioned previously in the book, the names of stars are unique. However no such restriction exists for executives. Thus, both name and address are required as join columns.Alternate solution:SELECT name,addressFROM MovieStarWHERE gender = 'F'AND (name, address) IN(SELECT name,addressFROM MovieExecWHERE netWorth > 10000000) ;(b)SELECT name,addressFROM MovieStarWHERE (name,address) NOT IN(SELECT name addressFROM MovieExec) ;6.3.6By replacing the column in subquery with a constant and using IN subquery forthe constant, statement equivalent to EXISTS can be found.i.e. replace "WHERE EXISTS (SELECT C1 FROM R1..)" by "WHERE 1 IN (SELECT 1 FROM R1...)"Example:SELECT DISTINCT R.makerFROM Product RWHERE EXISTS(SELECT P.modelFROM PC PWHERE P.speed >= 3.0AND P.model =R.model) ;Above statement can be transformed to below statement.SELECT DISTINCT R.makerFROM Product RWHERE 1 IN(SELECT 1FROM PC PWHERE P.speed >= 3.0AND P.model =R.model) ;6.3.7(a)n*m tuples are returned where there are n studios and m executives. Each studiowill appear m times; once for every exec.(b)There are no common attributes between StarsIn and MovieStar; hence no tuplesare returned.(c)There will be at least one tuple corresponding to each star in MovieStar. Theunemployed stars will appear once with null values for StarsIn. All employedstars will appear as many times as the number of movies they are working in. Inother words, for each tuple in StarsIn(starName), the correspoding tuple fromMovieStar(name)) is joined and returned. For tuples in MovieStar that do nothave a corresponding entry in StarsIn, the MovieStar tuple is returned with nullvalues for StarsIn columns.6.3.8Since model numbers are unique, a full natural outer join of PC, Laptop andPrinter will return one row for each model. We want all information about PCs,Laptops and Printers even if the model does not appear in Product but vice versais not true. Thus a left natural outer join between Product and result above isrequired. The type attribute from Product must be renamed since Printer has atype attribute as well and the two attributes are different.(SELECT maker,model,type AS productTypeFROM Product) RIGHT NATURAL OUTER JOIN ((PC FULL NATURAL OUTER JOIN Laptop) FULL NATURAL OUTER JOIN Printer);Alternately, the Product relation can be joined individually with each ofPC,Laptop and Printer and the three results can be Unioned together. Forattributes that do not exist in one relation, a constant such as 'NA' or 0.0 canbe used. Below is an example of this approach using PC and Laptop.SELECT R.MAKER ,R.MODEL ,R.TYPE ,P.SPEED ,P.RAM ,P.HD ,0.0 AS SCREEN,P.PRICEFROM PRODUCT R,PC PWHERE R.MODEL = P.MODELUNIONSELECT R.MAKER ,R.MODEL ,R.TYPE ,L.SPEED ,L.RAM ,L.HD ,L.SCREEN,L.PRICEFROM PRODUCT R,LAPTOP LWHERE R.MODEL = L.MODEL;6.3.9SELECT *FROM Classes RIGHT NATURALOUTER JOIN Ships ;6.3.10SELECT *FROM Classes RIGHT NATURALOUTER JOIN ShipsUNION(SELECT C2.class ,C2.type ,C2.country ,C2.numguns ,C2.bore ,C2.displacement,C2.class NAME ,FROM Classes C2,Ships S2WHERE C2.Class NOT IN(SELECT ClassFROM Ships)) ;6.3.11(a)SELECT *FROM R,S ;(b)Let Attr consist ofAttrR = attributes unique to RAttrS = attributes unique to SAttrU = attributes common to R and SThus in Attr, attributes common to R and S are not repeated. SELECT AttrFROM R,SWHERE R.AttrU1 = S.AttrU1AND R.AttrU2 = S.AttrU2 ...AND R.AttrUi = S.AttrUi ;(c)SELECT *FROM R,SWHERE C ;6.4.1(a)DISTINCT keyword is not required here since each model only occurs once in PC relation.SELECT modelFROM PCWHERE speed >= 3.0 ;(b)SELECT DISTINCT R.makerFROM Product R,Laptop LWHERE R.model = L.modelAND L.hd > 100 ;(c)SELECT R.model,P.priceFROM Product R,PC PWHERE R.model = P.modelAND R.maker = 'B'UNIONSELECT R.model,L.priceFROM Product R,Laptop LWHERE R.model = L.modelAND R.maker = 'B'UNIONSELECT R.model,T.priceFROM Product R,Printer TWHERE R.model = T.modelAND R.maker = 'B' ;SELECT modelFROM PrinterWHERE color=TRUEAND type ='laser' ;(e)SELECT DISTINCT R.makerFROM Product R,Laptop LWHERE R.model = L.modelAND R.maker NOT IN(SELECT R1.makerFROM Product R1,PC PWHERE R1.model = P.model) ;better:SELECT DISTINCT R.makerFROM Product RWHERE R.type = 'laptop'AND R.maker NOT IN(SELECT R.makerFROM Product RWHERE R.type = 'pc') ;(f)With GROUP BY hd, DISTINCT keyword is not required. SELECT hdFROM PCGROUP BY hdHAVING COUNT(hd) > 1 ;(g)SELECT P1.model,P2.modelFROM PC P1,PC P2WHERE P1.speed = P2.speedAND P1.ram = P2.ramAND P1.model < P2.model ;SELECT R.makerFROM Product RWHERE R.model IN(SELECT P.modelFROM PC PWHERE P.speed >= 2.8)OR R.model IN(SELECT L.modelFROM Laptop LWHERE L.speed >= 2.8)GROUP BY R.makerHAVING COUNT(R.model) > 1 ;(i)After finding the maximum speed, an IN subquery can provide the manufacturer name.SELECT MAX(M.speed)FROM(SELECT speedFROM PCUNIONSELECT speedFROM Laptop) M ;SELECT R.makerFROM Product R,PC PWHERE R.model = P.modelAND P.speed IN(SELECT MAX(M.speed)FROM(SELECT speedFROM PCUNIONSELECT speedFROM Laptop) M)UNIONSELECT R2.makerFROM Product R2,Laptop LWHERE R2.model = L.modelAND L.speed IN(SELECT MAX(N.speed)FROM(SELECT speedFROM PCUNIONSELECT speedFROM Laptop) N) ;Alternately,SELECT COALESCE(MAX(P2.speed),MAX(L2.speed),0) SPEED FROM PC P2FULL OUTER JOIN Laptop L2ON P2.speed = L2.speed ;SELECT R.makerFROM Product R,PC PWHERE R.model = P.modelAND P.speed IN(SELECT COALESCE(MAX(P2.speed),MAX(L2.speed),0) SPEED FROM PC P2FULL OUTER JOIN Laptop L2ON P2.speed = L2.speed)UNIONSELECT R2.makerFROM Product R2,Laptop LWHERE R2.model = L.modelAND L.speed IN(SELECT COALESCE(MAX(P2.speed),MAX(L2.speed),0) SPEED FROM PC P2FULL OUTER JOIN Laptop L2ON P2.speed = L2.speed)SELECT R.makerFROM Product R,PC PWHERE R.model = P.modelGROUP BY R.makerHAVING COUNT(DISTINCT speed) >= 3 ;(k)SELECT R.makerFROM Product R,PC PWHERE R.model = P.modelGROUP BY R.makerHAVING COUNT(R.model) = 3 ;better;SELECT R.makerFROM Product RWHERE R.type='pc'GROUP BY R.makerHAVING COUNT(R.model) = 3 ;6.4.2(a)We can assume that class is unique in Classes and DISTINCT keyword is not required.SELECT class,countryFROM ClassesWHERE bore >= 16 ;(b)Ship names are not unique (In absence of hull codes, year of launch can help distinguish ships).SELECT DISTINCT name AS Ship_NameFROM ShipsWHERE launched < 1921 ;(c)SELECT DISTINCT ship AS Ship_NameFROM OutcomesWHERE battle = 'Denmark Strait'AND result = 'sunk' ;(d)SELECT DISTINCT AS Ship_NameFROM Ships S,Classes CWHERE S.class = C.classAND C.displacement > 35000 ;SELECT DISTINCT O.ship AS Ship_Name,C.displacement ,C.numGunsFROM Classes C ,Outcomes O,Ships SWHERE C.class = S.classAND = O.shipAND O.battle = 'Guadalcanal' ;SHIP_NAME DISPLACEMENT NUMGUNS------------------ ------------ -------Kirishima 32000 8Washington 37000 92 record(s) selected.Note: South Dakota was also in Guadalcanal but its class information is not available. Below query will return name of all ships that were in Guadalcanal even if no other information is available (shown as NULL). The above query is modified from INNER joins to LEFT OUTER joins.SELECT DISTINCT O.ship AS Ship_Name,C.displacement ,C.numGunsFROM Outcomes OLEFT JOIN Ships SON = O.shipLEFT JOIN Classes CON C.class = S.classWHERE O.battle = 'Guadalcanal' ;SHIP_NAME DISPLACEMENT NUMGUNS------------------ ------------ -------Kirishima 32000 8South Dakota - -Washington 37000 93 record(s) selected.(f)The Set opearator UNION guarantees unique results.SELECT ship AS Ship_NameFROM OutcomesUNIONSELECT name AS Ship_NameFROM Ships ;(g)SELECT C.classFROM Classes C,Ships SWHERE C.class = S.classGROUP BY C.classHAVING COUNT() = 1 ;better:SELECT S.classFROM Ships SGROUP BY S.classHAVING COUNT() = 1 ;(h)The Set opearator INTERSECT guarantees unique results.SELECT C.countryFROM Classes CWHERE C.type='bb'INTERSECTSELECT C2.countryFROM Classes C2WHERE C2.type='bc' ;However, above query does not account for classes without any ships belonging to them.SELECT C.countryFROM Classes C,Ships SWHERE C.class = S.classAND C.type ='bb'INTERSECTSELECT C2.countryFROM Classes C2,Ships S2WHERE C2.class = S2.classAND C2.type ='bc' ;SELECT O2.ship AS Ship_Name FROM Outcomes O2,Battles B2WHERE O2.battle = AND B2.date > ANY(SELECT B.dateFROM Outcomes O,Battles BWHERE O.battle = AND O.result ='damaged' AND O.ship = O2.ship);6.4.3a)SELECT DISTINCT R.maker FROM Product R,PC PWHERE R.model = P.modelAND P.speed >= 3.0;b)Models are unique.SELECT P1.modelFROM Printer P1LEFT OUTER JOIN Printer P2 ON (P1.price < P2.price) WHERE P2.model IS NULL ;c)SELECT DISTINCT L.model FROM Laptop L,PC PWHERE L.speed < P.speed ;Due to set operator UNION, unique results are returned.It is difficult to completely avoid a subquery here. One option is to use Views. CREATE VIEW AllProduct ASSELECT model,priceFROM PCUNIONSELECT model,priceFROM LaptopUNIONSELECT model,priceFROM Printer ;SELECT A1.modelFROM AllProduct A1LEFT OUTER JOIN AllProduct A2ON (A1.price < A2.price)WHERE A2.model IS NULL ;But if we replace the View, the query contains a FROM subquery. SELECT A1.modelFROM(SELECT model,priceFROM PCUNIONSELECT model,priceFROM LaptopUNIONSELECT model,priceFROM Printer) A1LEFT OUTER JOIN(SELECT model,priceFROM PCUNIONSELECT model,priceFROM LaptopUNIONSELECT model,priceFROM Printer) A2ON (A1.price < A2.price) WHERE A2.model IS NULL ;e)SELECT DISTINCT R.makerFROM Product R,Printer TWHERE R.model =T.modelAND T.price <= ALL(SELECT MIN(price)FROM Printer);f)SELECT DISTINCT R1.makerFROM Product R1,PC P1WHERE R1.model=P1.modelAND P1.ram IN(SELECT MIN(ram)FROM PC)AND P1.speed >= ALL(SELECT P1.speedFROM Product R1,PC P1WHERE R1.model=P1.modelAND P1.ram IN(SELECT MIN(ram)FROM PC));6.4.4a)SELECT DISTINCT C1.countryFROM Classes C1LEFT OUTER JOIN Classes C2 ON (C1.numGuns < C2.numGuns) WHERE C2.country IS NULL ;。

数据库系统基础教程(第二版)课后习题答案2

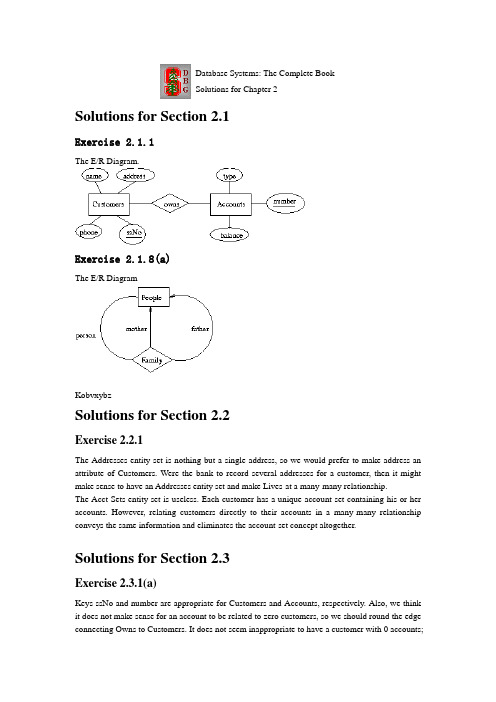

Database Systems: The Complete BookSolutions for Chapter 2Solutions for Section 2.1Exercise 2.1.1The E/R Diagram.Exercise 2.1.8(a)The E/R DiagramKobvxybzSolutions for Section 2.2Exercise 2.2.1The Addresses entity set is nothing but a single address, so we would prefer to make address an attribute of Customers. Were the bank to record several addresses for a customer, then it might make sense to have an Addresses entity set and make Lives-at a many-many relationship.The Acct-Sets entity set is useless. Each customer has a unique account set containing his or her accounts. However, relating customers directly to their accounts in a many-many relationship conveys the same information and eliminates the account-set concept altogether.Solutions for Section 2.3Exercise 2.3.1(a)Keys ssNo and number are appropriate for Customers and Accounts, respectively. Also, we think it does not make sense for an account to be related to zero customers, so we should round the edge connecting Owns to Customers. It does not seem inappropriate to have a customer with 0 accounts;they might be a borrower, for example, so we put no constraint on the connection from Owns to Accounts. Here is the The E/R Diagram,showing underlined keys andthe numerocity constraint.Exercise 2.3.2(b)If R is many-one from E1 to E2, then two tuples (e1,e2) and (f1,f2) of the relationship set for R must be the same if they agree on the key attributes for E1. To see why, surely e1 and f1 are the same. Because R is many-one from E1 to E2, e2 and f2 must also be the same. Thus, the pairs are the same.Solutions for Section 2.4Exercise 2.4.1Here is the The E/R Diagram.We have omitted attributes other than our choice for the key attributes of Students and Courses. Also omitted are names for the relationships. Attribute grade is not part of the key for Enrollments. The key for Enrollements is studID from Students and dept and number from Courses.Exercise 2.4.4bHere is the The E/R Diagram Again, we have omitted relationship names and attributes other than our choice for the key attributes. The key for Leagues is its own name; this entity set is not weak. The key for Teams is its own name plus the name of the league of which the team is a part, e.g., (Rangers, MLB) or (Rangers, NHL). The key for Players consists of the player's number and the key for the team on which he or she plays. Since the latter key is itself a pair consisting of team and league names, the key for players is the triple (number, teamName, leagueName). e.g., JeffGarcia is (5, 49ers, NFL).Database Systems: The Complete BookSolutions for Chapter 3Solutions for Section 3.1Exercise 3.1.2(a)We can order the three tuples in any of 3! = 6 ways. Also, the columns can be ordered in any of 3! = 6 ways. Thus, the number of presentations is 6*6 = 36.Solutions for Section 3.2Exercise 3.2.1Customers(ssNo, name, address, phone)Flights(number, day, aircraft)Bookings(ssNo, number, day, row, seat)Being a weak entity set, Bookings' relation has the keys for Customers and Flights and Bookings' own attributes.Notice that the relations obtained from the toCust and toFlt relationships are unnecessary. They are:toCust(ssNo, ssNo1, number, day)toFlt(ssNo, number, day, number1, day1)That is, for toCust, the key of Customers is paired with the key for Bookings. Since both include ssNo, this attribute is repeated with two different names, ssNo and ssNo1. A similar situation exists for toFlt.Exercise 3.2.3Ships(name, yearLaunched)SisterOf(name, sisterName)Solutions for Section 3.3Exercise 3.3.1Since Courses is weak, its key is number and the name of its department. We do not have arelation for GivenBy. In part (a), there is a relation for Courses and a relation for LabCourses that has only the key and the computer-allocation attribute. It looks like:Depts(name, chair)Courses(number, deptName, room)LabCourses(number, deptName, allocation)For part (b), LabCourses gets all the attributes of Courses, as:Depts(name, chair)Courses(number, deptName, room)LabCourses(number, deptName, room, allocation)And for (c), Courses and LabCourses are combined, as:Depts(name, chair)Courses(number, deptName, room, allocation)Exercise 3.3.4(a)There is one relation for each entity set, so the number of relations is e. The relation for the root entity set has a attributes, while the other relations, which must include the key attributes, have a+k attributes.Solutions for Section 3.4Exercise 3.4.2Surely ID is a key by itself. However, we think that the attributes x, y, and z together form another key. The reason is that at no time can two molecules occupy the same point.Exercise 3.4.4The key attributes are indicated by capitalization in the schema below:Customers(SSNO, name, address, phone)Flights(NUMBER, DAY, aircraft)Bookings(SSNO, NUMBER, DAY, row, seat)Exercise 3.4.6(a)The superkeys are any subset that contains A1. Thus, there are 2^{n-1} such subsets, since each of the n-1 attributes A2 through An may independently be chosen in or out.Solutions for Section 3.5Exercise 3.5.1(a)We could try inference rules to deduce new dependencies until we are satisfied we have them all.A more systematic way is to consider the closures of all 15 nonempty sets of attributes.For the single attributes we have A+ = A, B+ = B, C+ = ACD, and D+ = AD. Thus, the only new dependency we get with a single attribute on the left is C->A.Now consider pairs of attributes:AB+ = ABCD, so we get new dependency AB->D. AC+ = ACD, and AC->D is nontrivial. AD+ = AD, so nothing new. BC+ = ABCD, so we get BC->A, and BC->D. BD+ = ABCD, giving usBD->A and BD->C. CD+ = ACD, giving CD->A.For the triples of attributes, ACD+ = ACD, but the closures of the other sets are each ABCD. Thus, we get new dependencies ABC->D, ABD->C, and BCD->A.Since ABCD+ = ABCD, we get no new dependencies.The collection of 11 new dependencies mentioned above is: C->A, AB->D, AC->D, BC->A, BC->D, BD->A, BD->C, CD->A, ABC->D, ABD->C, and BCD->A.Exercise 3.5.1(b)From the analysis of closures above, we find that AB, BC, and BD are keys. All other sets either do not have ABCD as the closure or contain one of these three sets.Exercise 3.5.1(c)The superkeys are all those that contain one of those three keys. That is, a superkey that is not a key must contain B and more than one of A, C, and D. Thus, the (proper) superkeys are ABC, ABD, BCD, and ABCD.Exercise 3.5.3(a)We must compute the closure of A1A2...AnC. Since A1A2...An->B is a dependency, surely B is in this set, proving A1A2...AnC->B.Exercise 3.5.4(a)Consider the relationThis relation satisfies A->B but does not satisfy B->A.Exercise 3.5.8(a)If all sets of attributes are closed, then there cannot be any nontrivial functional dependenc ies. For suppose A1A2...An->B is a nontrivial dependency. Then A1A2...An+ contains B and thus A1A2...An is not closed.Exercise 3.5.10(a)We need to compute the closures of all subsets of {ABC}, although there is no need to think about the empty set or the set of all three attributes. Here are the calculations for the remaining six sets: A+ = AB+ = BC+ = ACEAB+ = ABCDEAC+ = ACEBC+ = ABCDEWe ignore D and E, so a basis for the resulting functional dependencies for ABC are: C->A and AB->C. Note that BC->A is true, but follows logically from C->A, and therefore may be omitted from our list.Solutions for Section 3.6Exercise 3.6.1(a)In the solution to Exercise 3.5.1 we found that there are 14 nontrivial dependencies, including the three given ones and 11 derived dependencies. These are: C->A, C->D, D->A, AB->D, AB-> C, AC->D, BC->A, BC->D, BD->A, BD->C, CD->A, ABC->D, ABD->C, and BCD->A.We also learned that the three keys were AB, BC, and BD. Thus, any dependency above that does not have one of these pairs on the left is a BCNF violation. These are: C->A, C->D, D->A, AC->D, and CD->A.One choice is to decompose using C->D. That gives us ABC and CD as decomposed relations. CD is surely in BCNF, since any two-attribute relation is. ABC is not in BCNF, since AB and BC are its only keys, but C->A is a dependency that holds in ABCD and therefore holds in ABC. We must further decompose ABC into AC and BC. Thus, the three relations of the decomposition are AC, BC, and CD.Since all attributes are in at least one key of ABCD, that relation is already in 3NF, and no decomposition is necessary.Exercise 3.6.1(b)(Revised 1/19/02) The only key is AB. Thus, B->C and B->D are both BCNF violations. The derived FD's BD->C and BC->D are also BCNF violations. However, any other nontrivial, derived FD will have A and B on the left, and therefore will contain a key.One possible BCNF decomposition is AB and BCD. It is obtained starting with any of the four violations mentioned above. AB is the only key for AB, and B is the only key for BCD.Since there is only one key for ABCD, the 3NF violations are the same, and so is the decomposition.Solutions for Section 3.7Exercise 3.7.1Since A->->B, and all the tuples have the same value for attribute A, we can pair the B-value from any tuple with the value of the remaining attribute C from any other tuple. Thus, we know that R must have at least the nine tuples of the form (a,b,c), where b is any of b1, b2, or b3, and c is any of c1, c2, or c3. That is, we can derive, using the definition of a multivalued dependency, that each of the tuples (a,b1,c2), (a,b1,c3), (a,b2,c1), (a,b2,c3), (a,b3,c1), and (a,b3,c2) are also in R.Exercise 3.7.2(a)First, people have unique Social Security numbers and unique birthdates. Thus, we expect the functional dependencies ssNo->name and ssNo->birthdate hold. The same applies to children, so we expect childSSNo->childname and childSSNo->childBirthdate. Finally, an automobile has a unique brand, so we expect autoSerialNo->autoMake.There are two multivalued dependencies that do not follow from these functional dependencies. First, the information about one child of a person is independent of other information about that person. That is, if a person with social security number s has a tuple with cn,cs,cb, then if there isany other tuple t for the same person, there will also be another tuple that agrees with t except that it has cn,cs,cb in its components for the child name, Social Security number, and birthdate. That is the multivalued dependencyssNo->->childSSNo childName childBirthdateSimilarly, an automobile serial number and make are independent of any of the other attributes, so we expect the multivalued dependencyssNo->->autoSerialNo autoMakeThe dependencies are summarized below:ssNo -> name birthdatechildSSNo -> childName childBirthdateautoSerialNo -> autoMakessNo ->-> childSSNo childName childBirthdatessNo ->-> autoSerialNo autoMakeExercise 3.7.2(b)We suggest the relation schemas{ssNo, name, birthdate}{ssNo, childSSNo}{childSSNo, childName childBirthdate}{ssNo, autoSerialNo}{autoSerialNo, autoMake}An initial decomposition based on the two multivalued dependencies would give us {ssNo, name, birthDate}{ssNo, childSSNo, childName, childBirthdate}{ssNo, autoSerialNo, autoMake}Functional dependencies force us to decompose the second and third of these.Exercise 3.7.3(a)Since there are no functional dependencies, the only key is all four attributes, ABCD. Thus, each of the nontrvial multivalued dependencies A->->B and A->->C violate 4NF. We must separate out the attributes of these dependencies, first decomposing into AB and ACD, and then decomposing the latter into AC and AD because A->->C is still a 4NF violation for ACD. The final set of relations are AB, AC, and AD.Exercise 3.7.7(a)Let W be the set of attributes not in X, Y, or Z. Consider two tuples xyzw and xy'z'w' in the relation R in question. Because X ->-> Y, we can swap the y's, so xy'zw and xyz'w' are in R. Because X ->-> Z, we can take the pair of tuples xyzw and xyz'w' and swap Z's to get xyz'w and xyzw'. Similarly, we can take the pair xy'z'w' and xy'zw and swap Z's to get xy'zw' and xy'z'w.In conclusion, we started with tuples xyzw and xy'z'w' and showed that xyzw' and xy'z'w must also be in the relation. That is exactly the statement of the MVD X ->-> Y-union-Z. Note that the above statements all make sense even if there are attributes in common among X, Y, and Z.Exercise 3.7.8(a)Consider a relation R with schema ABCD and the instance with four tuples abcd, abcd', ab'c'd, and ab'c'd'. This instance satisfies the MVD A->-> BC. However, it does not satisfy A->-> B. For example, if it did satisfy A->-> B, then because the instance contains the tuples abcd and ab'c'd, we would expect it to contain abc'd and ab'cd, neither of which is in the instance.Database Systems: The Complete BookSolutions for Chapter 4Solutions for Section 4.2Exercise 4.2.1class Customer {attribute string name;attribute string addr;attribute string phone;attribute integer ssNo;relationship Set<Account> ownsAcctsinverse Account::ownedBy;}class Account {attribute integer number;attribute string type;attribute real balance;relationship Set<Customer> ownedByinverse Customer::ownsAccts}Exercise 4.2.4class Person {attribute string name;relationship Person motherOfinverse Person::childrenOfFemalerelationship Person fatherOfinverse Person::childrenOfMalerelationship Set<Person> childreninverse Person::parentsOfrelationship Set<Person> childrenOfFemaleinverse Person::motherOfrelationship Set<Person> childrenOfMaleinverse Person::fatherOfrelationship Set<Person> parentsOfinverse Person::children}Notice that there are six different relationships here. For example, the inverse of the relationship that connects a person to their (unique) mother is a relationship that connects a mother (i.e., a female person) to the set of her children. That relationship, which we call childrenOfFemale, is different from the children relationship, which connects anyone -- male or female -- to their children.Exercise 4.2.7A relationship R is its own inverse if and only if for every pair (a,b) in R, the pair (b,a) is also in R. In the terminology of set theory, the relation R is ``symmetric.''Solutions for Section 4.3Exercise 4.3.1We think that Social Security number should me the key for Customer, and account number should be the key for Account. Here is the ODL solution with key and extent declarations.class Customer(extent Customers key ssNo){attribute string name;attribute string addr;attribute string phone;attribute integer ssNo;relationship Set<Account> ownsAcctsinverse Account::ownedBy;}class Account(extent Accounts key number){attribute integer number;attribute string type;attribute real balance;relationship Set<Customer> ownedByinverse Customer::ownsAccts}Solutions for Section 4.4Exercise 4.4.1(a)Since the relationship between customers and accounts is many-many, we should create a separate relation from that relationship-pair.Customers(ssNo, name, address, phone)Accounts(number, type, balance)CustAcct(ssNo, number)Exercise 4.4.1(d)Ther is only one attribute, but three pairs of relationships from Person to itself. Since motherOf and fatherOf are many-one, we can store their inverses in the relation for Person. That is, for each person, childrenOfMale and childrenOfFemale will indicate that persons's father and mother. The children relationship is many-many, and requires its own relation. This relation actually turns out to be redundant, in the sense that its tuples can be deduced from the relationships stored with Person. The schema:Persons(name, childrenOfFemale, childrenOfMale)Parent-Child(parent, child)Exercise 4.4.4Y ou get a schema like:Studios(name, address, ownedMovie)Since name -> address is the only FD, the key is {name, ownedMovie}, and the FD has a left side that is not a superkey.Exercise 4.4.5(a,b,c)(a) Struct Card { string rank, string suit };(b) class Hand {attribute Set theHand;};For part (c) we have:Hands(handId, rank, suit)Notice that the class Hand has no key, so we need to create one: handID. Each hand has, in the relation Hands, one tuple for each card in the hand.Exercise 4.4.5(e)Struct PlayerHand { string Player, Hand theHand };class Deal {attribute Set theDeal;}Alternatively, PlayerHand can be defined directly within the declaration of attribute theDeal. Exercise 4.4.5(h)Since keys for Hand and Deal are lacking, a mechanical way to design the database schema is to have one relation connecting deals and player-hand pairs, and another to specify the contents of hands. That is:Deals(dealID, player, handID)Hands(handID, rank, suit)However, if we think about it, we can get rid of handID and connect the deal and the player directly to the player's cards, as:Deals(dealID, player, rank, suit)Exercise 4.4.5(i)First, card is really a pair consisting of a suit and a rank, so we need two attributes in a relation schema to represent cards. However, much more important is the fact that the proposed schema does not distinguish which card is in which hand. Thus, we need another attribute that indicates which hand within the deal a card belongs to, something like:Deals(dealID, handID, rank, suit)Exercise 4.4.6(c)Attribute b is really a bag of (f,g) pairs. Thus, associated with each a-value will be zero or more (f,g) pairs, each of which can occur several times. We shall use an attribute count to indicate the number of occurrences, although if relations allow duplicate tuples we could simply allow duplicate (a,f,g) triples in the relation. The proposed schema is:C(a, f, g, count)Solutions for Section 4.5Exercise 4.5.1(b)Studios(name, address, movies{(title, year, inColor, length,stars{(name, address, birthdate)})})Since the information about a star is repeated once for each of their movies, there is redundancy. To eliminate it, we have to use a separate relation for stars and use pointers from studios. That is: Stars(name, address, birthdate)Studios(name, address, movies{(title, year, inColor, length,stars{*Stars})})Since each movie is owned by one studio, the information about a movie appears in only one tuple of Studios, and there is no redundancy.Exercise 4.5.2Customers(name, address, phone, ssNo, accts{*Accounts})Accounts(number, type, balance, owners{*Customers})Solutions for Section 4.6Exercise 4.6.1(a)We need to add new nodes labeled George Lucas and Gary Kurtz. Then, from the node sw (which represents the movie Star Wars), we add arcs to these two new nodes, labeled direc tedBy and producedBy, respectively.Exercise 4.6.2Create nodes for each account and each customer. From each customer node is an arc to a node representing the attributes of the customer, e.g., an arc labeled name to the customer's name. Likewise, there is an arc from each account node to each attribute of that account, e.g., an arc labeled balance to the value of the balance.To represent ownership of accounts by customers, we place an arc labeled owns from each customer node to the node of each account that customer holds (possibly jointly). Also, we placean arc labeled ownedBy from each account node to the customer node for each owner of that account.Exercise 4.6.5In the semistructured model, nodes represent data elements, i.e., entities rather than entity sets. In the E/R model, nodes of all types represent schema elements, and the data is not represented at all. Solutions for Section 4.7Exercise 4.7.1(a)<STARS-MOVIES><STAR starId = "cf" starredIn = "sw, esb, rj"><NAME>Carrie Fisher</NAME><ADDRESS><STREET>123 Maple St.</STREET><CITY>Hollywood</CITY></ADDRESS><ADDRESS><STREET>5 Locust Ln.</STREET><CITY>Malibu</CITY></ADDRESS></STAR><STAR starId = "mh" starredIn = "sw, esb, rj"><NAME>Mark Hamill</NAME><ADDRESS><STREET>456 Oak Rd.<STREET><CITY>Brentwood</CITY></ADDRESS></STAR><STAR starId = "hf" starredIn = "sw, esb, rj, wit"><NAME>Harrison Ford</NAME><ADDRESS><STREET>whatever</STREET><CITY>whatever</CITY></ADDRESS></STAR><MOVIE movieId = "sw" starsOf = "cf, mh"><TITLE>Star Wars</TITLE><YEAR>1977</YEAR></MOVIE><MOVIE movieId = "esb" starsOf = "cf, mh"><TITLE>Empire Strikes Back</TITLE><YEAR>1980</YEAR></MOVIE><MOVIE movieId = "rj" starsOf = "cf, mh"><TITLE>Return of the Jedi</TITLE><YEAR>1983</YEAR></MOVIE><MOVIE movieID = "wit" starsOf = "hf"><TITLE>Witness</TITLE><YEAR>1985</YEAR></MOVIE></STARS-MOVIES>Exercise 4.7.2<!DOCTYPE Bank [<!ELEMENT BANK (CUSTOMER* ACCOUNT*)><!ELEMENT CUSTOMER (NAME, ADDRESS, PHONE, SSNO)> <!A TTLIST CUSTOMERcustId IDowns IDREFS><!ELEMENT NAME (#PCDA TA)><!ELEMENT ADDRESS (#PCDA TA)><!ELEMENT PHONE (#PCDA TA)><!ELEMENT SSNO (#PCDA TA)><!ELEMENT ACCOUNT (NUMBER, TYPE, BALANCE)><!A TTLIST ACCOUNTacctId IDownedBy IDREFS><!ELEMENT NUMBER (#PCDA TA)><!ELEMENT TYPE (#PCDA TA)><!ELEMENT BALANCE (#PCDA TA)>]>Database Systems: The CompleteBookSolutions for Chapter 5Solutions for Section 5.2Exercise 5.2.1(a)PI_model( SIGMA_{speed >= 1000} ) (PC)Exercise 5.2.1(f)The trick is to theta-join PC with itself on the condition that the hard disk sizes are equal. That gives us tuples that have two PC model numbers with the same value of hd. However, these two PC's could in fact be the same, so we must also require in the theta-join that the model numbers be unequal. Finally, we want the hard disk sizes, so we project onto hd.The expression is easiest to see if we write it using some temporary values. We start by renaming PC twice so we can talk about two occurrences of the same attributes.R1 = RHO_{PC1} (PC)R2 = RHO_{PC2} (PC)R3 = R1 JOIN_{PC1.hd = PC2.hd AND PC1.model <> PC2.model} R2R4 = PI_{PC1.hd} (R3)Exercise 5.2.1(h)First, we find R1, the model-speed pairs from both PC and Laptop. Then, we find from R1 those computers that are ``fast,'' at least 133Mh. At the same time, we join R1 with Product to connect model numbers to their manufacturers and we project out the speed to get R2. Then we join R2 with itself (after renaming) to find pairs of different models by the same maker. Finally, we get our answer, R5, by projecting onto one of the maker attributes. A sequence of steps giving the desired expression is: R1 = PI_{model,speed} (PC) UNION PI_{model,speed} (Laptop)R2 = PI_{maker,model} (SIGMA_{speed>=700} (R1) JOIN Product)R3 = RHO_{T(maker2, model2)} (R2)R4 = R2 JOIN_{maker = maker2 AND model <> model2} (R3)R5 = PI_{maker} (R4)Exercise 5.2.2Here are figures for the expression trees of Exercise 5.2.1 Part (a)Part (f)Part (h). Note that the third figure is not really a tree, since it uses a common subexpression. We could duplicate the nodes to make it a tree, but using common subexpressions is a valuable form of query optimization. One of the benefits one gets from constructing ``trees'' for queries is the ability to combine nodes that represent common subexpressions.Exercise 5.2.7The relation that results from the natural join has only one attribute from each pair of equated attributes. The theta-join has attributes for both, and their columns are identical.Exercise 5.2.9(a)If all the tuples of R and S are different, then the union has n+m tuples, and this number is the maximum possible.The minimum number of tuples that can appear in the result occurs if every tuple of one relation also appears in the other. Surely the union has at least as many tuples as the larger of R and that is, max(n,m) tuples. However, it is possible for every tuple of the smaller to appear in the other, so it is possible that there are as few as max(n,m) tuples in the union.Exercise 5.2.10In the following we use the name of a relation both as its instance (set of tuples) and as its schema (set of attributes). The context determines uniquely which is meant.PI_R(R JOIN S) Note, however, that this expression works only for sets; it does not preserve the multipicity of tuples in R. The next two expressions work for bags.R JOIN DELTA(PI_{R INTERSECT S}(S)) In this expression, each projection of a tuple from S onto the attributes that are also in R appears exactly once in the second argument of the join, so it preserves multiplicity of tuples in R, except for those thatdo not join with S, which disappear. The DELTA operator removes duplicates, as described in Section 5.4.R - [R - PI_R(R JOIN S)] Here, the strategy is to find the dangling tuples of R and remove them.Solutions for Section 5.3Exercise 5.3.1As a bag, the value is {700, 1500, 866, 866, 1000, 1300, 1400, 700, 1200, 750, 1100, 350, 733}. The order is unimportant, of course. The average is 959.As a set, the value is {700, 1500, 866, 1000, 1300, 1400, 1200, 750, 1100, 350, 733}, and the average is 967. H3>Exercise 5.3.4(a)As sets, an element x is in the left-side expression(R UNION S) UNION Tif and only if it is in at least one of R, S, and T. Likewise, it is in the right-side expressionR UNION (S UNION T)under exactly the same conditions. Thus, the two expressions have exactly the same members, and the sets are equal.As bags, an element x is in the left-side expression as many times as the sum of the number of times it is in R, S, and T. The same holds for the right side. Thus, as bags the expressions also have the same value.Exercise 5.3.4(h)As sets, element x is in the left sideR UNION (S INTERSECT T)if and only if x is either in R or in both S and T. Element x is in the right side(R UNION S) INTERSECT (R UNION T)if and only if it is in both R UNION S and R UNION T. If x is in R, then it is in both unions. If x is in both S and T, then it is in both union. However, if x is neither in R nor in both of S and T, then it cannot be in both unions. For example, suppose x is not in R and not in S. Then x is not in R UNION S. Thus, the statement of when x is in the right side is exactly the same as when it is in the left side: x is either in R or in both of S and T.Now, consider the expression for bags. Element x is in the left side the sum of the number of times it is in R plus the smaller of the number of times x is in S and the number of times x is in T. Likewise, the number of times x is in the right side is the smaller ofThe sum of the number of times x is in R and in S.The sum of the number of times x is in R and in T.A moment's reflection tells us that this minimum is the sum of the number of times x is in R plus the smaller of the number of times x is in S and in T, exactly as for the left side.Exercise 5.3.5(a)For sets, we observe that element x is in the left side(R INTERSECT S) - T。

Chapter 6 - Solid Solutions

Solid Solutions

22. P A I R P R O B A B I L I T Y F U N C T I O N S : THERMODYNAMIC PROPERTIES

A solid phase containing two or more kinds of atom, the relative proportions of which may be varied within limits, is described as a solid solution. Terminal solid solutions are based on the structures of the component metals; intermediate solid solutions may have structures which are different from any of those of the constituents. Most solid solutions are of the substitutional type, in which the different atoms are distributed over one or more sets of common sites, and may interchange positions on the sites. In interstitial solutions, the solute atoms occupy sites in the spaces between the positions of the atoms of the solvent metal; this can only happen when the solute atoms are much smaller than the atoms of the solvent. We must also distinguish between ordered and disordered solid solutions. In the fully ordered state each set of atoms occupies one set of positions, so that the atomic arrangement is similar to that of a compound. This is only possible at compositions where the ratios of the numbers of atoms of different kinds are small integral numbers, but the atomic arrangement may still be predominantly ordered in this way for alloys of arbitrary composition. In disordered solid solutions, the atoms are distributed among the sites they occupy in a nearly random manner. This classification is only approximate, and we shall formulate these concepts more precisely. The definition of the unit cell, and the concept of the translational periodicity of the lattice, lose their strict validity when applied to a disordered solid solution. The mean positions of the atoms, considered as mathematical points, will no longer be specified exactly by (5.8), since there will be local distortions depending on the details of the local configurations. Moreover, a knowledge of the type of atom at one end of a given interatomic vector no longer implies knowledge of the atom at the other end, as it does for a pure component or a fully ordered structure. In a solid solution, precise statements of this nature have to be replaced by statements in terms of the probability of the atom being of a certain type. For many purposes, the strict non-periodicity of the structure is not important, since most physical properties are averages over reasonably large numbers of atoms. Thus the positions of X-ray diffraction maxima depend only on the average unit cell dime Theory of Transformations in Metals and Alloys

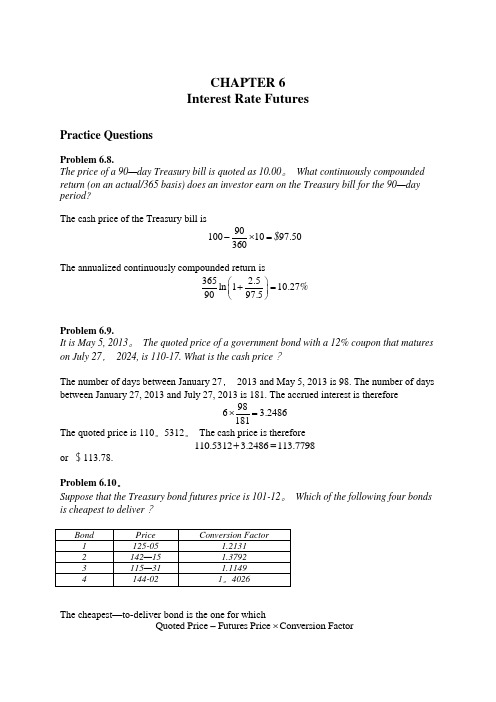

HullFund8eCh06ProblemSolutions【范本模板】

CHAPTER 6Interest Rate FuturesPractice QuestionsProblem 6.8.The price of a 90—day Treasury bill is quoted as 10.00。

What continuously compounded return (on an actual/365 basis) does an investor earn on the Treasury bill for the 90—day period?The cash price of the Treasury bill is 90100109750360$-⨯=.The annualized continuously compounded return is 36525ln 1102790975%.⎛⎫+=. ⎪.⎝⎭Problem 6.9.It is May 5, 2013。

The quoted price of a government bond with a 12% coupon that matures on July 27, 2024, is 110-17. What is the cash price ?The number of days between January 27, 2013 and May 5, 2013 is 98. The number of days between January 27, 2013 and July 27, 2013 is 181. The accrued interest is therefore 98632486181⨯=. The quoted price is 110。

5312。

The cash price is therefore1105312324861137798.+.=.or $113.78.Problem 6.10。

Solutions (6)

Chapter 66.1 When an LED has 2V applied to its terminals, it draws 100mA and produces 2mW of optical power. What is LED ’s conversion efficiency from electrical to optical power? Solution:210020021%200e o e P UI V mA mWP mW P mW η==⨯====6.2 A GaAs laser diode has a 1.5-nm gain linewidth, and its cavity length is 0.5mm, Sketch the output spectrum, including as many details as you can ( for example, the emitted wavelength and the number of the modes ) . Solution:()26230.9100.24222 3.350.5101.560.242c nm nL nm N λλ--⨯∆===⨯⨯⨯=≈6.3 An erbium-doped fiber amplifier has a noise figure of 6 and a gain of 100. The input signal has a 30-dB signal-to-noise ratio and a signal power of 10 W μ. Computer the signal power ( in dBm) and signal-to-noise ratio ( in dB) at the amplifier ’s output.Solution:102010log67.78307.7822.222010lg1000in out in out P W dBmF dB S S F dB dB dBP dBm dBmμ==-===-=-==-+=λ6.4 For an LED, compute the fraction of inject charges that produce photons if 2 mW of optical power are radiated with a drive current of 50mA at 1.3m μ. Solution:198346P 2 1.610 4.2%3106.62610501.310g g i Pe W e W i mW C m s J s mA mηη---⎛⎫=⇒= ⎪⎝⎭⨯⨯==⨯⨯⋅⨯⨯⨯6.5 Source emitting at different wavelength can be multiplexed onto a single fiber, providing multiple channels of information. Assuming a spectral width of 0.02nm for each laser source and a channel separation of 0.05nm (to avoid crosstalk), how many channels can be fitted into the C band.Solution:()():1530~156515651530357000.050.05C band nm nmnm nm N nmnm --===6.6 An erbium- doped fiber amplifiers at 1550nm and is pumped at 980nm. Compute the amplifier efficiency if the only energy loss is due to the fact that it takes one 980nm photon to produce one 1550nm photon. Solution:211298063.2%1550ch nm c nmh λληλλ==== 6.7 Raman scattering results in a downshift in the optical frequency of about 13.2 Thz. If the input wavelength is 1540 nm, compute both the input frequency and the downshifted frequency. Solution:88310193.551550193.5513.2180.35310 1.663180.35shift shift cm s f THz nmf THz THz THz m s m THzλλμ⨯====-=⨯==。

ch06partSolution

Selected Solutions for Exercises inNumerical Methods with Matlab:Implementations and ApplicationsGerald W.RecktenwaldChapter6Finding the Roots of f(x)=0The following pages contain solutions to selected end-of-chapter Exercisesfrom the book Numerical Methods with Matlab:Implementations andApplications,by Gerald W.Recktenwald,c 2000,Prentice-Hall,Upper Saddle River,NJ.The solutions are c 2000Gerald W.Recktenwald.ThePDF version of the solutions may be downloaded or stored or printed onlyfor noncommercial,educational use.Repackaging and sale of these solutionsin any form,without the written consent of the author,is prohibited.The latest version of this PDFfile,along with other supplemental material for the book,can be found at /recktenwald.2Finding the Roots of f(x)=0 6–2The function f(x)=sin(x2)+x2−2x−0.09has four roots in the interval−1≤x≤3.Given the m-file fx.m,which containsfunction f=fx(x)f=sin(x.^2)+x.^2-2*x-0.09;the statement>>brackPlot(’fx’,-1,3)produces only two brackets.Is this result due to a bug in brackPlot or fx?What needs to be changed so that all four roots are found?Demonstrate that your solution works.Partial Solution:The statement>>Xb=brackPlot(’fx’,-1,3)Xb=-0.15790.05262.1579 2.3684returns two brackets.A close inspection of the plot of f(x)reveals that f(x)crosses the x-axis twice near x=1.3.These two roots are missed by brackPlot because there default search interval is too coarse.There is no bug in brackPlot.Implementing a solution using afiner search interval is left as an exercise.6–11Use the bisect function to evaluate the root of the Colebrook equation(see Exercise8) for /D=0.02and Re=105.Do not modify bisect.m.This requires that you write an appropriate function m-file to evaluate the Colebrook equation.Partial Solution:Using bisect requires writing an auxiliary function to evaluate the Cole-brook equation in the form F(f)=0,where f is the friction factor.The following form of F(f)is used in the colebrkz function listed below.F(f)=1√f+2log10/D3.7+2.51Re D√fMany other forms of F(f)will work.function ff=colebrkz(f)%COLEBRKZ Evaluates the Colebrook equation in the form F(f)=0%for use with root-finding routines.%%Input:f=the current guess at the friction factor%%Global Variables:%EPSDIA=ratio of relative roughness to pipe diameter%REYNOLDS=Reynolds number based on pipe diameter%%Output:ff=the"value"of the Colebrook function written y=F(f)%Global variables allow EPSDIA and REYNOLDS to be passed into%colebrkz while bypassing the bisect.m or fzero functionglobal EPSDIA REYNOLDSff=1.0/sqrt(f)+2.0*log10(EPSDIA/3.7+2.51/(REYNOLDS*sqrt(f)));Because the bisect function(unlike fzero)does not allow additional parameters to be passed through to the F(f)function,the values of /D and Re are passed to colebrkz via global variables.Running bisect with colebrkz is left to the reader.For Re=1×105and /D=0.02the solution is f=0.0490.Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.Chapter6:Finding the Roots of f(x)=03 6–13Derive the g3(x)functions in Example6.4and Example6.5.(Hint:What is thefixed-pointformula for Newton’s method?)Partial Solution:Thefixed point iteration formulas designated as g3(x)in Example6.4 and Example6.5are obtained by applying Newton’s method.The general form of Newton’smethod for a scalar variable isx k+1=x k−f(x k) f (x k)Example6.4:The f(x)function and its derivative aref(x)=x−x1/3−2f (x)=1−13x−2/3Substituting these expressions into the formula for Newton’s method and simplifying givesx k+1=x k−x k−x1/3k−21−(1/3)x−2/3k=x k(1−(1/3)x−2/3k)−(x k−x1/3k−2)1−(1/3)x−2/3k=x k−(1/3)x1/3k−x k+x1/3k+21−(1/3)x−2/3k=(2/3)x1/3k+21−(1/3)x k=2x1/3k+63−x−2/3kRepeating this analysis for Example6.5is left as an exercise.Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.4Finding the Roots of f(x)=0 6–17K.Wark and D.E.Richards(Thermodynamics,6th ed.,1999,McGraw-Hill,Boston,Example 14-2,pp.768–769)compute the equilibrium composition of a mixture of carbon monoxide and oxygen gas at one atmosphere.Determining thefinal composition requires solving3.06=(1−x)(3+x)1/2 x(1+x)1/2for x.Obtain afixed-point iteration formula forfinding the roots of this equation.Implement your formula in a Matlab function and use your function tofind x.If your formula does not converge,develop one that does.Partial Solution:Onefixed point iteration formula is obtained by isolating the factor of (3+x)in the numerator.3.06x(1+x)1/21−x =(3+x)1/2=⇒x=3.06x(1+x)1/21−x2−3=⇒g1(x)=3.06x(1+x)1/21−x2−3Anotherfixed point iteration formula is obtained by solving for the isolated x in the denomi-nator to getx=(1−x)(3+x)1/23.06(1+x)=⇒g2(x)=(1−x)(3+x)1/23.06(1+x)Performing10fixed point iterations with g1(x)givesit xnew1-7.6420163e-012-2.5857113e+003-1.0721050e+014-7.9154865e+015-7.1666488e+026-6.6855377e+037-6.2575617e+048-5.8590795e+059-5.4861826e+0610-5.1370394e+07Thus,g1(x)does not converge.The g2(x)function does converge to the true root of x= 0.340327....Matlab implementations of thefixed point iterations are left as an Exercise. Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.Chapter6:Finding the Roots of f(x)=05 6–24Create a modified newton function(say,newtonb)that takes a bracket interval as input instead of a single initial guess.From the bracket limits take one bisection step to determine x0,the initial guess for Newton e the bracket limits to develop relative tolerances on x and f(x)as in the bisect function in Listing6.4.Solution:The newtonb function is listed below.The demoNewtonb function,also listed below, repeats the calculations in Example6.8with the original newton function and with the new newtonb function.Running demoNewtonb gives>>demoNewtonbOriginal newton function:Newton iterations for fx3n.mk f(x)dfdx x(k+1)1-4.422e-018.398e-01 3.526644293139032 4.507e-038.561e-01 3.521380147397333 3.771e-078.560e-01 3.521379706804574 2.665e-158.560e-01 3.5213797068045750.000e+008.560e-01 3.52137970680457newtonb function:Newton iterations for fx3n.mk f(x)dfdx x(k+1)1-4.422e-018.398e-01 3.526644293139032 4.507e-038.561e-01 3.521380147397333 3.771e-078.560e-01 3.521379706804574 2.665e-158.560e-01 3.5213797068045750.000e+008.560e-01 3.52137970680457The two implementations of Newton’s method give identical results because the input to newtonb is the bracket[2,4].This causes the initial bisection step to produce the same initial guess for the Newton iterations that is used in the call to newton.function demoNewtonb%demoNewtonb Use newton and newtonb to find the root of f(x)=x-x^(1/3)-2%%Synopsis:demoNewton%%Input:none%%Output print out of convergence history,and comparison of methodsfprintf(’\nOriginal newton function:\n’);r=newton(’fx3n’,3,5e-16,5e-16,1);fprintf(’\nnewtonb function:\n’);rb=newtonb(’fx3n’,[24],5e-16,5e-16,1);Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.6Finding the Roots of f(x)=0 function r=newtonb(fun,x0,xtol,ftol,verbose)%newtonb Newton’s method to find a root of the scalar equation f(x)=0%Initial guess is a bracket interval%%Synopsis:r=newtonb(fun,x0)%r=newtonb(fun,x0,xtol)%r=newtonb(fun,x0,xtol,ftol)%r=newtonb(fun,x0,xtol,ftol,verbose)%%Input:fun=(string)name of mfile that returns f(x)and f’(x).%x0=2-element vector providing an initial bracket for the root%xtol=(optional)absolute tolerance on x.Default:xtol=5*eps%ftol=(optional)absolute tolerance on f(x).Default:ftol=5*eps%verbose=(optional)flag.Default:verbose=0,no printing.%%Output:r=the root of the functionif nargin<3,xtol=5*eps;endif nargin<4,ftol=5*eps;endif nargin<5,verbose=0;endxeps=max(xtol,5*eps);feps=max(ftol,5*eps);%Smallest tols are5*epsif verbosefprintf(’\nNewton iterations for%s.m\n’,fun);fprintf(’k f(x)dfdx x(k+1)\n’);endxref=abs(x0(2)-x0(1));%Use initial bracket in convergence testfa=feval(fun,x0(1));fb=feval(fun,x0(2));fref=max([abs(fa)abs(fb)]);%Use max f in convergence testx=x0(1)+0.5*(x0(2)-x0(1));%One bisection step for initial guessk=0;maxit=15;%Current and max iterationswhile k<=maxitk=k+1;[f,dfdx]=feval(fun,x);%Returns f(x(k-1))and f’(x(k-1))dx=f/dfdx;x=x-dx;if verbose,fprintf(’%3d%12.3e%12.3e%18.14f\n’,k,f,dfdx,x);endif(abs(f/fref)<feps)|(abs(dx/xref)<xeps),r=x;return;endendwarning(sprintf(’root not found within tolerance after%d iterations\n’,k));Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.Chapter6:Finding the Roots of f(x)=07 6–27Implement the secant method using Algorithm6.5and Equation(6.13).Test your program by re-creating the results in Example6.10.What happens if10iterations are performed?Replace the formula in Equation(6.13)withx k+1=x k−f(x k)(x k−x k−1)f(x k k−1,whereεis a small number on the order ofεm.How and why does this change the results? Partial Solution:The demoSecant function listed below implements Algorithm(6.5)using Equation(6.13).The f(x)function,Equation6.3,is hard-coded into demoSecant.Note also that demoSecant performs ten iterations without checking for convergence.function demoSecant(a,b);%demoSecant Secant method for finding the root of f(x)=x-x^(1/3)-2=0%Implement Algorithm6.5,using Equation(6.13)%%Synopsis:demoSecant(a,b)%%Input:a,b=initial guesses for the iterations%%Output:print out of iterations;no return values.%copy initial guesses to local variablesxk=b;%x(k)xkm1=a;%x(k-1)fk=fx3(b);%f(x(k))fkm1=fx3(a);%f(x(k-1))fprintf(’\nSecant method:Algorithm6.5,Equation(6.13)\n’);fprintf(’n x(k-1)x(k)f(x(k))\n’);fprintf(’%3d%12.8f%12.8f%12.5e\n’,0,xkm1,xk,fk);for n=1:10x=xk-fk*(xk-xkm1)/(fk-fkm1);%secant formula for updating the rootf=fx3(x);fprintf(’%3d%12.8f%12.8f%12.5e\n’,n,xk,x,f);xkm1=xk;xk=x;%set-up for next iterationfkm1=fk;fk=f;endCopyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.8Finding the Roots of f(x)=0 Running demoSecant with an initial bracket of[3,4](the same bracket used in Example6.10) gives>>demoSecant(3,4)Secant method:Algorithm6.5,Equation(6.13)n x(k-1)x(k)f(x(k))0 3.00000000 4.00000000 4.12599e-011 4.00000000 3.51734262-3.45547e-032 3.51734262 3.52135125-2.43598e-053 3.52135125 3.52137971 1.56730e-094 3.52137971 3.52137971-8.88178e-165 3.52137971 3.52137971-2.22045e-166 3.52137971 3.521379710.00000e+007 3.52137971 3.521379710.00000e+00Warning:Divide by zero.>In/werk/MATLAB_Book/SolutionManual/roots/mfiles/demoSecant.m at line228 3.52137971NaN NaN9NaN NaN NaN10NaN NaN NaNThe secant method has fully converged in6iterations.Continuing the calculations beyond convergence gives afloating point exception because f(x k)−f(x k−1)=0in the denominator of Equation(6.13).In general,it is possible to have f(x k)−f(x k−1)=0before the secant iterations reach convergence.Thus,thefloating point exception exposed by demoSecant should be guarded against in any implementation of the secant method.Implementing thefix suggested in the problem statement is left as an exercise for the reader.Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.Chapter6:Finding the Roots of f(x)=09 6–33Write an m-file function to compute h,the depth to which a sphere of radius r,and specific gravity s,floats.(See Example6.12on page281.)The inputs are r and s,and the output ish.Only compute h when s<0.5.The s≥0.5case is dealt with in the following Exercise.If s≥0.5is input,have your function print an error message and stop.(The built-in error function will be useful.)Your function needs to include logic to select the correct root from the list of values returned by the built-in roots function.Partial Solution:The floata function listed below performs the desired computations.We briefly discuss three of the key statements in floata The coefficients of the polynomial are stored in the p vector.Thenc=getreal(roots(p));finds the real roots of the polynomial.The getreal subfunction returns only the real elements of a ing getreal is a defensive programming strategy.The sample calculation in Example6.12obtained only real roots of the polynomial,so getreal would not be necessary in that case.Thek=find(c>0&c<r);statement extracts the indices in the c vector satisfying the criteria0≤c k≤r.Then h=c(k);copies those roots satisfying the criteria to the h vector.No assumption is made that only one root meets the criteria.If more than one root is found a warning message is issued before leaving floata.Testing of floata is left to the reader.Copyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.10Finding the Roots of f(x)=0 function h=floata(r,s)%float Find water depth on a floating,solid sphere with specific gravity<0.5%%Synopsis:h=floata(r,s)%%Input:r=radius of the sphere%s=specific gravity of the sphere(0<s<1)%%Output:h=depth of the sphereif s>=0.5error(’s<0.5required in this version’)elsep=[1-3*r04*s*r^3];%h^3-3*r*h+4*s*r^3=0c=getreal(roots(p));k=find(c>0&c<r);%indices of elements in c such that0<c(k)<rh=c(k);%value of elements in c satisfying above criterionendif length(h)>1,warning(’More than one root found’);end%==============================function cr=getreal(c)%getreal Copy all real elements of input vector to output vector%%Synopsis:cr=getreal(c)%%Input:c=vector of numerical values%%Output cr=vector of only the real elements of c%cr=[]if c has only imaginary elementsn=0;for k=1:length(c)if isreal(c(k))n=n+1;cr(n)=c(k);endendif n==0,cr=[];warning(’No real elements in the input vector’);endCopyright c 2000,Gerald W.Recktenwald.Photocopying is permitted only for non-commercial educational purposes.。

供应链管理英文 Chapter 6 answers to problems