成本与管理会计亨格瑞第13版英文版CA16

亨格瑞 成本与管理会计

亨格瑞成本与管理会计

亨格瑞(Hengrui)是一家知名的成本与管理会计公司。

他们专注于提供成本管理、绩效管理和策略管理等方面的解决方案和咨询服务。

成本管理是指通过对企业资源和活动的成本进行测算、分析和控制,来提高企业效益和降低成本的管理方法。

亨格瑞通过帮助企业建立

成本计划和预算、制定成本控制策略、优化成本结构等手段,帮助

企业降低成本、提高利润。

绩效管理是指通过设定绩效目标、制定绩效评价体系、实施绩效测

算和分析,来提高企业绩效和激励员工的管理方法。

亨格瑞通过设

计和实施绩效管理制度、开展绩效评估和考核、提供培训和改进方

案等手段,帮助企业优化绩效,实现战略目标。

策略管理是指通过对企业内外环境的分析和评估,制定和执行战略

计划,来提高企业竞争力和市场地位的管理方法。

亨格瑞通过帮助

企业制定战略目标、开展战略规划和执行、提供战略改善建议等手段,帮助企业提升竞争力,实现可持续发展。

亨格瑞拥有一支专业的团队,拥有丰富的成本与管理会计经验,能

够根据企业的实际情况,提供量身定制的解决方案,帮助企业提高

运营效率和盈利能力。

《成本与管理会计》(第13版) CHAPTER 03

基本公式的衍生

可以将基本公式重新整理如下: 销售额 – 变动成本 – 固定成本 = 营业利润 (售价 x 销售量) – (单位变动成本 x 销售量) – 固定成本 = 营业利润 销售量(售价 – 单位变动成本) – 固定成本 = 营业利润 销售量 (单位贡献毛益) – 固定成本 = 营业利润

请记住最后那个公式,后续仍要使用

第3章

本量利分析

© 2009 Pearson Prentice Hall. All rights reserved.

决策制定、计划与控制:五步决策制 定程序(复习)

1. 确定问题与不确定性 2. 获取信息 3. 预测未来 4. 利用本量利分析方法,选择方案做决策 5. 实施决策,评价业绩与学习

© 2009 Pearson Prentice Hall. All rights reserved.

本量利分析的假设

收入和成本水平的变动仅仅是因为销售的产品数量变 动引起的

总成本能分解为不随销售量而变得固定成本部分和随 销售量而变的变动部分

如果给定一个相关范围(和一个时间区间),用图表 示的总收入和总成本性态对销售量是线性的(既可以 用直线表示)

售价,单位变动成本和总固定成本(在一个相关范围 和时间段内)是已知且不变的

为计算净利润,目标利润的CVP计算要用目标净利 润来取代目标营业利润:

目标营业利润 = I I 目标净利润 I (1-所得税税率)

© 2009 Pearson Prentice Hall. All rights reserved.

敏感性分析

本量利分析可以帮助管理人员回答一系列“如果…… 那么”问题

可以对盈亏平衡点基本公式进行简单的改变,即可计算 目标营业利润对应的销售量

成本与管理会计-亨格瑞-第13版-英文版-CA08_图文_图文

15

Variable overhead spending variance

=($29/machine hour-$30 /machine hour) ×4 500 machine-hours =(-1machine hour) ×4 500 machine-hours =$4 500F

=1 728 000/57 600=30/hour

Budgeted variable overhead cost rate per output unit

5

=0.4hour/unit×30=12/jacket

Variable overhead cost variances(P208 )

6

Flexible-budget analysis

The variable overhead efficiency variance measures the efficiency with which the costallocation base is used.

11

Variable Overhead Variances

Actual Variable Overhead Incurred

Step 3:

Identify the variable overhead costs associated with each costallocation base.

Step 4:

Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

成本与管理会计-亨格瑞-第13版-英文版-CA04共76页PPT资料

Learning objective 1 Learning objective 1

Basic Costing Terminology,conts.

Cost Assignment

Direct Costs

Indirect Costs

Cost Object

Cost Allocation

overhead

including responsibility

The direct costs of a cost object are costs that are related to the cost object and can be traced to the cost object in an economically feasible manner.

centers, departments,

customers, products, etc.

Basic Costing Terminology ,conts.

Cost assignment is a general term that includes cost tracing and cost allocation.

Costing

•Adjusting the Systems •Job costing vs

Over/Underappl

Process costing

ied Situations

Structure

•Journal Entries for the flow of

《成本与管理会计》习题及答案 costacctg13_SolPPT_ch01

a. Production Production Distribution d. Marketing

a. Cost of oil for the deep fryer b. Wages of the counter help who give customers the food they order c. Cost of the costume for the King on the Burger King television commercials d. Cost of children’s toys given away free with kids’ meals

Value chain and classification of costs Classify each of the cost items (a–h) as one of the business functions of the value chain shown in Exhibit 1-2 (p. 7). Burger King, a hamburger fast food restaurant, incurs the following costs:

Charles T. Horngren Srikant M. Datar George Foster Madhav Rajan Christopher Ittner

Cost Accounting A Managerial Emphasis thirteenth edition

This presentation includes: Exercises 1-18, 1-21 Problem 1-25

Garnicki performs a taste test at the local shopping mall to see if consumers like the taste of its proposed new chicken pie product. b. Garnicki sales managers estimate they will sell more meat pies in their northern sales territory than in their southern sales territory. c. Garnicki managers discuss the possibility of introducing a new product.

成本管理会计资料

预测

决策

编制预算 实际与预算的比较 业绩评估

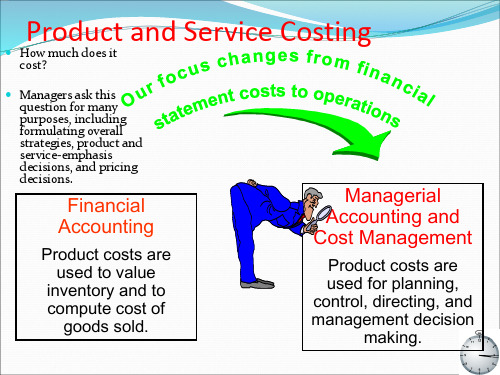

成本会计、管理会计与财务会计的关 系

• 成本会计是财务会计与管理会计的混合物

• 成本会计需要向财务会计和管理会计提供必要 的数据

• 就财务报表的编制而言,成本会计附属于财务 会计;

但从管理角度来看,成本会计也是管理会 计的一个重要组成部分,换言之,成本会计是 以管理为重心的。更进一步地讲,财务会计与 管理会计,两者都必须依赖于成本会计系统所 提供的信息。

今天的经济环境要求重新构建 成本管理系统,成本管理会计 正在经历着显著的变化。

• 全球竞争的加剧 • 产业结构的变化 • 生产环境的进步 • 适时生产系统

(JIT)的出现 • 全面质量管理(TQC)

的要求 • 作业基础成本法

(ABC)的应用

• 现代成本管理会计, 已是包括了作业成本 管理、质量成本管理、 战略成本管理等内容, 以全面提高企业竞争 能力为核心的现代会 计信息系统。

财务会计、管理会计、成本会计的关系

• 管理会计与财务会计是现代会计的二大分 支,但两者之间存在明显的区别。

• 成本会计原本是财务会计的核心组成部分, 随着成本会计的重要性日益增强,它逐渐 从财务会计中独立出来,构成了管理会计 的核心,它与管理控制共同组成了现代成 本管理会计。

成本会计是以管理为重心的

《成本管理会计》课程内容体系

• 概论

• 成本核算原理

• 成本计算方法

– 品种法 分批法 分步法 分类法

• 成本决策系统

成本习性和变动成法 策

CVP分析 短期决

• 成本控制系统

全面预算 标准成本系统 责任会计

• 课程特点 –计算比重大 –计算方法多

《成本与管理会计》习题及答案 costacctg13_SolPPT_ch04

Job costing, process costing In each of the following situations, determine whether job costing or process costing would be more appropriate.

Normal Cost $40,000 30,000 54,000 $124,000

3. At the end of 2009, compute the under- or overallocated manufacturing overhead under normal costing. Why is there no under- or overallocated overhead under actual costing?

= 1.90 or 190%

1. Compute the actual and budgeted manufacturing overhead rates for 2009.

2. During March, the job-cost record for Job 626 contained the following information: Direct materials used $40,000 Direct manufacturing labor costs $30,000 Compute the cost of Job 626 using (a) actual costing and (b) normal costing.

Job costing Process costing Job costing Process costing Job costing Process costing Job costing Job costing (some process)

亨格瑞成本与管理会计

亨格瑞成本与管理会计引言亨格瑞成本与管理会计是一种用于帮助企业管理和控制成本的方法。

它通过收集、分类和分析成本数据,帮助企业制定决策并改善绩效。

本文将介绍亨格瑞成本与管理会计的背景、概念和应用。

背景亨格瑞成本与管理会计是由美国会计学家Dale F. Hengry 于20世纪60年代提出的。

在当时,传统的财务会计主要关注企业的财务报表,而忽视了管理层对成本的关注。

亨格瑞成本与管理会计的出现填补了这一空缺,为企业提供了更全面、准确、及时的成本信息。

概念成本成本是指企业为生产或提供产品或服务所支付的资源的衡量。

它包括直接成本和间接成本。

直接成本是直接与产品或服务相关的成本,如原材料、直接人工等。

间接成本是与产品或服务间接相关的成本,如企业管理费用、销售费用等。

管理会计管理会计是一种专门用于管理决策和绩效评估的会计方法。

它与财务会计不同,会计师关注于为内部管理层提供更详细、实用的信息,以便他们做出决策和改进企业绩效。

管理会计强调成本控制、预算制定和业绩评估等方面。

亨格瑞成本法亨格瑞成本法是亨格瑞成本与管理会计的主要方法之一。

它通过以成本对象为基础,将企业的成本分为固定成本、可变成本和半固定成本,以帮助企业管理和控制成本。

固定成本是与产量无关的成本,如租金、折旧等。

可变成本是与产量成正比的成本,如直接材料、直接人工等。

半固定成本是与产量有部分相关的成本,如修理费用、研发费用等。

应用亨格瑞成本与管理会计广泛应用于各类企业中,帮助管理层制定决策、控制成本,提高企业绩效。

以下是亨格瑞成本与管理会计的几个常见应用:成本控制亨格瑞成本与管理会计为企业提供了更准确、详细的成本信息,帮助企业管理层控制成本。

通过对各类成本进行分类和分析,管理层可以识别哪些成本是可控的,从而采取相应的措施降低成本。

预算制定亨格瑞成本与管理会计可用于预算制定。

通过对成本进行分析,企业可以预测未来的成本,并制定相应的预算。

预算能够帮助企业管理层合理安排资源,控制成本。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Joint Cost Allocation Methods

Physical Measures – allocate using tangible attributes of the products, such as pounds, gallons, barrels, etc.

Market-Based – allocate using market-derived data (dollars):

CHAPTER 16

Cost Allocation: Joint Products and Byproducts

Learning objectives

Identify the splitoff point in a joint-cost situation Distinguish joint products from byproducts Explain why joint costs are allocated to individual products Allocate joint costs using four methods Explain why the sales value at splitoff method is preferred

Sales value at splitoff Net Realizable Value (NRV) Constant Gross-Margin percentage NRV

Sales Value at Splitoff Method

Uses the sales value of the entire production of the accounting period to calculate allocation percentage

Determination of inventoriable costs and cost of goods sold for internal reporting purposes such as division profitability analysis.

Cost reimbursement when a company has costreimbursement contracts as with a governmental agency.

Joint Products – outputs of a joint production process that yields two or more products with a high sales value compared to the sales values of any other outputs

ቤተ መጻሕፍቲ ባይዱ

Chart of Joint Cost Terminology

Separable Costs

Joint Cost Terminology,conts.

Categories of Joint Process Outputs:

Outputs with a positive sales value Outputs with a zero sales value

Main Product – output of a joint production process that yields one product with a high sales value compared to the sales values of the other outputs.P452(574)

Product – any output with a positive sales value, or an output that enables a firm to avoid incurring costs

Value can be high or low

Joint Cost Terminology ,conts.

when allocating joint costs Explain why joint costs are irrelevant in a sell-or-process-

further decision Account for byproducts using two methods

Joint Cost Terminology

Joint Costs – costs of a single production process that yields multiple products simultaneously

Splitoff Point – the place in a joint production process where two or more products become separately identifiable

Reasons for Allocating Joint Costs

Determination of inventoriable costs and cost of goods sold for external financial reporting and income tax determination.

Separable Costs – all costs incurred beyond the splitoff point that are assignable to each of the nowidentifiable specific products

Example of Joint Cost stituation

Byproducts – outputs of a joint production process that have low sales values compare to the sales values of the other outputs

Joint Process Flowchart