成本与管理会计 亨格瑞 第13版 英文版 CA15

亨格瑞 成本与管理会计

亨格瑞成本与管理会计

亨格瑞(Hengrui)是一家知名的成本与管理会计公司。

他们专注于提供成本管理、绩效管理和策略管理等方面的解决方案和咨询服务。

成本管理是指通过对企业资源和活动的成本进行测算、分析和控制,来提高企业效益和降低成本的管理方法。

亨格瑞通过帮助企业建立

成本计划和预算、制定成本控制策略、优化成本结构等手段,帮助

企业降低成本、提高利润。

绩效管理是指通过设定绩效目标、制定绩效评价体系、实施绩效测

算和分析,来提高企业绩效和激励员工的管理方法。

亨格瑞通过设

计和实施绩效管理制度、开展绩效评估和考核、提供培训和改进方

案等手段,帮助企业优化绩效,实现战略目标。

策略管理是指通过对企业内外环境的分析和评估,制定和执行战略

计划,来提高企业竞争力和市场地位的管理方法。

亨格瑞通过帮助

企业制定战略目标、开展战略规划和执行、提供战略改善建议等手段,帮助企业提升竞争力,实现可持续发展。

亨格瑞拥有一支专业的团队,拥有丰富的成本与管理会计经验,能

够根据企业的实际情况,提供量身定制的解决方案,帮助企业提高

运营效率和盈利能力。

成本与管理会计亨格瑞第13版英文版CA

The development of management accounting emerged in the 1920s, when the focus shifted from mere cost measurement to cost analysis and control, emphasizing the role of accounting in decision-making and management control.

It involves the identification, measurement, and allocation of costs, as well as the preparation of cost reports and other management information to assist management in making decisions about product pricing, production, and resource allocation.

Direct and indirect costs

Activity Identification

The first step in the activity-based costing method involves identifying the various activities that take place within the organization.

Cost allocation and collection

Cost Allocation

Allocating costs to specific departments, projects, or products is essential for accurate financial reporting and decision-making.

成本与管理会计-亨格瑞-第13版-英文版-CA07共75页文档

2020/6/8

10

Static Budget

What was the actual operating profit?

Revenues (10,000 × $125) $1,250,000

Less Expenses:

Variable (10,000 × $95.01)

950,100

Fixed

285,000

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS) BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

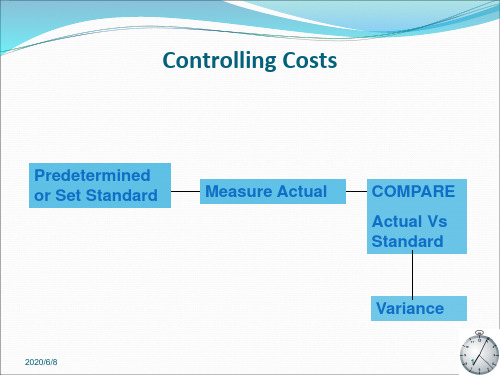

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2020/6/8

2

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

2020/6/8

$276 000 $120/JACKET 12 000JACKETS 10 000JACKETS

6

2020/6/8

7

Static Budget

es and sells jackets.

成本与管理会计 第15版 亨格瑞

成本与管理会计第15版亨格瑞简介《成本与管理会计》是由亨格瑞(Horngren)等人合著的一本经典教材,该教材详细介绍了成本和管理会计的基本概念、原则和技术。

本文将对该教材进行概览,探讨其中的关键内容。

第1章管理会计与组织绩效本章主要介绍管理会计的概念和作用,以及与组织绩效之间的关系。

管理会计是一种为管理决策提供支持的会计信息系统,通过提供与企业内部运营相关的成本和绩效信息,帮助管理层进行决策和控制。

第2章基本成本管理概念本章重点介绍成本管理的基本概念,包括成本对象、成本中心和成本效益分析等。

成本对象是指需要计算和分配成本的实体,成本中心是指组织内部负责经营活动的部门或单位,成本效益分析则是对不同决策方案进行成本与效益比较的方法。

第3章成本分类和费用估算本章讲解了成本分类和费用估算的方法和原则。

成本可以根据不同的分类方法进行归类,如按功能分类、按行业分类等。

费用估算的方法包括直接费用估算和间接费用估算,其中间接费用估算需要通过成本驱动因素进行分配。

第4章成本行为成本行为是指成本与产量或活动水平之间的关系。

本章将介绍常见的成本行为模式,如固定成本、变动成本和半固定成本。

了解成本行为模式有助于管理者预测和控制成本的变化。

第5章成本估算和预测成本估算和预测是管理会计的核心任务之一。

本章将介绍成本估算和预测的方法和技术,包括趋势分析、回归分析和敏感度分析等。

第6章作业成本系统作业成本系统是一种在生产中分配和追踪成本的方法。

本章将详细介绍作业成本系统的构成要素和运作流程,并介绍常见的作业成本方法,如作业订单和作业批次。

第7章过程成本系统过程成本系统是一种适用于连续流程生产的成本分配方法。

本章将介绍过程成本系统的特点和运作原理,以及与作业成本系统的异同。

第8章活动成本管理活动成本管理是一种基于活动的成本分析和管理方法。

本章将介绍活动成本管理的概念和技术,包括活动成本驱动因素的确定和活动成本分析模型的构建。

第9章管理会计信息系统管理会计信息系统是支持管理会计活动的信息系统。

亨格瑞成本与管理会计(中英第15版)中文PPT (10)[42页]

![亨格瑞成本与管理会计(中英第15版)中文PPT (10)[42页]](https://img.taocdn.com/s3/m/3c01b924ba0d4a7303763ac7.png)

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 10-4

y = a + bX

因变量: 被预测或管理的成本

自变量: 成本动因

截距: 固定成本

斜率: 单位变动成本

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 10-5

1. 高低点法 2. 回归分析法

这些方法不是相互排斥的,通常把它们结合起来使 用。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

10-12

通过分析实物形态下投入产出之间的关系来确 定成本函数。

包含时间和动作研究。

当投入和产出之间存在一种实物关系时,工业工 程法是估计成本函数的一种非常全面、详细的 方法,但是成本较高且非常耗时。

会计 变动成本 固定成本 混合成本

统计学 斜率 截距

线性成本函数

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 10-6

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 10-7

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

10-16

1. 选择因变量。(被预测或管理的成本) 2. 确认自变量或成本动因。(作业水平或成本动因) 3. 收集因变量和成本动因的数据。 4. 绘制散点图。 5. 估计成本函数。两种最常用的定量分析方法:高

成本与管理会计-亨格瑞-第13版-英文版-CA05

effective

base for each indirect-cost pool.

•Strategic decision

•Provide more data

•Price decision

•Multiple cost driver pools

•Market decision

2019/9/7

12

Refining a Costing System

2019/9/7

2

Structure of Lecture

Under- and over-costing – why it happens? Activity Based Costing (ABC) Indicators of need for ABC ABC system Difference between ABC and Traditional Product

Peanut-butter costing uses broad averages to assign (or spread) costs uniformly to cost objects.

The result can be undercosting or overcosting of products.

Increase in indirect costs. With modern technology, companies have experienced a decrease in direct costs with a resulting increase in indirect costs.

2019/9/7

4

Background

Easy to trace Direct materials and direct labor costs Overhead cannot be traced easily and must be

亨格瑞成本与管理会计(中英第15版)中文PPT (19)[32页]

![亨格瑞成本与管理会计(中英第15版)中文PPT (19)[32页]](https://img.taocdn.com/s3/m/6923d407b14e852459fb57c0.png)

产品质量也可能是环境发展的一个重要动力。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-3

1. 设计质量—衡量的是产品或服务的功能符合 顾客需求的程度。

的原因 6. 确定延迟的成本 7. 使用财务和非财务时间指标

Copyright © 2015 Pearson Education, Inc. All Rights Reserved 19-2

质量—根据规格制造或执行的产品或服务的总 特征和特性,以满足顾客在购买和使用期间的 具体需求。

这些公司发现,关注一种产品或服务的质量可以 成为产品生产的专家,降低生产成本,使该产品 的顾客产生较高的满意度,并为销售这些产品的 公司带来更高的未来收益。

随机差异可能发生,例如,设备高速运转中的随 机波动会导致生产出缺陷产品。

非随机差异也会发生,一般发生在因系统问题 (如不正确的速度设定、有缺陷的零件设计,或 组成部分处理不当) 而生产出缺陷产品时。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-15

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

19-16

超出控制范围的观测值作为帕累托图中的输入 点。

帕累托图反映的是每种缺陷发生的频率,按照从 最经常发生到频率最小的次序排列。

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

成本与管理会计 第15版 亨格瑞

成本与管理会计第15版亨格瑞

《成本与管理会计第15版亨格瑞》是一本关于成本和管理会计的教材,由亨格瑞(Horngren)等人合著。

该教材主要涵盖了成本与管理会计的基本概念、技术和应用,旨在帮助读者理解和应用成本与管理会计的原理和方法。

该教材的内容主要包括以下几个方面:

1. 成本与管理会计的基本概念:介绍了成本与管理会计的定义、目标和作用,以及与其他会计学科的关系。

2. 成本与管理会计的基本原理:介绍了成本与管理会计的基本原理,包括成本分类、成本行为、成本估算等。

3. 成本与管理会计的技术和方法:介绍了成本与管理会计的技术和方法,包括成本核算、成本控制、成本预测、绩效评估等。

4. 成本与管理会计的应用:介绍了成本与管理会计在不同行业和组织中的应用,包括制造业、服务业、非营利组织等。

5. 成本与管理会计的决策支持:介绍了成本与管理会计在决策过程中的应用,包括定价决策、投资决策、生产决策等。

《成本与管理会计第15版亨格瑞》的特点是理论与实践相结合,内容丰富全面,注重案例分析和实际应用。

该教

材适合会计、管理和经济学专业的学生,以及从业人员和研究者参考使用。

需要注意的是,由于该教材是第15版,可能存在一些更新和修订的内容。

建议读者在使用该教材时,参考最新的版本或与教材出版社联系,以获取最准确和详细的信息。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Single supporting department Multi supporting departments

Allocating Common Costs Cost Allocations and Contracting Revenue Allocation and Bundled Products

Fixed costs 4000(Budgeted) hours $250 per hour = $ 1000000 variable costs 3000(actual) hours $200 per hour = $ 600000

2012-10-5

8

Allocation Bases

Under either method, allocation of support costs can

2012-10-5 6

Methods to Allocate Support Department Costs,conts.

Dual-Rate Method – segregates costs within each cost pool into two segments: a variable-cost pool and a fixed-cost pool. P424(542)

7

Example for Dual-Rate Method

Budgeted fixed-costs rate P424(542)

$ 3000000 (Budgeted) ÷12000 (Budgeted or actual) hours= $250 per hour used

The costs Allocated for Microcomputer division

be based on one of the three following scenarios:

Budgeted overhead rate and budgeted hours

Budgeted overhead rate and actual hours

Actual overhead rate and actual hours

CHAPTER 15

Allocation of Support Department Costs, Common Costs, and Revenues

2012-10-5

1

CONTENT

Allocating Costs of a Supporting Department to Operating Departments

2012-10-5

3

Methods to Allocate Support Department Costs

Single-Rate Method – allocates costs in each cost pool

(service department) to cost objects (production departments) using the same rate per unit of a single allocation base p424(542)

18750-hour relevant range $200 per hour used Actual usage in 2009 in hours Microcomputer division 9000hours Peripheral equipment division 3000hours

2012-10-5 5

Example for Single-Rate Method

Budgeted usage 12000hours P424(542) Budgeted total cost pool

$3000000+12000hours $200 per hour= $ 5400000 Budgeted total rate per hour $ 5400000÷12000hours= $450 per hour used Allocation rate for Microcoputer division and Peripheral equipment division $450 per hour used Allocation cost for Microcoputer division 9000hours $450 per hour used= $ 4050000 Allocation cost for Peripheral equipment division 3000hours $450 per hour used= $ 1350000

2012-10-5 11

Allocation Bases, conts.

2012-10-5

12

Allocation Bases ,conts.

Choosing between actual and budgeted

rates

When allocations are based on budgeted usage

Fixed costs 8000(Budgeted) hours $250 per hour = $ 2000000

variable costs 9000(actual) hours $200 per hour = $ 1800000

The costs Allocated for Peripheral equipment division

2012-10-5

4

Example P424(542)

Practical capacity 18750hours Fixed costs of operating the computer facility $3000000 Budgeted long-run usage in hours Microcomputer division 8000hours Peripheral equipment division 4000hours Budgeted variable cost per hour in 6000-hour to

user divisions know in advance their allocated costs.

This can be of benefit in short-term and long-term planning. A disadvantage of using budgeted costs is that there is an incentive for managers to underestimate their planned usage thus being assigned a lower percentage of allocated costs. This can be overcome in part by assessing a higher charge for exceeding budgeted usage.

Each pool uses a different cost-allocation base

Dual-rate method treats fixed and variable costs

more realistically, but is more complex to implement

2012-10-5

2012-10-5

9

Example for Allocation Bases

Single-Rate Method P425(543)

Budgeted figeted) ÷18750 (capacity) hours= $160 per hour used Budgeted variable-costs rate $200 per hour used Allocation cost for Microcomputer division 9000hours $360 per hour used= $ 3240000 Allocation cost for Peripheral equipment division 3000hours $360 per hour used= $ 1080000 Fixed costs of unused computer capacity 6750hours $160 per hour used= $ 1080000

2012-10-5 13

Allocation Bases ,conts.

Allocating costs based on actual usage give a

more accurate allocation based on actual costs and usage.

Actual allocations have several disadvantages: a lack of timely information, reduced incentives for support to manage costs, and increased accounting costs.

2

2012-10-5

2

Allocating Costs of a Supporting Department to Operating Departments

Supporting Department –which is also called a

service department , provides the services that assist other internal departments in the company p423(541) Operating Department – which is also called a production department, directly adds value to a product or service