成本与管理会计亨格瑞第13版英文版CA05

亨格瑞 成本与管理会计

亨格瑞成本与管理会计

亨格瑞(Hengrui)是一家知名的成本与管理会计公司。

他们专注于提供成本管理、绩效管理和策略管理等方面的解决方案和咨询服务。

成本管理是指通过对企业资源和活动的成本进行测算、分析和控制,来提高企业效益和降低成本的管理方法。

亨格瑞通过帮助企业建立

成本计划和预算、制定成本控制策略、优化成本结构等手段,帮助

企业降低成本、提高利润。

绩效管理是指通过设定绩效目标、制定绩效评价体系、实施绩效测

算和分析,来提高企业绩效和激励员工的管理方法。

亨格瑞通过设

计和实施绩效管理制度、开展绩效评估和考核、提供培训和改进方

案等手段,帮助企业优化绩效,实现战略目标。

策略管理是指通过对企业内外环境的分析和评估,制定和执行战略

计划,来提高企业竞争力和市场地位的管理方法。

亨格瑞通过帮助

企业制定战略目标、开展战略规划和执行、提供战略改善建议等手段,帮助企业提升竞争力,实现可持续发展。

亨格瑞拥有一支专业的团队,拥有丰富的成本与管理会计经验,能

够根据企业的实际情况,提供量身定制的解决方案,帮助企业提高

运营效率和盈利能力。

《成本与管理会计》习题及答案 costacctg13_SolPPT_ch20

The purchasing officer of the Cloth Center has collected the following information:

Exercise 20-18

EOQ for a retailer The Cloth Center sells fabrics to a wide range of industrial and consumer users. One of the products it carries is denim cloth, used in the manufacture of jeans and carrying bags. The supplier for the denim cloth pays all incoming freight. No incoming inspection of the denim is necessary because the supplier has a track record of delivering high-quality merchandise. The purchasing lead time is 2 weeks. The Cloth Center is open 250 days a year (50 weeks for 5 days a week).

Exercise 20-32

Supply chain effects on total relevant inventory cost Cow Spot Computer Co. outsources the production of motherboards for its computers. It has narrowed down its choice of suppliers to two companies: Maji and Induk. Maji is an older company with a good reputation, while Induk is a newer company with cheaper prices. Given the difference in reputation, 5% of the motherboards will be inspected if they are purchased from Maji, but 25% of the motherboards will be inspected if they are purchased from Induk.

成本与管理会计亨格瑞第13版英文版CA02

different purposes Describe a framework for cost accounting and cost management

2020/10/8

Learning objective 1 Define and illustrate a cost object

2-3

2020/10/8

companies, and service-sector companies Describe the three categories of inventories commonly found in

manufacturing companies Distinguish inventoriable costs from period costs Explain why product costs are computed in different ways for

Following accumulation, costs are assigned to the chosen cost object. involves tracing and allocating costs

✓ Tracing:accumulated costs with a direct relationship to the cost object

成本与管理会计-亨格瑞-第13版-英文版-CA07共75页文档

2020/6/8

10

Static Budget

What was the actual operating profit?

Revenues (10,000 × $125) $1,250,000

Less Expenses:

Variable (10,000 × $95.01)

950,100

Fixed

285,000

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS) BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

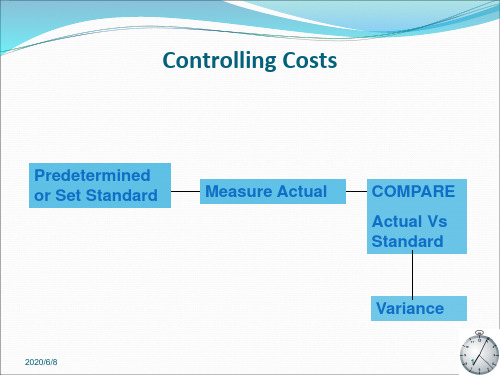

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2020/6/8

2

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

2020/6/8

$276 000 $120/JACKET 12 000JACKETS 10 000JACKETS

6

2020/6/8

7

Static Budget

es and sells jackets.

成本与管理会计 亨格瑞 第13版 英文版 CA05

2012-10-5

Broad Averaging and Cross-subsidization,conts.

When a company has a situation in which

undercosting or overcosting of products occurs, this is referred to as product-cost cross-subsidization. P110

costing system

2012-10-5

11

Rationale for Refining Costing System

Increase in product diversity •Customized products

•Differentiate from competitors

Guidelines for Refining

2012-10-5

4

Background

Easy to trace Direct materials and direct labor costs

Overhead cannot be traced easily and must be allocated with estimates.

Recall that Factory Overhead is applied to production in a

rational and systematic manner, using some type of averaging. There are a variety of methods to accomplish this goal.

Simple Methods Unrealistic

成本与管理会计-亨格瑞-第13版-英文版-CA08_图文_图文

15

Variable overhead spending variance

=($29/machine hour-$30 /machine hour) ×4 500 machine-hours =(-1machine hour) ×4 500 machine-hours =$4 500F

=1 728 000/57 600=30/hour

Budgeted variable overhead cost rate per output unit

5

=0.4hour/unit×30=12/jacket

Variable overhead cost variances(P208 )

6

Flexible-budget analysis

The variable overhead efficiency variance measures the efficiency with which the costallocation base is used.

11

Variable Overhead Variances

Actual Variable Overhead Incurred

Step 3:

Identify the variable overhead costs associated with each costallocation base.

Step 4:

Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

成本与管理会计-亨格瑞-第13版-英文版-CA08

Flexible Budget for Variable Overhead at Actual Hours

AH × SVR

Flexible Budget for Variable Overhead at

Standard Hours

SH × SVR

Spending Variance

Efficiency Variance

Workers were less skilled than expected in using machines?

Webb spend more on variable overhead costs , such as maintenance?

8

2019/10/7

Variable Overhead Variances

=$15 000U

14

2019/10/7

4500 HOURS VS 4000 HOURS

Possible causes for exceeding budget

Workers were less skilled than expected in using machines

Production scheduler inefficiently scheduled jobs ,resulting in more machinehours used than budgeted

overhead cost

Efficiency

cost-alocation base alocation based alowed

per unit of

Variance

used for actual output for actual output

成本与 管理会计第十三版读书笔记

成本与管理会计第十三版读书笔记好的,以下是为您生成的一篇关于“成本与管理会计第十三版读书笔记”的文章:在会计的世界里,成本与管理会计就像是一座神秘的宝藏,等待着我们去探索和发掘。

当我翻开这第十三版的书籍,仿佛打开了一扇通往智慧宝库的大门。

书中对于成本的阐述,那可真是精彩绝伦。

它可不是简单的数字罗列,而是有着深刻内涵的经济密码。

你想想,成本就像是我们日常生活中的开销,每一笔都得精打细算。

比如说,你要装修房子,买材料、请工人,这一笔笔费用不就是成本吗?要是不仔细核算,超支了可就麻烦啦!管理会计呢,则像是一位高明的军师。

它能帮助企业制定战略,做出明智的决策。

这不就像我们下棋,每一步都要深思熟虑,考虑到各种可能的情况和后果。

如果没有管理会计的指引,企业就像没头的苍蝇,到处乱撞,能成功才怪呢!书中讲到的成本分类,那叫一个细致入微。

固定成本、变动成本,这就好比我们的性格,有的部分始终不变,有的部分却会随着环境而改变。

再比如机会成本,这多像我们在人生的十字路口面临的选择,选择了一条路,就意味着放弃了其他可能的机会,那些被放弃的不就是机会成本吗?还有成本核算的方法,那可真是五花八门。

什么分批法、分步法,听起来复杂,其实理解了就会发现,它们就像做菜的不同步骤和技巧,只要掌握得当,就能做出美味的“财务大餐”。

再说说预算管理,这简直是企业的航行图。

如果没有预算,企业就像在大海中没有指南针的船只,不知道该往哪儿走,能不迷失方向吗?而通过合理的预算编制和控制,企业就能有条不紊地朝着目标前进。

成本控制更是关键中的关键。

就好比我们减肥,要控制饮食、增加运动,企业也要控制成本,优化流程,提高效率。

不然,臃肿的成本会把企业压得喘不过气来。

管理会计中的绩效评价,就像是给企业的表现打分。

做得好要奖励,做得不好要改进。

这和我们在学校考试得高分受表扬,低分要努力不是一个道理吗?总之,这本成本与管理会计第十三版,真的是让我大开眼界,收获满满。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

When a company has a situation in which undercosting or overcosting of products occurs, this is referred to as product-cost cross-subsidization. P110

Background

Easy to trace Direct materials and direct labor costs

Overhead cannot be traced easily and must be allocated with estimates.

Recall that Factory Overhead is applied to production in a rational and systematic manner, using some type of averaging.

entree dessert drinks

total

emma

11

0

4

15

james

20

8

14

42

jessica

15

4

8

27

matthew

14

4

6

24

total

60

16

32

108

average

15

4

8

27

Broad Averaging and Cross-subsidization,conts.

Historically, firms produced a limited variety of goods while their indirect costs were relatively small.

Present three guidelines for refining a costing system

Rationale for Refining Costing System

Increase in product diversity

Increase in Indirect Costs

•Customized products

Increase in product diversity. The growing demand for customized products has led to product diversity with the result that products demand differing levels of resources.

Allocating overhead costs was simple: use broad averages to allocate costs uniformly regardless of how they are actually incurred

The use of broad averages in allocating indirect costs can have a number of adverse consequences.

Advance in product and

•Differentiate from competitors

process technology increase indirect cost,

Guidelines for Refining a cost systems lower direct costs

The result can be undercosting or overcosting of products.

Overcosting – a product consumes a low level of resources but is allocated high costs per unit (Emma’s dinner)

1. Direct-cost tracing

classify as many of the total costs as

direct costs as is economically feasible.

2. Indirect-cost pools

expand the number of cost pools until

Refining a Costing System,conts

Three guidelines are presented for refining a costing system.

Costs ➢Activity Based Management (ABM) ➢Value and non-value added costs

LEARNING OBJECTIVE 1

Explain how broad averaging undercosts and overcosts products or services

Advances in IT

each of these pools is homogeneous. Competition in markets

3. Cost-allocation basis

•Make trace more cost- identify the preferred cost-allocation

成本与管理会计亨格瑞 第13版英文版CA05

2020年7月14日星期二

LEARNING OBJECTIVES

Explain how broad averaging undercosts and overcosts products or services

Present three guidelines for refining a costing system Distinguish between simple and activity-based costing systems Describe a four-part cost hierarchy Cost products or services using activity-based costing Explain how activity-based costing systems are used in activity-

of total costs

Sales are increasing, but profits are declining.

Marketing does not use costs reports for

pricing decisions

Product-line profit margins are hard

There are a variety of methods to accomplish this goal.

Simple Methods Unrealistic

Complex Methods Realistic

Broad Averaging and Cross-subsidization

P110

effective

base for each indirect-cost pool.

•Strategic decision

•Provide more data

•Price decision

•Multiple cost driver pools

•Market decision

Refining a Costing System

The results of overcosting one product and undercosting another.

The overcosted product absorbs too much cost, making it seem less profitable than it really is.

The undercosted product is left with too little cost, making it seem more profitable than it really is.

The Need for ABC

Direct labor is a small percentage

to explain

Line managers do not believe the product costs reports

Some products that have reported high profit margins are not sold by competitors

LEARNING OBJECTIVE 2

Traditional product-costing methods use a single indirect cost rate to allocate costs to all products.

Broad Averaging and Cross-subsidization, conts.

Refining a Costing System,conts

A refined cost system reduces the use of broad averages for assigning costs to resources. There are three principal reasons that have accelerated the demand for such refinements.