财务报表分析 第十版答案 第四章 (部分)

财务报表分析(第4版)练习题参考答案

财务报表分析(第四版)练习题参考答案第1章基本财务报表★网络习题略★业务题1.(1)年末资产总额=年末负债总额+年末所有者权益总额=20,000+30,000=50,000(元)年初资产总额=年末资产总额-20×1年度资产增加额=50,000-10,000=40,000(元)年初所有者权益总额=年初资产总额-年初负债总额=40,000-25,000=15,000(元)20×1年度利润=年末所有者权益总额-年初所有者权益总额-20×1年度资本投入净额=30,000-15,000-4,000=11,000(元)或者:所有者权益变动额=资产变动额-负债变动额=10,000-(20,000-25,000)=15,000(元)20×1年度利润=所有者权益变动额-20×1年度资本投入金额=15,000-4,000=11,000(元)(2)尽管根据前后两期的资产负债表就可以计算出当期利润,但是,这只是履行会计的内部职能(会计核算)。

基于现代企业制度与金融市场框架,会计还需要履行其外部功能,对外披露有助于决策的信息。

财务报表(利润表)是会计履行其外部职能的重要载体。

况且,利润表不仅仅要披露当期利润的数额,更要充分展现当期利润的形成过程。

因此,企业还要编制利润表。

2.(1)某服务企业20×1年度的利润表和资产负债表(2)某服务企业20×1年12月31日的未分配利润为13,516元。

★案例分析2.由此可能导致中间指标如销售毛利、营业利润、营业外收支净额和利润总额等有用信息的缺失。

第2章财务报表分析基本框架★案例分析1.(1)亨利与银行之间可能存在的利益冲突:股东作为“分享”阶层与债权人作为“支薪”的利益冲突。

债权人只关注“还本付息”问题。

(2)亨利与其他股东之间可能存在的利益冲突:大股东与小股东的利益冲突。

(3)亨利企业的经理与亨利和其他股东之间可能存在的利益冲突:经理作为“支薪”阶层与股东作为“分享”阶层的利益冲突,由此可能产生“道德风险”与“逆向选择”问题。

第四章 财务与报表处理系统(试题及答案)

第四章财务与报表处理系统单选题1.账套是用于存放核算单位会计数据的实体,一个账套代表一个________。

DA:核算项目B:会计期间C:数据文件D:核算单位2.在整个会计循环中账务处理系统对会计人员的技术要求,只在于从原始凭证到________的编制和确认。

BA:会计账簿B:记账凭证C:会计报表D:总分类账3.建立套账时需要指定的基本信息中没有________。

CA:账套主管B:账套启用期间C:结账日期D:账套存储路径A 4.计算机账务处理系统是建立在________和会计恒等式基础上的一个通用系统,其数据源仍然是历史的、能以货币计量的数据。

A:会计循环B:会计理论C:会计实务D:会计科目5.在凭证规则的制单控制中不包括________。

CA:资金及往来赤字控制B:预算控制与支票控制C:制单人员控制D:现金流量控制6.账务系统日常最基本的业务是凭证处理,其主要流程是________。

BA:填制凭证→凭证审核→凭证汇总B:填制凭证→凭证审核→凭证记账C:输入凭证→处理凭证→输出凭证D:查询凭证→显示凭证→打印凭证7.下列不属于会计科目设置内容的是________。

AA:科目余额B:是否核算数量C:是否核算现金流量D:是否辅助核算8.下列子系统中不需要从账务处理系统读取数据的是________。

CA:成本核算系统B:报表系统C:固定资产核算系统D:财务分析系统9.下列功能模块不属于账务处理系统的是________。

AA:工资设置B:账表管理C:出纳管理D:系统设置10.核算项目与明细科目的主要区别在于D________。

A:两者的编码不一样B:两者的作用不一样C:核算项目限于往来单位、部门、职员等,而明细科目更广泛D:核算项目与科目是多对多关系,而明细科目与上级科目是多对一关系11.辅助核算一般通过设置________A来实现。

A:核算项目B:会计科目C:会计报表D:会计账簿12.设某股份公司的各级科目均不超过99个,应D采用的科目代码结构是______。

《财务报表分析》课后习题参考答案

《财务报表分析》课后习题参考答案第二章(P82)1.(1) A 公司债权(应收账款、应收票据、其他应收款、预付账款等) 超过了资产总额的 75%,规模过大,说明公司的货币资金、存货、投资、固定资产、无形资产等在资产总额中不足 25%。

(2)应收母公司款项达公司债权的 80%以上,占公司资产总额的75%╳80%=60%。

如此庞大的关联交易债权值得怀疑,可能存在着转移资金、非法占用、控制利润等行为。

(3)母公司已严重资不抵债面临破产清算,意味着相应的债权不能收回或者不能彻底收回,将会使 A 公司遭受严重的资产损失,并将进一步导致公司严重亏损、资金周转艰难、股票价格暴跌、公司形象严重受损。

2.存货积压可能是因为采购过多,也可能是因为生产过多而销路不畅。

不管是哪种原因,在近期来看,公司没有什么损失;即使是销路不畅,但可使公司流动资产增加,给人一种短期偿债能力增强的假象;并可使大量费用予以资产化,降低了当期的费用,从而使当期利润有良好表现。

从长期看,存货积压会导致资金占用增加、储存费用增加;若存货积压属于产成品销路不畅,则后果更为严重,未来会发生存货资产损失和亏损。

3.2005 年科龙电器长期资产质量(1)固定资产。

部份设备严重老化,说明公司在较长一断时间内发展停滞,也缺乏技术进步;模具大量闲置,说明管理不到位,是采购有问题还是转产所致?不管什么原因造成闲置,都应及时加以处置减少损失。

至于部分公司住手经营,设备未能正常运转,可能与顾董事长出事、管理浮现真空有关。

固定资产是公司经营的核心资产,固定资产质量低劣,会对公司未来的业绩产生消极的影响。

(2)无形资产。

商标价值在过去可能存在着高估。

这也反映了公司当时存在着管理问题。

我们知道,商标惟独在购入或者接受投资时才需入账。

因此,商标价值过去高估,现在贬值,将直接给公司带来经济损失。

诉讼中的土地使用权,是因为转让方并没有向其受让方付款,所以转让方可能并没有转让的权利。

财务报告分析课后答案(3篇)

第1篇一、概述财务报告分析是财务学的一个重要组成部分,通过对企业财务报告的分析,可以帮助我们了解企业的财务状况、经营成果和现金流量。

本课后答案旨在对教材中的财务报告分析相关内容进行梳理和总结,并结合实际案例进行分析,以加深对财务报告分析的理解。

二、财务报告分析的基本方法1. 比率分析法比率分析法是通过计算和分析企业财务报表中的各项比率,来评价企业的财务状况和经营成果。

常见的比率包括:- 流动比率:衡量企业短期偿债能力的指标,计算公式为:流动资产/流动负债。

- 速动比率:衡量企业短期偿债能力的指标,计算公式为:(流动资产-存货)/流动负债。

- 资产负债率:衡量企业长期偿债能力的指标,计算公式为:负债总额/资产总额。

- 净资产收益率:衡量企业盈利能力的指标,计算公式为:净利润/净资产。

2. 趋势分析法趋势分析法是通过比较企业连续几个会计期间的财务报表数据,来分析企业的财务状况和经营成果的变化趋势。

通过趋势分析,可以了解企业的财务状况是否稳定,经营成果是否持续增长。

3. 比较分析法比较分析法是将企业的财务报表数据与行业平均水平、竞争对手或历史数据进行比较,来评价企业的财务状况和经营成果。

通过比较分析,可以了解企业在行业中的地位和竞争力。

三、案例分析以下以某上市公司为例,进行财务报告分析。

1. 比率分析法(1)流动比率:假设该公司2021年流动资产为100亿元,流动负债为50亿元,则流动比率为2。

(2)速动比率:假设该公司2021年存货为20亿元,则速动比率为1.2。

(3)资产负债率:假设该公司2021年负债总额为200亿元,资产总额为500亿元,则资产负债率为40%。

(4)净资产收益率:假设该公司2021年净利润为10亿元,净资产为50亿元,则净资产收益率为20%。

2. 趋势分析法(1)流动比率:假设该公司2018年至2021年流动比率分别为1.5、2、2.2、2,可以看出流动比率逐年上升,说明公司短期偿债能力增强。

(财务报表管理)财务报表分析 十版 七 答案(部分)

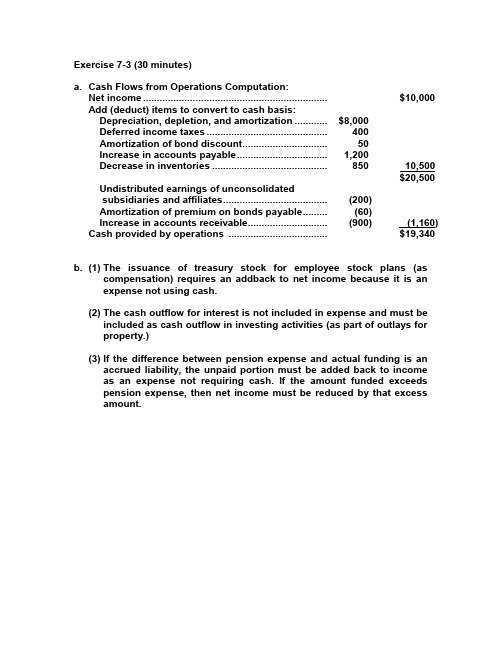

a. Cash Flows from Operations Computation:Net income ................................................................... $10,000 Add (deduct) items to convert to cash basis:Depreciation, depletion, and amortization ............ $8,000Deferred income taxes (400)Amortization of bond discount (50)Increase in accounts payable ................................. 1,200Decrease in inventories .......................................... 850 10,500$20,500 Undistributed earnings of unconsolidatedsubsidiaries and affiliates (200)Amortization of premium on bonds payable (60)Increase in accounts receivable ............................. (900) (1,160) Cash provided by operations .................................... $19,340 b. (1) The issuance of treasury stock for employee stock plans (ascompensation) requires an addback to net income because it is anexpense not using cash.(2) The cash outflow for interest is not included in expense and must beincluded as cash outflow in investing activities (as part of outlays forproperty.)(3) If the difference between pension expense and actual funding is anaccrued liability, the unpaid portion must be added back to incomeas an expense not requiring cash. If the amount funded exceedspension expense, then net income must be reduced by that excessamount.a. Beginning balance of accounts receivable ........ $ 305,000Net sales ............................................. 1,937,000Total potential receipts $2,242,000Ending balance of accounts receivable ............. - 295,000Cash collected from sales $1,947,000b. Ending balance of inventory ................................ $ 549,000Cost of sales ......................................................... +1,150,000Total ............................................. $1,699,000Beginning balance of inventory .......................... - 431,000Purchases ............................................................. $1,268,000 Beginning balance of accounts payable $ 563,000Purchases (from above) ....................................... 1,268,000Total potential payments ..................................... $1,831,000Ending balance of accounts payable .................. - 604,000Cash payments for accounts payable ................ $1,227,000c. Issuance of common stock.................................. $ 81,000Issuance of treasury stock .................................. 17,000Total nonoperating cash receipts ....................... $ 98,000d. Increase in land .................................................... $ 150,000Increase in plant and equipment ......................... 18,000Total payments for noncurrent assets ............... $ 168,000 Exercise 7-5 (20 minutes)b. X Fc. X Fd. X Ie. X Ff. NCNg. X Ih. NCSi. X Fj. X X Ob. X Fc. NCNd. X Ie. NCSf. NCNg. X Ih. NCSi. NE j. NE Exercise 7-7 (30 minutes)Net Cash from Cash2. NE NE +3. + + +4a. - NE NE4b. NE(1)+(2)+(2)4c. - +(2)+(2)5. NE + +6. - + (long-run -) + (long-run -)7. - -(5)+8. + NE NE9. +(3)+(4)+(4)10. NE + +11. + + +12. NE NE +13. NE NE +(1) Deferred tax accounting.(2) Depends on whether tax savings are realized in cash.(3) If profitable.(4) If accounts receivable collected.(5) Depends on whether interest is paid or accrued.Further explanations (listed by proposal number):1. Substituting payment in stock for payment in cash for its dividends will not affectincome or CFO but will increase cash position.2. In the short run, postponement of capital expenditures will save cash but have noeffect on income or CFO. In the long term, both income and CFO may suffer due to lower operating efficiency.Exercise 7-7—continued3. Cash not spent on repair and maintenance will increase all three measures. However,the skimping on necessary discretionary costs will adversely impact future operating efficiency and, hence, profitability.4. Managers advocating an increase in depreciation may have spoken in the mistakenbelief that depreciation is a source of cash and that consequently increasing it would result in a higher cash inflow. In fact, the level of depreciation expense has no effect on cash flow—the same amount of depreciation deducted in arriving at net income is added back in arriving at CFO. On the other hand, increasing depreciation for tax purposes will in all cases result in at least a short-term savings.5. Quicker collections will not affect income but will increase CFO because of loweraccounts receivable. Cash will also increase by the speedier conversion of receivables into cash. In the longer run this stiffening in the terms of sale to customers may result in sales lost to competition.6. Payments stretched-out will lower income because of lost discounts but doespositively affect CFO by increasing the level of accounts payable. Cash conservation will result in a higher cash position. Relations with suppliers may be affected adversely. Note: Long-term cash outflow will be higher because of the lost discount. 7. Borrowing will result in interest costs that will decrease income and CFO. Cashposition will increase.8. This change in depreciation method will increase income in the early stages of anasset's life. The opposite may hold true in the later stages of the asset's life.9. In the short term, higher sales to dealers will result in higher profits (assuming we sellabove costs) and, if they pay promptly, both CFO and cash will increase. However, unless the dealers are able to sell to consumers, such sales will be made at the expense of future sales.10. This will lead to less income from pension assets in the future which could causefuture pension expense to increase.11. The cost of funding inventory will be reduced in the future. In the current period netincome may also be increased by a LIFO liquidation from reduced inventory levels. 12. The current period decline in the value of the trading securities has been reflected incurrent period income, as has the previous gain. Although the sale will increase cash, it will have no effect on current period income. If the current period decline is deemed to be temporary, the company is selling a potentially profitable security for a short-term cash gain.13. Reissuance of treasury shares will increase cash, but will have no effect on currentperiod income as any “gain” or “loss” is reflected in additional paid in capital, not income. If the stock price is considered to be temporarily depressed, the company is foregoing a future sale at a greater market price and is, thus, suffering current dilution of shareholder value.Exercise 7-9 (60 minutes)Notes:[a] Balance at 7/29/Year 10 ........................................... $624.5 [33]Less: increase in Year 10 ........................................ (60.4) [61]$564.1[b]This amount is overstated by the provision for doubtful accounts expense that is included in another expense category.Note [a]: Item [89] represents dividends declared, not dividends paid (see also Item [77]).d. The entry for the income tax provision for Year 11 is:Income tax expense [27] ...................................... 265.9Deferred income tax (current) plug .................. 12.1Income tax payable ............................................ 230.4Deferred income tax (noncurrent) [a] .............. 23.4Notes:(1) The entry increases current liabilities by $12.1 since deferred income tax (current)is credited by this amount. It also increases current liabilities by $230.4 [124A], the amount of income taxes payable.(2) The [a] is the difference in the balance of the noncurrent deferred income tax item[176] = $258.5 - $235.1 = $23.4.(3) Also, $23.4 + $12.1 = $35.5, which is total deferred tax [59] or [127A]Exercise 7-9—continuede. Depreciation expense has no effect on cash from operations. The credit,when recording the depreciation expense, goes to accumulated depreciation, a noncash account.f. These provisions are added back because they affect only noncashaccounts, the charge to earnings must be removed in converting it to the cash basis.g. The “Effect of exchange rate changes on cash” represents translationadjustments (differences) arising from the translation of cash from foreign currencies to the U.S. dollar.h. Any gain or loss is reported under "other, net"—Item [60].i. Free cash flows =Cash flow from operations –Cash used for capital additions –Dividends paidYear 11: $805.2 – $361.1 – $137.5 = $306.6Year 10: $448.4 – $387.6 – $124.3 = $(63.5)Year 9: $357.3 – $284.1 – $86.7 = $(13.5)j. Start-up companies usually have greater capital addition requirements and lower cash inflows from operations. Also, start-ups rarely pay cash dividends. Free cash flow earned by start-up companies is usually used to fund the growth of the company, especially if successful.k. During the launch of a new product line, the statement of cash flows can be affected in several ways. First, cash flow from operations is lower because substantial advertising and promotion is required and sales growth has not yet been maximized. Second, substantial capital additions are usually necessary to provide the infrastructure for the new product line. Third, cash flow from financing can be affected if financing is obtained to launch this new product line.。

财务报表分析课后习题答案

财务报表分析课后习题答案第一章财务报表分析概述一、名词解释财务报表分析筹资活动投资活动经营活动会计政策会计估计资产负债表日后事项二、单项选择1.财务报表分析的对象是企业的基本活动,不是指()。

A筹资活动B投资活动C经营活动D全部活动2.企业收益的主要来源是()。

A经营活动B 投资活动C筹资活动D 投资收益3.短期债权包括()。

A 融资租赁B银行长期贷款C 商业信用D长期债券4.下列项目中属于长期债权的是()。

A短期贷款B融资租赁C商业信用D短期债券5.在财务报表分中,投资人是指()。

A 社会公众B 金融机构C 优先股东D 普通股东6.流动资产和流动负债的比值被称为()。

A流动比率B 速动比率C营运比率D资产负债比率7.资产负债表的附表是()。

A利润分配表B分部报表C财务报表附注D应交增值税明细表。

8.利润表反映企业的()。

A财务状况B经营成果C财务状况变动D现金流动9.我国会计规范体系的最高层次是()。

A企业会计制度B企业会计准则C会计法D会计基础工作规范10.注册会计师对财务报表的()。

A公允性B真实性C正确性D完整性三、多项选择1.财务报表分析具有广泛的用途,一般包括()。

A.寻找投资对象和兼并对象B.预测企业未来的财务状况C.预测企业未来的经营成果D. 评价公司管理业绩和企业决策E.判断投资、筹资和经营活动的成效2.分析可以分为()等四种。

A 定性分析B定量分析C因果分析D系统分析E以上几种都包括3.财务报表分析的主体是()。

A 债权人B 投资人C 经理人员D 审计师E 职工和工会4.作为财务报表分析主体的政府机构,包括()。

A税务部门B国有企业的管理部门C证券管理机构D会计监管机构E社会保障部门5.财务报表分析的原则可以概括为()。

A目的明确原则B动态分析原则C系统分析原则D成本效益原则E实事求是原则6.在财务报表附注中应披露的会计政策有()。

A坏账的数额B收入确认的原则C 所得税的处理方法D存货的计价方法E固定资产的使用年限7.在财务报表附注中应披露的会计政策有()。

财务报表分析(第十版)FSA_Lecture4

Financial Statement AnalysisLecture 4Analyzing Investing Activities Main References:–Subramanyam and Wild, chapters 4Assets•Assets are defined as resources with probable future benefits.•Distortions may generally arise from ambiguities about whether:–The firm owns/controls the economic resource–Future economic benefits can be measured with reasonable certainty–Fair values are higher or lower than book values Asset Distortions: Ownership / Control •Some types of transactions make it difficult to assess the ownership of an asset.•激进的收入确认可能会影响相关资产价值•管理层可能与审计人员或分析师持有不同的意见在资产估值方面。

•公认会计准则(GAAP)不可能抓住某些资产的所有权或控制权的微妙关联。

Assets Current Asset (流动资产)Operating cycle 营业周期 Working capital 营运资本Financial assets 金融资产 Operating assets 经营资产Credit analysis 信用分析Profitability analysis 盈利能力分析 Equity valuation 权益估值Current Asset (P153)Credit underwriting 应收款的信用包销Just-in-time inventory management实时存货管理降低流动资产投资,增强盈利能力和现金流量。

初级会计学第10版第四章E4-4答案

初级会计学第10版第四章E4-4答案一、单项选择题(本类题共24小题,每小题1.5分,共36分。

每小题备选答案中,只有一个符合题意的正确答案。

多选、错选、不选均不得分。

)1.下列各项中,不属于会计监督职能内容的是()。

[单选题] *A.会计对经济活动的合法性进行审查B.会计对经济活动的合理性进行审查C.会计对经济活动的真实性进行审查D.会计对经济活动的及时性进行审查(正确答案)答案解析:会计监督职能,是指对特定主体经济活动和相关会计核算的真实性、合法性和合理性进行监督检查。

选项D,不属于会计监督职能的内容。

2.下列有关会计等式的说法中,不正确的是()。

[单选题] *A.“资产=负债+所有者权益”属于静态等式B.“收入-费用=利润”属于动态等式C.“资产=负债+所有者权益”是复式记账法的理论基础D.“收入-费用=利润”是编制资产负债表的依据(正确答案)答案解析:选项D,“收入-费用=利润”是编制利润表的依据,“资产=负债+所有者权益”是编制资产负债表的依据。

3.下列各项中,不属于账户金额要素的是()。

[单选题] *A.期末余额B.期初余额C.本期增加发生额D.上期减少发生额(正确答案)答案解析:账户的四个金额要素为期初余额、期末余额、本期增加发生额、本期减少发生额。

4.审核原始凭证各项基本要素是否齐全、有关经办人员签章是否齐全等内容,这属于审核原始凭证的()。

[单选题] *A.合法性B.合理性C.完整性(正确答案)D.及时性答案解析:审核原始凭证的完整性是指审核原始凭证的内容是否齐全,包括有无漏记项目、日期是否完整、有关签章是否齐全等。

5.甲企业为增值税一般纳税人,采用实际成本法进行存货的日常核算。

2020年10月5日购入一批材料,增值税专用发票上注明的价款为50 000元,增值税税额为6 500元,运输途中发生合理损耗2 500元,材料已验收入库,款项已用银行汇票结算。

不考虑其他因素,下列各项中,关于该企业购入材料的会计处理正确的是()。