中级会计1考试1题库

中级会计考试题库

中级会计考试题库一、选择题1. 会计核算的基本原则包括()。

A.价值约束原则B.一贯性原则C.收益确认原则D.公允价值原则2. 固定资产的折旧计算通常采用的方法有()。

A.年限平均法B.直线法C.比例减值法D.复合法3. 会计报表中的“表外事项”是指()。

A.影响资产负债和损益表的一些事件B.影响利润分配的一些事项C.不对企业的财务状况和经营成果产生影响的事项D.影响股东权益的一些事项4. 下列哪个项目不属于财务费用()。

A.银行贷款利息支出B.应付账款利息C.所得税支出D.借款手续费5. 下列哪个不是财务报表中“应收账款”相关的项目()。

A.销售货物B.提供劳务C.利息收入D.投资收益二、判断题6. 利润表的报表期应该表现为一段时间,并由此期间内的损益表明细科目的数额构成。

()7. 固定资产的减值准备是资产减值的一个明确指标,其数额应准确反映实际变动。

()8. 应交税费是企业的一种负债,应资产减值准备是企业的一种负债。

()9. 短期投资是指企业长期投资能够获得预期经济利益的证券。

()10. 资产负债表是财务会计的基本报表之一,用以反映企业某一时点的财务状况。

()三、简答题11. 什么是会计准则?它的作用是什么?12. 什么是“资产负债表”?请简要描述其编制内容和用途。

13. 请简要说明“负债”的分类及其表现形式。

14. 请说明会计科目的分类及名称规范。

15. 什么是会计核算?其过程包括哪些内容?四、计算题16. 某公司2019年12月31日的固定资产原值为100万元,累计折旧80万元,净值为20万元。

若该公司2020年新增固定资产20万元,折旧5万元,求其2020年12月31日的固定资产净值为多少。

17. 某企业年初资产总额为200万元,年末资产总额为250万元,净利润为40万元,利润分配为10万元,求该企业的所有者权益变化额。

18. 某公司2020年收入为150万元,成本为80万元,期初存货为10万元,期末存货为15万元,求该公司的毛利润和存货周转率。

中级会计证考试题库及答案

中级会计证考试题库及答案一、单选题1. 会计的基本职能是()。

A. 记录和报告B. 监督和评价C. 计划和决策D. 控制和协调答案:A2. 会计信息的质量要求中,要求企业应当保证会计信息的()。

A. 及时性B. 准确性C. 完整性D. 可靠性答案:D3. 资产负债表中,资产的排列顺序是()。

A. 按流动性排列B. 按重要性排列C. 按价值大小排列D. 按取得时间排列答案:A二、多选题4. 以下哪些属于会计要素?()A. 资产B. 负债C. 所有者权益D. 利润答案:A, B, C, D5. 会计政策变更的类型包括()。

A. 会计估计变更B. 会计政策变更C. 会计估计错误更正D. 会计政策错误更正答案:B, C三、判断题6. 会计分期假设是企业会计核算的基础之一。

()答案:正确7. 会计信息的使用者只需要了解企业的财务状况,不需要了解企业的经营成果。

()答案:错误四、简答题8. 简述会计信息的使用者通常包括哪些?答案:会计信息的使用者通常包括投资者、债权人、政府及其相关部门、企业管理者以及社会公众等。

五、计算题9. 某企业在2023年1月1日购买了一项固定资产,原值为100万元,预计使用年限为10年,采用直线法计提折旧。

请计算该固定资产在2023年的折旧额。

答案:该固定资产在2023年的折旧额为100万元 / 10年 = 10万元。

六、案例分析题10. 某公司2023年的净利润为500万元,但该公司在2023年末进行了一项重大的会计估计变更,导致净利润减少了100万元。

请分析这一变更对公司的影响。

答案:会计估计变更导致净利润减少,可能会影响投资者和债权人对公司未来盈利能力的判断,降低公司的市场信誉,同时也可能影响公司的股价和融资成本。

结束语:以上为中级会计证考试题库及答案的一部分,希望能够帮助考生更好地复习和准备考试。

会计是一门实践性很强的学科,考生在掌握理论知识的同时,也应注重实际操作能力的培养。

中级会计考试真题题库及答案

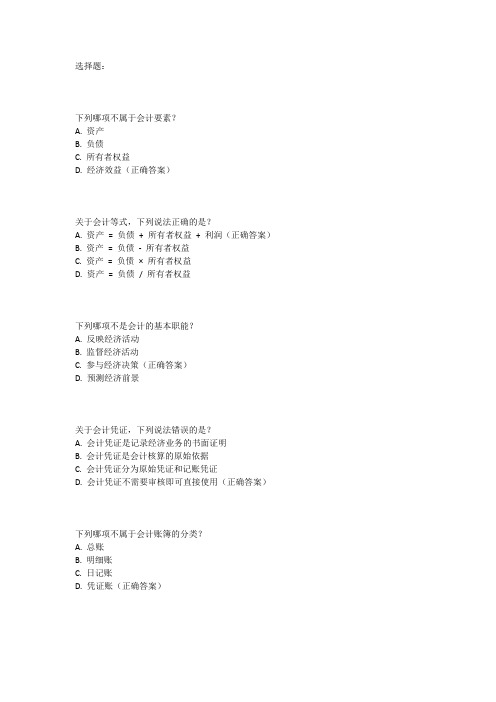

选择题:下列哪项不属于会计要素?A. 资产B. 负债C. 所有者权益D. 经济效益(正确答案)关于会计等式,下列说法正确的是?A. 资产= 负债+ 所有者权益+ 利润(正确答案)B. 资产= 负债-所有者权益C. 资产= 负债× 所有者权益D. 资产= 负债/ 所有者权益下列哪项不是会计的基本职能?A. 反映经济活动B. 监督经济活动C. 参与经济决策(正确答案)D. 预测经济前景关于会计凭证,下列说法错误的是?A. 会计凭证是记录经济业务的书面证明B. 会计凭证是会计核算的原始依据C. 会计凭证分为原始凭证和记账凭证D. 会计凭证不需要审核即可直接使用(正确答案)下列哪项不属于会计账簿的分类?A. 总账B. 明细账C. 日记账D. 凭证账(正确答案)关于会计报表,下列说法正确的是?A. 会计报表是反映企业一定时期财务状况的书面文件B. 会计报表只包括资产负债表和利润表C. 会计报表不需要经过审计即可对外公布D. 会计报表是根据会计账簿记录编制而成的(正确答案)下列哪项不是会计档案的内容?A. 会计凭证B. 会计账簿C. 会计报表D. 企业年度工作计划(正确答案)关于会计估计变更,下列说法错误的是?A. 会计估计变更是指由于资产和负债的当前状况及预期经济利益和义务发生了变化,从而对资产或负债的账面价值或资产的定期消耗金额进行调整B. 会计估计变更应当采用未来适用法C. 会计估计变更需要进行追溯调整(正确答案)D. 会计估计变更不会改变以前期间的会计估计下列哪项不属于会计职业道德的要求?A. 诚实守信B. 客观公正C. 保守商业秘密D. 追求个人利益最大化(正确答案)。

中级会计考试题库及答案大全

中级会计考试题库及答案大全中级会计考试是会计专业人员的重要考试之一,对于考生来说,备考资源是非常重要的。

本文将为大家提供中级会计考试题库及答案大全,帮助考生进行高效备考。

一、财务会计与审计类1. 托尔财务会计报告编制模板是由哪两个国际组织联合编制的?答案:国际会计准则理事会(IASB)、国际金融报告准则基金会(IFRS Foundation)2. 中级合伙企业的出资人之间如何确定出资比例?答案:按照各出资人的出资额总额占全部出资额总额的比例确定。

3. 企业合并中固定资产的核算处理方法是?答案:采用获取成本法核算。

二、管理会计与财务管理类1. 制造费用的核算方法有哪些?答案:作业成本法、直接成本法、统一成本法。

2. 在投资决策中,如何计算投资回收期?答案:投资回收期=投资金额/年净现金流入额3. 企业资本结构的组成有哪些?答案:内源性资本和外源性资本。

三、经济法与税法类1. 个人所得税的起征点是多少?答案:3500元。

2. 什么是反垄断法?答案:反垄断法是指国家为了维护市场竞争秩序,保护消费者权益而制定的法律法规。

3. 什么是增值税?答案:增值税是按照货物和劳务的增值额为征税对象,对企业销售货物和提供劳务的增值额按比例加征的一种间接税。

四、财务成本管理类1. 什么是财务成本管理?答案:财务成本管理是指企业在生产经营过程中,合理配置和使用资金,控制经营成本,最大限度地提高资金使用效益的管理活动。

2. 成本控制的目标是什么?答案:降低企业经营成本,提高企业经济效益。

3. 盈亏平衡点分析的目的是什么?答案:在利润不为负也不为正的情况下,找出使收益最大的产量并确定企业经营方向。

通过以上例题,希望能给大家提供一定的参考和帮助。

考生可以通过解析答案,了解题目类型和解题思路,加深对中级会计考试知识点的理解。

同时,在备考过程中,可以寻找相关资料进行更深入的学习和理解,提高备考的针对性和有效性。

总结起来,备考中级会计考试,除了掌握知识点外,备考资源也非常关键。

中级会计职称考试题库

一、选择题1.下列哪项不属于会计要素?A.资产B.负债C.所有者权益D.财务报表(答案)2.关于会计估计变更,下列说法正确的是?A.会计估计变更应采用未来准据法进行处理。

B.会计估计变更应调整以前期间的会计数据和财务报表。

(答案)C.会计估计变更不需要在财务报表中披露。

D.会计估计变更通常需要得到税务机关的批准。

3.下列哪项不是会计政策变更的处理方法?A.追溯调整法B.未来准据法C.初始应用法(答案)D.重新计算法4.关于会计档案的管理,下列说法错误的是?A.会计档案应定期归档并妥善保管。

B.会计档案的保管期限一般分为永久和定期两类。

C.所有会计档案均不得对外借阅或复制。

(答案)D.销毁会计档案时,应由单位档案机构和会计机构共同派员监销。

5.下列哪项不属于财务报表的组成部分?A.资产负债表B.利润表C.现金流量表D.会计账簿(答案)6.关于会计差错更正,下列说法正确的是?A.所有会计差错均应采用追溯重述法进行更正。

B.本期发现的以前年度非重大会计差错,应调整发现当期的期初留存收益。

C.本期发现的以前年度重大会计差错,应调整以前各期的相关项目。

(答案)D.会计差错更正不需要在财务报表附注中披露。

7.下列哪项不是会计循环的基本步骤?A.编制会计分录B.编制试算平衡表C.编制财务报表D.编制业务计划书(答案)8.关于会计估计,下列说法错误的是?A.会计估计是以最近可利用的信息或资料为基础的。

B.会计估计不会削弱会计核算的可靠性。

C.会计估计变更应按会计政策变更的处理方法进行处理。

(答案)D.会计估计通常涉及对结果不确定的交易或事项的判断。

中级财务会计1期末考试题

中级财务会计1期末考试题总分:98分1、某基层工会组织红五月演唱会,发生会场布置杂费500元。

根据《工会会计制度》规定,进行会计处理时,正确的借方一级科目是()。

[单选题] *A 业务支出B 职工活动支出(正确答案)C 职工服务支出D 行政支出答案解析:B 借记职工活动支出——文体活动支出。

2、某基层工会组织普法教育活动,以银行存款转账支付奖励优秀学员款5000元。

根据《工会会计制度》规定,进行会计处理时,正确的借方一级科目是()。

[单选题] *A业务支出B 职工活动支出(正确答案)C 职工服务支出D 行政支出答案解析:B 借记职工活动支出——教育活动支出。

3、某基层工会以银行存款转账支付职工素质提升补助40000元,根据《工会会计制度》规定,进行会计处理时,借方一级科目正确的是()。

[单选题] *A业务支出B 职工活动支出(正确答案)C 职工服务支出D 行政支出答案解析:B 借记职工活动支出——教育活动支出。

4、某基层工会为一生病住院慰问5000元,以银行存款转账支付,根据《工会会计制度》规定,进行会计处理时,借方一二级科目正确的是()。

[单选题] *A 维权支出——困难职工帮扶支出B 维权支出——送温暖支出C 职工活动支出——其他活动支出(正确答案)D 职工活动支出——会员活动支出答案解析:C 会员活动支出科目,核算基层工会用于组织会员观看电影、文艺演出、开展春5、某海员工会组织亲子游园活动,以银行存款转账支付相关费用3000元。

根据《工会会计制度》规定,进行会计处理时借方一二级科目正确的是()。

[单选题] *A 职工活动支出——文体活动支出(正确答案)B 职工活动支出——其他活动支出C 职工服务支出——会员活动支出D 维权支出——送温暖支出答案解析:A 核算基层工会用于开展或参加上级工会组织的职工业余文体活动所需器材、服装、用品等购置、租赁与维修方面的支出以及活动场地、交通工具的租金支出等,用于文体活动优胜者的奖励支出,用于文体活动中必要的伙食补助费。

中级会计师试题题库

1.下列关于资产减值准备的说法,正确的是:A.固定资产减值准备一经计提,在持有期间内不得转回。

B.存货跌价准备应在每年末至少进行一次减值测试。

C.长期股权投资采用权益法核算时,被投资单位发生减值不需要投资方计提减值准备。

D.无形资产减值准备在出现减值迹象时才进行计提。

2.企业将一项金融资产划分为以公允价值计量且其变动计入其他综合收益的金融资产时,其重分类表述正确的是:A.可以无条件重分类为以摊余成本计量的金融资产。

B.只有在满足特定条件时,可以重分类为以公允价值计量且其变动计入当期损益的金融资产。

C.重分类后的计量基础为转换日的公允价值。

D.重分类后的金融资产仍需在财务报表中单独列示。

3.下列哪项支出不应计入产品成本?A.直接材料费用B.直接人工费用C.废品损失D.企业管理人员工资4.关于现金折扣,以下哪项表述是正确的?A.现金折扣是一种融资方式,用于吸引客户提前付款。

B.现金折扣在发生时直接计入营业外收入。

C.现金折扣不影响应收账款的入账价值。

D.现金折扣金额的计算基数包括增值税税额。

5.编制现金流量表时,购买固定资产支付的现金应计入:A.经营活动产生的现金流量B.投资活动产生的现金流量C.筹资活动产生的现金流量D.不影响任何活动现金流量分类6.下列哪种情况不会导致长期股权投资的账面价值发生变化?A.被投资单位实现净利润B.被投资单位宣告发放现金股利C.投资方增加对被投资单位的投资D.投资方与被投资单位之间的内部交易未实现损益7.资产负债表日后调整事项是指:A.资产负债表日后至财务报告批准报出日之间发生的非调整事项B.资产负债表日已经存在,但在资产负债表日后才得以证实的事项C.资产负债表日后发生的对财务状况没有重大影响的事项D.资产负债表日后新发生的事项8.存货发出计价方法中,成本结转与实物流转完全一致的是:A.先进先出法B.加权平均法C.个别计价法D.移动加权平均法9.下列哪项不属于利润表的项目?A.营业收入B.营业成本C.盈余公积D.所得税费用10.下列关于政府补助的说法,正确的是:A.政府补助都是与资产相关的。

1.国开会计学专科《中级财务会计(一)》单项选择题库

国开会计学专科《中级财务会计(一)》单项选择题库按声母排列12月31日,A材料成本340万元,市场购买价格为280万元,预计销售发生的相关税费为10万元;用A材料生产的产成品的可变现净值高于材料成本。

据此,本年末A材料的账面价值应为(A)。

A.340万元1月3日购人M公司30%的普通股计划长期持有。

当年M公司实现税后利润180000元,宣告分派现金股利100000元。

采用权益法核算,不考虑其他影响因素,本项投资当年应确认投资收益(C)。

C.54000元2006年12月30日购人一台不需安装的设备并交付使用。

设备原价50 000元,预计使用5年,预计净残值2 000元。

若按年数总和法计提折旧,则2009年应计提折旧额\\B.9 600元2008年12月31日A商品的账面余值25 000元,预计可变现净值23 000元。

2009年12月31日该商品的账面余值没变,预计其可变现净值为26 000元。

则2009年末对A商品应做的会计处理是\\A.冲减跌价准备2 000元2009年7月1日A公司以每张900元的价格购人B公司2009年1月1日发行的面值1 000元、票面利率2%,3年期、到期一次还本付息的债券50张,计划持有至到期。

该项债券投资发生的折价金额应为\\B.5 500元2009年初购入设备一台自用,实际支付买价5 000元,支付安装费1 000元、增值税进项税850元。

则该设备的人账原值应为\\B.6 000元2010年12月31日,D存货库存成本35万元,预计售价(不含增值税)50万元、估计销售费用6万元。

之前该项存货未计提跌价准备,不考虑其他因素。

则2010年12月31日,D存货应计提跌价准备\\D.02010年4月2日购人M公司20%的普通股计划长期持有。

当年M公司实现税后利润180 000元,宣告分派现金股利100 000元。

如果采用成本法核算,本项投资当年应确认投资收益\\D.20 000元2010年初,企业购入同期发行的3年期分期付息债券一批计划持有至到期。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计考试2An adjusted trial balancea. is prepared after the financial statements are completed.b. proves the equality of the total debit balances and total credit balances of ledger accounts after all adjustments have been made.c. is a required financial statement under generally accepted accounting principles.d. cannot be used to prepare financial statements.Adjusting entries are necessary to1obtain a proper matching of revenue and expense.2achieve an accurate statement of assets and equities.3adjust assets and liabilities to their fair market value.a. 1b. 2c. 3d. 1 and 2A revenue collected, but not earned.a. Prepaid expenseb. Unearned revenuec. Accrued expensed. Accrued revenueaccrued expense can best be described as an amounta. paid and currently matched with earnings.b. paid and not currently matched with earnings.c. not paid and not currently matched with earnings.d. not paid and currently matched with earnings.The double-entry accounting system meansa. Each transaction is recorded with two journal entries.b. Each item is recorded in a journal entry, then in a general ledger account.c. The dual effect of each transaction is recorded with a debit and a credit.d. More than one of the above.which of the following is a recordable event or itema. Changes in managerial policyb. The value of human resourcesc. Changes in personneld. None of theseA journal entry to record a receipt of rent revenue in advance will include aa. debit to rent revenue.b. credit to rent revenue.c. credit to cash.d. credit to unearned rent.An expense incurred, but not paid.a. Prepaid expenseb. Unearned revenuec. Accrued expensed. Accrued revenueFactors that shape an accounting information system include thea. nature of the business.b. size of the firm.c. volume of data to be handled.d. all of these.The debit and credit analysis of a transaction normally takes placea. before an entry is recorded in a journal.b. when the entry is posted to the ledger.c. when the trial balance is prepared.d. at some other point in the accounting cycleA material item which is unusual in nature or infrequent in occurrence, but not both should be shown in the income statementDisclosedNet of TaxSeparately1.NoNo2.YesYes3.NoYes4.YesNoa. 1b. 2c. 3d. 4Comprehensive income includes all of the following excepta. dividend revenue.b. losses on disposal of assets.c. investments by owners.d. unrealized holding gains.Discontinuance of all production in the United States. The manufacturing operations were relocated in Mexico. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentThe primary advantage of the multiple-step format lies in the simplicity of presentation and the absence of any implication that one type of revenue or expense item has priority over another.FCompanies report the results of operations of a component of a business that will be disposed of separately from continuing operations.TWhich of the following is never classified as an extraordinary itema. Losses from a major casualty.b. Losses from an expropriation of assets.c. Gain on a sale of the only security investment a company has ever owned.d. Losses from exchange or translation of foreign currencies.Earnings management generally makes income statement information more useful for predicting future earnings and cash flows.FThe accountant for the Orion Sales Company is preparing the income statement for 2007 and the balance sheet at December 31, 2007. The January 1, 2007 merchandiseinventory balance will appeara. only as an asset on the balance sheet.b. only in the cost of goods sold section of the income statement.c. as a deduction in the cost of goods sold section of the income statement and as a current asset on the balance sheet.d. as an addition in the cost of goods sold section of the income statement and as a current asset on the balance sheet.Which of the following is not a selling expensea. Advertising expenseb. Office salaries expensec. Freight-outd. Store supplies consumedWhen a company discontinues an operation and disposes of the discontinued operation (component), the transaction should be included in the income statement as a gain or loss on disposal reported asa. a prior period adjustment.b. an extraordinary item.c. an amount after continuing operations and before extraordinary items.d. a bulk sale of plant assets included in income from continuing operations.The trial balance for the Starship Enterprise Inc. is presented below: Enterprise, Inc.Trial BalanceDec. 31, 2011Cash22,000Prepaid Insurance6,000Supplies12,000Equipment120,000Accounts Payable10,000Notes Payable80,000Retained Earnings57,000Dividends15,000Rent Revenue60,000Salaries Expense 15,000Insurance Expense 9,000Other Expense8,000207,000207,000Assuming that no year end adjustments are necessary, the net income for the year ended December 31, 2011 would be:a. $60,000b. $28,000c. $13,000d. $70,000Sloppy Seconds Corporation received cash of $60,750 on September 1, 2010 for one year’s rent in advance and recorded the transaction with a credit to Rent Revenue. The December 31, 2010 adjusting entry isa. debit Rent Revenue and credit Unearned Rent, $20,250.b. debit Rent Revenue and credit Unearned Rent, $40,500.c. debit Unearned Rent and credit Rent Revenue, $20,250.d. debit Cash and credit Unearned Rent, $40,500.y Seconds Corporation received cash of $60,750 on Septem ber 1, 2010 for one year’s rent in advance and recorded the transaction with a credit to Unearned Rent. The December 31, 2010 adjusting entry isa. debit Rent Revenue and credit Unearned Rent, $20,250.b. debit Rent Revenue and credit Unearned Rent, $40,500.c. debit Unearned Rent and credit Rent Revenue, $20,250.d. debit Cash and credit Unearned Rent, $40,500.Snead, Inc. incurred the following infrequent losses during 2007:A $70,000 write-down of equipment leased to others.A $40,000 adjustment of accruals on long-term contracts.A $60,000 write-off of obsolete inventory.In its 2007 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinarya. $170,000.b. $130,000.c. $110,000.d. $100,000.Dan Nicholson Corporation has an extraordinary loss of $50,000, an unusual gain of $35,000, and a tax rate of 40%. At what amount should Dan Nicholson report each itema. Extraordinary loss of $(50,000) and Unusual gain of $35,000b. Extraordinary loss of $(50,000) and Unusual gain of $21,000c. Extraordinary loss of $(30,000) and Unusual gain of $35,000d. Extraordinary loss of $(30,000) and Unusual gain of $21,000At Hall Company, events and transactions during 2007 included the following. The tax rate for all items is 30%.1)Depreciation for 2005 was found to be understated by $30,000.2)A strike by the employees of a supplier resulted in a loss of $25,000.3)The inventory at December 31, 2005 was overstated by $40,000.4)A flood destroyed a building that had a book value of $500,000. Floods are very uncommon in that area.The effect of these events and transactions on 2007 net income net of tax would bea. $17,500.b. $367,500.c. $388,500.d. $416,500.A review of the December 31, 2007, financial statements of Baden Corporation revealed that under the caption "extraordinary losses," Baden reported a total of $515,000. Further analysis revealed that the $515,000 in losses was comprised of the following items:1)Baden recorded a loss of $150,000 incurred in the abandonment of equipment formerly used in the business.2)In an unusual and infrequent occurrence, a loss of $250,000 was sustained as a result of hurricane damage to a warehouse.3)During 2007, several factories were shut down during a major strike by employees, resulting in a loss of $85,000.4)Uncollectible accounts receivable of $30,000 were written off as uncollectible.Ignoring income taxes, what amount of loss should Baden report as extraordinary on its 2007 income statementa. $150,000.b. $250,000.c. $400,000.d. $515,000.Cole Company, with an applicable income tax rate of 30%, reported net income of $210,000. Included in income for the period was an extraordinary loss from flood damage of $30,000 before deducting the related tax effect. The company's income before income taxes and extraordinary items wasa. $240,000b. $300,000c. $330,000d. $231,000Nominal accounts are also calleda. temporary accounts.b. permanent accounts.c. real accounts.d. none of these.The ending retained earnings balance is reported on both the retained earnings statement and the balance sheet.TrueA general journala. chronologically lists transactions and other events, expressed in terms ofdebits and credits.b. contains one record for each of the asset, liability, stockholders’ equity, revenue, and expense accounts.c. lists all the increases and decreases in each account in one place.d. contains only adjusting entries.Unearned revenue on the books of one company is likely to bea. a prepaid expense on the books of the company that made the advance payment.b. an unearned revenue on the books of the company that made the advance payment.c. an accrued expense on the books of the company that made the advance payment.d. an accrued revenue on the books of the company that made the advance payment.An accrued revenue can best be described as an amounta. collected and currently matched with expenses.b. collected and not currently matched with expenses.c. not collected and currently matched with expenses.d. not collected and not currently matched with expensesThe book value of any depreciable asset is the difference between its cost and its salvage value.FalseA journal entry to record the sale of inventory on account will include aa. debit to inventory.b. debit to accounts receivable.c. debit to sales.d. credit to cost of goods sold.Debit always meansa. right side of an account.b. increase.c. decrease.d. none of these.A revenue collected, but not earned.a. Prepaid expenseb. Unearned revenuec. Accrued expensed. Accrued revenueA general journal chronologically lists transactions and other events, expressed in terms of debits and credits to accounts.TrueWhich of the following is a change in accounting principlea. A change in the estimated service life of machineryb. A change from FIFO to LIFOc. A change from straight-line to double-declining-balanced. A change from FIFO to LIFO and a change from straight-line to double-declining- balanceAn item that should be classified as an extraordinary item isa. write-off of goodwill.b. gains from transactions involving foreign currencies.c. losses from moving a plant to another city.d. gains from a company selling the only investment it has ever owned.In order to be classified as an extraordinary item in the income statement, an event or transaction should bea. unusual in nature, infrequent, and material in amount.b. unusual in nature and infrequent, but it need not be material.c. infrequent and material in amount, but it need not be unusual in nature.d. unusual in nature and material, but it need not be infrequent.Obsolete inventory was written off. This was the first loss of this type in the company's history. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentPrior period adjustments can either be added or subtracted in the Retained Earnings Statement.TrueThe company neglected to record its depreciation in the previous year. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentThe company sold one of its warehouses at a loss. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentAn uninsured casualty loss was incurred by the company. This was the first loss ofthis type in the company's 50-year history. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentLoss on the disposal of a component of the business. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentSloppy Seconds Corporation received cash of $60,750 on September 1, 2010 for one year’s rent in advance and recorded the transaction with a credit to Rent Revenue. The December 31, 2010 adjusting entry isa. debit Rent Revenue and credit Unearned Rent, $20,250.b. debit Rent Revenue and credit Unearned Rent, $40,500.c. debit Unearned Rent and credit Rent Revenue, $20,250.d. debit Cash and credit Unearned Rent, $40,500.Hooti and the Blowfish receive interest on a $30,000, 8%, 5-year note receivable each April 1. At December 31, 2010, Hooti’s adjusting entry should be:a. Debit Interest Receivable and Credit Interest Revenue for $1,800b. Debit Interest Revenue and Credit Interest Receivable for $1,800c. Debit Interest Receivable and Credit Interest Revenue for $2,400d. Debit Interest Revenue and Credit Interest Receivable for $2,400James Bond Company sublet a portion of its warehouse for five years at an annual rental of $24,000, beginning on September 1, 2010. The tenant, Goldfinger, paid one year's rent in advance, which Bond recorded as a credit to Unearned Rental Revenue. Bond reports on a calendar-year basis. The adjustment on December 31, 2010 for Bond should beentryUnearned Rent Revenue and Credit Rent Revenue for $8,000Rent Revenue and Credit Unearned Rent Revenue for $8,000Unearned Rent Revenue Credit Rent Revenue for $16,000Saturn Company’s weekly payroll, paid on Friday, totalled $20,000 on Friday, January 4th. Employees work a 5-day week. The year end adjustment on December 31, should bea. Debit Salary Expense and Credit Salaries Payable for $4,000b. Debit Salaries Payable and Credit Salary Expense for $4,000c. Debit Salary Expense and Credit Salaries Payable for $16,000d. Debit Salaries Expense and Credit Cash for $16,000California Dreaming Corporation paid cash of $27,000 on June 1, 2010 for one year’s rent in advance and recorded the transaction with a debit to Rent Expense. The December 31, 2010 adjusting entry isa. debit Prepaid Rent and credit Rent Expense, $11,250.b. debit Prepaid Rent and credit Rent Expense, $15,750.c. debit Rent Expense and credit Prepaid Rent, $15,750.d. debit Prepaid Rent and credit Cash, $11,250.Motown Records rents a warehouse for five years to store their gold record music collection at an annual rental of $24,000, beginning on September 1, 2010. They pay the owner, Michael Jordan, one year's rent in advance, which Motown recorded as a debit to Rent Expense. Motown reports on a calendar-year basis. The adjustment on December 31, 2010 for Motown should bea. No entryb. Debit Rent Expense and Credit Prepaid Rent for $8,000c. Debit Prepaid Rent and Credit Rent Expense for $8,000d. Debit Prepaid Rent and Credit Rent Expense for $16,000Abba Corporation loaned $30,000 to another corporation on December 1, 2010 and received a 3-month, 8% interest-bearing note with a face value of $30,000. What adjusting entry should Abba make on December 31, 2010a. Debit Interest Receivable and credit Interest Revenue, $600.b. Debit Cash and credit Interest Revenue, $200.c. Debit Interest Receivable and credit Interest Revenue, $200.d. Debit Cash and credit Interest Receivable, $600.Gross billings for merchandise sold by Otto Company to its customers last year amounted to $15,720,000; sales returns and allowances were $370,000, sales discounts were $175,000, and freight-out was $140,000. Net sales last year for Otto Company werea. $15,720,000.b. $15,350,000.c. $15,175,000.d. $15,035,000.Agler Corp. had the following infrequent transactions during 2007:A $150,000 gain from selling the only investment Agler has ever owned.A $210,000 gain on the sale of equipment.A $70,000 loss on the write-down of inventories.In its 2007 income statement, what amount should Agler report as total infrequent net gains that are not considered extraordinarya. $80,000.b. $140,000.c. $290,000.d. $360,000.A review of the December 31, 2007, financial statements of Baden Corporation revealed that under the caption "extraordinary losses," Baden reported a total of $515,000. Further analysis revealed that the $515,000 in losses was comprised of the following items:1) Baden recorded a loss of $150,000 incurred in the abandonment of equipment formerly used in the business.2) In an unusual and infrequent occurrence, a loss of $250,000 was sustained asa result of hurricane damage to a warehouse.3) During 2007, several factories were shut down during a major strike by employees, resulting in a loss of $85,000.4) Uncollectible accounts receivable of $30,000 were written off as uncollectible.Ignoring income taxes, what amount of loss should Baden report as extraordinary on its 2007 income statementa. $150,000.b. $250,000.c. $400,000.d. $515,000.If the inventory account at the end of the year is understated, the effect will be toa. overstate the gross profit on sales.b. understate the net purchases.c. overstate the cost of goods sold.d. overstate the goods available for sale.The debit and credit analysis of a transaction normally takes placea. before an entry is recorded in a journal.b. when the entry is posted to the ledger.c. when the trial balance is prepared.d. at some other point in the accounting cycle.A general journala. chronologically lists transactions and other events, expressed in terms of debits and credits.b. contains one record for each of the asset, liability, stockholders’ equity, revenue, and expense accounts.c. lists all the increases and decreases in each account in one place.d. contains only adjusting entries.A trial balancea. proves that debits and credits are equal in the ledger.b. supplies a listing of open accounts and their balances that are used in preparing financial statements.c. is normally prepared three times in the accounting cycle.d. all of these.An expense incurred, but not paid.a. Prepaid expenseb. Unearned revenuec. Accrued expensed. Accrued revenueThe ending retained earnings balance is reported on both the retained earnings statement and the balance sheet.TrueWhy are certain costs of doing business capitalized when incurred and then depreciated or amortized over subsequent accounting cyclesa. To reduce the federal income tax liabilityb. To aid management in cash-flow analysisc. To match the costs of production with revenues as earnedd. To adhere to the accounting constraint of conservatismWhen an item of revenue is collected and recorded in advance, it is normally called a(n) ___________ revenue.a. accruedb. prepaidc. unearnedd. cashStockholders’ equity is not affected by alla. cash receipts.b. dividends.c. revenues.d. expenses.At the time a company prepays a costa. it debits an asset account to show the service or benefit it will receive in the future.b. it debits an expense account to match the expense against revenues earned.c. its credits a liability account to show the obligation to pay for the service in the future.d. more than one of the above.A strength of the income statement as compared to the balance sheet is that items that cannot be measured reliably can be reported in the income statement.Gains or losses from exchange or translation of foreign currencies are reported as extraordinary items.FalseThe occurrence which most likely would have no effect on 2007 net income (assuming that all amounts involved are material) is thea. sale in 2007 of an office building contributed by a stockholder in 1983.b. collection in 2007 of a receivable from a customer whose account was written off in 2006 by a charge to the allowance account.c. settlement based on litigation in 2007 of previously unrecognized damages from a serious accident which occurred in 2005.d. worthlessness determined in 2007 of stock purchased on a speculative basis in 2003.The components of other comprehensive income can be reported in a statement of stockholders’ equity.TrueIntraperiod tax allocation relates the income tax expense of the period to the specific items that give rise to the amount of the tax provision.The company neglected to record its depreciation in the previous year. Indicate how this should be treated in the financial statements.a. Ordinary or unusual (but not extraordinary) item on the income statementb. Discontinued operationsc. Extraordinary item on the income statementd. Prior period adjustmentSargeant Pepper’s Company's account balances at Decemb er 31, 2010 for Accounts Receivable and the related Allowance for Doubtful Accounts are $460,000 debit and $700 credit, respectively. From an aging of accounts receivable, it is estimated that $13,900 of the December 31 receivables will be uncollectible. The necessary adjusting entry would include a credit to the allowance account fora. $12,500.b. $13,200.c. $11,800.d. $700.Motown Records rents a warehouse for five years to store their gold record musiccollection at an annual rental of $24,000, beginning on September 1, 2010. They pay the owner, Michael Jordan, one year's rent in advance, which Motown recorded as a debit to Rent Expense. Motown reports on a calendar-year basis. The adjustment on December 31, 2010 for Motown should bea. No entryb. Debit Rent Expense and Credit Prepaid Rent for $8,000c. Debit Prepaid Rent and Credit Rent Expense for $8,000d. Debit Prepaid Rent and Credit Rent Expense for $16,000Jumping Jack Flash Company recorded journal entries for the issuance of common stock for $25,000, the payment of $10,000 on accounts payable, and the payment of salaries expense of $4,000. What net effect do these entries have on owners’ equitya. Increase of $25,000.b. Increase of $15,000.c. Increase of $21,000.d. Increase of $11,000.During the first year of James Taylor Co.'s operations, all purchases were recorded as assets. Store supplies in the amount of $19,350 were purchased. Actual year-end store supplies amounted to $6,450. The adjusting entry for store supplies willa. decrease net income by $12,900.b. decrease expenses by $12,900.c. decrease store supplies by $6,450.d. debit Accounts Payable for $6,450Fleming Company has the following items: write-down of inventories, $240,000; loss on disposal of Sports Division, $370,000; and loss due to an expropriation, $226,000. Ignoring income taxed, what total amount should Fleming Company report as extraordinary lossesa. $226,000b. $370,000c. $446,000d. $596,000Sam Hurd Company has the following items: write-down of inventories, $120,000; loss on disposal of Sports Division, $185,000; and loss due to strike, $113,000. Ignoring income taxes, what total amount should Sam Hurd Company report as extraordinary lossesa. $ -0-.b. $185,000.c. $233,000.d. $298,000If plant assets of a manufacturing company are sold at a gain of $820,000 less related taxes of $250,000, and the gain is not considered unusual or infrequent, the income statement for the period would disclose these effects asa. a gain of $820,000 and an increase in income tax expense of $250,000.b. operating income net of applicable taxes, $570,000.c. a prior period adjustment net of applicable taxes, $570,000.d. an extraordinary item net of applicable taxes, $570,000.If plant assets of a manufacturing company are sold at a gain of $820,000 less related taxes of $250,000, and the gain is not considered unusual or infrequent, the income statement for the period would disclose these effects asa. a gain of $820,000 and an increase in income tax expense of $250,000.b. operating income net of applicable taxes, $570,000.c. a prior period adjustment net of applicable taxes, $570,000.d. an extraordinary item net of applicable taxes, $570,000.Snead, Inc. incurred the following infrequent losses during 2007:A $70,000 write-down of equipment leased to others.A $40,000 adjustment of accruals on long-term contracts.A $60,000 write-off of obsolete inventory.In its 2007 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinarya. $170,000.b. $130,000.c. $110,000.d. $100,000.1. (Points:The financial statements most frequently provided include all of the following except thea. balance sheet.b. income statement.c. statement of cash flows.d. statement of retained earnings.吴晓波 10:14:04 PMThe Governmental Accounting Standards Boarda. oversees the activities of the SEC.b. is a private-sector body, which addresses state and local governmental reporting issues.c. is a division of the Securities and Exchange Commission, which oversees the corpo-rate accounting in annual reports.d. was terminated when the Financial Accounting Standards Board was created.奇奇 10:14:07 PMD奇奇 10:16:56 PMc周律君 10:16:56 PMc吴晓波 10:16:59 PMWhich of the following statements is not an objective of financial reportinga. Provide information that is useful in investment and credit decisions.b. Provide information about enterprise resources, claims to those resources, and changes to them.c. Provide information on the liquidation value of an enterprise.d. Provide information that is useful in assessing cash flow prospects.奇奇 10:17:41 PMc陈庚岸 10:17:39 PMc吴晓波 10:17:40 PM4. (Points:An effective capital allocation processa. promotes productivity.b. encourages innovation.c. provides an efficient market for buying and selling securities.d. all of these.奇奇 10:18:01 PMd吴晓波 10:18:00 PM。